inter-co-operative trading & community credit

DESCRIPTION

Inter-Co-Operative Trading & Community Credit. Prepared and presented by XO Limited www.barter-software.com Email: [email protected]. Problems Faced By Small & Medium Sized Businesses. COMPETITION There is no longer market protection for locally owned businesses - PowerPoint PPT PresentationTRANSCRIPT

Inter-Co-Operative Trading &

Community Credit

Prepared and presented by XO Limited

www.barter-software.comEmail: [email protected]

Problems Faced By Small & Medium Sized Businesses

COMPETITION

There is no longer market protection for locally owned businesses

Many customers are no longer loyal to businesses if there are “cheaper” or “newer” alternatives

The competitor may be a larger business which is better funded and/or has better marketing and/or is entrenched in the market

Some businesses can afford to make a “loss” in order to acquire customers, leaving other businesses unable to compete

Competitors cost of production may be less or they may receive subsidies from outside organizations in order to compete

Competitors may have a more diverse range of products or services

Consumers are price / range sensitive

THE INABILITY TO CAPITALIZE ON ECONOMIES OF SCALE

Larger businesses have a lower production costs and sell their products at a lower rate due to a number of factors:

Centralized administration

Consolidated storage and transport

Purchasing supplies in bulk

Purchasing at a negotiated discount

Small to medium sized businesses may be unable to achieve the same economies of scale – even when grouped together as they will still be responsible for their own accounting, storage, small item purchases and other expenses unique to themselves.

Problems Faced By Small & Medium Sized Businesses

LOCAL MARKET PRODUCTION COSTS MAY BE UNCOMPETITIVE

Staff and materials/supplies costs may be higher in the local market than outside it (cheaper overseas labor, subsidized labor, cheaper materials etc)

Regulations may exist which outside competition may not have to comply with

Compliance might involve the same amount of paperwork for a large business as a small/medium sized business – however a smaller business will have less staff and resources

Problems Faced By Small & Medium Sized Businesses

BUSINESS SALES AND INCOME MAY BE SEASONAL

Many small to medium sized businesses are seasonal in nature resulting in periods of lower income. Some types of these businesses are:

TourismFood ProductionManufacturing (demand and raw materials production related)Service Industries (during peak holiday periods etc)

Larger business may be able to diversify their product or service offerings to allow for seasonality causes. They may also be able to borrow funds to cover “off season” expenses at a lower cost than the lower market might be able to obtain (due to their size, risk profile, offshore lending capabilities, greater market reach etc).

One bad season may result in the failure of the entire business

Problems Faced By Small & Medium Sized Businesses

INABILITY TO HEDGE AGAINST MARKET DOWN-TURNS

Local producers are often unable to fully insure against local market down-turns. These could be caused by a variety of factors:

Natural disaster (flood, fire, drought etc)

Inability to acquire needed supplies (sold elsewhere for a better profit, out of stock, price-rise)

Poor seasonal returns (lower price received than usual because of a glut on the market, less product produced resulting in less income, market protections for competitors, fickle customers, more market exposure for the competitors)

Lack of cash available in the local economy (recession)

Problems Faced By Small & Medium Sized Businesses

SURPLUS STOCK/CAPACITY

In areas of high or unfair competition, or where there is a market down-turn or seasonal low, the result is a surplus of capacity. Historically surpluses are dealt with by one of two ways:

Marking down the product or service

• This may lower future price expectations from the market

• May require the overall reduction in price for non-surplus stock of the same type – thereby lowering total income

Binning / Destroying / Wasting the product or service

• Artificially keeps prices high

• Looses all of the value of the surplus

• May be dealt with through less production (and wasted capacity)

Problems Faced By Small & Medium Sized Businesses

LACK OF CAPITAL TO EXPAND THE BUSINESS

In order to compete against subsidized producers, or new competitors in the market a small business must expand in one of several ways:

produce or acquire more product at a lower cost diversify the product range and offering change market strategy / target market

In order to do this the business must get additional capital. However:

Bank loans come with high interest rates which a business may be unable to afford

Loans are only given based on the businesses current production capacity and profitability – in a market with a new competitor profitability may have dropped so loans may be unattainable

Third party investment into small business means the owner has the potential to loose control and returns may be siphoned off by other shareholders

Problems Faced By Small & Medium Sized Businesses

LACK OF INCENTIVE TO EXPAND THE BUSINESS

In order to compete businesses must expand. With expansion comes:

Greater risk (financial risk, stress, risk of loosing market share)Less free timeReduction in available capital (borrowed funds must be repaid with additional interest, new shareholder capital requires sharing of resulting products)More work for the business ownersPotential for less income (confusing the market, lack of focus, requirements for output exceeding available resources)

It is often easier to sell the business and “cash out” than it is to compete head-on against new entrants.

