uli ylg peer-to-peer equity financings and...

TRANSCRIPT

ULI YLG Peer-To-Peer

Equity Financings and Structures

November 2011

Table of Contents ULI YLG Peer-To-Peer

2

C:\Documents and Settings\friedara\Local Settings\Temporary Internet Files\OLK9E4\Equity Overview 11 14 11.ppt\A2XP\15 NOV 2011\9:27 AM\2

Section 1 What Is Equity

Section 2 Fund Level Equity vs. Project Level Equity

Section 3 Joint Venture Equity Structures

ULI YLG Peer-To-Peer

Section 1

What Is Equity

3

Debt

Equity

WHAT IS EQUITY

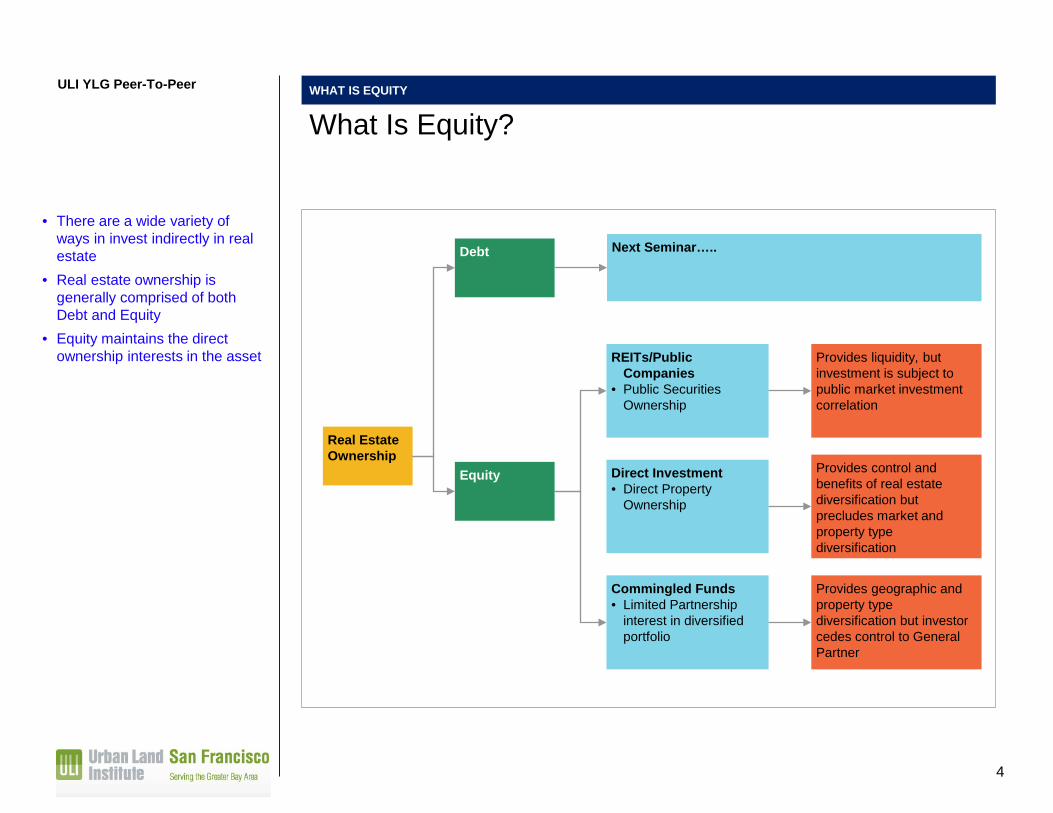

What Is Equity? ULI YLG Peer-To-Peer

4

Real Estate Ownership

REITs/Public Companies

• Public Securities Ownership

Provides liquidity, but investment is subject to public market investment correlation

Direct Investment • Direct Property

Ownership

Provides control and benefits of real estate diversification but precludes market and property type diversification

Commingled Funds • Limited Partnership

interest in diversified portfolio

Provides geographic and property type diversification but investor cedes control to General Partner

• There are a wide variety of ways in invest indirectly in real estate

• Real estate ownership is generally comprised of both Debt and Equity

• Equity maintains the direct ownership interests in the asset

Next Seminar…..

