tom kendall - conference summary - lbma · tom kendall - conference summary credit suisse director...

TRANSCRIPT

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 1

2

Tom Kendall - Conference Summary

Credit Suisse

Director

Head of Precious Metals Research

Securities Research and Analytics

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 2

3

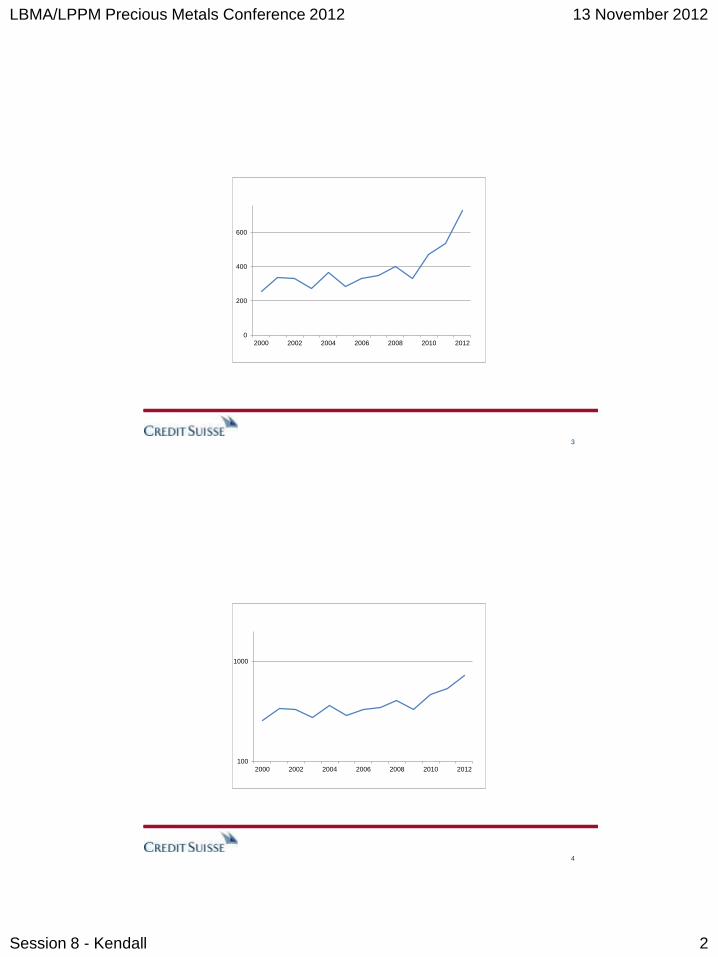

0

200

400

600

2000 2002 2004 2006 2008 2010 2012

4

100

1000

2000 2002 2004 2006 2008 2010 2012

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 3

5

100

1000

2000 2002 2004 2006 2008 2010 2012

LBMA Attendees Gold price

6

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 4

Mission Two Transform from a spot market to a derivative market.

In 2004, SGE successfully launched the deferred trading product.

From 2008, gold deferred trading has accounted for over 60% of

SGE’s gold market for three consecutive years and in 2011, the

percentage rose to 73%.

42.49 470.69 665.3 906.42

1,249.60 1828.13

4463.77 4710.819

6,051.50

37.38 491 795.23 1068.63 1947.51

3164.9

8696.05 10288.76

16,157.81

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

0

1000

2000

3000

4000

5000

6000

7000

2002 2003 2004 2005 2006 2007 2008 2009 2010

Billion Yuan Ton SGE’s Annual Trading Volume and Amount

(vi) Dollar devaluation

Without lowering the debt/GDP ratio to a sustainable level, there will be no real

economic recovery, but

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 5

China’s rebalancing: Rapid falling of current account surplus-to-GDP ratio

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

current account surplus-to-GDP ratio

From 10% to 2.8%, behind Germany now

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 6

22997-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

Real rates are low, the non-dollar price trend is rising

and gold is beating equities

Volatility is low OR Silver is cheap

OR sentiment is weak

Volatility is low AND Silver is cheap

AND sentiment is weak

Volatility is high and

price is overbought

Today

pg 12 pg 12

Gold prices appear to be highly negatively

correlated to real interest rates

As of 31 August 2012

SOURCE: Bloomberg

Refer to the Appendix for additional correlation information.

