tuesday 29 september 2015 global real estate trends and

TRANSCRIPT

© Copyright 2015 by K&L Gates LLP. All rights reserved.

Steven Cox, Of Counsel, K&L GatesSabina Kalyan, Global Chief Economist, CBRE Global InvestorsPeter Hobbs, Managing Director, Real Estate Research, MSCIMike Phillips, Editor, EuroProperty MagazineKristina Baurschmidt, Partner, K&L Gates Berlin

Global Real Estate Trends and Opportunities for 2015/2016

Tuesday 29th September 2015

CONFIDENTIAL AND PROPRIETARY

THE EUROPEAN REAL ESTATE OUTLOOK

SEPTEMBER 2015

Presented by:SABINA KALYAN, GLOBAL CHIEF ECONOMIST

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 2

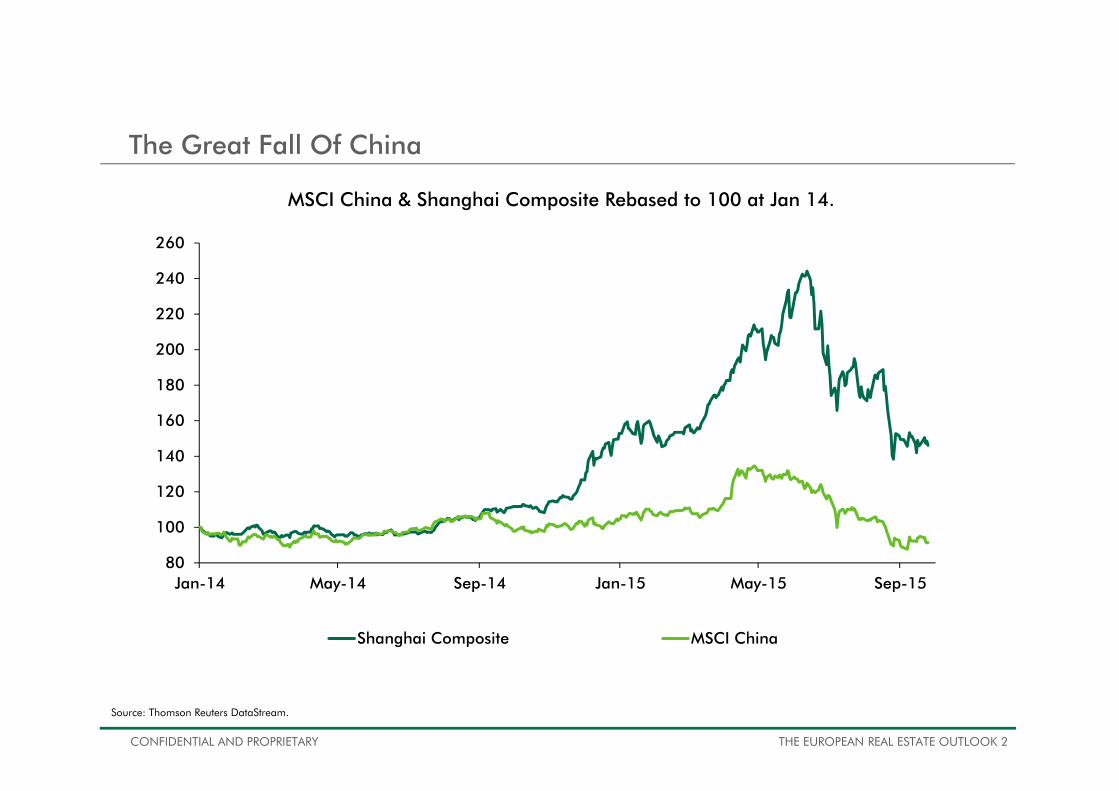

The Great Fall Of China

Source: Thomson Reuters DataStream.

80

100

120

140

160

180

200

220

240

260

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15

MSCI China & Shanghai Composite Rebased to 100 at Jan 14.

Shanghai Composite MSCI China

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 3

Another 20%?

Source: Thomson Reuters DataStream.

0.145

0.150

0.155

0.160

0.165

0.170

Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

CNY/USD Spot Rate.

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 4

Abenomics Is Doing A Lot

Source: Thomson Reuters DataStream.

-80

-60

-40

-20

0

20

40

60

Aug-90 Aug-93 Aug-96 Aug-99 Aug-02 Aug-05 Aug-08 Aug-11 Aug-14

Tankan Survey.

