top health care regulatory trends: new risks and opportunities

TRANSCRIPT

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. ebglaw.com

Top Health Care Regulatory Trends -New Risks and Opportunities

Lynn Shapiro Snyder

Ted Kennedy, Jr.

Oppenheimer ConferenceDecember 9, 2015

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Disclosures

The information herein is provided for informational purposes only. It is notintended to be, nor should it be relied upon in any way, as investment adviceto any individual person, corporation, or other entity. This information shouldnot be considered a recommendation or advice with respect to any particularstocks, bonds, or securities or any particular industry sectors and makes norecommendation whatsoever as to the purchase, sale, or exchange ofsecurities and investments. Any reference to any specific products, process, orservice does not necessarily constitute or imply its endorsement,recommendation, or favoring by Epstein Becker & Green, P.C. (“EBG”).

2

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Presented by

Lynn Shapiro Snyder

Senior Member of the Firm,Epstein Becker & Green

202-861-1806

Ted Kennedy, Jr.

Member of the Firm,Epstein Becker & Green

203-326-7426

Founder and President, WomenBusiness Leaders of the U.S. HealthCare Industry Foundation

www.wbl.org

State Senator

Connecticut General Assembly

3

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 4

• Epstein Becker & Green – EBG is a boutique

national health law firm with over 250 attorneys in 12offices across the country. EBG was established in 1973 toserve the health care industry and was at the forefront ofmanaged care. EBG has stayed at the forefront ofdevelopments in health care law and continues to helpclients in all segments of the health care and life sciencesindustry. http://www.ebglaw.com

• EBG Advisors – EBG Advisors is a network of

international attorneys, policy analysts, strategists andother professionals who specialize in providingcoordinated guidance and solutions across varioussegments of the health care and life sciences industry.http://www.ebgadvisors.com

• National Health Advisors – NHA is a

consultancy dedicated to the provision of legislative andregulatory advocacy.http://www.nationalhealthadvisors.com

LEGAL SERVICES | STRATEGY| CONSULTING | COMPLIANCE | ADVOCACY

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 5

Elections Matter

NOVEMBER 2017 ELECTION

OMBDOJCMS

FDAIRS

DOL

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Agenda

6

I. Payer Trends – Under 65; Medicaid; Medicare

II. Mental Health Parity

III. Pricing Pressures

IV. CMS/Private Payers – Hot Topics and Trends

V. FDA – Hot Topics and Trends

VI. Looking Ahead

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

PROJECTED SOURCE OF INSURANCE COVERAGE, YEAR 2023

ESI162 M58%

Medicaid40 M14%

Nongroupand OtherCoverage

28 M10%

Uninsured52 M18%

ESI155 M55%

Medicaid54 M19%

Nongroupand OtherCoverage

24 M8%

Exchanges(PrivatePlans)22 M8%

Uninsured27 M10%

Among 282 million people UNDER AGE 65

Without PPACA With PPACA

•Note: ESI is Employer-Sponsored Insurance•Note: It is yet to be determined what the ultimate sources of coverage might be since the Supreme Court gave statesdiscretion on whether to implement Medicaid expansion•Source: Congressional Budget Office, “Effects of the Affordable Care Act on Health Insurance Coverage—March 2015Baseline” (Mar. 9, 2015), available at http://www.cbo.gov/publication/43900.