From Jan '97 to Aug '12

0

1

2

3

4

5

6

7

8

9

-1 0 1 2 3 4 5

Real yield (10-year TIPS)

Real p

rice o

f g

old

(P

rice o

f g

old

/U.S

. C

PI In

dex)

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 7

LBMA Conference Hong Kong 2012: Graham Tuckwell Page

13

Buying a gold ETF: Total cost to an investor – 1 month

trade

European Gold ETFs US Gold ETFs

6

3

1

2

3

3

0 2 4 6 8 10

iShares

ETFS

SPDR

Total Cost (Bid-Offer Spred + 1 Month Total Expense Ratio)

Bid-Offer Spread 1mth TER

23

18

12

7

2

2

2

3

0 5 10 15 20 25

Source

iShares

Deutsche Bank

ETFS

Total Cost (Bid-Offer Spred + 1 Month Total Expense Ratio)

Bid-Offer Spread 1mth TER

14

中国工商银行与世界黄金协会合作

发布了中国第一款以“日均价格积

蓄黄金”的权益凭证式黄金投资产

品 ——“工银金行家·积存金”。

ICBC and World Gold Council

jointly launched Gold

accumulation program which is

the first equity style voucher

based on daily gold price in

China.

中国工商银行典型产品——积存金

Typical products of ICBC——Gold Accumulation Program

2.6 商业银行主要贵金属业务——理财类

Major services of ICBC——Financing

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 8

15

Japan --- Mature and Changing

Market behaviour changed along with gold price.

--- Between 1978 - 1980

Gold trading was liberalized in Japan in 1978.

In 1980, when gold price went up to $850, gold in yen soared close to 7000 yen per gram, which was the

historical high.

--- Between 1980 – 2001

About 20 years until 2001, gold price went down, Japanese trading firms kept on importing , and

Japanese people continued buying.

--- Between 2001 -- Present

Because of “911”, gold price started to soar up. From 2001 for 10 years, Japanese gold market reversed

trading behaviour. Investors’ liquidation on long position made Japan a net gold exporting country.

--- Current observation

We noticed a change this year that much less selling interest out of Japan. We foresee Japan could be a

buying country next year again, as we see younger generations are interested in investing in gold.

--- Speciality

GAP( Gold Accumulation Plan ) is the one biggest vehicle of the gold market in Japan. Estimated to

have around 550,000 to 600,000 accounts. Tanaka has the lion’s share, and over 80%.

--- Exchange

On March 23 1982 TOCOM started trading gold futures and it quickly became a very active market next to

COMEX. From 2008 TOCOM open interest went down as low as 1/5 of peak days and there were no

sign of recovery as now yet.

Topic 3

Part 1

16

C. How to open up Bullion Market in Asia?

Free up gold export;

Introducing gold derivative markets, such as Options and ETF;

Asia Bullion Banks must assist to provide market liquidities;

Looking into gold clearing and custodian services in Asia;

Gold fixing during Asia time zone.

Part 3

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 9

光洋僅供LBMA/ LPPM 年會參考資料禁止複製、轉載、外流│SOLARTECH DOCUMENT. FOR LBMA/LPPM CONF. DO NOT COPY

Taiwan Gold Import Demand (1989-2011)

2012/11/13 17

(Year)

Quantity (ton) Average Annual Demand >100 ton

光洋僅供LBMA/ LPPM 年會參考資料禁止複製、轉載、外流│SOLARTECH DOCUMENT. FOR LBMA/LPPM CONF. DO NOT COPY

Green. Value. Future.

Change for Excellence !

