the role of covenants in venture capital investment ... · pdf filetechnology and commerce....

TRANSCRIPT

The Role of Covenants

in Venture Capital Investment Agreements

Barbara Cornelius and Colin Hargreaves

No. 59 - October 1991

ISSN 0 157-0188

ISBN 0 85834 973 6

The Role of Covenants

in Venture Capital Investment Agreements

by

Barbara Cornelius

Dept of Accounting and Financial Management

University of New England

and

Colin Hargreaves

Dept of Econometrics

University of New England

@ Copyright: Cornelius and Hargreaves, 1991

The Role of Covenants

in Venture Capital Investment Agreements

i. Introduction

An investment agreement, in venture capital, describes the terms

and conditions that the investor (the venture capitalist) and the

investee (the entrepreneur) will try to abide by throughout the

period of their mutual involvement. These agreements are

comprised of several parts. Included are descriptions of the

securities to be used, the valuation of these securities and if

any, the collateral supporting debt. There is also a section

of representations and warranties where the parties to the

agreement specify that the information upon which the investment

was decided is true and accurate. There are detailed sections

which state who is responsible for which fees and services that

occur with closing the agreement. Specific statements of

documentary evidence that must be made available at closing and

other miscellany are also included in the agreement.

The part of the investment agreement under consideration

herein is that section which refers to particular covenants,

affirmative and negative. It was hypothesized that venture

capital investors would use covenants to provide them with

control over the management of their investee firms with a

consequent reduction in the riskiness of their investment. The

necessity for this control arises when there is a separation

between management and ownership. This problem was first defined

by Coase (1937) in his theory of the firm. This paper analyzes

2

the way in which covenants have been used in venture capital

contracts or agreements.

Data Collection

The analysis is based upon information gathered from both

American and Australian venture capitalists. A survey was

carried out using a questionnaire developed and vetted by

practising venture capitalists. The questionnaire was divided

into three sections. Section I requested information about the

respondent’s firm. Section II asked for investment data, ie the

investee stage of development or ISD, the types of securities and

covenants utilized, capital outlaid and ownership received as

well as the degree of agreement reached by investee and investor.

Section III referred to the investee requesting information about

company characteristics including the proportion of ownership

already held by outsiders and the professionalism of those

outsiders.

Potential respondents in Australia were selected from a list

of venture capitalists compiled by the Department of Industry

Technology and Commerce. The original list of forty-four venture

capitalists was reduced to twenty-three who could actually be

contacted. Thirteen of these twenty-three practitioners returned

questionnaires providing data on forty-three separate

investments. American venture capital respondents were randomly

selected from three cities, San Francisco, Chicago and Boston.

These cities were selected because they are known to be major

3

centres of venture capital activity. Thirty-five interviews were

conducted in America returning information on seventy-seven

investment agreements associated with fifteen venture capital

funds.

3. Negotiation of the Contract

Agency theory is based on the separation of ownership and control

(Demsetz, p. 376), (Klein, p. 369). It suggests that management

(the agent or in this case the investee) and the investor will

have divergent interests. That is, the investee will have some

interest in consumption on-the-job while the investor, being

removed from on-the-job consumption will expect alternative

benefits. Investees have the day to day management delegated to

them by the venture capital investor. The investee then, acts

as an agent for the investor making decisions about the

productive use of the investor’s capital. The amount of control

the investee has over the use of this capital varies according

to the ability of the investor to monitor and influence

decisions. This is most commonly done through a position on the

firm’s board of directors. Additional controls are established

through contractual arrangements, covenants, outlined in the

investment agreement.

The approach taken by an investor and investee, when

negotiating an investment agreement, will vary depending upon the

stage of development (risk) reached by the enterprise. While

both negotiators are attempting to gain a profitable position for

4

themselves,

remove the

negotiators.

they must do this in such a way that they do not

incentive to reach an agreement from the other

That is, if either the investor or the investee

feels they cannot negotiate a contract which places them in the

position of being better off than they were before beginning,

they would end negotiations. While this ability to revert to the

status quo as a threat position seems to be intuitively correct

there are a number of problems associated with the assumption.

Depending on the degree of desperation of either negotiator

the willingness to revert to pre-negotiating positions may vary.

For example, if the investee has mortgaged property, borrowed

heavily and has high expectations for profits from the venture

he or she may be dominated by an investor who has alternative

investment possibilities. Similarly, an investee may be able to

dominate an investor who is anxious to close the deal quickly.

The actual conditions under which either party to the

negotiations enters the bargaining arena may alter the utility

of various covenants.

4. Methods Adopted for Analyzing the Use of Different Covenants

We assess the factors influencing a venture capitalist’s decision

to use particular covenants. While we had hypothesised that this

decision is based upon risk considerations associated with the

stage of an investee’s development this hypothesis was quickly

disproven. The significance of the effect of investee stage of

development (ISD) on the choice of covenants was examined through

5

the analysis of contingency tables. Separate results were

determined for each country. At a five per cent (5%) level of

significance, given crosstabulations of sixteen covenants, three

investee stages of development (ISD) and two countries, 4.8 tests

would be expected to be significant. Contrary to expectations

only four of the tests showed any significance between ISD and

stages of development. Three of the significant results were

in Australia. The implications of these tests, especially on one

covenant, were counter-intuitive. This covenant provided for

performance goals to be built into the investment agreement and

was significantly associated with the late expansion stage of

development while one would expezt such covenants to be

associated with the earliest stages of a company’s development.

