united insurance company limited€¦ · head office & registered ... he was in unilever as the...

TRANSCRIPT

UNITEDINSURANCECOMPANY LIMITED

Twenty Eighth Annual Report & Accounts : 2012

Our VisionOur Vision

Our MissionOur Mission

To be the leading provider of the highest

quality of insurance service.

To operate in accordance with the law of the

land and as per international norms and

practices.

To provide promptly the best possible

services ensuring security of our clients.

To extend a professional hand to our clients

at all times.

To serve the interests of the shareholders.

INDEX

CONTENTS PAGE

Facts about the Company 3

Board of Directors 4

Head Office & Registered Office and Share Department 4

Brief Resume of the Directors 5-6

Executive Committee and Audit Committee 7

Executives, Legal Advisors, Auditors and Bankers 7

Branch offices 8

Key Operating and Financial Data 9

Chairman's Report 10-12

Report of the Board of Directors 13-21

Audit Committee Report 28

Value Added Statement 29

Auditors' Report 30-31

Balance Sheet 32-33

Profit and Loss Account 34-35

Consolidated Revenue Account 36-37

Fire Insurance Revenue Account 38-39

Marine Insurance Revenue Account 40-41

Motor Insurance Revenue Account 42-43

Miscellaneous Revenue Account 44-45

Statement of Changes in Shareholders' Equity 46

Cash Flow Statement 47

Notes to the Accounts 48-57

Classified Summary of Assets 58

UNITED INSURANCE COMPANY LIMITED

02

FACTS ABOUT THE COMPANY

PARTICULARS DATE

Incorporated 7 May 1985

Commenced underwriting 19 October 1985

First Dividend declared (12%) at 3rd AGM 30 June 1998

Listing in Dhaka Stock Exchange Limited 9 April 1990

Paid-up capital raised to Tk 60 million after public floatation of shares 20 May 1990

First trading of shares on Dhaka Stock Exchange Limited 28 October 1990

First Public AGM held at Sonargaon Hotel 27 May 1991

Paid-up capital raised to Tk 78 million (30%stock dividend) 20 May 1990

Electronic transaction of shares 22 May 2007

Credit rating "A" by CRISL in 2007 on 2006 Accounts 24 September 2007

Overseas Reinsurance Treaty commenced 1 April 2008

Paid-up capital raised to Tk 100 million (28.21% stock dividend) 8 May 2008

Paid-up capital raised to Tk 250 million (150% stock dividend) 7 May 2009

Paid-up capital raised to Tk 300 million (20% stock dividend) 22 April 2010

Paid-up capital raised to Tk 330 million (10% stock dividend) 2 June 2011

Credit rating "AA-" by CRISL in 2012 on 2010 Accounts 7 February 2012

Paid-up capital raised to Tk 363 million (10% stock dividend) 7 May 2012

Paid-up capital to be raised to Tk 400 million (10.19% stock dividend) 9 May 2013

UNITED INSURANCE COMPANY LIMITED

03

CORPORATE MANAGEMENT

BOARD OF DIRECTORS

CHAIRMAN

M. Moyeedul Islam

DIRECTORS

M. Saiful Islam National Brokers Ltd.

M. Shah Alam Amo Tea Company Ltd.

M. A. Azim The Allynugger Tea Company Ltd.

DIRECTORS FROM PUBLIC SUBSCRIBERS

Syed Aziz Ahmad Camellia Duncan Foundation.

M. Harunur Rashid Camellia Duncan Foundation.

INDEPENDENT DIRECTOR

M. M. Alam

M. Hafizullah

MANAGING DIRECTOR

Syed Shahriyar Ahsan

COMPANY SECRETARY

Badal Chandra Rajbangshi ACA, ACS

UNITED INSURANCE COMPANY LIMITED

04

M. Saiful IslamA Director from Chittagong Region

NOMINATED BY

United Leasing Co. Ltd.

HEAD OFFICE & REGISTERED OFFICE

CAMELLIA HOUSE22, Kazi Nazrul Islam Avenue,

Dhaka-1000, Bangladesh

Tel: PABX: 8619336-8, 8621716Fax: 880-2-8622330

E-mail: [email protected]:unitedinsurance.com.bd

SHARE DEPARTMENT

AHN TOWER (Level # 3)13,15, Biponon C/A, Sonargaon Road,

Banglamotor, Dhaka-1000

Tel: PABX: 9611612, 9611615Fax: 880-2-9611594

E-mail: [email protected]:unitedinsurance.com.bd

UNITED INSURANCE COMPANY LIMITED

05

BRIEF RESUME OF THE DIRECTORS

Mr. M. Moyeedul Islam

Mr. M. Moyeedul Islam has been the Chairman of United Insurance Company Limited since its establishment in

1985. A former Managing Director of Pakistan Insurance Corporation and a Vice President of Federation of

Afro-Asian Insurers and Re-insurers (FAIR), Mr. Islam was Chairman of Bangladesh Public Service Commission

from 1977 to 1982. He was Chairman of Uttara Bank, Chairman of Bangladesh Times Trust, Chairman of Copy

Rights Board, a Director of United Leasing Company Limited and Chairman of Insurance Association of

Bangladesh from 1988 to 1998. He has been Vice President of the Diabetic Association of Bangladesh (DAB)

since 1995.

Mr. M. Saiful Islam

A graduate from Chittagong University with distinctions, Mr. M. Saiful Islam, was associated with Brooke Bond

Pakistan Ltd. He was in Unilever as the Head of Tea, Foods and Exports. He joined the Board of Directors of

National Brokers Ltd in 1991. He has been the Managing Director of National Brokers Ltd, a leading

Chittagong-based tea broking company since 2010. He was the Chairman of Tea Traders Association, a

Member of Bangladesh Tea Board, President and Assistant Governor of Rotary Club and President of Old

Faujians Association.

Mr. M. Shah Alam

An Honours graduate in Political Science Mr. M. Shah Alam is an M.A in Public Administration with a degree in

Management from the United Kingdom. He is involved in tea plantation and represents M/s. Amo Tea

Company Ltd on the Board of Directors of United Insurance Company Limited. He is the Vice Chairman of

Bangladesh Tea Association and a Committee Member of Bangladesh Employers' Federation. He is a widely

travelled person.

Mr. M. A. Azim

A B.A (Hons) in Economics from Dhaka University and an M.A in Economics from Karachi, Mr. M. A. Azim has

been the Deputy Managing Director of United Leasing Company Ltd since 2005. He was a Director of United

Leasing Company Ltd from 2006 to 2012. He was a Manager Administration and Finance with Northwest

Hydraulic Consultants Ltd, a Canadian Firm working in Dhaka from 1982 to 1985 and was involved in tea

plantation from 1969 to 1982. He has wide contacts among entrepreneurs and industrialists operating in

various fields.

Mr. Syed Aziz Ahmad

A Bachelor of Science from F.C. College, Lahore, Mr. Syed Aziz Ahmad has a vast experience in management

and administration of tea estates. A former Director of United Leasing Company Limited, he was the Managing

Director of United Insurance Company Limited from 2001 to 2005 and also worked later as Director Corporate

Affairs of the Company. He is also a Director of Duncan Brothers (Bangladesh) Ltd, Octavius Steel & Co. of

Bangladesh Ltd, Eastland Camellia Ltd and Duncan Products Ltd.

UNITED INSURANCE COMPANY LIMITED

06

Mr. M. Harunur Rashid

Mr. M. Harunur Rashid, an ACII (gold medalist), is a Director of the Company from amongst the public

subscribers representing the Camellia Duncan Foundation. He was the Chief Executive Officer of United

Insurance Company Limited for several years since its inception in 1985. He was the Chief Executive of Pakistan

Insurance Corporation at Dhaka. He was also former Controller of Insurance, Government of Bangladesh. Mr.

Rashid has more than 50 years of experience in insurance sector.

Mr. M. M. Alam

A member of the Canadian Institute of Chartered Accountants, an M.A in Economics from Dhaka University

and an MBA from American University of Beirut Mr. M. M. Alam is an Independent Director and the Chairman

of the Audit Committee of the Company. He was Managing Director of United Leasing Company Ltd from

1995 to 2005 and a Director of the said Company from 2000 to 2011. He carries with him about 50 years of

experience in marketing, banking and financial services.

Mr. M. Hafizullah

A senior advocate of the Supreme Court of Bangladesh, Mr. M. Hafizullah is the Head of Orr, Dignam &

Company, Advocates and Barristers, a leading law firm of the country. He was enrolled in the High Court in

1966 upon passing the Chambership examination securing first position. Mr. Hafizullah was elected as the

Secretary of the Bangladesh Supreme Court Bar Association for 1978-79. He was nominated by the Chief

Justice of the Supreme Court of Bangladesh to attend the Academy of American & International Law in 1982

conducted by International & Comparative Law Centre in Dallas, USA. He was elected as the President of the

Bangladesh Supreme Court Bar Association for 1994-95. He is an Independent Director of the Company and

also a member of the Audit Committee of the Company.

Mr. Syed Shahriyar Ahsan

An M. Com in Finance from Dhaka University and an MBA, Mr. Ahsan has been the Managing Director and

Chief Executive Officer of the Company since 2007. Mr. Ahsan possesses more than 25 years of experience in

insurance and he worked in a couple of reputed insurance companies in various important positions. He was a

member of the Central Rating Committee (CRC) and was also a member of the Re-insurance Sub-Committee

and Technical Sub-Committee of Bangladesh Insurance Association (BIA). Mr. Ahsan has attended different

training courses and seminars on insurance and re-insurance both at home and abroad. He is at present a

member of the Executive Committee of Bangladesh Insurance Association and a member of several sub-

committees of Bangladesh Insurance Association.

EXECUTIVE COMMITTEE

M. Moyeedul Islam ChairmanSyed Aziz Ahmad MemberM. A. Azim MemberSyed Shahriyar Ahsan Member

AUDIT COMMITTEE

M. M. Alam FCA ChairmanM. Saiful Islam MemberM. Shah Alam MemberM. Hafizullah Member

EXECUTIVES, LEGAL ADVISORS, AUDITORS AND BANKERS

C.E.0 & MANAGING DIRECTORSyed Shahriyar Ahsan

HEAD OF MARKETINGGour Hari Saha

DEPUTY MANAGING DIRECTORRafiqul Islam

DEPUTY GENERAL MANAGERSBadal Chandra Rajbangshi ACA, ACSMaqsudul HuqueMd. JashimuddinFaiz Jalaluddin AhmadMd. Abdul KhaleqMohammed Ahsan Ullah Md. Nizamul Islam

ASSISTANT GENERAL MANAGERSRafiquddin Ahmed Khondaker Fakrul Alam

LEGAL ADVISORS AUDITORSORR, DIGNAM & CO, M. J. Abedin & Co.Advocates & Barristers Chartered AccountantsOffice No: 101-104 National Plaza (3rd Floor)Sajan Tower 2 (1st Floor) 109, Bir Uttam C. R. Datta Road,3, Segun Bagicha, Dhaka-1000 Dhaka-1205Bangladesh

BANKERSStandard Chartered BankThe Hongkong & Shanghai Banking Corporation Ltd.

