threadneedle investment conference absolute return ... · 12/31/2011 · quentin fitzsimmons and...

TRANSCRIPT

Quentin Fitzsimmons and Matthew Cobon

Threadneedle Investment ConferenceAbsolute Return Investing and the Absolute Return Bond Fund

9 February 2012

Agenda

01 Investment philosophy

02 Introducing the Absolute Return Bond Fund

03 Portfolio construction

04 Expanding on performance and addressing how the product can help you

05 Summary

PT/12/00889 2

Investment philosophy

01

Investment philosophy – out-think, out-perform

� We are stronger collectively than as individuals

� Our investment process is structured to reflect this belief

� We have a global approach and cover all asset classes

Teamwork defines us

out-think

teamwork

out-perform

All asset classes

Globalapproach

PT/12/00889 4

Investment process – out-think, out-perform

Economic background

Sectors and themes

Asset allocation

Valuation framework

Asset and sectorallocation models

Themes / analysis and debate

Bottom-up security selection across capital structure

Equity

Multi-asset

Fixed income

Absolute return

Debate Execution / deliveryIdea generation

+ +

2. Team work 3. Out-perform1. Out-think

out-think

teamwork

out-perform

All asset classes

Globalapproach

This sets the agenda for our specialist teams

Collectively we form a global investment view on

� The central case for economies

� The valuation of asset classes

PT/12/00889 5

Government debtInvestment Team

Source: Threadneedle as at 31 December 2011

An experienced group of macro-investors

Strong interconnection

Team incentivised to pool ideas

Credit Teams12 fund managers / analysts

Emerging Market Debt Team5 fund managers / analysts

Commodities Team3 fund managers / analysts

Regional Equity Teams45 fund managers / analysts

Quentin FitzsimmonsHead of Government Bonds20 years’ experience

Richard StevensPortfolio Manager / UK Specialist29 years’ experience

Dave ChappellPortfolio Manager / US Specialist24 years’ experience

Matthew CobonPortfolio Manager / FX Specialist15 years’ experience

Martin HarveyPortfolio Manager / EU Specialist7 years’ experience

Matthew ReesQuantitative Analyst3 years’ experience

PT/12/00889 6

Introducing the Absolute Return Bond Fund

02

Putting our ‘best ideas’ into action

Low correlation Absolute return

Correlating returns with the Absolute Return Bond Fund Correlation

UK Government 0.49

UK Corp Debt 0.07

UK High Yield Debt -0.29

Global Emerging Markets Sovereign & Corp -0.17

FTSE 100 Equity Index -0.27Source: Threadneedle as at 31 December 2011

Achieving diversification

Source: Threadneedle, Merrill Lynch and Bloomberg as at 31 December 2011. Based on weekly returns (performance chart) and monthly returns (correlation) since launch of Threadneedle Absolute Return Bond Fund (October 2005). All data calculated in fund currency. Gross performance from 31 March 2010 onwards is based on daily cash flows and valuations, from 1 January 2008 to 31 March 2010 based on Global Close prices, and prior to January 2008 based on 12pm prices. Fund data is quoted on a bid-bid basis with income re-invested at bid. Fund data is gross of tax and T.E.R to facilitate comparison with the indices.

30

35

40

45

50

55

60

65

70

75

80

2005 2006 2007 2008 2009 2010 2011

Threadneedle Absolute Return Bond Fund FTSE 100

FT UK Government Total Return 3-Month Libor

PT/12/00889 8

Portfolio construction

03

Threadneedle Absolute Return Bond FundBuilding blocks

Designed to deliver

Target – 300bpsOverlay

3 month LIBORUnderlay

+

PT/12/00889 10

Threadneedle Absolute Return Bond Fund Alpha investment strategies

� An overlay incorporating our best ideas to deliver alpha

� Diversified approach in liquid fixed interest and currency markets exploiting

� Direction

� Relative value

� Predominantly using derivatives including

� Exchange traded futures and options

� Bonds

� Options

� Currency forwards

� Interest rate swaps and CDS (e.g. iTraxx crossover)

Building blocks that work

Target –300bpsOverlay

3 month LIBORUnderlay

+

PT/12/00889 11

Threadneedle Absolute Return Bond FundShort dated, high grade bond portfolio

� A robust liquid underlay

� High quality bonds

� To achieve a cash cash-type return with good risk control

Contribution to duration 6.2 months

Sector breakdown

Sector Fund (%)Consumer Discretionary 3.4Consumer Staples 3.8Energy 2.3Financials 3.6Industrials 3.7Securitised Collateralised 4.2Sovereign & Sub-Sovereign 36.0Telecommunication Services 1.7Utilities (Non Collateralised) 7.4

Source: Threadneedle as at 31 January 2011

Building blocks that work

Target –300bpsOverlay

3 month LIBORUnderlay

+Credit rating breakdown

Rating Fund (%)AAA 36.0AA 8.1A 15.4BBB 6.3BB 0.3

Source: Threadneedle, as at 31 December 2011

PT/12/00889 12

Portfolio construction Implementing our ideas to build positions

Getting the best ideas into the portfolio

� Cash bonds

� Futures

� Options

� Forwards

� Swaps

Securities1.