Problems Faced By Small & Medium Sized Businesses

Solutions

Partial Solutions

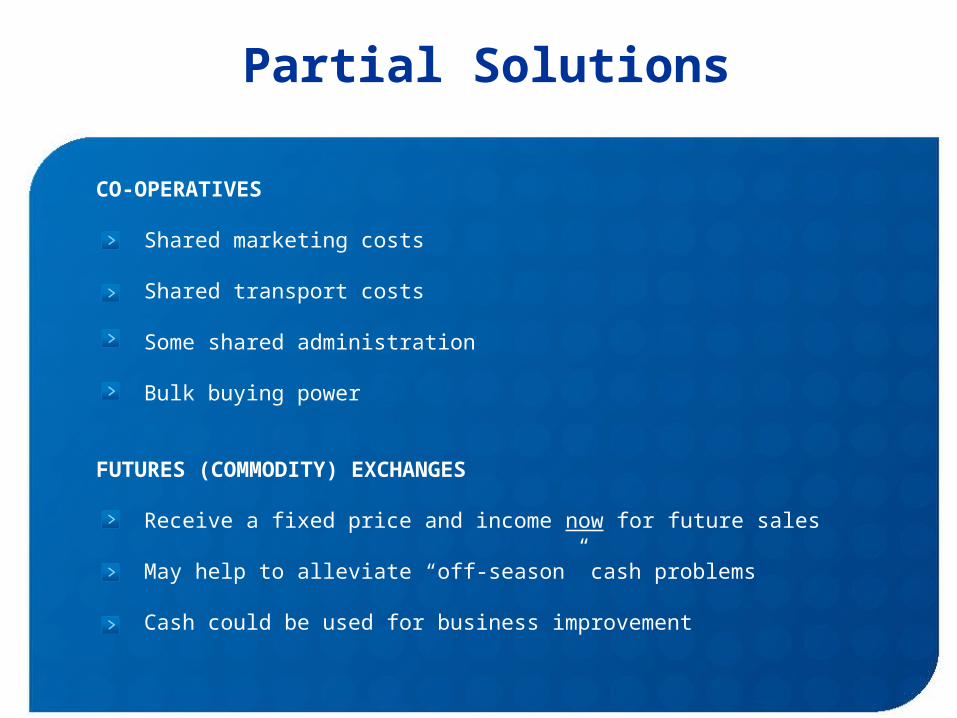

CO-OPERATIVES

Shared marketing costs

Shared transport costs

Some shared administration

Bulk buying power

FUTURES (COMMODITY) EXCHANGES

Receive a fixed price and income now for future sales

May help to alleviate “off-season” cash problems

Cash could be used for business improvement

Partial Solutions

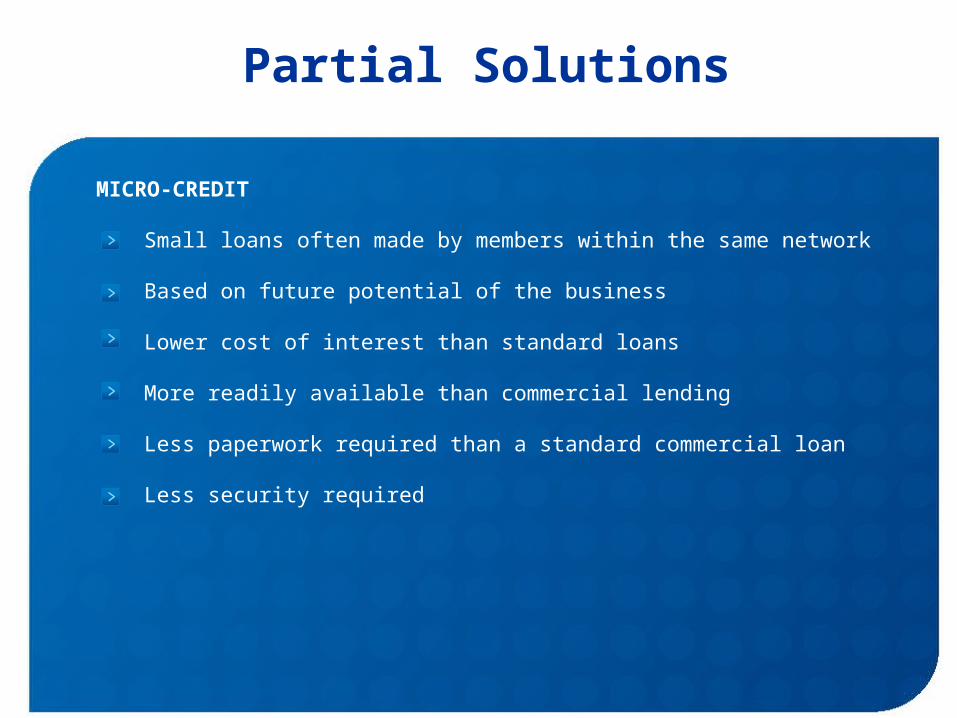

MICRO-CREDIT

Small loans often made by members within the same network

Based on future potential of the business

Lower cost of interest than standard loans

More readily available than commercial lending

Less paperwork required than a standard commercial loan

Less security required

Partial Solutions

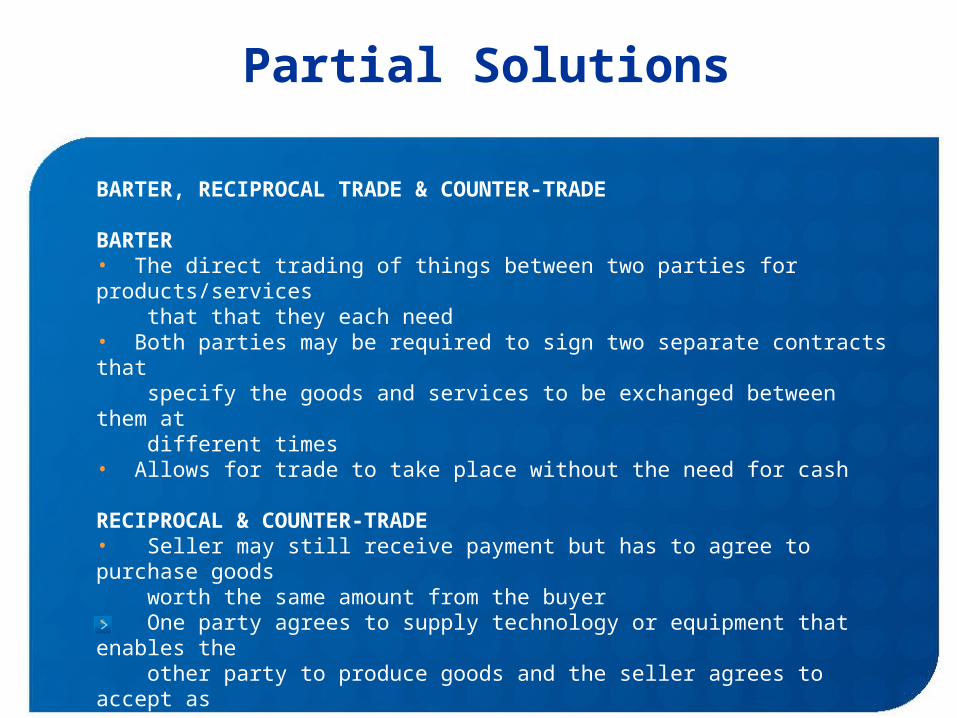

BARTER, RECIPROCAL TRADE & COUNTER-TRADE

BARTER• The direct trading of things between two parties for products/services that that they each need• Both parties may be required to sign two separate contracts that specify the goods and services to be exchanged between them at different times• Allows for trade to take place without the need for cash

RECIPROCAL & COUNTER-TRADE• Seller may still receive payment but has to agree to purchase goods worth the same amount from the buyer • One party agrees to supply technology or equipment that enables the other party to produce goods and the seller agrees to accept as payment a portion of the output or buy it back

Keeps money in the local community – even if bartering is not local the asset value in the community is not depleted

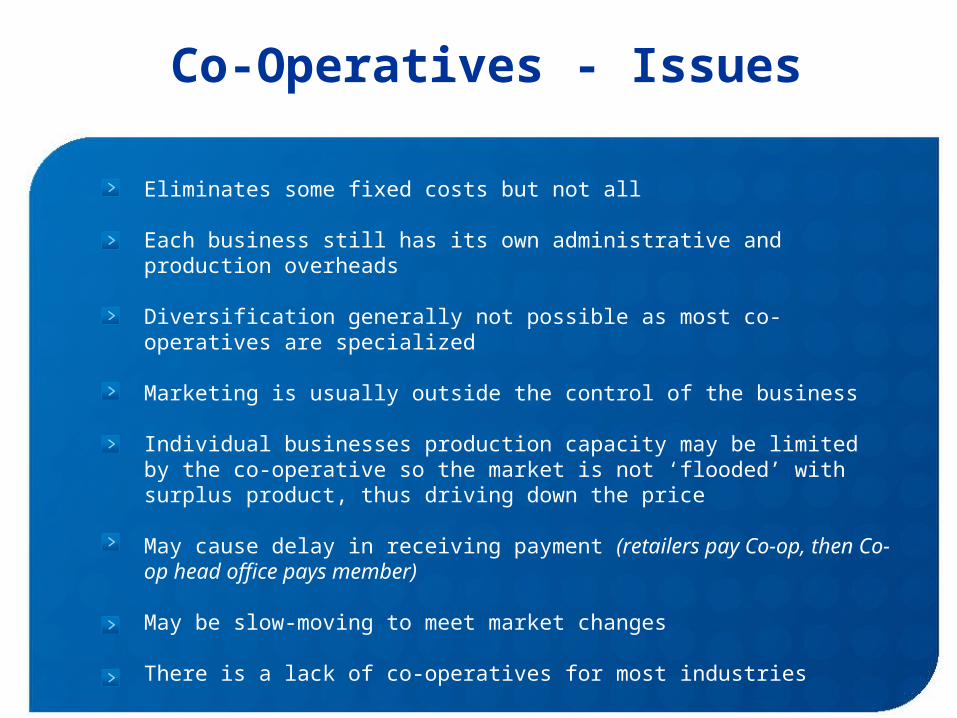

Co-Operatives - Issues

Eliminates some fixed costs but not all

Each business still has its own administrative and production overheads

Diversification generally not possible as most co-operatives are specialized

Marketing is usually outside the control of the business

Individual businesses production capacity may be limited by the co-operative so the market is not ‘flooded’ with surplus product, thus driving down the price

May cause delay in receiving payment (retailers pay Co-op, then Co-op head office pays member)

May be slow-moving to meet market changes

There is a lack of co-operatives for most industries

Futures Exchanges - Issues

Generally not available to small to medium businesses

Not available to all types of industries

Futures/Commodity traders receive the benefit of raises in prices if the value of the goods goes higher than usual

Quantity of product to be sold is pre-established and does not take into account any surplus

Short-falls have to be met by the producer – meaning a potential for greater risk

Micro-Credit - Issues

Often not available to larger businesses

Maximum loan size is very small (generally less than $1,000)

Attracts interest

Money may be borrowed from outside the community with the principle PLUS interest leaving the community

Lack of surety that then loan will result in a long-term stimulation of local trade

Some societies prohibit all forms of interest/usury (eg. Islam)

Barter - Issues

Requires a co-incidence of needs and wants (You have fish, I have milk. I want fish. You want milk. Let’s trade!)

Trades need to be of a similar value between participants

Bartering outside the local community does not increase the asset value of the community

Trade is conducted in an ad-hoc manner with no central registry of those wanting/needing trade

Does not allow for finance (buy now, repay later with own goods) unless there is a reciprocal need from the seller for the purchasers own goods

Is administratively difficult

The Complete Solution

A combined, synergistic, approach designed to:

Improve the amount and availability of capital for small to medium sized businesses

Work with business owners in a co-operative manner to increase and realize the value of their local assets

Eliminate the need for micro-credit, direct barter & high-cost finance

Enable the trade of products and services even in periods when cash may be hard to come by

