three global developments and a look at new zealand

TRANSCRIPT

www.centreforavia-on.com

CAPA-ACTENewZealandSummit,17-Oct-2017

PeterHarbisonExecu-veChairman,CAPA–CentreforAvia-on

ThreeglobaldevelopmentsandalookatNewZealand

www.centreforavia-on.com

SirTimClark,EmiratesPresidentandCEO:A“gatheringstorm”forairlines.“Thisisgoingtocomeandweneedtobereadytodealwithit.”“Nowyou’reseeingScoot,NorwegianandAirAsiaXcomingalong.Ithinkwe’reseeingthebeginningsofaninflec-onpoint,”

AkbaralBaker,QatarAirwaysCEO:“Maybelong-haullow-costwillworkwhenthefuelpriceis30dollarsabarrel.Butonceitgoesbeyond50dollarsIguaranteeitisnotfeasible.”

WillieWalsh,IAGCEOLonghaullowcostflightswillbecomea“significantpartofIAG.”

1. Are long haul low cost airlines sustainable?

www.centreforavia-on.com

2012 2013 2014 2015 2016 2017

180%

160%

140%

120%

100%

80%

60%

40%

20%

0%

-20%

-40%

Long Haul LCC Non-LCC Non-LCC * Gulf carriers ~ 2012 2.6% 97.4% 84.0% 13.4% 2013 3.0% 97.0% 82.0% 15.0% 2014 3.6% 96.4% 80.4% 16.0% 2015 4.0% 96.0% 78.5% 17.5% 2016 4.6% 95.4% 76.9% 18.5% 2017 5.1% 94.9% 76.9% 18.1%

Market Share

Seat Growth

Seats

Long Haul LCC Non-LCC Non-LCC * Gulf carriers ~ 2012 9.7m 368.2m 317.6m 50.6m 2013 11.8m 383.2m 323.8m 59.4m 2014 15.2m 408.2m 340.5m 67.7m 2015 17.8m 430.9m 352.4m 78.4m 2016 22.0m 456.8m 368.4m 88.4m 2017 26.1m 486.4m 393.9m 92.5m

LongHaul=Routegreaterthan4,000km*Non-LCCexcludingGulfcarriers~GulfCarriers=EK,EY,QR&TK

Long Haul LCC Non-LCC Non-LCC * Gulf carriers ~ 2013 21.7% 4.1% 4.1% 2.0% 2014 28.6% 5.7% 6.5% 5.1% 2015 17.8% 5.9% 5.6% 3.5% 2016 23.6% 6.5% 6.0% 4.5% 2017 18.4% 6.7% 6.5% 6.9%

Source: CAPA – Centre for Aviation and OAG

LCC Non-LCC Non-LCC excluding Gulf carriers

5 years’ interna9onal traffic growth

www.centreforavia-on.com

JustasLCCsreshapedshorthaul,LHLCCsaredrivingfullserviceairlinechangeInthesamewaytheyareeachevolvingtolookmorealike–connec-vity,premiumseats,lounges,FFPsFullserviceairlinesaremovingtoadoptLHLCCsubsidiariesoftheirownThereare54LCCsthatoperatelonghaul(>4,000km)routes