Securities

ULI YLG Peer-To-Peer WHAT IS EQUITY

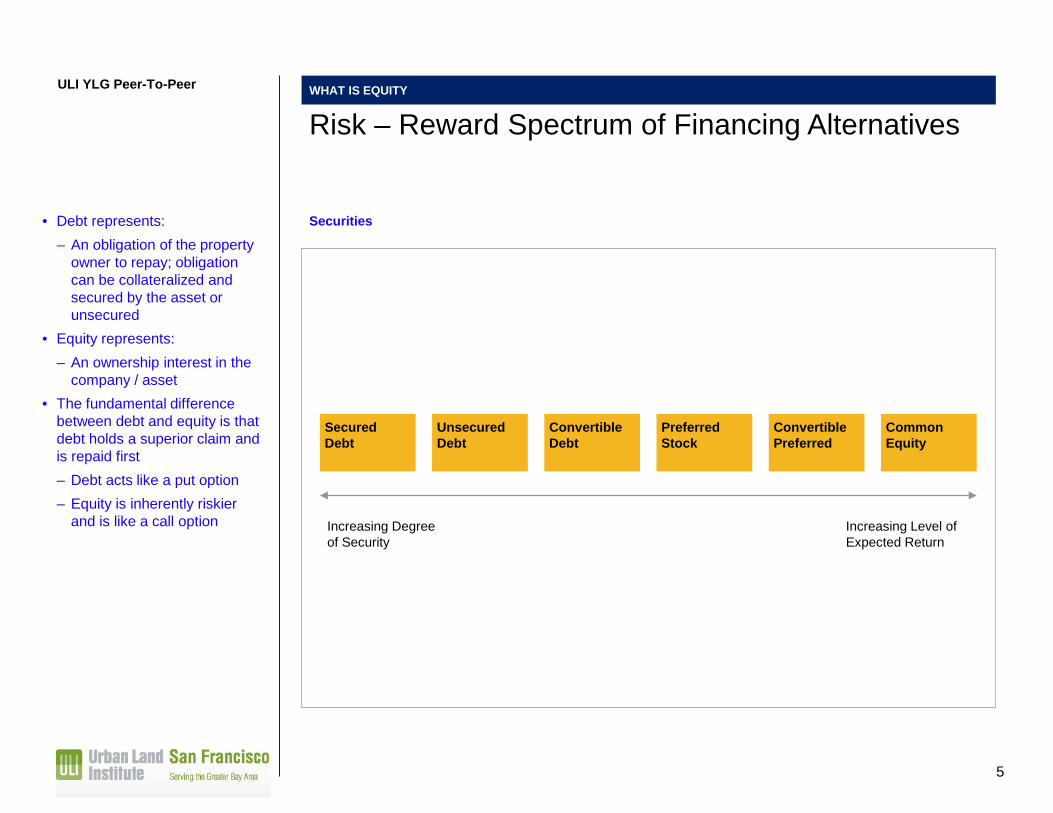

Risk – Reward Spectrum of Financing Alternatives

Secured Debt

Increasing Degree of Security

Increasing Level of Expected Return

Unsecured Debt

Convertible Debt

Preferred Stock

Convertible Preferred

Common Equity

5

• Debt represents: – An obligation of the property

owner to repay; obligation can be collateralized and secured by the asset or unsecured

• Equity represents: – An ownership interest in the

company / asset • The fundamental difference

between debt and equity is that debt holds a superior claim and is repaid first – Debt acts like a put option – Equity is inherently riskier

and is like a call option

ULI YLG Peer-To-Peer

Section 2

Fund Level Equity vs. Project Level Equity

6

ULI YLG Peer-To-Peer FUND LEVEL EQUITY VS. PROJECT LEVEL EQUITY

7

• Generally GP Capital • Advantage: Single Promote • Disadvantage: Local Expertise