UNITED INSURANCE COMPANY LIMITED

07

BRANCH OFFICES

UNITED INSURANCE COMPANY LIMITED

08

Central Development Unit Dhaka Zonal Office

CAMELLIA HOUSE AHN TOWER22, Kazi Nazrul Islam Avenue, Level # 3Dhaka-1000, Bangladesh 13,15, Biponon C/A, Sonargaon Road,Tel: PABX: 8619336-8, 9664348 Banglamotor, Dhaka-1000Fax: 880-2-8622330 Tel: PABX: 9611612, 9611615E-mail: [email protected] Fax: 880-2-9611594www:unitedinsurance.com.bd E-mail: [email protected]

Narayanganj Chapai Nawabganj Sylhet

29, S. M. Maleh Road, Holding No: 8 (1st Floor) Madhuban Shopping ComplexTanbazar, Godgari Road, Masjid Para 7774, Bandar BazarNarayanganj Chapai Nawabganj SylhetTel: 01817-116609 Tel: 01712-000026 Tel: 712301, 01558-360767E-mail: [email protected] E-mail: [email protected] E-mail: [email protected]

Khulna Bogra Rangpur

Hui House 146, Raja Bazar Sabera Mansion77, Gagon Babu Road 2nd Floor 147/1, Station RoadKhulna Bogra RangpurTel: 730257, 01711-824433 Tel: 64962, 01716-347386 Tel: 64235, 01718-409643E-mail: [email protected] E-mail: [email protected] E-mail: [email protected]

Pabna Khatunganj Agrabad

Al-Noman Plaza 678, Jail Road Ispahani Building3rd Floor 2nd Floor, Sk. Mujib RoadTulapatti Khatunganj Agrabad C/APabna Chittagong-4000 Chittagong-4000Tel: 64345, 01712945460 Tel: 620760, 01711-821928 Tel: 716227,716136,714882E-mail: [email protected] E-mail: [email protected] 711143, 01711-821928 E-mail: [email protected]

UNITED INSURANCE COMPANY LIMITED

10

CHAIRMAN'S REPORT - 2012 †Pqvig¨v‡bi cÖwZ‡e`b - 2012

Chairman M. Moyeedul Islam

DEAR SHAREHOLDERS

It is with great pleasure that I welcome you to the 28th Annual General Meeting of United Insurance Company Ltd.

You are aware that the insurance industry has been going through many vicissitudes since the establishment of the Insurance Development & Regulatory Authority (IDRA). Having tried consistently to abide by the provisions of the Insurance Act & Rules, we appreciate the role of IDRA in taking action against rebating and other malpractices prevalent in the insurance industry. It appears that although some progress has been made in curbing this vicious practice, rebating has staged a comeback after a short period. We hope that in course of time, the Authority would be able to contain payment of commission beyond the maximum of 15% of the premium allowable under law, violation of tariff and other malpractices that have been eating into the vitals of the industry.

wcÖq †kqvi‡nvìvie„›`

Avwg AZ¨š— Avb‡›`i mv‡_ BDbvB‡UW BbwmI‡iÝ †Kv¤úvbxi 28Zg evwl©K mvaviY mfvq Avcbv‡`i mKj‡K ¯^vMZ Rvbvw”Q|

Avcbviv Aek¨B Rv‡bb †h exgv Dbœqb I wbqš¿Y KZ…©c¶ (AvBwWAviG) cÖwZwôZ nIqvi ci †_‡K exgv wkí bvbv cwieZ©‡bi ga¨ w`‡q G¸‡”Q| ‡h‡nZz Avcbv‡`i †Kv¤úvbx eiveiB bxwZMZfv‡e exgv AvBb I wewa me©`vB AbymiY K‡i P‡j‡Q ZvB exgv wk‡í we`¨gvb †eAvBwbfv‡e cÖ`Ë Kwgkb cÖ`vb Ges wewea AcK‡g©i wei“‡× AvBwWAviG-Gi f~wgKv Avgiv ¯^-cÖksm `„wó‡Z †`‡LwQ| Z‡e g‡b n‡”Q †h hw`I G A‰bwZK Kvh©µg cÖwZ‡iv‡a wKQz cÖv_wgK mvdj¨ cwijw¶Z n‡q‡Q Z‡e wKQzw`‡bi g‡a¨B †eAvBwb Kwgkb cÖ`v‡bi †iIqvR Avevi wd‡i G‡m‡Q| Avgiv Avkv Ki‡ev †h AvBbvbyMfv‡e cÖ‡`q wcÖwgqv‡gi Dc‡i kZKiv c‡bi fvM-Gi AwZwi³ Kwgkb cÖ`vb, wcÖwgqvg nv‡ii j•Nb Ges Ab¨vb¨ `yb©xwZ hv exgv wk‡íi AMÖMwZ‡K e¨vnZ K‡i Avm‡Q Giƒc Kvh©Kjvc‡K KZ©„c¶ AwP‡iB `~i Ki‡Z mg_© n‡e|

UNITED INSURANCE COMPANY LIMITED

11

Business in 2012

Although, United Insurance Company has been able to increase its business slowly but steadily over the year, I am sorry to tell you that in 2012 the gross premium written by the Company was well short of the company's premium income in 2011. The shortfall is due to various factors over some of which we had no control. For years the multinational companies have been an important source of our premium income. Unfortunately, however, recently the total business emanating from the multinationals has dropped significantly as the multinationals have now made it their policy to reduce drastically their expenditure on insurance by going global and placing their insurance business almost with their own reinsurer. Some premium has also been lost because of reduction in the rates of premium obtained by some large companies on the basis of their favourable claims ratio.

However, we have tried substantially to reduce our losses of premium through increased efforts in procuring business from the social sector and the small & medium enterprises. We are happy to tell you that SMEs have been an important source of our premium income. Incidentally, this is in conformity with the declared policy of the government that the insurance companies should devote their efforts to extend insurance protection to the social sector and SMEs.

It will be our policy to concentrate more on hitherto neglected sectors of business reducing our dependence on business emanating from the multinationals. At the same time we would request the Authority to ensure that the multinationals do not divert their insurance business substantially outside the country.

Notwithstanding the fall of premium income, we are happy to tell you that the financial position of the company is better than before. Our underwriting profit increased from Tk. 27.06 million in 2011 to Tk. 31.34 million in 2012. Our profit before tax also went up from Tk. 132.09 million in 2011 to Tk. 134.64 million in 2012. The incidence of tax in 2012 was, however, much higher than in the previous year because our taxable income was earned primarily from our insurance business on which we had to pay income tax at the rate of 42.5%. In previous year a much larger part of our income was derived from the stock market on which the tax rate was only 10%.

2012 mv‡ji exgv e¨emv

hw`I BDbvB‡UW BbwmI‡iÝ †Kv¤úvbx wjwg‡UW eû eQi a‡i µgvMZB Zvi e¨emv ax‡i ax‡i evwo‡q P‡j‡Q Avwg AwZ `yt‡Li mv‡_ Avcbv‡`i Rvbvw”Q †h 2012 m‡b Avcbv‡`i †Kv¤úvbxi ‡gvU wcÖwgqvg Avq c~e©eZ©x eQ‡ii AewjwLZ †gvU wcÖwgqvg Av‡qi †P‡q Kg n‡q‡Q| GB Kg nIqvi wcQ‡b †h KviY¸‡jv i‡q‡Q Zvi A‡bK ¸‡jvi Dc‡iB Avgv‡`i †Kvb wbqš¿Y wQj bv| eû eQi a‡iB eûRvwZK †Kv¤úvbx¸‡jv Avgv‡`i wcÖwgqvg Av‡qi GKwU ¸i“Z¡c~Y© Ask wQj| yf©vM¨ekZ, mv¤úªwZKKv‡j eûRvwZK †Kv¤úvbx¸‡jv Zv‡`i exgv e¨emvi wmsnfvM Zv‡`i wbR¯ cybtexgvKvix‡`i gva¨‡g we‡`‡k ’vbvš—wiZ K‡i‡Q| wKQz wKQz eo cÖwZôvb †_‡K Avgv‡`i wcÖwgqvg Avq K‡g‡Q KviY exgv`vexi AbyKzj Abycv‡Zi Kvi‡Y wcÖwgqv‡gi nvi D‡j-L‡hvM¨fv‡e K‡g‡Q hw`I exgvK…Z SuywKi cwigvY n«vm cvqwb|

hv‡nvK AwaKZi cÖ‡Póvi gva¨‡g mvgvwRK LvZ Ges ¶z`ª I gvSvwi D‡`¨v³v‡`i KvQ †_‡K exgv e¨emv e„w×i gva¨‡g Avgiv wcÖwgqv‡gi mvwe©K ¶wZ Kgvevi †Póv K‡iwQ| Avgiv Avb‡›`i mv‡_ Avcbv‡`i ej‡Z PvB †h ¶z`ª I gvSvwi D‡`¨v³vivB n‡jb GLb Avgv‡`i wcÖwgqvg Av‡qi GKwU ¸i“Z¡c~Y© Ask| NUbvµ‡g, Avgv‡`i GB cÖ‡Póv miKv‡ii †NvwlZ bxwZi mv‡_ msMwZ m¤úbœ KviY miKviI PvB‡Qb †h exgv †Kv¤úvbxmg~n mvgvwRK I GmGgB Lv‡Z AwaKZi exgvi wbivcËv wbwðZ Ki“K|

Ghver Kvj Avgiv eûRvwZK †Kv¤úvbxmg~‡ni e¨emvi Dci wbf©ikxj wQjvg| GLb Avgv‡`i bxwZ n‡e G wbf©ikxjZv Kwg‡q D‡cw¶Z LvZmg~‡ni w`‡K AwaKZi `„wó †`Iqv| GKB mv‡_ Avgiv exgv KZ…©c¶‡K Aby‡iva Rvbvw”Q †h eûRvwZK †Kv¤úvbxmg~n †hb Zv‡`i wmsnfvM exgv e¨emv †`‡ki evB‡i cvVv‡Z bv cv‡i Zv wbwðZ Kiv †nvK|

Avgiv Avb‡›`i mwnZ Avcbv‡`i Rvbvw”Q †h wcÖwgqvg Avq Kg nIqv m‡Ë¡I †Kv¤úvbxi Avw_©K Ae¯’v Av‡Mi Zzjbvq A‡bKUv fvj| Avgv‡`i 2012 mv‡ji AewjLb gybvdv e„w× †c‡q 31.34 wgwjqb UvKv n‡q‡Q hv 2011 mv‡j wQj 27.06 wgwjqb UvKv| Avgv‡`i Kic~e© gybvdvI 2011 mv‡ji 132.09 wgwjqb UvKv †_‡K e„w× †c‡q 2012 mv‡j 134.64 wgwjqb UvKvq DbœxZ n‡q‡Q| 2012 mv‡j Avgv‡`i †Kv¤úvbxi K‡ii cwigvY mvKz‡j¨ MZev‡ii Zzjbvq A‡bK †e‡o‡Q hvi cÖv_wgK KviY nÕj exgv e¨emvq †_‡K Avgv‡`i Ki‡hvM¨ Avq †ekx n‡q‡Q hvi Dci AvqKi cÖ`vb Ki‡Z n‡q‡Q 42.5% nv‡i| MZeQi Avgv‡`i Av‡qi GKUv wekvj Ask wQj †kqvievRvi †_‡K cÖvß Avq hvi Dci Ki w`‡Z n‡qwQj 10% nv‡i|

UNITED INSURANCE COMPANY LIMITED

12

It would, however, be in the interest of the company to derive their profit more from the insurance business and from investment in other sectors than investment in the stock market.