2012/11/13 18

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 10

One Team One Vision With Pride

Future Supply Constraints

1. S.A Mining inflation 2007 – 2012

Electricity - 220%

Diesel - 110%

Steel - 100%

Wages - 75%

2. Productivity 2007 – 2012

– (11.5%)

3. Net speculative Pt. length at near record highs - > 2.0m oz

4. Above ground stocks adequate, but shrinking.

5. The days of cheap migrant labour are over.

6. Increased focus and cost of safety.

New Gitanjali print and TVC

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 11

Title and date 21

Summary

Future PGM demand profile from the aftertreatment sector will probably shift

to a somewhat higher Pt ratio due to new diesel market segments (heavy

duty diesel on road, non road).

In the gasoline sector major increase of PGM loading per car is unlikely.

There is no substitute for PGM on the horizon.

The biggest impact for future PGM demand will come from growth prospects

for the global economy.

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 12

Changing Demographics – To increase saving rate

0

20

40

60

80

100

0-4

5-9

10-1

4

15-1

9

20-2

4

25-2

9

30-3

4

35-3

9

40-4

4

45-4

9

50-5

4

55-5

9

60-6

4

65-6

9

70-7

4

75-7

9

80+

88% of India’s population to be less than 60 years old by 2025E

India’s age profile in 2025E (% of population)

Source: Kotak Institutional Equities estimates

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 13

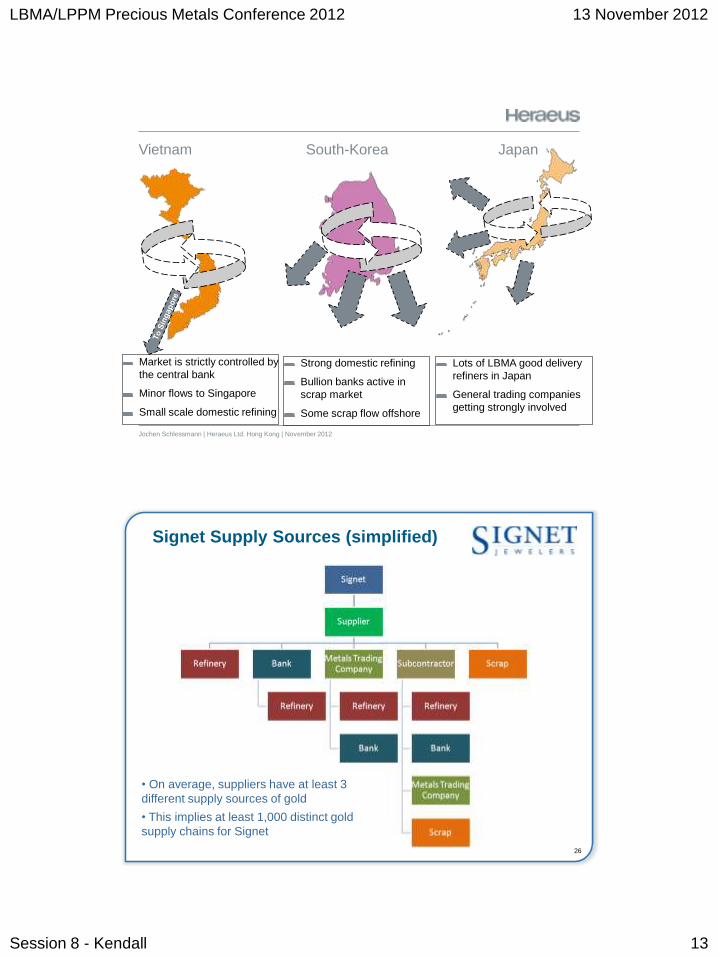

Vietnam South-Korea Japan

Jochen Schlessmann | Heraeus Ltd. Hong Kong | November 2012

Market is strictly controlled by

the central bank

Minor flows to Singapore

Small scale domestic refining

Strong domestic refining

Bullion banks active in

scrap market

Some scrap flow offshore

Lots of LBMA good delivery

refiners in Japan

General trading companies

getting strongly involved

26

Signet Supply Sources (simplified)

