the orwr of growth - macklin credit unionmacklin credit union limited co-operative principles cont....

TRANSCRIPT

Saskatchewan Credit Unions:The Way Forward

2014 ANNUAL GENERAL MEETING2015 ANNUAL GENERAL MEETING

Enginesof Growth

Annual Meeting Call to Order

Confirmation of Quorum Present (Minimum of 15 Members)

Introduction of Chairperson

Adoption of Agenda

Minutes of the 75th Annual General Meeting

Board of Directors Report

Management Discussion and Analysis

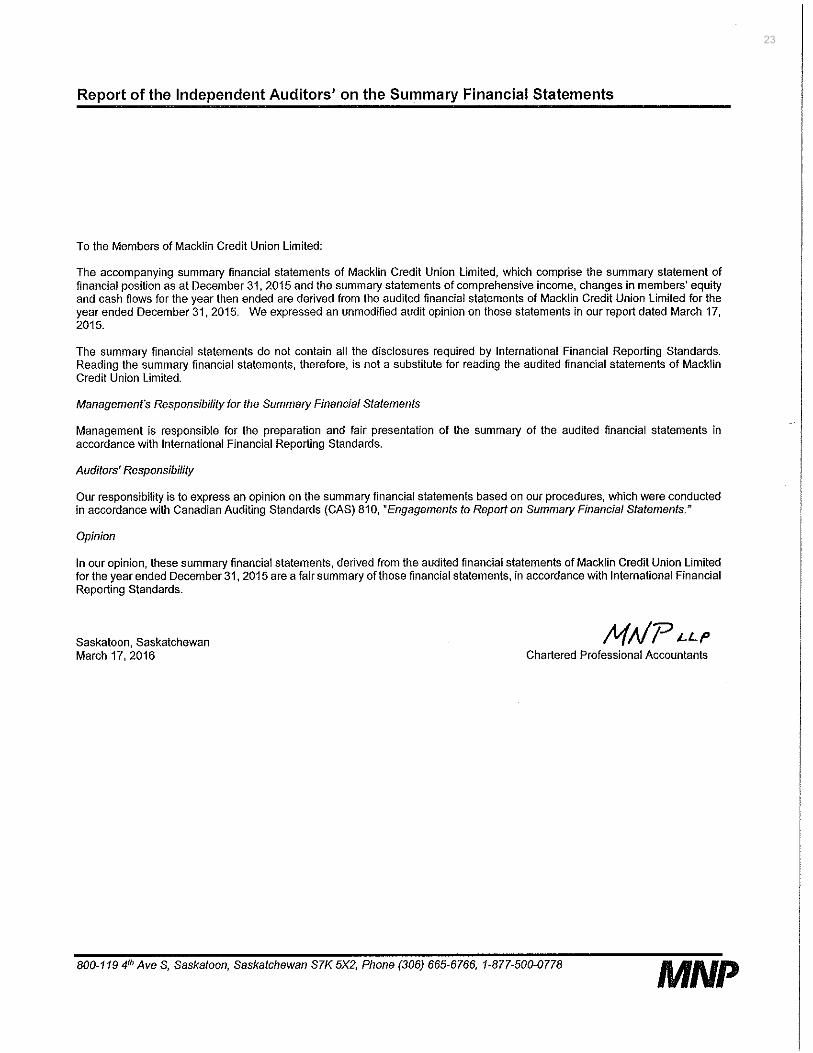

Auditor’s Report

Adoption or Disposal of Reports

Election Results

Appointment of Auditors

Appointment of Returning Officer

New Business

Service Awards

Door Prizes

Adjournment

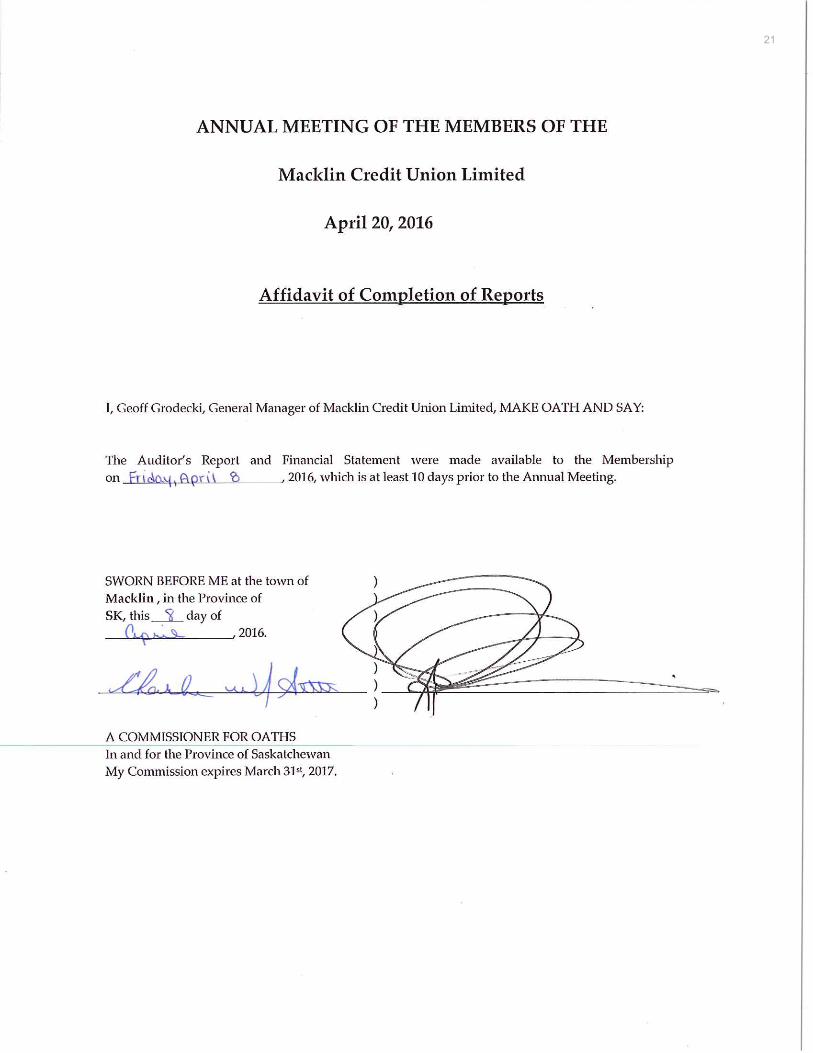

MACKLIN CREDIT UNION LIMITED

76th Annual General MeetingWednesday, April 20, 2016

VISIONYour first choice for financial services, where profit is shared with members and community.