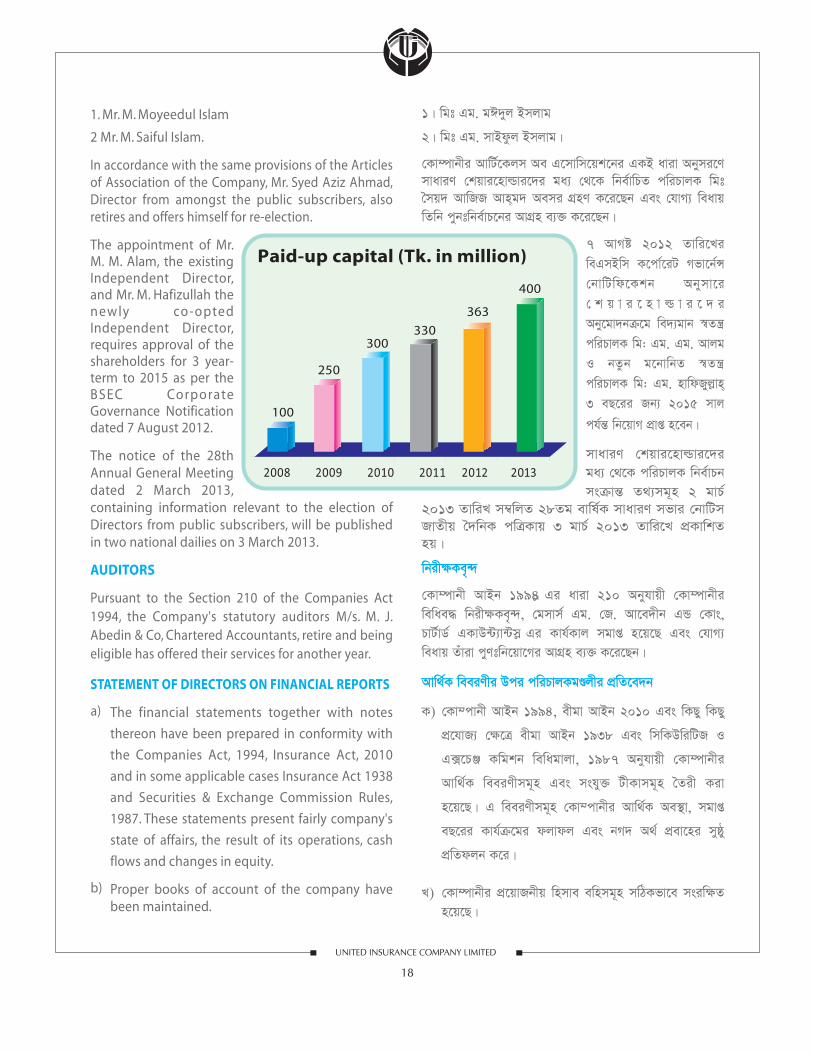

The Board of Directors has recommended a stock dividend of 10.19% raising the paid-up capital from Tk 363 million to Tk 400 million which is the minimum paid-up capital requirement for a non-life insurance company. As many as 13 non-life insurance companies have already raised their paid-up capital to Tk 400 million and above. We also have recommended a cash dividend of 7.5% by withdrawing Tk 12.25 million from the general reserves, leaving a balance of Tk 493.42 million of total reserves and surplus as against Tk 471.99 million in the previous year.

Prospects for 2013

We hope that the IDRA will be able to take effective measures to substantially reduce if not completely eliminate rebating, tariff violations and other malpractices prevalent in the insurance industry. Rules and Regulations are being gradually prepared and action has been taken against a few companies in some cases for gross violations of the provisions of the Insurance Act. We are also strengthening our marketing and other departments of the company to increase our gross premium income substantially and we hope to achieve a target of Tk. 360 million gross premium income in 2013.

(M. Moyeedul Islam)

Chairman

†Kv¤úvbxi ¯^v‡_©B Gi †ewkifvM gybvdv exgv e¨emv I Ab¨vb¨ Lv‡Zi wewb‡qvM †_‡K Avq Kiv evÃbxq Z‡e AwbwðZ †kqvievRvi †_‡K bq|

cwiPvjbv cl©` ‡Kv¤úvbxi cwi‡kvwaZ g~jab 363 wgwjqb UvKv †_‡K e„w× K‡i bb-jvBd BbwmI‡iÝ †Kv¤úvbxi Rb¨ wba©vwiZ by¨bZg cwi‡kvwaZ g~jab 400 wgwjqb UvKvq DbœxZ Kivi j‡¶¨ 10.19% †evbvm jf¨vs‡ki cÖ¯—ve K‡ib| cÖm½Zt 13 wUi g‡Zv bb-jvBd BbwmI‡iÝ †Kv¤úvbx BwZg‡a¨ Zv‡`i cwi‡kvwaZ g~jab 400 wgwjqb UvKv wKsev Zvi AwaK UvKvq DbœxZ K‡i‡Q| Avgiv AviI 7.5% bM` jf¨vsk-Gi cÖÖ¯—ve K‡iwQ, ZeyI mvaviY mwÂwZ †_‡K 12.25 wgwjqb UvKv ¯’vbvš—i Kivi ciI ‡gvU mwÂwZ I DØ„Ë wn‡m‡e c~e©eZ©x eQ‡ii 471.99 wgwjqb UvKvi ¯’‡j GeQi w¯’wZ i‡q‡Q 493.42 wgwjqb UvKv|

j¶¨gvÎv-2013

Avgiv Avkv KiwQ †h AvBwWAviG exgv wk‡í weivRgvb †iqvZ, exgv nv‡ii j•Nb I Ab¨vb¨ Awbqg mg~n m¤ú~Y©iƒ‡c wejyß Ki‡Z bv cvi‡jI eûjvs‡k Kgv‡bvi Rb¨ Kvh©Ki c`‡¶c wb‡Z m¶g n‡e| exgv msµvš— wewa I cÖweavb mg~n ax‡i ax‡i cÖ¯‘Z n‡”Q Ges wKQz wKQz †¶‡Î exgv AvB‡bi avivi ¸i“Zi j•NbKvix †Kv¤úvbxi wei“‡× kvw¯—g~jK e¨e¯’v †bIqv n‡q‡Q|

†Kv¤úvbxi ‡gvU wcÖwgqvg Avq e„w× Kivi j‡¶¨ Avgiv Avgv‡`i wecYb wefvM mn Ab¨vb¨ wefvM mg~n‡K AviI kw³kvjx KiwQ Ges Avgiv Avkv KiwQ †h 2013 mv‡ji †gvU wcÖwgqvg Avq 360 wgwjqb UvKvi j¶¨gvÎv AR©b Ki‡Z m¶g n‡ev|

(Gg. gC`yj Bmjvg) †Pqvig¨vb

UNITED INSURANCE COMPANY LIMITED

13

The Directors alongwith the Company Secretary at the 27th Annual General Meeting

REPORT OF THE BOARD OF DIRECTORS OF UNITED INSURANCE COMPANY LIMITED FOR THE YEAR ENDED 31 DECEMBER 2012

DEAR SHAREHOLDERS

The Directors have great pleasure in presenting the 28th Annual Report with the Audited Accounts of the Company for the year ended 31 December 2012.

INSURANCE INDUSTRY AND UIC'S BUSINESS IN 2012

With a view to reforming the insurance industry, the Insurance Development and Regulatory Authority (IDRA) has introduced some restrictions on placing sponsors' business. Payment of commission at a uniform rate of 15% in all classes of premium was introduced since 1st April 2012 payable only to properly licensed agents after deduction of 5% tax at source. This came as a surprise to all policyholders who were hitherto used to get rebate around 45% to 50% of their insurance premium. With a view to reducing insurance costs policy holders began to take the minimum coverage of the risk involved. Some of the big policy holders of your company like the multinationals took global policies of their risks from their own re-insurers at fantastic low rates of premium amounting to depriving the country of a legitimate share of the premium. As a result, your company lost around Tk 50 million of premium income towards the end of 2012.

BDbvB‡UW BbwmI‡iÝ †Kv¤úvbx wjwg‡UW-Gi cwiPvjbv cl©‡`i 2012 mv‡ji 31 wW‡m¤^i Zvwi‡L mgvß eQ‡ii evwl©K cÖwZ‡e`b

wcÖq †kqvi‡nvìvie„›`

AZxe Avb‡›`i mv‡_ cwiPvjKgÛjxi Zid †_‡K 2012 mv‡ji 31 wW‡m¤^i Zvwi‡L mgvß eQ‡ii wbixw¶Z wnmvemn †Kv¤úvbxi 28Zg evwl©K cÖwZ‡e`b Dc¯’vcb KiwQ|

exgv wk‡íi cwi‡ek I †Kv¤úvbxi 2012 mv‡ji exgv e¨emv

exgv wkí cybM©V‡bi j‡¶¨ exgv Dbœqb I wbqš¿b KZ…©c¶ (AvBwWAviG) D‡`¨v³v cwiPvjK‡`i wbR¯^ exgv e¨emv wbqš¿‡bi Rb¨ wKQz eva¨evaKZv Av‡ivc K‡i‡Qb| 1jv GwcÖj 2012 mvj †_‡K mKj †kÖbxi exgv e¨emv‡qi Dci mgfv‡e 15% nv‡i Kwgkb cÖ`vb-Gi cÖ_v Pvjy Kiv nq hv 5% nv‡i Drm-Ki KZ©b-Gi ci ïaygvÎ h_vh_ jvB‡mÝavix G‡R›U‡K cÖ‡`q| Ghver Kvj †h mKj exgvMÖnxZv Zv‡`i exgv wcÖwgqv‡gi Dci 45% †_‡K 50% nv‡i Kwgkb †c‡Zb GB cÖ_v Zv‡`i mKj‡KB wew¯§Z K‡i‡Q| exgv msµvš— e¨q h‡_ô cwigv‡Y Kgv‡bvi Rb¨ ZvB exgvMÖnxZvMY Zv‡`i exgv SuzwKi by¨bZg wbivcËvi Rb¨ cwjwm MÖnY Ki‡Qb| Avcbv‡`i †Kv¤úvbxi exgvMÖnxZv‡`i g‡a¨ wKQz msL¨K eo exgvMÖnxZv †hgb eûRvwZK †Kv¤úvbxmg~n Zv‡`i wek¦vqb bxwZ I wbR¯^ cybtexgvKvixi gva¨‡g by¨bZg wcÖwgqvg nv‡i exgv wbivcËv MÖnY K‡i‡Qb, Z‡e Zviv Gi gva¨‡g exgv wcÖwgqv‡gi b¨vh¨ Ask †_‡K Avgv‡`i †`k‡K ewÂZ Ki‡Qb| GB mKj Kvi‡Y 2012 mv‡ji †k‡li w`‡K Avcbv‡`i †Kv¤úvbx cÖvq 50 wgwjqb UvKv wcÖwgqvg Avq nvwi‡q‡Q|

UNITED INSURANCE COMPANY LIMITED

14

The Shareholders at the 27th Annual General Meeting

Gross premium (Tk. in million)

2008 2009 2010 2011 2012

208.01 221.68

255.41

295.16271.73

Your Company earned a gross premium income of Tk 271.73 million against Tk 295.15 million in 2011, registering a decline of 7.93%. United's gross premium of Tk 271.73 million includes its own business of Tk 236.06 million and Tk 35.67 million received from the Sadharan Bima Corporation as a share of the public sector business.

In spite of a fall in premium income United earned a significant underwriting profit of Tk 31.34 million in the year under review against Tk 27.06 million in 2011.

FIRE INSURANCE BUSINESS

The Company wrote direct fire insurance business with a gross premium income of Tk 107 million against Tk 134 million in 2011. After payment of the re-insurance premium, the net premium of the Fire Department amounted to Tk 29.40 million. You will be glad to know that in spite of the higher claims of Tk 7.93 million against Tk 2.38 million in 2011, the Company earned an underwriting profit of Tk 6.45 million from its fire insurance business as against a profit of only Tk 0.19 million in 2011.

Avcbv‡`i †Kv¤úvbx 2011 mv‡ji ‡gvU wcÖwgqvg Avq 295.15 wgwjqb UvKvi Zzjbvq GeQi K‡i‡Q 271.75 wgwjqb UvKv †hLv‡b wcÖwgqvg n«vm †c‡q‡Q 7.93%| BDbvB‡UW BbwmI‡iÝ †Kv¤úvbxi ‡gvU wcÖwgqvg Avq 295.15 wgwjqb UvKvi g‡a¨ †Kv¤úvbxi wbR¯^ e¨emv i‡q‡Q 236.06 wgwjqb UvKv Ges mvavib exgv K‡c©v‡ikb †_‡K ivóªxq Lv‡Zi Ask i‡q‡Q 35.67 wgwjqb UvKv|wcÖwgqvg Avq n«vm cvIqv m‡Ë¡I BDbvB‡UW BbwmI‡iÝ †Kv¤úvbx wjwg‡UW 2011 mv‡ji 27.06 wgwjqb UvKvi ¯’‡j Av‡jvP¨ eQ‡i D‡j-L‡hvM¨ 31.34 wgwjqb UvKv AewjLb gybvdv AR©b K‡i‡Q|

AwMœ exgv e¨emv

†Kv¤úvbx AwMœ exgv e¨emv

†_‡K †gvU wcÖwgqvg Avq

K‡i‡Q 107 wgwjqb UvKv hv 2011 mv‡j wQj 134 wgwjqb UvKv| cybtexgv wcÖwgqvg cÖ`v‡bi ci †Kv¤úvbxi AwMœexgv wefvM †_‡K †bU wcÖwgqvg Avq n‡q‡Q 29.40 wgwjqb UvKv| Avcbviv ‡R‡b Avbw›`Z n‡eb †h 2011

mv‡ji 2.38 wgwjqb UvKvi Zzjbvq AwaKZi exgv`vwe 7.93 wgwjqb UvKv cwi‡kv‡ai ciI weMZ eQ‡ii 0.19 wgwjqb UvKv gybvdvi ¯’‡j AwMœexgv wefvM †_‡K GeQi †Kv¤úvbx AewjLb gybvdv K‡i‡Q 6.45 wgwjqb UvKv|

UNITED INSURANCE COMPANY LIMITED

15

Total assets (Tk. in million)

20122008 2009 2010 2011

770 726

845

949

1,023

MARINE INSURANCE BUSINESS

The gross premium income from marine insurance business increased to Tk 90 million from Tk 83 million in 2011, yielding a net premium of Tk 64.66 million, after re-insurance cessions. The Company made an underwriting profit of Tk 14.13 million against Tk 13.79 million in 2011 after making necessary provision for claims, both paid and intimated.

