trading range intact

TRANSCRIPT

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 1/8

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 2/8

Investment Strategy Outlook

The day-to-day movements in the stock

market can amount to little more than

noise -- noise that should be actively

and intentionally drowned out. That

seems to have been especially true over

the past year-plus. The S&P 500

currently trades in close proximity to

where it began 2016 and where it began

2015. The wide range on the S&P 500

that we have seen in 2016 (between

1800 and 2120) has not covered any

ground not seen over the prior year and

a half. More recently, the S&P 500 has

re-settled into a narrower trading range

(support near 2040 and resistance near

2100) that was prominent in the first half

of 2015 and also re-emerged in the

fourth quarter of last year. In other

words, the S&P 500 has gone nowhere,but it has done so quickly.

Fed policy is neutral. Even if the 25

basis point rate hike from December is

followed by two more rate hikes this

year (which is the official expectation of

the Fed, but not the market), it would

be hard to argue that actual monetary

policy has tightened significantly or is

poised to have an undue negative

influence on stocks or bonds.

However, the disconnect between

market expectations and

prospective Fed actions does raise

risks for both stocks and bonds.

Fed officials have become more vocal

in expressing their view that the marketis underestimating the likelihood of

future rate hikes. Bond yields have

continued to drift lower and optimism in

bonds (which has produced higher

prices and as a result lower yields) has

reached levels not seen since 2012.