Non-manufacturing Manufacturing

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 5

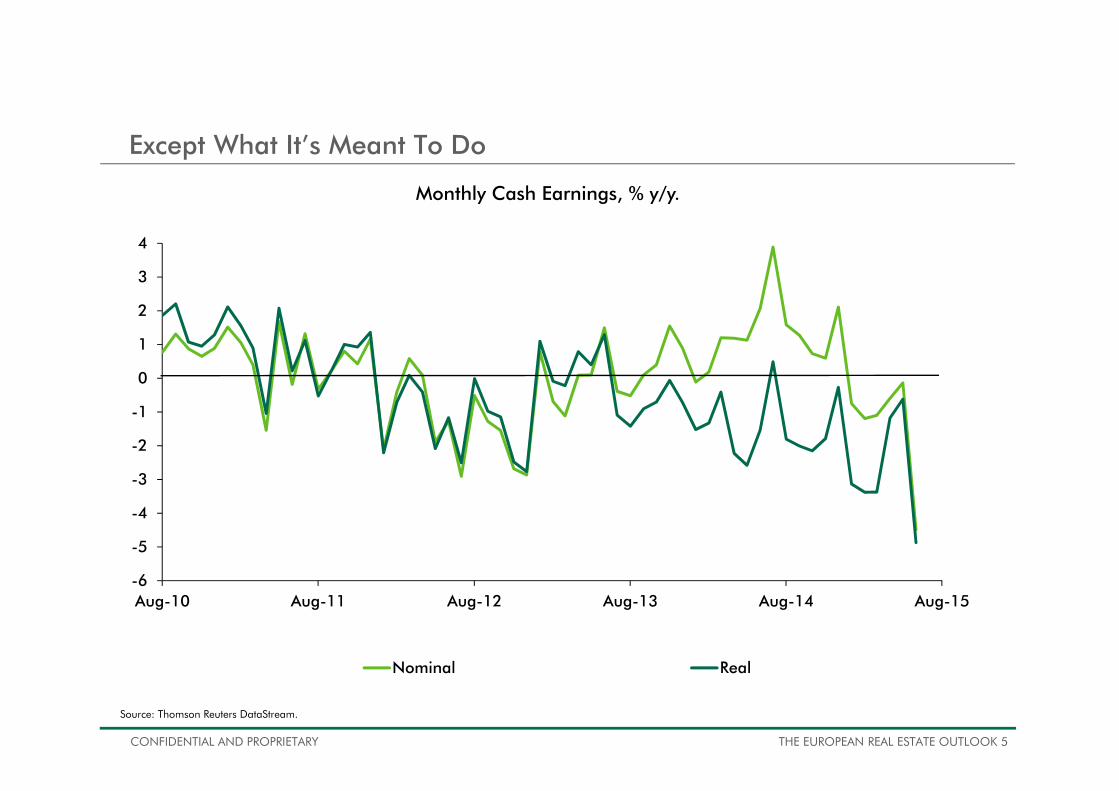

Except What It’s Meant To Do

Source: Thomson Reuters DataStream.

-6

-5

-4

-3

-2

-1

0

1

2

3

4

Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15

Monthly Cash Earnings, % y/y.

Nominal Real

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 6

The USA Struggles To Reach Escape Velocity

Source: Thomson Reuters DataStream.

30

35

40

45

50

55

60

65

Aug-00 Aug-03 Aug-06 Aug-09 Aug-12 Aug-15

ISM Business Activity Surveys.

Manufacturing Non-manufacturing

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 7

Monetary Tightening Threatened By Global Pressures

Source: Thomson Reuters DataStream.

0

1

2

3

4

1 Mo 3 Mo 6 Mo 1 Yr 2 Yr 3 Yr 5 Yr 7 Yr 10 Yr 20 Yr 30 Yr

Market Implied Path of US Interest Rates, %.

