the real facts about health care reform and our community

DESCRIPTION

The Real Facts About Health Care Reform and Our Community. August, 2009 Public Policy and Education Fund, www.ppefny.org Fiscal Policy Institute, www.fiscalpolicy.org New Yorkers for Fiscal Fairness, www.abetterchoiceforny.org. Myths About Health Care Reform. What have you heard? - PowerPoint PPT PresentationTRANSCRIPT

The Real Facts About Health Care Reform and Our Community

August, 2009

Public Policy and Education Fund, www.ppefny.orgFiscal Policy Institute, www.fiscalpolicy.org

New Yorkers for Fiscal Fairness, www.abetterchoiceforny.org

2

Myths About Health Care Reform

What have you heard? Some things we’ve heard:

Your health care will be rationed Reform will create a big government bureaucracy Reform will lead us down a path towards

“government-encouraged euthanasia” More on these myths later, but these 3

claims are all untrue!

3

What We’ll Discuss

1. House and Senate Bills: The major provisions and the facts as to how they impact you and me: e.g. insured and uninsured, small business owners

2. Debunking the myths: What the right-wing opponents of reform are saying and the truth

4

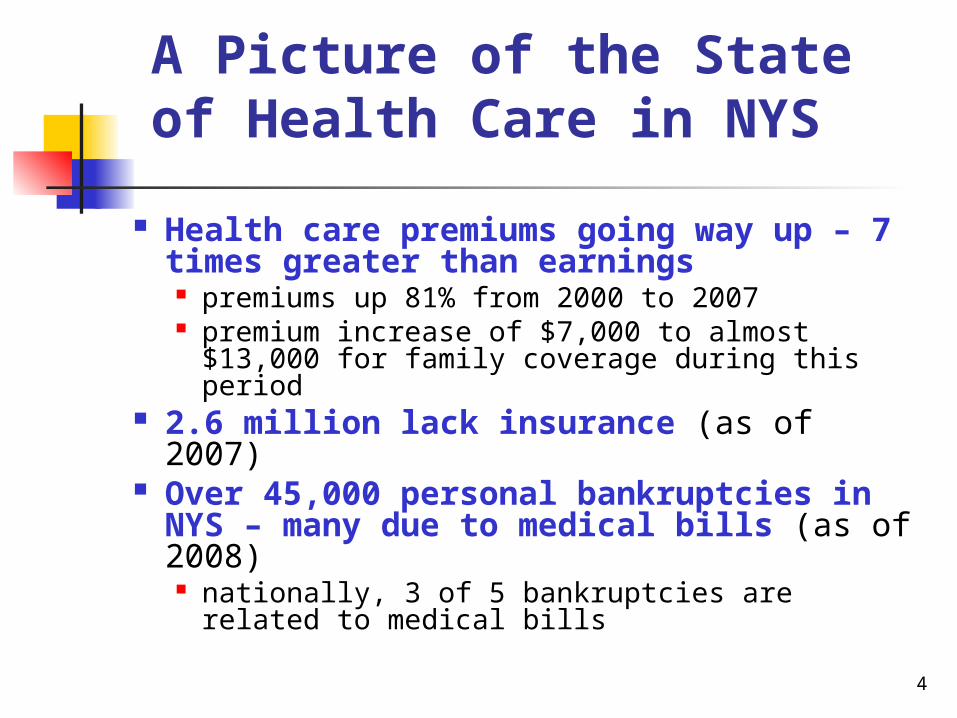

A Picture of the State of Health Care in NYS

Health care premiums going way up – 7 times greater than earnings premiums up 81% from 2000 to 2007 premium increase of $7,000 to almost

$13,000 for family coverage during this period

2.6 million lack insurance (as of 2007) Over 45,000 personal bankruptcies

in NYS – many due to medical bills (as of 2008) nationally, 3 of 5 bankruptcies are related to

medical bills

5

Overview of Health Care Reform and Congress

There are two major bills: Senate HELP Committee: Affordable Health

Choices Act Senate Finance Committee has issued policy

papers, but no bill House “Tri-Committee:” H.B. 3200 (America’s

Affordable Health Choices Act of 2009)

Next: What these proposals have in common, and a

few differences…

6

Overview of the Bills All individuals must obtain coverage “Exchanges” will be set up through which

individuals and smaller employers can purchase health coverage: like “shopping malls” where you can buy the

health care you need a means for small businesses and individuals,

who pay the highest costs, to pool their resources to get cheaper health insurance

all plans subject to same standards subsidies provided for individuals/families up to