MOTOR AND MISCELLANEOUS INSURANCE BUSINESS

In Motor, the Company earned a gross premium income of Tk 33 million as against Tk 35 million in 2011. The net claims in Motor slightly rose to Tk 5.76 million from Tk 5.12 million in 2011. The profit from Motor insurance business, however, rose slightly to Tk 9.70 million from Tk 9.06 million in 2011.

Premium income from Miscellaneous insurance business was Tk 42 million as was in 2011, and we registered a profit of Tk 1.05 million against Tk 4.01 million in 2011.

INCOME FROM INVESTMENT

Interest income derived from banks and non-banking financial institutions increased to Tk 60.39 million from Tk 42.52 million in 2011. This was the result of a high interest rate which was steady almost throughout the period.

The dividend income, other than from shares of our associate company, United Leasing Company Ltd, increased to Tk 0.34 million from Tk 0.11 million in

‡bŠ exgv e¨emv

†bŠ exgv e¨emv †_‡K †gvU wcÖwgqvg Avq MZeQ‡ii 83 wgwjqb UvKv †_‡K e„w× †c‡q G eQi n‡q‡Q 90 wgwjqb UvKv| cybtexgv wcÖwgqvg cÖ`v‡bi ci †Kv¤úvbxi ‡bŠ exgv wefvM †_‡K †bU wcÖwgqvg Avq n‡q‡Q 64.66 wgwjqb UvKv| cÖ`Ë I cÖ‡`q exgv`vwei wecix‡Z h_vh_ ms¯’v‡bi ci 2011 mv‡ji 13.79 wgwjqb UvKvi Zzjbvq 2012 mv‡j ‡Kv¤úvbx AewjLb gybvdv AR©b K‡i‡Q 14.13 wgwjqb UvKv|

‡gvUi I wewea exgv e¨emv

†Kv¤úvbx ‡gvUi exgv e¨emv †_‡K 2011 mv‡ji 35 wgwjqb UvKvi ¯’‡j 2012 mv‡j †gvU wcÖwgqvg AR©b K‡i‡Q 33 wgwjqb UvKv| ‡gvUi exgv`vwe 2011 mv‡j 5.12 wgwjqb UvKvi Zzjbvq GeQi mvgvb¨ †e‡o 5.76 wgwjqb UvKv n‡q‡Q| GZ`m‡Ë¡I ‡gvUi exgv e¨emv †_‡K gybvdv 2011 mv‡ji 9.06 wgwjqb UvKv †_‡K ‡e‡o G eQi 9.70 wgwjqb UvKvq DbœxZ n‡q‡Q| wewea exgv e¨emv †_‡K ‡gvU wcÖwgqvg Avq n‡q‡Q 42 wgwjqb UvKv hv 2011 mv‡ji Av‡qi mgcwigvY Ges 2011 mv‡ji gybvdv 4.01 wgwjqb UvKvi ¯’‡j Avgiv G wefvM ‡_‡K G eQi Ki‡Z †c‡iwQ 1.05 wgwjqb UvKv|

wewb‡qvM †_‡K Avq

e¨vsK I Ab¨vb¨ Avw_©K cÖwZôvb ‡_‡K AvgvbZ †_‡K cÖvß my` Avq 2011 mv‡ji 42.52 wgwjqb UvKvi ¯’‡j G eQi Zv e„w× †c‡q 60.39 wgwjqb UvKvq DbœxZ n‡q‡Q| Gi Ab¨Zg KviY n‡”Q cÖvq mviv eQi a‡iB D”P my‡`i nvi w¯’Zve¯’vq wQj| Avgv‡`i G‡mvwm‡qU BDbvB‡UW wjwRs †Kv¤úvbx wjwg‡UW †_‡K cÖvß jf¨vsk Avq e¨wZ‡i‡K Acivci †Kv¤úvbx mg~n †_‡K jf¨vsk Avq 2011 mv‡ji 0.11 wgwjqb UvKv †_‡K

Underwriting profit (Tk. in million)

20122008 2009 2010 2011

5.45

12.96

20.45

27.06

31.34

UNITED INSURANCE COMPANY LIMITED

16

PROFIT AND LOSS ACCOUNT

The salient features are given below:

2012 2011 Taka TakaGross Premium 271,730,213 295,150,130Net Premium 136,746,267 154,430,137Underwriting profit 31,343,473 27,056,310Interest income 60,048,736 42,369,412Dividend income 14,643,578 8,324,550Profit before tax 134,638,078 132,090,338Provision for tax 36,000,000 27,000,000Transfer to Reserve forexceptional losses 13,674,627 15,443,014

Divisible profit 52,012,240 58,592,283

2011. We also earned Tk 0.68 million through buying and selling of shares in the secondary market.

From United Leasing Company Limited, we received a cash dividend of Tk 14.30 million and 3,813,914 bonus shares in 2012 against a cash dividend of Tk 8.17 million and 544,845 bonus shares in 2011.

The incidence of tax in 2012 was, however, much higher than in the previous year because our taxable income was earned primarily from our insurance business on which we had to pay income tax at the rate of 42.5%. In previous year a much larger part of our income was derived from the stock market on which the tax rate was only 10%.

You know that owing to application of BAS-28: Investment in Associates, the balance of profit in the profit and loss appropriation account amounted to Tk 230.62 million which is not entirely divisible to the shareholders. However, after deducting the unrealised profit of its associate and with necessary adjustments regarding cash dividend received from the same associate and deferred tax income etc, the divisible profit for the year 2012 arises to Tk 52.01 million.

DIVIDEND

For the year 2011, the Company declared a cash dividend of 10% and a stock dividend of 10%. You know that all non-life insurance companies have to raise their paid-up capital at least to Tk 400 million.

Avgiv †kqvi evRv‡i †kqvi µq-weµ‡qi gva¨‡g Av‡jvP¨ eQ‡i 0.68 wgwjqb UvKv Avq K‡iwQ|

BDbvB‡UW wjwRs †Kv¤úvbx †_‡K Avgiv 2011 mv‡j 8.17 wgwjqb UvKv bM` jf¨vsk I 544,845wU †evbvm †kqvi ‡c‡qwQjvg| Avgiv Zv‡`i †_‡K GeQi †c‡qwQ 14.30 wgwjqb UvKv bM` jf¨vsk I 3,813,914wU †evbvm †kqvi|

2012 mv‡j ‡Kv¤úvbxi ‡gvU cÖ‡`q AvqKi eve` GKUv eo A‡¼i ms¯’vb ivLv n‡q‡Q| hvi Ab¨Zg KviY nÕj †Kv¤úvbxi g~j e¨emv A_©vr exgv e¨emv †_‡K Ki‡hvM¨ Avq h‡_ó cwigv‡Y †ekx n‡q‡Q ‡h Av‡qi Dci †Kv¤úvbx‡K AvqKi cÖ`vb Ki‡Z n‡”Q 42.5% nv‡i| Z‡e MZeQi Avgv‡`i gybvdvi GKUv weivU Ask wQj †kqvievRvi †_‡K cÖvß Avq hvi Dci †Kv¤úvbx‡K Ki w`‡Z n‡qwQj 10% nv‡i|

Avcbviv Rv‡bb †h evsjv‡`k wnmve gvb ÔweGGm-28: Bb‡f÷‡g›U Bb G‡mvwm‡qUmÕ cÖ‡qv‡Mi d‡j GeQi jvf-‡jvKmvb Ave›Ub wnmv‡ei DØ„Ë `uvwo‡q‡Q 230.62 wgwjqb UvKv hv ‡Kv¤úvbxi †kqvi‡nvìvi‡`i g‡a¨ m¤ú~Y©iƒ‡c e›Ub‡hvM¨ bq| Z‡e †Kv¤úvbxi mn‡hvMx cÖwZôv‡bi AbM`vqbK…Z gybvdv ev` ‡`Iqvi ci Ges Zv ‡_‡K cÖvß bM` jf¨vsk I wejw¤^Z AvqKi BZ¨vw` mgš^‡qi ci 2012 mv‡j †Kv¤úvbxi e›Ub‡hvM¨ gybvdv `vwo‡q‡Q 52.01 wgwjqb UvKv|

jf¨vsk

2011 mv‡ji e›Ub‡hvM¨ gybvdv †_‡K †Kv¤úvbxi cl©` 10% bM` jf¨vsk I 10% ÷K jf¨vsk mycvwik K‡iwQj| Avcbviv Rv‡bb †h mKj bb-jvBd BbwmI‡iÝ †Kv¤úvbx‡K Zv‡`i cwi‡kvwaZ g~jab Kgc‡¶ 400 wgwjqb UvKvq DbœxZ Ki‡Z

Net claims paid (Tk. in million)

2008

24 24

18

16

13

2009 2010 2011 2012

UNITED INSURANCE COMPANY LIMITED

17

Participants at the 20th Branch Managers' Conference at Camellia House

In compliance with the provisions of the Insurance Act, 2010 relating to minimum paid-up capital, we recommend a stock dividend of 10.19% amounting to Tk 37 million to raise the paid-up capital to Tk 400 million, and also a cash dividend of 7.5% from the divisible profit of 2012 and withdrawing Tk 12.25 million from the general reserve.

ASSETS

The assets of the Company increased to Tk 1,023.48 million from Tk 948.64 million in 2011.

PROSPECTS FOR 2013

We hope that the Insurance Development and Regulatory Authority (IDRA) will be able to introduce measures that will help to remove substantially the irregularities that have so far vitiated the smooth and efficient functioning of the insurance companies. If necessary reforms are implemented, we hope that United Insurance with its prudent underwriting will be able to achieve our target of a gross premium of Tk 360 million.