MISSIONTo provide competitive, professional, financial service with a focus on member needs. The result is prosperity for our members, community and credit union.

MACKLIN CREDIT UNION LIMITED

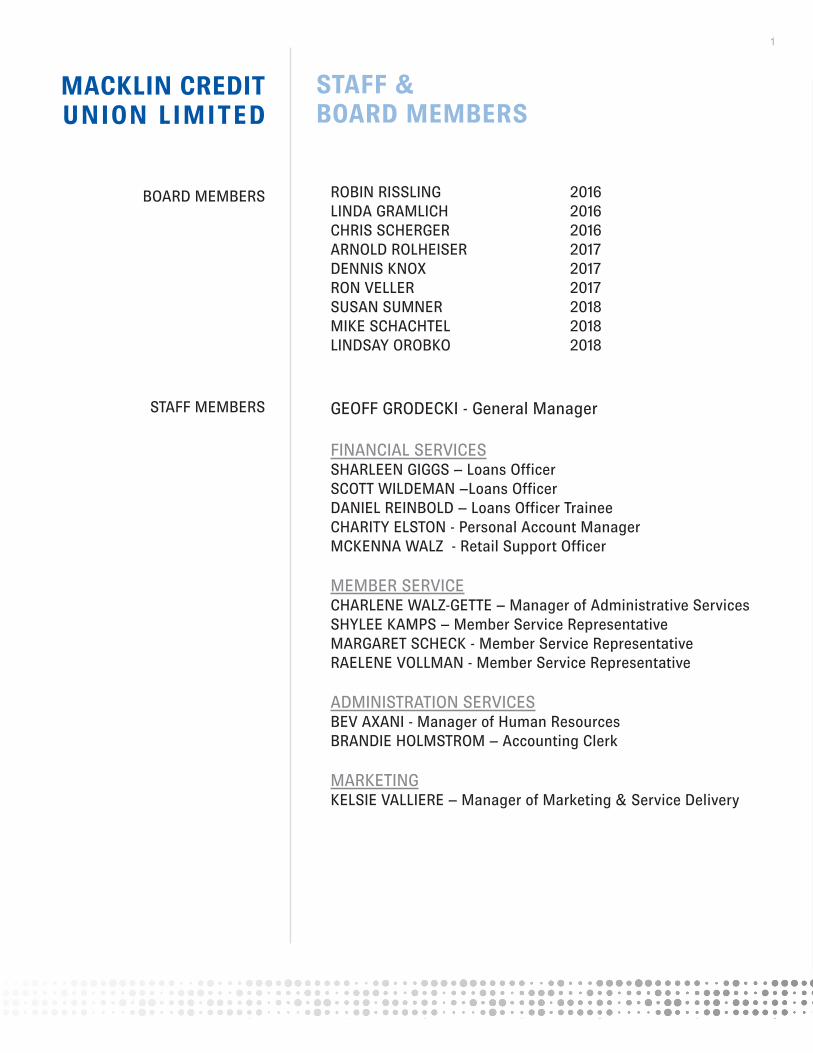

BOARD MEMBERS

STAFF MEMBERS

ROBIN RISSLING 2016LINDA GRAMLICH 2016 CHRIS SCHERGER 2016ARNOLD ROLHEISER 2017DENNIS KNOX 2017 RON VELLER 2017SUSAN SUMNER 2018MIKE SCHACHTEL 2018 LINDSAY OROBKO 2018

GEOFF GRODECKI - General Manager

FINANCIAL SERVICESSHARLEEN GIGGS – Loans OfficerSCOTT WILDEMAN –Loans OfficerDANIEL REINBOLD – Loans Officer Trainee CHARITY ELSTON - Personal Account ManagerMCKENNA WALZ - Retail Support Officer

MEMBER SERVICECHARLENE WALZ-GETTE – Manager of Administrative ServicesSHYLEE KAMPS – Member Service RepresentativeMARGARET SCHECK - Member Service RepresentativeRAELENE VOLLMAN - Member Service Representative

ADMINISTRATION SERVICESBEV AXANI - Manager of Human ResourcesBRANDIE HOLMSTROM – Accounting Clerk

MARKETINGKELSIE VALLIERE – Manager of Marketing & Service Delivery

STAFF & BOARD MEMBERS

1

MACKLIN CREDIT UNION LIMITED

CREDIT UNION MARKET CODE

Macklin Credit Union voluntarily adheres to the Credit Union Market Code. This code has been jointly developed by Saskatchewan credit unions, SaskCentral and Credit UnionDeposit Guarantee to ensure the protection of credit union members. The code sets forth guidelines for the following areas:

• Complaint handling, which outlines the process for dealingwith all complaints regarding the service, products, fees orcharges of Macklin Credit Union.

• Fair sales by outlining the roles and relationship of staff toall member/clients and in accordance with the financialservices agreement.

• Financial planning process to advise member/clients onthe risks and benefits associated with financial planningservices.

• Privacy to protect the interests of those who do businesswith Macklin Credit Union. Privacy is the practice to ensureall member/client information is kept confidential and usedonly for the purpose for which it was gathered.

• Professional standards to preserve a positive image ofMacklin Credit Union among our members, clients andcommunities.

• Capital management to ensure our capital structure alignswith our risk philosophy.

• Financial reporting to adhere to business and industrystandards.

• Governance practices to adhere to the intent andstipulation of our corporate bylaws, which are approved bythe membership of Macklin Credit Union.

• Risk management to ensure all risks are measured andmanaged in an acceptable fashion.

Front of Macklin Credit Union on Herald Street.