Two other covenants, one limiting constitutional changes and the

other providing investee buy-back rights, were associated with

even later stages of development. This analysis eliminated the

investee stage of development as a major factor in the selection

of covenants for inclusion in investment agreements.

Logit analysis was used to determine Whether the use of

different covenants was related to specific characteristics of

the investor and investee firms.

the covenants were recorded as

binary dependent variables.

Logit analysis was chosen as

either present or absent, ie

There were sixteen separate

covenants which are defined in Appendix A.

Fifteen covenants were used often enough to be regressed

individually against each of the explanatory variables, described

in Appendix B. No attempt has been made to assess groups of

covenants in a response model because of problems created by

6

multicollinearity of both dependent and independent variables.

What has been determined is the likelihood that any given

covenant would be utilized in an investment agreement given the

direction of the correlation between that covenant and a given

explanatory variable. Logit estimated coefficients provide

information about the probability that particular covenants will

be used given a set of explanatory independent variables. The

explanations for the use of each covenant, following the tables,

are subjective but based ~pon reasoned associations given

extensive experience of the venture capital industry.

5. Analysis of Covenants

While the tables list all the variables that are statistically

associated with the use of each covenant, there is little point

in commenting separately on each association. Appendix B gives

the full definition of the explanatory variables behind the

abbreviations used in the tables.

Table A: Salary limitationsAUSTRALIA

fund age 1.9753,total capital 2.4984investee age 1.9956,valueownershipperceptioncreditor

UNITED STATES BOTH

2.3956-2.7838

2.4305 2.13582.1897

2.3609

* To be significant at a 5% level in Australia a ’t’ statisticof 2.021 was required.

7

The use of the covenant, "salary limitations", is not

associated with the same variables in Australia as in America.

There was, in fact no overlap between these explanatory variables

in the two countries. The use of this covenant in Australia was

more commonly associated with venture funds which had been in the

business the longest. These funds, larger in terms of capital

had a tendency to invest in older and hence more established

investees. By contrast, theAmerican venture capitalists tended

to use this covenant in association with smaller investees (in

terms of value) when. the perceptions of the investor and investee

about the future suzcess or failure of the business did not

coincide. The ability to include this covenant appears to have

also been associated with higher levels of ownership taken by the

investor in the investee.

Table B: Performance goals built into contract

AUSTRALIA UNITED STATES BOTHfund age -2.0578 -2.2127 -3.0244experience 2.3761 2.1993assistance 2.5455 2.9472fund type -2.7492usual size 2.3053# of investments -2.5198early stage -2.0661 -2.3723middle stage 2.3353 2.0118external owners 2.7929 2.4975professionalism ofexternal owners 2.5323external creditorsdebt owed

2.0293 2.52631.99012.1276

8

Covenants building performance goals into the contract could

be explained by some of the same variables in the United States

as in Australia. It was anticipated that an insistence on

performance goals would be~ highly correlated with early stage

investments but, in fact, the only ISD associated with this

covenant was the middle (late expansion) stage of development.

The association of this covenant with younger funds is common

to both countries, however the interpretation of this common

explanatory variable is likely to be quite different in each.

In the U.S., the younger funds are likely to be managed by more

experienced venture capitalists, a correlation supported by the

test statistics here.

is not significantly

performance covenant.

In Australia the experience of management

associated with the selection of a

An additional factor in the selection of

this covenant in Australia appears to be the professionalism of

external equity holders as well as the level of assistance

provided by the investor. Where investors provide higher levels

of assistance (generally associated with larger investments) they

feel justified in demanding particular levels of performance.

Table C: Capital spending limitations

AUSTRALIAbusiness type -2.2788# employed byinvesteefund type# of investmentslate stage ISDv.c.ownership %investee valueperceptions

UNITED STATES

-2.2861-2.6883-2.0676

2.10372.8183

BOTH

-2.5686

-2.17962.11163.1795

-2.01351.9602

9

Capital spending restrictions, in Australia, were imposed

upon service ventures but no other explanatory variables were

significantly associated with the covenant. American venture

capitalists tended to impose capital spending limitations, on

smaller late stage investees, when they had taken significant

ownership positions.

TableD: Dividend limitations

fund ageexperiencetotal capitalassistanceusual size 2.6796investee value 2.4626% held externallyexternal creditor 2.0366outlay 2.0603yr. of investment-2.3151

AUSTRALIA

-2.3266

UNITED STATES

2.12571.9132"

-2.27043.2666

-2.1098

BOTH2.7327

1.9972

3.95873.4830

1.9492" 2.8806

* To be significant at a 5% level in the U.S. a ’t’ statistic of2.00 was required.

The use of dividend limitations can be explained in both

Australia and America on relatively common grounds. When the

investor fund is used to making sizeable investments and their

outlay on the specific investment is large, they will restrict

the use of dividends for the distribution of profits. Again, as

with performance goals, when external investors or creditors are

more professional their association with less experienced venture

capital management seems to result in decisions closely allied

to the decisions of experienced venture capital managers in the

U.S. The differences in significant explanatory variables in the

selection of this covenant are not striking.

i0

Table E: Voting restrictions

AUSTRALIA# employed byinvestor 2.0175total capital# of investmentsusual size 2.3151value 1.9354,outlay 1.9769,external ownersprofessionalism ofexternal owners

UNITED STATES BOTH

3.6514 4.10564.0154 4.28462.8338 2.34803.8614 4.24632.0179 3.08034.7672 5.0389

-2.4025

-2.5720

* To be significant at a 5% level in Australia a ’t’ statisticof 2.021 was required.

