the perspectives of international pipeline projects...

TRANSCRIPT

The Perspectives of International The Perspectives of International Pipeline Projects in NEA Pipeline Projects in NEA

March 2004

Heung Bog Lee

Better Energy, Better World

ContentsContents

I. Outlook of Natural Gas in the World

II. Proposed International PNG 1) Project in NEAFocusing on Irkutsk PNG Project

III. Brief Overviews on Future Studies of Natural Gas Projects in NEA

IV. Conclusion

1) PNG (Pipelined Natural Gas) means natural gas transported by pipeline without liquefaction process of natural gas

I. Outlook of Natural Gas in the WorldI. Outlook of Natural Gas in the World

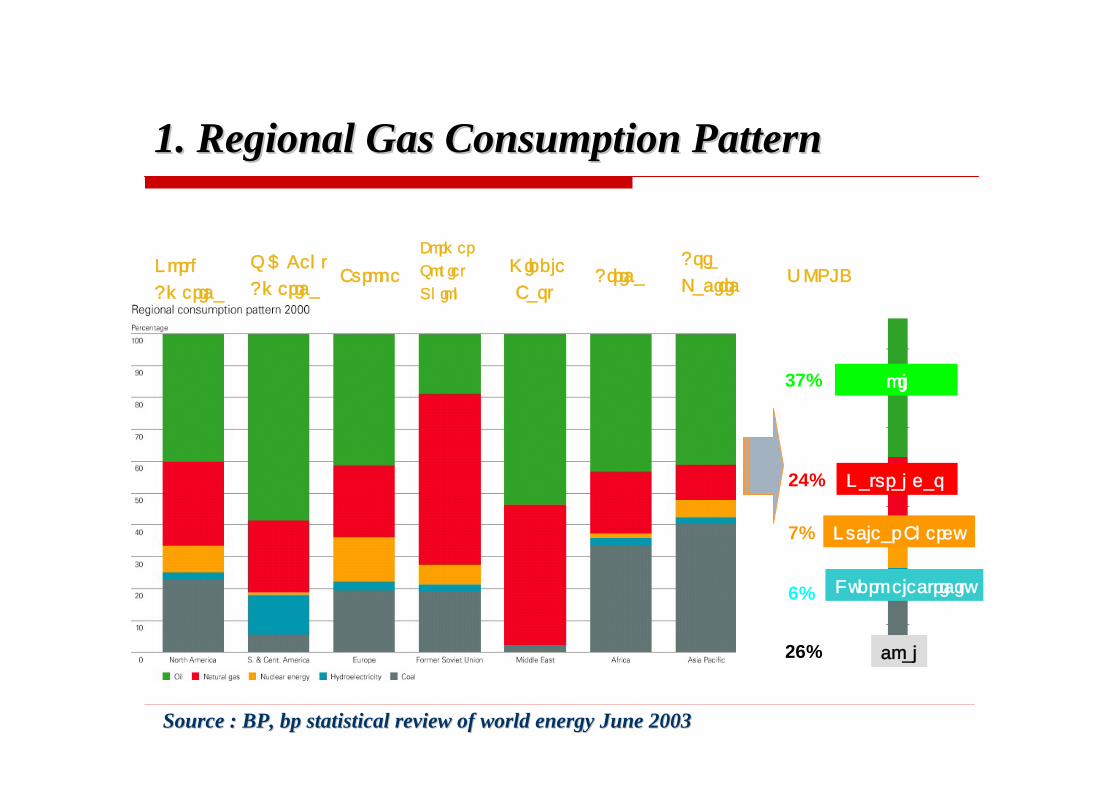

1. Regional Gas Consumption Pattern

2. Gas Consumption in the world

3. LNG Demand in Asia Pacific (Yr 2010)

4. Trends of LNG Markets in the world

5. Review of NEA Natural Gas Markets in Global

Context

North

America

S & Cent

AmericaEurope

Former

Soviet

Union

Middle

EastAfrica

Asia

PacificWORLD

37%

24%

7%

6%

26%

51%

10%

14%

1%

24%

Source : BP, Source : BP, bpbp statistical review of world energy June 2003statistical review of world energy June 2003

oil

Natural gas

Nuclear Energy

Hydro electricity

coal

1. Regional Gas Consumption Pattern1. Regional Gas Consumption Pattern

2. Consumption in the World (2002)2. Consumption in the World (2002)

Total : 1,930 mm tonTotal : 1,930 mm tonTrade Volume: 440 mm tonTrade Volume: 440 mm ton-- 23% of total consumption23% of total consumptionTraded by Traded by -- PNG: 330 mm ton (75%) PNG: 330 mm ton (75%) -- LNG: 110 mm ton (25%)LNG: 110 mm ton (25%)Major LNG Importers Major LNG Importers -- Japan : 53.9 mm ton (51.7%) Japan : 53.9 mm ton (51.7%) -- Korea : 17.8 mm ton(16.2 %)Korea : 17.8 mm ton(16.2 %)

unit : bcm76.65

10.9338.31

10.05

22.74

5.36

48.3

12.36

20.0730.59

8.2

3.7

Source : BP, Source : BP, bpbp statistical review of world energy June 2003statistical review of world energy June 2003

