the tax efficient investor

TRANSCRIPT

P R E PA R I N G P O R T F O L I O S F O R C H A N G E

T H E T A X E F F I C I E N T I N V E S T O R

In a low expected return environment, the prospect of changing tax rates has investors rightfully concerned about their bottom line. New research from The Northern Trust Institute sheds light on the potential impact of higher taxes on portfolios and offers tax-efficient strategies for current and expected tax environments.

2 P R E PA R I N G P O R T F O L I O S F O R C H A N G E

Typically, in the wake of a presidential election, the question is not if there will

be tax reform, but when and to what degree. Historically, new administrations,

regardless of party affiliation, propose tax policy changes for Congress to

enact. President Biden is no exception and his tax plan has caught investors’

attention, especially among high net worth investors. Investors’ top concerns

center on a few key elements of the proposed plan, including:

These changes almost always come slowly, as Congress debates the needs,

costs, and specifics of the new administration’s proposals. Rarely are the

resulting tax law changes applied retroactively. In fact, over the past four

administrations, changes took place on average 502 days after inauguration.

And while a few provisions of the 2001 tax law were applied retroactively

under the Bush administration, the only time comprehensive changes were

applied retroactively was in 1993 when President Clinton was in office.

While history is not obliged to repeat itself, it does suggest that any changes

to tax law are likely to provide ample time to understand the implications and

adjust your investment strategy in alignment with your goals. As of the time of

this writing, Congressional debates have not yet begun. But once they do, it is

unlikely, given Congress’ budget reconciliation process, that any change would

take effect until 2022.

37%

20%

39.6%

39.6%

I N C R E A S I N G T H E T O P I N C O M E B R A C K E T L O W E R I N G T H E E S T A T E T A X E X E M P T I O N

E L I M I N A T I N G T H E S T E P - U P I N T A X B A S I S U P O N D E A T H

I N C R E A S I N G T H E T A X R A T E O N L O N G - T E R M C A P I T A L G A I N S A N D Q U A L I F I E D D I V I D E N D S

for those earning more than $400,000 per year

on incomes above $1 million

P R E PA R I N G P O R T F O L I O S F O R C H A N G E3

P U T T I N G T H E P R O P O S E D C H A N G E S I N P E R S P E C T I V E

Recent history provides a helpful guide for interpreting the potential

magnitude of President Biden’s proposed tax changes. Exhibit 1 shows the

highest marginal tax rates on ordinary income and long-term capital gains over

the last 20 years. (Note that a beneficial tax rate on qualified dividends was

introduced under the Tax Relief Reconciliation Act of 2003, with an applicable

tax rate equal to that on long-term capital gains.) As the chart indicates, the

proposed income tax increase is relatively small and would return it to 2013-

2017 levels. In contrast, for investors in the highest tax bracket, the proposed

tax increase on qualified dividends and long-term capital gains is more

significant — and represents a material departure from recent history.

E X H I B I T 1 – H I S T O R I C A L U . S . T A X R A T E S

Source: The Northern Trust Institute

Ordinary Income Potential Income Capital Gains Potential Capital Gains

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

40.0%

35.0%

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0%

P R E PA R I N G P O R T F O L I O S F O R C H A N G E4

P O R T F O L I O I M P L I C A T I O N S O F T H E P R O P O S E D T A X P L A N

At Northern Trust, we have long considered taxes in our annual Capital Market

Assumptions (CMAs) and use after-tax portfolio optimizations to determine our

recommended Strategic Asset Allocation (SAA). Exhibit 2 shows return expectations

for strategic asset classes based on current tax policy and 2020-2021 CMAs:

Based on current tax rates, our return expectations come down 0.9% on average

after-tax across asset classes from their pre-tax forecasts. Under the proposed plan,

those same return expectations decrease 1.4% on average. Risk-control assets (cash,

TIPS, and investment-grade bonds) see a modest decrease in expected after-tax

return because their return is dominated by income, and the increase in the ordinary

income tax rate is modest. The after-tax return profile of municipal bonds remains

unchanged given their income exemption from federal tax.