2

MACKLIN CREDIT UNION LIMITED

CO-OPERATIVE PRINCIPLES

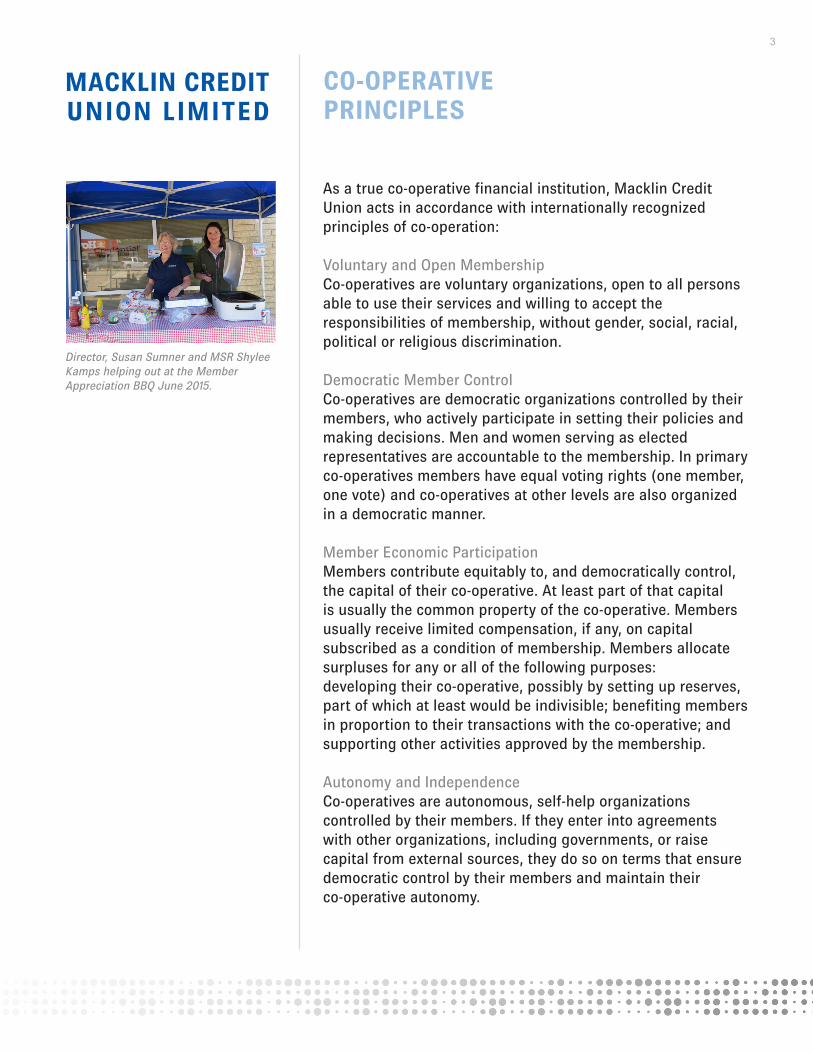

As a true co-operative financial institution, Macklin Credit Union acts in accordance with internationally recognized principles of co-operation:

Voluntary and Open MembershipCo-operatives are voluntary organizations, open to all persons able to use their services and willing to accept the responsibilities of membership, without gender, social, racial, political or religious discrimination.

Democratic Member Control Co-operatives are democratic organizations controlled by their members, who actively participate in setting their policies and making decisions. Men and women serving as elected representatives are accountable to the membership. In primary co-operatives members have equal voting rights (one member, one vote) and co-operatives at other levels are also organized in a democratic manner.

Member Economic Participation Members contribute equitably to, and democratically control, the capital of their co-operative. At least part of that capital is usually the common property of the co-operative. Members usually receive limited compensation, if any, on capital subscribed as a condition of membership. Members allocate surpluses for any or all of the following purposes: developing their co-operative, possibly by setting up reserves, part of which at least would be indivisible; benefiting members in proportion to their transactions with the co-operative; and supporting other activities approved by the membership.

Autonomy and Independence Co-operatives are autonomous, self-help organizations controlled by their members. If they enter into agreements with other organizations, including governments, or raise capital from external sources, they do so on terms that ensure democratic control by their members and maintain their co-operative autonomy.

Director, Susan Sumner and MSR Shylee Kamps helping out at the Member Appreciation BBQ June 2015.

3

MACKLIN CREDIT UNION LIMITED

CO-OPERATIVEPRINCIPLES CONT.

Education, Training and Information Co-operatives provide education and training for their members, elected representatives, managers, and employees so they can contribute effectively to the development of their co-operatives. They inform the general public - particularly young people and opinion leaders - about the nature and benefits of co-operation.

Co-operation among Co-operatives Co-operatives serve their members most effectively and strengthen the co-operative movement by working together through local, national, regional and international structures.

Concern for Community Co-operatives work for the sustainable development of their communities through policies approved by their members

Meal in the Field with the Gerlings. Pictured with Loans Officer, Sharleen Giggs.

4

MACKLIN CREDIT UNION LIMITED

MINUTES OF THE 75TH ANNUAL GENERAL MEETINGAnnual MeetingMacklin Credit UnionDate: April 15, 2015

Confirmation of Quorum Present: President Ron Veller, confirmed a quorum.

Introductions:Geoff recognized all Staff and Ron recognized all Board Members.

Adoption of Agenda:Motioned by Dennis Knox and Rudolph Stang to adopt agenda as presented.Carried

Minutes:Motioned by Susan Sumner and Arnold Rolheiser to adopt the minutes of the Annual Board Meeting on April 15, 2014, as presented. Carried

President’s Report:President Ron Veller reported on 2014 in review.

General Manager’s Report:Geoff went through the Quick Facts in the report. He also acknowledged what the staff has done over the past year as there has been a lot of change. The Credit Union held a very successful Ag Out-look Information Seminar as well we facilitated a Student Financial Education learning session called Money$ense at the school. We also will be offering a $1,500.00 scholarship to students that will be enrolling in a post-secondary program of study relatable to the financial industry. Geoff also announced that Macklin Credit Union will be celebrating our 75th anniversary in November.

Board of Directors/Manager/Auditor Reports:Motion by Sharleen Giggs and Wade Sumner to adopt the Reports as read.Carried

Election Results:There was no election this year. Mike Schachtel, Lindsay Orobko, and Susan Sumner had agreed to leave their names stand and will remain on the board for another three year term.

Prize winners from Credit Union Day. Pictured with employee Raelene Vollman.

5

MACKLIN CREDIT UNION LIMITED

MINUTES OF THE 75TH ANNUAL GENERAL MEETING CONT.

Appointment of Auditors:Motioned by Marg Scheck and Darlene Kidd to adopt the reappoint-ment of MNP as Auditor’s for 2015. Carried

Appointment of Returning Officer:Motioned by Denis Wildeman and Brandie Holmstrom to appoint Maureen Stang as returning officer.Carried

New Business: Nothing to report.

Presentations and Farewells:Thank-you and presentations were given to the following staff: Linda Briley – 5 Year Service AwardBrandie Holmstrom – 5 Year Service AwardMarg Scheck – 10 Year Service AwardCharlene Walz-Gette – 10 Year Service AwardDennis Knox – 20 Year Service Award

Door Prizes:Passport Cover & Gift Card – Marg ScheckSalt & Pepper Set – Dennis KnoxGloves & Seeds – Darlene KiddGloves & Seeds – Wally ReschnyCoffee Mug – Gwen StangWater Bottle & iTunes Gift Card – Lindsay OrobkoWater Bottle & iTunes Gift Card – Brandie HolmstromCoffee Mug – Arnold Rolheiser

Adjournment:Arnold Rolheiser

Donation to Macklin Soccer from 2015 Bunnock Pancake Breakfast in partnership with Delta Coop.