Direct Investment

Institutional Investors Managing Member

Discretionary Real Estate Fund

Real Estate

Debt

90-95% of Fund Equity 5-10% of Fund Equity

Project Equity 25-45% of Capitalization

55-75% of Capitalization

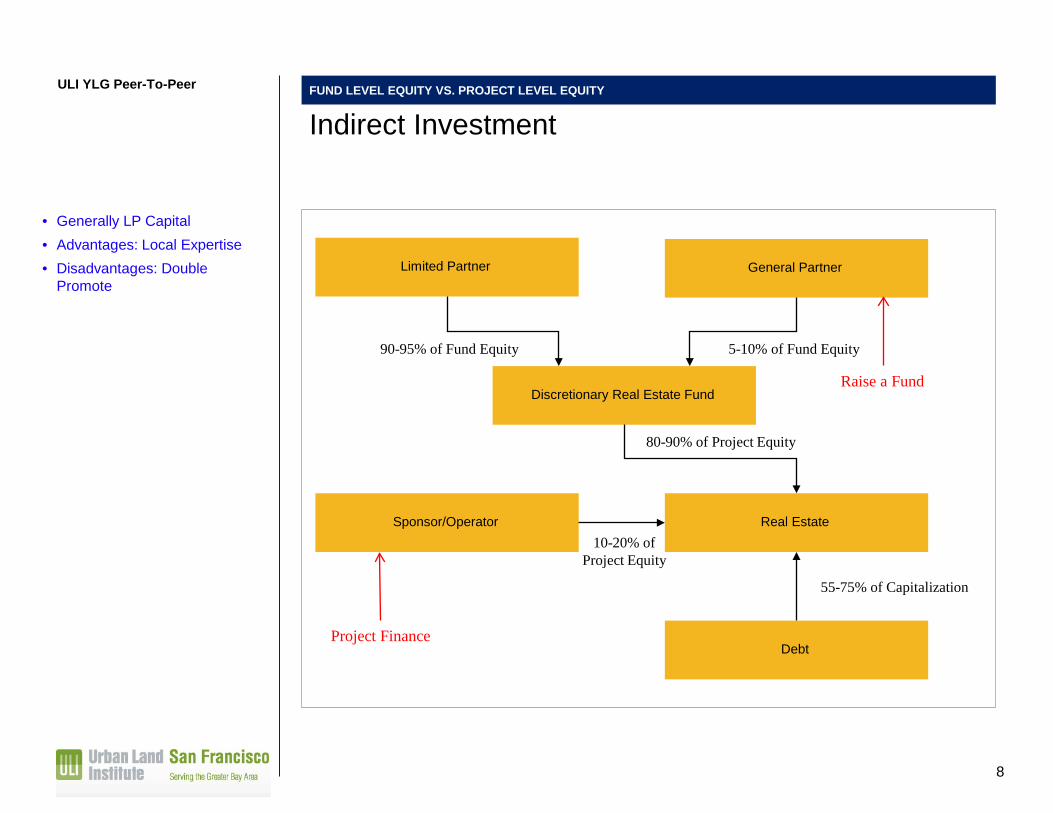

ULI YLG Peer-To-Peer FUND LEVEL EQUITY VS. PROJECT LEVEL EQUITY

8

• Generally LP Capital • Advantages: Local Expertise • Disadvantages: Double

Promote

Indirect Investment

