threadneedle european equities - fundsupermart.com · a leader in european equity €34.4 billion...

TRANSCRIPT

February 2013

Threadneedle European Equities

Francis Ellison

Contents

2

1. Introduction to Threadneedle European Equity team

2. Outlook

3. Funds

i. Pan European Strategy – Threadneedle(Lux) Pan European Equities Fund

ii. Why Small Cap?

iii. Pan European Smaller Companies Strategy – Threadneedle(Lux) Pan European Small Cap Opportunities Fund

Appendix1. Investment Process

Introduction

1

A leader in European equity

€34.4 billion AuM across all portfolios1

Excellent long-term performance

Deep resource

24-strong European equity team2

Close interaction across asset classes

Dedicated risk management

Clear investment philosophy, consistently applied

Stock selection key source of return

Culture of collaboration and debate

Threadneedle‟s European equity credentials

Source: Threadneedle as at 31 December 2012.

1 AuM includes externally managed portfolios, and includes UK-specific assets of €19.0 billion.

2 Includes 12 UK-specific investment professionals as at 31 October 2012.

4

European equities team

Source: Threadneedle, 31 January 2013.

5

Philip

Dicken

Dan

Ison

Ann

Steele

Nick

Davis

Mark

Heslop

David

Dudding

Paul

Doyle

Fred

Jeanmaire

Ben

Needham

Caroline

Duong

Industry

start 1997 1994 1982 2004 1999 1999 1990 2007 2010 2012

Threadneedle

start 2004 2007 2009 2010 2008 1999 1995 2011 2012 2012

Research

Small Cap

Forestry

& Paper

Automotive

Consumer Disc.

Industrials

Technology

Consumer

Disc.

Food Retail

Insurance

Healthcare

Consumer

Staples

Utilities

Small Cap

Basic Materials

Consumer

Staples

Med. Tech

Metals

Telecoms

Banks

Media

Support

Services

Electrical

Engineers

Beverages

Small Cap

Funds

managed

Institutional

Funds

Pan European

Smaller

Companies

Fund

Institutional

Funds

Pan European

Accelerando

Fund

T-Lux Pan

European Fund

Institutional

Funds

Pan European

Fund

European Fund

Pan European

Equity

Dividend Fund

Institutional

Funds

T-Lux Pan

European

Smaller

Companies

Fund

European

Select Fund

European

Smaller

Companies

Fund

Institutional

Funds

European Apex

Fund

Institutional

Funds

Outlook

2

Good news

US housing market showing signs of life, consumer in better spirits

Central banks committed to boosting asset prices

New regime in China raises prospects of stimulus

Bad news

US fiscal cliff threatens to tip economy into recession

Europe condemned to another year of pitiful economic performance

Risk of crisis remains, likely candidates are Spain and Greece

Deleveraging forces continue to hold back developed economies for the foreseeable future

Navigating the current environment

7

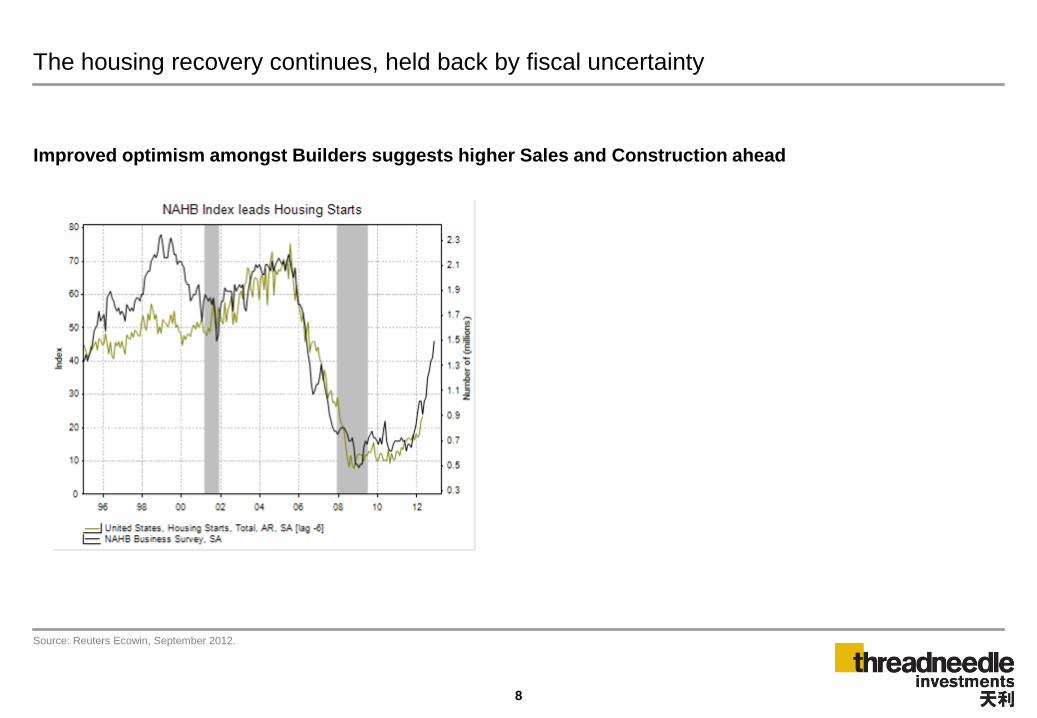

Improved optimism amongst Builders suggests higher Sales and Construction ahead

The housing recovery continues, held back by fiscal uncertainty

8

Source: Reuters Ecowin, September 2012.

Consumers feeling better about life for the first time since the crisis

Source: Reuters Ecowin, October 2012.

9

Central bank balance sheets v S&P 500

Central Bank policy: Who needs growth anyway?

