uk fiscal policy before the crisis

TRANSCRIPT

© Institute for Fiscal Studies

UK fiscal policy before the crisisPaul Johnson

20/09/13

Overview

• Currently in middle of biggest fiscal consolidation since the war– Borrowing hit 11% of GDP– Debt heading from 40% to 85% of GDP– Consolidation of 9% of GDP

© Institute for Fiscal Studies

Overview

• Currently in middle of biggest fiscal consolidation since the war• UK entered recession with a large structural deficit by

international standards– But smaller than in 1996

• Period from 2001-08 saw historically big spending increases– Accompanied by some tax increases

• Fiscal rules were only partially effective• As in the 1980s the Chancellor and Treasury assumed growth

would continue unabated– Spending decisions made on that basis

• Hard to see how we could have entered recession in a qualitatively different fiscal situation

© Institute for Fiscal Studies

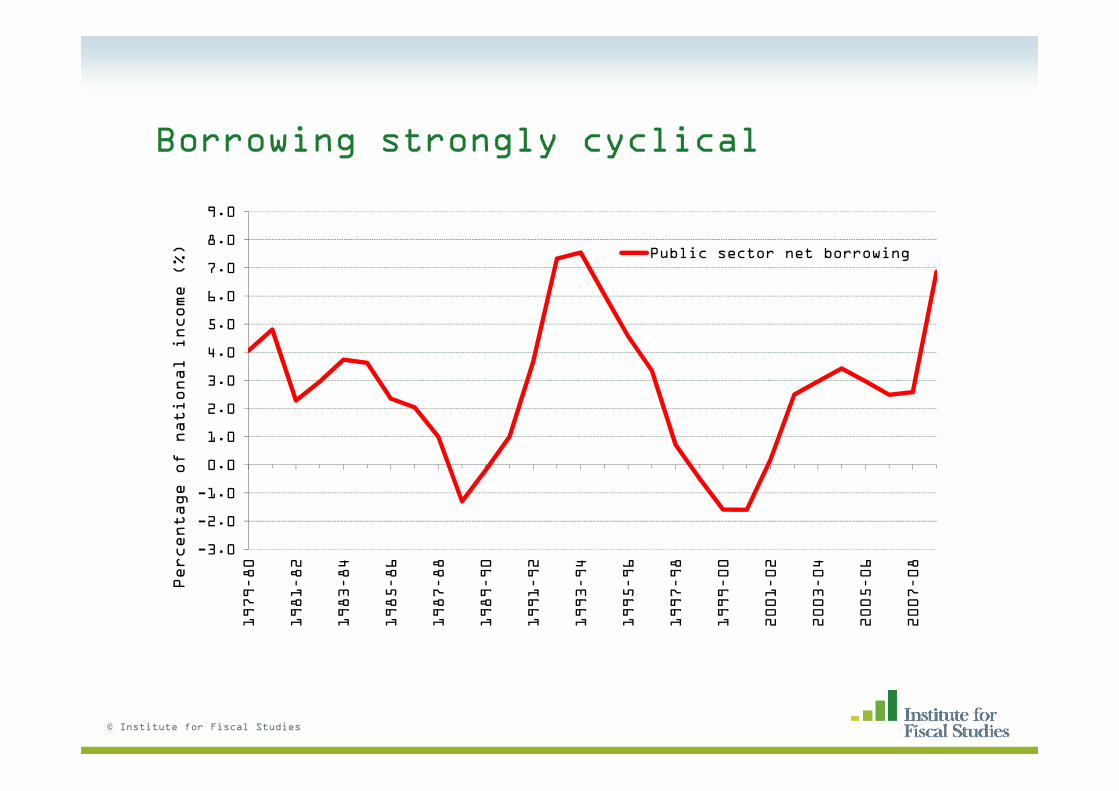

Borrowing strongly cyclical (of course)

• Rose dramatically in the early 1990s• Falling rapidly from mid 1990s• Then rising from early 2000s

© Institute for Fiscal Studies

Borrowing strongly cyclical

© Institute for Fiscal Studies

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1979–80

1981–82

1983–84

1985–86

1987–88

1989–90

1991–92

1993–94

1995–96

1997–98

1999–00

2001–02

2003–04

2005–06

2007–08

Percentage of national income (%) Public sector net borrowing

Borrowing strongly cyclical

© Institute for Fiscal Studies

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1979–80

1981–82

1983–84

1985–86

1987–88

1989–90

1991–92

1993–94

1995–96

1997–98

1999–00

2001–02

2003–04

2005–06

2007–08

Percentage of national income (%)

