the post-crisis fiscal outlook and strategies for fiscal ... · fiscal stimulus: 3 ½ financial...

TRANSCRIPT

1

Sovereign Balance Sheet and Accounting

for the Fiscal Response to the Global

Financial Crisis

Marco Cangiano

IMF – Fiscal Affairs Department

10th Annual OECD Public Sector Accruals Symposium

Paris, March 8-9, 2010

2

Outline

Setting the scene: the fiscal challenge

Range of interventions: a quick overview

Sovereign balance sheet: an old idea whose time

has come?

Definition

Issues

Challenges

Issues for discussion

3

Fiscal Challenge: Stylized Facts

The scale of the problem is unprecedented

Demographic trends remain unfavorable

Although financial sector support only a small

part of the increase in gross debt…..

….scale and range of interventions also

unprecedented…..

….thus, challenging the way we account for and

report on the state of public finance

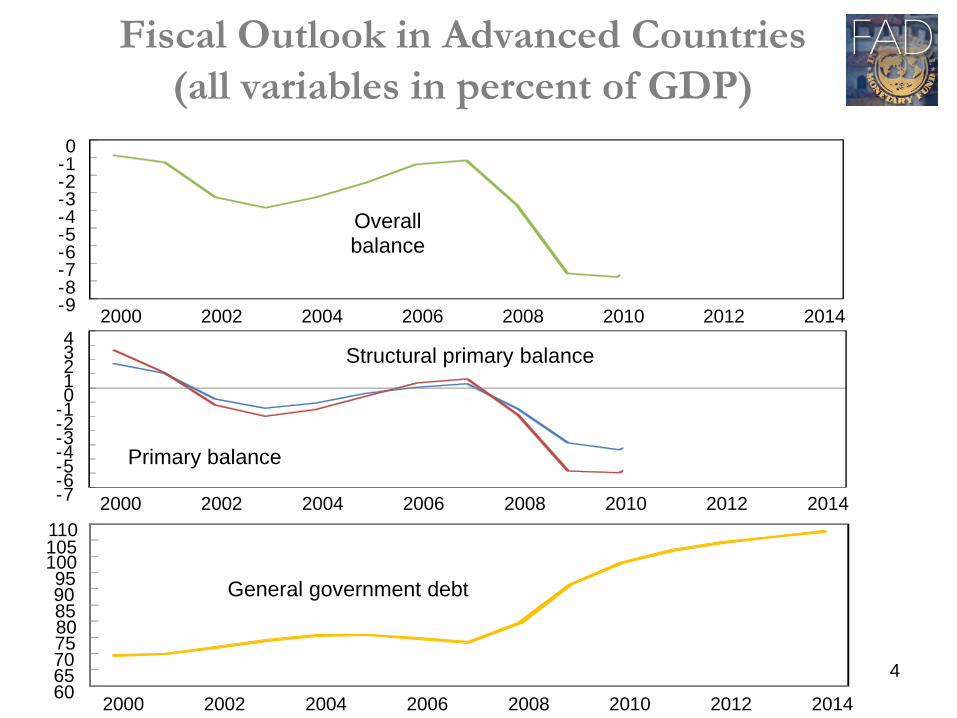

60 65 70 75 80 85 90 95

100 105 110

2000 2002 2004 2006 2008 2010 2012 2014

General government debt

Fiscal Outlook in Advanced Countries

(all variables in percent of GDP)

4

- 7 - 6 - 5 - 4 - 3 - 2 - 1 0 1 2 3 4

2000 2002 2004 2006 2008 2010 2012 2014

Primary balance

Structural primary balance

- 9 - 8 - 7 - 6 - 5 - 4 - 3 - 2 - 1 0

2000 2002 2004 2006 2008 2010 2012 2014

Overall balance

5

Fiscal Challenge: Stylized Facts

G-7 PPP-Weighted Public Debt, percent of GDP

0

20

40

60

80

100

120

140

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Japan Adjusted G-7 Average Gross Government Debt

G-7 Average Gross Government Debt

6

Decomposition of Government

Debt Increase, 2007 - 2014 (Total debt increase: 35.5 percent of GDP)

Other: 6

Fiscal stimulus: 3 ½

Financial support: 3

Higher interest payments: 4

Revenue loss from lower asset prices

and financial profits: 9

Automatic stabilizers: 10

7

Financial System Support Measures

Between January 2008-June 2009, about 5 percent of

GDP pledged—3 percent actually used

More than 50 countries among advanced, emerging,

and developing countries

Instruments: deposit insurance, guarantees,

recapitalization, asset swaps/purchases, direct lending,

and liquidity facilities

Agencies: central banks, treasuries, public

corporations, state-owned banks

8

Sovereign Balance Sheet: New Idea?