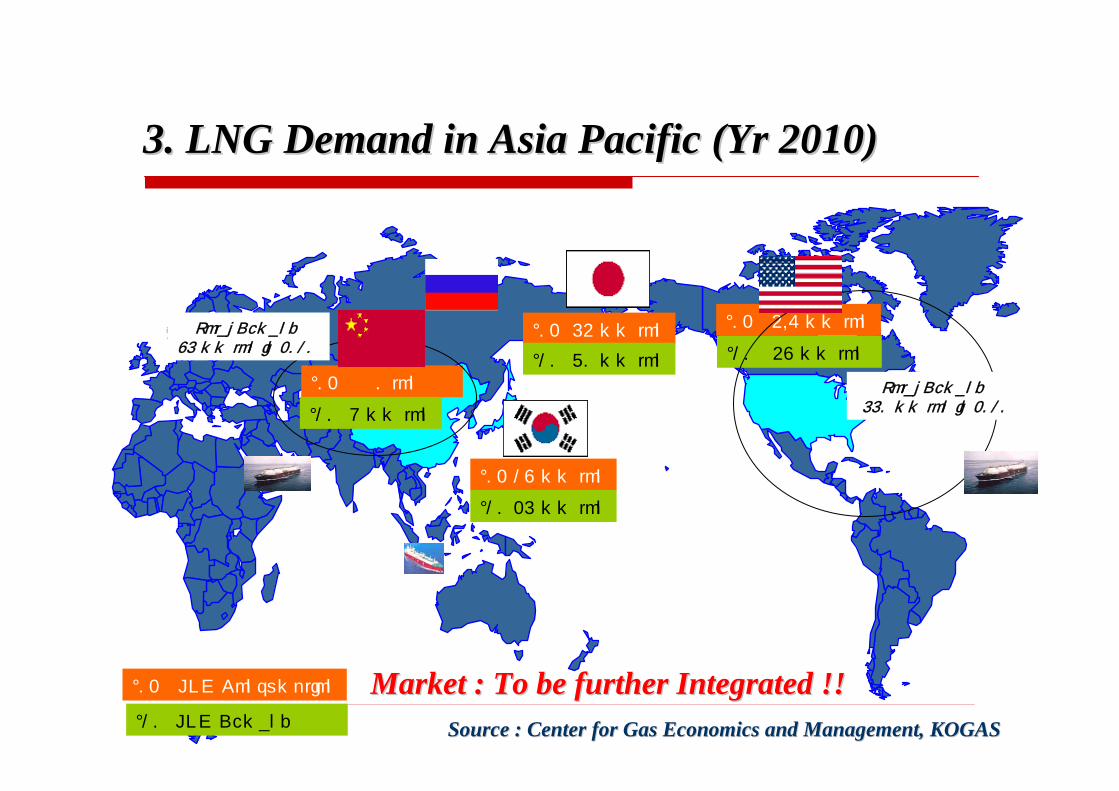

‘02 4.6 mm ton

‘02 0 ton

‘02 18 mm ton

‘02 54 mm ton‘10 48 mm ton

‘10 9 mm ton

‘10 25 mm ton

‘10 70 mm ton

Total Demand 85 mm ton in 2010

Total Demand550 mm ton in 2010

‘02 LNG Consumption

‘10 LNG Demand

Market : To be further Integrated !!Market : To be further Integrated !!

3. 3. LNG Demand in Asia Pacific (Yr 2010)LNG Demand in Asia Pacific (Yr 2010)

Source : Center for Gas Economics and Management, KOGASSource : Center for Gas Economics and Management, KOGAS

4. 4. Trends of LNG Market in the WorldTrends of LNG Market in the World (1/2)(1/2)

More Competitive Price : Driving Forces to reduce the Price

A. Buyers’ Market: Shifting Negotiation Power to Buyers- Sufficient Number of Gas Projects compared with the current demand

B. Cost Reduction by Technological Developments- LNG Chains : Liquefaction, Ship Building & Shipping, Storages

(Economy of Scale reduced the cost)

C. Penetration to the emerging markets such as China and Idia

D. Spot Markets to spur the integration of markets- Spot Market Share: 8%(2002) to 15%(2010)

E. The Roles of Majors and Success of Currently Operated LNG Projects

How much the price level will go down?How long Buyers’ market will continue?

More Flexible Terms and ConditionsA. Price : A reduced oil price linkage, S-curve or Price Cap

Various Pricing Mechanisms

B. Flexible Contract Volumes : Base Volume + OptionalVolume, The Secured Seasonal Volumes,

C. Lower Level of Take or PayD. Shorter Contract Period

E. More flexible Destination Clause: Chances of Trade

4. 4. Trends of LNG Markets in the WorldTrends of LNG Markets in the World (2/2)(2/2)

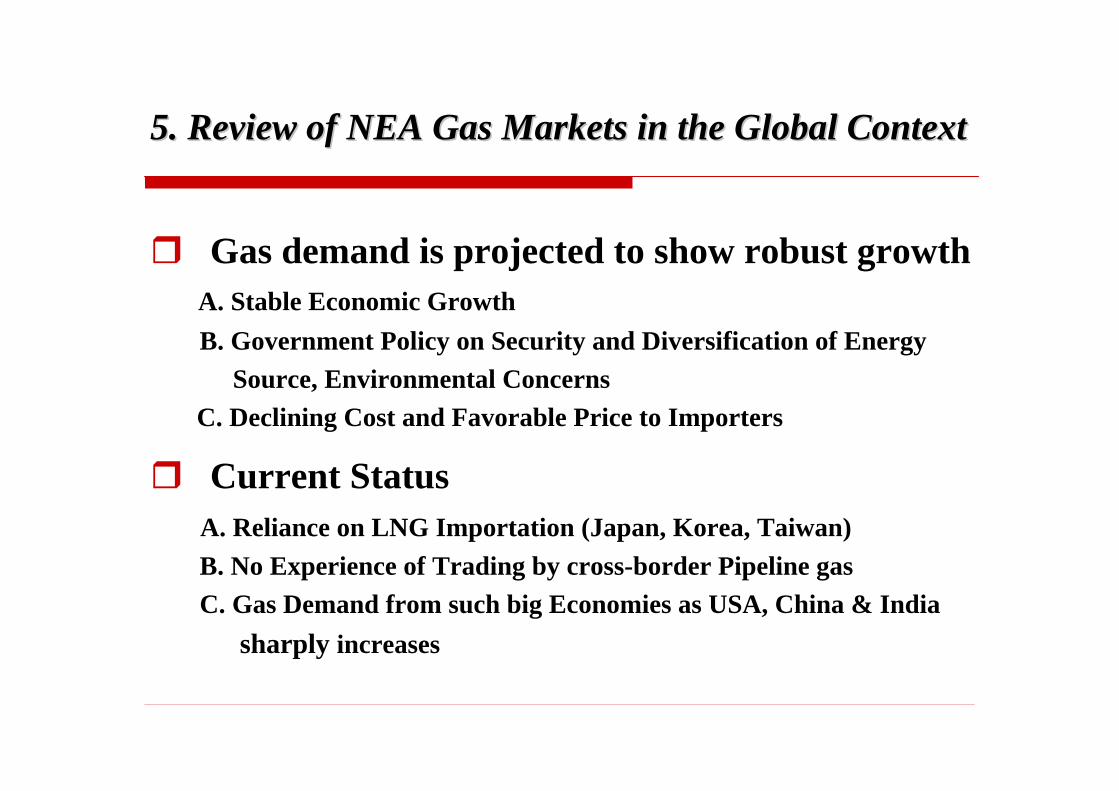

5. Review of NEA Gas Markets in the Global Context5. Review of NEA Gas Markets in the Global Context

Gas demand is projected to show robust growthA. Stable Economic GrowthB. Government Policy on Security and Diversification of Energy

Source, Environmental ConcernsC. Declining Cost and Favorable Price to Importers

Current StatusA. Reliance on LNG Importation (Japan, Korea, Taiwan)B. No Experience of Trading by cross-border Pipeline gas C. Gas Demand from such big Economies as USA, China & India

sharply increases

II. Proposed International PNG Project in NEA- Focusing on Irkutsk PNG Project -

Signing Ceremony for IFS (Beijing, Nov. 2000)

CoCom

Market WGPipeline WGField WGRussian Party

Chinese Party

Korean Party

Russian Party

Chinese Party

Korean Party

Russian Party

Chinese Party

Korean Party

General WG

Russian Party

Chinese Party

Korean Party

Russian Party

Chinese Party

Korean Party

Process•Trilateral•Cooperative

Report•Technical & Economic• 2003

1. 1. IFSIFS1)1) -- FrameworkFramework

1) 1) IFSIFS means International Feasibility by KOGAS, CNPC and RUSIA Petrolmeans International Feasibility by KOGAS, CNPC and RUSIA Petroleum Jointlyeum Jointly