Public sector net borrowing

Current budget deficit

Borrowing strongly cyclical

© Institute for Fiscal Studies

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1979–80

1981–82

1983–84

1985–86

1987–88

1989–90

1991–92

1993–94

1995–96

1997–98

1999–00

2001–02

2003–04

2005–06

2007–08

Percentage of national income (%)

Public sector net borrowing

Current budget deficit

Cyclically-adjusted netborrowing

Borrowing strongly cyclical (of course)

• Rose dramatically in the early 1990s

• Falling rapidly from mid 1990s

• Then rising from early 2000s

• The period from 2001 saw significant spending increases

– But also tax increases

• With debt rising

© Institute for Fiscal Studies

With debt following a similar pattern

© Institute for Fiscal Studies

0

5

10

15

20

25

30

35

40

45

501979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

Percentage of national income (%)

Public sector net debt

Persistent under-estimation of change in borrowing

© Institute for Fiscal Studies

-4

-2

0

2

4

6

8

10

1978–79

1980–81

1982–83

1984–85

1986–87

1988–89

1990–91

1992–93

1994–95

1996–97

1998–99

2000–01

2002–03

2004–05

2006–07

Percentage of national income

Financial year

What was state of public finances pre crisis?

• PSNB 2.4% of GDP

• Current budget deficit 0.4%

• Structural borrowing then estimated at 2.6% of GDP

– OBR now believe it was at 3.7% of national income

• These measures were all lower than in 1996/97

• But don’t look so healthy on international comparisons

© Institute for Fiscal Studies

© Institute for Fiscal Studies

% of national income

Rankings: OECD member

countries

Pre-crisis position

(2007)

Spending

General government

spending

43.7%

Place in OECD 12th/30 highest spending

Revenues

Tax and other revenues 41.0%

Place in OECD 18th/30 highest revenues

Borrowing

General government net

borrowing

2.7%

Place in OECD 6th/30 highest borrowing

Structural borrowing 4.5%

Place in OECD 3rd/26 highest borrowing

© Institute for Fiscal Studies

% of national income

Rankings: OECD member

countries

Pre-crisis position

(2007)

Change, 1997 to

2007

(% points)

Spending

General government

spending

43.7% +3.3

Place in OECD 12th/30 highest spending 2nd/30 largest

increase

Revenues

Tax and other revenues 41.0% +2.8

Place in OECD 18th/30 highest revenues 6th/30 largest

increase

Borrowing

General government net

borrowing

2.7% +0.5

Place in OECD 6th/30 highest borrowing 4th/30 largest

increase

Structural borrowing 4.5% +2.3

Place in OECD 3rd/26 highest borrowing 6th/26 largest

increase

Fiscal rules

• Were generally unclear pre-1997

– A broad aspiration to meet budget balance in the medium term

• From 1997:

– Golden Rule: current budget balance over the cycle

– Sustainable Investment Rule: keep net debt below 40% of GDP

• For the Treasury to determine whether rules were being met

© Institute for Fiscal Studies

Sustainable Investment Rule

• In 2008 Budget Treasury was (still) expecting 2% growth

– the central forecast was for debt to hit 39.8% of GDP in 2010

• At least appeared to drive the structure of many private finance deals

– Network Rail structure allowed £18 billion of debt not to count against the rule

• “Sustainability” appeared unrelated to future commitments

© Institute for Fiscal Studies

With debt following a similar pattern

© Institute for Fiscal Studies

0

5

10

15

20

25

30

35

40

45

501979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

Percentage of national income (%)

Public sector net debt

Sustainable debt rule

Golden Rule

• Effectively backward looking for period after 2001

– Using up “headroom” created by early surpluses

• Required dating of the cycle

– Dating which conveniently changed in 2005 when it looked like rule might be breached

– Start of cycle redated from 1999 to 1997

© Institute for Fiscal Studies

Golden Rule

• Effectively backward looking for period after 2001

– Using up “headroom” created by early surpluses

• Required dating of the cycle

– Dating which conveniently changed in 2005 when it looked like rule might be breached

– Start of cycle redated from 1999 to 1997

• Leading my predecessor Robert Chote to suggest that it was “not so much a cycle as a stretch limo”

© Institute for Fiscal Studies

What future for fiscal rules?

