today’s lecture - #26 insurance regulation introduction to insurance regulation rationale history...

TRANSCRIPT

Today’s Lecture - #26Insurance Regulation

Introduction to Insurance RegulationRationaleHistoryWhat Regulation Involves

State vs. Federal RegulationInsurance InsolvencyCurrent Problems with Insurance Regulation

Insurance companies are one of the most heavily regulated industries. What is the most important reason to regulate insurers?

A) To prevent deceptive sales practices

B) To make sure they stay solvent

C) To make sure they don’t set rates too high

D) To make sure they don’t discriminate unfairly

E) Some other reason

Why Regulate Insurance?

Market Power

Imperfect Information

Public Policy

Advance Nature of Contract

Insurer gets your money before fulfilling the contract

Brief History of Insurance Regulation

Paul v Virginia - 1869

US v Southeast Underwriters Association (SEUA) - 1944

McCarran Ferguson Act - 1946

You be the Supreme Court JudgeHow would you rule in the SEUA case?A) Uphold Paul v. Virginia:

Insurance is not commerceB) Overrule Paul v. Virginia:

Insurance is commerce and subject to Federal laws

C) Compromise:Insurance is commerce but should not

be subject to Federal laws

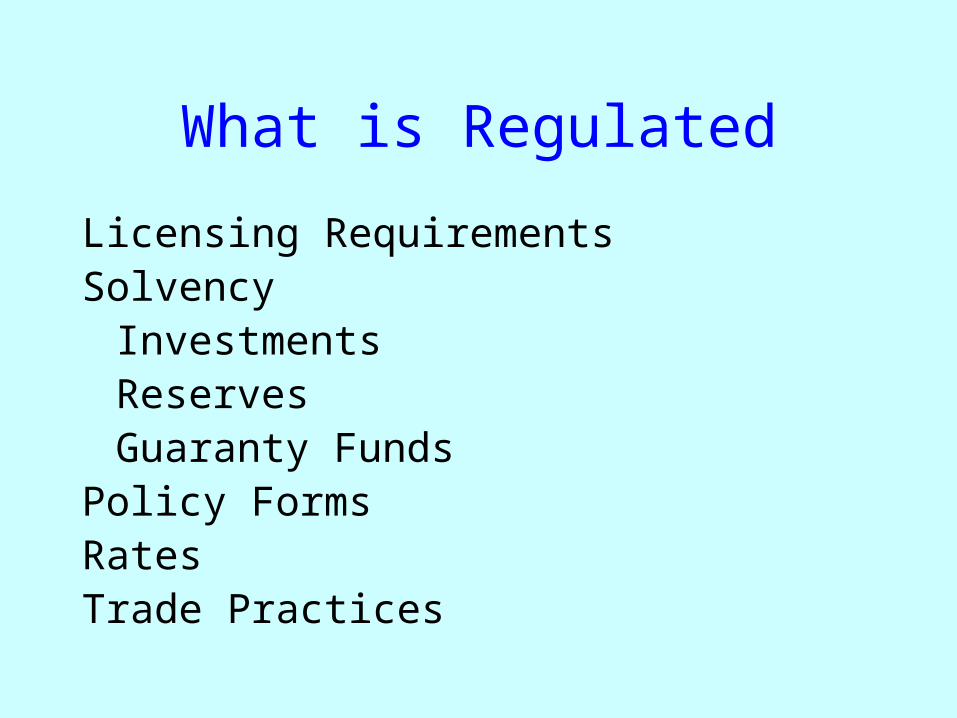

What is Regulated

Licensing RequirementsSolvency

InvestmentsReservesGuaranty Funds

Policy FormsRatesTrade Practices

Rate RegulationGeneral Requirements

Rates must be adequate, not excessive and not unfairly discriminatory

Methods

Prior approval

File and use

Open competition

Classification issues

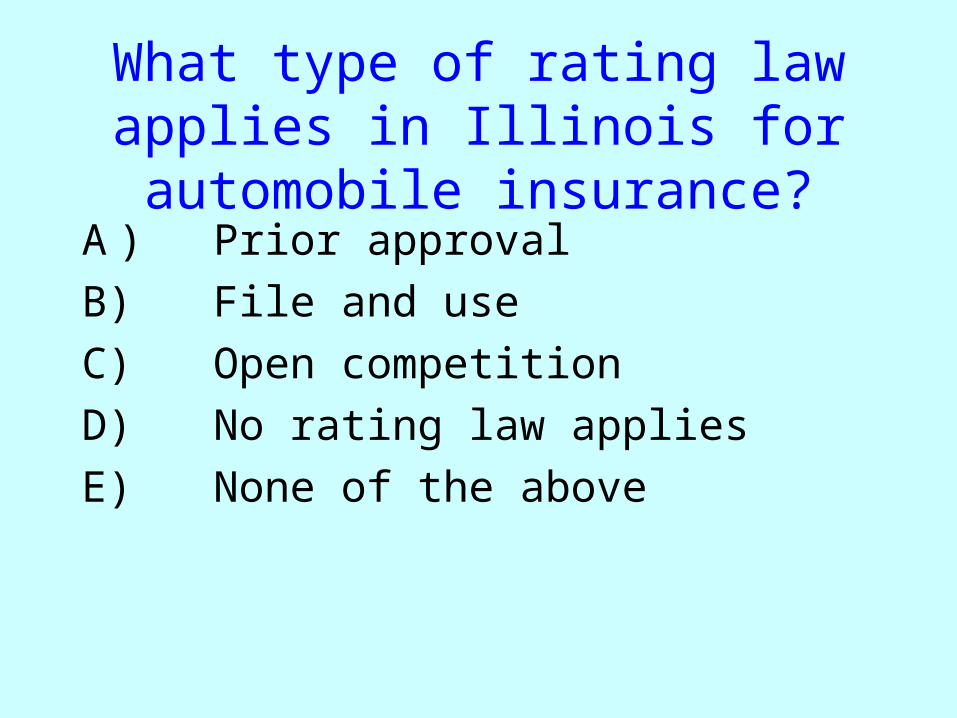

What type of rating law applies in Illinois for automobile insurance?

A) Prior approval

B) File and use

C) Open competition

D) No rating law applies

E) None of the above

Regulation of Trade PracticesAgents must be licensed

Prohibited activities for agents

Twisting

Rebating

Allowed in Florida and California

Effect of agents’ interests

Claim practices

Underwriting practices

General AdviceIf you are having a problem with an insurance company (billing, claims, unjustified cancellation, unfair treatment), contact the insurance department in the state where you live.

In Illinois, contact:Illinois Division of Insurance320 West Washington StreetSpringfield, IL 62767217-782-45151-866-445-5364 (toll free)

or online at:http://www.idfpr.com/DOI/Complaints/Complaints.asp

State vs. Federal Regulation

States Currently Regulate Insurance

Only Major Industry Regulated at State Level

Why?

Tradition

Paul v. Virginia

US v. SEUA - during W.W.II

Led to McCarran-Ferguson Act

Recent Proposals

Repeal of McCarran-Ferguson Act

Would lead to

Federal regulation instead of state

or Dual regulation

State regulation of small insurers

Federal regulation of major insurers

Claimed Advantages of State Regulation

Have Current Knowledge

Recognizes Local Conditions