Large funds, in terms of both the number of people employed

and total capital (USA), making larger investments in more highly

valued investees, tended to control their investees through

voting restrictions. This was true in both America and

Australia. The existence of less experienced external equity

holders was also associated with the imposition of this covenant

on the investee by professional investors.

Table F: Investor control over number of directors

AUSTRALIAfund age# of investmentsusual size 2.1607value 2.1138v.c. ownership %

UNITED STATES-2.4352-2.0403

2.2061

BOTH

2.2532

No pattern in the use of covenants providing investors with

control over the number of directors can be found that is

associated with both Australia and the United States. Australian

investors include this particular covenant in the investment

ii

agreement when they have made a sizable investment. American

investors enforce a covenant providing them with control over the

number of directors when there is a sizeable level of ownership

taken in the investee. Larger levels of ownership in the

U.S.were correlated with earlier ISDs and smaller outlays of

capital.

Table.G: Investor option to change directors

AUSTRALIA# employed byinvestor 2.3701% held by externalowners 2.0587investor experiencefund agefund typebusiness interestvalue

UNITED STATES

-2.0174-2.9674

3.2575

BOTH

2.0956

-2.19082.357~4

Again, as with the previous covenant, little similarity

about the factors influencing the decision to include a covenant

granting the investors the option to change directors can be seen

between the US and Australia. Larger Australian funds, when

investing in ventures with external equity holders, retain this

option. By contrast less experienced fund managers in less

established funds use this covenant in the USA. Manufacturing

interests of relatively higher value appear to have this covenant

imposed more commonly than other types of investees.

12

Table H: Entrepreneur option to change directors

AUSTRALIA# of investments 2.4784age of investee 2.1458external ownersprofessionalism ofexternal owners

UNITED STATES BOTH

2.8733-2.3419

-2.0134

The entrepreneurs’ option to change directors has no

reciprocity with the investors’ option to do the same. A large

proportion of equity held by external owners of the investee was

significantly associated with the investors selection of this

option while, in both countries, a lack of external owners are

associated with the entrepreneur being granted a similar option.

No particular explanatory variables are strongly associated with

American investor’s use of this covenant. Experienced Australian

entrepreneurs, negotiating with investors who have made a number

of investments are more likely to see the inclusion of this

covenant in their investment agreement.

Table I: Restrictions against changes in the by-laws (articles)

AUSTRALIAfundinvestmentsexperience -2.6796fund age 2.8147late stageinvestees 2.1986investee age 2.8635business interestassistancevalueoutlayexternalcreditors 2.2554debt owedprofessionalism ofcreditorsprofessionalism ofexternal owners -2.1126v.c. ownership %

UNITED STATES

-2.9555

3.1209

2.98412.7957

2.9837

2.4161

BOTH # of

2.5929

2.6063

-2.5437-2.4506

2.27013.4219

3.01842.6503

2.6392

13

Investors in both Australia and America apply covenants

restricting changes in the by-laws or articles to more mature

investees. Mature investees tend to have more creditors, to be

older and at a later stage of development. As a consequence of

age and later ISD, these more mature investees carry less risk

and hence are preferred by less experienced investors. In

America, negative correlations were found between the stage of

development and the assistance provided while positive

correlations existed between ISD and the size of the capital

outlay. The direction of these coefficients, too, support the

contention that restrictions against changes in the articles or

by-laws are associated with investments in later ISDs.

Table J: Key person insurance

AUSTRALIAtotal capital 2.8965# of investments 1.9774,assistance -2.0821# employed byinvestorinvestor experienceage of investee

UNITED STATES

-2.40871.9416"*

BOTH2.2675

2.08082.1007

* To be significant at a 5% level in Australia a ’t’ statisticof 2.021 was required.

** To be significant at a 5% level in the United States a ’t’statistic of 2.000 was required.

The use of key person insurance is significantly associated

with characteristics of the investor rather than of the investee.

However, it is interesting to note that the application of this

covenant appears to come from funds with quite different

characteristics in each country. That is, larger venture funds

14

require key person insurance in Australia while smaller funds

require this insurance in America. In both countries the use of

key person insurance tended to be associated with experienced

investors and more mature investees.

Table K: Buy back rights (entrepreneur’s departure)

AUSTRALIA# of investments 2.9958usual size -2.6545fund agev.c. experiencefund typeassistance 2.9958value 1.9751,outlay 1.9859,v.c. ownership %business interestexternal creditorsprofessionalism~ofexternal creditorsdebt owed

UNITED STATES BOTH

2.3355 2.9624-2.9486

2.5489 2.38522.7327

2.49612.2668

2.5579

2.55912.9066

2.94883.21132.4065

-2.3909

2.2959

* To be significant at a 5% level in Australia a ’t’ statisticof 2.021 was required.

A number of explanatory variables, associated both with the

investor and the investee, are significant factors affecting the

inclusion of investor buy-back rights in an American investment

agreement. The younger U.S. funds, managed by experienced

investors, were more likely to include a covenant allowing them

to buy out the entrepreneur when the investment was sizable and

the investor was taking a large equity interest. Some apparent

overlap with Australian investment strategies exists in that the

investees appear to be those in the middle to later stages of

development (this was ascertained by the inclusion of

professional creditors, high values and large outlays in the U.S

and by the level of assistance in Australia).