• Current fiscal mandate looks better than the golden rule

– Forward looking

• And independent OBR acts as arbiter

• But depends on judgments about what is “structural” as well as a five year forecast

• And with the secondary debt rule not turning out to be binding there is no anchor

• Clearly credible fiscal policy is about much more than fiscal rules

© Institute for Fiscal Studies

Spending

• Overall tightly controlled for decade after the 1990 recession

• Rising consistently after 2001

– Contrasting with volatile year on year changes previously

• Different patterns for public services and social security

© Institute for Fiscal Studies

Annual change in public service spending

© Institute for Fiscal Studies

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Real percentage increase (%)

Thatcher Blair

Major Brown

Cameron Output gap

Annual change in social security spending

© Institute for Fiscal Studies

-6.00

-4.00

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Real percentage increase (%)

Thatcher Blair

Major Brown

Coalition Claimant count rate

Spending

• Overall tightly controlled for decade after the 1990 recession

• Rising consistently after 2001

– Contrasting with volatile year on year changes previously

• Different patterns for public services and social security

• Was adequate caution built in?

• Is the process of three year spending reviews adequate?

• Are inefficient cycles avoidable?

© Institute for Fiscal Studies

The Grand Old Duke of York

© Institute for Fiscal Studies

4.000

4.200

4.400

4.600

4.800

5.000

5.200

5.400

5.600

5.800

1999Q1

2000Q1

2001Q1

2002Q1

2003Q1

2004Q1

2005Q1

2006Q1

2007Q1

2008Q1

2009Q1

2010Q1

2011Q1

2012Q1

2013Q1

2014Q1

2015Q1

2016Q1

2017Q1

2018Q1

General government employment (million)

General government employment

Forecast general government employment

Spending cuts

• Substantial cuts in spending from 2010 will only serve to return spending as a share of GDP to its 2004 level by 2018

– But with a very different pattern of spending

• Annually managed expenditure (including debt interest) continues to rise in real terms

• Public service spending is due to fall by nearly 20% in real terms

– By a third in “unprotected” areas

© Institute for Fiscal Studies

Composition of spending has changed

• Partly driven by demographics

– Number of pensioner rose by about 1.2% a year from 1980

• With a particular increase in the share of health spending

• Also driven by increased spending on working age welfare

– Despite falls in claimant count over much of the period

• Continual move towards a welfare state

– Maintained since 2008

© Institute for Fiscal Studies

Annual real spending growth

-1

0

1

2

3

4

5

6

7

8

1979-88 1989-99 2000-07

health

other publicservices

pensionerbenefits

other benefits

© Institute for Fiscal Studies

Changing composition of spending

1980-81 2017-180%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

other benefits

pensionerbenefits

health

other publicservices

© Institute for Fiscal Studies

Taxes

• Overall revenues respond quickly to economic activity

– So appear less cyclical than spending

© Institute for Fiscal Studies

Tax revenues over time

© Institute for Fiscal Studies

25

30

35

40

45

50

1978-79

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Percentage of national income

Current receipts

Forecast current receipts

Net taxes and National Insurance contributions

Forecast net taxes and National Insurance contributions

Taxes

• Overall revenues respond quickly to economic activity

– So appear less cyclical than spending

• Considerable reforms over the period

• Some, like big cuts in income tax rates in in 1980s stuck

– Even if they had to be paid for eventually by raising other taxes

• 1990s consolidation considerably more focussed on tax increases than is this one

© Institute for Fiscal Studies

Annual increases in net taxes and NICs

© Institute for Fiscal Studies

-6

-4

-2

0

2

4

6

8

-10

-5

0

5

10

15

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

2017-18

Real GDP growth (%)

Real percentage increase (%)

Thatcher Blair

Major Brown

Coalition Real GDP growth

Ratio of earnings to GDP growth

Tax policy

• Heavily influenced by the electoral cycle

– Big increases announced immediately after each election

• 1992 pre election Budget was a giveaway

– 1993 post election Budget a huge takewaway.