….Long haul low cost airlines are here to stay

AlmostallLHLCCflights4-7,000kmareoperatedbynarrowbodyaircraA

www.centreforavia-on.com

Long haul narrowbody is growing fast

Average Distance (km) 4,687

Median Distance (km) 4,514

Total Routes 1,339

Total Flights 271,837

Total Seats 44,808,640

Total Distance (km) 1,227,181,740

Total ASK’s 202,329,421,542

Domestic Flights Seats ASK

JFK-SFO 13,743 1,989,960 8,258,333,950

EWR-SFO 11,120 1,680,194 6,917,358,790

BOS-LAX 9,542 1,531,292 6,417,644,694

BOS-SFO 8,718 1,387,245 6,020,643,210

HNL-LAX 7,714 1,458,740 5,988,127,656

International Flights Seats ASK

PTY-GRU 3,973 611,842 3,108,769,150

PTY-SCL 3,852 593,208 2,849,771,260

LAX-PTY 2,307 355,278 1,719,900,800

EZE-PTY 1,940 298,760 1,597,170,940

KEF-YYZ 1,780 346,518 1,444,287,040

Source:CAPA–CentreforAvia-onandOAG

Heatmapofordersanddeliveriesoflonghaulnarrowbodies

(andnotjustLCCs.Thesearepredominantlyfullserviceairlines)

www.centreforavia-on.com

10 Year Growth rate*: 13% p/a *Includes Turkish Airlines Seats ASK Flight

Emirates 159.4% 177.6% 91.5%

Etihad 210.4% 296.9% 266.1%

Qatar 253.3% 365.9% 185.7%

Turkish 240.5% 372.8% 186.7%

But in 2017 growth was only 0.5% Emirates: 2.8% Qatar: 0.8% Etihad: -3.6% Turkish: 1.8%

Source: CAPA – Centre for Aviation and OAG

2. The Gulf carriers at a turning point

www.centreforavia-on.com

The Super-Connectors: Revising strategies

Previouslyonlyorganiclonghaulgrowth;nowtonetworkwithflydubaiReducingcosts,droppingpartnershipstrategy,butnonewstrategyyet(Temporarily?)hamstrungbyblockade;stronginvestments,inIAG,LATAMTroublesathome;reducingexpansionplans

www.centreforavia-on.com

3. Chinese tourism growth is unlike any previous market

1. Chinesetourismhasimmenseandpoten-allyrapidupside

2. Thesheerscaleandrapidityofgrowthdifferen-atesitfromprevioussourcemarkets

www.centreforavia-on.com

177

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

200

600

1,000

1,400

1,800

2,200

2,600

217 230 261415

658739

9321,133

1,909

2,211

China - New Zealand flight growth

NumberofairlinesflyingtoNewZealand

Over1,000%growth

ThescaleofChina’stourismgrowth– anditslikelyupside–hasmuchbroaderimplica-onsthanjusttourism.Itisoneelementofamajorglobaltransforma-on

Source:CAPA–CentreforAvia-on,OAG

Source:CAPA–CentreforAvia-on,OAGTrafficAnalyser*2017yeartodate

Air New Zealand average domes9c fares

$179

$174

$169

$171

$169

$162

$169

AirNewZealand’saveragedomes-cfaresdeclinedsignificantlybetween2011-2016,buthaverecoveredin2017todate

www.centreforavia-on.com

$190

$185

$180

$175

$170

$165

$160

$155

Air NZ average domes9c fares by airport

2011vs.2017AKL down9.0%CHC down4.3%DUD down6.4%QLG down6.6%ZQN down4.7%

2016vs.2017AKL up5.0%CHC up4.5%DUD up1.2%QLG up3.8%ZQN up8.1%

2011 2012 2013 2014 2015 2016 2017

AKL CHC DUD WLG ZQN

Source:CAPA-CentreforAvia-on,OAGTrafficAnalyser

www.centreforavia-on.com

-Anes-mated40,000appsareunderdevelopmentinthetravelspace-Ar-ficialIntelligence,voicerecogni-onarefastenhancingtheabilityofbotstohandlecomplextransac-ons-“Thirdpar-es”likegooglearerapidlyintrudingintothedistribu-onspace-Blockchainisnowenteringthepicture,allowingdirectdealingandchangingpayments-Privatebehaviouristransla-ngintothecorporate-Thiswillbean“un-dy”evolu-on.Probablyexplosive