400% of FPL (about $88,000/year) to buy insurance

7

Overview of the Bills (continued)

“Exchanges” offer a choice of public and private plans Problem: exchanges and therefore the

public plan won’t start going into effect until 2013 (under House bill)

Employers must offer coverage or pay a fee towards providing coverage (“pay-or-play”)

Medicaid expanded: to 150% FPL (Senate) or 133% FPL (House)

8

Individual Mandate

All individuals must obtain coverage with penalties if you don’t: maximum tax penalty of $750 in Senate

plan under House plan penalty is based on your

income, which is capped at the cost of the average premium

Exemptions from mandate: where affordable coverage isn’t available

(Senate) or financial hardship (House)

9

Health Insurance for Employees: House Bill

Most employers must “pay” or “play”. They must either: contribute 72.5% of premium costs for single coverage (65%

family coverage) for their employees or pay 2% to 8% of payroll into the exchange to ensure

employees get coverage (depends on payroll size) Keep in mind: small businesses with workers that

don’t have high average wages will get help in the form of a tax credit to pay for their employees’ health insurance

Exemptions from “pay or play:” annual payroll less than 500,000 employers negatively affected by job losses as a result of the

pay or play requirement Less than 4% of small businesses are subject to the

penalty for not obtaining coverage for their employees

10

Health Insurance for Employees: Senate Bill

Most employers must “play” or “pay”. They must either: contribute 60% of premium costs or pay $750 for each employee not

offered coverage Exemptions:

employers with 25 or fewer employees

11

Tax Credits for Small Businesses

Smaller employers (less than 50 employees, Senate; 25 employees, House) with smaller average payrolls will be eligible for a tax credit to help them cover health insurance costs for their employees

House credit: up to 50% of insurance premiums 471,300 small businesses in New York State would

quality for the House credit If you work for a company that doesn’t provide

insurance under the law, you can always go the health insurance “exchange” (shopping center) to purchase insurance on your own. That’s next…

12

Subsidies for Individuals to Buy Coverage: House & Senate Plans

Individuals, families up to 400% of the FPL (about $88,000 a year for a family of four) get subsidies, on a sliding scale that caps how much you have to pay for premiums based on your income

Examples of the premium subsidy in the House bill: family of 4 annual income of $29,000-$33,000: your premium

limited to 1.5% - 3% of income family of 4 annual income of $44,000-$55,000: your premium

limited to 5.5% – 8% of income family of 4 annual income of $88,000: your premium limited to

12% of income Senate premium subsidy:

family of 4 annual income of less than $33,000: your premium limited to 1% of income

family of 4 annual income of less of $88,000: your premium limited to 12.5% of income

*All income levels have been rounded off to the nearest $1000

13

Subsidies (cont.): Limits on “Out-of-Pocket” Expenses

House and Senate both also limit how much individuals and families will have to pay each year “out-of-pocket” Examples: deductibles, drug costs

Intent of the limits: to avoid bankruptcy or other financial disasters due to medical bills

These limits on “out-of-pocket” costs, called “cost-sharing” limits, are generally based on your income (see next slide)