Encourages Experimentation

Effects of Mistakes are Localized

Claimed Advantages of Federal Regulation

Uniformity

Could get the best regulators

Would be able to deal with large, multinational insurers

Federal Government in Action on Insurance Related Issues

Social SecurityBankrupt by 2040 or earlierPolitical environment prevents informed

discussions and solutionsFederal Savings and Loans Insurance Corporation

(FSLIC) 1934-1989Inadequate regulationPolitical pressure to keep insolvent S&Ls openTaxpayer cost of about $200 billion

Federal Government in Action on Insurance Related Issues - Cont.

Pension Benefit Guaranty Corporation (PBGC)12/31/04 financial position: negative $23.5 billionUnited Airlines termination in May, 2005: $9 billionCovered defined benefit pension plans

Underfunded by $600 billion (termination basis)

National Flood Insurance ProgramExpected cost from Katrina and Rita $22 billionNeed to borrow from Federal government

Cannot repay these loans from future premium income

What Happens When Your Insurer Goes Insolvent

State guaranty funds apply

Limits on coverage

Deductible on premium refunds

Delays in payment

Types of Guaranty FundsNew York

Pre-assessment fund1982 Legislature “appropriated” $87 millionRecently found illegal and forced to return funds

All Other StatesPost-assessment basisLonger delaysLimits on assessments

Lessons from Executive Life and Mutual Benefit

Executive Life

Taken over by California regulators in April, 1991

Company was sold

Policyholders received 70-80% of their benefits

Mutual Benefit

Taken over by New Jersey regulators in July, 1991

Withdrawals restricted until 1999

Significant penalties applied to withdrawals

Credited interest rates lowered below contract level

Basic Lessons

If a company is too big, then regulators will intervene and re-write the contracts rather than declare insolvency.

Current Problem Areas in Insurance

Complex product

Insolvencies

Rising costs of liability insurance

Lack of availability of property coverage in coastal areas

Irresponsible regulation

California - Proposition 103

New Jersey - Residual Auto Market ($3 billion in debt)

Current Problem Areas in Insurance

Crooked regulators – LouisianaSherman Bernard - Commissioner 1972-1988

Convicted of taking payoffs – sentenced to 41 months in prison

Douglas Green - Commissioner 1988-91Convicted of fraud, money laundering and bribery - served 12 years in federal prison

Jim Brown – Commissioner 1991-2002Convicted of lying to the FBI – sentenced to 6 months in prison

ConclusionsInsurance does need to be regulated

Current regulation is excessive and misdirected

Focus of regulation should be on solvency

Challenges presented by new financial instruments

Understanding derivatives

Dealing with international transactions

Hedging interest rate and similar risks

Expanding use of modeling

Need for competent, ethical regulators