trade facilitation and blockchain - deloitte united states€¦ · post-clearance audit authorised...

TRANSCRIPT

Trade facilitation and blockchainCreating the future, togetherSeptember 5, 2019

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 2

1. World Trade Organisation (WTO) Trade facilitation agreement (TFA) 3

2. Authorised economic operator

• Tool for roll-out of trade facilitation 16

3. WCO / WTO Nudge for transparency in trade data flow

• Advance Cargo Information implementationGuidelines (2018)

• Guidelines on Immediate Release (2018)

• Pre-arrival processing of import customs declaration (2017) 24

4. Trade data flow harmonisation

• Case for Blockchain adoption 30

Contents

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 3

World Trade Organisation (WTO) Trade Facilitation Agreement (TFA)

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 4

Trade Facilitation Agreement (TFA)

Streamlining, harmonising, and modernizing customs processes

Expediting movement, release and clearance of goods during Import, Export and Transit

Reduction in trade costs (administrative costs and inefficient border procedures)

1

2

3

Focus areas

“You could say that [TFA] is global trade's equivalent of the shift from dial-up internet access to broadband,”

“Trade costs in developing countries are equivalent to applying a 219 percent ad valorem tariff on international trade. Even in high-income countries, the same product would face an ad valorem equivalent of 134 percent in trade cost,”

“Full implementation of the TFA could slash members’ trade costs by an average of 14.3 percent”

A few quotes from WTO Director-General Roberto Azevêdo:

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 5

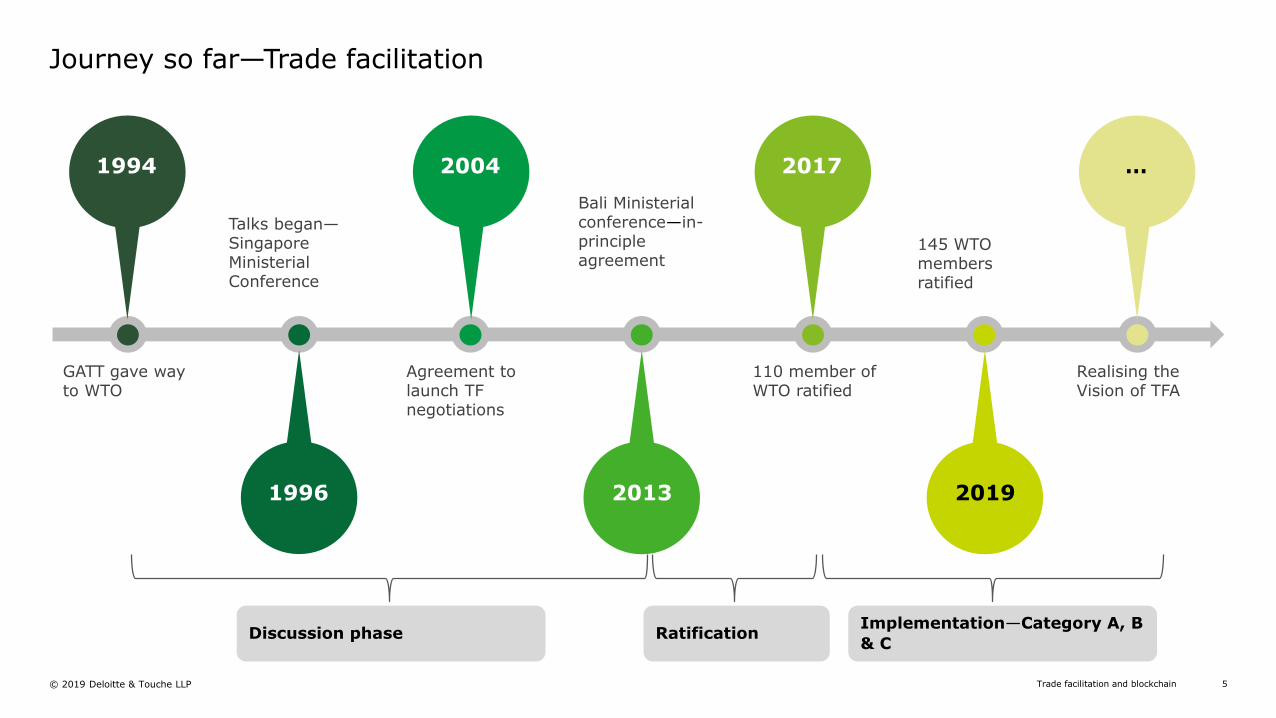

Journey so far—Trade facilitation

Discussion phase RatificationImplementation—Category A, B

& C

1994

GATT gave way to WTO

Talks began—Singapore Ministerial Conference

Agreement to launch TF negotiations

Bali Ministerial conference—in-principle agreement

110 member of WTO ratified

145 WTO members ratified

Realising the Vision of TFA

2004 2017 …

2013 20191996

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 6

Business to government partnership as facilitator of trade

TFA—Trigger for changing role of Customs

Tariff and border control

(traditional role of customs)

Trade facilitation

(Evolving role of customs)

• WCO SAFE Framework (2005)—Authorised Economic Operator (AEO)

• Revised Kyoto Protocol (2006)—Authorised Persons

• WTO Trade Facilitation Agreement (2017)—Authorised Operator—Article 7.7 of the TFA (Article 7—Release and clearance of goods)

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 7

TFA—A broad framework

Government

Government + Enterprise

Enterprise

Publication and Information

Opportunity to comment

Advance Ruling

Procedure for appeal and review

Measures to enhance impartiality, non-discrimination and

Transparency

Disciplines on fees and charges and Penalties

(w.r.t. imp/exp)

Release and clearance of goods

Border Agency Cooperation

Movement of goods intended for import under Customs

control

Formalities—import, export and transit

Freedom of transit

Customs cooperation

TFA Framework

Art. 1

Art. 2

Art. 3

Art. 4

Art. 5

Art. 6

Art. 7Art. 8

Art. 10

Art. 11

Art. 12

Art. 9

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 8

TFA—Tools of trade facilitation

1

Pre-arrival

processing

E-payment

Separation of Release from final

determination of duties etc.