14

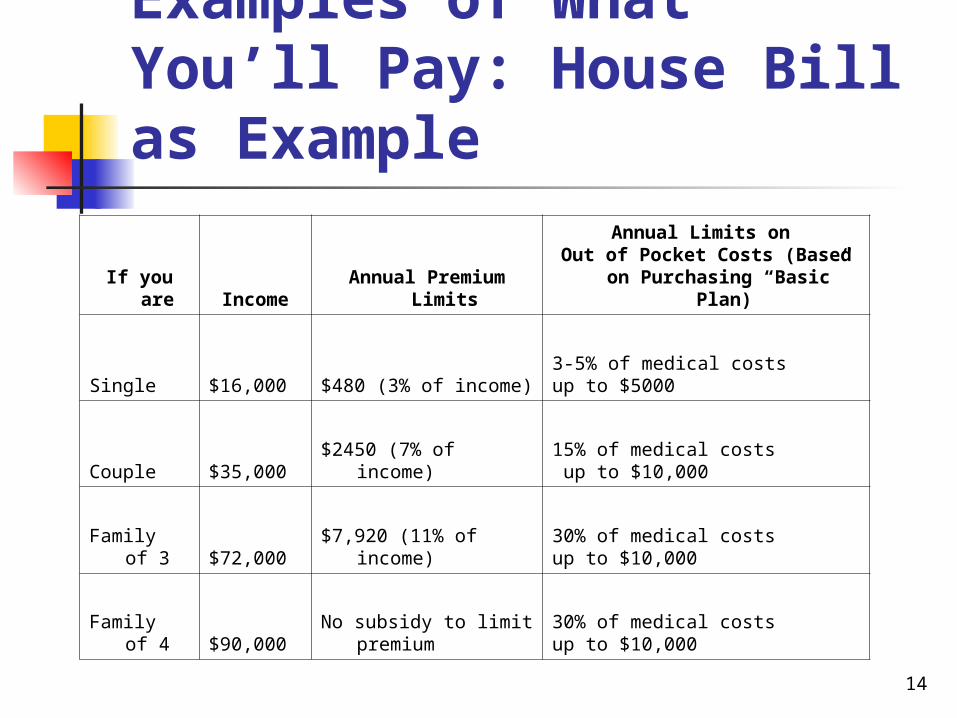

Examples of What You’ll Pay: House Bill as Example

If you are Income Annual Premium Limits

Annual Limits on Out of Pocket Costs (Based on

Purchasing “Basic” Plan)

Single $16,000 $480 (3% of income)3-5% of medical costs up to $5000

Couple $35,000 $2450 (7% of income)15% of medical costs up to $10,000

Family of 3 $72,000 $7,920 (11% of income)30% of medical costsup to $10,000

Family of 4 $90,000 No subsidy to limit

premium30% of medical costsup to $10,000

15

Choice of a Public Plan Through the Exchange

Exchanges, once established, will offer a public plan which meets the same requirements as private plans concerning benefit levels, provider networks, consumer protections, costs, etc.

Theory: to compete with the private plans and keep costs down

Who Can Enroll in Exchange and Public Plan: House bill: Eligibility for exchanges, and therefore

public plans generally limited to those not covered by existing private insurance, employer-coverage, Medicare or Medicaid

Senate bill: Eligibility for exchanges, and therefore public plans generally limited to those not eligible for employer-sponsored coverage, and those who have Medicare or Medicaid

16

Choice of a Public Plan Through the Exchange (cont.)

Problems: There are problems with the current public plan provisions in addition to the limitations on enrollment in the previous slide. For example, under House bill:

you can’t enroll in an exchange and therefore a public plan until at least 2013

the number of employers that can participate is very limited: In 2013, only employers with 10 or fewer employees can

participate In 2014, only employers with 20 or fewer employees can

participate Beginning in 2015, federal agency administering public option

may, but isn’t required to, expand to larger employers Generally, if you have coverage through your employer, you

can’t enroll. People with employer coverage, however, can get assistance with the employee share of the premiums if they are too high (at least under the House bill)

Despite the problems, we must fight to: stop the attacks on the public plans by the opponents of

reform keep the public option provisions as strong as possible

17

Next Section – Impact on Certain Groups

We’ve already dealt with certain major groups of consumers, for example, individuals insured through their employer

Now, we’ll cover: uninsured or people without employer insurance people who already have employer-provided

insurance people with Medicare immigrants our community as a whole!

18

If You Need to Purchase Insurance on Your Own or are Uninsured

If who purchase insurance on your own (“direct-pay”) rather than through a group, you pay the most of everyone

And everyone’s insurance is going up and up: 81% from 2000 to 2007 in NYS

The bill expands eligibility for Medicaid – so if you previously made too much to qualify, you might under the new law

If you still make too much for Medicaid, the House and Senate plans subsidize health insurance for individuals purchasing through the health insurance “shopping mall”

Bottom line: you can get insurance, and if you already have it, your health insurance costs should go down significantly

You don’t need to worry anymore about being denied coverage for a pre-existing condition

19

If You Already Have Insurance Through Your Employer

You will be able to keep the plan your employer provides. (In fact, you’re generally not eligible to enroll in the exchange.)

