uk housing market prospects summer 2015

TRANSCRIPT

UK HOUSING MARKET PROSPECTS

SUMMER 2015

RESEARCH

www.realestate.bnpparibas.com3

UK HOUSING MARKET PROSPECTS

With expectations that commodity prices, in particular oil, will remain subdued until global economic growth returns to a more robust footing, domestic spending power is likely to improve further.

FIGURE 2: IMPROVING SPENDING POWER

With the improving economic backdrop, it was inevitable that the Governor of the Bank of England would put us on warning to expect a rise in the base rate. Certainly this will be a headline grabbing event when it happens, probably in Q1 2016, following what is likely to be just short of seven years of the 0.5% historic low. However, in economic terms the impact is likely to be relatively modest, initially at least. The upward interest rate trajectory is expected to be slow and mild, which will be important to ease the readjustment of the UK’s consumer driven economy.

There are early signs that readjustment may already be underway. Business investment, which has proved painfully slow to return following the recession, is showing growth, up 5.7% in Q1 compared to same period in 2014. This is significant, as is the small improvement in productivity, which may suggest businesses are reaching capacity and therefore will need to invest further in order to grow. The appetite for business expansion and development has the potential to generate jobs and have a positive impact on the UK’s balance of payments. The improved confidence lies predominately with the service sector, which while not immune to events outside the UK, has proved resilient over the last 12 months (CIPS/Markit).

The economy will face the inevitable international uncertainties over the coming year. It will also be forced to adapt to tighter public sector finances and a private sector preparing to absorb the new employment costs announced in the June budget, albeit with some time before implementation. As a package these factors will have a dampening impact on growth, but overall the UK GDP story is relatively positive for 2015 all things considered. The pace of economic growth will be in line or slightly ahead of that achieved in 2014, which is encouraging given the global backdrop.

In contrast to the international environment, domestic demand has sustained the UK economy through a challenging period. For one, further chapters in the Eurozone saga are still being penned. An unbalanced, domestic dominated demand is not ideal, but the tenacity of the UK consumer has underpinned spending and the housing market, and low and briefly negative inflation has combined with rising incomes and employment growth to provide households with real wage increases.

• THE HEADLINES

CONTACTS

Despite little respite from world events impacting the UK economy, the pace of economic growth revived during the second quarter to 0.7% following the pre-election lull in Q1. However, the composition of this growth is not ideal. Export demand from the rest of Europe remains muted as the region’s protracted return to growth is overshadowed further by ongoing difficulties in Greece. This has taken its toll on UK manufacturers in particular, with the strengthened pound compounding their troubles. Furthermore, we are seeing a mixed picture of economic health elsewhere in the world with China growing at its slowest rate for six years.

FIGURE 1: SUMMARY OF ECONOMIC FORECASTS

• ECONOMIC BACKDROP

Simon Durkin Head of Research [email protected] 020 7338 4020

Adrian Owen Head of Residential [email protected] 020 7338 4064

Sam Blake London [email protected] 020 7338 4130

Tim Cann Central Southern, South Coast & South West [email protected] 011 7984 8405

Steven Cooper Central London [email protected] 020 7338 4045

David Couch North and Midlands [email protected] 011 4263 9221

Julian Gaynor South East of England [email protected] 020 7338 4162

Nadir Khan-Juhoor Scotland [email protected] 013 1260 1118

RESEARCH

RESIDENTIAL

BNP Paribas Real Estate 5 Aldermanbury Square London EC2V 7BP Tel.: 020 7338 4000

• BNP Paribas Real Estate forecast average nominal house price growth of 7.6% pa over the next four years, edging ahead of the long term trend in real terms assisted by low inflation. Regional markets with a positive economic story will see improved growth as the recovery spreads beyond London and the South East.

• Sustained economic growth is driving improved real incomes and greater affordability in the housing market, but supply shortages have hindered activity. A strong development pipeline, while inadequate overall, will have a dampening impact on prices in those areas benefiting from improved supply.