DIRECTORS-APPOINTMENT & RE-APPOINTMENT

In accordance with the provision of clauses 153, 154 and 155 of the Articles of Association of the Company, the following sponsor and institutional directors retire and being eligible offer themselves for re-election:

n‡e| exgv AvBb 2010-Gi by¨bZg cwi‡kvwaZ g~jab msµvš— weavb ‡gvZv‡eK ‡Kv¤úvbxi cwi‡kvwaZ g~jab 400 wgwjqb UvKvq DbœxZ Kivi j‡¶¨ Avgiv 2012 mv‡ji e›Ub‡hvM¨ gybvdv Ges mvaviY mwÂwZ †_‡K 12.25 wgwjqb UvKv D‡Ëvjb K‡i 10.19% nv‡i †gvU 37 wgwjqb UvKvi †evbvm †kqvimn AviI 7.5% bM` jf¨vsk-Gi cÖ¯—ve K‡iwQ|

cwim¤ú`

†Kv¤úvbxi cwim¤ú` 2011 mv‡ji 948.64 wgwjqb UvKv †_‡K †e‡o GeQi `uvwo‡q‡Q 1,023.48 wgwjqb UvKv|

2013 mv‡ji c~e©vfvm

Avgiv Avkv KiwQ ‡h mKj Awbqg BbwmI‡iÝ †Kv¤úvbxmg~‡ni mvewjj I my`¶ Kvh©µg eûjvs‡k ¶wZMÖ¯’ K‡i‡Q exgv Dbœqb I wbqš¿Y KZ…©c¶ (AvBwWAviG) †m¸wj h‡_ô cwigv‡Y `~i Ki‡Z cÖ‡qvRbxq Ges Kvh©Ki e¨e¯’v wb‡Z m¶g n‡e| hw` cÖ‡qvRbxq cybM©Vb e¨e¯’vw` ev¯—evqb Kiv m¤¢e nq Avgiv Avkv Kwi †h BDbvB‡UW BbwmI‡iÝ †Kv¤úvbx Gi my`¶ AewjL‡bi gva¨‡g Avgv‡`i 360 wgwjqb UvKvi †gvU wcÖwgqvg Av‡qi j¶¨gvÎv AR©b Ki‡Z m¶g n‡e|

cwiPvjKe„›`- wb‡qvM I cybtwb‡qvM

†Kv¤úvbxi AvwU©‡Kjm Ae G‡mvwm‡qk‡bi 153, 154 I 155

aviv Abyhvqx wbgœwjwLZ D‡`¨v³v Ges cÖvwZôvwbK cwiPvjKe„›`

Aemi MÖnY K‡i‡Qb Ges †hvM¨ weavq Zviv cybtwbe©vP‡bi

AvMÖn e¨³ K‡i‡Qb t

UNITED INSURANCE COMPANY LIMITED

18

20132008 2009 2010 2011 2012

Paid-up capital (Tk. in million)

100

250

300330

363

400

1. Mr. M. Moyeedul Islam

2 Mr. M. Saiful Islam.

In accordance with the same provisions of the Articles of Association of the Company, Mr. Syed Aziz Ahmad, Director from amongst the public subscribers, also retires and offers himself for re-election.

The appointment of Mr. M. M. Alam, the existing Independent Director, and Mr. M. Hafizullah the newly co-opted Independent Director, requires approval of the shareholders for 3 year-term to 2015 as per the BSEC Corporate Governance Notification dated 7 August 2012.

The notice of the 28th Annual General Meeting dated 2 March 2013, containing information relevant to the election of Directors from public subscribers, will be published in two national dailies on 3 March 2013.

AUDITORS

Pursuant to the Section 210 of the Companies Act 1994, the Company's statutory auditors M/s. M. J. Abedin & Co, Chartered Accountants, retire and being eligible has offered their services for another year.

STATEMENT OF DIRECTORS ON FINANCIAL REPORTS

The financial statements together with notes

thereon have been prepared in conformity with

the Companies Act, 1994, Insurance Act, 2010

and in some applicable cases Insurance Act 1938

and Securities & Exchange Commission Rules,

1987. These statements present fairly company's

state of affairs, the result of its operations, cash

flows and changes in equity.

Proper books of account of the company have been maintained.

1| wgt Gg. gC`yj Bmjvg

2| wgt Gg. mvBdzj Bmjvg|

†Kv¤úvbxi AvwU©‡Kjm Ae G‡mvwm‡qk‡bi GKB aviv Abymi‡Y mvaviY †kqvi‡nvìvi‡`i ga¨ †_‡K wbe©vwPZ cwiPvjK wgt ˆmq` AvwRR Avn&g` Aemi MÖnY K‡i‡Qb Ges †hvM¨ weavq wZwb cybtwbe©vP‡bi AvMÖn e¨³ K‡i‡Qb|

7 AvMó 2012 Zvwi‡Li weGmBwm K‡cv©‡iU Mfv‡b©Ý †bvwUwd‡Kkb Abymv‡i † k q v i ‡ n v ì v i ‡ ` i Aby‡gv`bµ‡g we`¨gvb ¯^Zš¿ cwiPvjK wg: Gg. Gg. Avjg I bZzb g‡bvwbZ ¯^Zš¿ cwiPvjK wg: Gg. nvwdRyj-vn& 3 eQ‡ii Rb¨ 2015 mvj ch©š— wb‡qvM cÖvß n‡eb|

mvaviY †kqvi‡nvìvi‡`i ga¨ †_‡K cwiPvjK wbe©vPb msµvš— Z_¨mg~n 2 gvP©

2013 ZvwiL m¤^wjZ 28Zg evwl©K mvaviY mfvi †bvwUm RvZxq ˆ`wbK cwÎKvq 3 gvP© 2013 Zvwi‡L cÖKvwkZ nq|

wbix¶Ke„›`

†Kv¤úvbx AvBb 1994- Gi aviv 210 Abyhvqx †Kv¤úvbxi wewae× wbix¶Ke„›`, †gmvm© Gg. †R. Av‡e`xb GÛ †Kvs, PvU©vW© GKvD›U¨v›Um- Gi Kvh©Kvj mgvß n‡q‡Q Ges †hvM¨ weavq Zuviv cyYtwb‡qv‡Mi AvMÖn e¨³ K‡i‡Qb|

Avw_©K weeiYxi Dci cwiPvjKgÊjxi cÖwZ‡e`b

†Kv¤cvbx AvBb 1994, exgv AvBb 2010 Ges wKQy wKQy

cÖ‡hvR¨ †¶‡Î exgv AvBb 1938 Ges wmwKDwiwUR I

G·‡PÄ Kwgkb wewagvjv, 1987 Abyhvqx †Kv¤úvbxi

Avw_©K weeiYxmg~n Ges mshy³ UxKvmg~n ˆZix Kiv

n‡q‡Q| G weeiYxmg~n †Kv¤cvbxi Avw_©K Ae¯’v, mgvß

eQ‡ii Kvh©µ‡gi djvdj Ges bM` A_© cÖev‡ni myôy

cÖwZdjb K‡i|

†Kv¤úvbxi cÖ‡qvRbxq wnmve ewnmg~n mwVKfv‡e msiw¶Z n‡q‡Q|

a)

b)

K)

L)

UNITED INSURANCE COMPANY LIMITED

19

A social gathering at 20th Branch Managers' Conference at Camellia House

Appropriate accounting policies have been consistently applied in preparation of the financial statements and the accounting estimates are based on reasonable and prudent judgment.

International Accounting Standards, as applicable in Bangladesh, have been followed in preparation of the financial statements.

The system of internal control is sound in design and has been effectively implemented and monitored.

There are no significant doubts about the company's ability to continue as a going concern.

There is no significant deviation from the operating result of the last year.

BOARD MEETING ATTENDANCE

During the year, 6 (six) Board Meetings were held. The attendance of the Directors is shown in Annexure-1.

PATTERN OF SHAREHOLDING

The pattern of shareholding as per clause 1.5 (xxi) of the BSEC Notification No: SEC/CMRRCD/2006-158/134/Admin/44 dated August 7, 2012 is shown in Annexure-2.

KEY OPERATING AND FINANCIAL DATA

The Company's summarised key operating and financial data for the last five years are shown in page 9.

Avw_©K weeiYxmg~n ˆZix‡Z mwVK wnmve bxwZgvjvmg~n h_vh_fv‡e cÖ‡qvM Kiv n‡q‡Q| Z‡e †hLv‡b Gi e¨Z¨q N‡U‡Q Zv cÖKvk Kiv n‡q‡Q| wnmve Abygvbmg~n hyw³ m½Zfv‡e I weP¶YZvi mv‡_ Kiv n‡q‡Q|

evsjv‡`‡k G ch©š— cÖ‡hvR¨ Avš—©RvwZK wnmvegvb mg~n Abyhvqx †Kv¤úvbxi Avw_©K weeiYxmg~n cÖ¯‘Z Kiv n‡q‡Q|

Af¨š—ixb wbqš¿Y e¨e¯’v my`„pfv‡e cÖYxZ Ges hvi cÖ‡qvM Ges ch©‡e¶Y AZxe Kvh©Ki|

Pjgvb cÖwZôvb wnmv‡e †Kv¤úvbxi m¶gZvq we›`ygvÎ †Kvb m‡›`n ‡bB|

weMZ eQ‡ii Kvh©µ‡gi Zzjbvq †Zgb ¸iZ¡c~Y© †Kvb wePz¨wZ †bB|

cl©` mfvq Dcw¯’wZ

Av‡jvP¨ eQ‡i 6 wU cl©` mfv AbywôZ nq| cwiPvjK‡`i Dcw¯’wZ Annexure-1 G ‡`Lv‡bv nÕj|

†kqvi‡nvwìs aiY

weGmBwm †bvwUwd‡Kkb bs GmBwm/wmGgAviAviwmwW/2006-158/134 /GWwgb/44/ ZvwiL AvM÷ 7, 2012 Gi wbix¶v 1.5 (xxi) Abyhvqx ‡Kv¤úvbxi ‡kqvi‡nvwìs Gi aiY Annexure-2 G †`Lv‡bv nÕj|

D‡j-L‡hvM¨ Avw_©K Z_¨

†Kv¤úvbxi c~e©eZ©x cuvP eQ‡ii D‡j-L‡hvM¨ Avw_©K I Ab¨vb¨ Z_¨mg~n 9g c„ôvq †`Lv‡bv nÕj|

c)

d)

e)

f )

g)

M)

N)

O)

P)

Q)

UNITED INSURANCE COMPANY LIMITED

20

Total Reserves (Tk. in million)

BRIEF RESUME OF THE DIRECTORS

Brief resume of the Directors as per clause 1.5 (xxii) of the BSEC Notification No: SEC/CMRRCD/2006-158/134/Admin/44 dated August 7, 2012 is shown in page 5.

REPORT ON THE ACTIVITIES OF THE AUDIT COMMITTEE

Pursuant to the clause 3.5 of the BSEC Notification No: SEC/CMRRCD/2006-158/134/Admin/44 dated August 7, 2012 the activities of the Audit Committee have been shown in page 28.

CORPORATE GOVERNANCE COMPLIANCE REPORT

Pursuant to the clause 7(ii) of the BSEC Notification No. SEC/CMRRCD/2006-158/134/Admin/44 dated August 7, 2012 we attach the Company's compliance status as Annexure-3.

CERTIFICATION ON COMPLIANCE OF CORPORATE GOVERNANCE

Certificate from professional accountants on compliance with the conditions as per clause 7(i) of the BSEC Notification No: SEC/CMRRCD/2006-158/134/Admin/44 dated August 7, 2012 has been shown as Annexure-4.

ACKNOWLEDGEMENT

We thank all our valued clients and well-wishers for the confidence they have reposed in us. We also thank our staff at the head office, zonal offices and branches and all our agents for their hard and dedicated work. We are grateful to our shareholders for their help, advice and cooperation in building United Insurance Company Limited as a Company that represents the best traditions of the

cwiPvjK‡`i msw¶ß Rxebx

weGmBwm †bvwUwd‡Kkb bs GmBwm/wmGgAviAviwmwW/2006-158/134/GWwgb/44/ ZvwiL AvM÷ 7, 2012 Gi wbix¶v 1.5 (xxii) Abyhvqx †Kv¤úvbxi cwiPvjK‡`i msw¶ß Rxebx 5g c„ôvq mshy³ Kiv n‡q‡Q|

wbix¶v KwgwUi Kvh©µ‡gi Dci cÖwZ‡e`b

weGmBwm †bvwUwd‡Kkb bs GmBwm/wmGgAviAviwmwW/2006-158/134/GWwgb/44/ ZvwiL AvM÷ 7, 2012 Gi wbix¶v 3.5 Abyhvqx †Kv¤úvbxi wbix¶v KwgwUi Kvh©µ‡gi Dci cÖwZ‡e`b 28Zg c„ôvq mshy³ Kiv n‡q‡Q|

K‡c©v‡iU Mfv‡b©Ý cwicvjb cÖwZ‡e`b

weGmBwm †bvwUwd‡Kkb bs GmBwm/wmGgAviAviwmwW/2006-158/134/GWwgb/44/ ZvwiL AvM÷ 7, 2012 Gi wbix¶v 7(ii) Abyhvqx †Kv¤cvbxi cwicvjb Ae¯’v Annexure-3 G mshy³ Kiv n‡q‡Q|

K‡c©v‡iU Mfv‡b©Ý cwicvjb-Gi mb`

weGmBwm †bvwUwd‡Kkb bs GmBwm/wmGgAviAviwmwW/2006-158/134/GWwgb/44/ ZvwiL AvM÷ 7, 2012 Gi wbix¶v 7(i) Abyhvqx †Kv¤úvbxi K‡c©v‡iU Mfv‡b©Ý cwicvjb-Gi mb` Annexure-4 G mshy³ Kiv n‡q‡Q|

K…ZÁZv m¦xKvi

mKj m¤§vwbZ MÖvnK I kyfvbya¨vqxe„›` †h Av¯’v Avgv‡`i Dci †i‡L‡Qb ‡mRb¨ Avgiv Zv†`i Avš—wiK ab¨ev` RvbvB| Avgiv

Avgv‡`i cÖavb Kvh©vjq, †Rvbvj Awdm I kvLv mg~‡ni mKj Kg©Pvix-Kg ©KZv © ‡K Ges G‡R›U‡`i‡K Zv‡`i wb‡ew`Z mvwe©K cÖ‡Póvi Rb¨ ab¨ev` Rvbvw”Q| m¤§vwbZ ‡kqvi‡nvìvie„›` Zv‡`i mvnvh¨, mn‡hvwMZv I Dc‡`‡ki gva¨‡g BDbvB‡UW BbwmI‡iÝ †Kv¤úvbx†K exgv wk‡í †kÖô HwZ‡n¨i aviK wn‡m‡e cÖwZwôZ Kivi Rb¨ Avgiv

Total reserves

2008

2009

2010

2011

2012

295

349

424

472

506

UNITED INSURANCE COMPANY LIMITED

21

insurance industry. We appreciate the help and cooperation that we have received from the various Ministries, the Bangladesh Bank and other banks and financial institutions, Dhaka Stock Exchange and Bangladesh Securities and Exchange Commission. We particularly appreciate the advice we have always received from the Chairman and Members and cooperation fromthe officers of the Insurance Development and Regulatory Authority (IDRA) and seek their continuous cooperation to run the affairs of the Company smoothly and in a prudent manner.