� Risk budget

� Liquidity

� Volatility

� Transparency

� Impact on existing portfolio

Size2.

� Price target

� Call level

� Rolling stop profit

� Time limits

Implementation3.

PT/12/00889 13

Portfolio constructionGoing into more detail on the risk budget

A flexible approach to risk-taking

Sources of return Proportion of risk budget (%)

Expected return (ER)

Implied informationratio (IR) Risk budget

Rates 60 175 0.6 325

Duration 20 40 0.3

Yield curve 20 55 0.6

Relative value 20 80 0.9

Currency 30 100 0.8 125

Short-dated bond fund 10 Cash + 25

Total 100 300 0.67 450

PT/12/00889 14

Expanding on performance and addressing how the product can help you

04

Threadneedle Absolute Return Bond Fund Gross monthly performance since launch

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Total Relative to Index

2005 0.27% 0.73% 1.01% +0.24%

2006 0.51% 0.47% 0.55% 0.41% 0.53% 0.27% 0.15% -0.43% 0.81% 0.49% 0.53% 0.10% 4.48% -0.46%

2007 -0.13% 1.40% -0.13% -0.26% -0.63% -0.61% 2.81% 1.55% 2.06% 0.94% 0.93% 0.34% 8.52% +2.18%

2008 2.33% 1.79% 2.83% -2.48% -1.29% -0.49% 0.82% 1.85% 1.21% 1.47% 2.35% 3.13% 14.18% +8.01%

2009 -0.18% 0.21% 0.36% 0.65% 1.29% 0.35% -0.01% 0.77% 0.19% 0.52% 0.16% -0.07% 4.33% +2.98%

2010 0.09% 0.03% 0.36% -0.30% -0.40% 0.18% -0.34% 1.23% -0.43% -0.20% -0.15% 0.14% 0.18% -0.61%

2011 -0.13% 0.25% 0.03% -0.35% -0.93% -0.73% -0.07% 1.04% 2.56% -1.03% 1.83% -0.80% 1.72% +0.78%

Consistent risk-adjusted performance

Source: Threadneedle as at 31 December 2011. All fund data is based initially in £ share classes, and converted to different currencies using Global Close FX rates. Fund data provided by Threadneedle. Gross performance based on Global Close prices adjusted by TER, and prior to January 2008 based on 12pm prices adjusted by TER. Fund data is quoted on a bid to bid basis with income re-invested at bid. Fund data is gross of tax and T.E.R to facilitate comparison with the indices. Index data provided by Thomson DataStream.

PT/12/00889 16

Source: Threadneedle as at 31 December 2011

Absolute Return Fund contribution analysis (£)

Strategy Jan Feb Mar Q1 Apr May Jun Q2 Jul Aug Sep Q3 Oct Nov Dec Q4 Total

Rates -0.07% 0.15% -0.44% -0.35% -0.76% -0.45% -0.47% -1.67% 0.00% 0.61% 0.45% 1.08% -0.42% 0.95% -0.20% 0.32% -0.69%

Currency -0.17% -0.05% 0.29% 0.07% 0.19% -0.43% -0.35% -0.59% -0.74% 0.13% 1.48% 0.85% -0.31% 0.37% -0.78% -0.73% -0.42%

Relative value 0.02% 0.03% 0.15% 0.20% -0.05% -0.01% -0.01% -0.07% 0.55% 0.14% 1.05% 1.76% -0.70% 0.71% 0.17% 0.17% 2.06%

Short dated bond fund and cash 0.09% 0.11% 0.03% 0.21% 0.26% -0.03% 0.10% 0.33% 0.12% 0.16% -0.43% -0.12% 0.41% -0.20% 0.01% 0.21% 0.66%

Total -0.13% 0.25% 0.03% 0.15% -0.35% -0.93% -0.73% -2.00% -0.06% 0.98% 2.56% 3.56% -1.03% 1.83% -0.80% -0.03% 1.61%

2011

Strategy Q2 2009 Q3 2009 Q4 2009 Total 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Total 2010