Limited Partner General Partner

Discretionary Real Estate Fund

Real Estate

Debt

90-95% of Fund Equity 5-10% of Fund Equity

80-90% of Project Equity

55-75% of Capitalization

Sponsor/Operator 10-20% of

Project Equity

Project Finance

Raise a Fund

ULI YLG Peer-To-Peer FUND LEVEL EQUITY VS. PROJECT LEVEL EQUITY

9

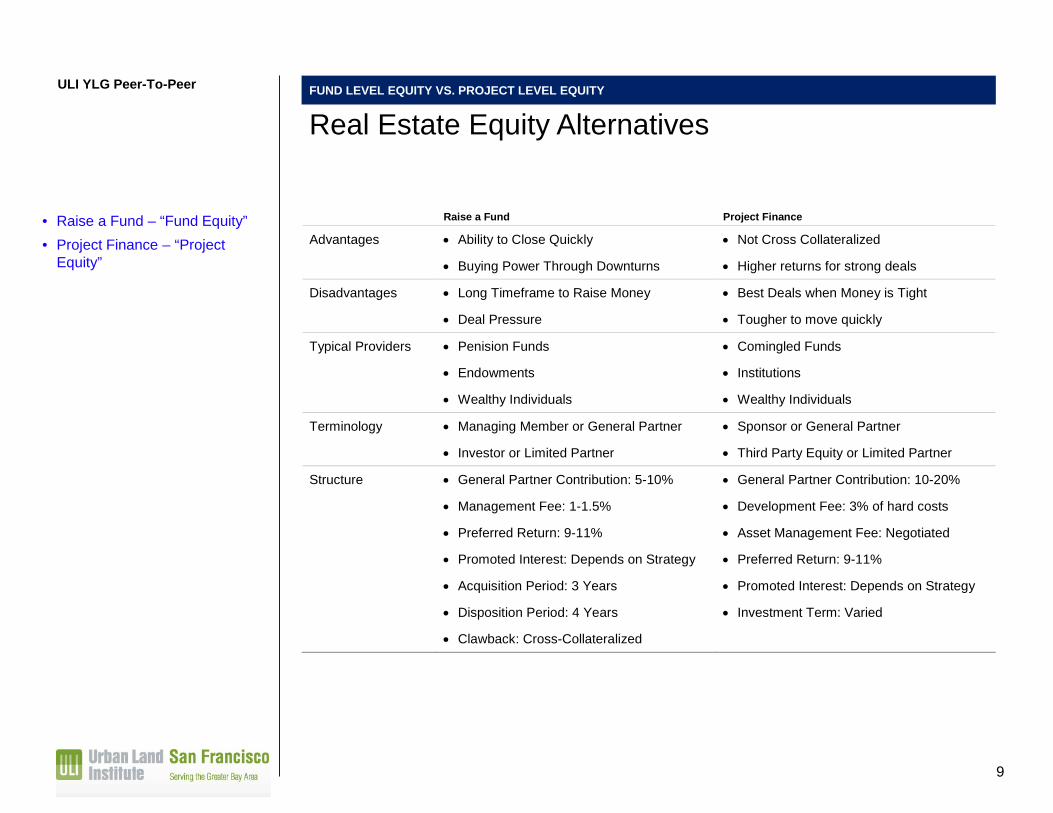

• Raise a Fund – “Fund Equity” • Project Finance – “Project

Equity”