FOR THE BOARD OF DIRECTORS

(M. MOYEEDUL ISLAM)Chairman

Zv‡`i cÖwZ Mfxi K…ZÁZv Ávcb KiwQ| Avgiv wewfbœ gš¿bvjq, evsjv‡`k e¨vsKmn Ab¨vb¨ evwYwR¨K e¨vsK, Avw_©K cÖwZôvb, XvKv ÷K G·‡PÄ I evsjv‡`k wmwKDwiwUR GÛ G·‡PÄ Kwgkb ‡_‡K †h mvnvh¨ I mn‡hvwMZv †c‡q G‡mwQ Zvi Rb¨ Mfxi K…ZÁZv cÖKvk KiwQ| exgv Dbœqb I wbqš¿Y KZ…©c¶ (AvBwWAviG)-Gi †Pqvig¨vb I m`m¨e„›` †_‡K me©`v †h Dc‡`k Avgiv †c‡qwQ Ges Kg©KZ©v‡`i wbKU †_‡K †h mn‡hvwMZv †c‡qwQ †mRb¨ Avgiv Zv‡`i cÖwZ we‡klfv‡e K…ZÁZv Ávcb KiwQ Ges ‡Kv¤úvbxi mKj Kvh©µg myPvi“iƒ‡c m¤úbœ Ki‡Z Zv‡`i KvQ †_‡K me©`v Abyiƒc mn‡hvwMZv Kvgbv KiwQ|

cwiPvjKgÛjxi c‡¶

(Gg.gC`yj Bmjvg)†Pqvig¨vb

UNITED INSURANCE COMPANY LIMITED

22

UNITED INSURANCE COMPANY LIMITED

23

STATUS OF COMPLIANCE OF CORPORATE GOVERNANCEStatus of compliance with the conditions imposed by the Securities and Exchange Commission's

notification no. SEC/CMRRCD/2006-158/134/Admin/44 dated August 7, 2012 issued under section2CC of the Securities & Exchange Ordinance, 1969:

Annexure -3

UNITED INSURANCE COMPANY LIMITED

24

UNITED INSURANCE COMPANY LIMITED

25

UNITED INSURANCE COMPANY LIMITED

26

Annexure-4

CERTIFICATE OF THE COMPLIANCE TO THE SHAREHOLDERS OFUNITED INSURANCE COMPANY LIMITED

(As required under the BSEC Guidelines)

We have examined compliance to the BSEC guidelines on Corporate Governance of United Insurance

Company Limited for the year ended 31st December 2012. These guidelines relate to the notification

no SEC/CMRRCD/2006-158/134/Admin/44 dated 7 August 2012 of Bangladesh Securities and

Exchange Commission (BSEC) on Corporate Governance. Such compliance to the codes of Corporate

Governance is the responsibility of the company. Our examination was limited to the procedures and

implementation thereof as adopted by the Management in ensuring compliance to the conditions of

Corporate Governance. This is a scrutiny and verification only and not an examination of opinion or

audit on the financial statements of the company.

In our opinion and to the best of our information and according to the explanations provided to us,

we certify that the Company has complied with the conditions of corporate governance as stipulated

in the above mentioned Guidelines issued by BSEC. We also state that such compliance is neither an

assurance as to the future viability of the company nor a certification on the efficiency or effectiveness

with which the Management has conducted the affairs of the company.

Chartered Accountants

Dated: DhakaApril 09, 2013

Hoque Bhattacharjee Das & Co.Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

28

REPORT OF THE AUDIT COMMITTEE-2012

The Committee comprises of four non-executive directors two of whom are independent directors. The members of the Committee are as follows:

Mr. M. M. Alam FCA (Independent Director), Chairman

Mr. M. Saiful Islam, Member

Mr. M. Shah Alam, Member

Mr. M. Hafizullah (Independent Director), Member

Mr. Badal Chandra Rajbangshi, Company Secretary is the Secretary to the Committee.

Mr. Syed Shahriyar Ahsan, Managing Director of the Company attended the meetings as an invitee. Other invitees to the meetings were the Chief Financial Officer and the Head of Internal Audit. Relevant heads of departments attended the meetings as required.

A total of 4 (four) meetings were held during 2012.

The following matters were discussed in the meetings and decisions taken were communicated to the Board of Directors:

Review of the auditors' report and audited accounts for the year 2011.

Review of the un-audited first quarter report 2012.

Review of the un-audited half-yearly report 2012.

Review of the un-audited third quarter report 2012.

Reviewed the job description of the Head of Internal Audit.

Review of internal audit reports of the Head Office/branches.

Review of the management letter 2011 submitted by the external auditors.

The committee was not aware of any issues in the following areas, which needs to be reported to the Board (i) Report on conflicts of interests; (ii) Suspected or presumed fraud or irregularity or material defect in the internal control system and (iii) Suspected infringement of laws, including securities related laws, rules and regulations.

Dated, Dhaka

2 March 2013

ChairmanAudit Committee

UNITED INSURANCE COMPANY LIMITED

29

VALUE ADDED STATEMENTFor the year ended 31 December 2012 (Taka in million)

Re-insurance ceded

Employees services and benefits

Net claims

Income tax to Government

Dividend to shareholders

Depreciation, retained profit and reserves

Head of accounts 2012 (Taka)

Gross premium income 271.73

Investment and other income 61.35

Share of profit of associate 47.27

Commission on re-insurance ceded 44.41

424.76

Less: Purchases of supplies and services 69.62

355.14

Re-insurance ceded 134.98 38%

Employees services and benefits 66.55 19%

Net claims 24.34 7%

Income tax to Government 36.00 10%

Dividend to shareholders 66.00 19%

Depreciation, retained profit and reserves 27.27 8%

355.14 100%

AUDITORS' REPORT TO THE SHAREHOLDERS OFUNITED INSURANCE COMPANY LIMITED

We have audited the accompanying balance sheet of the United Insurance Company Limited as of 31

December 2012 and the related revenue accounts as well as the profit and loss account, profit and loss

appropriation account, cash flow statement for the year then ended and a summary of significant

accounting policies and explanatory notes thereto.

Management's responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial statements in

accordance with Bangladesh Financial Reporting Standards (BFRSs), and for such internal control as

management determines is necessary to enable the preparation of these financial statements that are

free from material misstatement, whether due to fraud or error.

Auditors' responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We

conducted our audit in accordance with Bangladesh Standards on Auditing. Those standards require

that we comply with ethical requirements and plan and perform the audit to obtain reasonable

assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures

in the financial statements. The procedures selected depend on the auditors' judgment, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or

error. In making those risk assessments, auditor considers internal control relevant to the entity's

preparation and fair presentation of the financial statements in order to design audit procedures that

are appropriate in the circumstances, but not for the purpose of expressing an opinion on the

effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of

accounting policies used and the reasonableness of accounting estimates made by management, as

well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis

for our audit opinion.

Opinion

In our opinion, the financial statements prepared in accordance with Bangladesh Financial Reporting

Standards (BFRSs), give a true and fair view of the state of the Company's affairs as of 31 December

2012 and the results of its operations and its cash flows for the year then ended and comply with the

Companies Act 1994, the Insurance Act 2010 and in some applicable cases, Insurance Act 1938, the

Insurance Rules 1958, the Securities and Exchange Rules 1987 and other applicable laws and

regulations.

UNITED INSURANCE COMPANY LIMITED

30

We also report that:

we have obtained all the information and explanations which to the best of our knowledge and

belief were necessary for the purposes of our audit and made due verification thereof;

in our opinion, proper books of account as required by law have been kept by the company so

far as it appeared from our examination of those books and (where applicable) proper returns

adequate for the purpose of our audit have been received from branches not visited by us and

incorporated in the accompanying accounts;

the company's balance sheet and profit and loss account and cash flows dealt with by the report

are in agreement with the books of account;

the expenditure incurred were for the purposes of the company's business;

as per section 40-C (2) of the Insurance Act 1938 as amended, we certify that to the best of our

knowledge and belief and according to the information and explanations given to us, all

expenses of management wherever incurred and whether incurred directly or indirectly, in

respect of insurance business of the company transacted in Bangladesh during the year under

report have been duly debited to the related revenue accounts and the profit and loss account

of the company and

as per regulation 11 of part 1 of the third schedule of the Insurance Act 1938 as amended, we

certify that to the best of our information and as shown by its books, the company during the

year under report has not paid any person any commission in any form outside Bangladesh in

respect of any of its business re-insured abroad.

M. J. ABEDIN & CODhaka, 2 March 2013 Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

31

(i)

(ii)

(iii)

(iv)

(v)

(vi)

UNITED INSURANCE COMPANY LIMITED

32

Share capital:

Authorised:

50,000,000 ordinary shares of Tk 10 each

Issued, subscribed and paid-up:

36,300,000 ordinary shares of Tk 10 each (For 2011 - 33,000,000 ordinary shares of Tk 10 each fully paid-up)

Reserve or contingency accounts:

Reserve for exceptional losses

General reserve (Note-18)

Profit and loss appropriation account balance

Balances of funds and accounts:

Fire insurance business

Marine insurance business

Motor insurance business

Miscellaneous insurance business

Premium deposits

Estimated liability in respect of outstanding claims whether due or intimated

Amount due to other persons or bodies carrying on insurance business

Sundry creditors (including provision for expenses and taxes)

Lease obligations

Unclaimed dividend

500,000,000

363,000,000

199,944,952

70,350,000

235,370,860

11,759,124

26,378,112

13,104,414

3,972,838

55,214,488

1,085,554

18,801,652

10,302,553

64,015,875

-

5,394,889

1,023,480,823

4

5

6

7

8

21

22

500,000,000

330,000,000

186,270,325

82,600,000

203,115,773

21,220,449

21,042,296

13,397,333

7,701,870

63,361,948

770,613

8,040,780

6,537,439

64,345,887

343,720

3,251,887

948,638,372

BALANCE SHEET

CAPITAL & LIABILITIES Notes 2012 Taka

2011 Taka

Notes 1 to 31 form an integral part of these statement of accounts

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

UNITED INSURANCE COMPANY LIMITED

33

Investment

Statutory deposit: Bangladesh Govt. Treasury Bond

Investment in shares:

Shares - at cost

Investment in Associate

Deferred tax assets

Outstanding premium

Accrued interest

Amount due from other persons or bodies carrying on insurance business

Debtors (including advances, deposits and prepayments and others)