Source: Ned Davis Research

Source: Stock Charts

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 3/8

Investment Strategy Outlook

Robert W. Baird & Co. Page 3 of 8

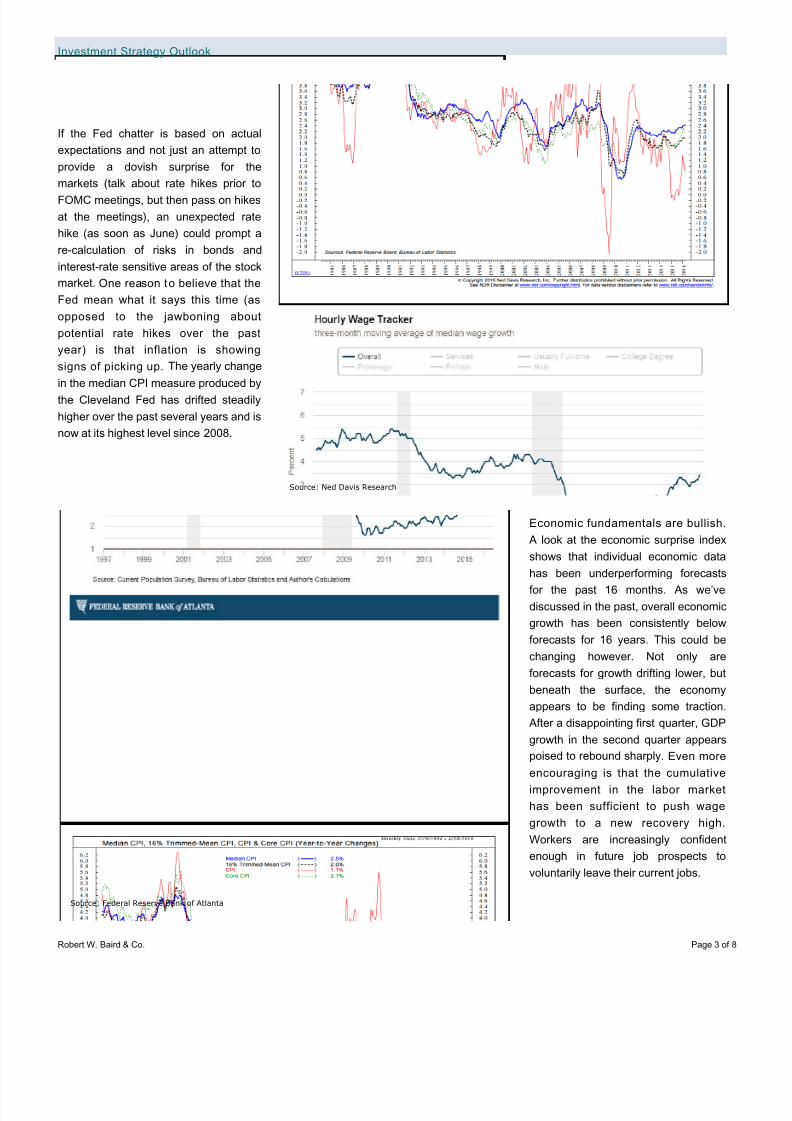

If the Fed chatter is based on actual

expectations and not just an attempt to

provide a dovish surprise for the

markets (talk about rate hikes prior to

FOMC meetings, but then pass on hikes

at the meetings), an unexpected rate

hike (as soon as June) could prompt a

re-calculation of risks in bonds and

interest-rate sensitive areas of the stock

market. One reason to believe that the

Fed mean what it says this time (as

opposed to the jawboning about

potential rate hikes over the past

year) is that inflation is showing

signs of picking up. The yearly change

in the median CPI measure produced bythe Cleveland Fed has drifted steadily

higher over the past several years and is

now at its highest level since 2008.

Economic fundamentals are bullish.

A look at the economic surprise index

shows that individual economic data

has been underperforming forecastsfor the past 16 months. As we’ve

discussed in the past, overall economic

growth has been consistently below

forecasts for 16 years. This could be

changing however. Not only are

forecasts for growth drifting lower, but

beneath the surface, the economy

appears to be finding some traction.

After a disappointing first quarter, GDP

growth in the second quarter appears

poised to rebound sharply. Even more

encouraging is that the cumulative

improvement in the labor market

has been sufficient to push wage

growth to a new recovery high.

Workers are increasingly confident

enough in future job prospects to

voluntarily leave their current jobs.

Source: Federal Reserve Bank of Atlanta

Source: Ned Davis Research

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 4/8

Investment Strategy Outlook

Robert W. Baird & Co. Page 4 of 8

Valuations remain bearish. In time,

Keynes is right -- the market can stay

irrational longer than you can stay

solvent. But over time, elevated

valuations have tended to be followed

by periods of sub-par returns. Applying

this to the current case, there is little

evidence that the currently extended

valuations will prompt a price correction

(although the risk is certainly there). A

more likely scenario is that stocks

will struggle to make meaningful

progress to the upside without strong

evidence that fundamentals are

improving. Currency-related earnings

tailwinds would be helpful, but what isreally needed is a sustained up-tick in

top-line growth.

Sentiment is neutral. The early

optimism that accompanied the March

rally in stocks has faded. A big concern

for us was that the rally in stocks would

produce excessive optimism. To some

extent, the opposite has happened.

Stocks have been relatively resilient

in the face of waning optimism (on

the sentiment surveys) and

persistent equity fund outflows.

Fund flows are not just reflecting a

secular shift from mutual funds to ETFs

but are showing a net move away from

equities. While some of the shorter-term sentiment indicators show

excessive pessimism, the message

from the more intermediate-term

measures (including the NAAIM

Exposure Index) is that optimism has

faded but sentiment is still neutral.

Source: Ned Davis Research

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 5/8

Investment Strategy Outlook

Robert W. Baird & Co. Page 5 of 8

Seasonal patterns and trends are

neutral. After the experience of 2015,

the "Sell in May" chorus has been loud

this year (perhaps contributing to the

fading in investor optimism discussed

above). History shows that this seasonalpattern tends not to works as well in

Presidential Election years. The noise

and uncertainty associated with political

campaigns may overwhelm other

seasonal impacts. While historically the

stock market does better in years when

the incumbent party wins (as shown in

the chart), the nature of the victory also

matters. Close elections tend to mean

more uncertainty and that is a negative

for stocks. Landslides (by ether party)

can be anticipated earlier and selling

gives way to buying well in advance of

the actual election. While we continue

to expect election-related noise to

add to stock market volatility, this is

likely mostly noise and seasonal

patterns are neutral.

The tape (breadth) is still neutral.

