thursday, december 8, 2011, at 2:00 est moderated by ...€¦ · moderated by pattie mastin,...

TRANSCRIPT

Tips for Managing Delinquencies

Thursday, December 8, 2011, at 2:00 EST

Moderated by

Pattie Mastin, Account Manager

WELCOME

AGENDA

Defaulted Loans with Campus Partners Past Due Account Processing Reporting Features Past Due Notifications

Services Designed to Manage Delinquencies Q&A

What is Default? A loan is considered “in default” when the borrower fails to make an installment payment when it is due or comply with other terms of the promissory note or written payment agreement.

True Default vs. Cohort Default

Defaulted Loans with Campus Partners: Loans that are considered past due have a status code of 49. A letter following this code will indicate the collection agency status. C = in collection R = returned or recalled E = eligible for collection, manual placement W = withheld from collections

Past Due Loans Reports: •Past Due Loans Report –

an aging report of past due loans, not including loans in collection or loans in exception billing

•Exception and Special Billing Report – a listing of loans in Special Billing or, in Deferment, because of Hardship or Customer Adjustments

•IRS Skip Tracing Report –

a listing of borrowers who meet the IRS Skip Tracing Guidelines

•Rehabilitation Monitoring Report – a listing of borrowers who are currently in a rehabilitation status, loans that have dropped from rehabilitation, and borrower that have completed rehabilitation

Past Due Loans Reports, cont.:

•Borrowers to Receive a Notice Report (Optional) – a listing of borrowers who must be sent a notice; the customer selects the age break(s)

•Loans Brought Current (Optional) – a report of loans that became current during the reporting period

•Loan Monitoring Report (Optional) –

this is a list of loans coded for monitoring at the request of the customer

Past Due Notifications: Campus Partners performs past-due follow-up that is consistent with federal regulations and school requirements. Standard past-due contacts:

•15-Day Past-Due Notice •45-Day Past-Due Notice •60-Day Final Demand Letter •90-Day Collections Telephone Contact

**Automatic acceleration can be provided; with verbiage included in the 60-Day Final Demand Letter. If the account is not brought current, the entire unpaid principal balance, accrued interest, late charges and other delinquent fees become due and payable.**

Past Due Notifications: •Past due follow-up performed by Campus Partners is fully documented in the borrower’s permanent loan history

•Each telephone contact or attempts made by Campus Partners is documented providing the date, time, and borrower’s comments.

**3 attempts, at different times, made over a 3 day period.**

Sample 15-Day Past-Due Notification -

Sample 45-Day Past-Due Notification -

Sample 60-Day Final Demand Letter -

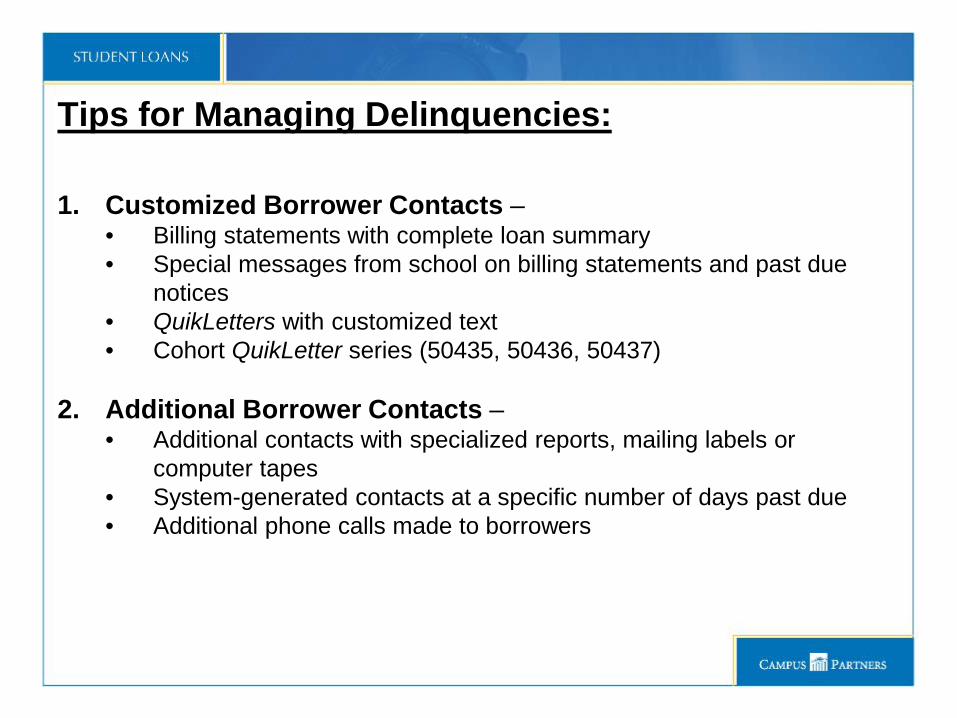

Tips for Managing Delinquencies: 1. Customized Borrower Contacts –

• Billing statements with complete loan summary • Special messages from school on billing statements and past due

notices • QuikLetters with customized text • Cohort QuikLetter series (50435, 50436, 50437)

2. Additional Borrower Contacts – • Additional contacts with specialized reports, mailing labels or

computer tapes • System-generated contacts at a specific number of days past due • Additional phone calls made to borrowers

Tips for Managing Delinquencies, cont.: 3. Exit/E-Exit Interviews –

• Regulations require that schools conduct exit interview with borrowers before they leave school. • The borrower must be informed of the terms of the loan and the

benefits associated with the loan.