Rates 1.36% -0.38% -0.15% 0.98% -0.06% -0.78% 0.19% -0.25% -0.90%

Currency 0.52% 0.38% 0.21% -0.13% -0.15% 0.07% -0.25% 0.02% -0.30%

Relative value 0.13% 0.07% 0.19% 0.64% 0.12% 0.01% 0.16% -0.22% 0.07%

Short dated bond fund and cash 0.31% 0.89% 0.37% 2.85% 0.56% 0.17% 0.35% 0.23% 1.31%

Total 2.32% 0.96% 0.61% 4.34% 0.47% -0.53% 0.45% -0.21% 0.18%

PT/12/00889 17

Summary

05

Threadneedle Absolute Return Bond Fund

� Positive performance in different market environments

� Diversification

� Broad market coverage

A flexible fund designed to perform in all market conditions by taking an holistic approach to risk, managed by an experienced team providing diversification for our clients

PT/12/00889 19

The economic background

2012 forecast GDP growth (%) Inflation (%)

USA 1.5 2.0

Eurozone 0.0 2.0

UK 0.0 2.3

Japan 0.5-1.0 -0.2

China 8.0-8.5 3.5¹

Brazil 3.0-3.3 5.3¹

Source: Threadneedle, November 20111 Consensus Economics

Source: Bloomberg

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Mid

pric

e

When will all the policy measures really start to improve things?

PT/12/00889 20

Macro challenges for bond marketsUltra low interest rates – the return on your money

� Monetary policy is highly accommodative

� Central banks have cut interest rates to unprecedented levels

� They have augmented this by quantitative easing (buying assets such as government bonds by creating money)

Policy rates

Source: Reuters EcoWin

20.0

United Kingdom, Bank RateGermany, ECB Main refinancing, Fixed Rate, EURUnited States, Fed Funds Effective Rate, Average, USD

56

%

0.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

59 62 65 68 71 74 77 80 83 86 89 92 95 98 01 04 07 10

Can interest rates increase? What if they do?

PT/12/00889 21

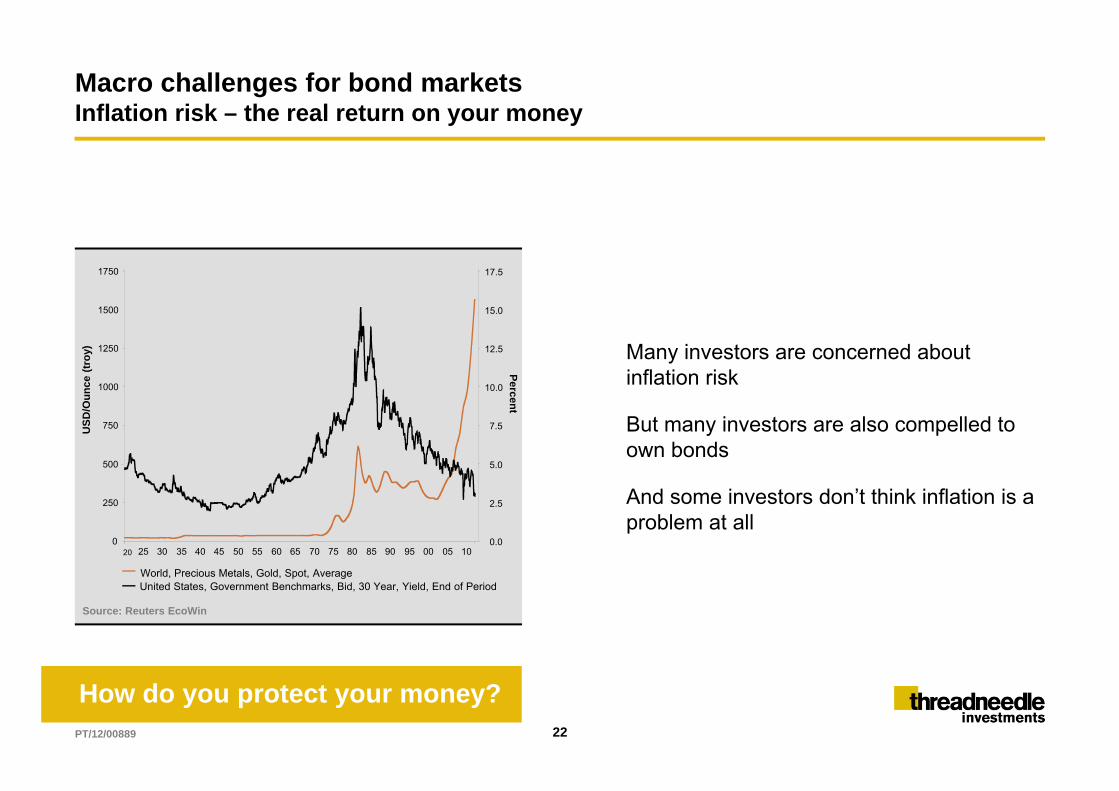

Macro challenges for bond marketsInflation risk – the real return on your money

Source: Reuters EcoWin

� Many investors are concerned about inflation risk

� But many investors are also compelled to own bonds

� And some investors don’t think inflation is a problem at all

How do you protect your money?