15

One difference between the use of this covenant in the two

countries was associated with the usual size of investments made

by the investor group. In Australia the covenant was

significantly associated with venture capital funds that usually

made smaller investments while the opposite was true in America.

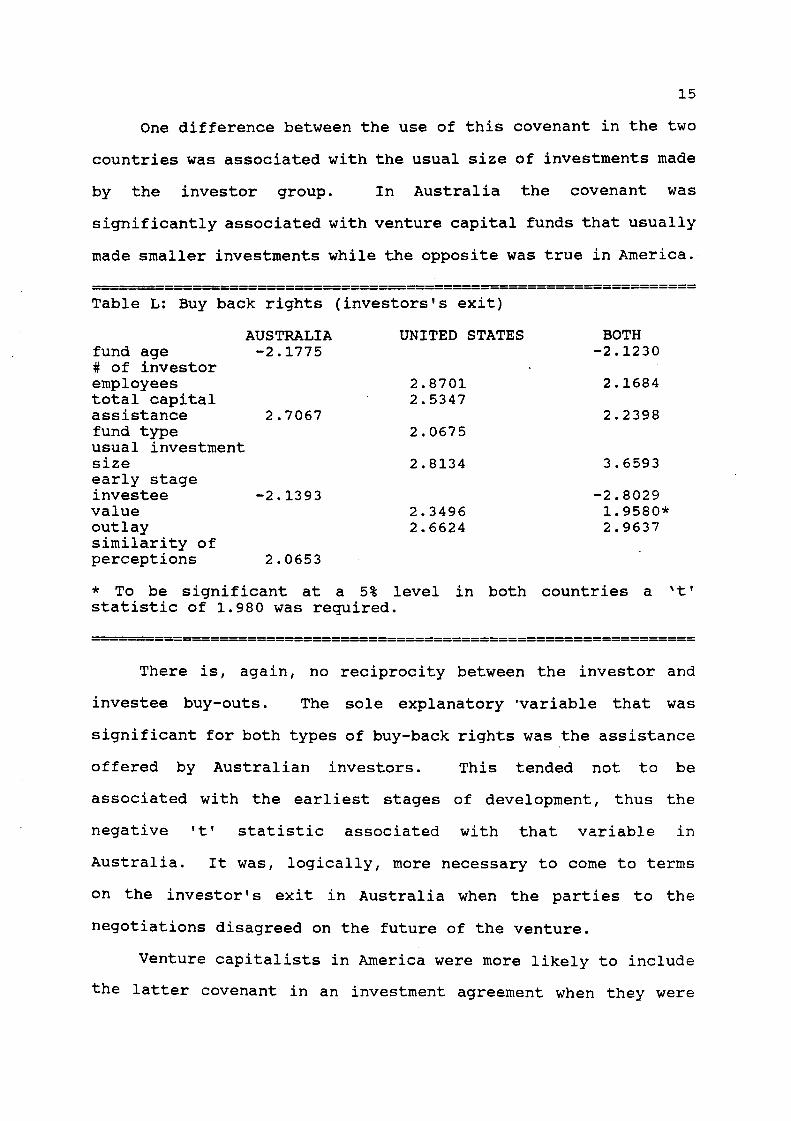

Table L: Buy back rights (investors’s exit)

fund age# of investoremployeestotal capitalassistancefund typeusual investmentsizeearly stageinvesteevalueoutlaysimilarity ofperceptions

AUSTRALIA-2.1775

2.7067

-2.1393

2.0653

UNITED STATES

2.87012.5347

2.0675

2.8134

BOTH-2.1230

2.1684

2.2398

3.6593

-2.80292.3496 1.9580"2.6624 2.9637

* To be significant at a 5% level in both countries a ’t’statistic of 1.980 was required.

There is, again, no reciprocity between the investor and

investee buy-outs. The sole explanatory °variable that was

significant for both types of buy-back rights was the assistance

offered by Australian investors. This tended not to be

associated with the earliest stages of development, thus the

negative ’t’ statistic associated with that variable in

Australia. It was, logically, more necessary to come to terms

on the investor’s exit in Australia when the parties to the

negotiations disagreed on the future of the venture.

Venture capitalists in America were more likely to include

the latter covenant in an investment agreement when they were

16

part of a large investment fund that regularly made sizable

investment outlays in relatively valuable investees. The size,

age, or ISD of the investee had no affect on their judgement.

Table M: Performance bonuses

AUSTRALIA# employees ininvestor fundv.c.experiencelate stage investeevalueexternal owners

UNITED STATES

2.21162.50061.9893"

BOTH

3.1018

1.98752.2769

* To be significant at a 5% level in the United States a ’t’statistic of 2.000 was required.

Covenants granting performance bonuses, were used

infrequently in Australia (9 times in 44 contracts). No

explanatory variables were statistically significantly associated

with its use. Performance bonuses were associated, in the United

States, with large, experienced funds investing in the later

stages of ISD.

Table N: Performance option plans

AUSTRALIA# employees ininvestor fundtotal capitalfund type -2.2429# of investmentslate stage investeeexternal owners 2.4034external owners %outlay

UNITED STATES

3.31762.4741

2.30412.4116

2.40972.1628

BOTH

3.21162.6139

2.31142.25662.02712.85502.3503

17

More than bonuses, option plans were used by large American

funds. They were used for the same later stage investees as were

bonuses. The only statistically significant variable associated

with option plans in Australia is the existence of external

owners. When looking at the combined data, it is clear that this

covenant is used in a similar fashion in both countries.