Source: Threadneedle, Bloomberg, Reuters Ecowin, October 2012, Combined balance sheet = ECB + Federal Reserve + Bank of England.

1500

2000

2500

3000

3500

4000

4500

5000

09 10 11 12

600

700

800

900

1000

1100

1200

1300

1400

1500

Combined Central Bank balance sheet S&P 500 (RHS)

IndexUSD bn

Central bank balance sheets (rebased, Jan 08 = 100)

50

100

150

200

250

300

350

400

450

08 09 10 11 12

ECB Fed BoE

Index (Jan 08 = 100) Central Bank Assets

“…lower mortgage rates will make housing more affordable and allow more homeowners to

refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost

consumer wealth and help increase confidence, which can also spur spending.” Ben Bernanke,

November 2010

10

Tentative signs of improvement in China

Source: Threadneedle, UBS, October 2012

Growth rate (% y/y) Growth of infrastructure investment (% y/y 3mma)

11

The US fiscal cliff in 2013 We expect fiscal drag of roughly 1.5% in the coming year

Source: Morgan Stanley, April 2012.

12

Percentage points of potential GDP

-4.5

-3.0

-1.5

0.0

1.5

3.0

4.5

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Fiscal year

Fiscal Restraint (+)

Fiscal Stimulus (-)

Current Law

2013 Fiscal Cliff

(% of GDP )

Expiration of

unemployment

benefits

-0.2%

Automatic

spending cuts

(sequestration)

-0.8%

Expiration of

payroll tax cuts -0.8%

Expiration of Bush

tax cuts -0.8%

C.-3.0%

Growth divergence is not new, but cannot continue

Time for decisive action

Source: Threadneedle, Reuters Ecowin, Reuters Ecowin October 2012

Eurozone Unemployment Rates

Corporate loan growth, %YoY

13

-10

-5

0

5

10

15

20

25

30

35

04 05 06 07 08 09 10 11 12

Italy Spain Germany France

Lending to Corporations%

oya

5

6

7

8

9

10

11

12

93 95 97 99 01 03 05 07 09 11

5

7

9

11

13

15

17

19

21

23

25

Germany Italy Spain (RHS)

%%

European banks not yet started necessary

deleverage2

European lenders have a long way to go

1Source: Companies data, Westhouse Securities, October 2012. 2Source: Thomson Reuters Datastream, Arbuthnot, October 2012

14

Cumulative loan loss provisions as a % of peak

loan assets1

Corporate balance sheets are strong – excluding financials!

Source: MSCI, Worldscope, Morgan Stanley Research, 31 December 2012.

All data above based on companies within the MSCI Europe ex-Financials.

Ex-financials debt to equity (%) Cash on balance sheets

15

European companies sales are increasingly global

European equities are a play on global growth

Source: Published accounts/Redburn IDEAS database.

16

460 European non-financial companies

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Rest of World Asia ex Japan Other Americas USA and Canada Japan Europe

Extrapolation

Volatility to continue

Remain alive to macro developments

Many alpha opportunities

A stockpicker‟s paradise

Valuations remain attractive

1 Source: Mirabaud Securities LLP, 30 November 2012.

Equities are cheap1

6

10

14

18

22

26

30

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

Multip

le (

x)

of tr

end e

arn

ings

EU Ex Bubble Trend PE Median + 1 SD -1 SD

17

Index Level 2013E PE 2014E PE PCF 2012 yield (%)

US - S&P 500 1,466 14.4 13.8 8.4 1.9

Europe – MSCI

Europe 99 13.6 12.4 7.5 3.3

Japan – TOPIX 889 17.8 13.2 5.3 3.2

Asia Pacific ex. Japan –

MSCI Asia Pacific ex

Japan

476 13.2 12.3 8.9 2.9

Source: Threadneedle Investments, Bloomberg, 4 January 2013

18

Valuations remain attractive

Characteristics of companies we like

Source: Threadneedle as at 31 December 2012.

Themes Portfolio strategy Examples

Strong franchises / unique

assets

Market leaders

Strong finances / management

Barriers to entry

Nestlé, Ryanair, Fresenius Medical

Care

Restructuring / recovery

New management strategy

Improving returns

Value creation

Allianz, Merck

Quality cyclicals

Growth potential

Overseas earnings

Strong finances

Sika, SGS, Lanxess

Structural growth

Demographic trends

Energy efficiency

Global shortages

Innovation

Syngenta, Atlas Copco, Novo Nordisk

Emerging markets opportunities Emerging markets exposure

Reasonable valuations Edenred, ABI

19

The market is trading at an attractive valuation historically and relative to other assets such

as bonds

Cash flows are healthy and balance sheets are strong, yet cash balances are earning little

M&A activity is likely to be a feature

Whilst problems in some countries have caused euro weakness this benefits a number of

exporting companies, particularly in northern Europe

Despite tough macroeconomic conditions, it is still very possible to find companies, even in

the peripheral eurozone – There are great opportunities.

Why European equities now ?

20

Pan European Strategy ▪ Threadneedle (Lux) Pan European Equities Fund

3i

A core Pan European equity offering that provides a broad and diversified exposure.

Portfolio characteristics

22

Pan European equity strategy

Source: Threadneedle as at 30 September 2012. This represents the Europe inc. UK Core Plus composite strategy. Where references are made to portfolio guidelines

and features, these may be subject to change over time and prevailing market conditions. Actual investment parameters will be agreed and set out in the prospectus or

formal investment management agreement. Please note that the performance target may not be attained and is over a rolling 3-year period.

Strategy Pan-European Large Cap

(Europe inc. UK Core Plus)

Outperformance target 2.0% p.a.