However, you will enormously benefit from the reform legislation in Congress:

new rules like banning pre-existing coverage limitations and rescissions will protect you too

the competition from other plans in the exchange, including the public plan, will keep your premiums down

people with employer coverage can get assistance with the employee share of the premiums if they are too high (at least under the House bill)

20

If You Have Medicare

You will continue to be covered by Medicare and the program is being improved

Under the House bill: 215,200 seniors in New York State who have hit the

“donut hole” will save 50% on their drug costs in the short term

and the donut hole will be closed over a number of years

co-payments and deductibles will be eliminated for preventative services

Greater focus on prevention and management of chronic diseases will lower program costs, protecting the program long-term

21

If You Are An Immigrant We think it’s the right thing for Congress to help all

people -- including undocumented immigrants -- connect with quality, affordable health care and ask them to pay their fair share

Immigrants pay taxes; it’s not fair to exclude them from purchasing insurance through exchanges or Medicaid

The current health care reform bills: explicitly prohibit federal dollars from being used for

health insurance for undocumented workers, including for subsidizing health insurance through the exchanges (bad provision)

keep the current five-year waiting period for Medicaid for lawfully residing immigrant adults (also bad provision)

apparently allow undocumented immigrants to purchase insurance through the exchanges, but without the subsidy others will get (mixed provision)

allow subsidies to purchase insurance for lawfully residing (documented) immigrants (good provision)

22

Impact on Our Entire Community

Impact in New York State of the House bill: hospitals and health care providers in New

York State receive billions in aid to care for the uninsured (“uncompensated care”)

1.7 million uninsured in the state coveredHealth care for all will significantly help

both our residents and our economy!

23

Debunking the Myths

Right-wing politicians and well-funded lobbyists and

“Astroturf” activists are spreading myth

after myth about reform.

Let’s review a few ones we haven’t discussed yet…

24

Myth: Your Health Care Will Be Rationed This claim is seriously misleading. The current bills expand the number of

people covered and the benefits people will receive

Under current system, care is “rationed” every day by private insurers through: pre-existing conditions and rescissions unaffordable policies and unaffordable care arbitrary decisions by insurance companies

These practices would be ended or limited

25

Myth: Public Plan Will Result in a Big Government Bureaucracy

Again, this claim is seriously misleading. Do you like the current system in which private insurance

company bureaucrats stand between you and your doctor?

Under current system, insurance company “bureaucrats:”

deny coverage despite what your doctor says search people’s private health records to charge high premiums enforce pre-existing coverage limits

Study after study: government programs like Medicare are more efficient

Government’s role will be to set standards, not make individual decisions on coverage. Government is more accountable than profit-maximizing insurance companies

26

Myth: Next step is Canadian-Style “Single-Payer” System

Not true. While many of us feel single-payer is highly

desirable, the reality is that single-payer is not being considered seriously by Congress

There will an American solution to health care – a mixture of public and private providers

Congress is considering a choice of a public plan and a private plan. No one will be forced into the public plan

If private insurance companies provide competitive services, there’s no reason to fear a government plan will put them out of business

27

Myth: “Government-Encouraged” Euthanasia Not true. FactCheck.org: The claim the House bill

“may start us down a treacherous path toward government-encouraged euthanasia” is “nonsense.” Neither is there any basis to the claim that Congress is setting up “death panels” to decide which patients to euthanize!

The bill permits medical professionals who perform counseling on issues like living wills at the patient’s request to be reimbursed, as with other medical services

Source of myth: Republican House Leader John Boehner & others

28

Myth: Small Businesses Will Be Hurt By Reform Not true: nearly all will be helped. Under the present system, small businesses are being

hurt by: increased costs for health care every year high administrative costs making small business

coverage unaffordable The bills will address these threats to small business Once again:

health insurance “shopping centers” (the exchanges) will help keep small business costs down because exchanges will enable them to pool resources and get better rates

small businesses will have significant subsidies to help them pay for insurance for their employees

less than 4% of small businesses (House bill) are subject to the penalty for not obtaining coverage for their employees

29

Other Myths These other claims are also not true:

Private plans will be outlawed Health reform will pay for abortions (not that there’s

anything wrong with that!) Reform will give government access to everyone’s

bank accounts Opponents will keep engaging in

distortions and outright lying. Solution: consult these good sources for truthful information:

Congressional committees Kaiser Family Foundation Media Matters Health Care for America Now

30

Summing Up Health care for all will have a positive impact on

our community

The facts show that reform will help: people who currently have insurance and those without people who purchase insurance on their own seniors small business owners hospitals and health care providers our community as a whole!

We need to ignore the scare tactics of insurance companies, corporations and lobbyists with a vested interest in opposing change

31

Selected Major Sources

House Committee on Ways and Means

Kaiser Family Foundation Center for Policy Analysis Health Care for America Now