7

I. Payer Trends

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

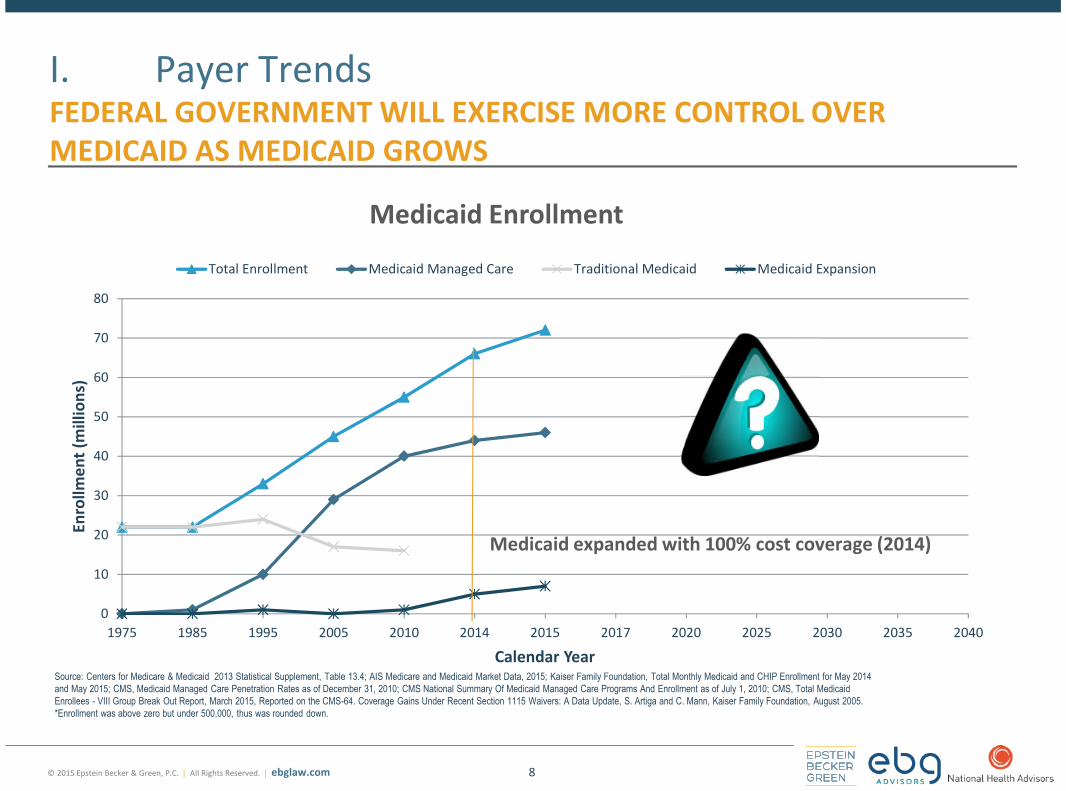

I. Payer TrendsFEDERAL GOVERNMENT WILL EXERCISE MORE CONTROL OVERMEDICAID AS MEDICAID GROWS

8

0

10

20

30

40

50

60

70

80

1975 1985 1995 2005 2010 2014 2015 2017 2020 2025 2030 2035 2040

Enro

llme

nt

(mill

ion

s)

Calendar Year

Total Enrollment Medicaid Managed Care Traditional Medicaid Medicaid Expansion

Medicaid expanded with 100% cost coverage (2014)

Source: Centers for Medicare & Medicaid 2013 Statistical Supplement, Table 13.4; AIS Medicare and Medicaid Market Data, 2015; Kaiser Family Foundation, Total Monthly Medicaid and CHIP Enrollment for May 2014and May 2015; CMS, Medicaid Managed Care Penetration Rates as of December 31, 2010; CMS National Summary Of Medicaid Managed Care Programs And Enrollment as of July 1, 2010; CMS, Total MedicaidEnrollees - VIII Group Break Out Report, March 2015, Reported on the CMS-64. Coverage Gains Under Recent Section 1115 Waivers: A Data Update, S. Artiga and C. Mann, Kaiser Family Foundation, August 2005.*Enrollment was above zero but under 500,000, thus was rounded down.

Medicaid Enrollment

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

I. Payer TrendsOVER 65 POPULATION – SOURCE OF COVERAGE

9

Key fact: Former President George W. Bush’s birthday: July 6, 1946 & Former President Bill Clinton’s birthday: August 19,1946

Note: Enrollment numbers are based on Part A enrollment only. Beneficiaries enrolled only in Part B are not included.Source: CMS Office of the Actuary. 2014

20.39828.433

34.25139.688

47.72

64.471

82.00589.666 93.368

99.907107.454

114.244121.248

0

20

40

60

80

100

120

140

1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2089

En

rollm

ent(

inM

illio

ns)

Calendar Year

Actual and Projected Medicare Enrollment

Bush/Clinton turn 65 People born in 1956 and die at age80 (average life expectancy)

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 10

I. Payer TrendsINNOVATIVE HYBRID MEDICARE PROGRAM LEADS TO INCREASEDINTEGRATION AND COLLABORATION

10

Original Medicare Medicare Advantage

Innovative HybridMedicare Program

• A La Carte Medicare• “Bill Payer”• “Public Plan”

• Utilization Management• Disease Management• Episodes of Care• Bundle of Owned Services• Bundle of Network Services• Pay for Performance• Customization

• Managed Care• “Consumer Protection”• “Outsourcing

Public/PrivatePartnership”

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

The Mental Health Parity and Addiction Equity Act (MHPAEA) requiresinsurers that offer mental health and substance use disorder benefits toprovide those benefits in no more restrictive way than other coveredmedical.• The New York State Attorney General has entered into settlement agreements with multiple

health insurance plans that were found to have violated the MHPAEA. (Fifth settlementannounced in March 2015.)