On Right: Board President, Ron Veller

6

MACKLIN CREDIT UNION LIMITED

A MESSAGE FROM THE BOARD PRESIDENT

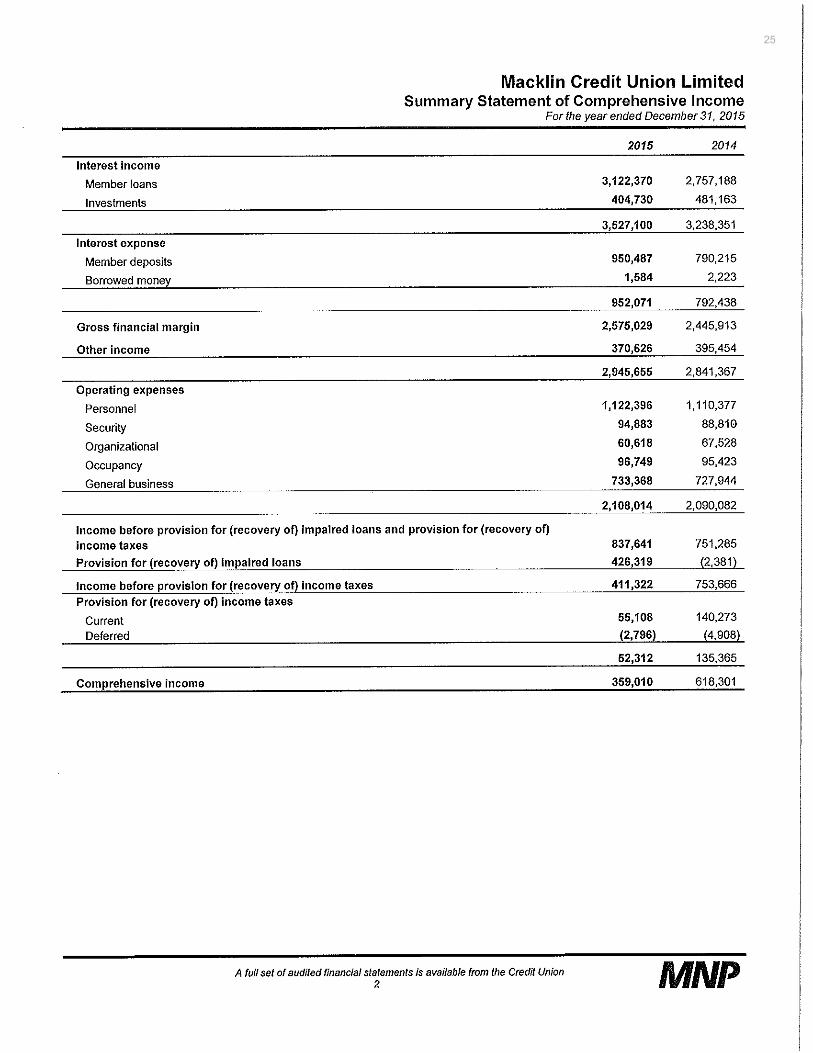

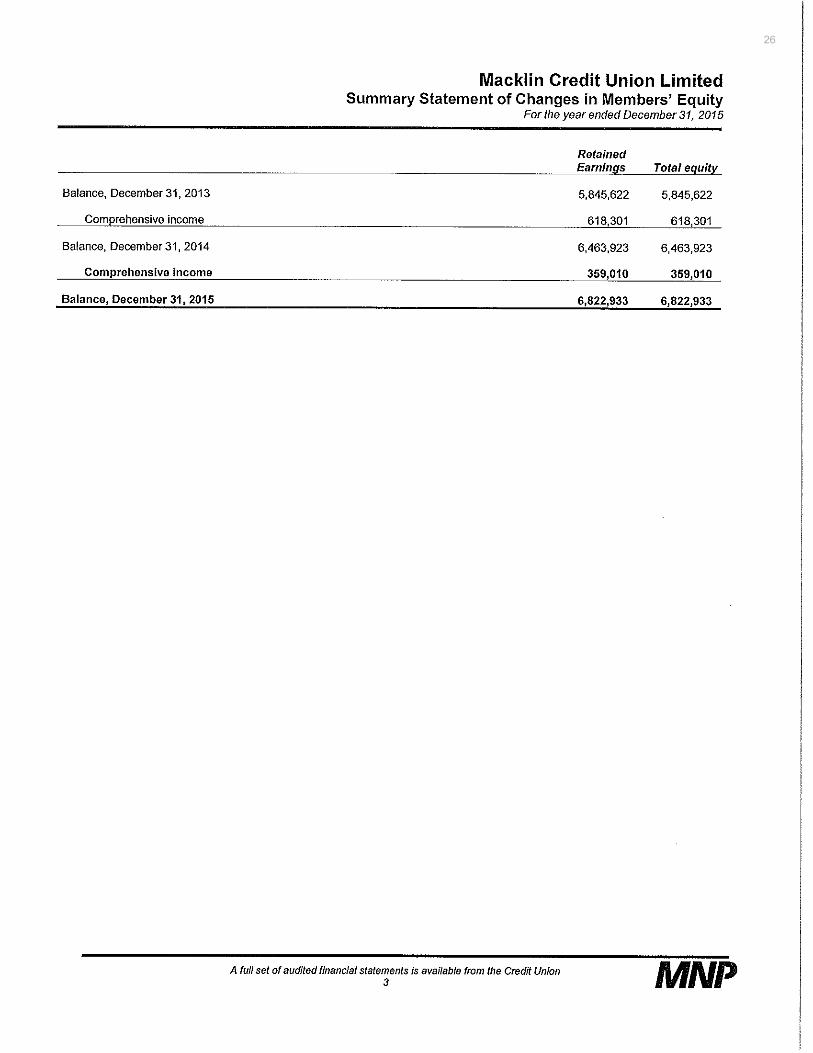

In 2015 Macklin Credit Union demonstrated growth in all key financial aspects when compared to 2014. Assets are at $103,070,225 million an increase of $5 million. Deposits are at $96,056,373 an increase of $11 million while loans at $79,320,403 are $11 million higher than the previous year. Retained Earnings of $6.822,933 represents an approximate increase of $400,000 (6.5% of assets). Income Growth for Macklin Credit Union totalled $359,010 and would have been $838,641 if not for a significant loan loss. Of major significance is that Risk Weighted Capital at year end was 13.06 % with a target of 13.25%; however, since the yearend statement for 2015 Macklin Credit Union’s Risk Weighted Capital is now at 13.26% and exceeds the target. As can be noted from this information Macklin Credit Union is certainly performing satisfactorily and compares favourably to the financial performances of similar sized or even slightly larger Credit Unions.