Promote and foster local trade and enterprise

Ensure the majority of assets stay within the local community

Promote local entrepreneurship

Improve the competitiveness of local business

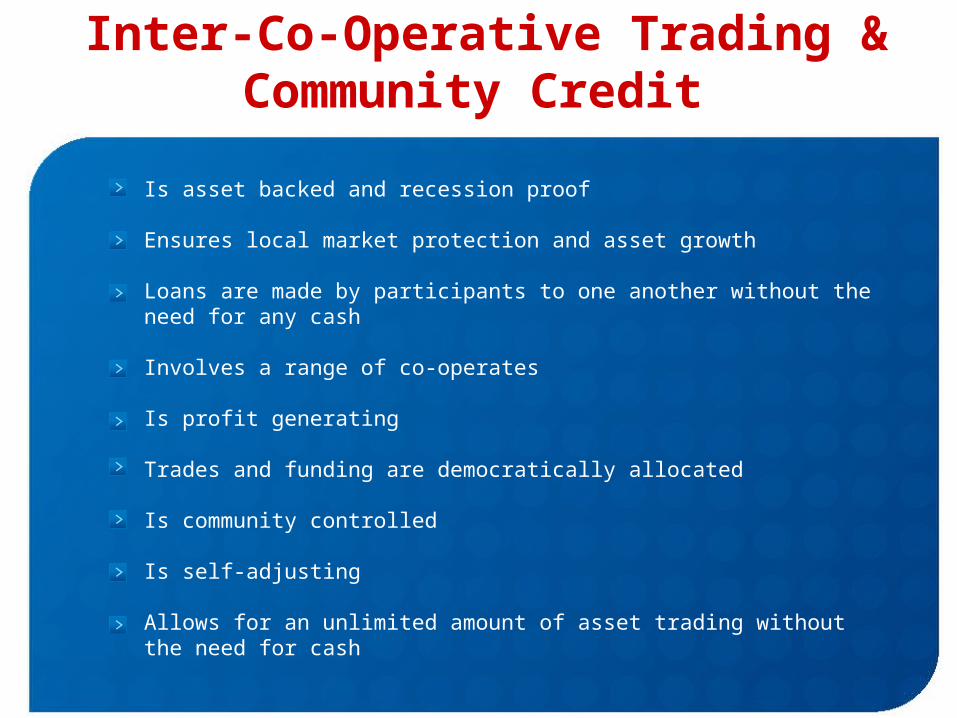

Inter-Co-Operative Trading & Community Credit

Is asset backed and recession proof

Ensures local market protection and asset growth

Loans are made by participants to one another without the need for any cash

Involves a range of co-operates

Is profit generating

Trades and funding are democratically allocated

Is community controlled

Is self-adjusting

Allows for an unlimited amount of asset trading without the need for cash

Components of the Solution

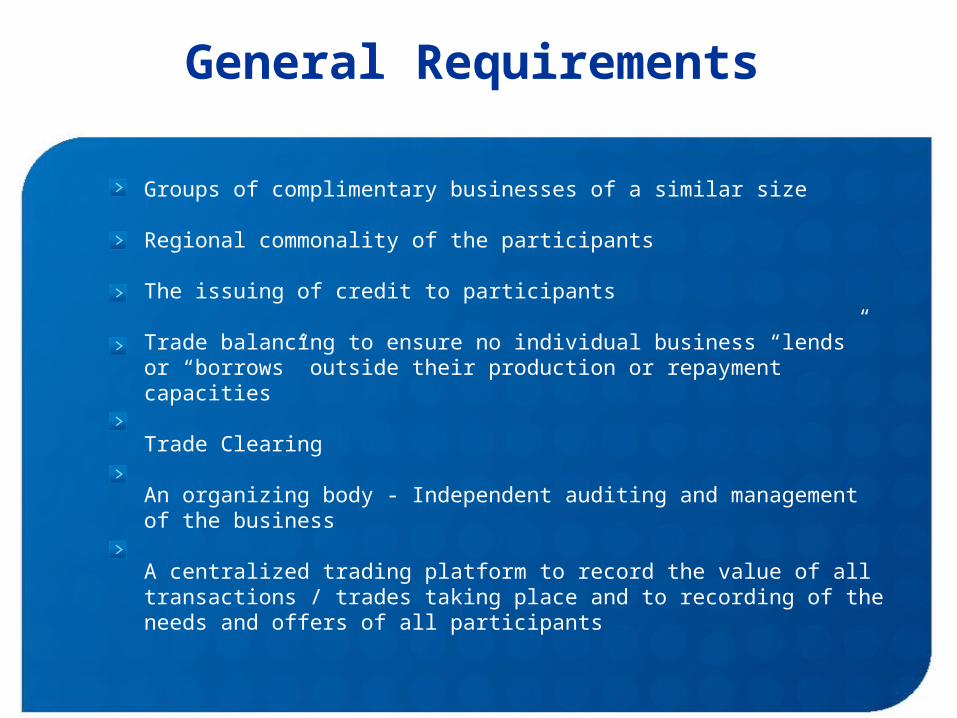

General Requirements

Groups of complimentary businesses of a similar size

Regional commonality of the participants

The issuing of credit to participants

Trade balancing to ensure no individual business “lends” or “borrows” outside their production or repayment capacities

Trade Clearing

An organizing body - Independent auditing and management of the business

A centralized trading platform to record the value of all transactions / trades taking place and to recording of the needs and offers of all participants

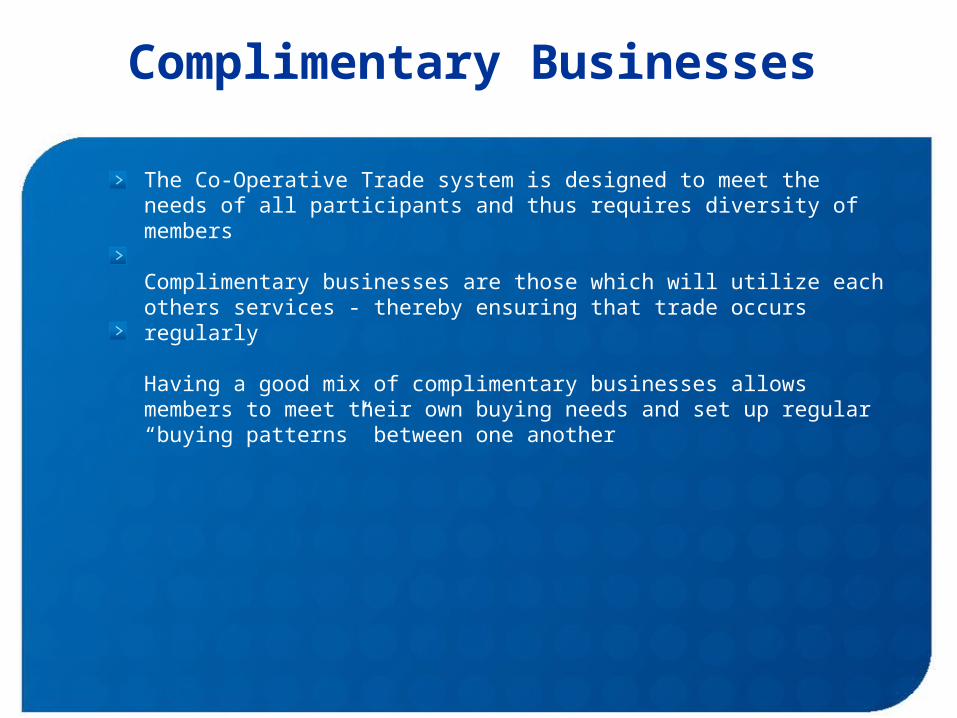

Complimentary Businesses

The Co-Operative Trade system is designed to meet the needs of all participants and thus requires diversity of members

Complimentary businesses are those which will utilize each others services - thereby ensuring that trade occurs regularly

Having a good mix of complimentary businesses allows members to meet their own buying needs and set up regular “buying patterns” between one another

Why Group Businesses Together?

In order for businesses to meet each others needs they must share common traits

Businesses are generally grouped together (recruited) by the following:

• Turn-over (revenue and profitability)

• Excess capacity / surpluses

• Cost to supply / meet additional capacity demandsi.e. Service based industries have less cash cost than those selling products

• Geographic, business associations (links) and/or ethnic ties

Why Group Businesses Together?

Businesses with 1 employee can rarely supply all of the needs of a business with 100 employees as not all of the “production & manufacturing” cost to produce the items for sale may be met within the local trade community

Small to medium-sized businesses can co-exist with one another provided balanced trade levels are achieved until the volume of membership and trade allows for majority of all “production” costs for each business to be met by the system

Businesses need to be acquired in a manner which will promote maximum trade through every phase of the businesses growth:

1. Acquire bigger businesses which all participants will utilize2. Medium-sized businesses used by most participants may be next3. Businesses used by some participants irregularly may be last

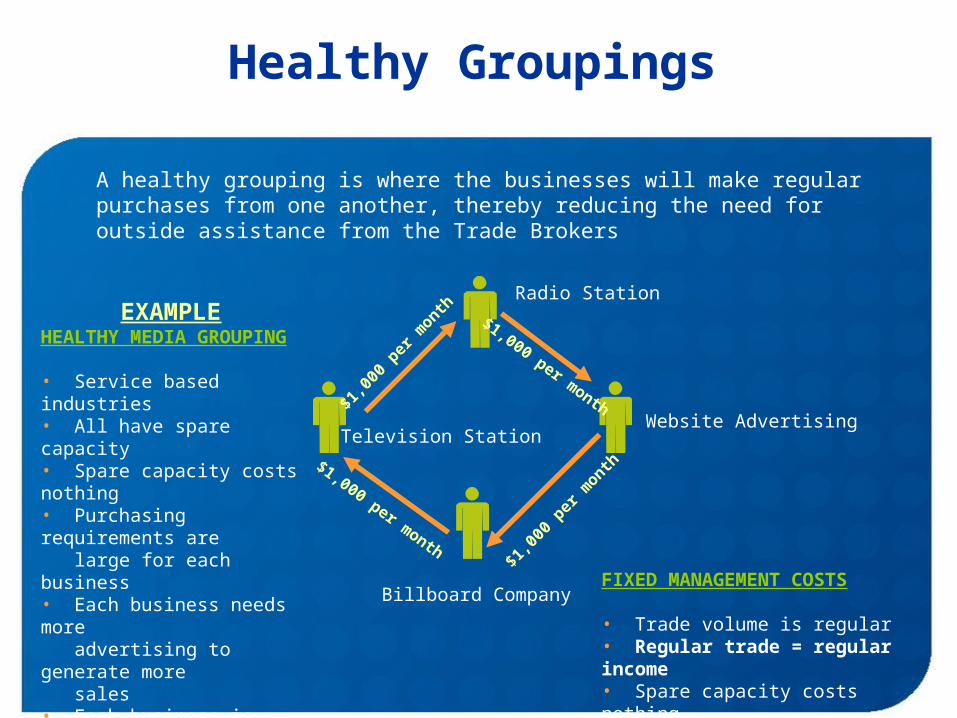

Healthy Groupings

A healthy grouping is where the businesses will make regular purchases from one another, thereby reducing the need for outside assistance from the Trade Brokers

Radio Station

Website Advertising

Billboard Company

Television Station

$1,000 per month$1,0

00 p

er m

onth

$1,0

00 p

er m

onth$1,000 per month

EXAMPLEHEALTHY MEDIA GROUPING

• Service based industries• All have spare capacity• Spare capacity costs nothing• Purchasing requirements are

large for each business• Each business needs more advertising to generate more sales• Each business is non- competing even though they are in the same industry