• As the pace of off-plan sales eases in London we expect greater focus on owner-occupier buyers, but with potential implications for prices, development timing and funding. Across the capital as a whole, the continued expansion of the highly skilled workforce will intensify affordability pressures, as more high income employees chase housing stock.

• CONTENTS

THE HEADLINES .......................................................................................................................3

ECONOMIC BACKDROP ............................................................................................................3

HOUSING MARKET CONTEXT ................................................................................................4

MARKET OUTLOOK: HOUSE PRICE GROWTH, 2016-2019 ................................................6

EXPECTATIONS FOR LONDON ................................................................................................6

2012 2013 2014 2015 2016 2017 2018GDP GROWTH1 0.7 1.7 2.8 3.0 2.5 2.4 2.4INFLATION

CPI 2.1 1.9 1.6 0.6 1.6 1.7 2.0RPIX 3.2 3.1 2.4 1.6 2.4 2.5 2.7

UNEMPLOYMENT (MILLIONS)ANNUAL AV2 1.6 1.4 1.0 0.8 0.7 0.7 0.64TH QTR 1.6 1.3 0.9 0.7 0.7 0.7 0.6

EXCHANGE RATE3 83.0 81.6 87.1 90.7 90.8 90.7 90.33 MONTH INTEREST RATE 0.9 0.6 0.6 0.6 1.0 1.6 2.15 YEAR INTEREST RATE 0.9 1.3 1.8 1.8 2.2 2.5 2.5CURRENT BALANCE (£BN) -53.2 -65.9 -84.2 -77.8 -78.2 -78.8 -79.5PSBR (£BN) 110.6 95.2 88.6 84.0 79.6 58.7 39.1

1 Expenditure estimate at factor cost2 U.K. unemployed excluding school leavers (new basis)3 Sterling effective exchange rate, Bank of England Index (2005 = 100)

Source: ONS (historic); Liverpool Macroeconomic Research (forecast)