USD

/Oun

ce (t

roy)

World, Precious Metals, Gold, Spot, AverageUnited States, Government Benchmarks, Bid, 30 Year, Yield, End of Period

200

250

500

750

1000

1250

1500

1750

0.0

2.5

5.0

7.5

10.0

12.5

15.0

17.5

25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 00 05 10

Percent

PT/12/00889 22

FX trends: Competitive devaluationsThe return of your money?

Source: Bloomberg, January 2012

1.20

1.25

1.30

1.35

1.40

1.45

1.50

Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11 Sep-11 Dec-111000

1100

1200

1300

1400

1500

1600

EURUSD Relative size of Central bank balance sheet (RHS)

PT/12/00889 23

FX composite volatility

CVIX current volatility

Source: Bloomberg, January 2012

0

5

10

15

20

25

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Old range

New range?

Or back to old range?

PT/12/00889 24

Reserve diversification has been an important FX market driver

China FX reserves

Source: Bloomberg, January 2012

0

500

1000

1500

2000

2500

3000

3500

Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11

Is it different this time?

PT/12/00889 25

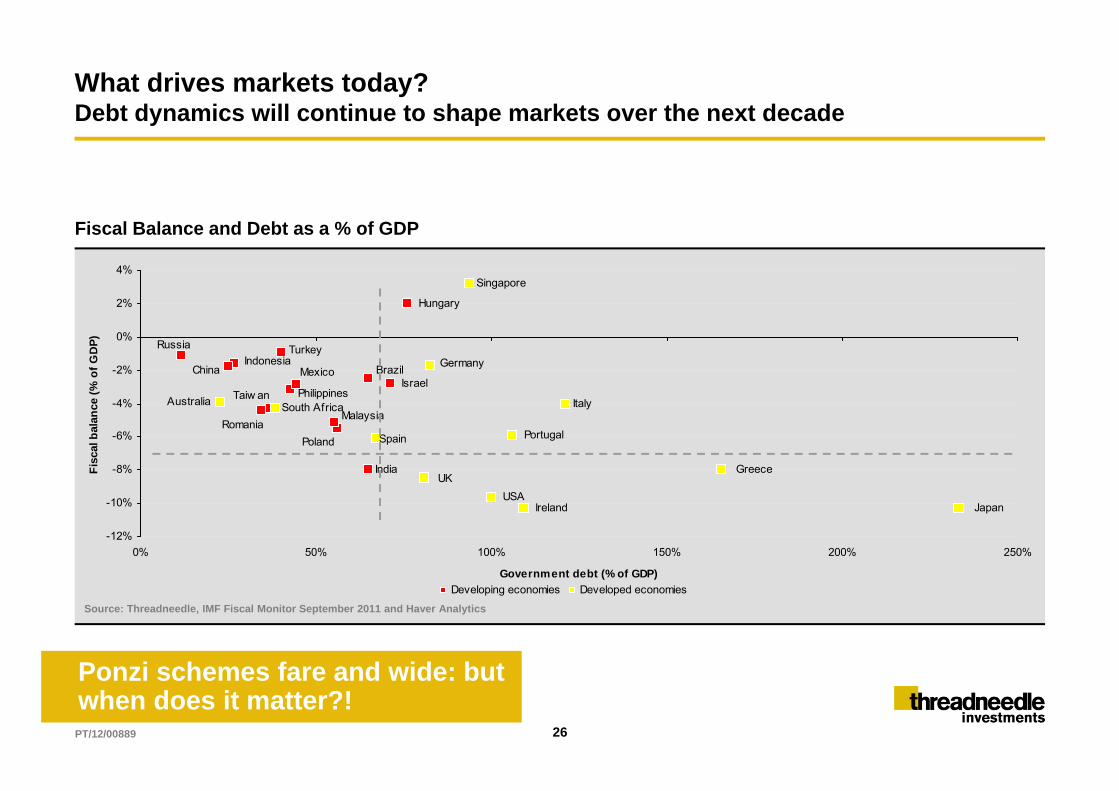

Fiscal Balance and Debt as a % of GDP

Source: Threadneedle, IMF Fiscal Monitor September 2011 and Haver Analytics

Portugal

USA Ireland

Philippines

Malaysia

Indonesia

India

China

South Africa

Israel

TurkeyRussia

Romania

Hungary

Poland

Mexico Brazil

Italy

Spain

Greece

Germany

Japan

UK

Australia Taiw an

Singapore

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

0% 50% 100% 150% 200% 250%

Government debt (% of GDP)

Fisc

al b

alan

ce (%

of G

DP)

.