FIXED MANAGEMENT COSTS

• Trade volume is regular• Regular trade = regular income• Spare capacity costs nothing

Healthy Groupings

A healthy grouping has the following traits:

Members can spend all community credits that they earn

They can spend regularly

They can earn regularly

If they do not spend regularly then they can save up for something that is available through the network

A healthy network may be comprised of a range of businesses with different types of offerings

A healthy grouping may be small or large

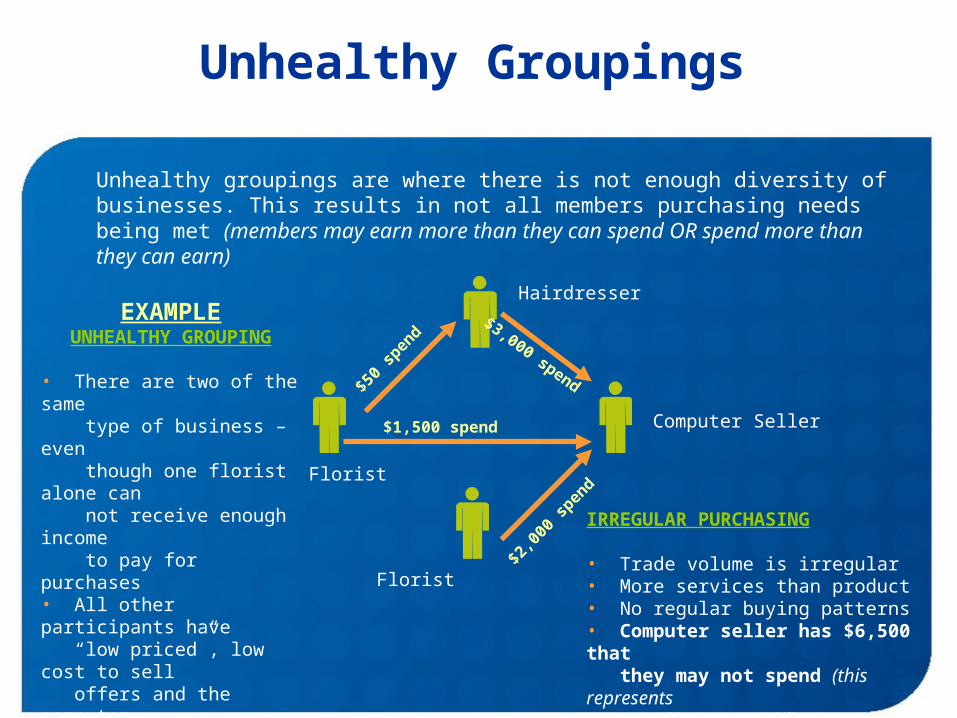

Unhealthy Groupings

Unhealthy groupings are where there is not enough diversity of businesses. This results in not all members purchasing needs being met (members may earn more than they can spend OR spend more than they can earn)

Hairdresser

Computer Seller

$3,000 spend

$2,0

00 s

pend

$1,500 spend

Florist

Florist

$50

spen

d

IRREGULAR PURCHASING

• Trade volume is irregular• More services than product• No regular buying patterns• Computer seller has $6,500 that they may not spend (this represents

A LOT of haircuts and flowers)

EXAMPLEUNHEALTHY GROUPING

• There are two of the same type of business – even though one florist alone can not receive enough income to pay for purchases• All other participants have “low priced”, low cost to sell offers and the computer seller has a high-priced, high

cost to sell, offer• There is no need to regularly

trade unless each participant

requires the services of the other often

Unhealthy Groupings

Unhealthy groupings may share some or all of the following traits:

Members may earn more than they can spend

There is too much of one type of business who needs Community Credit income but

If they do not spend regularly then they can save up for something that is available through the network

Types of Groupings

SERVICE INDUSTRIES

Low cost to make additional revenue – only cost is unsold/spare timeVery few service industries are at 100% capacityOnce a business has received enough income to cover its cash costs any revenue received through selling “unsellable” time is pure profitSome types of service industries already barter (e.g. media)Also includes capacity based businesses such as theatres, venues, airlines (may not include taxes which are levied on a per-person basis) etc

Examples include: media, accountants, lawyers, doctors etc

MAJORITY SERVICE / SMALL PRODUCT COST INDUSTRIESMixed businesses which involve a large amount of service and little product costExamples include mechanical servicing, hotels (extra room cleaning charge, mini-bar, phone calls, internet), pool cleaning, pest control, carpet cleaning, Internet access etc

Types of Groupings

PRODUCT INDUSTRIES – PRIMARY PRODUCERS

Low cost, high margin product sellersWholesalers, Manufacturers, ProducersBusinesses with surplus stock which needs to be sold outside of existing marketsLiquidators, liquidation outlets

RETAIL (RESELLER) PRODUCT PROVIDERSMedium to low profit margin on salesHigh cost to meet additional sales

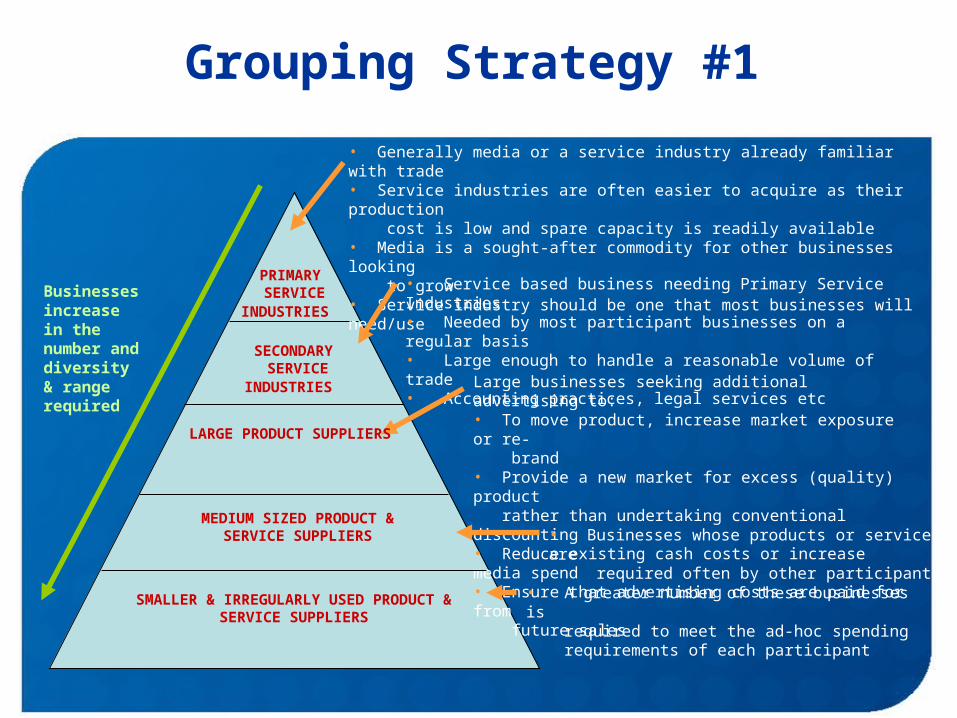

Grouping Strategy #1

• Generally media or a service industry already familiar with trade• Service industries are often easier to acquire as their production cost is low and spare capacity is readily available• Media is a sought-after commodity for other businesses looking to grow• Service industry should be one that most businesses will need/use

Large businesses seeking additional advertising to: • To move product, increase market exposure or re- brand• Provide a new market for excess (quality) product rather than undertaking conventional discounting• Reduce existing cash costs or increase media spend• Ensure that advertising costs are paid for from future sales

• Service based business needing Primary Service Industries• Needed by most participant businesses on a regular basis• Large enough to handle a reasonable volume of trade• Accounting practices, legal services etc

PRIMARY SERVICE

INDUSTRIES

SECONDARY SERVICE

INDUSTRIES

LARGE PRODUCT SUPPLIERS

MEDIUM SIZED PRODUCT & SERVICE

SUPPLIERS• Businesses whose products or services are required often by other participants

SMALLER & IRREGULARLY USED PRODUCT & SERVICE SUPPLIERS

• A greater number of these businesses is required to meet the ad-hoc spending requirements of each participant