Not particularly new—see earlier IMF work on BSA,

GFSM 2001 framework, SWF, more recently BPM 6

But its appeal has been revamped in light of global

crisis and nature of interventions

The concept is easy to grasp—less so to implement:

Comprehensive information of all public assets and liabilities

as analytical tool to assist governments managing their resources

while taking into account their combined implications

9

Sovereign Balance Sheet:

Institutional Coverage

Non-Financial Financial Total Net Worth

A L A L A L (A-L)

Non-Financial Financial Total Net Worth

A L A L A L (A-L)

Sovereign/Whole-of-Government

General government

Central government

Including:

Budgetary central government

Other central government agencies

e.g., Social security institutions

Subnational governments

Public enterprises 1/

Financial

e.g., Central bank

Deposit insurance fund

SWF

AMC

Non-financial

1/ If market producers.

10

Sovereign Balance Sheet: Issues

Coverage: comprehensiveness relies at the moment on

―control,‖ but is this the relevant concept?

Institutional independence needs to be preserved, but

who manages the sovereign balance sheet?

How are tensions going to be resolved between

general government levels, particularly in a federal

system? And with ―independent‖ central banks?

Tensions also emerge across government (i.e., non-

profit) institutions and commercially-run public

enterprises

11

Sovereign Balance Sheet:

Prerequisites

Ongoing work with IPSASB is looking at how

interventions have been accounted for and reported

on in a few advanced economies

Not surprisingly, the answer is…very differently

This is a key problem as the magnitude of the fiscal

adjustment will require concerted efforts

Agreeing on the ―correct‖ figures is not a trivial

exercise

12

What are the

Challenges/Prerequisites?

Fiscal risk, contingent liabilities (and assets)

Accounting framework and standards

Reporting entities

Valuation of assets, in particular, treatment of

gains and losses

13

Fiscal Risk

Disclosure of explicit and implicit contingent

obligations (off-balance sheet)

Publish a statement of fiscal risks with annual

budget documents, including the different types

of risks related to announced public

interventions in support of the financial sector

Empirical evidence suggests a link between

greater fiscal risk disclosure and better sovereign

credit ratings (next slide)