Source: ONS

Note: Average Earnings – y/y % change in monthly average weekly pay

www.realestate.bnpparibas.com5

UK HOUSING MARKET PROSPECTS

Source: BNP Paribas Real Estate

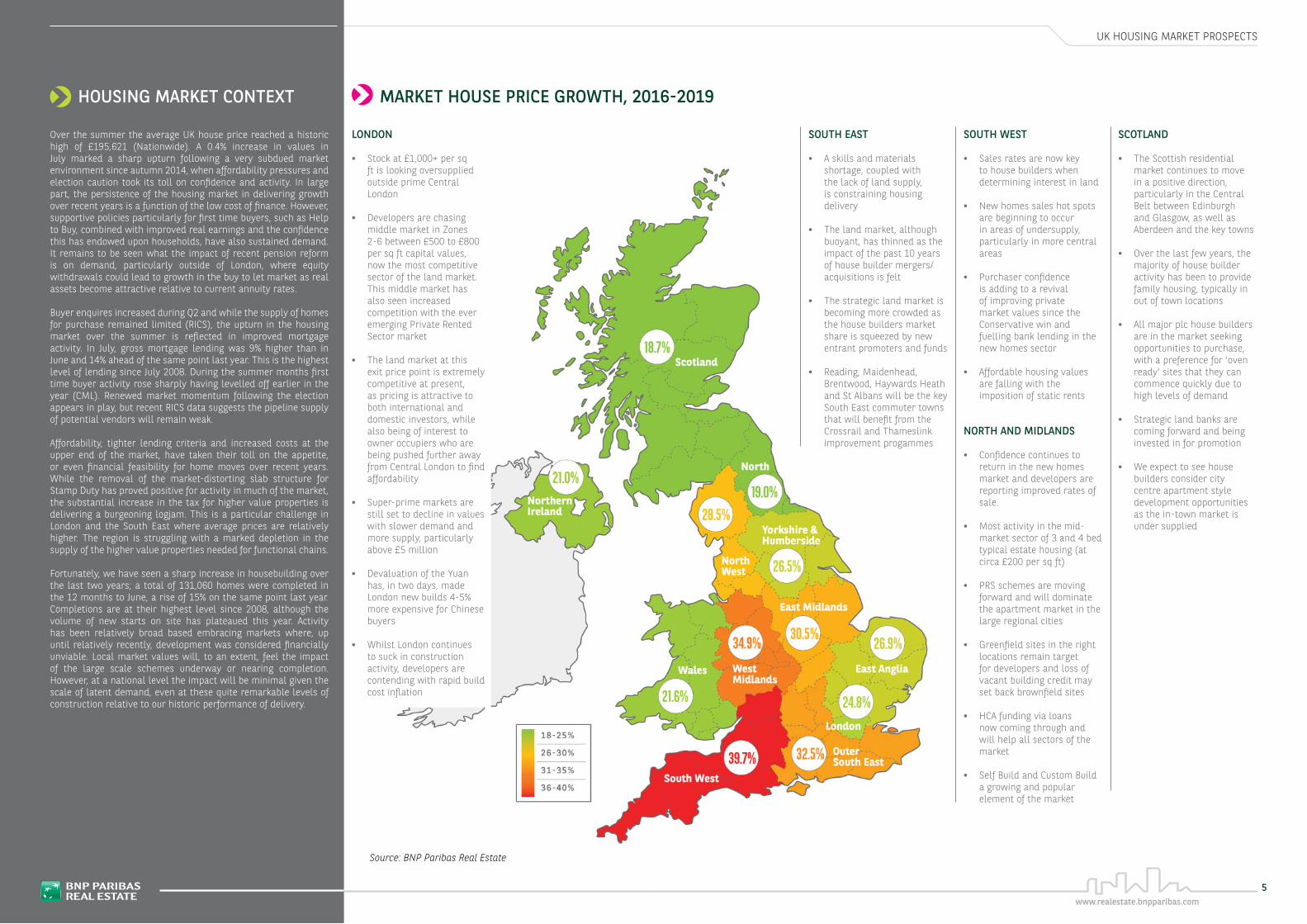

Over the summer the average UK house price reached a historic high of £195,621 (Nationwide). A 0.4% increase in values in July marked a sharp upturn following a very subdued market environment since autumn 2014, when affordability pressures and election caution took its toll on confidence and activity. In large part, the persistence of the housing market in delivering growth over recent years is a function of the low cost of finance. However, supportive policies particularly for first time buyers, such as Help to Buy, combined with improved real earnings and the confidence this has endowed upon households, have also sustained demand. It remains to be seen what the impact of recent pension reform is on demand, particularly outside of London, where equity withdrawals could lead to growth in the buy to let market as real assets become attractive relative to current annuity rates.

Buyer enquires increased during Q2 and while the supply of homes for purchase remained limited (RICS), the upturn in the housing market over the summer is reflected in improved mortgage activity. In July, gross mortgage lending was 9% higher than in June and 14% ahead of the same point last year. This is the highest level of lending since July 2008. During the summer months first time buyer activity rose sharply having levelled off earlier in the year (CML). Renewed market momentum following the election appears in play, but recent RICS data suggests the pipeline supply of potential vendors will remain weak.

Affordability, tighter lending criteria and increased costs at the upper end of the market, have taken their toll on the appetite, or even financial feasibility for home moves over recent years. While the removal of the market-distorting slab structure for Stamp Duty has proved positive for activity in much of the market, the substantial increase in the tax for higher value properties is delivering a burgeoning logjam. This is a particular challenge in London and the South East where average prices are relatively higher. The region is struggling with a marked depletion in the supply of the higher value properties needed for functional chains.

Fortunately, we have seen a sharp increase in housebuilding over the last two years; a total of 131,060 homes were completed in the 12 months to June, a rise of 15% on the same point last year. Completions are at their highest level since 2008, although the volume of new starts on site has plateaued this year. Activity has been relatively broad based embracing markets where, up until relatively recently, development was considered financially unviable. Local market values will, to an extent, feel the impact of the large scale schemes underway or nearing completion. However, at a national level the impact will be minimal given the scale of latent demand, even at these quite remarkable levels of construction relative to our historic performance of delivery.