E X H I B I T 2 - N O R T H E R N T R U S T ’ S C A P I T A L M A R K E T A S S U M P T I O N S ( C U R R E N T )

Source: Northern Trust Investment Policy Committee and The Northern Trust Institute

Pre-Tax Current After-Tax Proposed After-Tax

Priv

ate

Equi

ty

Real

Est

ate/

In

fras

truc

ture

Hig

h Yi

eld

Glo

bal

Equ

ity

Nat

ural

Res

ourc

es

Hed

ge F

und

s

Inve

stm

ent G

rad

e Bo

nds

TIPS

Cas

h

Mun

icip

al B

ond

s

10.0%

9.0%

8.0%

7.0%

6.0%

5.0%

4.0%

3.0%

2.0%

1.0%

0%

10-Y

ear R

etur

n Fo

reca

st

P R E PA R I N G P O R T F O L I O S F O R C H A N G E5

The proposed tax change on long-term capital gains and qualified dividends,

however, is more impactful for after-tax returns. For example, the expected

after-tax return for global equity investments that typically dominate Risk Asset

portfolios would be reduced by an additional 1.1%, for a total reduction of 2.0%

relative to our pre-tax forecast. Asset classes with particularly favorable capital

market assumptions like private equity (-2.6%) and real estate/infrastructure

(-2.5%) are even more impacted.

Exhibit 3 shows how the relative weighting to risk assets, like global equity, largely

influences just how impactful the tax proposals could be for total portfolio returns:

Under current tax policy, we forecast a tax-driven reduction in our Moderate Risk

portfolio of 0.9% on its 5.0% pre-tax return, while our Maximum Risk portfolio

would realize a 1.4% reduction on its 6.5% pre-tax return. If the administration’s tax

proposals were enacted as is, expected after-tax returns for the same Moderate Risk

portfolio would be further reduced by 0.5% (1.4% total), while the Maximum Risk

portfolio would see a further reduction of 0.8% in expected return (2.2% total).

E X H I B I T 3 – E X P E C T E D R E T U R N S B Y R I S K - B A S E D I N V E S T M E N T O B J E C T I V E

Source: The Northern Trust Institute Research of tax-optimized strategic asset allocation models

Pre-Tax Current After-Tax Proposed After-Tax

MaxMod HighModerateMod LowLow

5.0%

4.0%

3.0%

2.0%

1.0%

0%

6.0%

7.0%

2.8%

4.1%

2.5%

3.4%

2.4%

3.1%

3.6%

5.0%

4.1%

5.8%

4.6%

4.0%

6.5%

5.1%

4.3%

P R E PA R I N G P O R T F O L I O S F O R C H A N G E6

F I V E C O R E P R I N C I P L E S F O R T A X - E F F I C I E N T I N V E S T I N G

We believe assets serve a purpose — to fund goals. Therefore, a personal

investor’s overriding investment objective should be to fund lifetime goals

efficiently. While taxes are one of many factors to consider in achieving

that objective, the tax “tail” should not be allowed to wag the “dog” when

developing an investment strategy.

Instead, we advise employing five core principles for tax-efficient investing

should tax reform be enacted as currently proposed.

7 P R E PA R I N G P O R T F O L I O S F O R C H A N G E

R E A L I Z E C A P I T A L G A I N S W H E N N E C E S S A R Y T O F U N D G O A L S O R M A N A G E R I S K

Financial goals – whether funding one’s lifestyle, securing wealth transfer goals,

or philanthropic gifting – should be the primary driver of your investment

strategy and wealth plan. Efficient goal funding considers the timing, magnitude

and priority-level of each individual goal. The overall goal profile provides a

roadmap of necessary liquidity events, with implications for optimal asset-goal

alignment through time. For example, if the step up in tax basis is eliminated,

low-basis assets may be better suited to fund philanthropic goals than wealth

transfer goals. Similarly, occasional gains may need to be taken to fund your

lifestyle goals efficiently over time and to keep your portfolio aligned with your

risk preferences. Periodic rebalancing may be necessary to manage risk and

maintain robust diversification across and within asset classes even though it

may incur capital gains tax.

A V O I D R E A L I Z I N G C A P I T A L G A I N S U N N E C E S S A R I LY

Although short-term and long-term capital gains would be taxed at the same rate

under the proposed plan, your after-tax return would still benefit from longer

holding periods due to deferral of the capital gains tax. In fact, the difference

in after-tax returns over time is even greater with higher capital gains tax rates.