Developing economies Developed economies

What drives markets today?Debt dynamics will continue to shape markets over the next decade

Ponzi schemes fare and wide: but when does it matter?!

PT/12/00889 26

Current strategy

Overall Neutral Duration� Long US Treasuries� Long Australian Debt� Short Italian BTPs� Short UK Government bonds (gilts)� Short Japanese Government bondsCDS Strategies� Long protection on Japan, Bulgaria and BelgiumCurrency� Negative Euro versus US Dollar� Long Malaysia Ringgit, Russian Rouble, Canadian Dollar & Mexican Peso� Short Australian Dollar, Swedish Krona, Swiss Franc & Japanese Yen Short dated bond holdingsFocused on diversificationTaking advantage of high quality “covered” bond issuance

PT/12/00889 27

Key investor theme for 2012 will continue to be the politicisation of markets

� Global macro imbalances and currency markets

� Government guaranteed banking systems

� Punishing the speculator

� Quantitative easing

Exceptionally serious … I won't let up on this (the tough conditions imposed for bailouts) because otherwise ... primacy of politics over finance can't be enforced

Angela Merkel, 23 November 2010

China shouldn't bow to foreign pressurePeoples' Bank of China adviser Li,

22 November 2010

... conditions…are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.

Federal Reserve, 9 August 2011

PT/12/00889 28

Summary and outlook

� Developed governments are betting the ranch

� There will be on-going concerns about solvency

� The politicisation of markets makes the outlook for government bonds treacherous

� The concept of what is risk free is evolving

� We strongly recommend absolute return-orientated investment strategies to improve bond portfolio diversification in this environment

PT/12/00889 29

Important information

For Investment Professionals use only, not to be relied upon by private investors.

Subscriptions to a fund may only be made on the basis of the current Prospectus or Simplified Prospectus and the latest annual or interim reports, which can be obtained free of charge on request.

Past performance is not a guide to future performance. The value of investments can fluctuate. The dealing price may include a dilution adjustment where the fund experiences large inflows and outflows of investment. Further details are available in the Prospectus.

The research and analysis included in this document has been produced by Threadneedle for its own investment management activities, may have been acted upon prior to publication and is made available here incidentally. Information obtained from external sources is believed to be reliable but its accuracy or completeness cannot be guaranteed. Any opinions expressed are made as at the date of publication but are subject to change without notice.

The interest rate on most government and corporate bonds will not increase in line with inflation. Thus, over time, the real value of investor's income could fall. The Fund may deduct the annual management charge from capital rather than from income. This may erode capital or reduce the potential for capital growth over time.

The Threadneedle Absolute Return Bond, Threadneedle Target Return Fund, and Threadneedle Target Return Core Fund may hold up to 100% in cash or money market securities. Therefore, investors should be aware that these Funds may not participate fully in a market rise. The Funds’ exposure involves short sales of securities and leverage which increases the risk of the Funds. Short selling is designed to make a profit from falling prices. However, if the value of the underlying investment increases, the short position will negatively affect the Funds’ value. Leverage amplifies the effect of changes in the price of an investment on the Funds’ value. As such, leverage can enhance returns to shareholders but can also increase losses. For the avoidance of doubt, these Fund does not offer any form of guarantee with respect to investment performance, and no form of capital protection will apply.

The mention of any specific shares or bonds should not be taken as a recommendation to deal.

Standard & Poor's Fund Services is an independent company that awards ratings based on a wide variety of factors including performance, fund management style, overall investment process, corporate profile and stability of investment team. Fund Management Ratings range from 'A' to 'AAA'.

The information provided in this presentation is for the sole use of those intermediaries attending the presentation. It may not be reproduced in any form without the express permission of Threadneedle and to the extent that it is passed on, care must be taken to ensure that this is in a form that accurately reflects the information presented here.

Threadneedle Investment Services Limited, 60 St Mary Axe, London EC3A 8JQ, registered no. 3701768. Authorised and regulated in the UK by the Financial Services Authority. Threadneedle is a brand name, and both the Threadneedle name and logo are trademarks or registered trademarks of the Threadneedle group of companies

PT/12/00889 30