Macklin Credit Union has continued to engage in collaborative initiatives with other Credit Unions. One of the main focuses of management and staff has been a continued drive in developing a ‘service culture’. Allindications are that this particular focus is moving in the right direction. Macklin Credit Union staff continues to deliver the ‘Money$ense Program’ to grade 11 & 12 students at Macklin School and it certainly seems to be well received. Although there is now a challenging economic climate Macklin Credit Union is determined to respond in a proactive manner. For example, management has reached out to engage members who may be experiencing financial difficulties to assist them. Macklin Credit Union continues its strong commitment to community involvement whether that is in donations of time or money.

Macklin Credit Union has a very committed and dedicated group of employees who are led by a very competent management team. It is because of their efforts that Macklin Credit Union is a successful financial institution. Thank you to all employees for your service. Regrettably, Geoff will be moving on to a well deserved opportunity with a much larger Credit Union. His three years of service to Macklin Credit Union have been nothing less than exceptional. Under his guidance MCU is a thriving institution with a strong future. Good luck and thank you to Geoff for a job very well done!

As always it is important to acknowledge my Board colleagues who have given so much of their personal time and effort. The Board consists of a group representing diversified backgrounds and experiences which assist greatly in the performance of their duties and responsibilities. They are to be commended for the good work done on behalf of Macklin Credit Union.

Ultimately the success of Macklin Credit Union depends on its members. On behalf of the Board of Directors we thank members for their continued loyalty and patronage and ask for your continued support!

Ron Veller, PresidentMacklin Credit Union

Ron VellerBoard President

7

MACKLIN CREDIT UNION LIMITED

Geoff GrodeckiGeneral Manager

A MESSAGE FROMTHE GENERAL MANAGER

With the current economic challenges both locally and provincially, 2015 was a very challenging year for Macklin Credit Union. However, we had a very successful year, given the challenges presented to us and continue to have strong financial results. Macklin Credit Union looks very sustainable going forward.

The focus internally at Macklin Credit Union has been to continue working toward strengthening our Service Culture and to create value for our members by engaging in proactive conversations with you. Our Credit Union and staff have come a long way in the last few years and I am very proud of OUR Credit Union and our team. We are in much better financial position, we have a solid strategic direction and a dedicated and knowledgeable team including our board, our staff and management.

Again Macklin Credit Union had a good year considering both the local and provincial economies, especially relating to oil sector. Our credit union grew $4,514,805 OR 4.60%, in assets bringing them to $103,070,255 as of December 31/15. We have used a measured approach in building our assets to ensure we also build Capital which is essential to the Credit Union. Our assets are made up of a balance of loans and deposits as well as the equity of the Credit Union. Our loan portfolio grew $10,727,840 or 15.64% bringing our loans portfolio to 76.77% of our assets. This is important as we get a much larger return by borrowing our money out than by investing it at the current rates. Our deposits also grew in 2015 by $4,209,055 or 4.58% which given the economic challenges was excellent.

Macklin Credit Union’s income was lower than expected due to a loan loss in 2015 that came up half way through the year. We are proud of the fact that the credit union is in a strong position and was able to absorb the loss of $426,319, it is regrettable and was primarily driven by the economy. We will be taking the second part of this loss in 2016 but have been able to plan and prepare for it. Overall we had gross revenue of $411,322 pre-tax and net revenue of $359,010. This is lower than our goals but factoring in the loss we would have been right on our budget projections for 2015. All things being equal challenges like this arise from time to time and it speaks to the strengths of Macklin Credit Union that we are still moving in a positive direction even through the challenging situation, all the while still providing a high level of service and value to our members.

Continued on next page.

8

Another area we focus on in leading Macklin Credit Union is in building Capital, which allows us to continue to build our credit union and allow us the ability to deal with adversity like we have had in 2015. Our Risk Weighted Capital ended the year at 13.06%, with the new buffer of an additional 2.50% coming in for 2016. Through our internal process of determining the capital needs of the credit union being at 13.25%, we found ourselves very close to our goal and at the time of completing this report have reached that milestone early in 2016. Our Leveraged Capital (Tier 1) is also continuing to trend upward at 6.60% for 2015. These are both very positive indicators in the long term sustainability of Macklin Credit Union going forward.

It is also with mixed emotions that I must announce that I will be leaving Macklin Credit Union for another opportunity with a Credit Union in BC. I want to thank the Board for having the trust and faith in me to make a positive impact and for working with me in a positive manner, as members you should be happy to have a group of people in charge of the stewardship of Macklin Credit Union. I also want to thank the staff, we have travelled a difficult road and I commend the staff for doing their absolute best to provide the services to our members, create value for our communities and most of all to create a place where our members enjoy coming for their financial services. Again this credit union is lucky to have such a dedicated group of professionals. Lastly I want to thank our members, without you supporting your credit union, there simply isn’t one. We all appreciate your patronage. Thank you again.

Geoff GrodeckiGeneral ManagerMacklin Credit Union

MACKLIN CREDIT UNION LIMITED

A MESSAGE FROMTHE GENERAL MANAGER CONT.

Geoff GrodeckiGeneral Manager

9

After a strong performance in 2014, 2015 saw continued growth in assets of 4.60% or $4,514,805 to $103,070,225 in spite of a downturned market. This was made possible by continued focus on balance sheet management and better deployment of our assets. Our income levels have grown to the point that managed asset growth can be comfortably sustained. Increased focus on superior member service has also allowed us to proactively address challenges that come with an unsteady marketplace.

MACKLIN CREDIT UNION LIMITED

MANAGEMENTDISCUSSION & ANALYSIS

Macklin Credit Union is one of 46 credit unions operating in Saskatchewan. Our organization strives to offer full financialoptions to our members including a complete range of lending, deposits, registered, and wealth management services.

INTRODUCTION

The vision for Macklin Credit Union is to be the “first choice for financial services in our community.” To monitor specific objectives throughout the year that support this vision, the board develops a strategic plan which is a framework that establishes, measure and monitors the progress towards achieving our goals.