TableO: Registration rights

AUSTRALIA# employees ininvestor fund 2.1874investor experiencev.c.fund ageinvestee valueperceptions

UNITED STATES

-2.20172.5429

BOTH

3.12542.42372~0768

-2.4146

Larger funds (in terms of the number of employees) in

Australia and small funds in the U.S. were concerned with

registration rights when making their investments. This covenant

was more often included in an investment agreement in both

countries, when an investee was of considerable value and the

investor and investee agreed on its future directions. This

agreement probably included the perception that the firm would

go public.

18

6. Summary of Analysis of Covenants

No patterns of use across all covenants stand out when examining

covenants and significant explanatory variables by country. The

most common explanatory variables in Australia (Table 6.1) are

those associated with the investor fund. Table 6.2 shows that

this is also the case in America. The reference of the covenants

as covenants A to 0 is shown in Appendix A. The experience of

the venture capital management group appears to have little

significance in the selection of covenants in Australia while it

is a major factor in the selection of covenants in the United

States. While it was anticipated that the investee stage of

development would have an impact on the choice of covenants as

well as securities, these correlations do not stand out in the

tables for either country.

It is interesting to note that the number of positive

correlations is nearly double the number of negative correlations

in both Australia and the U.S. Apart from the variables

’assistance’ and ’perceptions’, positive correlations indicate

more mature, larger, or more experienced positions (e.g. catyrank

= professionalism of external owners and catirank = the

professionalism of creditors). This means that covenants are

more often associated with larger funds, larger outlays of

capital, and older, larger investees.

19

Table 6.1: Summary of Covenants A-O and SignificantExplanatory Variables in Australia

Var A B C D E F G H I J K L M N O

numpeoplexpagetotalsassist#investsusua~sze

+ +

+ - + -+ +

+ - + ++ + +

+ + + + -.

earlymiddlelateage2valueoutsider%heldoutcatyrankcreditoroutlayperceptnyrinvest

++ + +

+

++

+

Table 6.2: Summary of Covenants A-O and SignificantExplanatory Variables in America

Variable A B C D E F G H I J K L M

numpeoplexpagetotalsassist#investsusualsze

+

++ +

++

latepeoplnumvalueoutsider%heldoutcatyrankcreditordebtowedcatirank

+ ++ ++ +

N

outlay + +ownershp + + +perceptn +

+

+

+ + + ++ +

2O

Table 6.3: Summary of Covenants A-O and SignificantExplanatory Variables in Australia and the USA

variable A B C D E F G H I J K L M N O

numpeopl + + + +exp + + + +age - + + -totals + + +assist + - +#invests - - + + +usualsze + + + +

+++

early -middle +lateage2 +peoplnumvalueoutsider +%heldoutcatyrank +creditor + +debtowed +catirank

+ +

+ + +

+++

++ +

+

outlayownershpperceptn

Table 6.3 is a result of Logit analysis, variable by

variable, with all cases from both countries that used each

covenant. Here a pattern does emerge more obviously than was

apparent in the individual countries. Although the fund

characteristics are still significant, it is the value of the

investee that plays the greatest part in the selection of

covenants. It will be remembered that "value" was interpreted

differently in Australia than in America. Despite this, value

did increase as ISD increased throughout early and traditional

funding stages in both countries. Other explanatory variables

that are associated with the selection of covenants a third or

more of the time include the age and experience of the investment

21

group as well as the number of investments made. From this it

can be ascertained that experience is influential in the

selection of covenants for investment agreements.

Contingency tables failed to show any relationship between

the use of particular covenants and the investee stage of

development. Because covenants were recorded as binary dependent

variables Logit analysis, performed individually on each covenant

and each explanatory variable, was used to reveal correlations

between them. The most common explanatory variables correlated

to the selection of covenants were those associated with venture

fund characteristics. Covenants were usually correlated with

larger funds, larger investees and more sizeable investments when

each country was examined individually. However, when responses

from the two countries were combined it became obvious that the

major factors influencing the choice of covenants were the value

of the investee and the experience of the investor.

It should be emphasized that the analysis performed here

assessed each covenant individually. Those factors which

influence the selection of these covenants ha~e a distinct effect

on each separately. Covenants themselves are not significantly

correlated and no blocks of covenants can be grouped together.

22

Appendix A: Covenant Definitions

A) Salary limitations: a restriction on increased compensationor withdrawals by anyone involved with the investee over theagreed compensation on a set date. (Gries and Brezic, p.20, 1980)

B) Performance goals built into contract: specified milestoneswhich must be achieved by specified periods or the management isin default on contractual obligations. The investor group willhave specified the actions that they may take in the event ofsuch a default.

C) Capital spending limitations: restricted spending (nothing inexcess of a pre-specified amount) on capital improvements withoutprior approval from the investor group (Gladstone 1988, p.172).

D) Dividend limitations: restricting the distribution of profits,either completely or to a given percentage level, until some settime or until a particular level of profits have been reached.

E) Voting restrictions: a method of controlling investeedecisions through the delegation of voting power to voting trustsor proxies. Investees can be restricted in particular issues,pooling their voting rights with the investor or management maybe given proxies to allow them voting control unless or until atriggering event revokes the proxy (Rollinson in Halloran et al,1982, p.49).

F) Investor control over number of directors: the right of theinvestor group to specify the number of directors on the boardof the investee firm. This specification is made in theinvestment agreement (Ridley in Halloran et al, 1982, p. 18).

G) Investor option to change directors: the investor’s right tochange their board representatives at will.