31 Dec 13

30 Jun 15

31 Dec 14

25-Sep-15

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 8

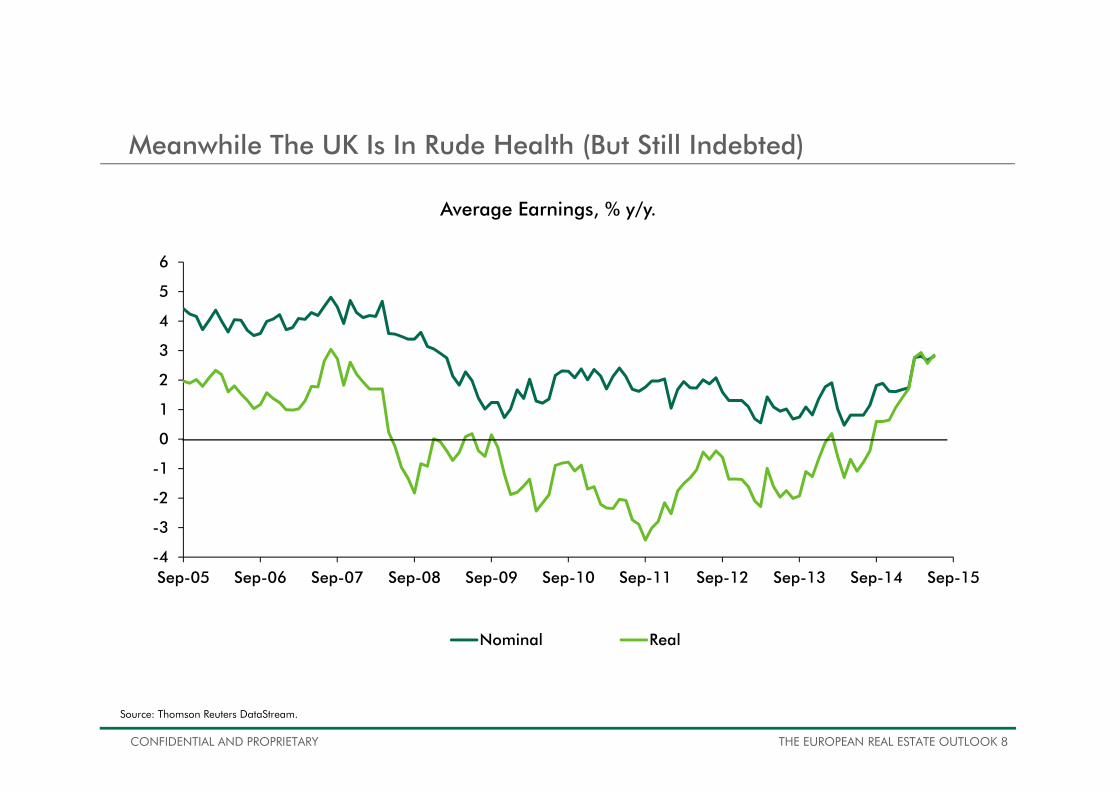

Meanwhile The UK Is In Rude Health (But Still Indebted)

Source: Thomson Reuters DataStream.

-4

-3

-2

-1

0

1

2

3

4

5

6

Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15

Average Earnings, % y/y.

Nominal Real

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 9

And Wrestling With The Same Policy Dilemma As The USA

Source: Thomson Reuters DataStream.

75

80

85

90

95

100

105

110

115

120

95 97 99 01 03 05 07 09 11 13 15

Real Effective Exchange Rate Indices.

GBP USD

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 10

By Contrast The Eurozone Is At The Start Of Its Easing Cycle

Source: Gavekal.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Fed QE3 Fed QE2 BoE QE2 BoJ 2013 BoE QE1 BoJ 2014 ECB QE1

Ratio of Central Bank’s Government Bond Purchases To Net Bond Issuance.

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 11

The Demand For Credit Is Recovering

Source: European Central Bank.

-5

0

5

10

15

20

04 05 06 07 08 09 10 11 12 13 14 15

Loan Growth, % y/y.

Consumer credit Corporate creditMortgage debt

Source: European Central Bank.

-60

-50

-40

-30

-20

-10

0

10

20

30

07 08 09 10 11 12 13 14 15

Net Change In Demand For Credit.

Large firms Small firms Consumers

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 12

And Frankly There Isn’t Much Between The USA & The Eurozone

Sourec: OEF except USA which is Moody’s.

0

1

2

3

4

5

6

7GDP Forecasts, % pa.

2015 2016 2017 2018 2019 2015-2019

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 13

So Where Does Europe Stand Relative To Its Global Peers

THE EUROZONE

• EASY MONETARY POLICY

• WEAKENING EXCHANGE RATE

• RECOVERING DEMAND

• AND DESPITE BREXIT & GREXIT, COMPARABLY STABLE POLITICAL & LEGAL BACKDROP

THE UK

• MONETARY POLICY CYCLE EXTENED BY GLOBAL VOLATILITY

• LATE CYCLE BUT DEMAND STILL SURPRISINGLY STRONG

• BACK TO A SAFE HAVEN ONCE THE EU REFERENDUM IS TRAVERSED (?)