• On average, suppliers have at least 3

different supply sources of gold

• This implies at least 1,000 distinct gold

supply chains for Signet

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 14

27

Endowment (Moz)(1)

0

20

40

60

80

100

120

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Discovery Year

Declining Discovery Rates

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

0

20

40

60

80

100

120

140

160

180

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Go

ld a

nd

Co

pp

er-G

old

Exp

lora

tio

n S

pen

din

g (U

S$M

)

End

ow

men

t (M

oz)

Discovery Year

Gold and copper-gold 3 year average

Sources: Metals Economics Group, Intierra and Barrick

Exploration spending

0

1,500

3,000

4,500

6,000

7,500

9,000

0

20

40

60

80

100

120

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Gold

Explo

ration S

pendin

g (

US$M

)

Endow

ment (M

oz)

Discovery Year

Gold Exploration Spending (US$B)

0

1.5

3.0

4.5

6.0

7.5

9.0

Features of China’s Gold Industry

▪ Fast development, unrivalled as World’s largest gold producer

▪ Small size, low grade, mining alongside with exploration, small scale development for large mines

▪ Consolidation is the trend and mainly led by governments

▪ Great potential for deep exploration

▪ Low capital cost

LBMA/LPPM Precious Metals Conference 2012 13 November 2012

Session 8 - Kendall 15

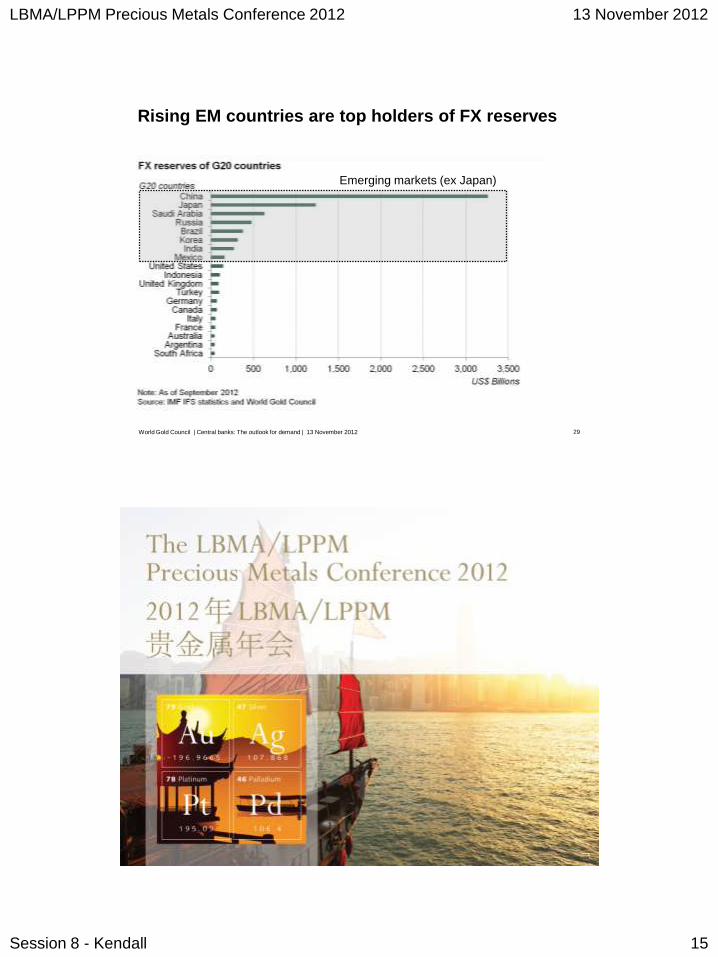

Rising EM countries are top holders of FX reserves

29 World Gold Council | Central banks: The outlook for demand | 13 November 2012

Emerging markets (ex Japan)