Longer holding periods also preserve optionality should future tax changes revert

to a lower long-term capital gains tax rate, as has happened in the past.

M I N I M I Z E T A X A B L E I N C O M E W I T H O U T U N D E R M I N I N G D I V E R S I F I C A T I O N

Interest income tax is no less onerous than dividend income tax under the

proposed plan, making interest income relatively more attractive than it is under

current tax rules. However, despite gains being taxed at the same rate, long-term

capital gains would still benefit from a lower overall tax burden than interest or

dividend income due to the after-tax return compounding benefit of the tax

deferral. We caution, however, that tax strategies focused blindly on minimizing

dividend or interest income can undermine portfolio efficiency by producing

undesired concentrations and risk exposures.

1

2

3

P R E PA R I N G P O R T F O L I O S F O R C H A N G E8

E M P L O Y A S S E T L O C A T I O N T O M A X I M I Z E R E T U R N C O N T R I B U T I O N A N D D I V E R S I F I C A T I O N B E N E F I T S

Interest income, dividend income, and realized capital gains are not taxed in

tax-favored accounts, such as IRAs. Place less tax-efficient assets, such as high-

yield and other taxable bonds, real estate investment trusts, high-dividend

equity and high-turnover active strategies, in tax-favored accounts. However,

when using asset location to mitigate taxes, it is important to do so within

a broader framework that considers overall portfolio diversification across

taxable and tax-favored accounts, and goal-funding liquidity needs over time.

U S E A F T E R - T A X P O R T F O L I O O P T I M I Z A T I O N

Find the optimal after-tax mix of asset classes across taxable and tax-favored

accounts. After-tax portfolio optimization can show whether an asset’s

diversification benefit outweighs an otherwise less-efficient tax profile. After-

tax portfolio optimization is the gold standard, as it simultaneously solves the

asset allocation and asset location problem. And it can sometimes override the

other principles detailed above.

4

5

P R E PA R I N G P O R T F O L I O S F O R C H A N G E9

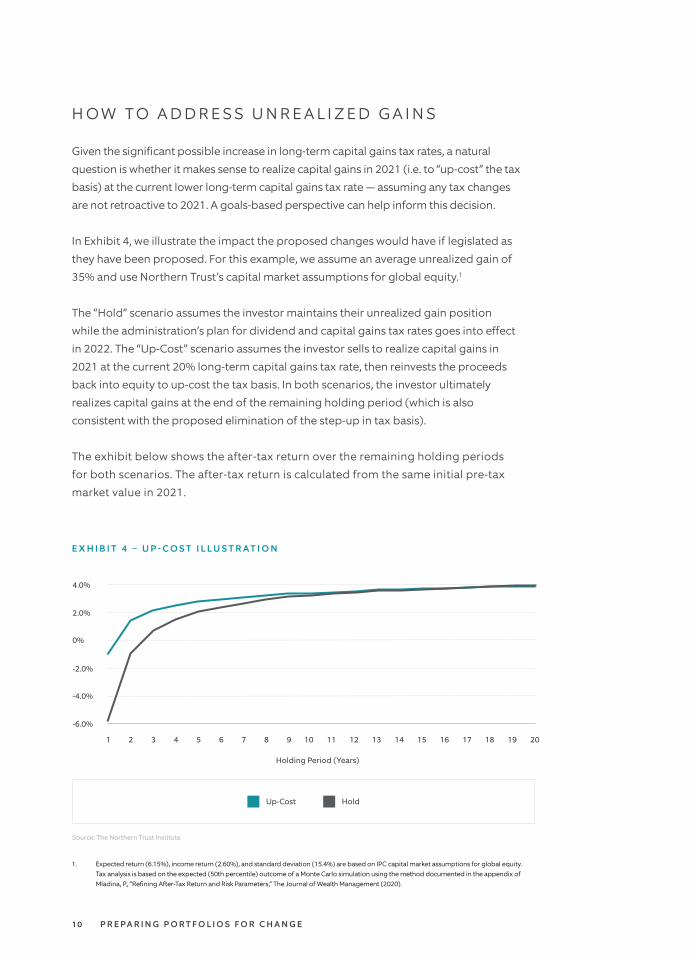

H O W T O A D D R E S S U N R E A L I Z E D G A I N S

Given the significant possible increase in long-term capital gains tax rates, a natural

question is whether it makes sense to realize capital gains in 2021 (i.e. to “up-cost” the tax

basis) at the current lower long-term capital gains tax rate — assuming any tax changes

are not retroactive to 2021. A goals-based perspective can help inform this decision.