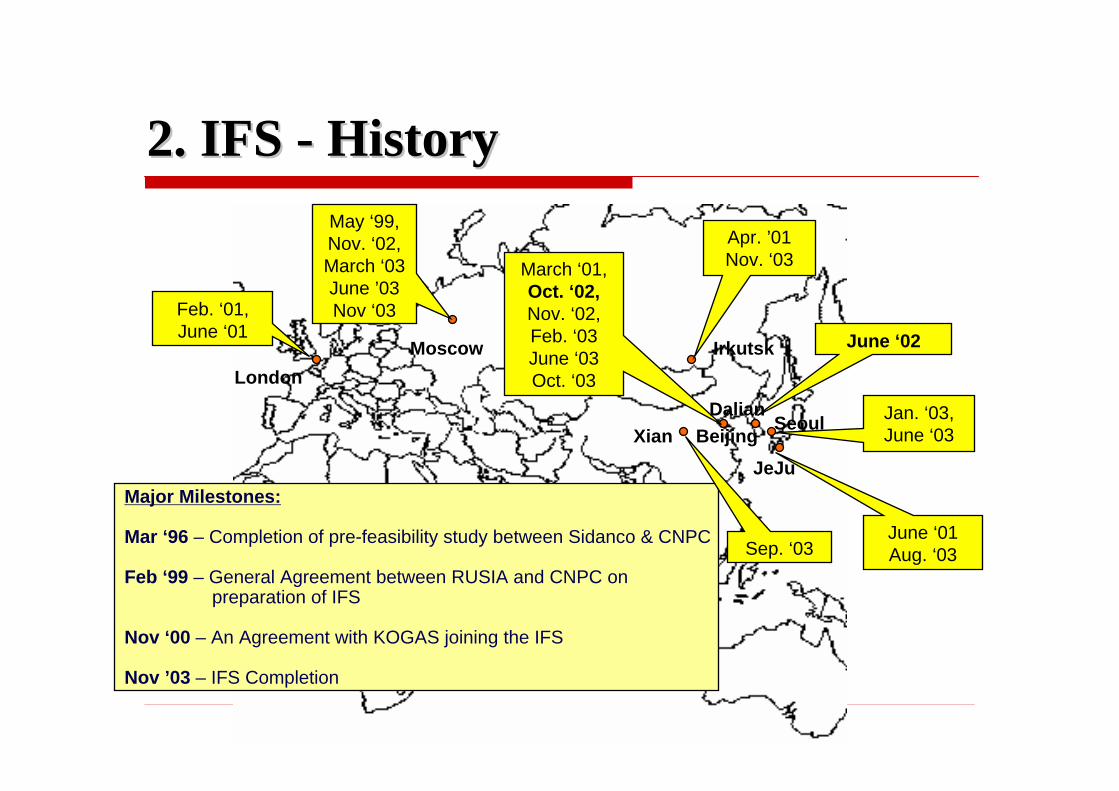

May ‘99, Nov. ‘02, March ‘03June ’03Nov ‘03Feb. ‘01,

June ‘01

Apr. ’01Nov. ‘03

June ‘02

March ‘01,Oct. ‘02,Nov. ‘02, Feb. ‘03June ‘03Oct. ‘03

Jan. ‘03, June ‘03

June ‘01Aug. ‘03

MoscowLondon

Irkutsk

Beijing Seoul

JeJu

Dalian

Major Milestones:

Mar ‘96 – Completion of pre-feasibility study between Sidanco & CNPC

Feb ‘99 – General Agreement between RUSIA and CNPC on preparation of IFS

Nov ‘00 – An Agreement with KOGAS joining the IFS

Nov ’03 – IFS Completion

Sep. ‘03

Xian

2. 2. IFS IFS -- HistoryHistory

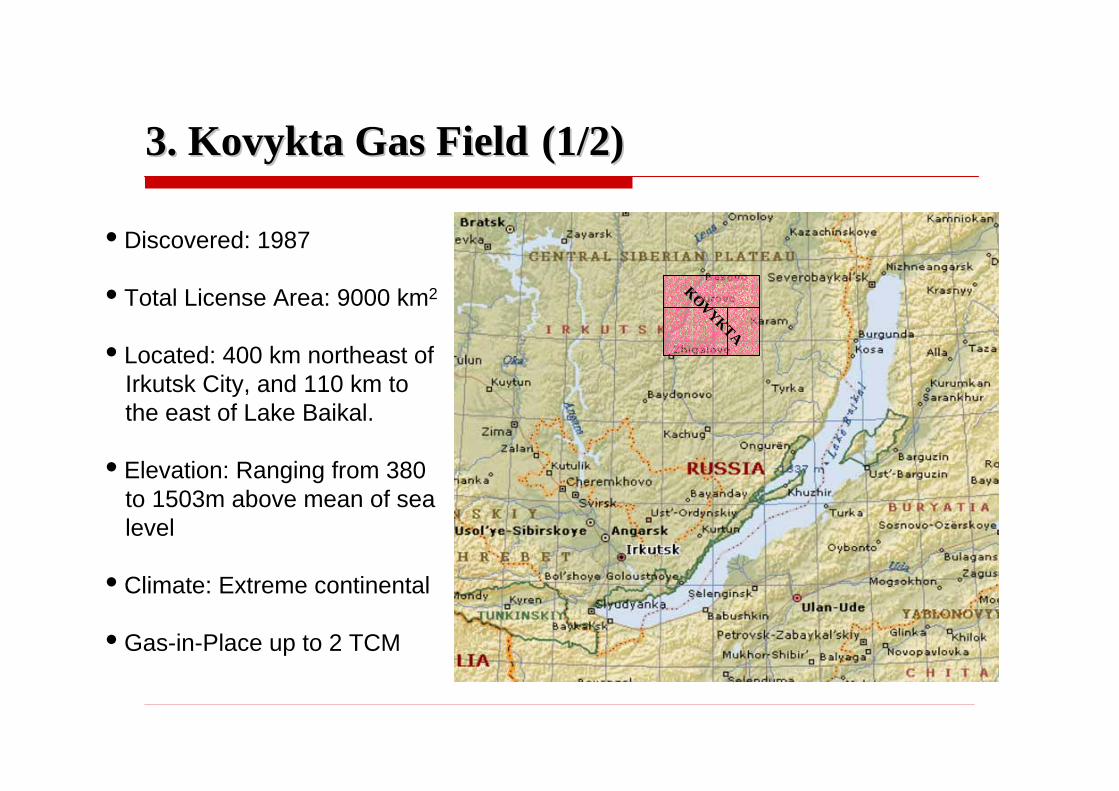

3. 3. KovyktaKovykta Gas FieldGas Field (1/2)(1/2)

KOVYKTA

• Discovered: 1987

• Total License Area: 9000 km2

• Located: 400 km northeast of Irkutsk City, and 110 km to the east of Lake Baikal.