Cash and cash equivalents

Other accounts:

Property, plant and equipment (at cost less accumulated depreciation)

Stationery and forms

Net Asset Value per share (2011: restated)

4,500,000

21,470,925

369,001,568

9,798,098

37,425,376

26,673,124

39,924,393

13,233,027

484,266,293

16,367,559

820,460

1,023,480,823

23.93

9

9

10

11

12

13

14

4,500,000

21,037,187

336,034,999

8,756,462

51,763,919

19,944,528

33,740,066

8,163,401

456,527,480

7,403,073

767,257

948,638,372

22.09

AS AT 31 DECEMBER 2012

PROPERTY & ASSETS Notes 2012Taka

2011 Taka

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

34

Expenses of management (not applicable to anyparticular fund or account):

Audit fees

CDBL expenses

Directors' fees

Depreciation (Note-14)

Interest on loan and overdraft

Publicity and advertisement

Registration renewal fees

Profit for the year carried down to appropriation account

270,000

708,015

138,000

2,771,197

-

543,751

893,925

5,324,888

134,638,078

139,962,966

17

180,000

423,422

135,000

1,024,314

193,205

689,050

775,882

3,420,873

132,090,338

135,511,211

PROFIT AND LOSS ACCOUNT

PROFIT AND LOSS APPROPRIATION ACCOUNT

Notes 2012Taka

2011Taka

Transfer to reserve for exceptional losses

(10% of net premium)

Provision for income taxes

Issuance of bonus share

Cash dividend paid

Balance transferred to Balance Sheet

Earnings per share (2011: restated)

13,674,627

36,000,000

33,000,000

33,000,000

235,370,860

351,045,487

2.72

15,443,014

27,000,000

30,000,000

30,000,000

203,115,773

305,558,787

2.90

Notes 2012Taka

2011 Taka

Notes 1 to 31 form an integral part of these statement of accounts

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

Notes 2012Taka

2011 Taka

Interest, dividend and rents (not applicable to any particular fund or account)

Interest and dividend income

Share of profit of associate

Profit transferred from :

Fire revenue account

Marine revenue account

Motor revenue account

Miscellaneous revenue account

Gain on sale of investments in shares

Other income

60,390,136

47,268,747

6,453,157

14,133,038

9,704,815

1,052,463

31,343,473

678,772

281,838

139,962,966

15

9

16

42,521,287

44,033,387

190,494

13,792,587

9,060,668

4,012,561

27,056,310

21,530,293

369,934

135,511,211

FOR THE YEAR ENDED 31 DECEMBER 2012

FOR THE YEAR ENDED 31 DECEMBER 2012

Balance brought forward from last year

Deferred tax (Note-10)

Profit for the year brought down from profit and loss account

Transferred from general reserve

203,115,773

1,041,636

134,638,078

12,250,000

351,045,487

165,169,147

899,302

132,090,338

7,400,000

305,558,787

UNITED INSURANCE COMPANY LIMITED

35

Notes 2012 Taka

2011 Taka

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

36

Claims under policies less re-insurance :

Paid during the year

Total estimated liability in respect of outstanding claims at the end of the year whether due or intimated

Less : Outstanding at the end of previous year

Agency commission

Expenses of management

Profit transferred to profit and loss account

Balance of account at the end of the year as shown in the balance sheet:

Reserve for unexpired risk being:

40% premium income of the year except Marine Hull

100% premium income of the year on Marine Hull

13,583,951

18,801,652

32,385,603

8,040,780

24,344,823

35,408,395

98,212,000

31,343,473

54,354,520

859,968

55,214,488

244,523,179

14,334,071

8,040,780

22,374,851

9,252,386

13,122,465

49,566,060

94,866,732

27,056,311

60,712,126

2,649,822

63,361,948

247,973,516

CONSOLIDATED REVENUE ACCOUNT

All expenses of management wherever incurred whether directly or indirectly in respect of fire, marine, motor and miscellaneous insurance business transacted in Bangladesh have been fully debited in the respective revenue accounts as expenses in the ratio of gross premium income.

Amount in Taka2012 2011

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

UNITED INSURANCE COMPANY LIMITED

37

Balance of account at the beginning of the year :

Reserve for unexpired risk

Premium less re-insurance

Commission on re-insurance ceded

63,361,948

136,746,267

44,414,964

244,523,179

45,826,787

154,430,137

47,716,592

247,973,516

FOR THE YEAR ENDED 31 DECEMBER 2012

Amount in Taka2012 2011

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

38

Claims under policies less re-insurance:

Paid during the year

Total estimated liability in respect of outstanding claims at the end of the year whether due or intimated

Less : Outstanding at the end of previous year

Agency commission

Expenses of management

Profit/(Loss) transferred to profit and loss account

Balance of account at the end of the year as shown in the balance sheet :

Reserve for unexpired risk being40% premium income of the year

2,042,496

8,704,689

10,747,185

2,815,168

7,932,017

15,641,424

39,764,258

6,453, 157

11,759,124

81,549,980

1,187,808

2,815,168

4,002,976

1,626,852

2,376,124

26,251,078

42,925,690

190,494

21,220,449

92,963,835

FIRE INSURANCE REVENUE ACCOUNT

Amount in Taka2012 2011

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

UNITED INSURANCE COMPANY LIMITED

39

Balance of account at the beginning of the year :

Reserve for unexpired risk

Premium less re-insurance

Commission on re-insurance ceded

21,220,449

29,397,809

30,931,722

81,549,980

7,144,200

53,051,123

32,768,512

92,963,835

FOR THE YEAR ENDED 31 DECEMBER 2012

Amount in Taka2012 2011

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

40

Claims under policies less re-insurance:

Paid during the year

Total estimated liability in respect of outstanding claims at the end of the year whether due or intimated

Less : Outstanding at the end of previous year

Agency commission

Expenses of management

Profit transferred to profit and loss account

Balance of account at the end of the year as shown in the balance sheet:

Reserve for unexpired risk being

40 % Premium income of the year on Marine Cargo

100 % Premium income of the year on Marine Hull

5,546,224

6,980,277

12,526,501

2,383,684

10,142,817

11,495,631

30,900,989

14,133,038

25,518,144

859,968

26,378,112

93,050,587

3,398,658

2,383,684

5,782,342

1,977,776

3,804,566

10,683,615

26,670,423

13,792,587

18,392,474

2,649,822

21,042,296

75,993,487

MARINE INSURANCE REVENUE ACCOUNT

Amount in Taka2012 2011

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

UNITED INSURANCE COMPANY LIMITED

41

Balance of account at the beginning of the year:

Reserve for unexpired risk

Premium less re-insurance

Commission on re-insurance ceded

21,042,296

64,655,329

7,352,962

93,050,587

17,999,497

48,631,007

9,362,983

75,993,487

FOR THE YEAR ENDED 31 DECEMBER 2012

Amount in Taka2012 2011

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

UNITED INSURANCE COMPANY LIMITED

42

Claims under policies less re-insurance:

Paid during the year

Total estimated liability in respect of outstanding claims at the end of the year whether due or intimated

Less : Outstanding at the end of previous year

Agency commission

Expenses of management

Profit transferred to profit and loss account

Balance of account at the end of the year as shown in the balance sheet:

Reserve for unexpired risk being 40% Premium income of the year

5,264,899

2,681,194

7,946,093

2,182,225

5,763,868

4,755,737

12,829,534

9,704,815

13,104,414

46,158,367

7,039,548

2,182,225

9,221,773

4,113,051

5,108,722

6,785,963

11,261,222

9,060,668

13,397,333

45,613,908

MOTOR INSURANCE REVENUE ACCOUNT

Amount in Taka2012 2011

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

UNITED INSURANCE COMPANY LIMITED

43

Balance of account at the beginning of the year:

Reserve for unexpired risk

Premium less re-insurance

Commission on re-insurance ceded

13,397,333

32,761,034

-

46,158,367

12,120,575

33,493,333

-

45,613,908

FOR THE YEAR ENDED 31 DECEMBER 2012

Amount in Taka2012 2011

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

MISCELLANEOUS INSURANCE REVENUE ACCOUNT

UNITED INSURANCE COMPANY LIMITED

44

Claims under policies less re-insurance:

Paid during the year

Total estimated liability in respect of outstanding claims at the end of the year whether due or intimated

Less : Outstanding at the end of previous year

Agency commission

Expenses of management

Profit transferred to profit and loss account

Balance of account at the end of the year as shown in the balance sheet:

Reserve for unexpired risk being40% premium income of the year

2,708,057

659,703

3,367,760

1,534,707 1,833,053

5,845,404

14,009,398

4,012,562

7,701,870

33,402,286

730,332

435,492

1,165,824

659,703 506,121

3,515,603

14,717,220

1,052,463

3,972,838

23,764,245

Amount in Taka2012 2011

M. M. AlamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. Saiful IslamDirector

FOR THE YEAR ENDED 31 DECEMBER 2012

UNITED INSURANCE COMPANY LIMITED

45

Balance of account at the beginning of the year:

Reserve for unexpired risk

Premium less re-insurance

Commission on re-insurance ceded

7,701,870

9,932,095

6,130,280

23,764,245

8,562,515

19,254,674

5,585,097

33,402,286

Amount in Taka2012 2011

Syed Shahriyar AhsanManaging Director

M. J. Abedin & Co.Chartered Accountants

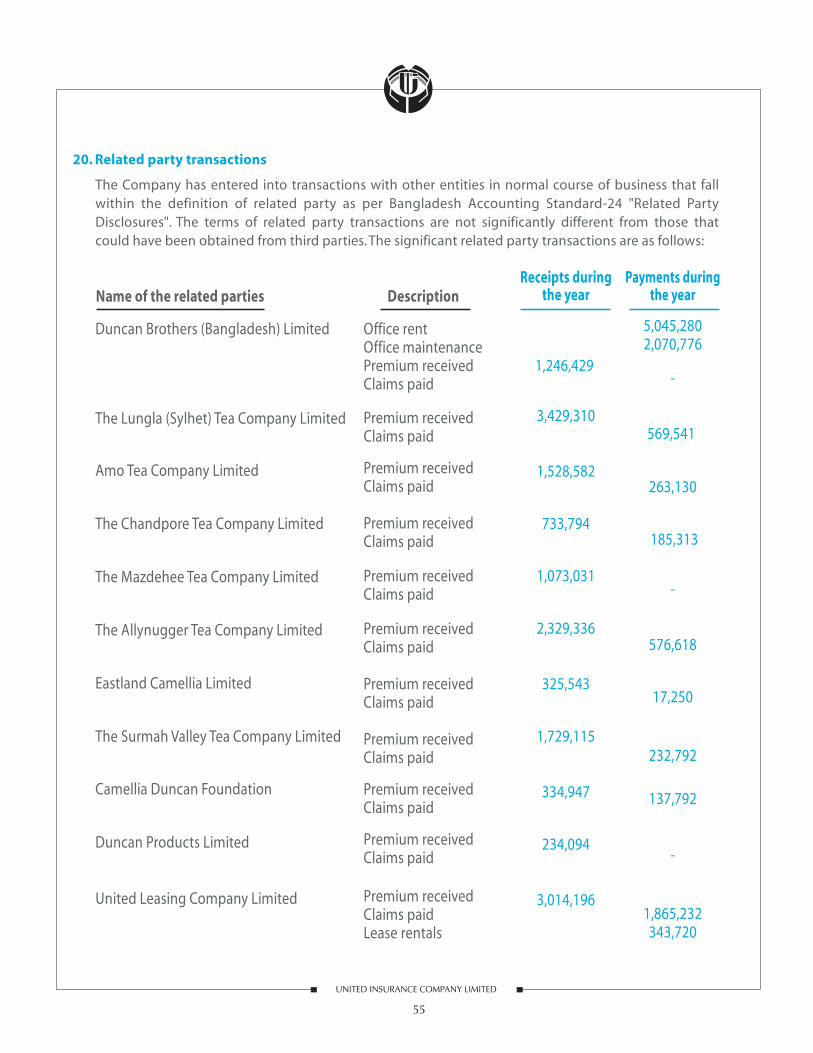

STATEMENT OF CHANGES IN SHAREHOLDERS EQUITYFor the year ended 31 December 2012

UNITED INSURANCE COMPANY LIMITED

46

Particulars

Balance at 1 January 2011

Issue of share capital (Bonus share)