• EBG Advisors has a free webinar available that addresses the challenges and rewards ofintegrating behavioral health into primary care.http://www.ebgadvisors.com/complimentary-webinar-addresses-challenges-rewards-integrating-behavioral-health-primary-care/

• Look for expansion into developmental disability care.

The days of separating mental health and physical health are OVER.

But, what is “parity” and when will additional regulations be published?

II. Mental Health ParityMENTAL HEALTH PARITY LAWS FINALLY MERGE

11

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

III. Pricing Pressures

Government• Entitlements Effect

• Deficit Reduction

• Debt Ceiling

Commercial• Cadillac Tax

• 10% Rule

• Federal Department of Insurance

Payers – Providers – Pharmaceutical and Device Firms

Is your company part of the problem or part of the solution?

Even with increasing demand, will your company have attractive margins?

12

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 13

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

Pricing Pressure • Healthier Populationto Reduce Costs

• Other CostsReduction Initiativesat the Insurer,Provider, andPharm/Device Levels

• Premium Level – Competitionfor coverage inside thepremium; additional wellnessspending; narrow networks;integration; risk transfers

• Provider Level – Integration;collaboration; outsourcing(staffing, back office, etc.)

• Pharmaceutical / Device Level –Outsourcing functions(engineering, manufacturing,testing); compliance supportvendors

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 14

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

Government as theDominant Purchaser

Greater ComplianceResources to ReduceRisk

• Firms that outsourcecompliance functions

• Firms that monitor for updatesand advocacy

• Firms that perform mock auditsand billing guidance

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 15

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

Movement Away fromInpatient Facility-Based Procedures• CMS has removed

knee reconstructionfrom “inpatient onlylist” and addedarthroscopy of joint tolist of ASC coveredsurgical procedures.(Nov. 2015)

Shift Care to LessExpensive Sites ofServices

• Outpatient facilities and ASCs• Home health providers that can

facilitate recovery at home

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 16

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

New PaymentMethods for Value• Mandatory bundle

under theComprehensive Carefor Joint Replacement(CJR) model (Nov2015)

• Bundled Payments forCare Improvement(BPCI) is still ongoing

Metrics and other datacollection and analyticsservices to assure thatvalue payments createadequate margins andavoid losses

• Vendors that help providersadopt and manage pay for valuecompensation systems andassume risk

