trust owned life insurance (toli) - esquire cle · trust owned life insurance (toli) the audit...

TRANSCRIPT

TRUST OWNED LIFE INSURANCE (TOLI)

THE AUDIT PROCESSRM Name

CRN 201403 - 158589

• About Lenox Advisors, Inc.

• Trustee Duties - Uniform Prudent Investor Act

• Risks and Common Problems

• Policy Audit Process

• Q & A

AGENDA

2| TOLI – The Audit Process

• We are a wholly-owned subsidiary of National Financial Partners (NFP).

• A comprehensive, multi-faceted and integrated financial services firm providing high net worth clients with a variety of wealth management services.

• Offices in New York, Chicago, San Francisco, Los Angeles and Stamford.

LENOX ADVISORS, INC .

3| TOLI – The Audit Process

Fee-based financial planning services offered through Lenox Advisors, Inc. Lenox Advisors, Inc., offers access to securities and asset management services through MML Investors Services, LLC., 530 5th Avenue, 14th Floor, New York, NY 10036, 212-536-6000, member SIPC. Investment adviser representatives of Lenox Advisors, Inc. offering fee-based financial planning services may also be registered representatives and investment adviser representatives of MML Investors Services, LLC. for purposes of offering securities and asset management services, as applicable. Lenox Advisors, Inc. is a wholly owned subsidiary of National Financial Partners Corp. (NFP). Lenox Advisors, Inc. and NFP are not affiliates or subsidiaries of MML Investors Services, LLC. Services offered through Lenox Advisors, Inc. as an Independent Registered Investment Advisor are not sponsored or offered through MML Investors Services, LLC.

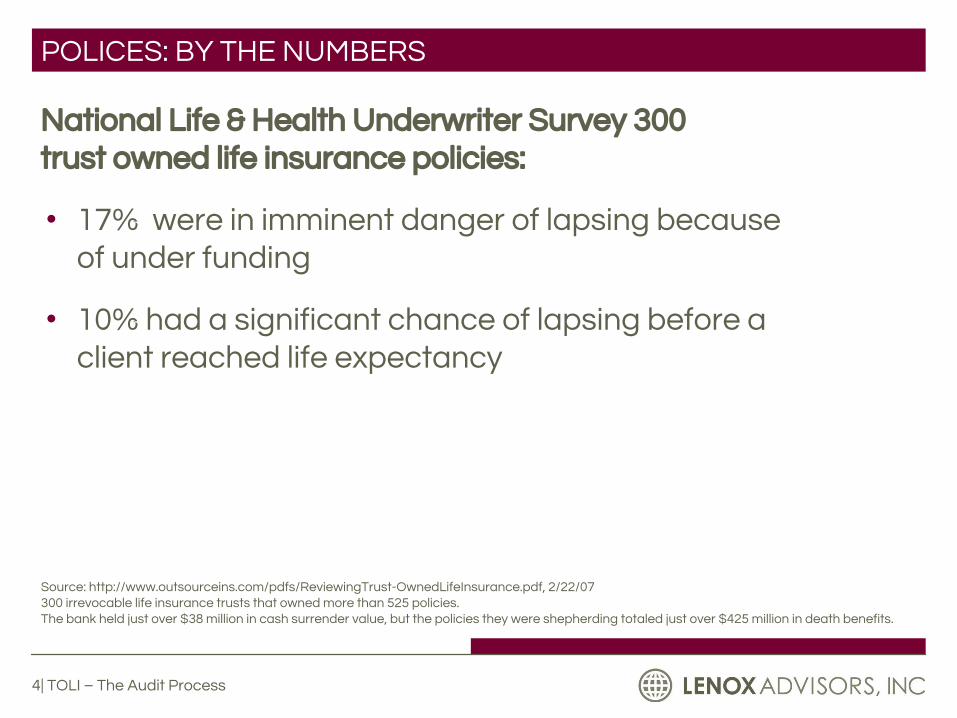

National Life & Health Underwriter Survey 300 trust owned life insurance policies:

• 17% were in imminent danger of lapsing because of under funding

• 10% had a significant chance of lapsing before a client reached life expectancy

POLICES: BY THE NUMBERS

4| TOLI – The Audit Process

Source: http://www.outsourceins.com/pdfs/ReviewingTrust-OwnedLifeInsurance.pdf, 2/22/07300 irrevocable life insurance trusts that owned more than 525 policies. The bank held just over $38 million in cash surrender value, but the policies they were shepherding totaled just over $425 million in death benefits.

Issues you should consider:

• The average (TOLI) policy death benefit is $1,710,923.

• The average death benefit for failing policies approximates $3,350,000.

• Risk to the interest of beneficiaries, the current performance and funding with life policies is knowable and may be significant.

• Request from TOLI trustee’s annual product suitability analysis, and recognize the red flags warranting further scrutiny.

• Key Bank Case –Most significant case to date as it relates to TOLI.