Risk Management

Post-clearance Audit

Authorised Operator

Expedited Shipments

91

Perishable goodsAdvance

cargo intimation

Risk based facilitation and interdiction

To expedite release of goods while ensuring compliances

Trusted partner in trade

Expedited release at air cargo facilities

Priority in customs clearance

Payment of Customs duty

and fees

Time Release Study

Publication of average release time

6

7

8

5

Speedy and safe release & clearance of goods

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 9

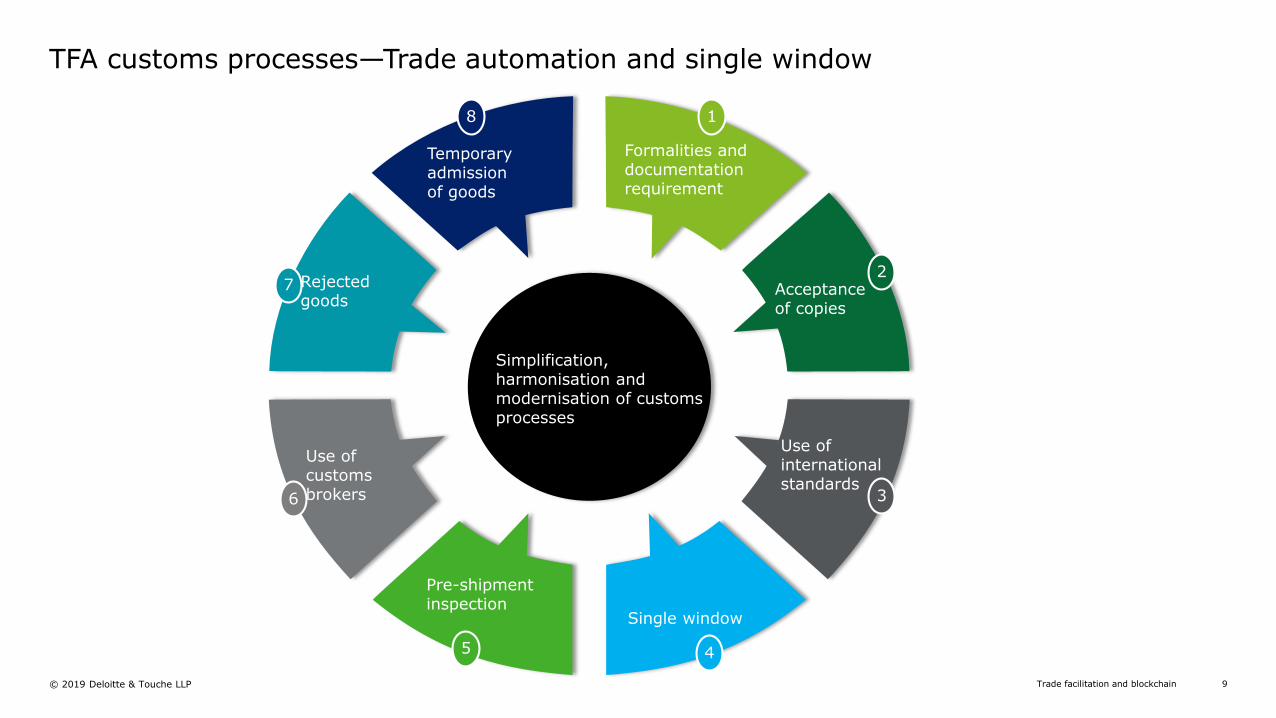

TFA customs processes—Trade automation and single window

Temporary admissionof goods

Formalities and documentation requirement

Acceptance of copies

Use of international standards

Single window

Pre-shipment inspection

Use of customs brokers

Rejected goods

Simplification, harmonisation and modernisation of customs processes

8 1

2

3

45

6

7

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 10

Region-wise—Time and Cost to Export (2019)

Source: Doing Business Report, 2019 :Trading Across Borders

Border and Documentary compliance-15 MT of non-containerised cargo

Time to Export (hours) Cost to Export (USD)

170.1

137

125.9

114.4

112.3

46.4 14.9

Sub-Saharan Africa South Asia

Middle East & North Africa Latin America & Caribbean

East Asia & Pacific Europe & Central Asia

OECD high income

774.6

687

640.2

507.5

491.6

255.4174.3

Sub-Saharan Africa Middle East & North Africa

Latin America & Caribbean South Asia

East Asia & Pacific Europe & Central Asia

OECD high income

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 11

Region-wise—Time and Cost to Import (2019)

Source: Doing Business Report, 2019 :Trading Across Borders

Border and Documentary compliance-15 MT of containerised cargo

Time to import (hours) Cost to import (USD)

224

196.6

180.9

141.7

126.2

45.8 11.9

Sub-Saharan Africa South Asia

Middle East & North Africa Latin America & Caribbean

East Asia & Pacific Europe & Central Asia

OECD high income

967.8

805

781.3

763.5

525.3

256.2125.1

Sub-Saharan Africa Middle East & North Africa

South Asia Latin America & Caribbean

East Asia & Pacific Europe & Central Asia

OECD high income

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 12

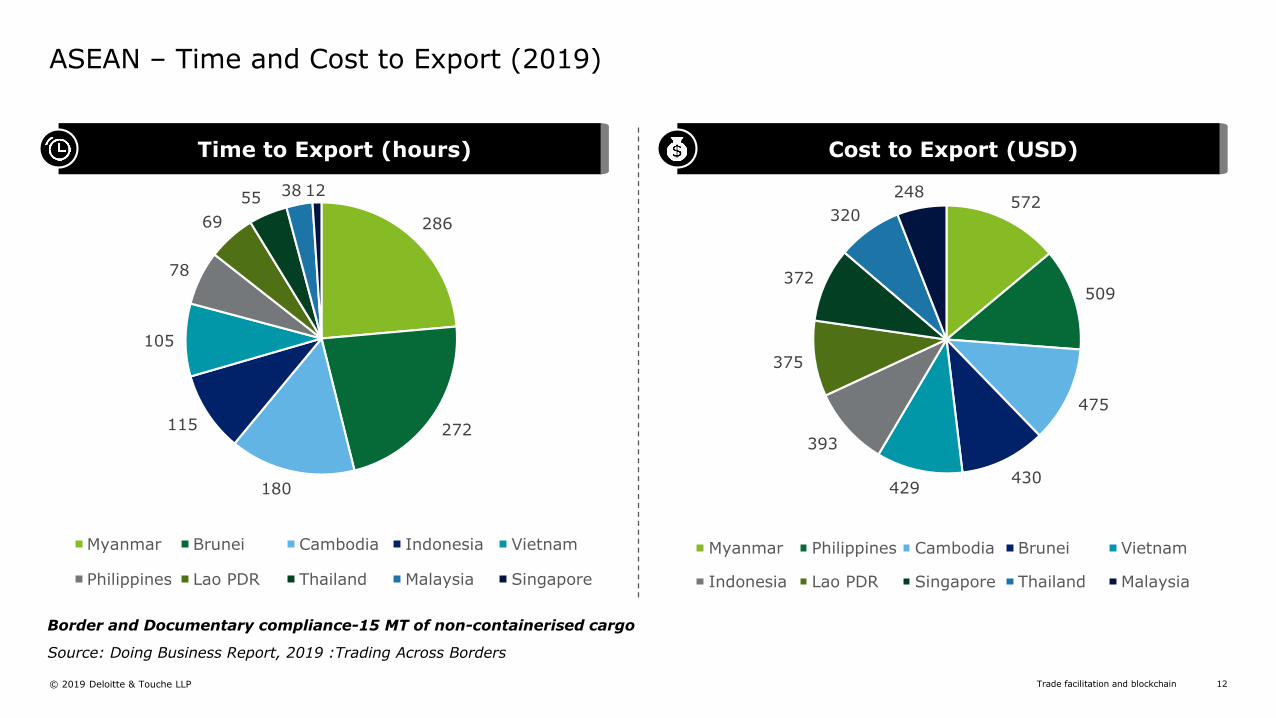

ASEAN – Time and Cost to Export (2019)