H) Entrepreneur option to change directors: the investee’s rightto change their board representatives at will.

I) Restrictions against changes in the by-laws (articles): aprohibition of any amendments that would change the operationsof the investee, or affect the rights of the investor without theconsent of the investor (MacDonald and Testa, in Pratt, 1981, p.86) .

J) Key person insurance: indemnity for the investor in the eventof essential people on the entrepreneurial team beingincapacitated.

K) Buy back rights (entrepreneur’s departure): investors, throughtheir ownership in the investee company can arrange the rightfor the company to purchase or "call" in a shareholders shares

23

at a previously negotiated price (Max in Halloran et al, 1982,p.32). Alternatively, the investor can purchase the entrepreneursshares directly and avoid the necessity of paying for thoseshares from profits and paid in surplus.

L) Buy back rights (investors’s exit): an opportunity (orobligation) for the entrepreneur(s) to repurchase shares duringa specified period. These can be organized as redeemable shares(restricted by law) or as a "put" option. A put is a redemptionagreement by the venture to purchase its own shares at apredetermined price. Shares to be purchased only from profitsand paid in surplus (section 107.302/303. Regulation of SBICsand Section 301d licensees, Gerald L. Feigen 1981 p.99).

M) Performance bonuses: usually equity incentives to encourageinvestee management to reach specified goals. The bonus oftentakes the form of increased ownership in the venture.

N) Performance option plans: an equity incentive where managementis given options on shares exercisable in annual incrementsprovided specified conditions have been met (Barton, 1982,p.257).

O) Registration rights: the right of an investor or a group ofinvestors to force a registration with the proper authorities forthe public offering of shares. The contract must specify who paysfor the registration and what percentage of whose shares may beoffered if the offer is limited (Glassmeyer, in Pratt, 1981, p.65).

P) Anti-dilution provisions: a right to maintain a givenownership percentage through a first call on new share offerings.This does not mean that an investors refusal to purchase newshares would prevent the investee from raising those fundselsewhere and diluting the current investors ownership (Marco,1990, p.7).

24

Appendix B: Explanatory Variable Definitions

Name Explanatory Variable DescriPtion

numpeopl Number of People Employed by Investorjrexp Years Experience of Junior Managementexp experience=’(jrexp+srexp)/2’srexp Years Experience of Senior Managementage fund age; Age of Investortotals total capital; Capital under Management by Investorassist assistance; Amount of Management Assistance Providedfund type Type of Investment Fund#invests # of investments; No of Investments made since Startedearly early stage; ISD = seed or start-upmiddle middle stage; ISD=early expansionlate late stage; ISD=late expansion, mezzanine or LBO ,outlay Categories of Capital Investment Sizeownershp ownership %; %age of Ownership given to Investorperceptn perception; Similarities of Investor/InvesteePerceptions

of Futurebusiness type; Category of Investee Businessage2 Investee agepeoplnum # employed by investeenumpeopl # employed by investorvalue Investee Value at time of Investmentoutsider external owners; Whether Investee has External

Shareholders%heldout %age of Investee held by External Shareholderscatyrank Professionalism of External Shareholder in Investeecreditor Whether Investee had External Creditorsdebtowed Size of Investees External Debtcatirank Professionalism of External Creditor of Investeeusualsze usual size; Usual Size of Investors Capital Investmentsyrstart Year Investee Company Startedyrinvest yr. of investment; Investment Year

25Bibliography

Adler, F.R.,1984, "l’he venture capital business" IMEADE conference paper, June

Anderson, P.,1991, "Legal doubt on partner plan", Financial Review, Feb. 22, p.41

Ansley, M.H.,1985, "Warning to brokers against ’going public’ prematurely", FinancialReview, Nov.21, pp31

Australian Federal Tax Reporter, Section 77F, CCH Australia Limited, North Ryde,pp22378-22687

Australian National Companies and Securities Legislation, 7th ed, 1988, vl-2, CC[-IAustralia Ltd. North Ryde

Barton, A.J., 1982, ’"l’he investor’s perspective in structuring a venture capitalinvestment" from Eighth Annual Management Institute conference papers,National Association of Small Business Investment Comp.anies, Washington D.C.,Sept. 24, pp241-258

Blair, F., 1985, "All you ever wanted to know about venture capital", Chicago TechConnection, May/June, pp3-5

Brophy, D., 1984, "Venture capital investment market in the United States", University ofMichigan, ppl-26

Bygrave, W., 1989 Venture Capital Investb~g, a resource exchange perspective, DoctoralDissertation, Boston University

Bylinsky, G.,1967, "General Doriot’s Dream Factory", Fortune, August, pp103-107+

Cailinan and Dimovski, 1985 "Accountants, their clients and MIC’s" The AustralianAccountant, March pp21-23 .-

Campb.ell, J.K.: 1981, Australian Financial System Final Report of the Committee of~nquiry, Australian Government Printing Service, Canberra, September

Chen,A.H. and Kensinger J.W., 1988, "Puttable stock: a new innovation in equityfinancing", Journal of Financial Management, Spring, pp.27-37

Cornelius B.H., 1992, Ph.D. thesis, unpublished, University of New England

Crawford, Sir John, 1979, Study Group on Structural Adjusonent: Report, Australia~JGovernement Printing Service, Canberra,

Dauten, C.A., 1951, "Investment development companies", Journal of Finance, v.VI, #3,September pp276-290

Department Of Industry, Technology and Commerce, 1988, Australian Venture CapitalDirectory, Australian Government Printing Service, June, Canberra