Real Estate Equity Alternatives

Raise a Fund Project Finance

Advantages • Ability to Close Quickly

• Buying Power Through Downturns

• Not Cross Collateralized

• Higher returns for strong deals

Disadvantages • Long Timeframe to Raise Money

• Deal Pressure

• Best Deals when Money is Tight

• Tougher to move quickly

Typical Providers • Penision Funds

• Endowments

• Wealthy Individuals

• Comingled Funds

• Institutions

• Wealthy Individuals

Terminology • Managing Member or General Partner

• Investor or Limited Partner

• Sponsor or General Partner

• Third Party Equity or Limited Partner

Structure • General Partner Contribution: 5-10%

• Management Fee: 1-1.5%

• Preferred Return: 9-11%

• Promoted Interest: Depends on Strategy

• Acquisition Period: 3 Years

• Disposition Period: 4 Years

• Clawback: Cross-Collateralized

• General Partner Contribution: 10-20%

• Development Fee: 3% of hard costs

• Asset Management Fee: Negotiated

• Preferred Return: 9-11%

• Promoted Interest: Depends on Strategy

• Investment Term: Varied

ULI YLG Peer-To-Peer FUND LEVEL EQUITY VS. PROJECT LEVEL EQUITY

10

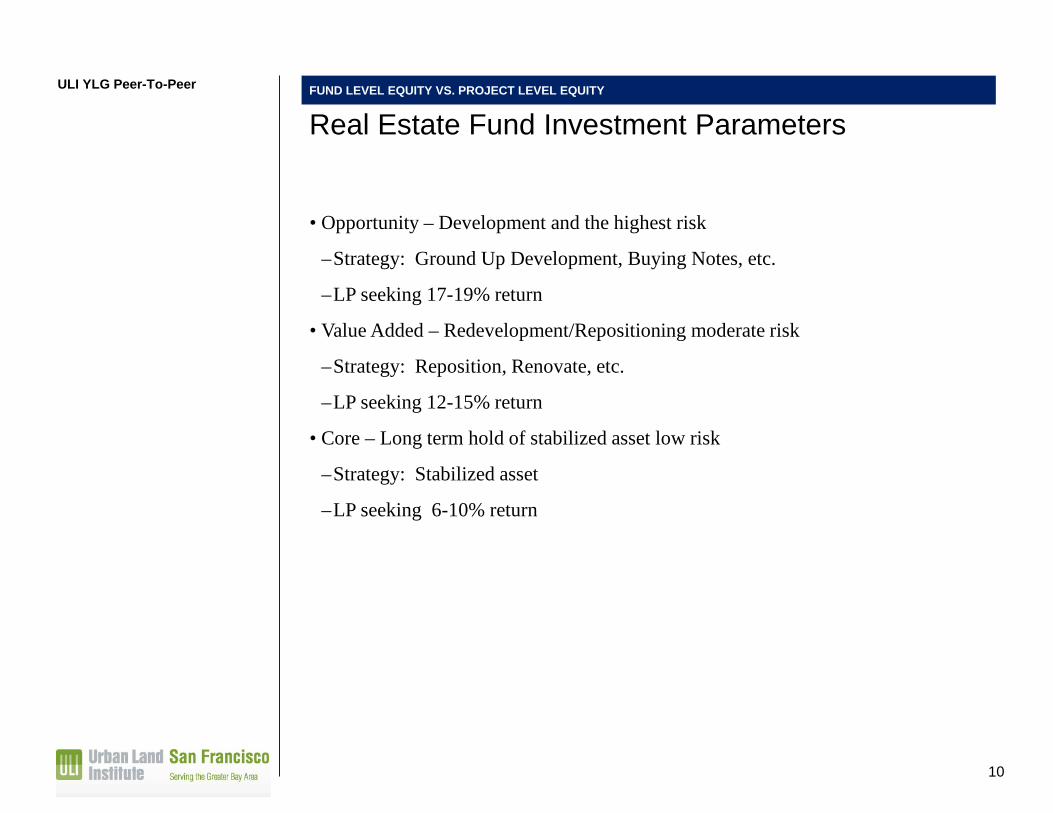

Real Estate Fund Investment Parameters

• Opportunity – Development and the highest risk

–Strategy: Ground Up Development, Buying Notes, etc.

–LP seeking 17-19% return

• Value Added – Redevelopment/Repositioning moderate risk

–Strategy: Reposition, Renovate, etc.

–LP seeking 12-15% return

• Core – Long term hold of stabilized asset low risk

–Strategy: Stabilized asset

–LP seeking 6-10% return

ULI YLG Peer-To-Peer

Section 3

Joint Venture Equity Structures

11

JOINT VENTURE EQUITY STRUCTURES

The Role of Capital Partners and Operating Partners Alignment of Interest

ULI YLG Peer-To-Peer

12

• Capital / Limited Partners

– Share the same investment philosophy as the sponsor

– Institutional Investors or High Net worth individuals

– Typically provide 80%+ of equity

– Typically do not sign recourse guarantees

– Approve all major decisions (Design changes and all capital transactions)

• Operating / General Partners

– National, Regional or Local Operators

– Manage day-to-day operations of the project

– Provide recourse guarantees to the lender

– Provide all reporting to capital partner

– If a project sells for an IRR greater than the preferred return, the sponsor gets a promoted interest.