Businesses increase in the number and diversity & range required

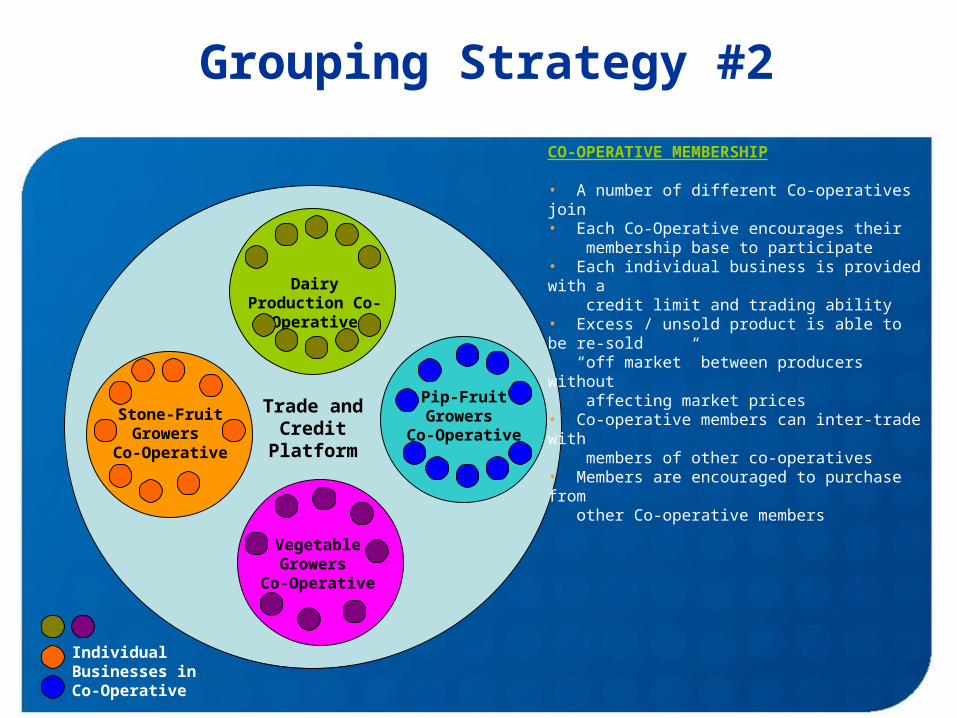

Grouping Strategy #2

Dairy Production Co-

Operative

Pip-Fruit Growers

Co-OperativeStone-Fruit Growers

Co-Operative

Vegetable Growers

Co-Operative

CO-OPERATIVE MEMBERSHIP

• A number of different Co-operatives join• Each Co-Operative encourages their membership base to participate• Each individual business is provided with a credit limit and trading ability• Excess / unsold product is able to be re-sold “off market” between producers without affecting market prices• Co-operative members can inter-trade with members of other co-operatives• Members are encouraged to purchase from other Co-operative members

Individual Businesses in Co-Operative

Trade and Credit

Platform

Why Issue Credit?

Community Credit provides an alternative means by which participants can make sales and purchases that is:

A merchandise / asset backed trading mechanismSecure, with trades formally recordedInterest-freeLocally created and controlledAvailable in sufficient supplyDoes not depend on Banks, the Reserve Bank or the Government

The issuing of credit:

Enables businesses the means to conduct purchases and sales even if cash is unavailable

Enables the sale of future and/or excess production capacity

Enables local businesses and entrepreneurs to employ or utilize more of the locally available labor, skills, and resources and pay for these with their own assets / output

Why Issue Credit?

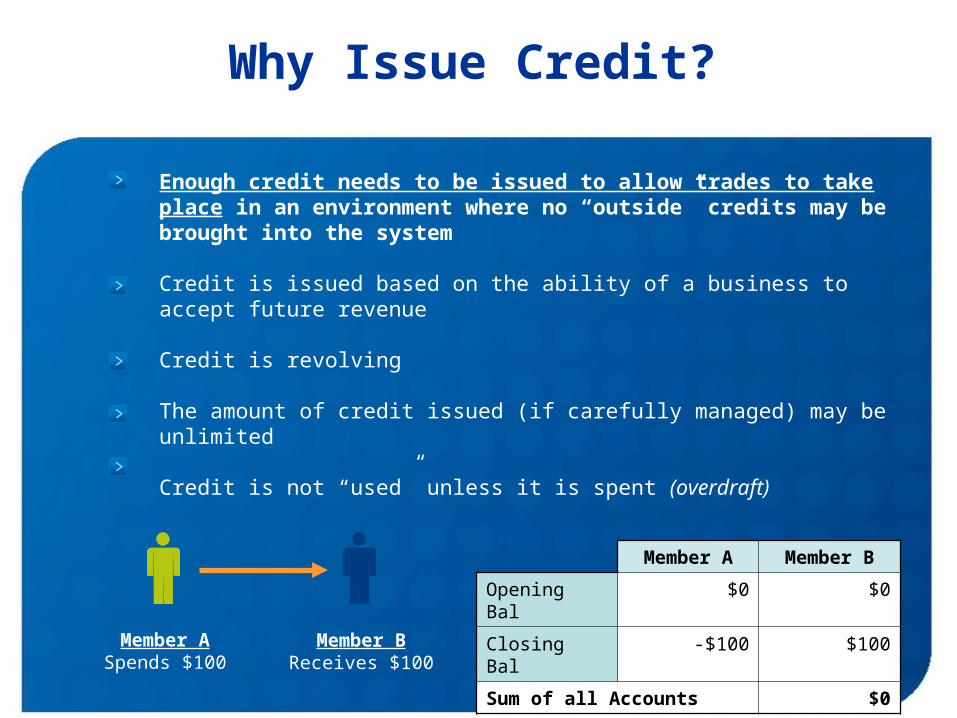

Enough credit needs to be issued to allow trades to take place in an environment where no “outside” credits may be brought into the system

Credit is issued based on the ability of a business to accept future revenue

Credit is revolving

The amount of credit issued (if carefully managed) may be unlimited

Credit is not “used” unless it is spent (overdraft)

Member ASpends $100

Member BReceives $100

Member A Member B

Opening Bal $0 $0

Closing Bal -$100 $100

Sum of all Accounts $0

Balancing Accounts

Ensure that participants can spend any credits received

Promote the participants who are in debt to the participants who are in credit

Issue credit based on a participants ability to accept trade from other members (e.g. a florist may be able to spend $100,000 per year however the demand for the florist may only be $10,000 per year)

Ensure that the amount of credit issued to a participant can be repaid within a reasonable time-frame

Help participants establish regular trading patterns

Different credit limits will be issued to different participants

Ensure that defaults are repaid through either a debt reserve fund or the introduction of additional commodities which are sold for trade and applied against any default account debt balances

How Does Clearing Work?

Trade Credits accounts are provided to all participants as an intermediary device to enable transactions to take place

When you sell something, your trade credit balance is credited (increased)

When you buy something, your trade credit balance is debited (decreased)

Trade Credit account balances and transactional records are maintained by the system

The system is fully balanced and assets may not leave the community – if one member is in debit (negative) there is always one or more members whose accounts are in credit (positive) to the same amount

Ultimately, goods and services pay for other goods and services

Advantages Closed Circulation

Currency credits can only be redeemed within the trading platform for products and services

For this reason they are captured within the local economy and will not stray very far

Their re-circulation within the community provides a built-in “buy local” bias, which stimulates entire clusters of local economies affecting the National economy positively

They give multiple local sources of supply preference over non local (external) sources

The Organizing Body

Overview

The Organizing Body must meet the following requirements:

Charge sufficient fees/charges to cover the costs of operation and make the project self sustaining

Some fees will necessarily be cash fees needed to cover unavoidable cash expenses

Compliance with local laws and taxation requirements

Administrative and personnel (facilitators or brokers) should be paid, but a portion of their income may be paid via the Community Credit system

All salaries and related taxes where applicable should be paid out of revenues generated from service fees

There should be no system account deficits

There should be provision for covering socioeconomic needs during downturns and unforeseen circumstances

Structure

The Organizing Body is comprised of:

Senior Management

Trade Floor Managers / Trade Brokers

Accounting / Credit / Ledger Support

Marketing Support for Participants

The majority of responsibility for assisting the trades and ensuring the liquidity of the system lies with the trade floor managers

Trade Floor Managers

Trade Floor Managers handle the day-to-day trading activities of the system including:

Conducting personalized matching services between participants based on their needs and offers

Actively seeking out new businesses to provide goods or services required by the existing participants

Print a membership directory of all members along with details of their products or services

Produce regular newsletters promoting specific members who have spare capacity, are in Community Credit dollar debt, or who wish to acquire new customers

Conduct networking events for member businesses

Trade Floor Managers

Being responsible for credit control within the exchange and ensuring sound fiscal policy and ensuring liquidity of the barter dollar (monetary flow between members, ensuring that no member is in credit or debt for any great period of time)

Ensuring that any unrecoverable deficit balances are accounted for and balanced out with new barter dollars brought into the system (usually through the exchange purchasing another members barter dollars for cash, or through the retailing of cash-purchased goods or services by the exchange to its members for barter dollars) and/or an increased speed of barter dollar flow between members

The Trade Platform

Overview

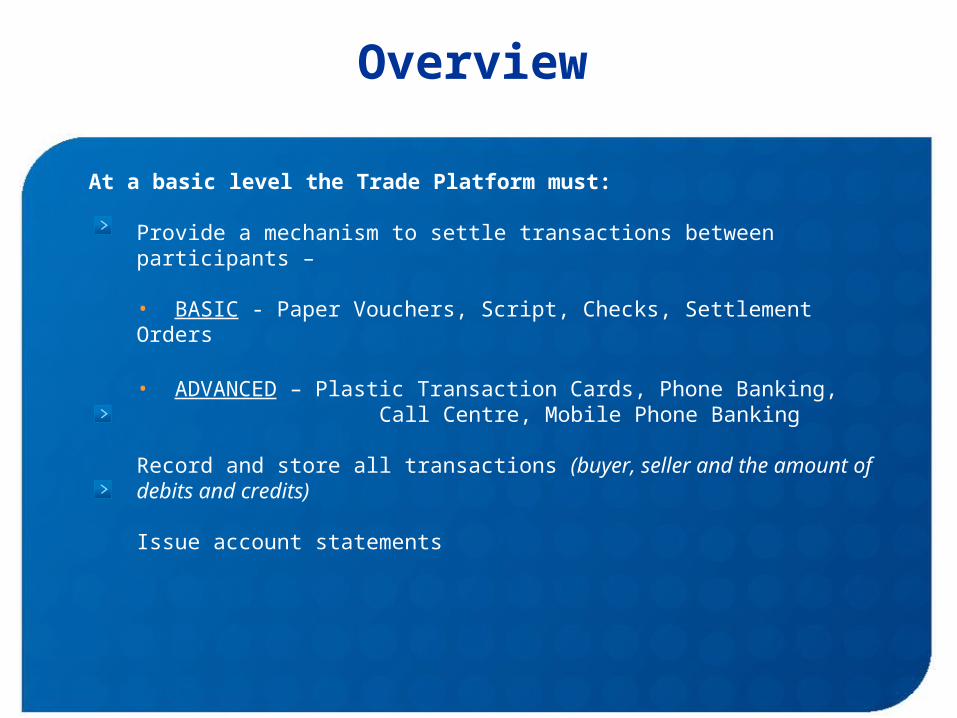

At a basic level the Trade Platform must:

Provide a mechanism to settle transactions between participants –

• BASIC - Paper Vouchers, Script, Checks, Settlement Orders

• ADVANCED – Plastic Transaction Cards, Phone Banking, Call Centre, Mobile Phone Banking

Record and store all transactions (buyer, seller and the amount of debits and credits)

Issue account statements

Overview

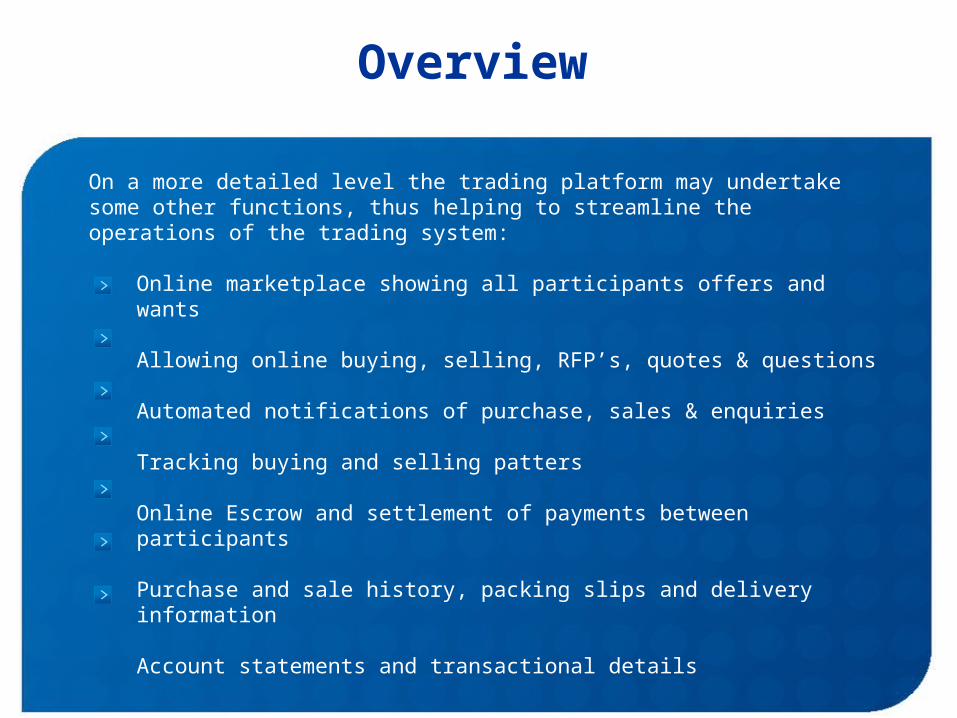

On a more detailed level the trading platform may undertake some other functions, thus helping to streamline the operations of the trading system:

Online marketplace showing all participants offers and wants

Allowing online buying, selling, RFP’s, quotes & questions

Automated notifications of purchase, sales & enquiries

Tracking buying and selling patters

Online Escrow and settlement of payments between participants

Purchase and sale history, packing slips and delivery information

Account statements and transactional details

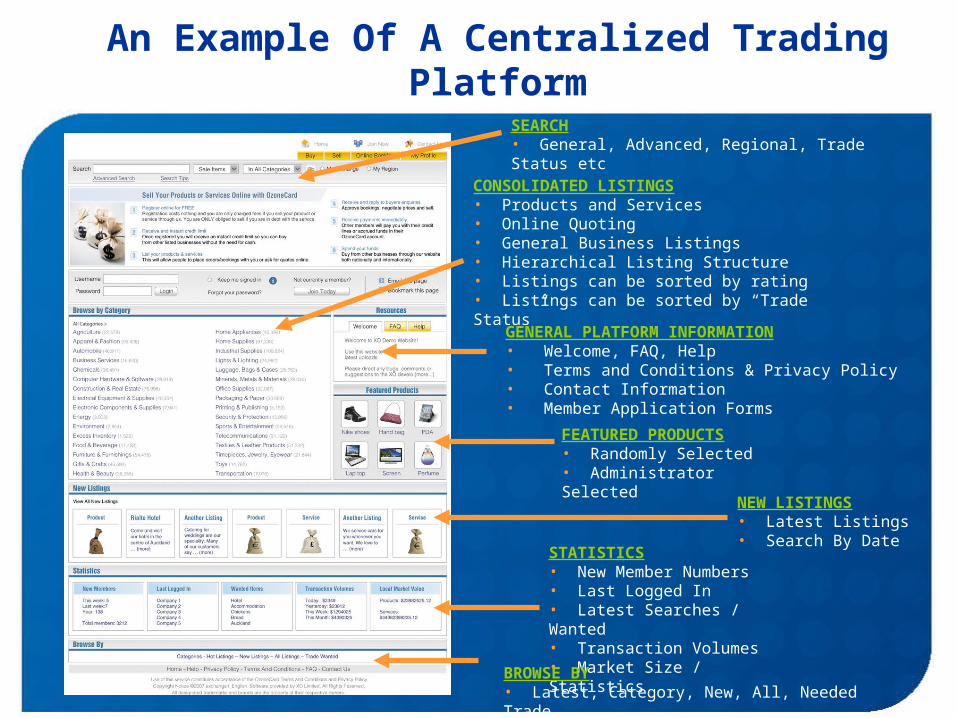

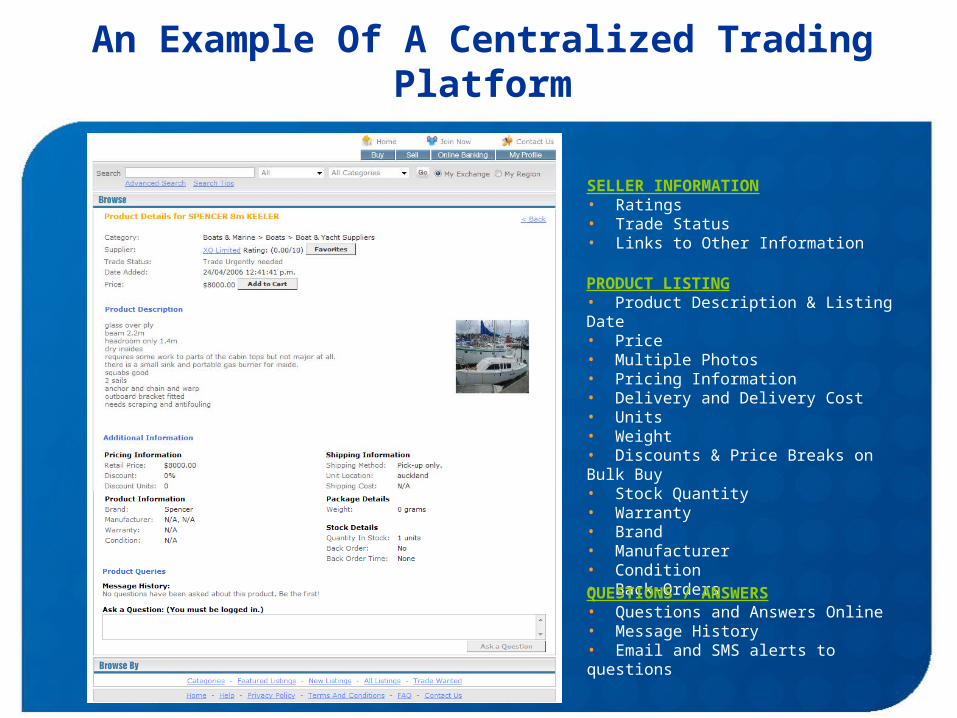

An Example Of A Centralized Trading Platform

STATISTICS• New Member Numbers• Last Logged In• Latest Searches / Wanted• Transaction Volumes• Market Size / Statistics

NEW LISTINGS• Latest Listings• Search By Date

BROWSE BY• Latest, Category, New, All, Needed Trade

CONSOLIDATED LISTINGS• Products and Services• Online Quoting• General Business Listings• Hierarchical Listing Structure• Listings can be sorted by rating• Listings can be sorted by “Trade Status”

FEATURED PRODUCTS• Randomly Selected• Administrator Selected

GENERAL PLATFORM INFORMATION• Welcome, FAQ, Help• Terms and Conditions & Privacy Policy• Contact Information• Member Application Forms