Our key strategic objectives for 2016 revolve around:• Member Service Excellence• People – Staff & Management• Finance• Community• Visionary Leadership

STRATEGIC PLAN

Macklin Credit Union uses strategic and financial plans that are approved by the Board of Directors. Monthly, the Board reviews results including assets, liabilities, income and expenses - focusing in on a number of key ratios.

FINANCIAL RESULTS

10

Our ROA before taxes in 2015 was $411,322 or .40%. This has allowed Macklin Credit Union to continue to positively address increased focus on the Capital Adequacy of the Credit Union and this will remain a focus going forward. If you factor in a significant loan loss in 2015 representing .42% ROA, Macklin Credit Union would have reached its strategic goals for the year.

Macklin Credit Union did sustain a significant loan loss totaling $426,319 for the year of 2015. It is a testament to the work done by both the staff and board that this loss has been absorbed with the Credit Union still seeing a profit for the year. As the market continues to affect our membership, strategies surrounding our approach to credit risk will be adapted accordingly. Macklin Credit Union has taken steps to work proactively with our members during this economic downturn and will continue to provide assistance where we can.

The Credit Union’s loan portfolio increased by $10,727,840 or 15.64% in 2015 with net loans to assets increasing to 76.77%.

MACKLIN CREDIT UNION LIMITED

MANAGEMENTDISCUSSION & ANALYSIS CONT.

FINANCIAL RESULTS cont.

11

LOAN PORTFOLIO

MEMBERDEPOSITS

MACKLIN CREDIT UNION LIMITED

MANAGEMENTDISCUSSION & ANALYSIS

Loan growth was attained through organic growth along with accessing loans through syndication and purchasing leases. We also attribute some of the growth to our shift to a more service driven culture within the branch.

Through better deployment of the Credit Union’s assets we are seeing more robust income growth, which in turn will continue to strengthen our Capital Position. The loan portfolio continues to be well diversified.

FINANCIAL RESULTS cont.

Macklin Credit Union also saw deposit growth of 4.58%, or $4,209,055, for 2015. Such growth is average for our organization. By maintaining strong financial relationships with our members we believe this positive trend will continue in 2016 and beyond.

12

As a Board of Directors, plans need to be put into place that work to balance the use of capital (return on equity) and the amount of capital given risks (capital required to absorb losses). The Credit Union is required to maintain, at all times, a capital base which is adequate in relation to the business conducted.

MACKLIN CREDIT UNION LIMITED

CAPITALRATIOS

We measure capital adequacy using two key measures; Tier 1 Capital/Total Assets and Risk-Weighted Capital ratios. Credit Union Deposit Guarantee Corporation (CUDGC) sets strong regulatory guidelines to which credit unions must adhere.

Tier 1 Capital/Total Assets is a measure of the adequacy of capital. Regulators consider 5% to be the minimum level acceptable for this ratio. With the size and structure of Macklin Credit Union a target is in place to achieve a Tier 1 ratio of 7.00%. Macklin Credit Union ended 2015 with a Tier 1 Capital/Total Assets ratio of 6.60% and will continue to focus on increasing this ratio.

Risk Weighted Capital is a measure of the adequacy of capital with considerations given to the risk of assets. MNP describes this as the level of capital required as based on a prescribed percentage of the total value of risk rated assets, each asset of the Credit Union being assigned a risk factor based on the probability that a loss may be incurred on the ultimate realization of that asset.

13

MACKLIN CREDIT UNION LIMITED

CAPITALRATIOS CONT.

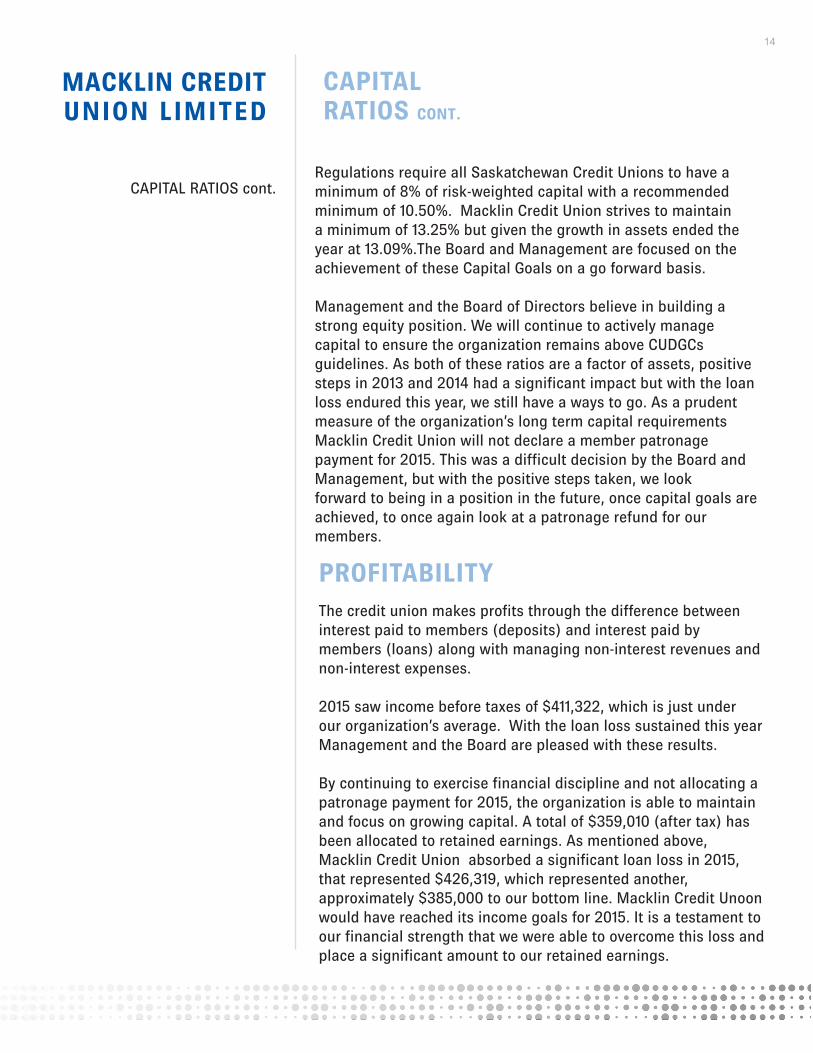

Regulations require all Saskatchewan Credit Unions to have a minimum of 8% of risk-weighted capital with a recommended minimum of 10.50%. Macklin Credit Union strives to maintain a minimum of 13.25% but given the growth in assets ended the year at 13.09%.The Board and Management are focused on the achievement of these Capital Goals on a go forward basis.