• Elevation: Ranging from 380 to 1503m above mean of sea level

• Climate: Extreme continental

• Gas-in-Place up to 2 TCM

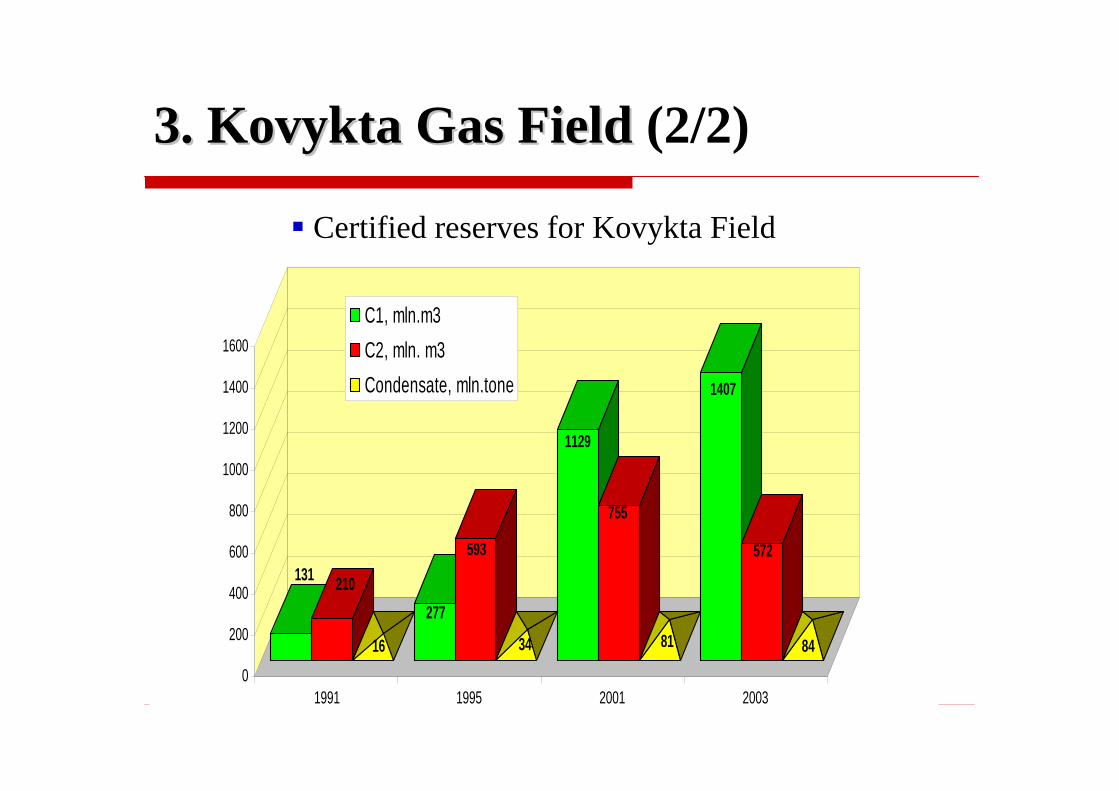

131 210

16

277

593

34

1129

755

81

1407

572

840

200

400

600

800

1000

1200

1400

1600

1991 1995 2001 2003

C1, mln.m3 C2, mln. m3Condensate, mln.tone

3. 3. KovyktaKovykta Gas Field Gas Field (2/2)

Certified reserves for Kovykta Field

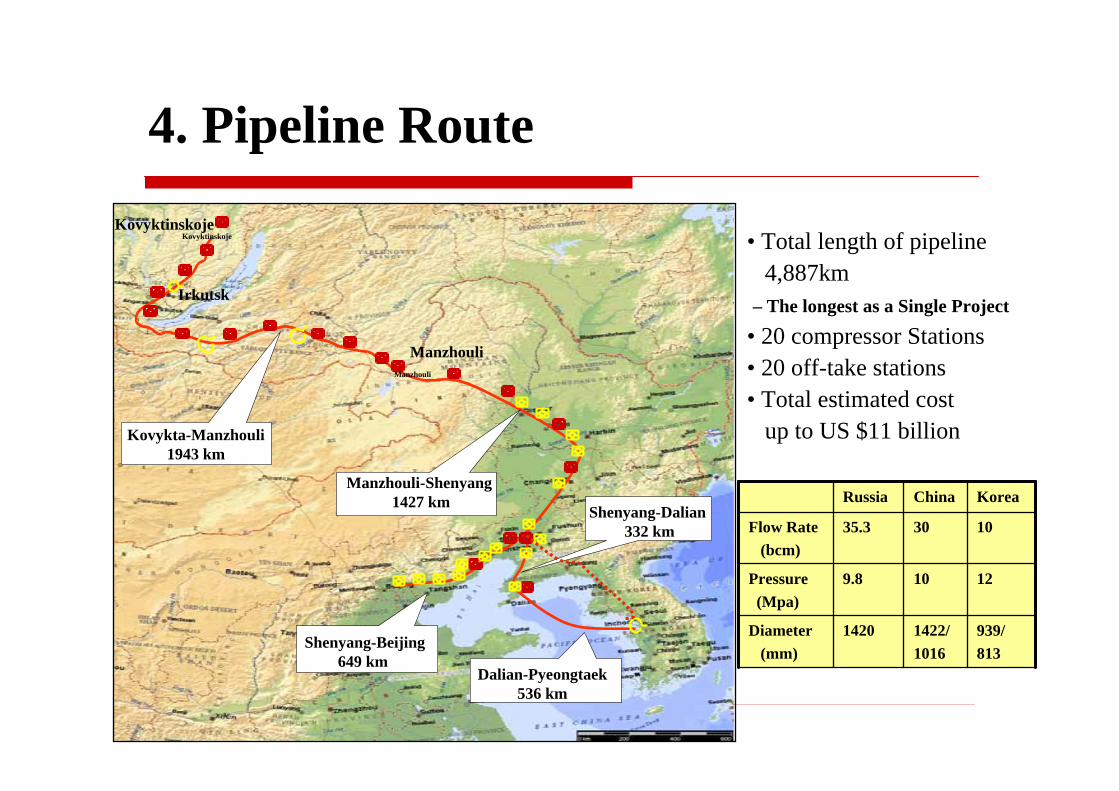

Pyeongtaek

Beijing

Changchun

Manzhouli

Kovyktinskoje

Manzhouli-Shenyang1427 km

Shenyang-Beijing649 km

Kovykta-Manzhouli1943 km

Shenyang-Dalian332 km

Dalian-Pyeongtaek536 km

Manzhouli

Irkutsk

Kovyktinskoje• Total length of pipeline

4,887km– The longest as a Single Project

• 20 compressor Stations• 20 off-take stations• Total estimated cost

up to US $11 billion

4. Pipeline Route

939/813

1422/1016

1420Diameter(mm)

12109.8Pressure (Mpa)

103035.3Flow Rate (bcm)

KoreaChinaRussia

Pyeongtaek

Beijing

Changchun

Manzhouli

Kovyktinskoje

:

4 bcm/a

8 bcm/a

12 bcm/a

10 bcm/a

5. Market : Demand for Kovykta Gas (1/4)

0

10

20

30

40

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Dem

and

bcm

/a

Russia China Korea

4 bcm/aRussia (2006-08)

10 bcm/aKorea (2008)

8 bcm/aBohai China (2013)

12 bcm/aNE China (2008)

Plat. Sales Market (First Gas)

9 year build-up to plateau for export.