Expected tracking error 3%–6%

Expected information ratio 0.5–1.0

Stock weightings +/- 4% versus benchmark

Sector weightings +/-10% versus benchmark

Total AUM in strategy €2.4 billion

Actively seeking the best opportunities

Threadneedle (Lux) Pan European Equities Fund Top 10 positions

Source: Threadneedle as at 31 December 2012. Index is MSCI Europe Index.

23

Stock Sector Fund (%) Index (%) Active (%)

Rio Tinto Mining 3.7 1.1 2.6

Nestlé Food Producers 3.6 2.9 0.7

Allianz Nonlife Insurance 3.2 0.9 2.3

SAP Software & Computer Services 3.1 1.0 2.0

BNP Paribas Banks 3.0 0.8 2.2

Unilever Food Producers 3.0 0.7 2.3

Diageo Beverages 3.0 1.0 1.9

Novartis Pharmaceuticals & Biotechnology 2.8 2.0 0.8

Volkswagen Automobiles & Parts 2.5 0.5 2.1

Anheuser-Busch InBev Beverages 2.3 1.0 1.3

Total 30.1 11.9 18.3

24

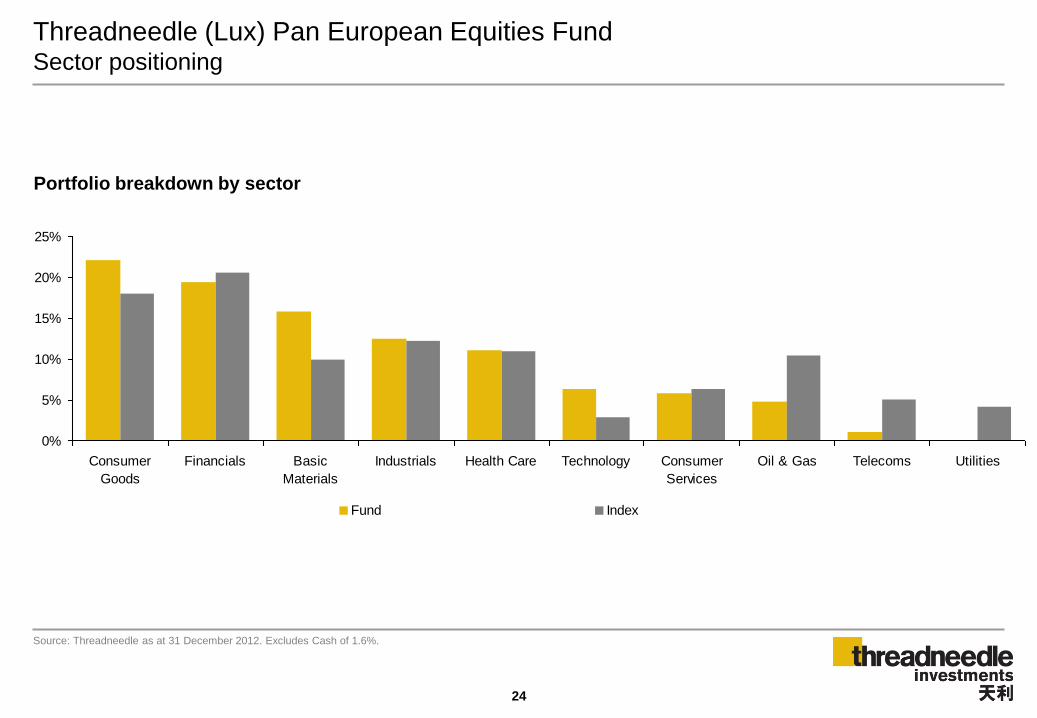

Threadneedle (Lux) Pan European Equities Fund Sector positioning

Source: Threadneedle as at 31 December 2012. Excludes Cash of 1.6%.

0%

5%

10%

15%

20%

25%

Consumer

Goods

Financials Basic

Materials

Industrials Health Care Technology Consumer

Services

Oil & Gas Telecoms Utilities

Fund Index

Portfolio breakdown by sector

25

Threadneedle (Lux) Pan European Equities Fund Geographic breakdown

Source: Threadneedle as at 31 December 2012. Excludes Cash of 1.6%.

Other consists of Austria, Greece, Ireland and Chile.

0%

5%

10%

15%

20%

25%

30%

35%

40%

UK Germany Switzerland France Netherlands Spain Belgium Sweden Denmark Norway Portugal Finland Italy Other

Fund Index

Portfolio breakdown by country

Threadneedle (Lux) Pan European Equities Fund

Source: Style Research as at 31 December 2012.

26

Style Analysis - Portfolio Style SkylineTM

What are we looking for in a company?

27

Strong 3-year relative performance

Source: Threadneedle and DataStream as at 31 December 2012. Performance in EUR and rebased to 100.

Initial purchase – October 2009.

2 Source: Bloomberg as at 9 January 2013.

The mention of stocks is not a recommendation to deal.

Sustainable competitive advantage

Swiss watch heritage cannot be copied by low cost alternatives

Dominance of global watch movement market a strong barrier to

entry and a driver of pricing power

Growth

More than 40% of sales from emerging markets

Market underestimating the strength and profitability of growth

(Asia, Americas underpenetrated)

Stable, experienced management team pursuing a clear, long-

term brand strategy coupled with a strong balance sheet model

Valuation

Trading on P/E of 15.1x (excluding cash) in 2011, falling to 11.5x

(excluding cash) in 2013e

80

100

120

140

160

180

200

220

Jan 09 Jul 09 Jan 10 Jul 10 Jan 11 Jul 11 Jan 12 Jul 12

Reb

ased

= 1

00

Sw atch relative to MSCI Europe Index

Year to Dec2 2012e 2013e

P/E 18.4x 16.6x

EV/EBITDA 11.8x 10.6x

ROE 17% 17%

UBS

1 Source: Datastream, as at 31 December 2012, in local currency.

2 Source: Autonomous estimates.

The mention of stocks is not a recommendation to deal.