Management and the Board of Directors believe in building a strong equity position. We will continue to actively manage capital to ensure the organization remains above CUDGCs guidelines. As both of these ratios are a factor of assets, positive steps in 2013 and 2014 had a significant impact but with the loan loss endured this year, we still have a ways to go. As a prudent measure of the organization’s long term capital requirements Macklin Credit Union will not declare a member patronage payment for 2015. This was a difficult decision by the Board and Management, but with the positive steps taken, we look forward to being in a position in the future, once capital goals are achieved, to once again look at a patronage refund for our members.

PROFITABILITYThe credit union makes profits through the difference betweeninterest paid to members (deposits) and interest paid by members (loans) along with managing non-interest revenues and non-interest expenses.

2015 saw income before taxes of $411,322, which is just under our organization’s average. With the loan loss sustained this year Management and the Board are pleased with these results.

By continuing to exercise financial discipline and not allocating a patronage payment for 2015, the organization is able to maintain and focus on growing capital. A total of $359,010 (after tax) has been allocated to retained earnings. As mentioned above, Macklin Credit Union absorbed a significant loan loss in 2015, that represented $426,319, which represented another, approximately $385,000 to our bottom line. Macklin Credit Unoon would have reached its income goals for 2015. It is a testament to our financial strength that we were able to overcome this loss and place a significant amount to our retained earnings.

CAPITAL RATIOS cont.

14

Each year our credit union spends significant resources measuring and assessing risks to ensure we are adequately prepared to serve our communities now and in the future. This process is called Enterprise Risk Management (ERM) and is a requirement of all credit unions in Saskatchewan as set out by Credit Union Deposit Guarantee Corporation. Annually the Board of Directors have identified key risks associated with the organization’s specific business activities. Through this process, the following risks have been identified:

Credit• Inability to maintain low delinquency and to maintain

necessary allowance.• Risk of potential losses due to makeup of loan portfolios.

Market• The risk that market prices will change (interest rates) having

a negative affect on earnings or capital.

Legal and Regulatory• Inability to absorb the human and financial costs of sustaining

compliance with increasing regulatory requirements.• Inability to develop and implement an internal audit process.

Operational• Inability to attract and retain qualified and capable personnel• Dependency on 3rd party suppliers• Inability to cope with a disaster.

Strategic• Impact of changing economic environment• Failure to anticipate the timing for seeking amalgamation

while in a position of strength.

MACKLIN CREDIT UNION LIMITED

ENTERPRISERISK MANAGEMENT

IDENTIFIED RISKS

15

MACKLIN CREDIT UNION LIMITED

Credit RiskCredit risk is the risk of loss arising from a borrower or counterparty’s inability to meet its obligations. There is increased credit risk due to the current economy. Due to the significant loan loss, Macklin Credit Union has undertaken a comprehensive review of the top twenty-five borrowers to ensure all financial information is up to date, all security registrations are up to date and valid and any risks have been addressed. The increased due diligence will ensure Macklin Credit Union is prepared and protected during the challenging economy.

Market RiskMarket risk is the exposure to potential loss from changes in market prices or rates. Losses can occur when values of assets andliabilities or revenues are adversely affected by changes in market conditions such as interest rate or foreign exchange movement.

Legal and Regulatory RiskLegal and regulatory risk is the risk arising from potential violation of, or nonconformance with, laws, rules, regulations, prescribed practices, or ethical standards.

Operational RiskOperational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems, or external events. Exposures to this risk arise from deficiencies in internal controls, technology failures, human error, employee integrity or natural disasters.

Strategic RiskStrategic risk is the risk that adverse decisions, ineffective or inappropriate business plans, or failure to respond to changes in the competitive environment, customer preferences, product obsolescence, or resource allocation will impact our ability to meet our objectives. This risk is a function of the compatibility of an organization’s strategic goals, the business strategies developed to achieve these goals, the resources deployed against these goals, and the quality of implementation.

Liquidity RiskLiquidity risk is the potential inability to meet obligations such as liability maturities, deposit withdrawals, or funding loans without incurring unacceptable losses. Liquidity risk includes the inability to manage unplanned decreases or changes in funding sources.

ENTERPRISERISK MANAGEMENT CONT.

IDENTIFIED RISKS

16

The governance of Macklin Credit Union is anchored in the co-operative principle of democratic member control.

Mandate and ResponsibilitiesThe Board is responsible for the strategic oversight, business direction and supervision of management of Macklin Credit Union. Acting in the best interest of the credit union and its members, the Board’s actions adhere to the standards set out in The Credit Union Act 1998, the Standards of Sound Business Practice, and other applicable legislation.

The Board of Directors acknowledges these key roles:

• Exercising the powers of the credit union directly or indirectlythrough employees

• Establishing and maintaining prudent policies for theoperation of the credit union

• Directing management on the business affairs of the creditunion

• Acting honestly and in good faith with a view to the bestinterests of the credit union at the exclusion of other interests

• Exercising the care, diligence and skill of a prudent person indirecting the credit union’s affairs.

Board CompositionThe Board is composed of 9 individuals elected for 3 year terms. Each Board member must sign and acknowledge a declaration of office, statement of disclosure and conflict of interest yearly.

CommitteesThe responsibilities of the Board of a modern financial services organization involve an ever-growing list of duties. Macklin Credit Union maintains a number of committees comprised of directors. This partitioning of responsibilities enables a clear focus on specific areas of activity vital to the effective operation of our credit union.

MACKLIN CREDIT UNION LIMITED

CORPORATE STRUCTURE& GOVERNANCE

BOARD OF DIRECTORS

DIRECTORS

17

MACKLIN CREDIT UNION LIMITED

Audit CommitteeThis committee oversees the financial reporting process, reviews financial statements, liaisons with internal and external auditors and regulators. The committee consists of at least 3 directors. The Board determines the skills and abilities needed on the committee and chooses its members accordingly.

Risk CommitteeThis committee is in place to oversee the Risk Tolerances of the Credit Union through the ICAAP and ERM process, the risk levels and policies and procedures are developed in kind. As above, this committee consists of at least 3 Directors.

Nominating CommitteeThe Nominating Committee oversees the nomination and election processes for elections of credit union directors. The committee is comprised of three Board members elected the previous year.

Conduct Review CommitteeThe Conduct Review Committee ensures that Macklin Credit Union acts with the full integrity and objectivity of its directors and employees by having in place policies, processes and practices that protect people and the organization from claims and from the perception of unfair benefit or conflict of interest.