• HOUSING MARKET CONTEXT • MARKET HOUSE PRICE GROWTH, 2016-2019

LONDON

• Stock at £1,000+ per sq ft is looking oversupplied outside prime Central London

• Developers are chasing middle market in Zones 2-6 between £500 to £800 per sq ft capital values, now the most competitive sector of the land market. This middle market has also seen increased competition with the ever emerging Private Rented Sector market

• The land market at this exit price point is extremely competitive at present, as pricing is attractive to both international and domestic investors, while also being of interest to owner occupiers who are being pushed further away from Central London to find affordability

• Super-prime markets are still set to decline in values with slower demand and more supply, particularly above £5 million

• Devaluation of the Yuan has, in two days, made London new builds 4-5% more expensive for Chinese buyers

• Whilst London continues to suck in construction activity, developers are contending with rapid build cost inflation

SOUTH EAST

• A skills and materials shortage, coupled with the lack of land supply, is constraining housing delivery

• The land market, although buoyant, has thinned as the impact of the past 10 years of house builder mergers/acquisitions is felt

• The strategic land market is becoming more crowded as the house builders market share is squeezed by new entrant promoters and funds

• Reading, Maidenhead, Brentwood, Haywards Heath and St Albans will be the key South East commuter towns that will benefit from the Crossrail and Thameslink improvement progammes

SOUTH WEST

• Sales rates are now key to house builders when determining interest in land

• New homes sales hot spots are beginning to occur in areas of undersupply, particularly in more central areas

• Purchaser confidence is adding to a revival of improving private market values since the Conservative win and fuelling bank lending in the new homes sector

• Affordable housing values are falling with the imposition of static rents

NORTH AND MIDLANDS

• Confidence continues to return in the new homes market and developers are reporting improved rates of sale.

• Most activity in the mid-market sector of 3 and 4 bed typical estate housing (at circa £200 per sq ft)

• PRS schemes are moving forward and will dominate the apartment market in the large regional cities

• Greenfield sites in the right locations remain target for developers and loss of vacant building credit may set back brownfield sites

• HCA funding via loans now coming through and will help all sectors of the market

• Self Build and Custom Build a growing and popular element of the market

SCOTLAND

• The Scottish residential market continues to move in a positive direction, particularly in the Central Belt between Edinburgh and Glasgow, as well as Aberdeen and the key towns

• Over the last few years, the majority of house builder activity has been to provide family housing, typically in out of town locations

• All major plc house builders are in the market seeking opportunities to purchase, with a preference for ‘oven ready’ sites that they can commence quickly due to high levels of demand

• Strategic land banks are coming forward and being invested in for promotion

• We expect to see house builders consider city centre apartment style development opportunities as the in-town market is under supplied