• Exit Interviews with Campus Partners – paper and on-line exits • Automated • Notification to Customer Service Representative • System III – XPKG • E-Exit (through mycampusloan.com)

Tips for Managing Delinquencies, cont.: 4. Forbearance –

• Available to borrowers for a period of 3 years • Interest continues to accrue

PERKINS REGULATION: Section 674.33(d) – Forbearance – has been amended to eliminate the

requirement that a borrower make a “written” request in order to obtain a forbearance on his or her Perkins Loan. It does not, however, eliminate the requirement of supporting documentation.

Tips for Managing Delinquencies, cont.: 5. Unemployment and Economic Hardship Deferments –

• 1998 Reauthorization added provision for unemployment and economic hardships for a period of 3 years (request period must be on or after October 7, 1998)

• Principal and interest are deferred Economic Hardship (Section 674.34 amended - effective October 1, 2007) - The

definition of economic hardship has been revised to read: (e)(3)(ii) – “an amount equal to 150% of the poverty line applicable to the borrower’s family size, as determined in accordance with section 673(2) of the Community Service Block Grant Act.

Hardship Deferment (available on loans made before 7/1/93) - Borrowers who are

temporarily unable to make their regular payments may receive a hardship deferment; principal is deferred and interest continues to accrue. There are two unique options: • Billing interest during the deferment period to maintain contact with the borrower and

to avoid a large lump-sum payment at the end or bill for interest at the end of the deferment;

• Automatic scheduling of the remaining balance at the end of the deferment to ensure repayment of the loan within the term of the note

Tips for Managing Delinquencies, cont.: 6. Extension of Repayment Period (eligible on all loans) -

• Perkins regulations published in the Federal Register of November 30, 1994, provide for an extension of the repayment period due to prolonged illness or unemployment

7. Customer Adjustments –

• To provide customers with a means to remove bills or to prevent bills from accruing • Customer Adjustment allows a break in the repayment period that is not covered by

any loan regulations; works like a deferment, with a beginning and ending date. • Allows system to automatically reprocess a loan since all periods of time are

accounted for • Used only in emergency situations. These are not deferments authorized on federal

loans.

8. Judgment Loans – • Loans with court-ordered judgment that allows for special payment

arrangements based on that judgment. • CSR to code judgment flag • Increase the interest rate as approved by the courts and apply any attorney

fees as applicable.

Tips for Managing Delinquencies, cont.: 9. AutoDraft –

• Offers borrowers convenient way to repay loan; ensures timely payments; provides a more consistent cash flow for school

• Option available to borrowers through mycampusloan.com • AutoDraft information is mailed to borrowers by Campus Partners in

their early bill

10. E-Bill – • Borrowers may elect to receive E-Bill notice • Borrowers sign up for services via mycampusloan.com • Campus Partners send email notification that instructs borrower to

view their billing statement on-line

Tips for Managing Delinquencies, cont.: 11. Special Billing –

• Temporarily bill a borrower an amount larger or smaller than the regular repayment scheduled

• The system can calculate the amount necessary to bring the loans current, or you may bill the borrower for any amount during the special billing period.

12. Rehabilitation –

• Effective July 1, 2000, rehabilitation became available to Perkins borrowers

• One-time benefit that enables borrowers to erase past negative credit history

PERKINS REGUALTION: Section 674.39(a)(2) – Loan rehabilitation – Changes the number of

consecutive on-time, monthly payments a borrower must make to successfully rehabilitate a defaulted Perkins Loan from 12 to 9

Tips for Managing Delinquencies, cont.: 13. Automatic Assessment of Late Charges –

• Assessment of late charges if no longer mandatory on Federal Perkins; however schools may assess late charges on past due installments

• Encourages timely payments; schools are reimbursed for expense required for additional billing procedures

14. Credit Bureau Reporting –

• Excellent deterrent to delinquency • Required for all federal loans • Automatic reporting to all three major credit bureaus

15. Skip Tracing –

• Good addresses for mailing bills and notices is vital to the prevention of delinquencies

• Storage of borrower’s primary, billing and up to three secondary addresses

• Basic Skip Tracing vs. Enhanced Skip Tracing

Tips for Managing Delinquencies, cont.:

16. Early Intervention Program: • EIP is a service designed to prevent borrowers from entering into

default. • In addition to the standard due diligence, EIP provides a series of

specialized letters and phone contacts to borrowers who are 15 to 105 days past due on their loan payments.

• The objective of these contacts is to reach the borrower and return their account to a current status.

• Many benefits available through EIP: • Experienced counselors • Multiple Payment Efforts • Intensive telephone and mail campaign • Skip tracing services

Early Intervention Schedule of Activity: EARLY INTERVENTION PROGRAM

Early Intervention Program activities are performed based on the following schedule:

# DAYS PAST DUE CONTACT ACTIVITY DESCRIPTION

15-29 Borrower Counseling Phone Call

Contact Borrower by phone - Offer Pay by Phone and AutoDraft - Review available deferments - Discuss payment options

30 Borrower Collection Letter Specialized final past due bill

30-44 Borrower Counseling Phone Call

Contact Borrower by phone - Offer Pay by Phone and AutoDraft - Review available deferments - Discuss payment options

45-49 Borrower Counseling Phone Call

Contact Borrower by phone - Offer Pay by Phone and AutoDraft - Review available deferments - Discuss payment options

50 Borrower Collection Letter Specialized 50-day bill

60-74 Borrower Counseling Phone Call

Contact Borrower by phone - Offer Pay by Phone and AutoDraft - Review available deferments - Discuss payment options

75 Borrower Collection Letter Specialized 75-day bill

75-90 Borrower Counseling Phone Call

Contact Borrower by phone - Offer Pay by Phone and AutoDraft - Review available deferments - Discuss payment options

105 Borrower Final Past Due Notice Specialized final past due bill

QUESTIONS?

Thank you for joining us!

Should you have questions or need additional training, please contact Pattie Mastin at

[email protected] or call 800-458-4492 Ext. 2011