Source: Doing Business Report, 2019 :Trading Across Borders

Border and Documentary compliance-15 MT of non-containerised cargo

Time to Export (hours) Cost to Export (USD)

286

272

180

115

105

78

69

55 38 12

Myanmar Brunei Cambodia Indonesia Vietnam

Philippines Lao PDR Thailand Malaysia Singapore

572

509

475

430429

393

375

372

320

248

Myanmar Philippines Cambodia Brunei Vietnam

Indonesia Lao PDR Singapore Thailand Malaysia

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 13

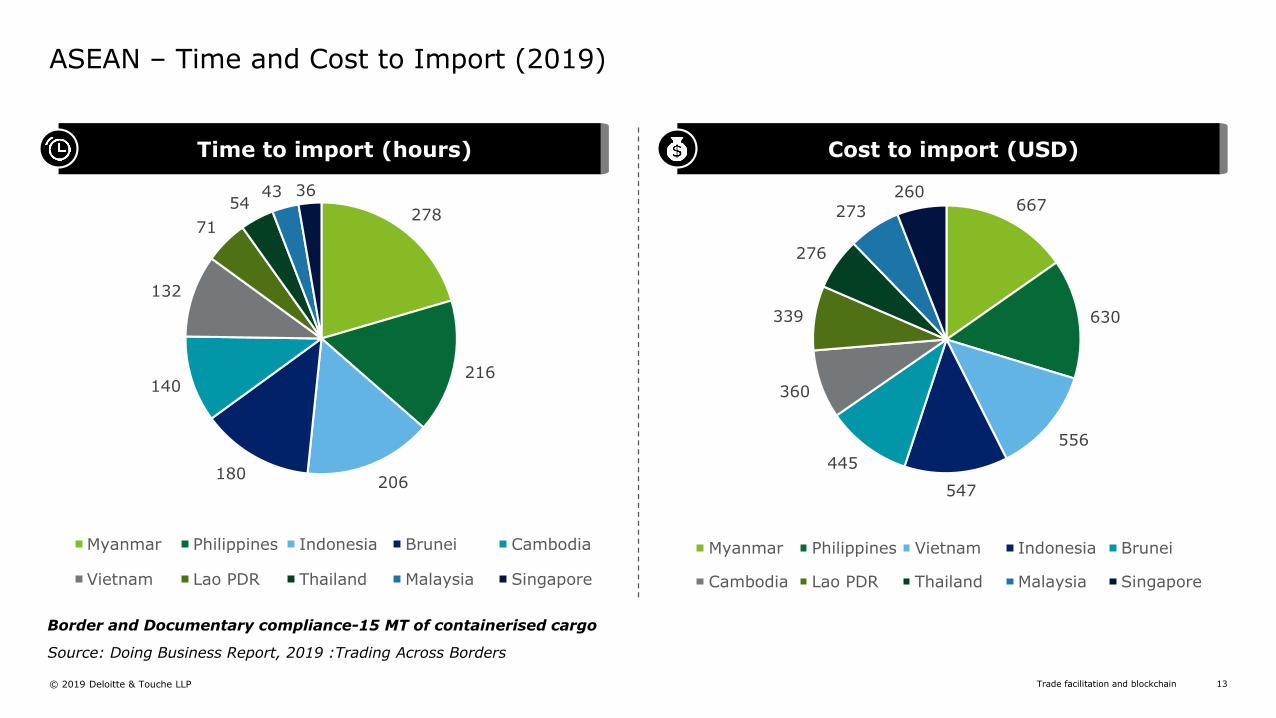

ASEAN – Time and Cost to Import (2019)

Source: Doing Business Report, 2019 :Trading Across Borders

Border and Documentary compliance-15 MT of containerised cargo

Time to import (hours) Cost to import (USD)

278

216

206180

140

132

71

5443 36

Myanmar Philippines Indonesia Brunei Cambodia

Vietnam Lao PDR Thailand Malaysia Singapore

667

630

556

547

445

360

339

276

273

260

Myanmar Philippines Vietnam Indonesia Brunei

Cambodia Lao PDR Thailand Malaysia Singapore

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 14

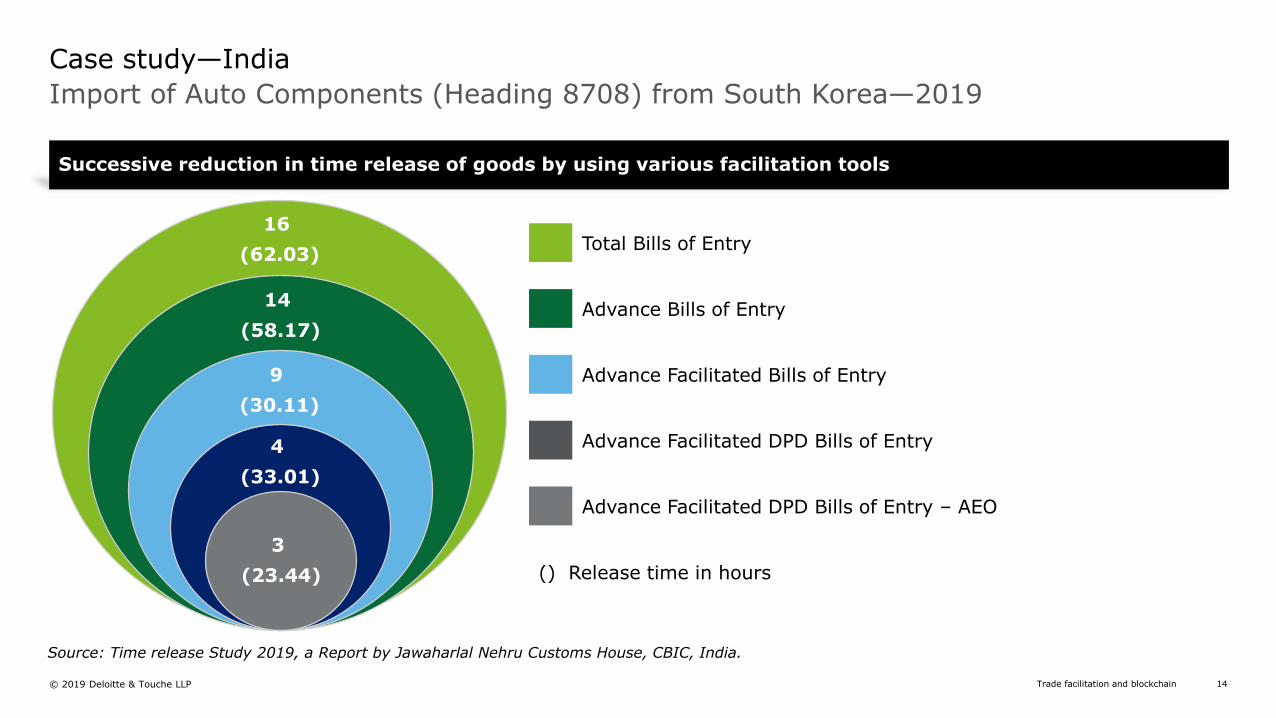

Import of Auto Components (Heading 8708) from South Korea—2019

Case study—India

Successive reduction in time release of goods by using various facilitation tools