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 14

The Problem Is That Europe’s Attractions Are Not Unnoticed

Source: CBRE EMEA Research.

0

10

20

30

40

50

60

70

80

90

06 07 08 09 10 11 12 13 14 15

Investment Volumes, EUR bn per quarter.

-100

-80

-60

-40

-20

0

20

40

60

80

'06 '07 '08 '09 '10 '11 '12 '13 '14 15

Investment Volumes, % y/y.

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 15

Closed End Funds Are Back And Targeting Europe

Source: Preqin.

3475

0

50

100

150

200

250

300

06 07 08 09 10 11 12 13 14 H115

Closed End Fund Dry Powder, EURbn.

Europe North America Asia Rest of World

20% 30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

06 07 08 09 10 11 12 13 14 H115

Closed End Fund Dry Powder By Region, % Of Total.

Europe North America Asia Rest of World

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 16

Desperate Investors Are Using Portfolios To Place Capital Quickly

Source: Real Capital Analytics.

0 1 2 3 4 5 6 7 8

QIAKlepierre

Deut. Ann.BrookfieldStarwoodLone Star

BlackstoneGreystar REP

CPPIBNorthStar

PatriziaCitycon OyjCale Street

CerberusLGIM

Top 15 Portfolio Investors In Europe In H1 2015, EURbn.

Inst/Sov Wealth Debt REIT Private Equity

14%

37%

0

20

40

60

80

100

120

08 09 10 11 12 13 14 15

Portfolio Acquisitions By Capital Source, EURbn & Global as a % of

Total.

Domestic European Global

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 17

The Biggest Increase In Activity Has Been In The South

Source: CBRE EMEA Research.

0%

10%

20%

30%

40%

50%

60%Market Share, % of Total.

H1 15 Average

26

-50

0

50

100

150

200Investment Volumes, % H1 2015/H1 2014.

750!

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 18

But London Still Dominates Transaction Activity

Source: Real Capital Analytics.

€0B

€5B

€10B

€15B

€20B

€25B

€30B

€35B

Transactions In Europe In H1 2015.

Paris

Berlin

Frankfurt

Madrid

In H1’15 London accounted for more transaction volume than the next 7 European cities combined.

London Munich

MilanHamburg

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 19

Pricing Is Reaching Record Levels

Source: CBRE EMEA Research.

3

4

5

6

7

8

9

10

88 91 94 97 00 03 06 09 12 15

Prime EU-15 Yields, %.Latest=June 2015.

Retail IndustrialOffice Retail trendIndustrial trend Retail trend

75

100

125

150

175

200

225

86 89 92 95 98 01 04 07 10 13

Prime EU-15 Real Rents Rebased to 100 in 1986. Latest=June 2015.

Retail IndustrialOffice Retail trendIndustrial trend Retail trend

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 20

Spain In Particular Has Seen Yields Compress At A Rapid Rate

Source: CBRE EMEA Research.

-100

-50

0

50

100

150

200

250

300

06 07 08 09 10 11 12 13 14 15

Prime Office Yield Premium Over West End, bps.