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 17

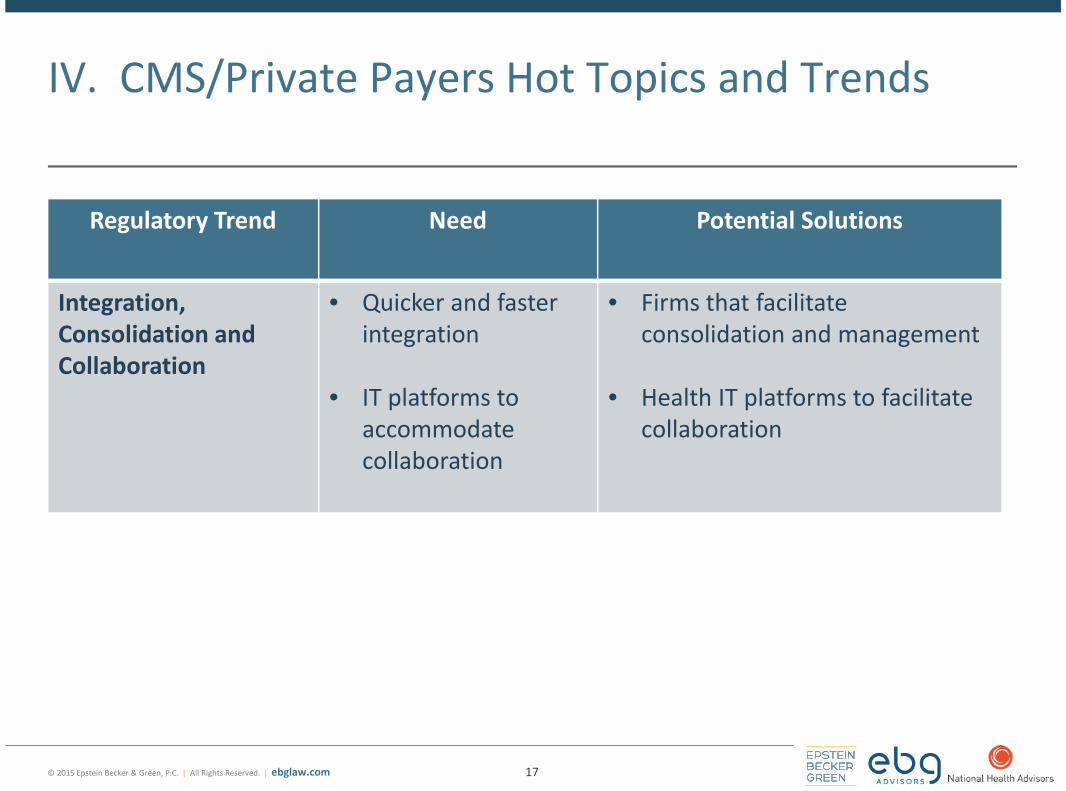

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

Integration,Consolidation andCollaboration

• Quicker and fasterintegration

• IT platforms toaccommodatecollaboration

• Firms that facilitateconsolidation and management

• Health IT platforms to facilitatecollaboration

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 18

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

Mental Health Parity Payer compliance

More providersintegrating mentalhealth services

• Telehealth• Psychiatric nursing• Outpatient programs• Residential treatment• Vendors that offer services and

products to help plans integratethe benefit offerings

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 19

IV. CMS/Private Payers Hot Topics and Trends

Regulatory Trend Need Potential Solutions

Shortage of HealthProfessionals forChangingDemographics

• More healthprofessionals

• Each healthprofessional topractice theirprofession at thehighest level of theirlicense

• Staffing companies• Companies that support

licensed professionals(accreditation, continuingeducation, initial training forlicensed and unlicensedworkers, ongoing onlinetraining)

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

New FDA Guidance

• Mobile Medical Applications (Feb. 2015)

• Clinical Decision Support Guidance (Scheduled for this year)

Potential Legislation to Limit FDA Regulation of Certain Health Software

• The SOFTWARE Act (H.R.2396)

• The MEDTECH Act (S.1101)

Will FDA continue to take an innovator-friendly approach to regulation?

How heavily will FDA regulate in the Clinical Decision Support Guidance?

Will Congress take the ball out of FDA’s hands for some software?

How will mobile health affect regulation & innovation in pharma?

• Pharma is starting to pair “mobile apps” with drugs to improve patient outcomes– new territory for FDA

V. FDA Hot Topics and TrendsFDA REGULATION OF MOBILE HEALTH

20

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Still a lot of work being done on the policy development and application side

EBG Coalitions

V. FDA Hot Topics and TrendsFDA REGULATION OF MOBILE HEALTH

21

mHealth Coalitionhttp://mhealthregulatorycoalition.org/

The Coalition’s purpose is to serve as athought leader in the mHealth ecosystem toprovide its expertise on what mHealthtechnologies should be regulated and howthey should be regulated.

Clinical Decision Support Coalitionhttp://cdscoalition.org

The Coalition’s mission is to ensure thatclinical decision-making software does notbecome overregulated while still ensuringpatient safety and enabling the advancementof innovative decision support tools thatimprove patient care.

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com 22

V. FDA Hot Topics and Trends

Characteristics LDT IVD

What are they? Diagnostic Tests Diagnostic Tests

Who regulates right now? CMS (under CLIA) FDA (under FDCA)

Who makes them? Clinical Labs Manufacturers

Path to Market? • Validate internally• Start offering the test

• Spends years dealingwith FDA to get approval

On-going Requirements Limited A real pain

Two Broad Categories of Tests• Laboratory Developed Tests (LDT): Developed for in-house

(single lab) use• In Vitro Diagnostics Tests (IVD): Developed to sell to multiple

laboratories

DIAGNOSTIC TESTS

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Will “industry disrupters” lead to greater competition?

• Billions of dollars at stake

• Most high value genetic tests, advanced diagnostics for cancer, etc. are LDTs

• Many large and small labs rely heavily on LDTs for revenue

Will FDA move forward with its LDT regulation proposal?

Will Congress step in?

• Congress is weighing several options for LDT regulation

• Some would also change FDA regulation of IVDs (tests FDA currently regulates)

How would FDA regulation of LDTs affect IVD companies?