14

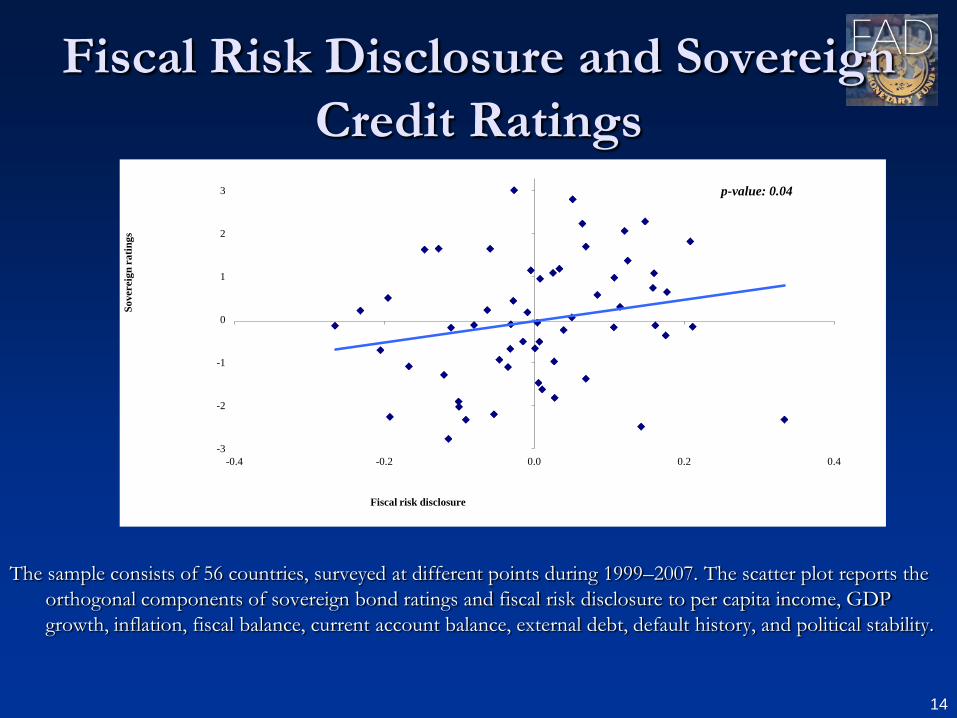

Fiscal Risk Disclosure and Sovereign

Credit Ratings

The sample consists of 56 countries, surveyed at different points during 1999–2007. The scatter plot reports the

orthogonal components of sovereign bond ratings and fiscal risk disclosure to per capita income, GDP

growth, inflation, fiscal balance, current account balance, external debt, default history, and political stability.

-3

-2

-1

0

1

2

3

-0.4 -0.2 0.0 0.2 0.4

So

vereig

n r

ati

ng

s

Fiscal risk disclosure

p-value: 0.04

15

Reporting entity

International public sector accounting standards (IPSAS) as well as

statistics (GFSM 2001) require that government financial statements

provide a consolidated view of the finances of all entities controlled by

the government for accounting purposes

The existence of control in the context of consolidated financial report

does not in any way indicate that there is necessarily control over the

manner in which statutory/professional functions are performed by an

entity

Control may have become less relevant in light of global crisis, even in

light of SNA 2008 clarification

A different standard may be required, that capture the responsibility a

government has vis-à-vis taxpayers, i.e., how a government is

accountable

16

Accounting Frameworks and Standards

The accounting basis defines the timing of recognition of

economic events in the financial statements and, therefore,

determines whether particular assets, liabilities, revenues or

expenses are reported

Integrated framework, based on the accrual accounting

concept, in accordance with explicit national or international

standards

Frameworks that focus mainly on reporting cash flows may

provide less comprehensive information, if any, on assets and

actual or contingent liabilities

17

Valuation

The choice of accounting policies on valuation and related

gains and losses have a direct impact on the measurement of

key indicators such as fiscal surplus or deficit.

Adherence to accepted accounting standards will enhance

countries’ accountability.

Generally GAAPs require ―fair value‖ asset valuation

Recent developments have led to pressures for a retreat from

marking-to-market

Recent proposed IFRS amendments to accounting for

financial instruments retain a preference for ―fair value‖ and

limit alternatives to simple debt instruments held for their

underlying cash flows

18

Issues for Discussion

Fiscal risk statement: increasingly good practice, but

far from being comprehensive or reliable

Is control the relevant concept? Wouldn’t

accountability be a better concept?

Accounting framework and standards, including

valuation criteria: mandatory vs. voluntary?

Timeliness for decisions makers

Last, who is the ultimate decision maker in managing

the sovereign balance sheet? Or, who is accountable

for it?

19

Selected IMF References IMF, 2010, Broadening Financial Indicators in the Special Data

Dissemination Standard, March 10, 2010

IMF, 2009, Crisis-Related Measures in the Financial System and

Sovereign Balance Sheet Risks, July 31, 2009

http://www.imf.org/external/np/sec/pn/2009/pn09118.htm

IMF, 2009, Disclosing Fiscal Risks in the Post-Crisis World, IMF Staff

Position Note, SPN/09/18, July 2009

www.imf.org/external/pubs/ft/spn/2009/spn0918.pdf

Fiscal Risks—Sources, Disclosures and Management, IMF Fiscal Affairs

Department, 2009 www.imf.org/external/pubs/ft/dp/2009/dp0901.pdf

IMF, 2007, Manual on Fiscal Transparency.

IMF, 2006, Public Private Partnerships, Government Guarantees, and

Fiscal Risk

http://www.imf.org/external/pubs/cat/longres.cfm?sk=18587.0