Paris Stockholm Frankfurt Amsterdam Madrid Prague

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 21

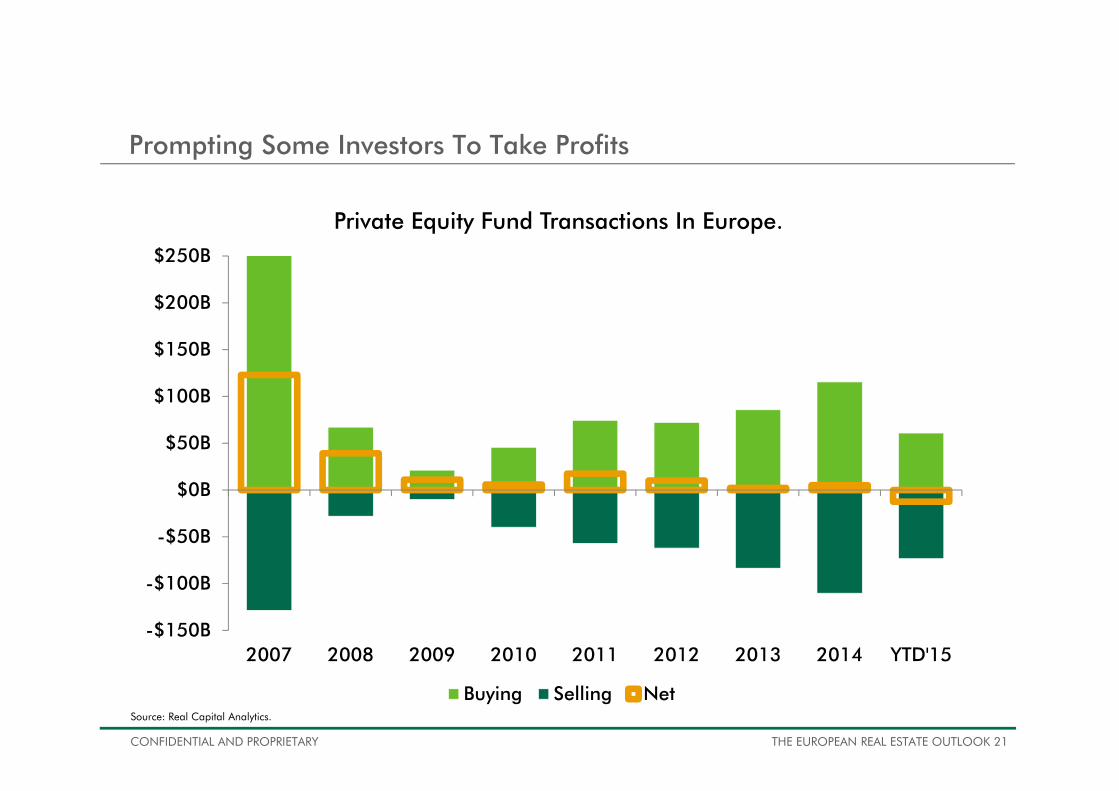

Prompting Some Investors To Take Profits

Source: Real Capital Analytics.

-$150B

-$100B

-$50B

$0B

$50B

$100B

$150B

$200B

$250B

2007 2008 2009 2010 2011 2012 2013 2014 YTD'15

Private Equity Fund Transactions In Europe.

Buying Selling Net

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 22

Others Are Looking For Higher Yielding Assets

Source: CBRE EMEA Research.

0

50

100

150

200

250

300

350

400

450

Yield Gap Over The Current Cycle.