RISK MANAGEMENT CONSIDERATIONS

5| TOLI – The Audit Process

Source: http://www.lifeinsurancebuyers.com/LIBI/media_files/TOLI_Risk_Management_at_Litigation_Crossroads.pdf April 12, 2007

• 84% of the trusts had no written guidelines or procedures to guide the trustee in its ownership of life insurance.

• 96% had no policy statements on how to handle life insurance investments.

• 71% of personal trustees had not reviewed their trust’s life insurance policies in the past 5 years.

TRUSTS: BY THE NUMBERS

6| TOLI – The Audit Process

Source: http://www.lifeinsurancebuyers.com/LIBI/media_files/TOLI_and%20Settlements.pdf 09/16/2005

7| TOLI – The Audit Process

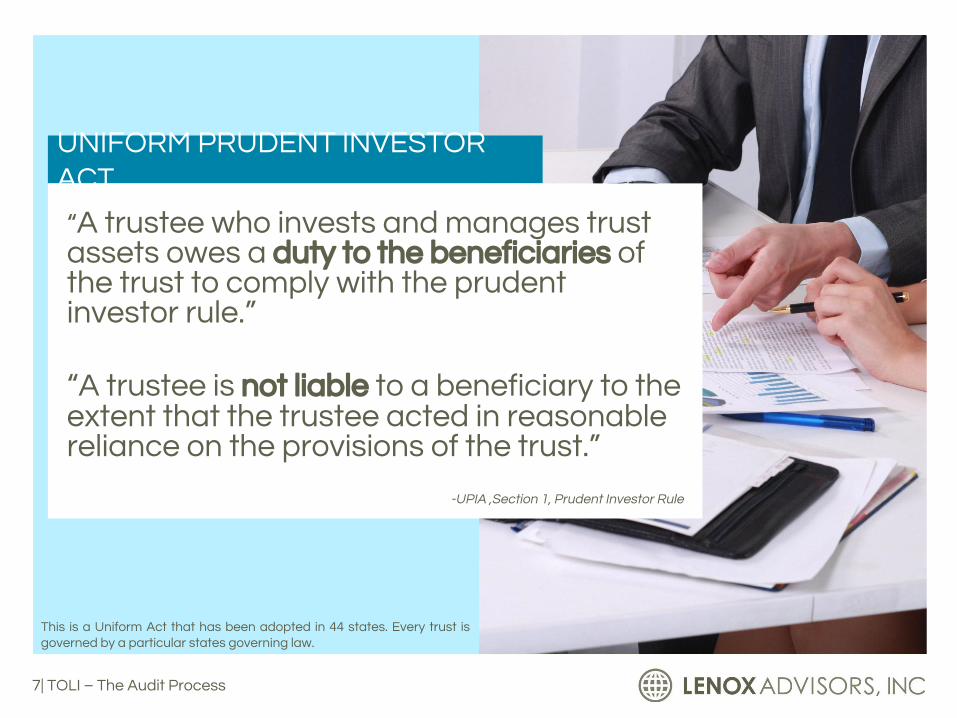

This is a Uniform Act that has been adopted in 44 states. Every trust is governed by a particular states governing law.

UNIFORM PRUDENT INVESTOR ACT

“A trustee who invests and manages trust assets owes a duty to the beneficiaries of the trust to comply with the prudent investor rule.”

“A trustee is not liable to a beneficiary to the extent that the trustee acted in reasonable reliance on the provisions of the trust.”

-UPIA ,Section 1, Prudent Investor Rule

“A trustee shall invest and manage trust assets as a prudent investor would, by considering the purposes, terms, distribution requirements, and other circumstances of the trust. In satisfying this standard, the trustee shall exercise reasonable care, skill, and caution.”

-Section 2, Standard of Care; Portfolio Strategy; Risk and Return Objectives

UNIFORM PRUDENT INVESTOR ACT

8| TOLI – The Audit Process

“A trustee may delegate investment and management functions… [The trustee] is not liable to the beneficiaries or to the trust for the decisions or actions of the agent to whom the function was delegated.”

-Section 9, Delegation of Investment and Management Functions

States adopting the UPIA(43) (in whole or in majority):

Alabama, Alaska, Arizona, Arkansas, California, Colorado, Connecticut, District of Columbia, Hawaii, Idaho, Indiana, Iowa, Kansas, Maine, Massachusetts, Michigan, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, Rhode Island, South Carolina, Tennessee, Texas, U.S. Virgin Islands, Utah, Vermont, Virginia, Washington, West Virginia, Wisconsin, Wyoming

TRUSTEE DUTIES - STATE ADOPTION OF UPIA

Source: National Conference of Commissioners on Uniform State Laws

9| TOLI – The Audit Process

• No Investment Policy Statement.

• No trust provision to delegate periodic policy evaluation.

• A personal or advisor trustee who lacks extensive knowledge of life insurance products and does not obtain credible third-party policy evaluation.

• Not providing a periodic report to the beneficiaries confirming that the policy is suitable for the trust purpose and that its performance achieves benchmark expectations.