Improving breadth has marked the rally

off of the early 2016 lows as different

from the rallies seen over the pastseveral years (in particular, the rally off

of the Q3 2015 lows). Whether

looking from the perspective of

individual stocks, industry groups

or sectors, the participation in this

rally has been broad and

encouraging. Sector-level price,

momentum and breadth trends were

better at the early 2016 lows than the

late 2015 lows (a positive breadth

divergence) and have improved ahead

of the S&P 500 for most of the ensuing

rally. While breadth has been better,

we have not yet seen sufficient

strength to prompt an upgrade in this

indicator. That could come on an

upside breakout or if breadth shows

better resiliency than price in the event

of a pullback.

Source: Ned Davis Research

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 6/8

Investment Strategy Outlook

Robert W. Baird & Co. Page 6 of 8

Despite the overall neutral message

from the weight of the evidence, there

are still relative opportunities for

tactical investors. As mentioned at the

outset, small-caps and international

stocks have struggled, losing groundwhile the S&P 500 has marked time. We

continue to see relative leadership from

U.S. large-cap stocks (reflecting the

improving trends for the average stock,

an equal-weight approach may be more

appropriate than a cap-weighted

approach).

Equities overall have seen outflows,

but defensive and yield-generating

areas of the market continue to look

crowded. If bond yields start to movehigher, sentiment in these areas could

shift quickly. We have already seen

hints of that, while bond yields have

hardly budged.

Given the prospect of upward pressure

in bond yields and volatility in stocks

(and in light of the neutral message

from the weight of the evidence),

holding elevated levels of cash may

continue to be appropriate.

From a sector allocation perspective,

defensive groups have struggled to

hold onto their leadership positions.

Cyclical areas are gaining strength.

Materials and Energy are in the sector

leadership group and have relativestrength trends that are moving up.

More than anything, the sector

rankings have shown elevated rotation

and volatility as a new set of leaders

emerges and previous leaders have

faded.Source: Baird. Ranking of 1 indicates best relative strength; ranking of 10 indicates worst relative

strength.

Source: Stock Charts

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 7/8

Investment Strategy Outlook

Robert W. Baird & Co. Page 7 of 8

B AIRD STRATEGIC ASSET ALLOCATION MODEL PORTFOLIOS

Baird offers six strategic asset allocation model portfolios for consideration (see table below), four of which have a mix of equity and

fixed income. An individual’s personal situation, preferences and objectives may suggest an allocation more suitable than those shown

below. Please consult a Baird Financial Advisor in determining an asset allocation that will meet your needs.

Model PortfolioMix: Stocks /

(Bonds + Cash)Risk Tolerance Strategic Asset Allocation Model Summary

All Growth 100 / 0 Well above averageEmphasis on providing aggressive growth of capital with highfluctuations in the annual returns and overall market value of theportfolio.

Capital Growth 80 / 20 Above averageEmphasis on providing growth of capital with moderately highfluctuations in the annual returns and overall market value of theportfolio.

Growth withIncome

60 / 40 AverageEmphasis on providing moderate growth of capital and somecurrent income with moderate fluctuations in annual returns andoverall market value of the portfolio.

Income withGrowth

40 / 60 Below averageEmphasis on providing high current income and some growth ofcapital with moderate fluctuations in the annual returns and

overall market value of the portfolio.Conservative

Income20 / 80 Well below average

Emphasis on providing high current income with relatively smallfluctuations in the annual returns and overall market value of theportfolio.

CapitalPreservation

0 / 100 Well below averageEmphasis on preserving capital while generating current incomewith relatively small fluctuations in the annual returns andoverall market value of the portfolio.

Baird’s Investment Policy Committee offers a view of potential tactical allocations among equity, fixed income and cash, based upon a

consideration of U.S. Federal Reserve policy, underlying U.S. economic fundamentals, investor sentiment, valuations, seasonal trends

and broad market trends. As conditions change, the Investment Policy Committee adjusts the weightings. The table below shows both

the normal range and current recommended allocation to stocks, bonds and cash. Please consult a Baird Financial Advisor indetermining if an adjustment to your strategic asset allocation is appropriate in your situation.