0

1

2

3

4

5

2008 2009 2010 2011 2012

bcm

/a

Pow er generation HeatingChemical/Petrochemical IndustryResidential sector

5. Market - Russia (2/4)

Sector Demand: bcm/aPower: 2.7Chemicals: 0.6Heating: 0.5Industry: 0.2Residential: 0.1

Sector Demand: bcm/aPower: 2.7Chemicals: 0.6Heating: 0.5Industry: 0.2Residential: 0.1

• Strong potential for growth – energy markets increasing by

2.5% - 3.5% p.a.

• Early regional supply could start as early as 2006/7

•Total gas demand of 4bcm/a by 2012

• Major consumption in heat generation and power sectors

5. Market - China (3/4)

0

5

10

15

20

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

bcm

/a

Power Chemical Industrial fuel City gas

Sector Demand: bcm/aPower: 4.9Chemical: 3.1Industry: 3.6City gas: 8.3

Sector Demand: bcm/aPower: 4.9Chemical: 3.1Industry: 3.6City gas: 8.3

• China market is ready for Russian gas imports• Economic growth and population will result in significant future demand growth

• China market is ready for Russian gas imports• Economic growth and population will result in significant future demand growth

5. Market – Korea (4/4)

0

5

10

15

20

2008 2009 2010 2011 2012 2013 2014 2015

Dem

and

bcm

a

Expected Gas Shortage Build Up

• Target Market: Power Plants & Industries

• Competing Fuels: Heavy Fuel Oil, Coal, and LNG

Expected Gas Shortage & Build-up for Kovykta Gas

6. General : 6. General : Business Organizational ModelBusiness Organizational Model (1/2)(1/2)

Gas field Russian pipeline Chinese pipeline Korean pipeline

Russian sales company

Chinese sales company

Korean sales company

Russia China Korea

Gas field company

Russian Pipeline company

Chinese Pipeline company

Korean Pipeline company

Gas field Russian pipeline Chinese pipeline Korean pipeline

Russian sales company

Chinese sales company

Korean sales company

Russia China Korea

Gas field company

Russian Pipeline company

Chinese Pipeline company

Korean Pipeline company

A number of different business models have been evaluatedThe IFS recommends a segregated model by both country and function

A number of different business models have been evaluatedThe IFS recommends a segregated model by both country and function

6. General: 6. General: Legal, Financing, TaxationLegal, Financing, Taxation (2/2)(2/2)

Legal & Contractual Issues• PSA status / GSPA• Intergovernmental Agreements

Financing• Project Finance will be required given scale of investment• Involvement of international agencies and commercial banks

Taxation System: Needs to be stable and favourable to encourageinvestment

Economic Analysis & Gas Pricing

Results indicate that the project is economically viable under conditions

A. Project is technically and commercially viable – IFS objectives have been met by the parties

- Sound Markets and Proper Reserves

B. Project will be beneficial to both governments, customers, suppliers & investors.

C. Development of the project will require significant investment and create a large number of jobs

D. Development of NEA and Provision of clean energy for the 21st century

E. Government support for the project will be critical

7. 7. Conclusions Conclusions in IFS in IFS

A. Joint-working Experience and Outcome of IFS is a cornerstone to understand each other for expediting Implementation of the Project– Very Serious Study Supported by Three Governments

B. Governments have recognized that Government supports are critical

C. Way Forward

- The Authorized Exporter and Pipeline Owner to be selected by Russian

Government - Negotiation to set beneficial price both to seller and buyers - Optimization through Further Engineering to reduce the Cost Estimation.- Launching the official Inter-government discussions among three countries- Further Efforts to develop Win-Win Program by Trilateral Governments and