28

Leading wealth manager in the world: UBS has a

relationship with half of the world‟s billionaires

Refocusing on wealth management announced in

October 2012 shows management discipline and

realism.

Consensus estimates for a return on equity of 13-

15% by 2015 are too low. ROE could be closer to

18-20%

UBS trades on 1.3x its tangible book value, and

could trade in a 1.6-2.0x range once its

restructuring is complete

28

Absolute performance and relative strength

2-year performance¹

50

60

70

80

90

100

110

120

130

Dec 10 Apr 11 Aug 11 Dec 11 Apr 12 Aug 12 Dec 12

Reb

ased

= 1

00

UBS UBS relative to FTSE W Europe Index

Year to Dec² 2013e 2014e 2015e

P/E 15.0x 12.1x 9.2x

EV/EBITDA 1.3x 1.2x 1.2x

RoE 8.3% 10.4% 13.0%

3ii

Why Small Cap?

Superior growth to large cap

Smaller companies are more flexible and able to adapt to changing market conditions

Entrepreneurial managements

Large opportunity set, greater opportunity to generate alpha

Lower analyst coverage

M&A: Cash-rich large caps likely to boost low organic growth with acquisitions

Valuation appears attractive relative to other asset classes and history

Large caps may be more at risk of government intervention/regulation than small caps.

Attractions of Pan European Small/Mid Cap

30

Characteristics of smaller companies

1 Source: Goldman Sachs International as at 11 July 2012.

2 Source: Datastream, July 2012.

3 Source :JP Morgan as at 31 December 2011.

Dispersion of returns1

-55%-45%-35%-25%-15%-5%5%

15%25%35%45%55%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Ou

t-/u

nd

erp

erf

orm

an

ce, 12-

mo

nth

ro

llin

g

75th percentile outperformance Large 75th percentile outperformance Small

25th percentile underperformance Large 25th percentile underperformance Small

Smaller companies outperform2

Risk-adjusted return since 1995

0.27

0.21

0.32

0.230.220.22

0.43

0.35

0.0

0.1

0.2

0.3

0.4

0.5

US

S&

P

500

US

S&

P

600 S

mall

Cap

UK

FT

SE

350

UK

Sm

all

Glo

bal

MS

CI

World

Glo

bal

MS

CI

World

Sm

all

Euro

pe e

x

UK

FT

SE

W.E

uro

pe

exU

KE

uro

pe e

x

UK

HS

BC

Sm

alle

r

Euro

pe e

x

Ris

k a

dju

ste

d r

etu

rn

31

Fewer analysts1

10

15

20

25

30

35

Less than €3 bn €3 - €5 bn €5 - €10 bn Greater than €10

bnMarket cap size

No

. o

f an

aly

sts

Sales growth – outperforming in 19 of the last 22

years3

Small Caps – Why now?

Source: JPMorgan – 10 January 2013. Pan European data.

PE Yr+1

Current

PE Yr+1

15 yr avg

P/B

Current

P/B

15 yr avg

EPS growth

2012e

EPS growth

2013e

Small/Mid Caps 12.2x 14.5x 1.9x 2.5x 4.9% 19.7%

Large Caps 13.3x 16.2x 2.3x 2.9x 5.9% 13.2%

Small/Mid caps are trading at a discount to 15-year average multiples

Small/Mid caps are expected to grow faster than Large caps

32

Structural growth – five examples

Theme Implication How can we benefit

European austerity Decline in consumer spending

Downtrading

Cheap US natural gas Improved US competitiveness

Reinvestment in basic industries

Ageing populations Increased incidence of cancer

Emerging market growth Consumption of luxury goods

Energy and environment Demand for energy-efficient

solutions

33

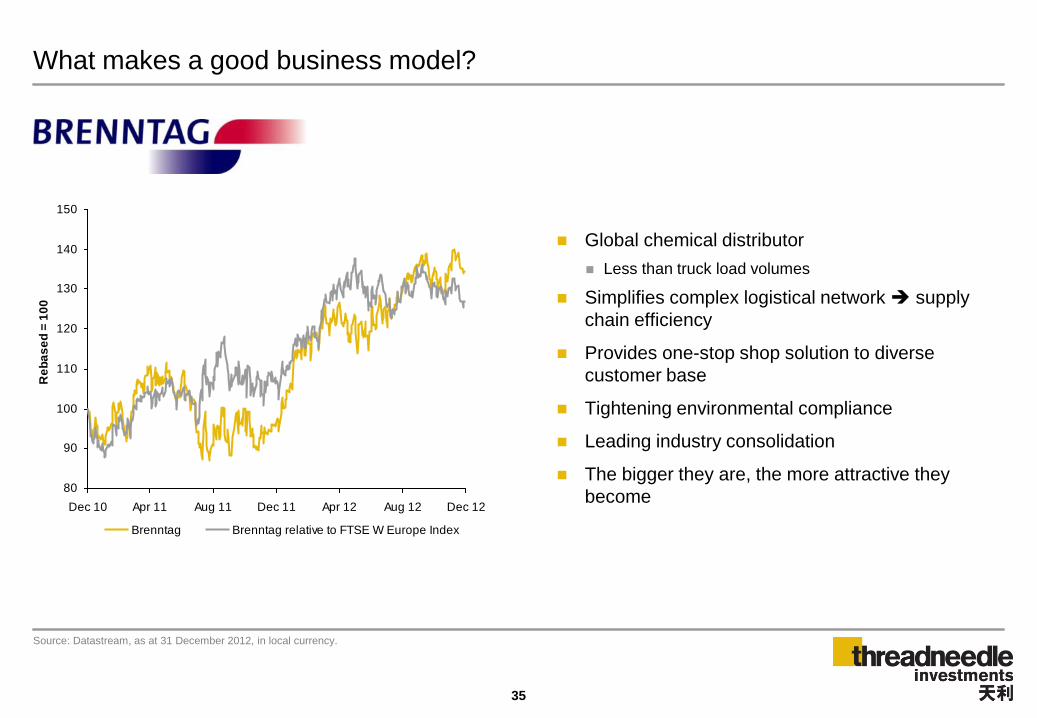

What makes a good business model?