• Labs that make LDTs are both competitors and customers of IVD companies

• LDT regulation takes away labs’ competitive advantage, but could also changes labs’ business

models and affect how they buy products from IVD companies

V. FDA Hot Topics and TrendsLAB DEVELOPED TESTS (LDT)

23

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

V. FDA Hot Topics and Trends

Changing the paradigm for “lab” testing

• Old way: Collect a patient sample, send to a lab, and waits days/weeks for results

• New way: Test in the exam room or clinic, get results, and treat right away

FDA regulation of Point-of-Care Tests creates a big barrier to innovation

• Standards being applied are biased against point of care

• Standards don’t give due consideration to its benefits to patients

Huge market potential exists if we can fix regulatory problems

• Huge demand and large customer base for products if we can get them to market

Change may be coming in the next few years

• Great response from Capitol Hill (bills are pending calling for review of standards),and dialogue with FDA continues

24

CLIA Waiver Coalition(www.cliawaiverreform.org)

EBG launched the CLIA Waiver Coalition last year: anindustry-public interest group coalition advocating forpoint-of-care reforms.

POINT OF CARE TESTING

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

All of these areas tie into Personalized Medicine• The Holy Grail of medical care – treatment is personalized to every

individual patient, giving them the best health care

Will the federal government price personalized medicine productsand services at the marginal cost or will the government allow higherprices due to the significant research and development costs?

Will companies be able to adequately acquire, store, and use the vastquantity of data needed to develop effective personalized medicineproducts?

How will the FDA regulate these products in the future? WillCongress pass laws implicating personalized medicine research andpricing?

Will providers embrace and advocate for personalized medicine?

V. FDA Hot Topics and TrendsPERSONALIZED MEDICINE

25

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

VI. Looking Ahead – Cadillac Tax

Will Congress eliminate or amend the Cadillac Tax?

Pressure from employers

Pressure from unions

26

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

VI. Looking Ahead – Drug Prices

Will Congress regulate drug prices?• Bipartisan concerns about recent spike in drug prices (hearings,

investigations)

Various proposals to address drug prices:• Allow Medicare to negotiate drug prices?• Rebates for drugs for low-income beneficiaries?• Re-importation?• Ban pay-for-delay settlements between brands and generics?• Requirement to disclose research costs?• Eliminate tax benefits for consumer drug ads?• Cut the period of exclusivity for biologics to seven years• Cap out of pocket costs in drug plans?• Speed up FDA review for certain biosimilars?

Will the private market help solve the problem? (e.g. Express Scripts)

27

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

VI. Looking Ahead – Medicare Advantage

Will insurers offering Medicare Advantage plans continueto see increased payment?

On Dec. 1, 2015, CMS announced that the Medicare fee-for-service baseline rate will increase by 3.1% in 2017. This figure is acomponent of the formula to calculate Medicare Advantagepayments.

28

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

VI. Looking Ahead – Enforcement

False Claims Act and other fraud liability still exists even withpay for value and with Medicare Advantage and MedicaidManaged Care

Increased individual criminal and civil fraud liability due tothe Yates Memo (September 9, 2015)

• A new DOJ initiative designed to combat corporatemisconduct and seek accountability from individuals involvedin suspected corporate wrongdoing

• Board members and executives must remain attuned tocorporate activities

29

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

VI. Looking Ahead – Role of the FederalGovernmentThe government will increasingly be the dominant payer and dominant regulator of health care

goods and services. So, . . .

30

The Political Landscape MattersThe Federal Enforcement Landscape

Matters

Advocacy Risk Management and Compliance

Health care companies should monitor and/or engage in the federal political,regulatory, and enforcement landscapes.

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Visit the www.ebglaw.com website for the various alerts we have published on a widerange of issues related to health reform and the Medicare and Medicaid programs

Our attorneys are active in blogging. For insights, commentary, and conversation on abroad range of topics that affect your business, visit our blogs below.

31

www.healthlawadvisor.com www.techhealthperspectives.com www.pharmamedtechinsights.com

© 2015 Epstein Becker & Green, P.C. | All Rights Reserved. | ebglaw.com

Presented by

Lynn Shapiro Snyder

Senior Member of the Firm,Epstein Becker & Green

202-861-1806

Ted Kennedy, Jr.

Member of the Firm,Epstein Becker & Green

203-326-7426

Founder and President, WomenBusiness Leaders of the U.S. HealthCare Industry Foundation

www.wbl.org

State Senator

Connecticut General Assembly

32

Questions