Business Sectors

8. Meanings of IFS and Way Forward8. Meanings of IFS and Way Forward

III. Brief Overviews on Future Studies of Gas Projects in NEA

1. By Gazprom (Russia)

2. By Chinese Gas Association (China)

3. By Northeast Asian Gas & Pipeline Forum

4. Japan

5. Korea

- -

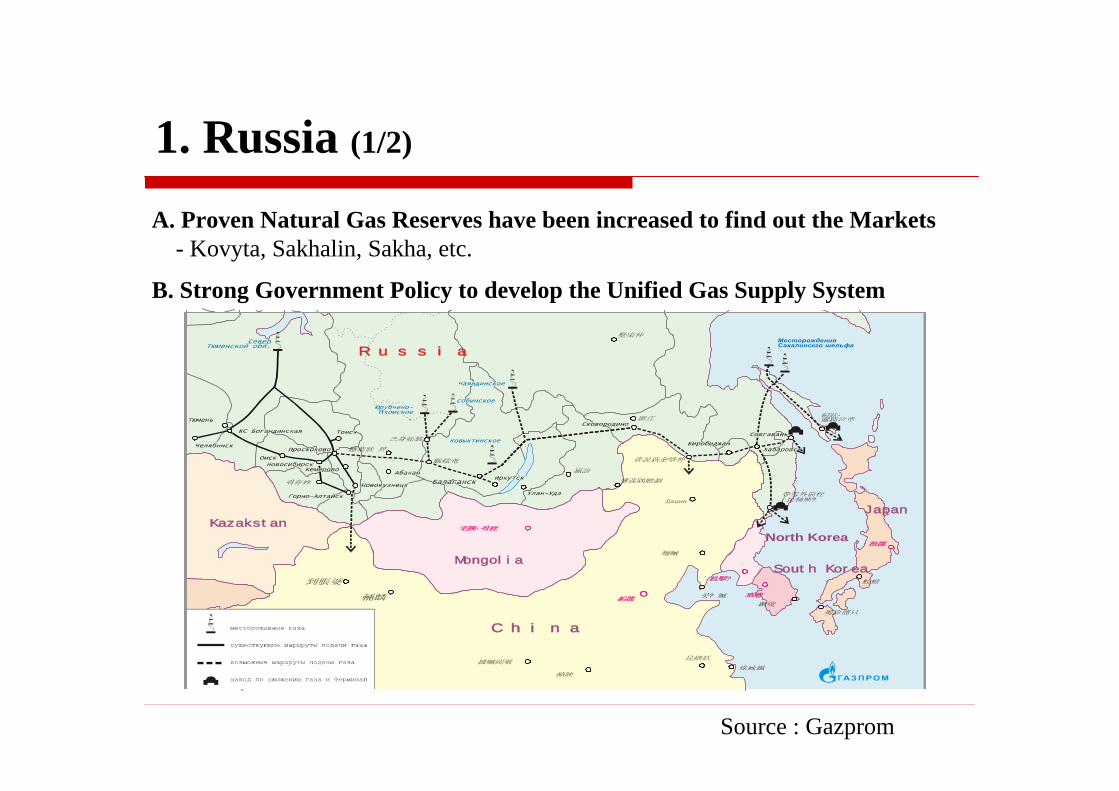

A. Proven Natural Gas Reserves have been increased to find out the Markets- Kovyta, Sakhalin, Sakha, etc.

B. Strong Government Policy to develop the Unified Gas Supply System

R u s s i a

C h i n a

Mongolia

Kazakstan

줘存姓

輛麟

憾葉狀 猝

腦橒奄

즈身妬裝

墅寀仲

机孼?到脹婆

躬孺

羸診

宅陝-줘桎

據贓闖塡

酪陝

麵贓

杻孺

Japan

МесторожденияСахалинскго шельфа

쥰說荻余孼仲

煤臧纖

행蓀隅贍劃

祠狀-邏鎚泣章

昆檣妖

珞窓

蛟蟾

South Korea

蹶焌

褐診溜只

콧? 贓

匿庄

Дацин

North Korea

쯤雪外前桎(昆軸殃?

Source : Gazprom

1. Russia (1/2)

R u s s i a

C h i n a

Mongolia

Kazakstan

줘存姓

輛麟

憾葉狀 猝

腦橒奄

즈身妬裝

墅寀仲

机孼?到脹婆

躬孺

羸診

宅陝-줘桎

據贓闖塡

酪陝

麵贓 杻孺

Japan

МесторожденияСахалинскго шельфа

쥰說荻余孼仲

煤臧纖

행蓀隅贍劃

祠狀-邏鎚泣章

쯤雪外前桎(昆軸殃?