UK HOUSING MARKET PROSPECTS

www.realestate.bnpparibas.com7

www.realestate.bnpparibas.com7

www.realestate.bnpparibas.com7

UK HOUSING MARKET PROSPECTS

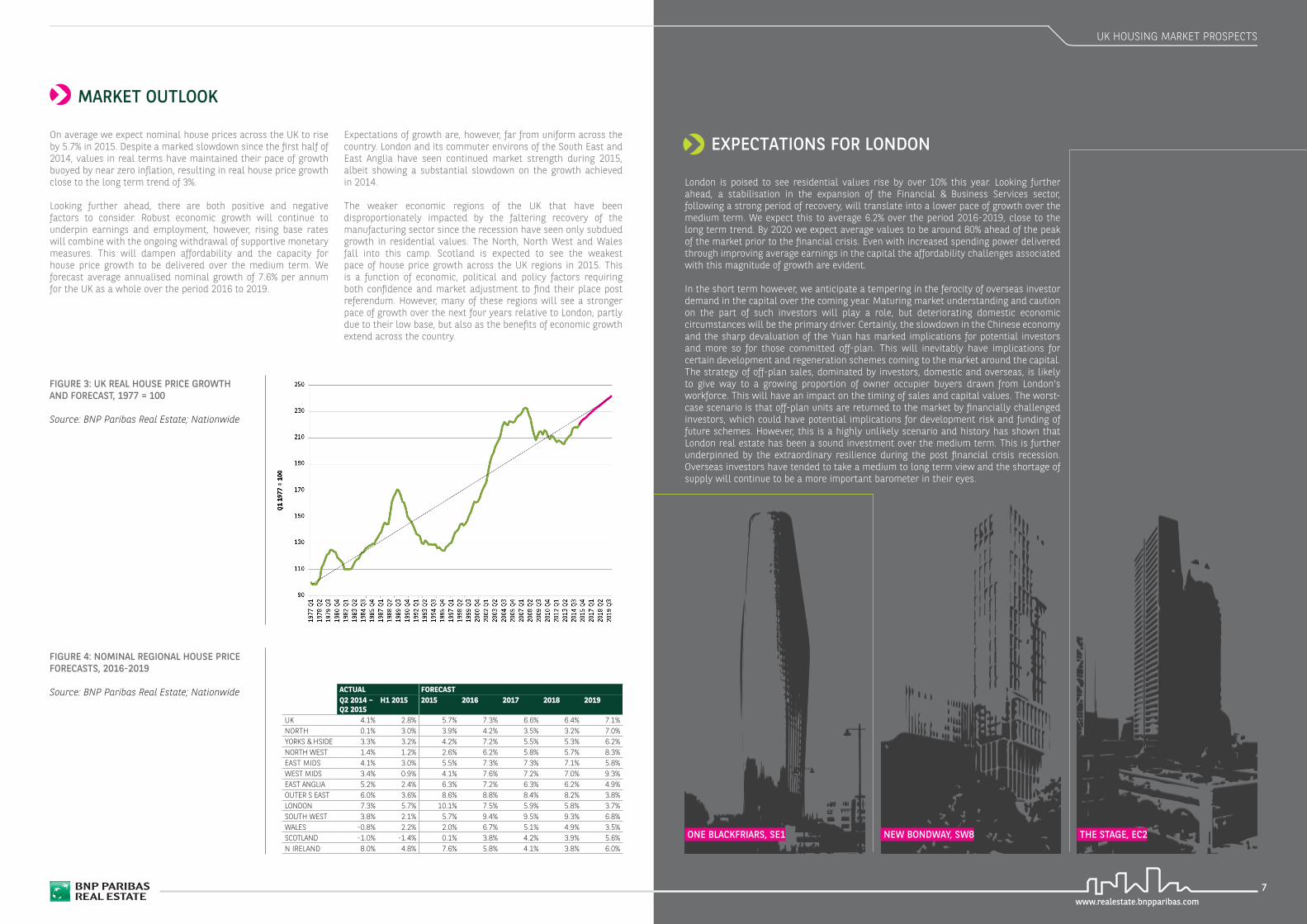

On average we expect nominal house prices across the UK to rise by 5.7% in 2015. Despite a marked slowdown since the first half of 2014, values in real terms have maintained their pace of growth buoyed by near zero inflation, resulting in real house price growth close to the long term trend of 3%.

Looking further ahead, there are both positive and negative factors to consider. Robust economic growth will continue to underpin earnings and employment, however, rising base rates will combine with the ongoing withdrawal of supportive monetary measures. This will dampen affordability and the capacity for house price growth to be delivered over the medium term. We forecast average annualised nominal growth of 7.6% per annum for the UK as a whole over the period 2016 to 2019.

• MARKET OUTLOOK

• EXPECTATIONS FOR LONDON

London is poised to see residential values rise by over 10% this year. Looking further ahead, a stabilisation in the expansion of the Financial & Business Services sector, following a strong period of recovery, will translate into a lower pace of growth over the medium term. We expect this to average 6.2% over the period 2016-2019, close to the long term trend. By 2020 we expect average values to be around 80% ahead of the peak of the market prior to the financial crisis. Even with increased spending power delivered through improving average earnings in the capital the affordability challenges associated with this magnitude of growth are evident.