34

1 Pricing power Fragmented

supplier base

Diverse customer base Dominant market position

2. Barriers to entry

Value added know-how

Scale

Regulatory compliance

Mission critical

+ =

A sustainably

high return on

capital

3 Structural growth drivers

Emerging market growth

Outsourcing

Supply chain efficiency/increased productivity

What makes a good business model?

Source: Datastream, as at 31 December 2012, in local currency.

35

Global chemical distributor

Less than truck load volumes

Simplifies complex logistical network supply

chain efficiency

Provides one-stop shop solution to diverse

customer base

Tightening environmental compliance

Leading industry consolidation

The bigger they are, the more attractive they

become 80

90

100

110

120

130

140

150

Dec 10 Apr 11 Aug 11 Dec 11 Apr 12 Aug 12 Dec 12

Re

ba

se

d =

10

0

Brenntag Brenntag relative to FTSE W Europe Index

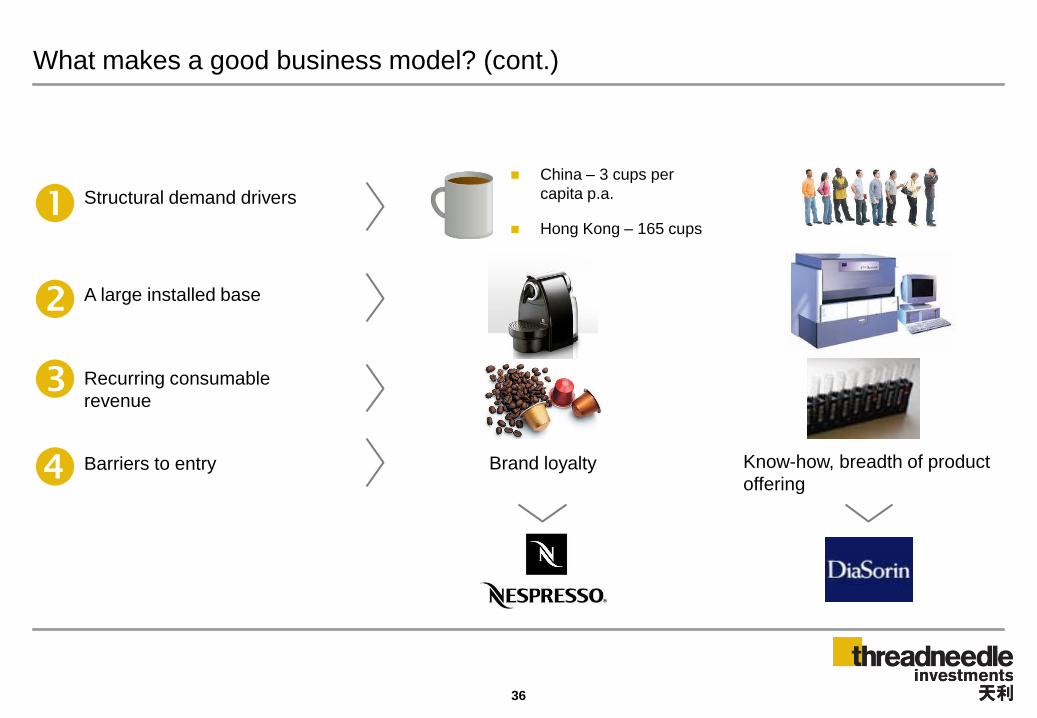

What makes a good business model? (cont.)

36

Structural demand drivers

A large installed base

Recurring consumable

revenue

Barriers to entry Know-how, breadth of product

offering Brand loyalty

China – 3 cups per

capita p.a.