Asset Class /Model Portfolio

All Growth Capital GrowthGrowth with

IncomeIncome with

GrowthConservative

IncomeCapital

Preservation

Equities:

Suggested allocation 95% 75% 55% 35% 15% 0%

Normal range 90 – 100% 70 - 90% 50 - 70% 30 - 50% 10 - 30% 0%

Fixed Income:

Suggested allocation 0% 15% 35% 45% 50% 60%

Normal range 0 - 0% 10 - 30% 30 - 50% 40 - 60% 45 - 65% 55 – 85%

Cash:Suggested allocation 5% 10% 10% 20% 35% 40%

Normal range 0 - 10% 0 - 20% 0 - 20% 10 - 30% 25 - 45% 15 - 45%

8/16/2019 Trading Range Intact

http://slidepdf.com/reader/full/trading-range-intact 8/8

Investment Strategy Outlook

Robert W. Baird & Co. Page 8 of 8

ROBERT W. B AIRD’S INVESTMENT POLICY COMMITTEE

Bruce A. Bittles B. Craig Elder Jay E. Schwister, CFAManaging Director Director Managing DirectorChief Investment Strategist PWM – Fixed Income Analyst Baird Advisors, Sr. PM

Kathy Blake Carey, CFA Jon A. Langenfeld, CFA Timothy M. Steffen, CPA, CFPDirector Managing Director Director

Associate Director of Asset Mgr Research Head of Global Equities Director of Financial Planning

Patrick J. Cronin , CFA, CAIA Warren D. Pierson, CFA Laura K. Thurow, CFADirector Managing Director Managing DirectorInstitutional Consulting Baird Advisors, Sr. PM Co-Director of PWM Research, Prod &

William A. Delwiche, CMT, CFADirector Investment Strategist

Appendix – Important Disclosures and Analyst Certi fi cat ion

This is not a complete analysis of every material fact regarding any company, industry or security. The opinions expressed here reflect o judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we canguarantee the accuracy.

ADDITIONAL INFORMATION ON COMPANIES MENTIONED HEREIN IS AVAILABLE UPON REQUESTThe indices used in this report to measure and report performance of various sectors of the market are unmanaged and direct investmentindices is not available.

Baird is exempt from the requirement to hold an Australian financial services license. Baird is regulated by the United States Securities aExchange Commission, FINRA, and various other self-regulatory organizations and those laws and regulations may differ from Australilaws. This report has been prepared in accordance with the laws and regulations governing United States broker-dealers and not Australlaws.

Copyright 2016 Robert W. Baird & Co. Incorporated

Other Disclosures

United Kingdom (“UK”) disclosure requirements for the purpose of distri buting this research into the UK and other countries which Robert W. Baird Limi ted (“RWBL” ) holds a MiFID passpor t.

This material is distributed in the UK and the European Economic Area (“EEA”) by RWBL, which has an office at Finsbury Circus House, Finsbury Circus, London EC2M 7EB and is authorized and regulated by the Financial Conduct Authority (“FCA”).

For the purposes of the FCA requirements, this investment research report is classified as investment research and is objective.

This material is only directed at and is only made available to persons in the EEA who would satisfy the criteria of being "Professioninvestors under MiFID and to persons in the UK falling within articles 19, 38, 47, and 49 of the Financial Services and Markets Act of 20(Financial Promotion) Order 2005 (all such persons being referred to as “relevant persons”). Accordingly, this document is intended only persons regarded as investment professionals (or equivalent) and is not to be distributed to or passed onto any other person (such persons who would be classified as Retail clients under MiFID).

Robert W. Baird & Co. Incorporated and RWBL have in place organizational and administrative arrangements for the disclosure aavoidance of conflicts of interest with respect to research recommendations.

This material is not intended for persons in jurisdictions where the distribution or publication of this research report is not permitted under tapplicable laws or regulations of such jurisdiction.

Investment involves risk. The price of securities may fluctuate and past performance is not indicative of future results. Any recommendatcontained in the research report does not have regard to the specific investment objectives, financial situation and the particular needs any individuals. You are advised to exercise caution in relation to the research report. If you are in any doubt about any of the contentsthis document, you should obtain independent professional advice.

RWBL is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the FCA under UK laws, whmay differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.