SEARCH• General, Advanced, Regional, Trade Status etc

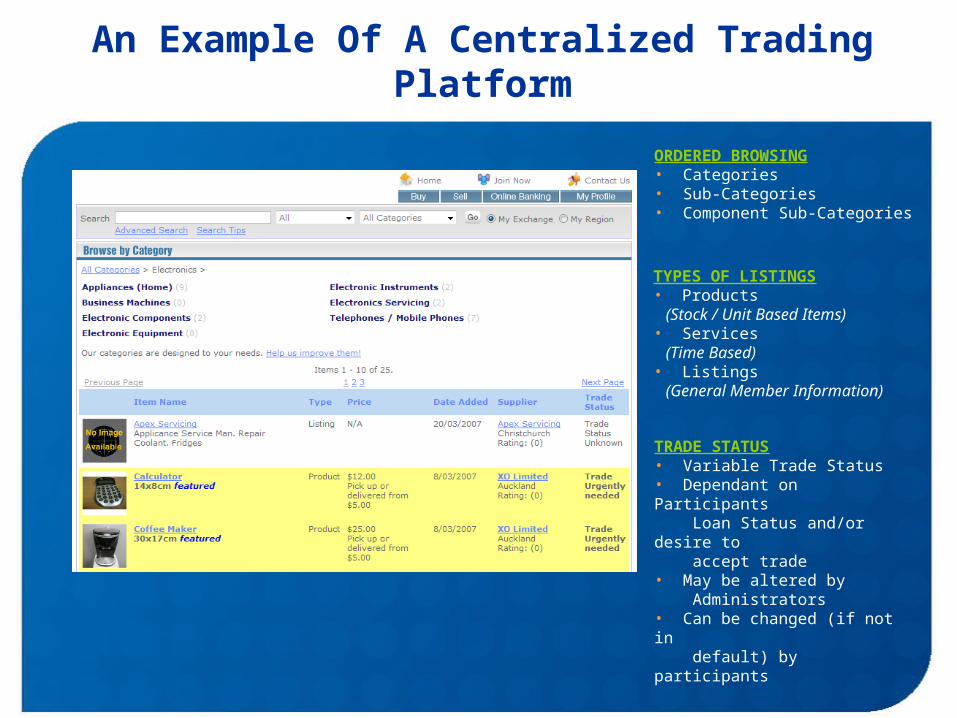

An Example Of A Centralized Trading Platform

TYPES OF LISTINGS• Products (Stock / Unit Based Items)• Services (Time Based)• Listings (General Member Information)

TRADE STATUS• Variable Trade Status• Dependant on Participants Loan Status and/or desire to accept trade• May be altered by Administrators• Can be changed (if not in default) by participants

ORDERED BROWSING• Categories• Sub-Categories• Component Sub-Categories

An Example Of A Centralized Trading Platform

PRODUCT LISTING• Product Description & Listing Date• Price • Multiple Photos• Pricing Information• Delivery and Delivery Cost• Units• Weight• Discounts & Price Breaks on Bulk Buy• Stock Quantity• Warranty• Brand• Manufacturer• Condition• Back-Orders

QUESTIONS / ANSWERS• Questions and Answers Online• Message History• Email and SMS alerts to questions

SELLER INFORMATION• Ratings• Trade Status• Links to Other Information

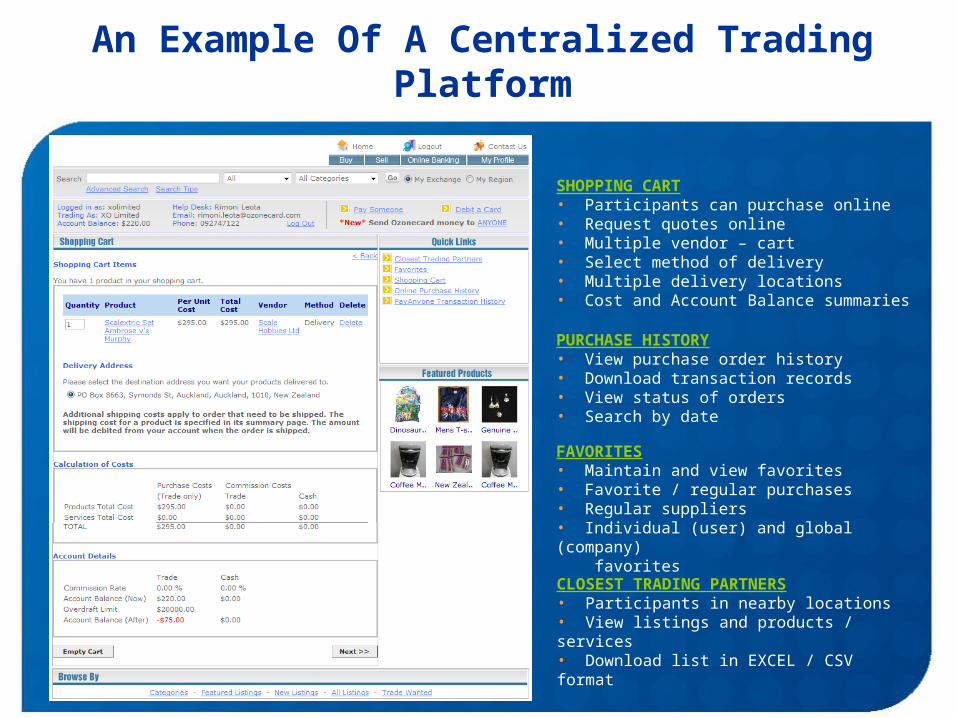

An Example Of A Centralized Trading Platform

SHOPPING CART• Participants can purchase online• Request quotes online• Multiple vendor – cart• Select method of delivery• Multiple delivery locations• Cost and Account Balance summaries

PURCHASE HISTORY• View purchase order history• Download transaction records• View status of orders• Search by date

FAVORITES• Maintain and view favorites• Favorite / regular purchases• Regular suppliers• Individual (user) and global (company) favorites

CLOSEST TRADING PARTNERS• Participants in nearby locations• View listings and products / services• Download list in EXCEL / CSV format

An Example Of A Centralized Trading Platform

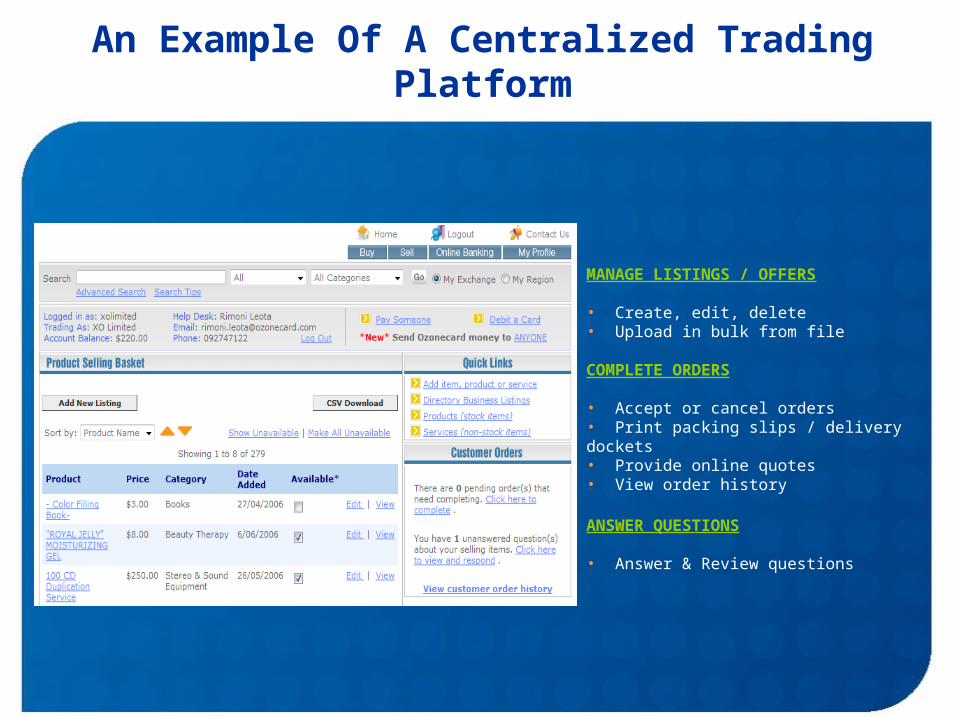

MANAGE LISTINGS / OFFERS

• Create, edit, delete• Upload in bulk from file

COMPLETE ORDERS

• Accept or cancel orders• Print packing slips / delivery dockets• Provide online quotes• View order history