Executive CommitteeThe Executive Committee is in place to act on behalf of the Board between regular or special board meetings on all board matters where appropriate. This committee is composed of the President, Vice President and one other Director.

Building CommitteeThe Building Committee is in place to ensure the facilities of the Credit Union are maintained and any issues are dealt with in a timely fashion. As well any major facility requirements are examined and dealt with.

CompensationThe Credit Union has policies in place which states that directors receive nominal compensation for their service. Directors receive per diems for meetings attended and are reimbursed for travel and training required by the organization.

Director TrainingThe Credit Union provides the necessary opportunities for personal and professional self development of the directors and committee members. The Credit Union Director Achievement Program (CUDA) is a national program giving board members a better understanding of their role and of the business for which they are accountable. Attendance at credit union system meetings, conferences, conventions and seminars also provide opportunities to support director development

CORPORATE STRUCTURE& GOVERNANCE CONT.

BOARD COMMITTEES

From Left: Director, Arnold Rolheiser along with his spouse, Linda, MSR Marg Scheck and her husband, Ernest on the blue carpet at the 75th Celebration.

18

The management team consists of four positions:

• General Manager – Geoff Grodecki-responsible for all areas of the operation.

• Manager of Administrative Services – Charlene Walz-Gette-responsible for the member service representatives,investments, compliance and all administrative functions.

• Manager of Marketing & Service Delivery - Kelsie Valliere-responsible for the financial services department-responsible for all marketing and employee service culturedevelopment.

• Manager of Human Resources - Bev Axani-responsible for the administration of payroll, benefits andpension plan for all employees.-responsible for implementation of performance managementsystem and ongoing learning plans with staff.

MACKLIN CREDIT UNION LIMITED

EXECUTIVE MANAGEMENT

CORPORATE STRUCTURE& GOVERNANCE CONT.

19

MACKLIN CREDIT UNION LIMITED

• Today there are 46 credit unions in Saskatchewan serving 230communities through 264 service outlets.

• Credit unions offer financial products and services to more than472,000 members.

• Saskatchewan credit union assets reached $20.8 billion withrevenue of over $881 million.

• Credit union lending amounts to $16.6 billion.

• Almost 450 board members are locally elected by members of eachcredit union to provide strategic direction to their managementteams.

• As independent financial institutions owned and controlled by theirmembers, credit unions are shaped by community needs.Saskatchewan credit unions range in asset size from $17 million tomore than $5 billion.

• In 2015, Saskatchewan credit unions returned close to $7.3 millionto their members in the form of patronage equity contribution anddividends.

• Credit unions are a major contributor to Saskatchewan’s economy,employing almost 3,500 people.

• In 2014, Saskatchewan credit unions contributed $73,607 tointernational development projects to help co-operatives andcredit unions in other countries. (2015 numbers are not available.)

• In 2014, Saskatchewan credit unions contributed more than $7.4million to growing communities. Our fundraising effortsbrought in almost $430,000 for causes like the Children’s HospitalFoundation of Saskatchewan, Red Cross Disaster Relief, Terry FoxRun and Telemiracle. Our employees logged more than 43,000 hoursof volunteer time for community organizations. (2015 numbers arenot available.)

• Funds held on deposit in Saskatchewan credit unions arefully guaranteed through the Credit Union Deposit GuaranteeCorporation. The full guarantee is made possible through acomprehensive deposit protection regime that is focused onprevention.

QUICK FACTS

AS OF DEC. 31/15 UNLESS OTHEWISE INDICATED

Employees Kelsie Valliere and Charity Elston presenting Money$ense to the Grade 11 students at Macklin School.

20

21

22

23

24

25

26

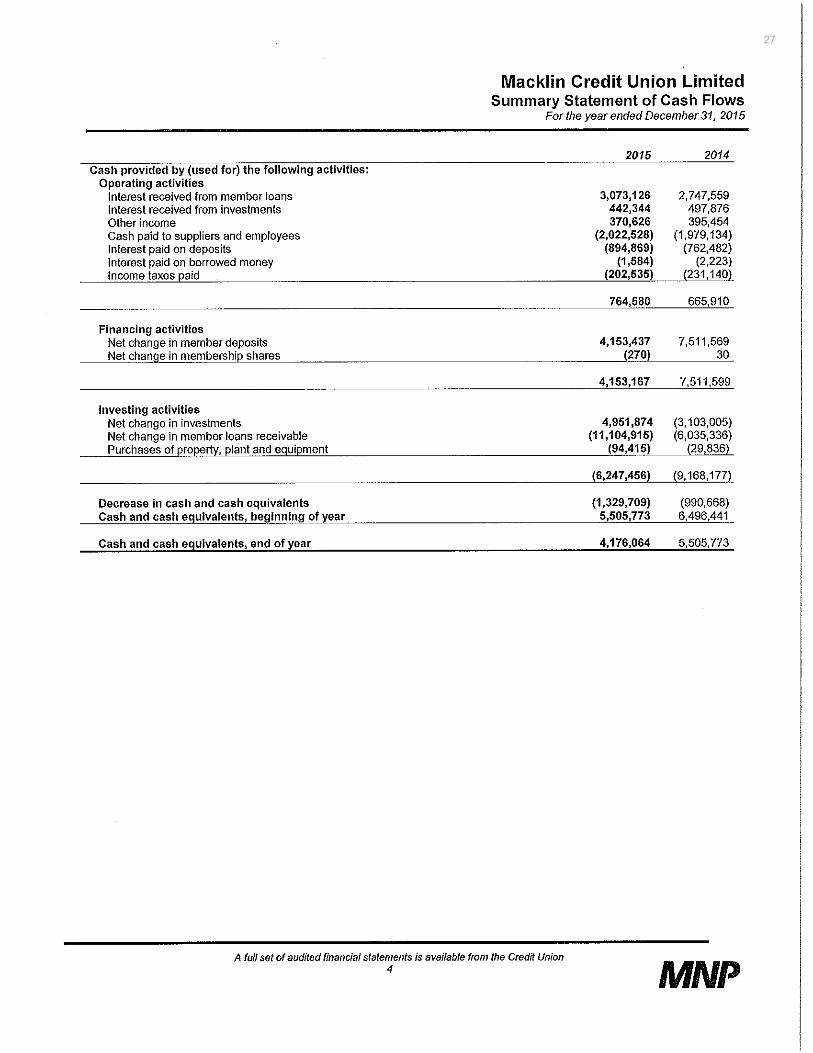

27