Maximum Minimum Q2 15

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 23

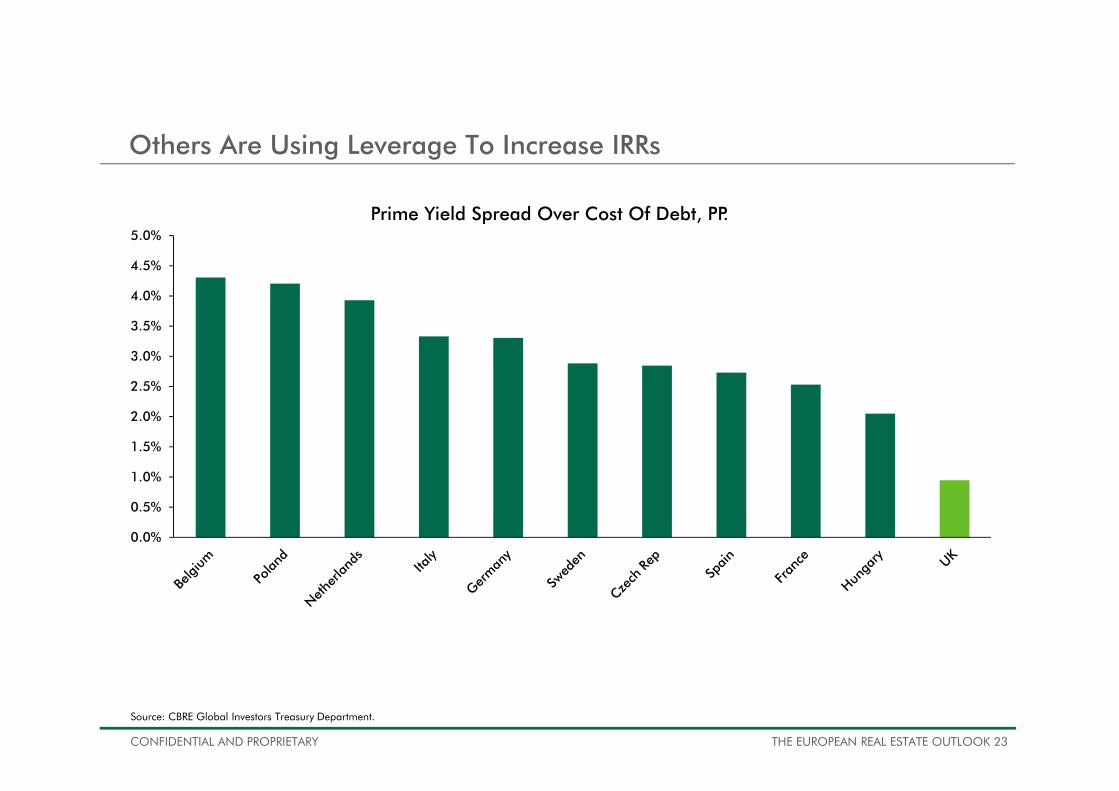

Others Are Using Leverage To Increase IRRs

Source: CBRE Global Investors Treasury Department.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%Prime Yield Spread Over Cost Of Debt, PP.

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 24

So Is There Still Embedded Value In This Market?

Source: CBRE EMEA Research.

20

30

40

50

60

70

80

90

100

110

120

06 07 08 09 10 11 12 13 14 15

Real Prime Office Capital Values Per Sq M Rebased To 100 In Q2 2007.

Frankfurt

Amsterdam

London City

Paris

Prague

London West End

Madrid

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 25

We Are Still Early Cycle For The Rent Recovery

-5

0

5

10

15

20

High Street Retail Shopping Centre

Real Prime Rent Growth, % cumulative, 2015-2019

Source: CBRE Global Investors.

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 26

European Real Estate Investment Themes

DOMINANT RETAIL CENTRES PRIME LOGISTICS FACILITIES IN MAJOR DISTRIBUTION HUBS

CYCLICAL OFFICE RECOVERY NICHE RESIDENTIAL IN UNDER-SUPPLIED MARKETS

Retailers are concentrating their presence in dominant retail locations/formats

PreferredMarkets

Central London & Paris high street retailNW European dominant shopping centres with asset management potentialSouthern Europe for yield compression & rent growth

Shortage of modern facilities and strong demand driven by e-commerce

PreferredMarkets

Major NW European marketsWarsaw and Czech RepBarcelona

Shortage of modern space in city centres combined with strong demand from media and tech companies in emerging locations

PreferredMarkets

London & ManchesterAmsterdam South AxisMadrid & BarcelonaFor higher risk-adjusted return investors - Budapest

Demographic trends combined with shortage of supply for Independent/assisted living facilities and student accommodation

PreferredMarkets

London residentialStudent housing in NWEuropeSenior living in the UKDutch social housing given regulatory change

Preferred Investment

Themes

CONFIDENTIAL AND PROPRIETARY THE EUROPEAN REAL ESTATE OUTLOOK 27

DisclaimerThis presentation ( the “Presentation”) is being furnished on a confidential basis to a limitednumber of accredited investors on a “one-on-one” basis for information and discussionpurposes only and does not constitute an offer to sell or a solicitation of an offer to purchaseany security. Any such offer or solicitation shall be made only pursuant to a confidentialprivate placement memorandum (as amended, restated, supplemented or otherwisemodified from time to time, the “Memorandum”) of the corresponding fund or program,which describes risks related to an investment in such fund or program as well as otherimportant information about the fund or program and its sponsor. Offers and sales ofinterests in any fund or program may not be registered under the laws of any jurisdiction andwill be made solely to qualified investors under all applicable laws. By accepting thePresentation, you agree to keep it confidential and to not disclose it to anyone except to (i)your legal, tax and financial advisors who agree to maintain these materials in confidence,or (ii) a governmental official upon request, if entitled to such information pursuant to ajudicial or governmental order. The information set forth herein does not purport to becomplete and is subject to change. This Presentation is qualified in its entirety by all of theinformation set forth in a Memorandum, including, without limitation, all disclaimers, riskfactors and conflicts of interest. A Memorandum and a partnership agreement andsubscription documents of a fund or program must be read carefully in their entirety prior toinvesting in a fund or program. This Presentation does not constitute a part of aMemorandum.

The information contained herein is given as of the date of this Presentation and must betreated in a confidential manner and may not be reproduced, used or disclosed, in whole orin part, without the prior written consent of CBRE Global Investors.