16

(62.03)

14

(58.17)

9

(30.11)

4

(33.01)

3

(23.44)

Total Bills of Entry

Advance Bills of Entry

Advance Facilitated Bills of Entry

Advance Facilitated DPD Bills of Entry

Advance Facilitated DPD Bills of Entry – AEO

() Release time in hours

Source: Time release Study 2019, a Report by Jawaharlal Nehru Customs House, CBIC, India.

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 15

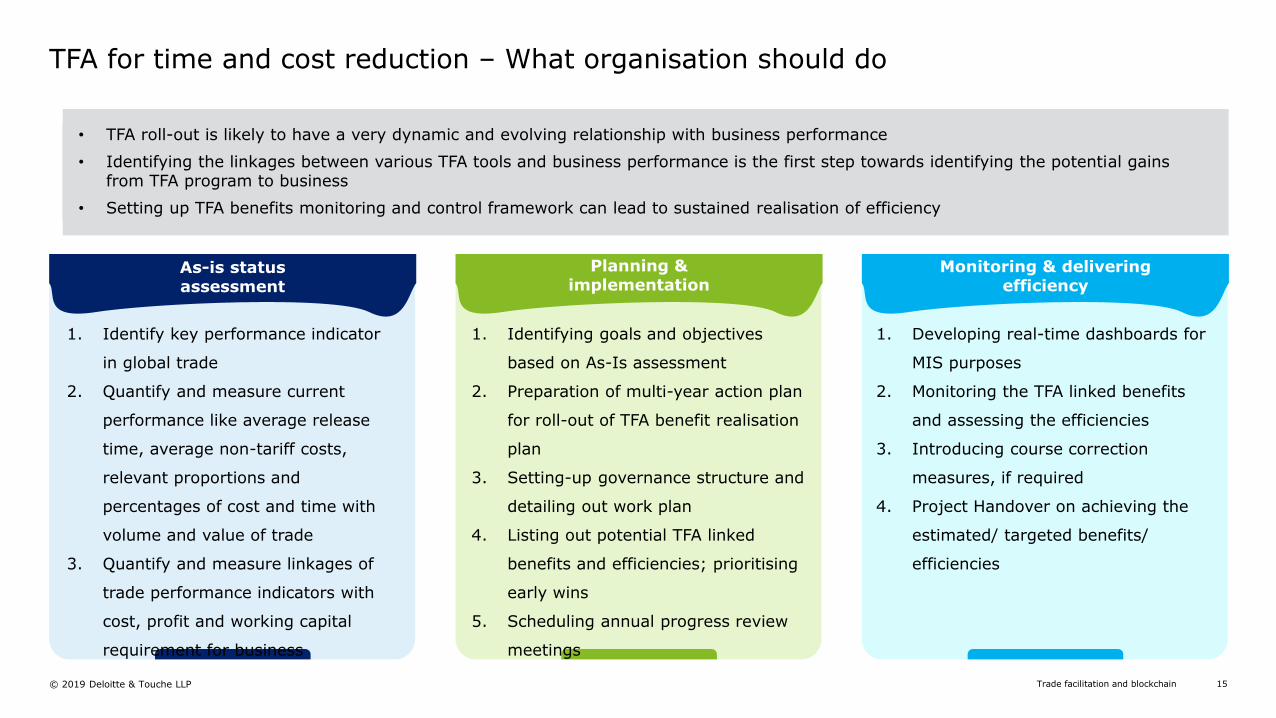

TFA for time and cost reduction – What organisation should do

As-is statusassessment

Planning & implementation

Monitoring & deliveringefficiency

1. Identify key performance indicator

in global trade

2. Quantify and measure current

performance like average release

time, average non-tariff costs,

relevant proportions and

percentages of cost and time with

volume and value of trade

3. Quantify and measure linkages of

trade performance indicators with

cost, profit and working capital

requirement for business

1. Identifying goals and objectives

based on As-Is assessment

2. Preparation of multi-year action plan

for roll-out of TFA benefit realisation

plan

3. Setting-up governance structure and

detailing out work plan

4. Listing out potential TFA linked

benefits and efficiencies; prioritising

early wins

5. Scheduling annual progress review

meetings

1. Developing real-time dashboards for

MIS purposes

2. Monitoring the TFA linked benefits

and assessing the efficiencies

3. Introducing course correction

measures, if required

4. Project Handover on achieving the

estimated/ targeted benefits/

efficiencies

• TFA roll-out is likely to have a very dynamic and evolving relationship with business performance

• Identifying the linkages between various TFA tools and business performance is the first step towards identifying the potential gains from TFA program to business

• Setting up TFA benefits monitoring and control framework can lead to sustained realisation of efficiency

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 16

Authorised Economic Operator (AEO)Tool for roll-out of trade facilitation

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 17

Tool for roll-out of trade facilitation

AEO

• TFA benefits to unfold and evolve over a period of time

• TFA/ AEO can be a strategic tool for driving efficiency and cost reduction in international supply chain

Streamlines and simplifies global Trade

Processes

Reduces Non Tariff transaction costs

Increased velocity and efficiency of trade

TFA

AEO

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 18

Industry participation in India

AEO certified entities

651

423

42588

AEO LO

AEO T2

AEO T3

AEO T1

AEO Circular—July 2016

June 2018

950 2,110

December 2018

3,666

July 2019

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 19

Tool for roll-out of trade facilitation

AEO

Key drivers for AEO certification

• deferred payment of duties, taxes, fees, and charges—leading to working capital efficiency

• use of comprehensive or reduced guarantees – leading to reduction in transaction cost

• a single customs declaration

• clearance of goods at the premises of the authorised operator

• opportunity for automation and improved controls

• low documentary and data requirements

• low rate of physical inspections and examinations

• rapid release time

Global objective to facilitate legitimate trade

AEO certification is evolving into an industry standard of good governance

AEO certification issued to importers, exporters and service providers in the international supply chain

01

02

03

Financial BenefitsBusiness process

efficiencyFacilitation at

Customs

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 20

Industry: Key questions

Why should we apply for AEO and when?

Who should be the organisational sponsor for this transformation?