In the short term however, we anticipate a tempering in the ferocity of overseas investor demand in the capital over the coming year. Maturing market understanding and caution on the part of such investors will play a role, but deteriorating domestic economic circumstances will be the primary driver. Certainly, the slowdown in the Chinese economy and the sharp devaluation of the Yuan has marked implications for potential investors and more so for those committed off-plan. This will inevitably have implications for certain development and regeneration schemes coming to the market around the capital. The strategy of off-plan sales, dominated by investors, domestic and overseas, is likely to give way to a growing proportion of owner occupier buyers drawn from London’s workforce. This will have an impact on the timing of sales and capital values. The worst-case scenario is that off-plan units are returned to the market by financially challenged investors, which could have potential implications for development risk and funding of future schemes. However, this is a highly unlikely scenario and history has shown that London real estate has been a sound investment over the medium term. This is further underpinned by the extraordinary resilience during the post financial crisis recession. Overseas investors have tended to take a medium to long term view and the shortage of supply will continue to be a more important barometer in their eyes.

ACTUAL FORECASTQ2 2014 – Q2 2015

H1 2015 2015 2016 2017 2018 2019

UK 4.1% 2.8% 5.7% 7.3% 6.6% 6.4% 7.1%NORTH 0.1% 3.0% 3.9% 4.2% 3.5% 3.2% 7.0%YORKS & HSIDE 3.3% 3.2% 4.2% 7.2% 5.5% 5.3% 6.2%NORTH WEST 1.4% 1.2% 2.6% 6.2% 5.8% 5.7% 8.3%EAST MIDS 4.1% 3.0% 5.5% 7.3% 7.3% 7.1% 5.8%WEST MIDS 3.4% 0.9% 4.1% 7.6% 7.2% 7.0% 9.3%EAST ANGLIA 5.2% 2.4% 6.3% 7.2% 6.3% 6.2% 4.9%OUTER S EAST 6.0% 3.6% 8.6% 8.8% 8.4% 8.2% 3.8%LONDON 7.3% 5.7% 10.1% 7.5% 5.9% 5.8% 3.7%SOUTH WEST 3.8% 2.1% 5.7% 9.4% 9.5% 9.3% 6.8%WALES -0.8% 2.2% 2.0% 6.7% 5.1% 4.9% 3.5%SCOTLAND -1.0% -1.4% 0.1% 3.8% 4.2% 3.9% 5.6%N IRELAND 8.0% 4.8% 7.6% 5.8% 4.1% 3.8% 6.0%

FIGURE 4: NOMINAL REGIONAL HOUSE PRICE FORECASTS, 2016-2019

FIGURE 3: UK REAL HOUSE PRICE GROWTH AND FORECAST, 1977 = 100

Source: BNP Paribas Real Estate; Nationwide

Expectations of growth are, however, far from uniform across the country. London and its commuter environs of the South East and East Anglia have seen continued market strength during 2015, albeit showing a substantial slowdown on the growth achieved in 2014.

The weaker economic regions of the UK that have been disproportionately impacted by the faltering recovery of the manufacturing sector since the recession have seen only subdued growth in residential values. The North, North West and Wales fall into this camp. Scotland is expected to see the weakest pace of house price growth across the UK regions in 2015. This is a function of economic, political and policy factors requiring both confidence and market adjustment to find their place post referendum. However, many of these regions will see a stronger pace of growth over the next four years relative to London, partly due to their low base, but also as the benefits of economic growth extend across the country.

Source: BNP Paribas Real Estate; Nationwide

ONE BLACKFRIARS, SE1 NEW BONDWAY, SW8 THE STAGE, EC2

BNP

Pari

bas

Real

Est

ate:

Sim

plifi

ed jo

int s

tock

com

pany

wit

h ca

pita

l of €

329

,196

,608

€ -

692

012

180

RCS

Nan

terr

e -

Code

NAF

411

0BCE

iden

tific

atio

n nu

mbe

r FR

666

920

121

80

- H

eadq

uart

ers:

167

, Qua

i de

la B

atai

lle

de S

talin

grad

- 9

2867

Issy

Les

Mou

linea

ux C

edex

BN

P Pa

riba

s Re

al E

stat

e is

par

t of t

he B

NP

Pari

bas

Bank

ing

Gro

up

ABU DHABIAl Bateen Area Plot n° 144, W-11 New Al Bateen Municipality Street n° 32 P.O. Box 2742 Abu Dhabi Tel.: +971 44 248 277 Fax: +971 44 257 817

BELGIUMBoulevard Louis Schmidtlaan 2 B3 1040 Brussels Tel.: +32 2 290 59 59 Fax: +32 2 290 59 69

CZECH REPUBLICPobřežní 3 186 00 Prague 8 Tel.: +420 224 835 000 Fax: +420 222 323 723

DUBAIEmaar Square Building n° 1, 7th Floor P.O. Box 7233, Dubaï Tel.: +971 44 248 277 Fax: +971 44 257 817

FRANCE Headquarters 167, Quai de la Bataille de Stalingrad 92867 Issy-les-Moulineaux Tel.: +33 1 55 65 20 04 Fax: +33 1 55 65 20 00

GERMANYGoetheplatz 4 60311 Frankfurt Tel.: +49 69 2 98 99 0 Fax: +49 69 2 92 91 4

HONG KONG63 /F Two international finance Center - 8 Finance Street Hong Kong Tel.: +852 2909 2806 Fax: +852 2865 2523

HUNGARY Alkotás u. 53. H-1123 Budapest, Tel.: +36 1 487 5501 Fax: +36 1 487 5542

IRELAND20 Merrion Road, Dublin 4 Tel.: +353 1 66 11 233 Fax: +353 1 67 89 981

ITALYVia Carlo Bo, 11 20143 Milan Tel.: +39 (0)2 58 33 141 Fax: +39 (0)2 3706 9209

JERSEY 3 Floor, Dialogue House 2 - 6 Anley Street St Helier, Jersey JE4 8RD Tel.: +44 (0)1 534 629 001 Fax: +44 (0)1 534 629 011

LUXEMBOURGAxento Building Avenue J.F. Kennedy 44 1855 Luxembourg Tel.: +352 34 94 84 Fax: +352 34 94 73 Investment Management Tel.: +352 26 26 06 06 Fax: +352 26 26 06 06

NETHERLANDS JJ Viottastraat 33 1071 JP Amsterdam Tel.: +31 20 305 97 20

POLAND Al. Jana Pawła II 25 00-854 Warsaw Tel.: +48 22 653 44 00 Fax: +48 22 653 44 01

ROMANIAUnion International Center 11 Ion Campineanu Street 6th floor, 1st district Bucharest 010031 Tel.: +40 21 312 7000 Fax: +40 21 312 7001

SINGAPORE10 Collyer Quay, #31-01 Ocean Financial Centre Singapore 049315 Tel.: +65 62 10 12 88 DID: +65 62 10 31 99

SPAINMaría de Molina, 54 28006 Madrid Tel.: +34 91 454 96 00 Fax: +34 91 454 97 65

UNITED KINGDOM5 Aldermanbury Square London EC2V 7BP Tel.: +44 20 7338 4000 Fax: +44 20 7430 2628

MAIN LOCATIONS ALLIANCES

AUSTRIA

CYPRUS

ESTONIA

FINLAND

GREECE

INDIA

LATVIA

LITHUANIA

NORTHERN IRELAND

NORWAY

RUSSIA

SERBIA

SWEDEN

SWITZERLAND

TURKEY

UKRAINE

USA

Hong Kong

U.A.E

USA

FRANCE Headquarters 167, Quai de la Bataille de Stalingrad 92867 Issy-les-Moulineaux Tel.: +33 1 55 65 20 04 Fax: +33 1 55 65 20 00

BELGIUMBoulevard Louis Schmidtlaan 2 B3 1040 Brussels Tel.: +32 2 290 59 59 Fax: +32 2 290 59 69

CZECH REPUBLICPobřežní 3 186 00 Prague 8 Tel.: +420 224 835 000 Fax: +420 222 323 723