Past performance of the prior funds’ or programs’ investments is not necessarily indicative ofthe future returns of any current or future fund or program. There can be no assurance thatany fund or program will be able to make investments similar to those made in the prior funsor programs. The ultimate returns realized by any fund or program will depend on numerousfactors that are subject to uncertainty. Accordingly, there can be no assurance that any returnobjectives will actually be realized.

Targeted and forecasted returns are derived from analysis based upon both quantitative andqualitative factors, including market experience and historical and expected averages relatedto the risk/return profile and criteria for investments (the “Investment Targets”) of the fund orprogram. The Investment Targets are based on the expected cumulative internal rates ofreturn generated by the expected investments across a multi-year period. After synthesizingthis information, CBRE Global Investors has arrived at what it believes are realistic targetreturns for the fund or program. Any target data or other forecasts contained herein arebased upon subjective estimates and assumptions about circumstances and events that maynot yet have taken place and may never do so. If any of the assumptions used do not proveto be true, results may vary substantially. Actual individual investment performance may notachieve the Investment Targets upon realization/liquidation as initially expected, which mayhave a material effect on overall realized portfolio performance over the life of the fund orprogram and the ability to achieve targets. The ability to achieve a given Investment Targetmay be affected by numerous factors including, but not limited to, investment values, cashflow, environmental and structural factors, ratings and market conditions.

Many factors affect performance including changes in market conditions and interest ratesand changes in response to other economic, political or financial developments. The targetreturns are pre-tax and represent possible returns that may be achieved, but are in no wayguaranteed. The target returns are subject to change at any time and are current as of thedate hereof only. In any given year, there may be significant variation from these targets,and there is no guarantee that the fund or program will be able to achieve the InvestmentTargets in the long term.

Assets under management (AUM) refers to current fair market value of real estate-relatedassets with respect to which CBRE Global Investors provides, on a global basis, oversight,investment management services and other advice, and which generally consist of propertiesand real estate-related loans; securities portfolios; and investments in operating companies,joint ventures and in private real estate funds under its fund of funds program. CBRE GlobalInvestors' calculation of AUM may differ from the calculations of other asset managers. CBREGlobal Investors changed its calculation of AUM with the ING REIM acquisition. The changein methodology has not had a material impact on its AUM calculation. The new methodologyhas been used to derive pro forma combined AUM as of September 30, 2011.

Statements contained in this Presentation that are not historical facts are based on currentexpectations, estimates, projections, opinions and beliefs of the fund or program’s sponsor.Such statements involve known and unknown risks, uncertainties and other factors, andundue reliance should not be placed thereon. Additionally, this Presentation contains“forward looking statements.” Actual events or results or the actual performance of any fundor program may differ materially from those reflected or contemplated in such forward-looking statements.

Certain economic and market information contained herein has been obtained frompublished sources prepared by third parties and in certain cases has not been updatedthrough the date hereof. Neither CBRE Global Investors, any fund or program or its generalpartner, nor their respective affiliates nor any of their respective employees or agents assumeany responsibility for the accuracy or completeness of such information.

All target or projected gross internal rates of return (IRRs) do not reflect any managementfees, acquisition fees, reserves, carried interest, taxes, transaction costs and other expenses tobe borne by certain and/or all investors, which will reduce returns. Gross IRR or Gross Returnshall mean an aggregate, compound, annual, gross internal rate of return on investments.

CBRE Global Investors has not made any representation or warranty, express or implied, withrespect to the fairness, correctness, accuracy, reasonableness or completeness of any of theinformation contained herein (including but not limited to information obtained from thirdparties), and they expressly disclaim any responsibility or liability therefore. CBRE GlobalInvestors does not have any responsibility to update or correct any of the informationprovided in this Presentation.

Prior to investing in a fund or program, prospective investors should consult with their owninvestment, accounting, regulatory, tax and other advisors as to the consequences of aninvestment in the fund or program.

The information in this document is confidential and meant for use only by the intended recipient. This material is intended for informational purposes only, does notconstitute investment advice, or a recommendation, or an offer or solicitation, and is not the basis for any contract to purchase or sell any security, property or otherinstrument, or for CBRE Global Investors to enter into or arrange any type of transaction. This information is the sole property of CBRE Global Investors and itsaffiliates. Acceptance and/or use of any of the information contained in this document indicates the recipient’s agreement not to disclose any of the informationcontained herein.

www.cbreglobalinvestors.com