Hong Kong – 165 cups

3iii

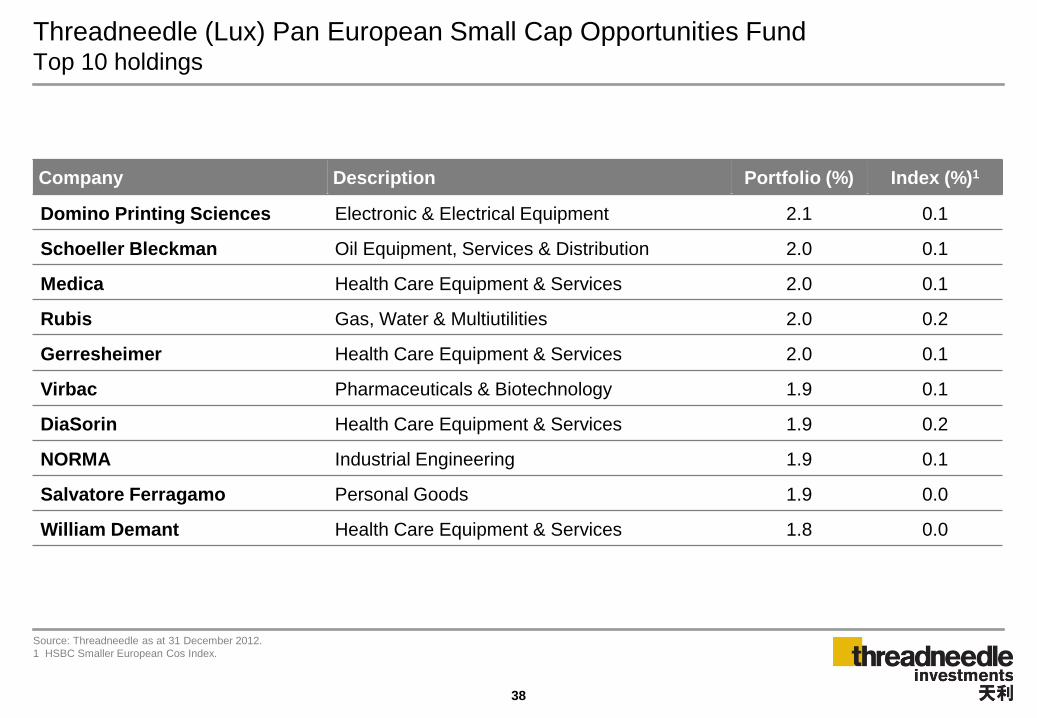

Pan European Smaller Companies Strategy ▪ Threadneedle (Lux) Pan European Small Cap Opportunities Fund

A well-diversified portfolio of smaller company Pan European stocks.

Company Description Portfolio (%) Index (%)1

Domino Printing Sciences Electronic & Electrical Equipment 2.1 0.1

Schoeller Bleckman Oil Equipment, Services & Distribution 2.0 0.1

Medica Health Care Equipment & Services 2.0 0.1

Rubis Gas, Water & Multiutilities 2.0 0.2

Gerresheimer Health Care Equipment & Services 2.0 0.1

Virbac Pharmaceuticals & Biotechnology 1.9 0.1

DiaSorin Health Care Equipment & Services 1.9 0.2

NORMA Industrial Engineering 1.9 0.1

Salvatore Ferragamo Personal Goods 1.9 0.0

William Demant Health Care Equipment & Services 1.8 0.0

Threadneedle (Lux) Pan European Small Cap Opportunities Fund Top 10 holdings

Source: Threadneedle as at 31 December 2012.

1 HSBC Smaller European Cos Index.

38

Threadneedle (Lux) Pan European Small Cap Opportunities Fund Sector weightings

Source: Threadneedle as at 31 December 2012. Excludes cash at 1.7%.

1 HSBC Smaller European Cos Index.

Sector Portfolio (%) Index (%)1

Industrials 30.8 25.4

Health Care 18.7 6.6

Consumer Goods 12.4 10.2

Financials 11.7 21.8

Basic Materials 8.0 6.1

Oil & Gas 5.7 7.0

Technology 4.3 6.1

Consumer Services 3.1 13.5

Utilities 2.0 1.8

Telecoms 1.6 1.4

Unclassified 0.0 0.1

0%

5%

10%

15%

20%

25%

30%

35%

Industr

ials

Health C

are

Consum

er

Goods

Fin

ancia

ls

Basic

Mate

rials

Oil

& G

as

Technolo

gy

Consum

er

Serv

ices

Utilit

ies

Tele

com

s

Uncla

ssifie

d

Fund Index

Threadneedle (Lux) Pan European Small Cap

Opportunities Fund

39

Threadneedle (Lux) Pan European Small Cap Opportunities Fund Country profile

Source: Threadneedle as at 31 December 2012. Excludes cash at 1.7%.

Other includes: Greece, Portugal, Malaysia, Peru, Bermuda and US.

1 HSBC Smaller European Cos Index.

Sector Portfolio (%) Index (%)1

UK 23.4 28.0

Germany 20.9 9.8

France 13.7 8.9

Italy 6.6 8.1

Sweden 5.8 7.1

Switzerland 5.2 7.6

Denmark 4.9 2.5

Austria 4.8 2.2

Norway 4.7 4.6

Finland 2.6 3.6

Netherlands 1.9 3.5

Ireland 1.3 1.5

Israel - Domestic 0.9 0.0

Belgium 0.8 3.2

Spain 0.6 5.1

Other 0.0 4.2

0%

5%

10%

15%

20%

25%

30%

35%

UK

Germ

any

Fra

nce

Italy

Sw

eden

Sw

itzerland

Denm

ark

Austr

ia

Norw

ay

Fin

land

Neth

erlands

Irela

nd

Isra

el -

Dom

estic

Belg

ium

Spain

Oth

er

Fund Index

Threadneedle (Lux) Pan European Small Cap

Opportunities Fund

40

Threadneedle (Lux) Pan European Small Cap Opportunities Fund

Source: Style Research as at 31 December 2012.

Style Analysis - Portfolio Style SkylineTM

41

Elekta

Porter’s Five Forces

1 Source: Datastream, as at 31 December 2012, in local currency (Swedish Krona).

2 Source: Bloomberg, as at 24 January 2013.

The mention of stocks is not a recommendation to deal.

42

+ Growth

EM healthcare spend

Increasing cancer

incidence

Ageing population

Reducing

(e.g. Siemens

quitting sector)

Degree of rivalry

Technology

Regulatory approval

References

Barriers to entry

Low

Other oncology

treatment

Threat of

substitution

Main input is own

intellectual

property

Supplier power

Medium (high-cost

product)

Buyer power

Absolute performance and relative strength

2-year performance¹

Year to April2 2013e 2014e

P/E 25.2x 20.8x

EV/EBITDA 16.0x 13.8x

RoE 27% 27%

80

100

120

140

160

180

Dec 10 Apr 11 Aug 11 Dec 11 Apr 12 Aug 12 Dec 12

Re

ba

se

d =

10

0

Elekta Elekta relative to FTSE W Europe Index

42

William Demant

Porter’s Five Forces

1 Source: Datastream, as at 31 December 2012, in local currency.

2 Source: Bloomberg, as at 24 January 2013.

The mention of stocks is not a recommendation to deal.