Dividend paid

Transferred to/(from) general reserve

Deferred tax income

Profit after tax for the year 2011

Appropriation made during the year

Balance at 31 December 2011

Issue of share capital (Bonus share)

Dividend paid

Transferred to/(from) general reserve

Deferred tax income

Profit after tax for the year 2012

Appropriation made during the year

Balance at 31 December 2012

Share capital

300,000,000

30,000,000

-

-

-

-

330,000,000

33,000,000

-

-

-

-

363,000,000

Reserve for exceptional

losses

170,827,311

-

-

-

-

15,443,014

186,270,325

-

-

-

-

13,674,627

199,944,952

General reserve

90,000,000

-

-

(7,400,000)

- -

82,600,000

-

-

(12,250,000)

-

-

70,350,000

Profit & loss appropriation

165,169,147

(30,000,000)

(30,000,000)

7,400,000

899,302

105,090,338

(15,443,014)

203,115,773

(33,000,000)

(33,000,000)

12,250,000

1,041,636

98,638,078

(13,674,627)

235,370,860

Total equity

725,996,458

-

(30,000,000)

-

899,302

105,090,338

-

801,986,098

-

(33,000,000)

-

1,041,636

98,638,078

-

868,665,812

Amuont in Taka

M. Saiful IslamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. M. AlamDirector

Syed Shahriyar AhsanManaging Director

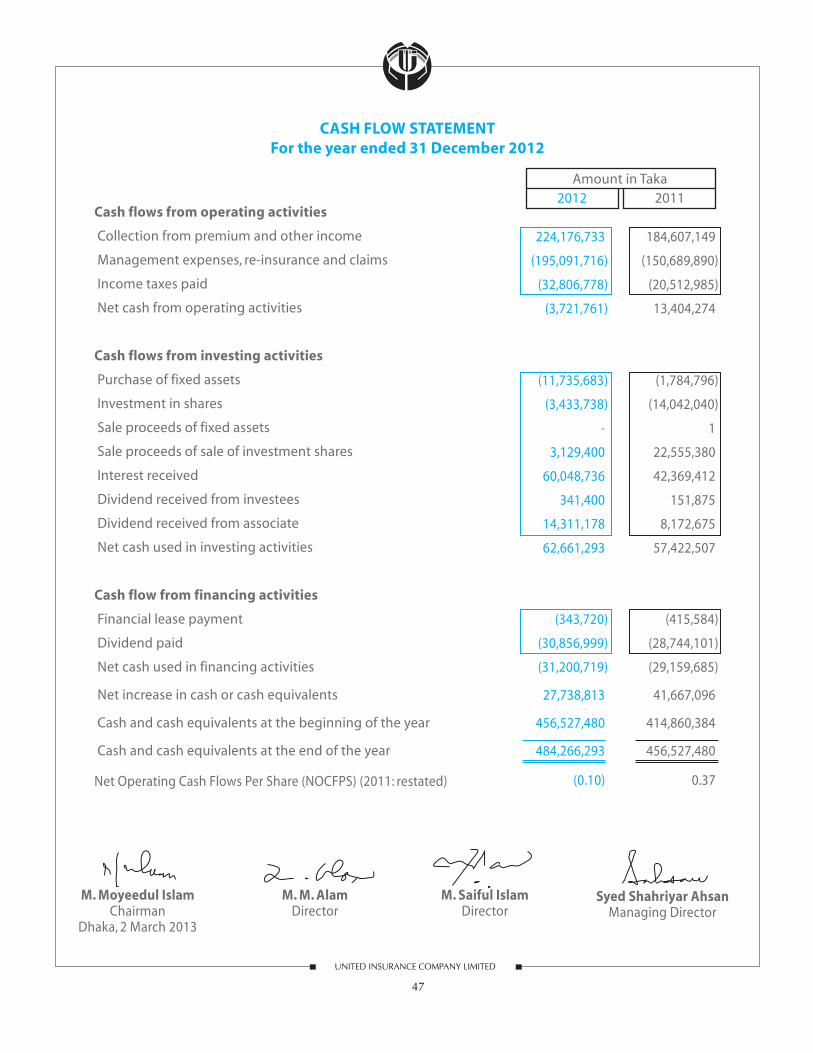

CASH FLOW STATEMENT For the year ended 31 December 2012

UNITED INSURANCE COMPANY LIMITED

47

Cash flows from operating activities

Collection from premium and other income

Management expenses, re-insurance and claims

Income taxes paid

Net cash from operating activities

Cash flows from investing activities

Purchase of fixed assets

Investment in shares

Sale proceeds of fixed assets

Sale proceeds of sale of investment shares

Interest received

Dividend received from investees

Dividend received from associate

Net cash used in investing activities

Cash flow from financing activities

Financial lease payment

Dividend paid

Net cash used in financing activities

Net increase in cash or cash equivalents

Cash and cash equivalents at the beginning of the year

Cash and cash equivalents at the end of the year

Net Operating Cash Flows Per Share (NOCFPS) (2011: restated)

224,176,733

(195,091,716)

(32,806,778)

(3,721,761)

(11,735,683)

(3,433,738)

-

3,129,400

60,048,736

341,400

14,311,178

62,661,293

(343,720)

(30,856,999)

(31,200,719)

27,738,813

456,527,480

484,266,293

(0.10)

184,607,149

(150,689,890)

(20,512,985)

13,404,274

(1,784,796)

(14,042,040)

1

22,555,380

42,369,412

151,875

8,172,675

57,422,507

(415,584)

(28,744,101)

(29,159,685)

41,667,096

414,860,384

456,527,480

0.37

Amount in Taka2012 2011

M. Saiful IslamDirector

M. Moyeedul IslamChairman

Dhaka, 2 March 2013

M. M. AlamDirector

Syed Shahriyar AhsanManaging Director

UNITED INSURANCE COMPANY LIMITED

48

NOTES TO THE ACCOUNTS For the year ended 31 December 2012

1. Background The Company was incorporated on 7 May 1985 and obtained the Certificate of Commencement of Business from the Registrar of Joint Stock Companies, Bangladesh with effect from 12 October 1985. However, the Certificate of Registration was obtained on 15 October 1985 from the Department of Insurance, Government of the People's Republic of Bangladesh. The Company was listed in Dhaka Stock Exchange Limited on 9 April 1990.

2. Basis of presenting accounts and significant accounting policies 2.1 Basis of presenting accounts

a) These accounts have been prepared under Generally Accepted Accounting Principles (GAAP) on historical cost convention.

b) The Balance Sheet has been prepared in accordance with the regulations contained in Part I of the First Schedule and as per Form "A" as set forth in Part II of that schedule and the Revenue Account of each class of non-life insurance business has been prepared in accordance with the regulations as contained in Part I of the Third Schedule and as per Form "F" as set forth in Part II of that Schedule of the Insurance Act 1938 as amended.

c) The Insurance Act, 2010 has been promulgated on 18 March 2010. The Insurance Development & Regulatory Authority Act, 2010 has also been promulgated on 18 March 2010. But necessary rules & regulations have not yet been gazateed by the Government for the application of the said Acts. As a result, the Balance Sheet, Revenue Accounts have been prepared in accordance with the provisions of the Insurance Act, 1938 and the Insurance Rules, 1958.

2.2 Significant accounting policies a) Public Sector Business

Company's share of public sector business is accounted for in the year in which the statements of accounts from the Sadharan Bima Corporation are received. As at 31 December 2012, statements of accounts for the period from 1 July 2011 to 30 June 2012 had been received from the Sadharan Bima Corporation and accordingly, the Company's share of public sector business for that period had been accounted for in the accompanying accounts. This practice is being followed consistently.

b) Property, plant and equipment These are stated at cost less accumulated depreciation. Fully depreciated assets are carried in the books at nominal value of Tk. 1 for the purpose of identification. Assets procured under lease finance have been accounted for following finance method in compliance with Bangladesh Accounting Standard 17 effective from 2005.

c) Depreciation on property, plant and equipment Depreciation on property, plant and equipment is charged on straight line method at rates varying from 10% to 20% depending on the estimated useful lives of the assets. Depreciation on newly acquired assets are charged for the full year irrespective of date of acquisition, while no depreciation is charged during the year in which assets are disposed of.

d) Basis of recognition of income in respect of premium deposit Amounts received against issuance of cover notes are recognised as income if the cover notes are converted into policies or after expiry of nine months following the issuance of cover notes in accordance with the Circular issued by the Chief Controller of Insurance.

e) Recognition of income from Associate The Company holds 20.64% in the equity of United Leasing Company Limited, an associate of the Company. Pursuant to provision of relevant accounting standard, the proportionate income of the associate company has been accounted for under equity method and recognised in the company's books of account. Accordingly, during the year under review, an amount of Tk. 44,033,387 has been recognised as income and reflected in the accompanying profit and loss account.

UNITED INSURANCE COMPANY LIMITED

49

f) Income tax Current Tax Provision for income tax has been made at 42.5% on the basis of Finance Act, 2012. Advance income tax including tax deducted at source (TDS) has been shown and appearing in the financial statements after deduction of provision for taxes. Deferred Tax Deferred tax is provided on temporary differences arising between the tax base values of assets and liabilities and their carrying amounts in the financial statements in accordance with BAS-12. Tax rate is used at 42.5% for determining deferred tax. Deferred tax assets are recognised on the carry forward of unabsorbed tax losses and other deductible temporary differences when it is probable that future taxable profit will be available against which the temporary differences can be utilised.

g) Retirement benefit scheme Gratuity: The Company operates an unfunded gratuity scheme, provision in respect of which, has been made in the accompanying accounts covering all of its eligible employees. Provident Fund: Under a defined contribution scheme, company operates provident fund managed by independent Board of Trustees for all permanent employees. The company's contributions to the scheme are charged to profit and loss account in the year in which they relate.

h) Expenses on agency commission are recognised on cash payment basis. 3. Valuation of assets

The value of all assets at 31 December 2012 as shown in the Balance Sheet and in the Classified Summary of Assets on Form 'AA' annexed have been reviewed and the said assets have been set forth in the Balance Sheet at amounts at their respective book values which in the aggregate do not exceed their aggregate market value.

4. Share capital Authorised: 50,000,000 ordinary shares of Tk 10 each Issued, subscribed and paid-up: 36,300,000 ordinary shares of Tk 10 each fully paid-up(For 2011 - 33,000,000 ordinary shares ofTk 10 each fully paid-up)

500,000,000 500,000,000

363,000,000 330,000,000

Holding of shares

Less than 500500 to 5,0005,001 to 10,00010,001 to 20,00020,001 to 30,00030,001 to 40,00040,001 to 50,00050,001 & above

Classification of shareholding position of the Company at 31 December 2012 was as follows:

3,111901

783856

95

414,239

3,369916

794115

79

374,473

Number of shareholders2012 2011

1.333.541.551.531.430.880.60

89.14100.00

1.594.001.681.641.090.721.24

88.04100.00

Percentage of total holdings2012 2011

2012 Taka

2011Taka

UNITED INSURANCE COMPANY LIMITED

50

8. Sundry creditors (including provision for expenses and taxes) Liabilities for management expenses Provision for gratuityAdvance received from policyholder against Open Marine Cover note VAT payable for December 2012 paid in January 2013 Provision for taxation - net of advance tax and TDS Others

3,546,955 23,050,850

2,424,656 2,639,009

21,385,18510,969,220 64,015,875

4,267,250 19,385,380 10,699,734

5,956,205 15,453,807

8,583,511 64,345,887

7. Amounts due to other persons or bodies carrying on insurance business

The following is the make-up of the balance due to Sadharan Bima Corporation on account of re-insurance arrangements and under co-insurance scheme for payment to other insurance companies.

(31,572,472) 41,875,025 10,302,553

(22,749,945) 29,287,384

6,537,439

Re-insurers (Receivable)Co-insurers

302,467 665,467 362,945

3,629,945 2,419,967

8,504,766 20,414,443 36,300,000