How should the benefits be quantified and monitored?

What more should be expected from the Government?

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 21

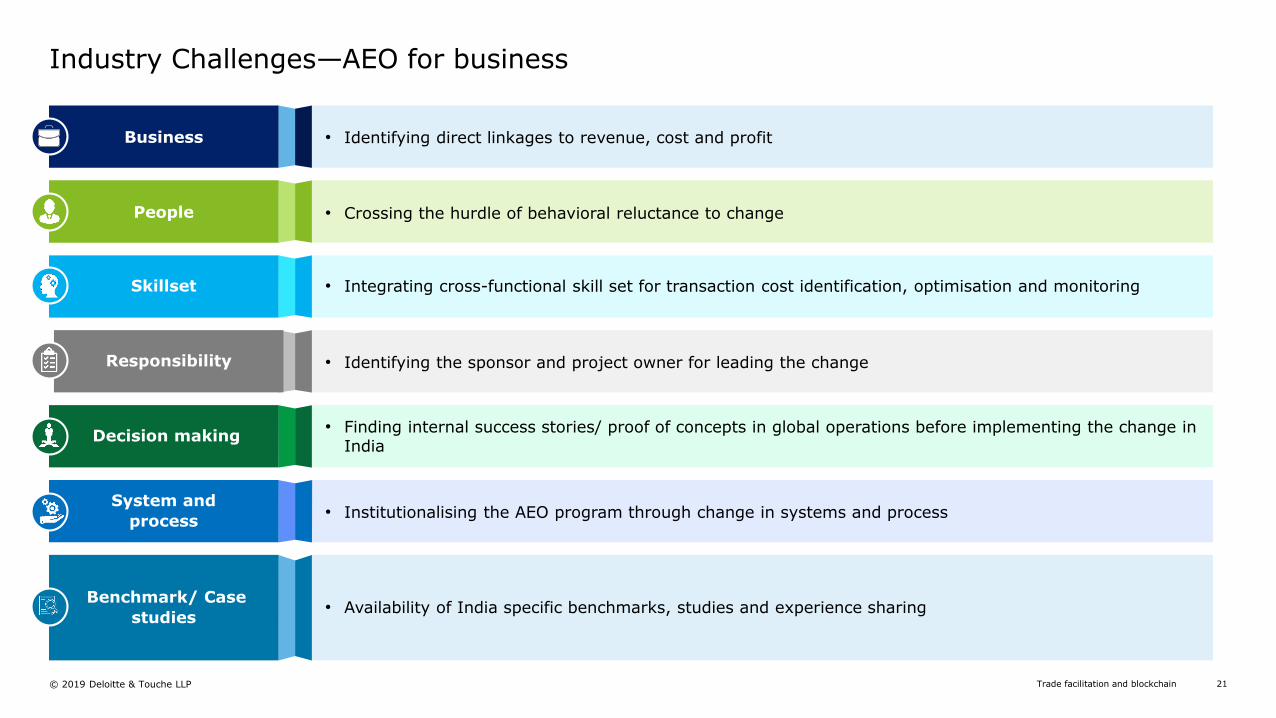

Industry Challenges—AEO for business

Benchmark/ Case

studies• Availability of India specific benchmarks, studies and experience sharing

Business • Identifying direct linkages to revenue, cost and profit

People • Crossing the hurdle of behavioral reluctance to change

Skillset • Integrating cross-functional skill set for transaction cost identification, optimisation and monitoring

Responsibility • Identifying the sponsor and project owner for leading the change

Decision making • Finding internal success stories/ proof of concepts in global operations before implementing the change in

India

System and

process • Institutionalising the AEO program through change in systems and process

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 22

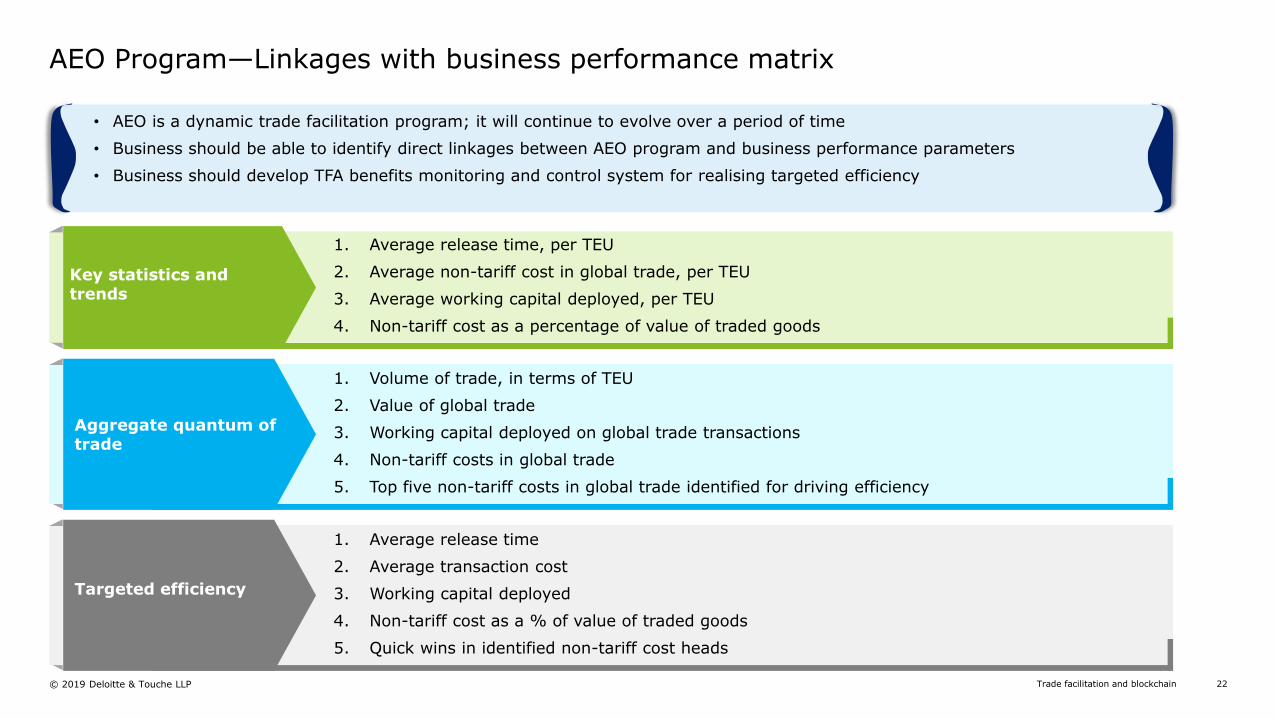

AEO Program—Linkages with business performance matrix

Key statistics and trends

1. Average release time, per TEU

2. Average non-tariff cost in global trade, per TEU

3. Average working capital deployed, per TEU

4. Non-tariff cost as a percentage of value of traded goods

• AEO is a dynamic trade facilitation program; it will continue to evolve over a period of time