• Annual performance reports for variable universal life policies that do not affirm the asset allocation strategy and related volatility-tested premium adequacy evaluation.

FAILURES OF TOLI RISK MANAGEMENT

Source: http://www.lifeinsurancebuyers.com/LIBI/media_files/TOLI_Risk_Management_at_Litigation_Crossroads.pdf April 12, 2007.

10| TOLI – The Audit Process

• Flexible premium policies now approximate 35% - 40% of Inforce TOLI policies as compared to less than one percent 25 years ago. Larger death benefit policies tend to be flexible premium non-guaranteed death benefit policies purchased in the past 25 years.

• A significant number of Inforce TOLI policies warrant remediation due to their under-performance of policy acceptance benchmark values. Adjust this statistic for guaranteed policies and it is likely to be 100% of non-guaranteed policies.

• Over 90% of TOLI policies are unattached, without an assigned servicing agent.

WHAT’S THE PROBLEM

Source: http://www.lifeinsurancebuyers.com/LIBI/media_files/TOLI_Risk_Management_at_Litigation_Crossroads.pdf April 12, 2007.

11| TOLI – The Audit Process

COMMON PROBLEMS: BENEFICIARY/GRANTOR LIFE CHANGES

• Has the need for insurance increased or decreased over time?

• Is there an unexpected premium increase required to fund the policy?

• Have the financial needs and concerns changed over time?

• Has the insured health changed significantly?

Family, financial or business status may impact your clients' life insurance coverage needs.

12| TOLI – The Audit Process

• Have all premiums been paid as scheduled and on time?

• Have there been any loans or withdrawals from the

policy?

• Have there been statements or notices suggesting an

increase premium or of pending lapse?

COMMON PROBLEMS: TRUSTEE-BASED

13| TOLI – The Audit Process

COMMON PROBLEMS: POLICY-BASED

Universal and Variable Life Policies:

• Changes in interest rate and expense charges

• Underperforming funds• Appropriate premium

funding• Late premiums, lost

guarantee

Whole Life Policies:

• Decreases in dividends• Strength of Carrier• Complex term/

supplemental riders• Policy withdrawal or loans

Term Policies:

• Nearing expiration of level

premium period with large

increases in premium

anticipated

• Newer term products may

be more cost effective

• Conversion features near

expiration

• Appropriate premium

funding

14| TOLI – The Audit Process

COMMON PROBLEMS: CARRIER-BASED

• The strength and stability of the insurance company is reflected in the financial ratings of the major rating agencies

• Carriers own investment experience

• Stock versus Mutual Companies - What's the difference?

15| TOLI – The Audit Process

THIRD PARTY TOLI AUDIT

Key Bank Lessons

• The main takeaway from Key Bank was that a third-party audit was preformed, which released the trustee from liability.

Delegation Permitted

• Trustees are typically permitted under applicable state law (and/or by the terms of the trust) to delegate duties (e.g., insurance reviews) to third parties. See, e.g., Section 9 of the UPIA.

Delegation Possibly Required

• A trustee might be required to delegate certain trust duties (e.g., insurance reviews) where the trustee does not have the required expertise.

16| TOLI – The Audit Process

• Fact Find

• Illustration Request Letter

• In force Policy Pages

• Policy Management Statement

• Policy Audit Report

• Comparison Coverage: At the request of the trustee

TOLI AUDIT: THE LENOX PROCESS

17| TOLI – The Audit Process

FACT FIND

18| TOLI – The Audit Process

CLIENT AUTHORIZATION LETTER

19| TOLI – The Audit Process

INFORCE ILLUSTRATION FROM CARRIER

20| TOLI – The Audit Process

POLICY MANAGEMENT STATEMENT

21| TOLI – The Audit Process

POLICY AUDIT

22| TOLI – The Audit Process

POLICY AUDIT

23| TOLI – The Audit Process

POLICY AUDIT RATINGS

24| TOLI – The Audit Process

COMDEX OVERVIEW

25| TOLI – The Audit Process

LIFE INSURANCE RATE CLASSES

Ultra Preferred Non-Tobacco

Select Preferred Non-Tobacco

Non-TobaccoPlus

Non-Tobacco

Select Preferred Tobacco

Tobacco

26| TOLI – The Audit Process

LIFE INSURANCE RATINGS

The following is a summary of the typical rating classifications utilized:

Category Mortality Charges as % of “Standard”

Preferred Plus -25%Preferred -20%Standard 0%Substandard Table 2 +50%Substandard Table 4 +100%Substandard Table 6 +150%Substandard Table 8 +200%

27| TOLI – The Audit Process

MARKET ANALYSIS

28| TOLI – The Audit Process

SOLUTION

• Discuss process with your partners on how to handle the issue.

• Identify trusts in which the firm is trustee on.

• Hire consultant to audit those policies.

• Don’t stop there, ask every client when the last time they audited their policies.

• In fact, ask all clients if they are trustees on ILIT’s for any of their family or friends.

• Market that you provide this value added service.

29| TOLI – The Audit Process