JOINT VENTURE EQUITY STRUCTURES

Joint Venture Economics ULI YLG Peer-To-Peer

13

• Structure of hurdles and promotes can be dependent on the following:

– Asset type / inherent risk

– Leverage

– Operating experience of partner

– Market competitive dynamics

• Operating partners are paid through promoted interests (i.e, dilution of Capital Partner position) and management fees

– Sample JV terms:

– 95% / 5% deal to a 12% return for Capital Partner

– 75% / 25% deal to a 18% return for Capital Partner (Operator receives a 20% promoted interest on top of their 5% initial contribution)

• Hurdles are based on IRR of one cash flow stream (generally that of the Capital Partner)

– Short term investments may have an equity multiple hurdle as well

JOINT VENTURE EQUITY STRUCTURES

Capital Contributions / Distributions & Fees ULI YLG Peer-To-Peer

14

• Distributions

– Distributions come from Net Cash Flow and/or Capital Proceeds

– Net Cash Flow is cash flow from operations (less debt service & expenses)

– Capital Proceeds are from sales or refinancings

• Capital contributions

– Mandatory / Required Capital

– Capital for initial investment, necessary to make expenditures going forward, shortfalls on debt service / operations

• Fees

– Acquisition fees, asset management fees, guaranty fees

JOINT VENTURE EQUITY STRUCTURES

Joint Venture Structures ULI YLG Peer-To-Peer

15

• Management & Control is governed by an operating agreement on how to make major decisions

• Typical Major Decisions: Sales, financings & refinancings, leases, budgets / approvals of expenditures, additional capital contributions, litigation / bankruptcy, any matters outside ordinary course of business

– Generally for 90+% partners, most major decisions are unilateral (vs. unanimous)

• Other key management issues:

– Key Man provisions

– Duties of the operating member (general partner)

– Non-compete

• Breach of other key management issues can result in removal / forfeiture events (loss of promote, punitive dilution, etc)

JOINT VENTURE EQUITY STRUCTURES

Joint Venture Sample Term Sheet ULI YLG Peer-To-Peer

16

November 15, 2010 Mr. Apartment Developer ABC Development Group Any Street Any City, Any State 12345 RE: TERM SHEET – CLASS A APARTMENT COMMUNITY Dear Apartment Developer: The purpose of this letter is to evidence our mutual intent to form a limited partnership (the “Partnership”) between a ABC DEVELOPMENT GROUP entity (“ABC”) and an affiliate of PRIVATE EQUITY GROUP (“PE”) for the purpose of acquiring a 100 unit apartment community located in ANY CITY, USA. The parties hereto agree to negotiate in good faith and proceed with due diligence to convert this agreement (the “Term Sheet”) into an acceptable partnership agreement. Below we have outlined how our company would like to structure the investment.

Philosophy – ABC and PE will form a partnership, which will have as its purpose the acquisition, renovation, and sale of an 100-unit apartment community. PE will structure its position in the partnership as a Limited Partner. The partners agree that the goal of the Partnership is to maximize investment returns and sell the project as quickly as possible for the highest achievable price.

Capitalization - We assume a total project cost of approximately $20,000,000, and a loan for $15,000,000, leaving an equity requirement of $5,000,000. PE will contribute 90% or $4,500,000 of cash equity to the joint venture. ABC will contribute the remaining 10% of cash equity required or $500,000.

Preferred Returns - The PE and ABC cash equity contributions will be treated equally, and both will earn a preferred interest rate of 10% beginning with PE’s first equity contribution. The preferred returns will accrue and be payable from project cash flow. All preferred interest will compound annually.

Payments to ABC - ABC will be paid an acquisition fee of 1% of the Total Budget (exclusive of the fee itself). The acquisition fee shall be paid upon acquisition of the project.

17

PE Equity Fee – Simultaneously with the acquisition of the project, PRIVATE EQUITY GROUP shall be paid, an equity fee of 1% of total project cost exclusive of the fee itself. This amount shall not be treated as a return on or return of the PE capital, or as any other capital contribution to the Partnership.