Dizard, J.W., 1982, "Do we have too many venture capitalists?", Fortune Oct.4, pp 106-119

Donham, P.. and Fitzgerald,,, C. 1959, "More reason in small business financing, HarvardBusiness Review, July/August, v37 #4, pp.93-103

Dotzler, Crosspoint Ventures, Public Lecture, 1986, Wayne State UniversityEntrepreneurship Conference, April 29

Espie,Sir Frank, 1983, Developing High TechnoloD, Enterprises for Australia, Australi~nAcademy of Technological Sciences, Victoria, April

Feigen, G. "Regulations of SBICs and Section 301 (d) Licensees" from Seventh AnnualManagement h~stitute conference papers, 1981, National Association of SmallBusiness Investment Companies, Washington D.C., September, pp86-107

Gries and Brezie , 1980, "Representations and warrenties, affirmative and negativecovenants, and events of default which should be included in an SBIC’s financingagreement for an early stage investment", from Seventh Annual ManagementInstitute conference papers, 1981 National Association of Small BusinessInvestment Companies, Washington D.C., September pp.l-26

I-lalloran, M.J. and Hewitt, W.J., 1982, "Venture Capital Fund Formation, Operation andRegulation" from Eighth Annual Management Institute conference papers, 1982,National Association of Small Business Investment Companies, Washington D.C.,September 24, pp9-45

Hoban, J., 1981, "Characteristics of venture capital investmenls", American Journal ofSmall Business, v.Vl, #2, October/December, pp.3-13

Johns,B.C., 1976, Finance for Small Busb~ess in Australia: An Assessment of AdequacT,Australian Government Printing Service, Canberra

Juilland, M.J., 1987, "What do you want from a venture capitalist?", Venture, August,pp.30-35

Juiiland, M.J., 1988, "Strategies for a time of transition" Venture, June, pp31-34

Malitz, I., 1986, "On financial contracting: the determinants of bond covenants", FinancialManagement, Summer, pp.18-25

Management Investment Company Act, 1983, #123 of 1983, Australian GovernmentPrinting Service "

Marco, f., 1990, "Legal documents should help, not hinder venture deals" Venture CapitalJournal, March, pp6-7

McDonald and Testa 1981, "Legal documents of venture fina0cing" in Pratt, S.E., 1981,Guide to Vetlture Capital Sources, 5th ed. Capital Publishing CorporationWellesley Hills MA, pp77-85

Meyers, R.H., 1980, Report of the Committee of Inquiry b~to Technological ChangeAustralia, vl,lll,IV Australian Government Printing Service, Canberra

MICLBAnnual Report 1988-1989, Australian Government Printing Service, Canberra

Miller, D. and Friesen P., 1983, "Successful and unsuccessful phases of the corporate lifecycle", Organization Studies, April 4, pp339-356

Noone, C. Rubel, S. 1970, SBICs: pion.eers hi organized venture capital, Capital Pul~lishingCompany, Chicago

Roberts, J.L., 1983, "Venture firms lack people experience", Wall Street Journal,December 8

Silver, A.D. 1985, Venture Capital: The Complete Guide for htvestors, John Wiley andSons, New York,

Small Business Investment Act of 1958, as amended 1977, Committee of Small Business,House of Representatives, U.S. Governement Printing Office, Washington D.C.

Small Business Investment Company Regulations and ltutex, Oct. 1979, Jan. 1981, ’"Fitle 13,code of Federal Regulations, part 107", National Association of Small BusinessInvestment Companies, Washington D.C.

Smith, C.W., and Warner, J.B.,1979 "On financial contracting: an analysis of bondcovenants", Journal of Financial Economics, #7, pp117-161

Smith, R.G., 1984, "One type of security in retrospect", The Journal of Accounting andBusiness Studies, Sydney University Press, V 20, #2, December pp138-155

77~e Wall Street Journal, 1984,"Who’s got leverage?", June 21, pp28

Van Horn�, Nicol, Wright, 1985, Financial Management in Australia, Prentice Hall ofAustralia Pry. Ltd. Sydney

Venture Capital Journal, 1988, "Citicorp investment management, no longer a banksubsidiary", June 1988, ppl-3

Wan, V, 1986, "Venture capital", in Ratnatunga J. and Dixon, J., Australian SmallBusiness Manual, CCH Australia Ltd. Sydney, pp233-243

Wiltshire, E.M., 1973, Report of the Committee on Small Busb~ess, Department of Tradeand Industry, Australian Government Printing Service, Canberra ’

Annual Reports and other investor data

Advent Western Pacific Ltd. 1987Austech Ventures Ltd. 1986Australian Industry Development Corporation 1987Australian Pacific Technology Ltd. 1986B.T. Innovation Ltd. 1986Barrack Technology Ltd. 1986C.P. Ventures Ltd. 1987Citicorp 1987Commonwealth Development Bank of AustraliaContinental Venture Capital Ltd. 1986Development Capital of Australia Ltd., (information memorandum)H-G Ventures Ltd. 1987InveteehNew South Wales Investment CorporationPrivest Ltd. (prospectus)Small Busineks Development Corporation (W.A.) 1987Stinoc Ltd. (prospectus) ’ ’Techniche Ltd. 1987Victorian Economic Development Corporation 1987Victorian Investment Corporation 1987Westinteeh Innovation Corporation Ltd. 1986

28

Eo~ fi~ ~o~. LunE-Fel Lee and Wllllam E. Grlfflths,No. I - March 1979.