In Exhibit 4, we illustrate the impact the proposed changes would have if legislated as

they have been proposed. For this example, we assume an average unrealized gain of

35% and use Northern Trust’s capital market assumptions for global equity.1

The “Hold” scenario assumes the investor maintains their unrealized gain position

while the administration’s plan for dividend and capital gains tax rates goes into effect

in 2022. The “Up-Cost” scenario assumes the investor sells to realize capital gains in

2021 at the current 20% long-term capital gains tax rate, then reinvests the proceeds

back into equity to up-cost the tax basis. In both scenarios, the investor ultimately

realizes capital gains at the end of the remaining holding period (which is also

consistent with the proposed elimination of the step-up in tax basis).

The exhibit below shows the after-tax return over the remaining holding periods

for both scenarios. The after-tax return is calculated from the same initial pre-tax

market value in 2021.

1. Expected return (6.15%), income return (2.60%), and standard deviation (15.4%) are based on IPC capital market assumptions for global equity. Tax analysis is based on the expected (50th percentile) outcome of a Monte Carlo simulation using the method documented in the appendix of Mladina, P., “Refining After-Tax Return and Risk Parameters,” The Journal of Wealth Management (2020).

E X H I B I T 4 – U P - C O S T I L L U S T R A T I O N

Source: The Northern Trust Institute

Up-Cost Hold

Holding Period (Years)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

4.0%

2.0%

0%

-2.0%

-4.0%

-6.0%

P R E PA R I N G P O R T F O L I O S F O R C H A N G E1 0

T A X E F F I C I E N T I N V E S T I N G

The final form of any future tax law change is uncertain, and history tells

us any changes may not endure as economic and political environments

shift. The key to successfully maneuvering through the unknown is to have

an investment strategy and wealth plan that can easily adapt to changing

circumstances and evolving goals. That is what Goals-Driven Wealth

Management at Northern Trust is all about.

The up-cost scenario outperforms over holding periods of one to about ten years.

At ten years, the difference in annualized after-tax return decreases to about

0.20%. After ten years, the difference is immaterial until it slightly benefits the Hold

scenario over long holding periods.

These results suggest that up-costing equity may be prudent for investors funding

near and intermediate-term (1-10 year) goals. For longer-term goals, the up-cost

benefit dissipates, and investors may choose to retain optionality in the event that

future tax reform lowers the capital gains tax rate.

1 1 P R E PA R I N G P O R T F O L I O S F O R C H A N G E

© 2021 Northern Trust Corporation The Northern Trust Company Member FDIC • Equal Housing Lender

This document is a general communication being provided for informational and educational purposes only and is not meant to be taken as investment advice or a recommendation for any specific investment product or strategy. The information contained herein does not take your financial situation, investment objective or risk tolerance into consideration. Readers, including professionals, should under no circumstances rely upon this information as a substitute for their own research or for obtaining specific legal, accounting or tax advice from their own counsel. Any examples are hypothetical and for illustration purposes only. All investments involve risk and can lose value, the market value and income from investments may fluctuate in amounts greater than the market. All information discussed herein is current only as of the date of publication and is subject to change at any time without notice. Forecasts may not be realized due to a multitude of factors, including but not limited to, changes in economic conditions, corporate profitability, geopolitical conditions or inflation. This material has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Northern Trust and its affiliates may have positions in, and may effect transactions in, the markets, contracts and related investments described herein, which positions and transactions may be in addition to, or different from, those taken in connection with the investments described herein.

LEGAL, INVESTMENT AND TAX NOTICE. This information is not intended to be and should not be treated as legal, investment, accounting or tax advice.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. Periods greater than one year are annualized except where indicated. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.

Northern Trust 50 South La Salle Street Chicago, IL 60603

866-296-1526

N O RT H E R N T R U S T. C O M / I N S T I T U T E