• Business should be able to identify direct linkages between AEO program and business performance parameters

• Business should develop TFA benefits monitoring and control system for realising targeted efficiency

Aggregate quantum of trade

1. Volume of trade, in terms of TEU

2. Value of global trade

3. Working capital deployed on global trade transactions

4. Non-tariff costs in global trade

5. Top five non-tariff costs in global trade identified for driving efficiency

Targeted efficiency

1. Average release time

2. Average transaction cost

3. Working capital deployed

4. Non-tariff cost as a % of value of traded goods

5. Quick wins in identified non-tariff cost heads

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 23

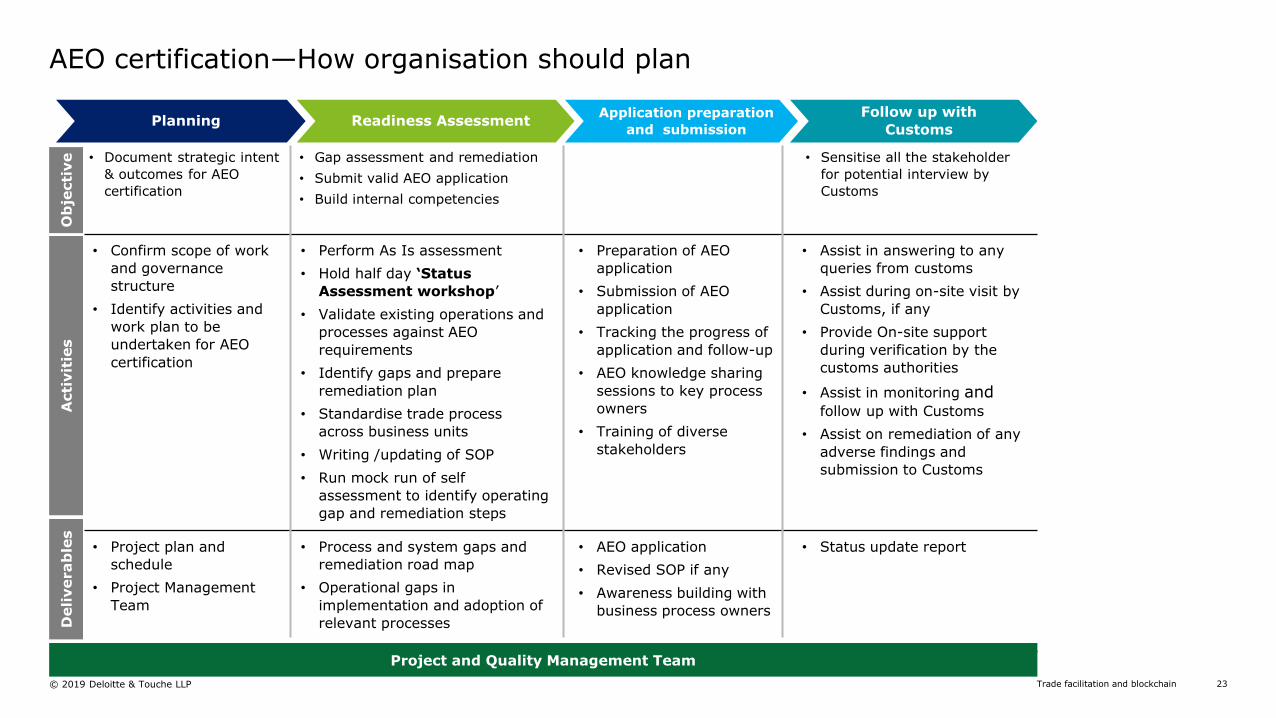

AEO certification—How organisation should plan

• Confirm scope of work

and governance

structure

• Identify activities and

work plan to be

undertaken for AEO

certification

• Perform As Is assessment

• Hold half day ‘Status

Assessment workshop’