43

+ Growth

Ageing

population

Low penetration

Innovation

Absolute performance and relative strength

2-year performance¹

85

95

105

115

125

135

145

155

Dec 10 Apr 11 Aug 11 Dec 11 Apr 12 Aug 12 Dec 12

Re

ba

se

d =

10

0

William Demant William Demant relative to FTSE W Europe Index

Year to Dec² 2012e 2013e 2014e

P/E 23.4x 18.8x 16.6x

EV/EBITDA 15.8x 13.6x 12.4x

RoE 34% 35% 33%

43

Oligopoly

Weak competitors

Degree of rivalry

Scale

R&D investment

Distribution

Barriers to entry

Very low

Threat of

substitution

Low

Supplier power

Very fragmented

But consolidating

Buyer power

Investment Process

AP1

A company‟s intrinsic value is determined by its growth, returns on capital and its sustainable competitive

advantage

The market typically underestimates the potential of some companies to increase their intrinsic value

Targeted research will enable us to identify these companies

European equity philosophy

Our core portfolios tend to display a growth bias

45

European equity investment process

46

Idea generation

Macro and themes

European equity team and other

investment professionals

Company meetings

Implementation

Portfolio construction

Risk management

Research / debate

Stock analysis

Investable universe – 2,400 companies

600 stocks researched

50-70 holdings

Idea generation

47

Company meetings, site visits and contacts

1,200+ meetings each year

Provides insight into competitors, suppliers and wider industry

Daily team meeting and informal discussions

Forum for discussion of short-term news

Interaction with other teams on specific stocks and

themes

Global / credit inputs

Weekly stock reviews

Interpretation of future trends, margins, pricing etc.

Valuation analysis

Quarterly strategy and sector reviews

Industry trends and changes assessed

Stock recommendations

Macro and themes

European Equity team and other

investment professionals

Company meetings

Idea generation

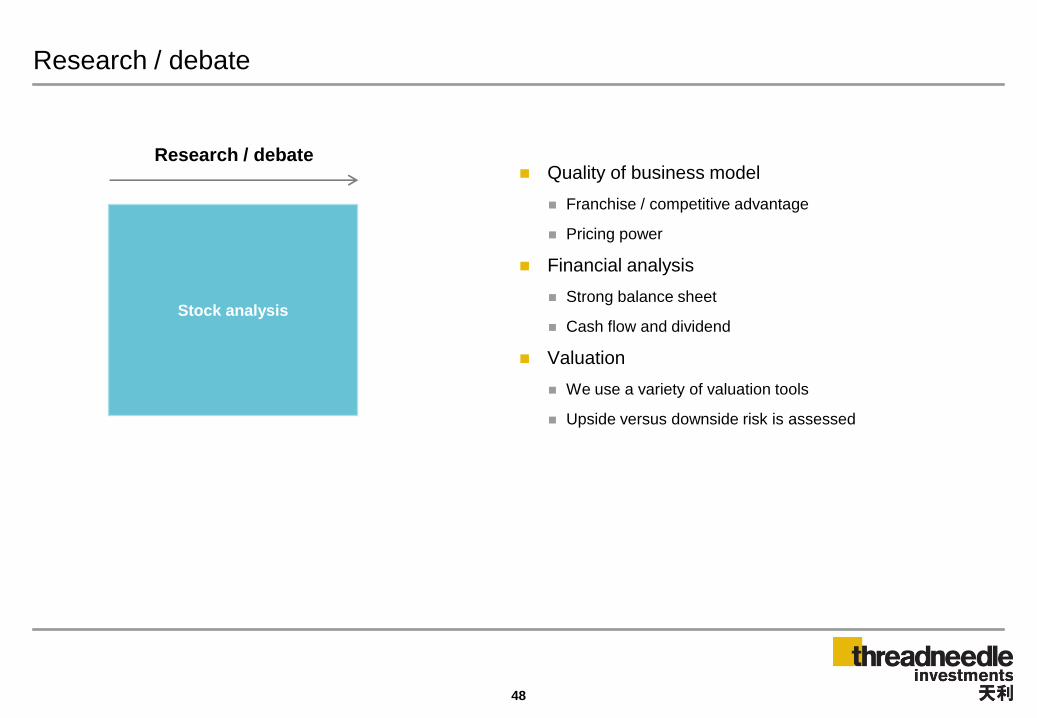

Research / debate

48

Quality of business model

Franchise / competitive advantage

Pricing power

Financial analysis

Strong balance sheet

Cash flow and dividend

Valuation

We use a variety of valuation tools

Upside versus downside risk is assessed

Research / debate

Stock analysis

Implementation

49

Position sizes determined by:

Upside potential

Impact on the portfolio‟s risk exposure

Liquidity

On-going assessment

Holdings monitored against valuation / performance targets

New stock ideas; new themes

Sell discipline

Changing risk / reward characteristics

Competition for capital

Target price reached

Portfolio

Risk management

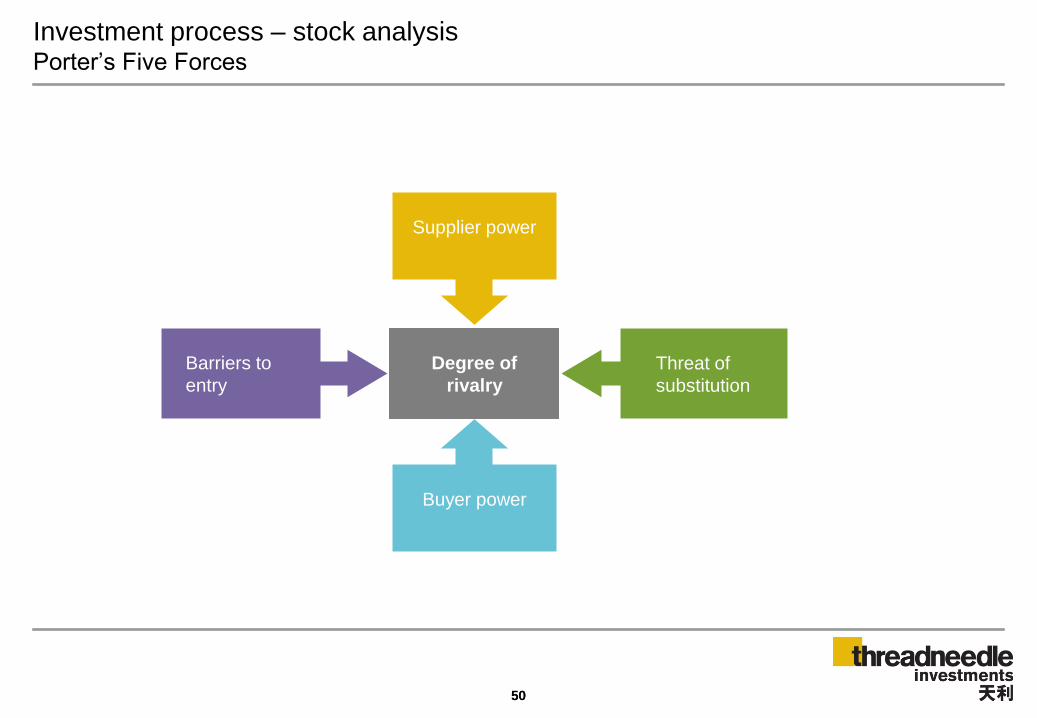

Investment process – stock analysis Porter‟s Five Forces

50 50

Buyer power

Degree of

rivalry

Barriers to

entry

Threat of

substitution

Supplier power

Integrated approach to risk management

Note: The example provided above is for illustrative purposes only.

51

Portfolio managers constantly re-assess

Business risk

Portfolio risk

Benchmark risk

Risk team independently produces comprehensive

daily risk analytics for every portfolio

Proprietary risk modelling system („IRIS‟ – Investment

Risk Information System)

Used to support and enhance portfolio manager decision-

making

Used for management oversight

Risk Committee reviews portfolios quarterly

Daily risk report

52

The research and analysis included in this document have not been prepared in accordance with the legal requirements designed to promote its independence and have been

produced by Threadneedle for its own management activities, may have been acted upon prior to publication and is made available here incidentally. Any opinions expressed are

made as at the date of publication but are subject to change without notice. Information obtained from external sources is believed to be reliable but its accuracy or completeness

cannot be guaranteed. This document is for the sole use of those attending the presentation. It may not be reproduced in any form or passed on to any third party without the

express written permission of Threadneedle. This document is the property of Threadneedle and must be returned upon request.

Past performance of the fund and its manager and any forecasts or information on the economic trends are not necessarily indicative of the future or likely performance of the

fund or its manager or a guarantee of future trends. The price of shares and the income accruing to those shares, if any, may fall or rise and an investor may not get back the

amount invested. Due to the investment policies of the fund, it may experience greater volatility in its net asset value.

Threadneedle does not give any investment advice. The mention of any specific shares or bonds should not be taken as a recommendation to deal. This document is for

informational purpose only and does not constitute an offer or solicitation of an order to buy or sell any securities or other financial instruments or to provide investment advice or

services. Investors are advised to exercise caution. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

A Singapore prospectus (“Prospectus”) can be obtained free of charge from any of our authorized distributors or downloaded from www.threadneedle.com. Investors should read

the Prospectus for further details before deciding whether to subscribe for or purchase shares. The Fund may invest in financial derivative instruments to the extent permitted

under relevant laws. Past performance of the Fund and its Manager and any forecasts or information on the economic trends are not necessarily indicative of the future or likely

of the Fund or its Manager or a guarantee of future trends. The information provided in this document is for informational purpose only and does not constitute an offer or

solicitation of an order to buy or sell any securities or other financial instruments, or to provide investment advice or services. This publication does not have regard to the specific

investment objective(s), financial situation or the particular needs of any person. Investors may wish to seek advice from financial adviser before making a commitment to invest.

In the event of an investor chooses not to seek advice from a financial adviser, the investor should consider whether the Fund is suitable for him. Threadneedle (Lux) is an

investment company with variable capital (Société d‟investissement à capital variable, or “SICAV”) formed under the laws of the Grand Duchy of Luxembourg. The SICAV issues,

redeems and exchanges shares of different classes, which are listed on the Luxembourg Stock Exchange. Threadneedle Management Luxembourg S.A is advised by

Threadneedle Asset Management Ltd. and/or selected sub-advisors. Threadneedle Management Luxembourg S.A has appointed State Street Bank and Trust Company –

Singapore Branch as its Singapore representative.

Issued in Singapore by Threadneedle Investments Singapore (Pte.) Limited, 3 Killiney Road, #07-07, Winsland House 1, Singapore 239519. Regulated in Singapore by the

Monetary Authority of Singapore under the Securities and Futures Act (Chapter 289). License number: CMS100182-1. This document is not a prospectus as defined in the SFA.

Accordingly, statutory liability under the SFA in relation to the content of prospectuses would not apply. Threadneedle Investments is a brand name and both the Threadneedle

Investments name and logo are trademarks or registered trademarks of the Threadneedle group of companies.

Important Information – Singapore