?~an~ ~(od~. HowardE. Doran and Rozany R. Deen, No. 2 - March 1979.

Wllllam Grlfflths and Dan Dao, No. 3 - Aprll 1979.

~uin~. G.E. Battese and W.E. Grlfflths, No. 4- Aprll 1979.

D.S. Prasada Rao, No. 5- Aprll 1979.

~ad~: ~ ~)~.~iaa ~ ~ o~ ~ic32.nr~. Howard E. Doran,No. 6 - june 1979.

~e’~ R~ ~ada~. George E. Battese andBruce P. Bonyhady, No. 7- September 1979.

Howard E. Doran and Davld F. Wllllams, No. 8 - September 1979.

D.S. Prasada Rao, No. 9 - October 1980.

~/~Tus2ixln ~Do22~ - 1979. W.F. Shepherd and D.S. Prasada Rao,

No. I0 - October 1980.

v~ ~~ and ~ex~ Aiar~ R~. W.E. Griffiths andJ.R. Anderson, No. 11- December 1980.

£az/~-O~-~ii Sea~ in tim ~ae~anae o~ M~u~. Howard E. Doranand Jan Kmenta, No. 12 - April 1981.

~&~x~t Orulea ~ ~9~. H.E. Doran and W.E. Griffiths,No. 13 - june 1981.

~tin~ ~ee/d~ ~ox~ Ruie. Pauline Beesley, No. 14 - July 1981.

Yoie/~ ~)oia. Georse E. Battese and Wayne A. Fuller, No. 15 - February1982.

~ge~. H.I. Tort and P.A. Cassldy, No. 16- February 1985.

29

H.E. Doran, No. 17 - February 1985.

J.W.B. Guise and P.A.A. Beesley, No. 18 - February 1985.

W.E. Grlfflths and K. Surekha, No. 19- August 1985.

8t~ Pr~ice~. D.S. Prasada Rao, No. 20 - October 1985.

H.E. Doran, No. 21- November 1985.

~ae-~e~ ~~~/9%e~ ~od~. William E. Grlffiths,R. Carter Hill and Peter J. Pope, No. 22 - November 1985.

~~ ~on. Wllllam E. Grlfflths, No. 23 - February 1986.

~ Doin~ 8tu~. T.J. Coelll and G.E. Battese. No. 24 -February 1986.

~:~xiz~ ~u~ ~ ~ Do/Zz. George E. Battese andSohail J. Mallk, No. 25 - April 1986.

George E. Battese and Sohall J. Mallk, No. 26 - April 1986.

~o~. George E. Battese and Sohall J. Mallk, No. 27 - May 1986.

George E. Battese, No. 28- June 1986.

Nan~. D.S. Prasada Rao and J. Salazar-Carrillo, No. 29 - August1986.

W.E. Grlffiths and P.A. Beesley, No. 30 - August 1987.

William E. Griffiths, No. 31 - November 1987.

H.E. Doran,

Chris M. Alaouze, No. 32 - September, 1988.

3O

G.E. Battese, T.J. Coelll and T.C. Colby, No. 33- January, 1989.

~a~n~Zo~a~~can~-~ide~ode//i~. Colin P. Hargreaves,No. 35 - February, 1989.

William Grlfflths and George Judge, No. 36 - February, 1989.

~anag~o~ 8ani9~ ~o~ ~ani~ ~~. Chris M. Alaouze,No. 37 - April, 1989.

~ ~o ~o~ ~ ~:u~. Chris M. Alaouze, No. 38 -July, 1989.

Chris M. Alaouze and Campbell R. Fitzpatrick, No. 39 - August, 1989.

~o/~. Guang H. Wan, William E. Grlfflths and Jock R. Anderson, No. 40 -September 1989.

o~ ~han~ R~ O/neaatixm. Chris M. Alaouze, No. 41 - November,1989.

~ SAean9 and~~ ~s~a4x~. William Griffiths andHelmut Lfitkepohl, No. 42 - March 1990.

Howard E. Doran, No. 43 - March 1990.

~ YAe XoI#nan ~ to SatZm~tte~-~o~. Howard E. Doran,No. 44 - March 1990.

~e~. Howard Doran, No. 45 - May, 1990.

Howard Doran and Jan Kmenta, No. 46 - May, 1990.

~n~f~ff:~m~/ ~aaiZiea and ~~ ~rdr_2_a. D.S. Prasada Rao andE.A. Selvanathan, No. 47 - September, 1990.

~caaxlrni~ Y~ ui ~ ~ o~ h’ets ~ng~nn~. D.M. Dancer andH.E. Doran, No. 48- September, 1990.

31

D.S. Prasada Rao and E.A. Selvanathan, No. 49 - November, 1990.

~in ~ ~c~. George E. Battese,No. 50 - May 1991.

~~ ~uton~ %G~ ~orun. Howard E. Doran,No. 51 - May 1991.

~e~~on-~eated ~o~. Howard E. Doran, No. 52 - May 1991.

~aa%~ ~. C.J. O’Donnell and A.D. Woodland,No. 53 - October 1991.

¯ ~ ~ec~. C. Hargreaves, J. Harrlngton and A.M.

Siriwardarna, No. 54 - October, 1991.

Mnn~. Colin Hargreaves, No. 55 - October 1991.

~ROh’~R I/ea~ion 2. O. T.J. Coelll, No. 57 - October 1991.

Barbara Cornelius and Colin Hargreaves, No. 58 - October 1991.