• Validate existing operations and

processes against AEO

requirements

• Identify gaps and prepare

remediation plan

• Standardise trade process

across business units

• Writing /updating of SOP

• Run mock run of self

assessment to identify operating

gap and remediation steps

• Preparation of AEO

application

• Submission of AEO

application

• Tracking the progress of

application and follow-up

• AEO knowledge sharing

sessions to key process

owners

• Training of diverse

stakeholders

• Assist in answering to any

queries from customs

• Assist during on-site visit by

Customs, if any

• Provide On-site support

during verification by the

customs authorities

• Assist in monitoring andfollow up with Customs

• Assist on remediation of any

adverse findings and

submission to Customs

• Project plan and

schedule

• Project Management

Team

• Process and system gaps and

remediation road map

• Operational gaps in

implementation and adoption of

relevant processes

• AEO application

• Revised SOP if any

• Awareness building with

business process owners

• Status update report

• Document strategic intent

& outcomes for AEO

certification

• Gap assessment and remediation

• Submit valid AEO application

• Build internal competencies

• Sensitise all the stakeholder

for potential interview by

Customs

Project and Quality Management Team

Acti

vit

ies

Ob

jecti

ve

Deli

verab

les

Readiness AssessmentPlanning Follow up with

Customs

Application preparation

and submission

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 24

World Customs organisation(WCO)/WTO nudge for transparency in trade data flow

Driving harmonisation

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 25

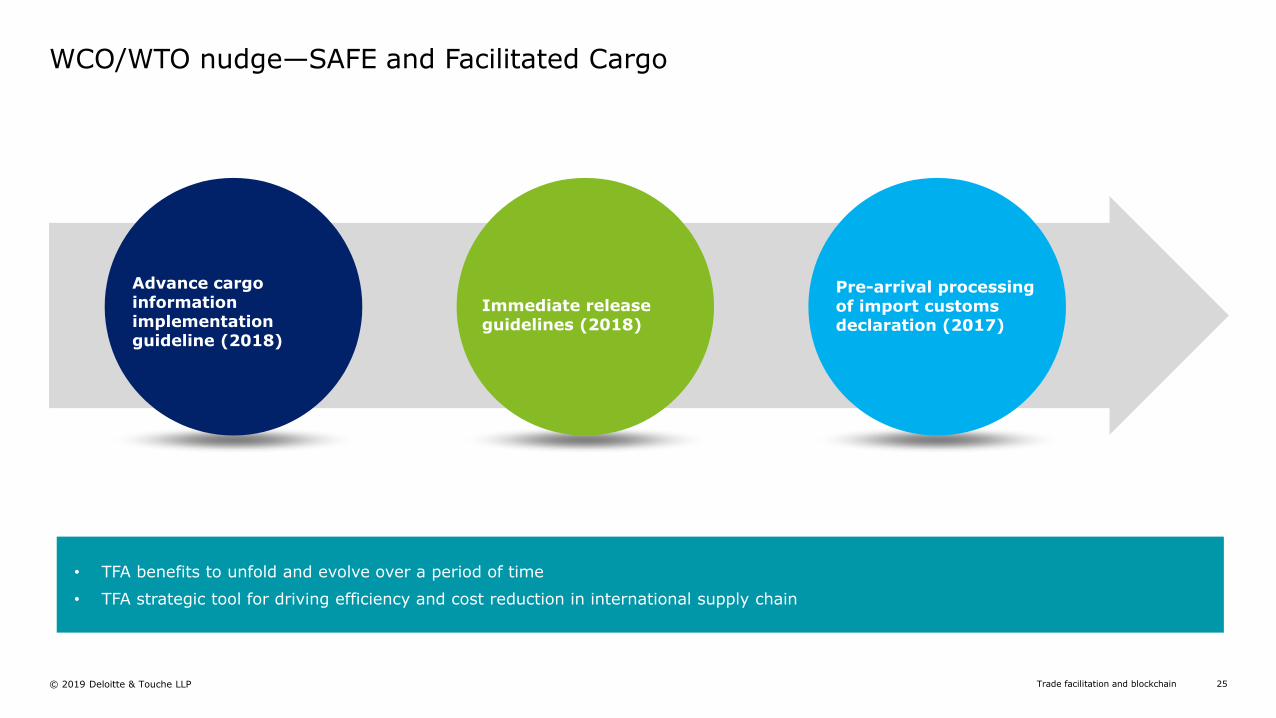

WCO/WTO nudge—SAFE and Facilitated Cargo

• TFA benefits to unfold and evolve over a period of time

• TFA strategic tool for driving efficiency and cost reduction in international supply chain

Immediate release guidelines (2018)

Pre-arrival processing of import customs declaration (2017)

Advance cargo information implementation guideline (2018)

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 26

• Invoice

• Packing list

• Buyer / Sellers

• Terms of supply

Commercial data

• Classification

• Valuation

• Licensing / controls

• Country of origin

Customs dataDeparture/Arrival

manifest

• Commercial data

• Shipping data

• Customs data

• Other data

• Port of loading / discharge

• Date of departure / arrival

• Shipping details

Shipping data

Risk assessment and pre-arrival

Trade data flow—Single pipeline, multiple stakeholders

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 27

WCO Guidelines—Advance Cargo Information (ACI)

Information from Bill of Lading

• Process flow of ACI data set and Customs decision making detailed in the next slide

• ACI paves the way for smarter border controls-reduced inspections, storage and time delay related costs. Business to provide quality data for ACI and Customs

• ACI is an aid to deliver the vision of WCO SAFE Framework

• ACI data set can help to identify high-risk cargo prior to loading and/or arrival.

• ACI allows Customs intervention prior to loading / arrival.

• Customs Risk management system analyses ACI data set to categorise shipments as document, non-dutiable, low value and high value

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 28

Interdiction before departure or arrival

WCO Advance Cargo Information (ACI)—Typical workflow

Port of Origin

Carrier files ACI-

data drawn from Bill

of Lading

Containers marked

with? Do not Load?

Message is

segregated

Containers cleared

from Risk are loaded

on vessel for port of

destination

Carrier may amend

ACI data submitted

Carrier files Arrival

notification

Customs receives

ACI Data

Customs conduct

Risk Assessment

If positive risk

found-customs issue

? Control at

discharge?

notification

Custom do not allow

Amendment of ACI,

If container is

selected for

inspection

Carriers presents

the container for

customs inspection

Customs retrieves

risk results

Customs inspects

container wherever

required

Container with Risk

is stored separately,

before a Bill of Entry

is filed by importer

Importer files Bill of

Entry for clearance

of shipment

Cargo inspected

basis the Risk

identified before

release of shipment

to importer

Port of Destination

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 29

Enable immediate release of shipments from customs

WCO—Guidelines on Immediate Release of shipments

Category 4

• High value consignments (full declaration)

Streamline and expedite the handling of the

consignments upon arrival

Category 2

• Low value consignments—no duties (De-

minimus)

Category 1

• Correspondence and documents (Documents)

Facilitate the pre-arrival processing and risk management

based on advance cargo information

Categorisation of shipments and immediate release

procedures are same for export and imp[ort

Consignments presented for immediate release

divided into four categories

Category 3

• Low value dutiable consignments (simplified

declaration)

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 30

Trade data flow harmonisation

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 31

Enabling facilitation and fraud detection

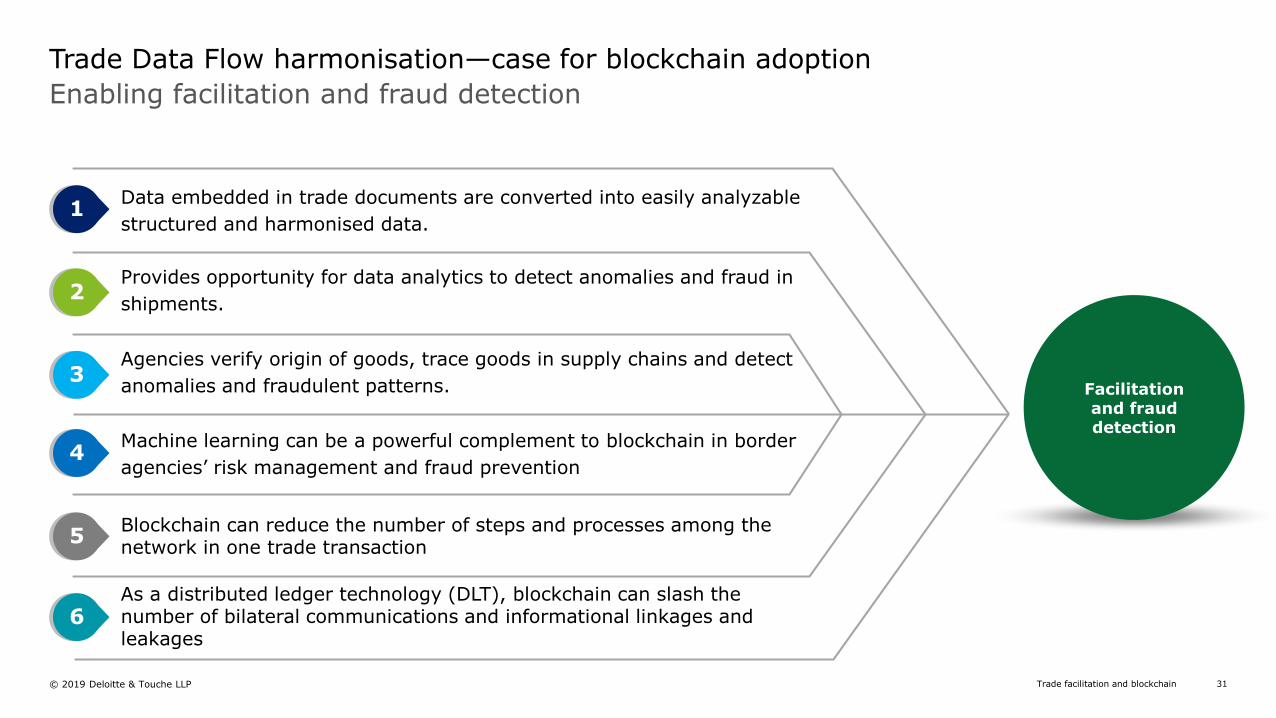

Trade Data Flow harmonisation—case for blockchain adoption

Data embedded in trade documents are converted into easily analyzable

structured and harmonised data.