A Torrent of apps, AI, chatbots, big data, Blockchain, google, Facebook, Amazon, Alibaba……

www.centreforavia-on.com

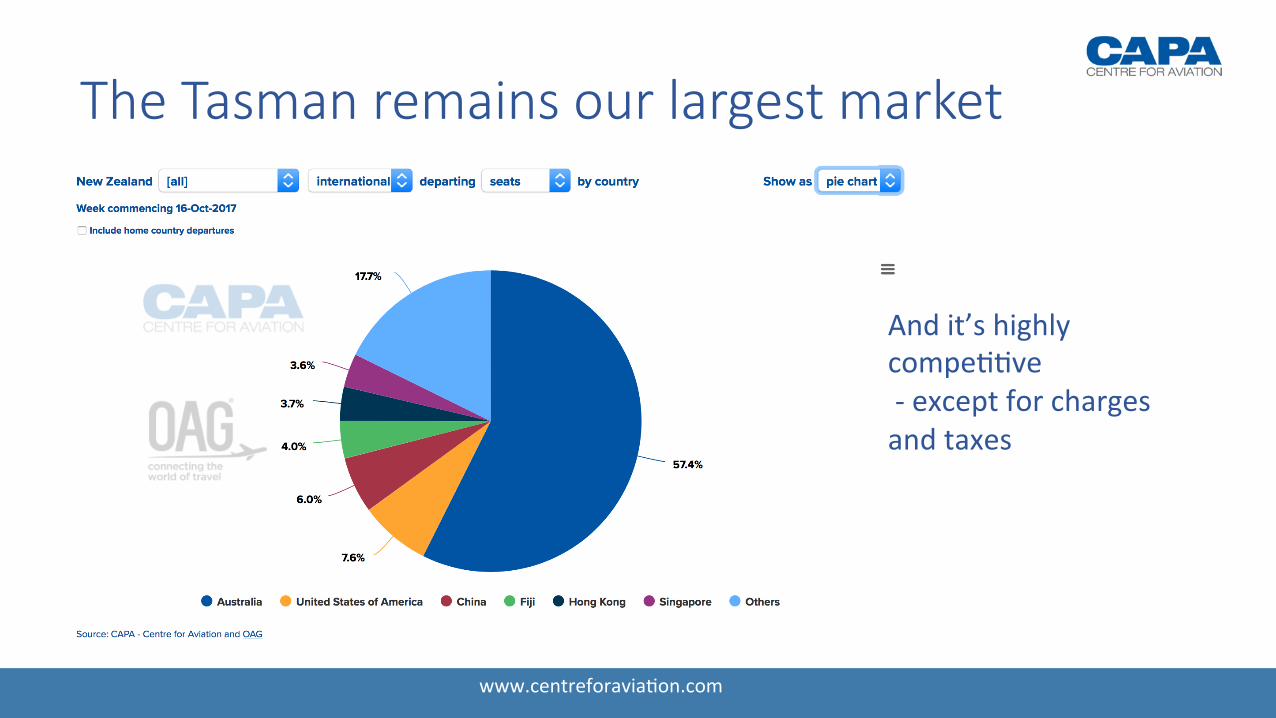

The Tasman remains our largest market

Andit’shighlycompe--ve-exceptforchargesandtaxes

www.centreforavia-on.com

AirlinesDes-na-ons

10/97

115/9

*AU/NZ

2007 2017

44%SeatGrowth

Australia-NewZealand

FlightsSeats

18,0003,500,000

24,0005,100,000

2007 2017• Addi-onaldes-na-onsinAustraliaincludeCBR,

MCY.

• ]NewZealandnolongerflyingtoHLZorPMR• 2010-2014flightstoROToperated.

Tasman: good growth in a “mature” market

Source:CAPA–CentreforAvia-on,OAG

www.centreforavia-on.com

The majority of future capacity growth will be into Asia – but the Americas have poten9al

Newaircrauaremakinglongandthinroutespossible

www.centreforavia-on.com

Air New Zealand Passenger Growth 2013-2017

www.centreforavia-on.com

Thankyou!