© Institute for Fiscal Studies

Taxes increase after elections

© Institute for Fiscal Studies

-5.3-6.7

-9.4-17.9

-9.42.43.6

-6.125.3

17.4-0.8

-8.51.3

8.15.7

-3.5-1.1-0.6-1.3

-5.20.0

12.00.90.70.40.30.60.7

3.71.12.6

0.31.3

3.12.2

5.34.9

1.36.9

-0.20.30.0

-0.70.1

-30 -20 -10 0 10 20 30

Spring 1985 BudgetSpring 1986 BudgetSpring 1987 BudgetSpring 1988 BudgetSpring 1989 BudgetSpring 1990 BudgetSpring 1991 BudgetSpring 1992 BudgetSpring 1993 BudgetAutumn 1993 BudgetAutumn 1994 BudgetAutumn 1995 BudgetAutumn 1996 BudgetSummer 1997 BudgetSpring 1998 BudgetSpring 1999 Budget

Autumn 1999 PBRSpring 2000 Budget

Autumn 2000 PBRSpring 2001 Budget

Autumn 2001 PBRSpring 2002 Budget

Autumn 2002 PBRSpring 2003 Budget

Autumn 2003 PBRSpring 2004 Budget

Autumn 2004 PBRSpring 2005 Budget

Autumn 2005 PBRSpring 2006 Budget

Autumn 2006 PBRSpring 2007 Budget

Autumn 2007 PBRSpring 2008 Budget

Autumn 2008 PBRSpring 2009 Budget

Autumn 2009 PBRSpring 2010 BudgetJune 2010 BudgetAutumn 2010 AS

Spring 2011 BudgetAutumn 2011 AS

Spring 2012 BudgetAutumn 2012 AS

£ billion (2012–13 terms)

Tax policy

• Heavily influenced by the electoral cycle

– Big increases announced immediately after each election

• 1992 pre election Budget was a giveaway

– 1993 post election Budget a huge takewaway.

• Norman Lamont:

– 1992 Budget “was not a very good Budget. But it did help us to win the 1992 election

– 1993 Budget: "helped to lose the 1997 election for the Conservatives, but it was definitely my best budget”

© Institute for Fiscal Studies

Revenue composition

• Not changed as much as spending composition

– Despite dramatic changes in rates

© Institute for Fiscal Studies

Changing composition of tax revenues

© Institute for Fiscal Studies

32.4%25.7% 27.6% 28.6%

17.5%

17.3%18.3%

19.5%

8.5%15.6%

18.5% 15.6%

17.3%13.4%

14.8%10.2%

6.1% 10.6%

6.7%

7.8%

1.0% 1.3%0.6%

1.5%2.1%2.7%

1.7%4.5%

15.2% 13.3% 11.8% 12.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1978-79 1989-90 1993-94 2007-08

Percentage of total net taxes and NICs

Other

Capital taxes

North sea taxes

Onshore CT

Excise duties

VAT

NICs

Income tax

Revenue composition

• Not changed as much as spending composition

– Despite dramatic changes in rates

• In part reflecting big increases in taxable incomes

– Especially towards the top of the distribution

– Dependence on richest income tax payers has grown dramatically

• Little in the way of consistent reform

– Savings/pensions

– CGT

– Corporate tax

– VAT

• Failure to implement reform (unquantifiably) costly© Institute for Fiscal Studies

Two specific taxes

• 1980s were cushioned by massive revenues from the North Sea

– Collapse of which made the fiscal problems of 1990s much worse

© Institute for Fiscal Studies

North Sea Oil Revenues (%GDP)

© Institute for Fiscal Studies

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1978-79

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

Percentage of national income (%)

Realised receipts

Two specific taxes

• 1980s were cushioned by massive revenues from the North Sea

– Collapse of which made the fiscal problems of 1990s much worse

• Onshore corporation tax is highly cyclical

– Unlike other taxes fell significantly in nominal terms after 2008

– And takes a while to recover

© Institute for Fiscal Studies

Onshore Corporation Tax revenues (%GDP)

© Institute for Fiscal Studies

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.51978-79

1979-80

1980-81

1981-82

1982-83

1983-84

1984-85

1985-86

1986-87

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

2015-16

2016-17

Percentage of national income (%)

Realised receipts

Conclusions

• Fiscal policy pre-crisis cannot be described as reckless

– There were tax increases as well as spending increases

– We could not have avoided a substantial tightening

• But in both 1980s and 2000s excessive optimism (at least ex post) seems to have been built in

• Spending review processes take inadequate account of long term effects

– Long term sustainability more generally plays too peripheral a role

• Pre crisis fiscal rules were inadequate

– And arguably gamed by the government that introduced them

• Too little focus on both structure and long term sustainability of the tax system

© Institute for Fiscal Studies