Provides opportunity for data analytics to detect anomalies and fraud in

shipments.

Agencies verify origin of goods, trace goods in supply chains and detect

anomalies and fraudulent patterns.

Machine learning can be a powerful complement to blockchain in border

agencies’ risk management and fraud prevention

Blockchain can reduce the number of steps and processes among the network in one trade transaction

As a distributed ledger technology (DLT), blockchain can slash the number of bilateral communications and informational linkages and leakages

Facilitation and fraud detection

1

2

3

4

5

6

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 32

ABC

ABC

ABC

ABC

ABC

ABC

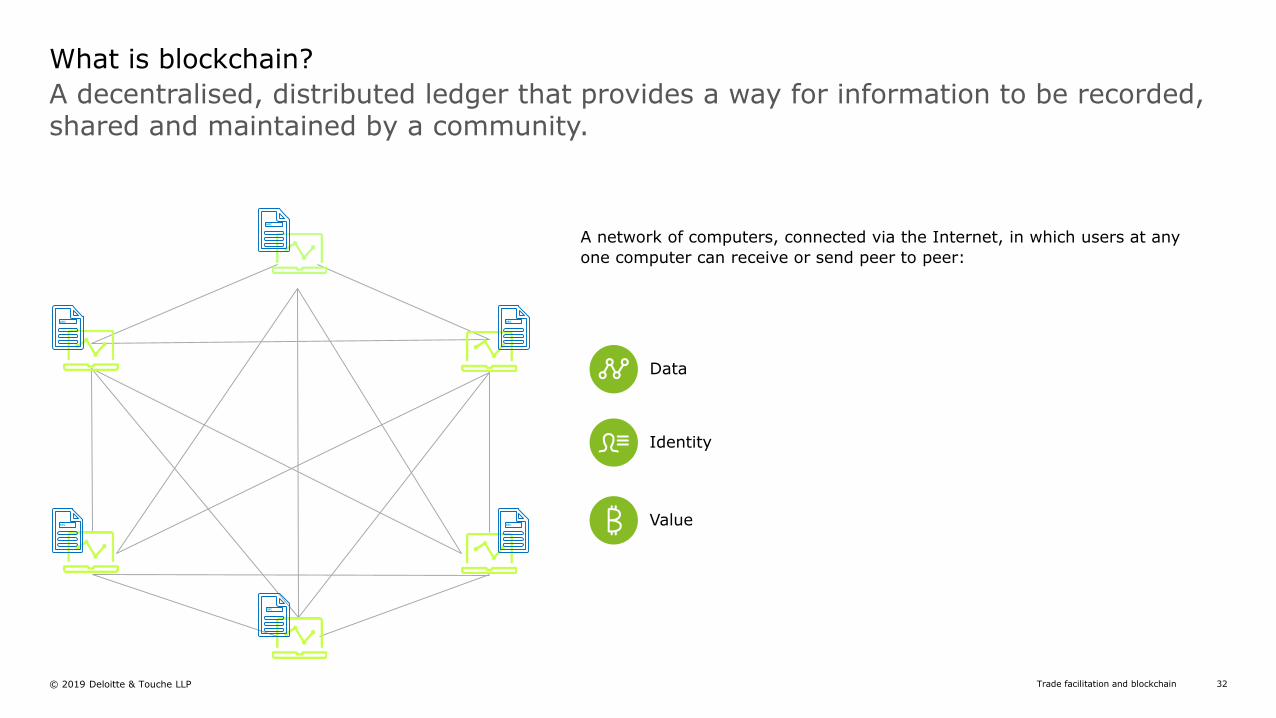

A network of computers, connected via the Internet, in which users at any

one computer can receive or send peer to peer:

Value

Identity

Data

What is blockchain?

A decentralised, distributed ledger that provides a way for information to be recorded, shared and maintained by a community.

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 33

Transactions recorded chronologically and cannot be

changed once added to the chain

For blocks to be added to the blockchain, it must be

achieved through Consensus

############# ##########################

#############

Each block can contain transactions, data and a reference to the previous blockchain (creating the chain)

What is blockchain?

A blockchain is a series of interconnected blocks, with new blocks added on the end of the ever lengthening chain.

Trade facilitation and blockchain© 2019 Deloitte & Touche LLP 34

What is not blockchain?

Common misconceptions about blockchain continue to pose a challenge in enterprise adoption

Blockchain is not an Enterprise Database

• Vast amounts of information that require absolute privacy within a single organisation is meant to be stored in an accessible location for viewing / querying (i.e. an enterprise database)

• Blockchain is designed to record specific transactions meant to be shared across a network of parties with a need for transparency and collaboration

Blockchainsecurity does not mean inherent data privacy

• The identity of the submitter is captured through private-public digital keys but Blockchain’s real secure characteristic is the relationship with all historical blocks in the chain

• This interrelation means that tampering historical data requires altering every subsequent block across every distributed node simultaneously

Blockchain is not Bitcoin

• Bitcoin is a type of cryptocurrency that uses Blockchain cryptography technology to securely record monetary transactions

• Blockchain properties provide the underlying technology that has enabled bitcoin and other cryptocurrencies to rise in popularity

Blockchain is not always public

• A public Blockchain is available for anyone to participate in the consensus process—it is permissionless

• A private Blockchain contains permissions stipulating the ability to view data, add to the chain, and participate in the consensus process

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms and their affiliated entities are legally separate and independent entities. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our network of member firms in more than 150 countries and territories serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 286,000 people make an impact that matters at www.deloitte.com.

Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities provide services in Australia, Brunei Darussalam, Cambodia, East Timor, Federated States of Micronesia, Guam, Indonesia, Japan, Laos, Malaysia, Mongolia, Myanmar, New Zealand, Palau, Papua New Guinea, Singapore, Thailand, The Marshall Islands, The Northern Mariana Islands, The People’s Republic of China (incl. Hong Kong SAR and Macau SAR), The Philippines and Vietnam. In each of these, operations are conducted by separate and independent legal entities.

About Deloitte SingaporeIn Singapore, services are provided by Deloitte & Touche LLP and its subsidiaries and affiliates.

Deloitte & Touche LLP (Unique entity number: T08LL0721A) is an accounting limited liability partnership registered in Singapore under the Limited Liability Partnerships Act (Chapter 163A).

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2019 Deloitte & Touche LLP