Distribution Priority - Any ordinary cash flow remaining after payment of debt service on the Loan and establishment of a $300 per unit per year replacement reserve fund (“Net Cash Flow”) and any extraordinary cash flow proceeds from the sale, refinance or other liquidation of the property after full payment of the first mortgage loan (“Extraordinary Proceeds”) will be distributed as follows: First, repayment of loans or excess capital contributions made by partners, plus a return. Second, to the Partners, pari passu, in payment of each Partner’s accrued, but unpaid, 10% preferred return on initial cash investments. Third, to the Partners, pari passu, to return their initial cash investment. Fourth, to each Partner, as set forth in the Ownership Section below.

Ownership - After distributions are made in accordance with the distribution priority section above, all Net Cash Flow and all Extraordinary Proceeds will be distributed 75% to PE and 25% to ABC until PE has achieved an 18% IRR. Distributions above an 18% IRR and up to a 22% IRR shall be distributed 60% to PE and 40% to ABC. Returns above a 22% IRR shall be split 50% to PE and 50% to ABC.

IRR Calculation – The IRR is calculated using the “= IRR” function in a Microsoft Excel spreadsheet applied to a schedule of the actual monthly cash contributions and distributions for PE. All contributions and distributions are assumed to be made on the first of the month nearest the actual date made. The resulting monthly percentage calculated by the “= IRR” function is then multiplied by twelve to arrive at an annual percentage.

Major Decisions - PE will leave day-to-day management of the partnership to ABC. PE will retain the right to approve all major decisions, including those decisions that affect the design and specifications of the project, as well as those that involve any capital transactions, including a sale or refinance.

Defaulting and disabling Events - The partnership agreement will include definitions of “defaulting” and “disabling” events, such as failure to honor the guaranty of non-recourse carve-outs under the mortgage loan, misappropriation of Partnership funds, withholding distributable cash flow, bankruptcy of a partner or guarantor, the transfer of a partner's interest or withdrawal of a partner from the Partnership in violation of the partnership agreement.

18

Upon the occurrence of a defaulting event by ABC, all fees payable to ABC will cease, PE may elect to terminate any ABC affiliate contract, and PE will have the following rights listed below:

Key Personnel Default – If there is a change in control of the General Partner or if the persons in control of the General Partner cease having direct or indirect control of the General Partner or withdraw as members or partners of the General Partner, PE will have the right to replace ABC as the General Partner and to convert the interest of ABC to that of a limited partner without any decision making rights.

Bankruptcy – If ABC or any of the Guarantors files for bankruptcy, then PE will have the right to replace ABC as General Partner and to convert the interest of ABC to that of a silent limited partner without any decision making or voting rights.

Fraud and other “bad boy acts” - Misappropriation of Partnership funds, withholding distributable cash flow, violations of Partnership transfer restrictions, and other willful misconduct or gross negligence by the General Partner will result in a termination of the General Partner’s interest in the Partnership, and such right to terminate for “bad boy acts” will be secured by a pledge of the General Partner’s interest in the Partnership. ABC agrees that until this Term Sheet is terminated by mutual agreement of the parties hereto, ABC will not conduct negotiation with any other potential investors regarding the transaction described in this Term Sheet and will terminate any current negotiations with respect thereto; provided, however, that the foregoing covenant by ABC shall terminate and the provisions of this term sheet shall automatically expire in the event the parties have not executed a Partnership Agreement by December 15 , 2011. Please note that PE will require final Advisory Board Approval for this proposed joint venture. We understand ABC’s approval is subject to its own process as well. This Term Sheet is not intended to constitute a legally binding contract between the two parties and the terms contained are subject to the satisfactory completion of our due diligence including, but not limited to, receipt and approval of:

Engineering and environmental reports; A copy of the purchase contract; A copy of the partnership agreement and all related documents; Copies of all due diligence materials provided by the seller; A detailed marketing and leasing plan for the project; Plans and specifications including the community amenities, unit amenities, clubhouse interior design and FFE; Construction capabilities audit to be performed by PE’s Construction Management Team; All loan, bond, title, and other related documents.

19

We look forward to finalizing this proposal with you. Sincerely yours, PRIVATE EQUITY GROUP By:_________________________________ Date:__________________ Mr. Capital Partner Managing Director This Letter of Intent offer is accepted by Sponsor: ABC DEVELOPMENT GROUP By:__________________________________ Date:__________________

20

21