GERMANYGoetheplatz 4 60311 Frankfurt Tel.: +49 69 2 98 99 0 Fax: +49 69 2 92 91 4

HONG KONG25 /F Three Exchange Square, 8 Connaught Place, Central, Hong Kong Tel.: +852 2909 2806 Fax: +852 2865 2523

HUNGARY Alkotás u. 53. H-1123 Budapest, Tel.: +36 1 487 5501 Fax: +36 1 487 5542

IRELAND20 Merrion Road, Dublin 4 Tel.: +353 1 66 11 233 Fax: +353 1 67 89 981

ITALYVia Carlo Bo, 11 20143 Milan Tel.: +39 02 58 33 141 Fax: +39 02 3706 9209

JERSEY 3 Floor, Dialogue House 2 - 6 Anley Street St Helier, Jersey JE4 8RD Tel.: +44 (0)1 534 629 001 Fax: +44 (0)1 534 629 011

LUXEMBOURGAxento Building Avenue J.F. Kennedy 44 1855 Luxembourg Tel.: +352 34 94 84 Fax: +352 34 94 73 Investment Management Tel.: +352 26 26 06 06 Fax: +352 26 26 06 26

NETHERLANDS Antonio Vivaldistraat 54 1083 HP Amsterdam Tel.: +31 20 305 97 20

POLAND Al. Jana Pawła II 25 00-854 Warsaw Tel.: +48 22 653 44 00 Fax: +48 22 653 44 01

ROMANIAUnion International Center 11 Ion Campineanu Street 6th floor, 1st district Bucharest 010031 Tel.: +40 21 312 7000 Fax: +40 21 312 7001

SPAINC/ Génova 17 28004 Madrid Tel.: +34 91 454 96 00 Fax: +34 91 454 97 65

U.A.EABOU DHABIAl Bateen Area Plot n° 144, W-11 New Al Bateen Municipality Street n° 32 P.O. Box 2742 Abu Dhabi Tel.: +971 44 248 277 Fax: +971 44 257 817

DUBAIEmaar Square Building n° 1, 7th Floor P.O. Box 7233, Dubaï Tel.: +971 44 248 277 Fax: +971 44 257 817

UNITED KINGDOM5 Aldermanbury Square London EC2V 8HR Tel.: +44 20 7338 4000 Fax: +44 20 7430 2628

MAIN LOCATIONS ALLIANCES

ALGERIA *

AUSTRIA

CYPRUS

ESTONIA

FINLAND

GREECE

HUNGARY ***

IVORY COAST *

LATVIA

LITHUANIA

MOROCCO

NORTHERN IRELAND

NORWAY

RUSSIA

SERBIA

SLOVAKIA **

SWEDEN

SWITZERLAND

TUNISIA *

TURKEY

UKRAINE

USA

PLEASE CONTACT

Alliances Florence HesseTel.: +33 (0)1 47 59 17 [email protected]

Research Christophe Pineau Tel.: +33 (0)1 47 59 24 77 [email protected]

* Coverage via our alliance in Morocco ** Coverage via our alliance in Austria*** Covering Transaction, Valuation & Consulting

Hong Kong

U.A.E

USA

BNP

Pari

bas

Real

Est

ate:

Sim

plifi

ed jo

int s

tock

com

pany

wit

h ca

pita

l of €

383

.071

.696

- 6

92 0

12 1

80 R

CS N

ante

rre

- Co

de N

AF 7

010

ZCE

iden

tific

atio

n nu

mbe

r FR

666

920

121

80

- H

eadq

uart

ers:

167

, Qua

i de

la B

atai

lle

de S

talin

grad

- 9

2867

Issy

Les

Mou

linea

ux C

edex

BN

P Pa

riba

s Re

al E

stat

e is

par

t of t

he B

NP

Pari

bas

Bank

ing

Gro

up

PLEASE CONTACT

Research SImon Durkin Tel.: +44 20 7338 4020 [email protected]

Front cover image credit: www.webbaviation.co.uk