昆檣妖

珞窓

蛟蟾

South Korea

蹶焌

褐診溜只

콧? 贓

匿庄

Дацин

North Korea

Source : Gazprom

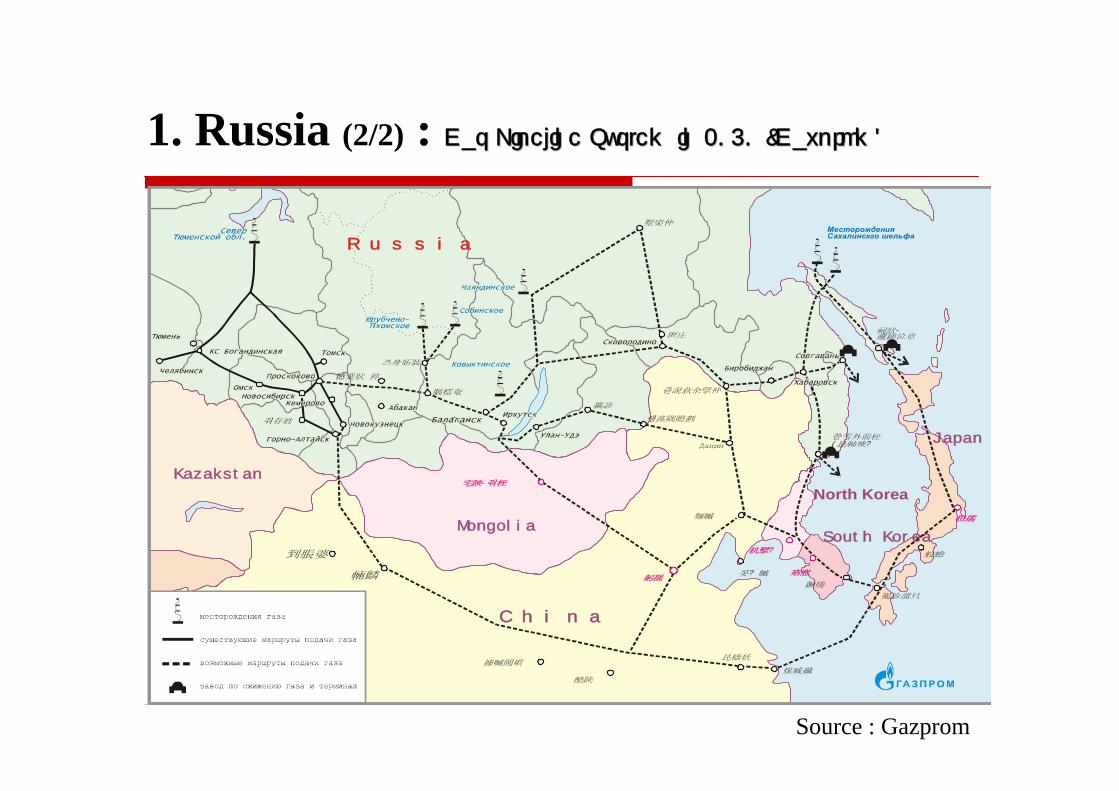

1. Russia (2/2) : Gas Pipeline System in 2050 (Gas Pipeline System in 2050 (GazpromGazprom))

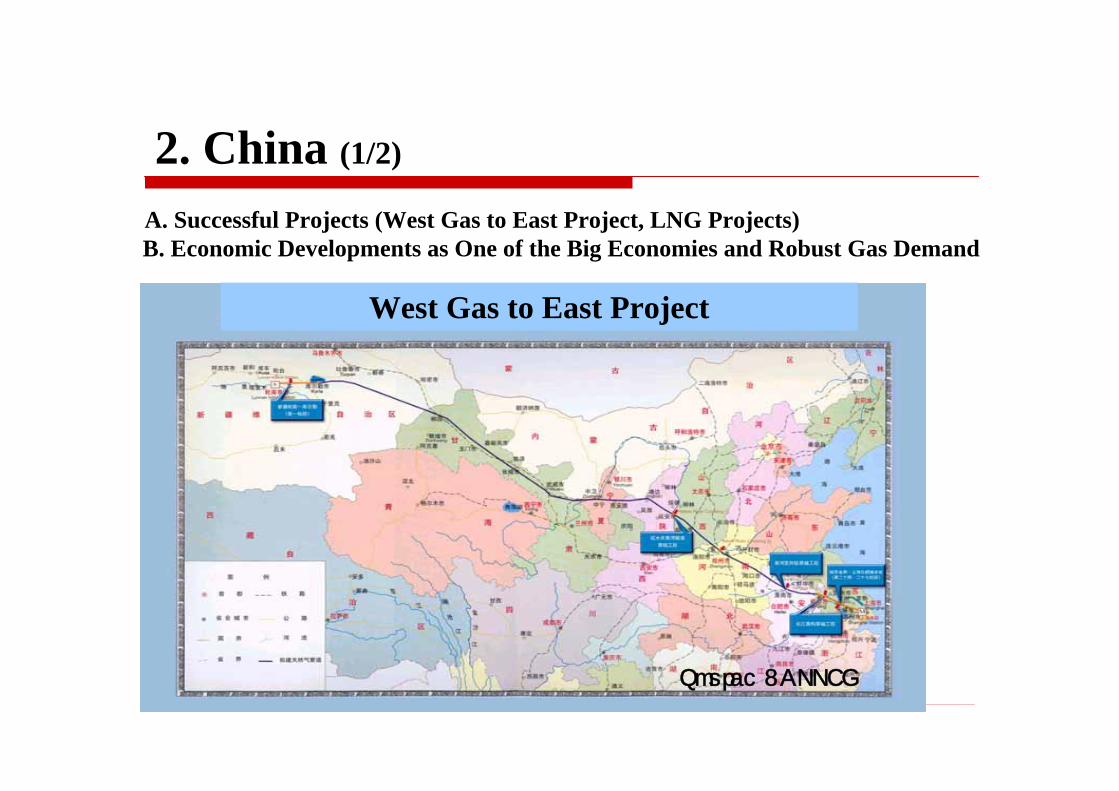

A. Successful Projects (West Gas to East Project, LNG Projects)B. Economic Developments as One of the Big Economies and Robust Gas Demand

West Gas to East Project

Source : CPPEI

2. China (1/2)

Source : Chinese Gas Association in 2002

2. China (2/2) : Chinese Gas Pipeline System in 2020Chinese Gas Pipeline System in 2020

Source : Northeast Asian Gas & Pipeline Forum (NAGPF) in 2002

Surgut

T om sk

U rum qi

W est S iberia

Irkutsk

Y akutskN orth Sakhalin

C hangchun

K habarovsk

C hita

T arim

C entral Asia

N atural Gas F ield

P lanned P ipe line R outes

Possible P ipeline R outes

G as Flow

3. NAGPF’s Pipeline Route Map in NEA

LNG Terminal (existing)LNG Terminal (under construction)

Main Gas Pipeline [existing](except major gas company)Main Gas Pipeline [under construction or planning] (except major gas company)

Main Gas Pipeline [existing](major gas company)

Main Gas Pipeline [under construction or planning] (major gas company)

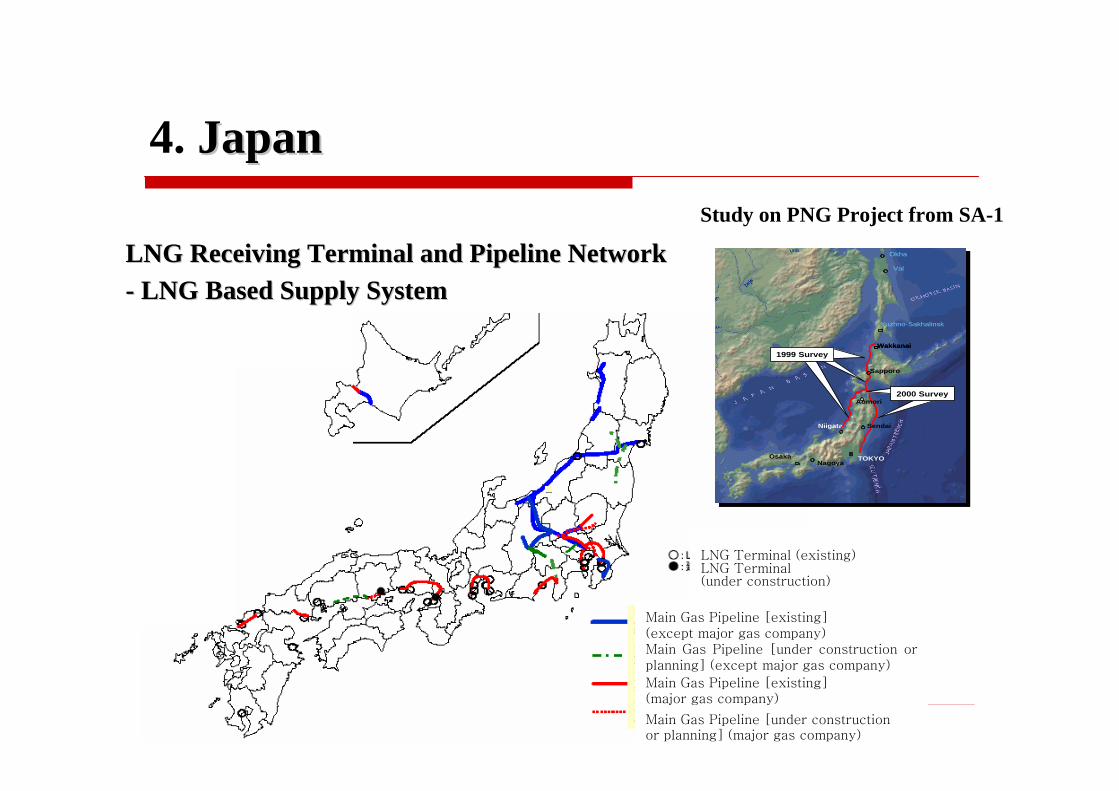

LNG Receiving Terminal and Pipeline NetworkLNG Receiving Terminal and Pipeline Network-- LNG Based Supply SystemLNG Based Supply System

4. JapanJapan

Okha

Val

Niigata

Sapporo

Yuzhno-Sakhalinsk

TOKYONagoya

Osaka

Sendai

Aomori

Wakkanai1999 Survey

2000 Survey

Okha

Val

Niigata

Sapporo

Yuzhno-Sakhalinsk

TOKYONagoya

Osaka

Sendai

Aomori

WakkanaiWakkanai1999 Survey

2000 Survey

Study on PNG Project from SA-1

LNG Based Supply SystemLNG Based Supply System-- 3 terminals and 2,460 km national grid3 terminals and 2,460 km national grid

Two Options to import natural gas- LNG or PNG

Intention to implement international PNG Project- diversification and security of energy

sources for the long terms

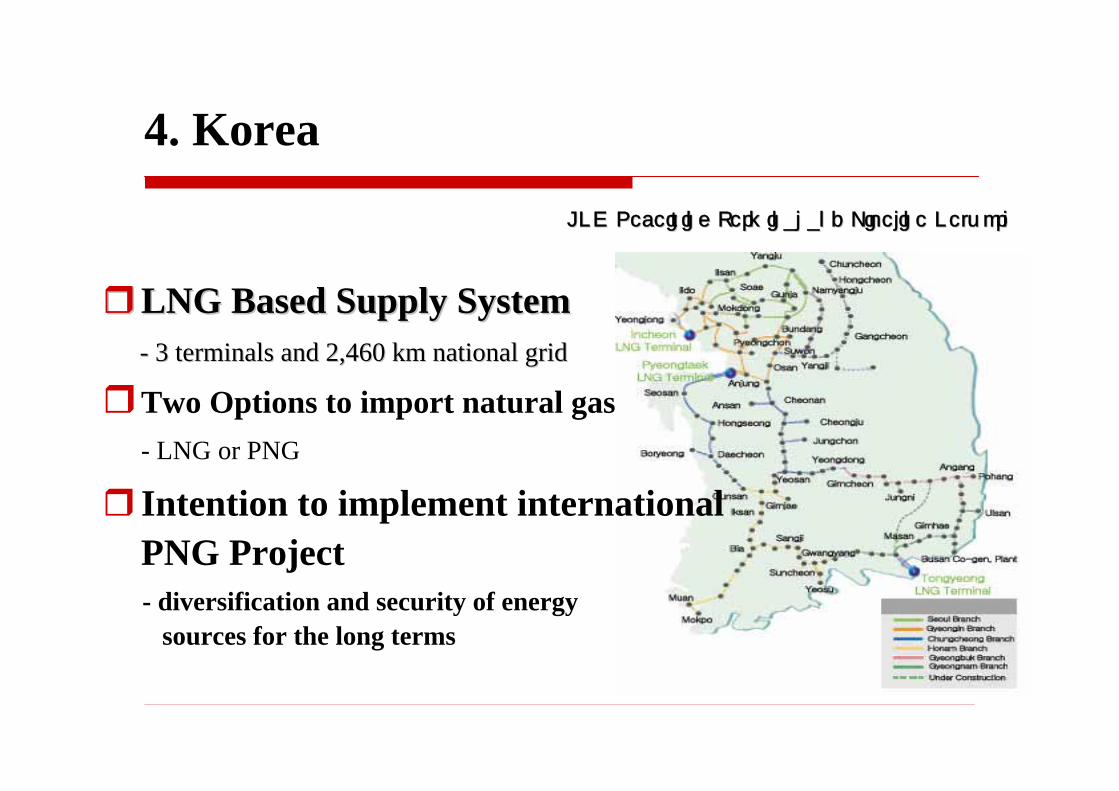

4. Korea

LNG Receiving Terminal and Pipeline NetworkLNG Receiving Terminal and Pipeline Network

Contribution to Economy, Public Welfare and Environments in NEA over 50 to 100 years (during the Project Life Time)

- Beneficial to both Exporters and Importers

- To build “21 Century Energy Express Way” through Int’l Cooperation

Emergence of Integrated NEA gas market through construction of

International Pipeline Infrastructure

Diversification of Energy Sources and Enhanced Security of Gas Supply

IV. Conclusions IV. Conclusions (1/3)(1/3) : : Value of PNG Projects in NEA Value of PNG Projects in NEA

In the short term, Current LNG Markets including Sa-2 LNG Project

will stimulate PNG to be more flexible and competitive

- Otherwise, Potential Markets in China, Korea & Japan will take LNG

China will continue to promote Domestic Projects, as well as LNG Projects

and International PNG Projects

In the mid and long term, PNG will also play an important role in

NEA Gas Markets

- Realization of PNG Projects will be heavily dependent upon strong

Government support and Close International Cooperation

IV. Conclusions IV. Conclusions (2/3) : Perspectives(2/3) : Perspectives

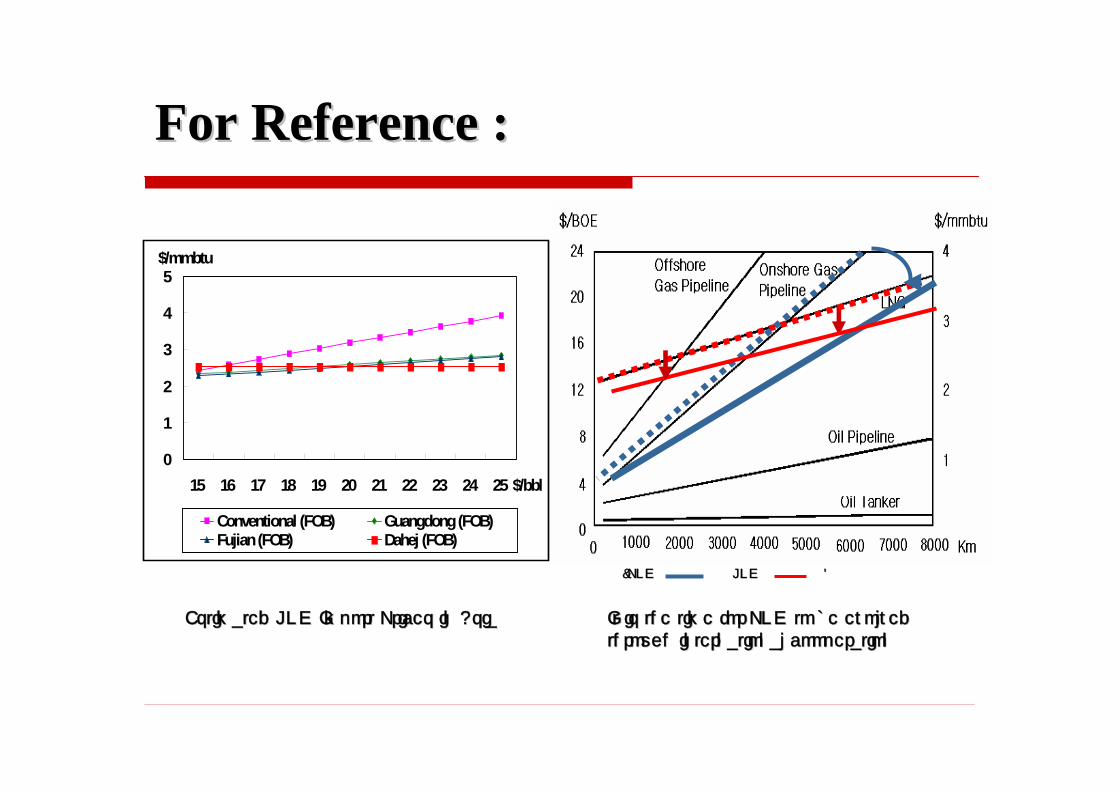

For Reference :For Reference :

0

1

2

3

4

5

15 16 17 18 19 20 21 22 23 24 25 $/bbl

$/mmbtu

Conventional (FOB) Guangdong (FOB)Fujian (FOB) Dahej (FOB)

Estimated LNG Import Prices in AsiaEstimated LNG Import Prices in Asia It is the time for PNG to be evolved It is the time for PNG to be evolved through international cooperation through international cooperation

(PNG LNG )(PNG LNG )

Intergovernmental Cooperation and Agreement are crucial

- Need of Win-Win Program and harmonization of different Legal and Tax Systems,

Level of Economy, Political System, tariff system, etc between countries

- Strong Supports to construct International Gas Infrastructure

- Government Approval on large volumes of gas import for better economics- Selection of Sound Project Players and favorable investment Conditions

Close Cooperation and Compromise between Project participants

- Adoption of Optimal Project Management to reduce CAPEX/OPEX

- Lower profitability may be compensated by gaining of long-term project security

from the government

- Continuous efforts to realize the Project with the long-term point of view

IV. Conclusions IV. Conclusions (3/3) : Suggestions(3/3) : Suggestions

Thanks You !!!Thanks You !!!

Better Energy, Better World