ANSWER QUESTIONS

• Answer & Review questions

An Example Of A Centralized Trading Platform

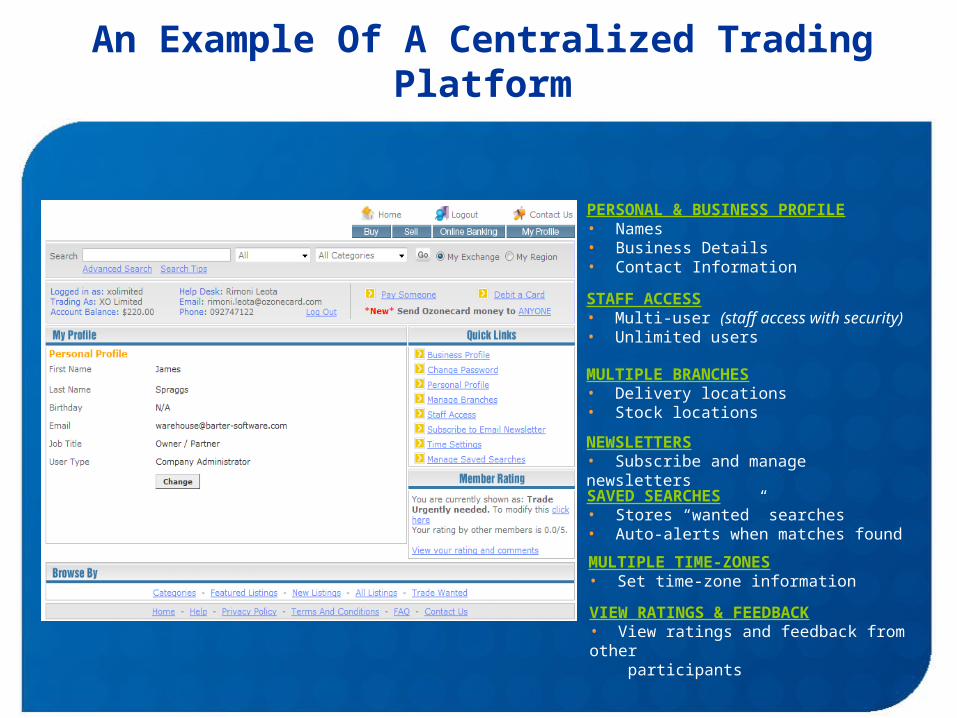

STAFF ACCESS• Multi-user (staff access with security)• Unlimited users

SAVED SEARCHES• Stores “wanted” searches• Auto-alerts when matches found

PERSONAL & BUSINESS PROFILE• Names• Business Details• Contact Information

MULTIPLE BRANCHES• Delivery locations• Stock locations

NEWSLETTERS• Subscribe and manage newsletters

MULTIPLE TIME-ZONES• Set time-zone information

VIEW RATINGS & FEEDBACK• View ratings and feedback from other participants

An Example Of A Centralized Trading Platform

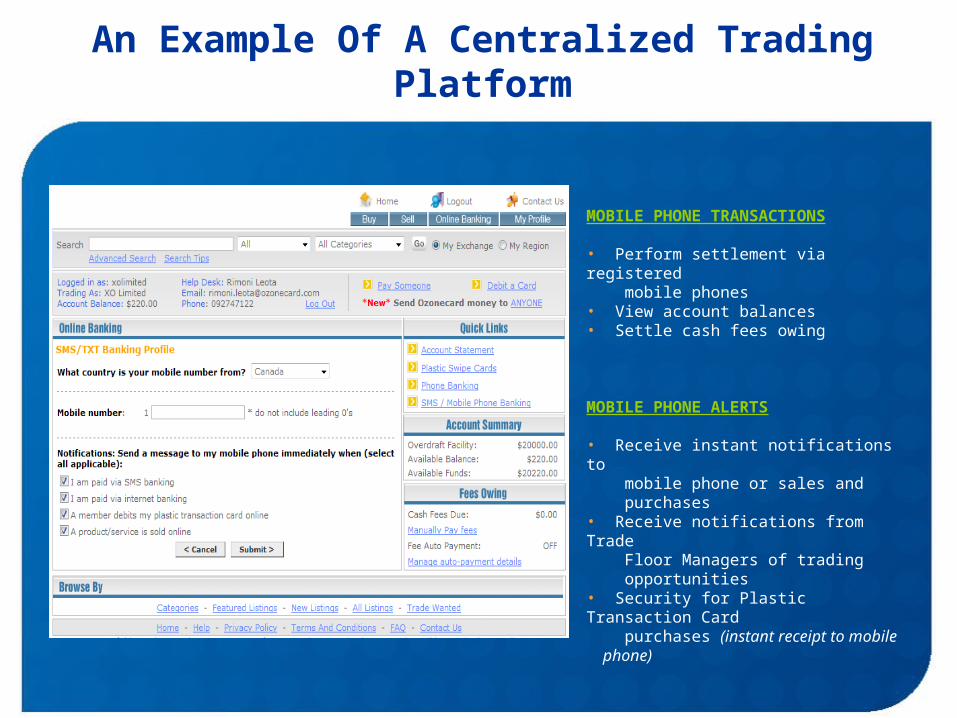

MOBILE PHONE TRANSACTIONS

• Perform settlement via registered mobile phones• View account balances• Settle cash fees owing

MOBILE PHONE ALERTS

• Receive instant notifications to mobile phone or sales and purchases• Receive notifications from Trade Floor Managers of trading opportunities• Security for Plastic Transaction Card purchases (instant receipt to mobile phone)

An Example Of A Centralized Trading Platform

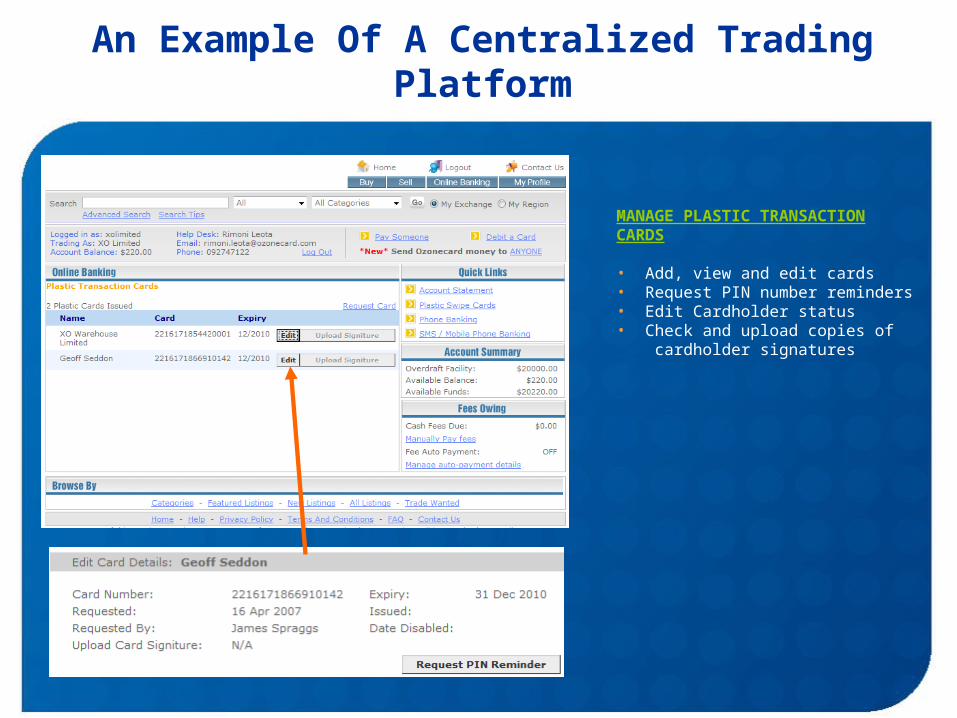

MANAGE PLASTIC TRANSACTION CARDS

• Add, view and edit cards• Request PIN number reminders• Edit Cardholder status• Check and upload copies of cardholder signatures

An Example Of A Centralized Trading Platform

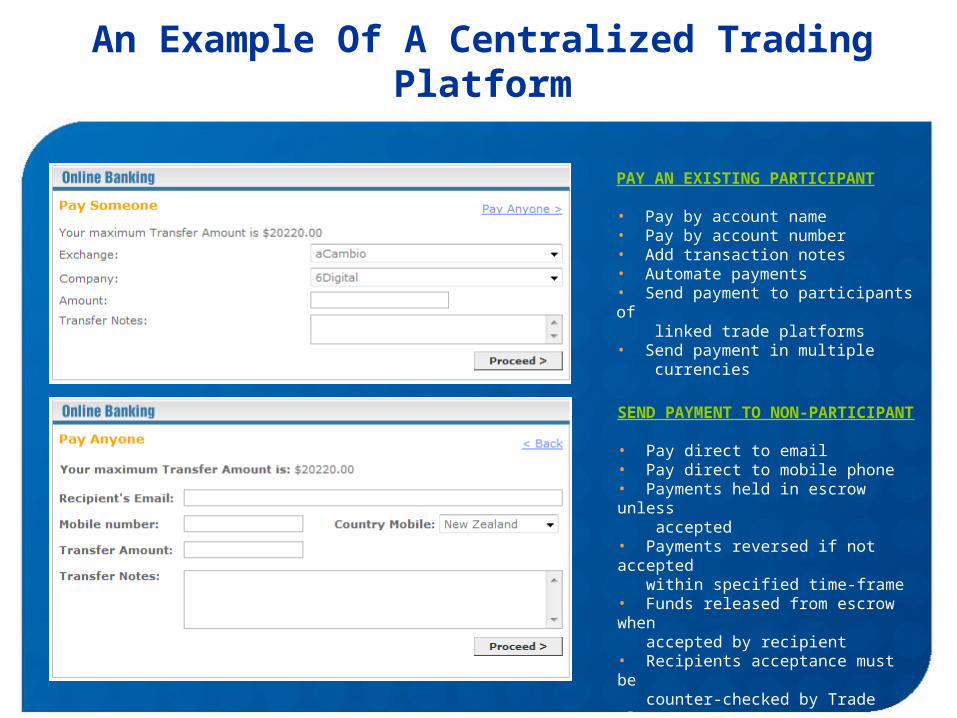

PAY AN EXISTING PARTICIPANT

• Pay by account name• Pay by account number• Add transaction notes• Automate payments• Send payment to participants of linked trade platforms• Send payment in multiple currencies

SEND PAYMENT TO NON-PARTICIPANT

• Pay direct to email• Pay direct to mobile phone• Payments held in escrow unless accepted• Payments reversed if not accepted

within specified time-frame• Funds released from escrow when accepted by recipient• Recipients acceptance must be counter-checked by Trade Floor Managers and released

An Example Of A Centralized Trading Platform

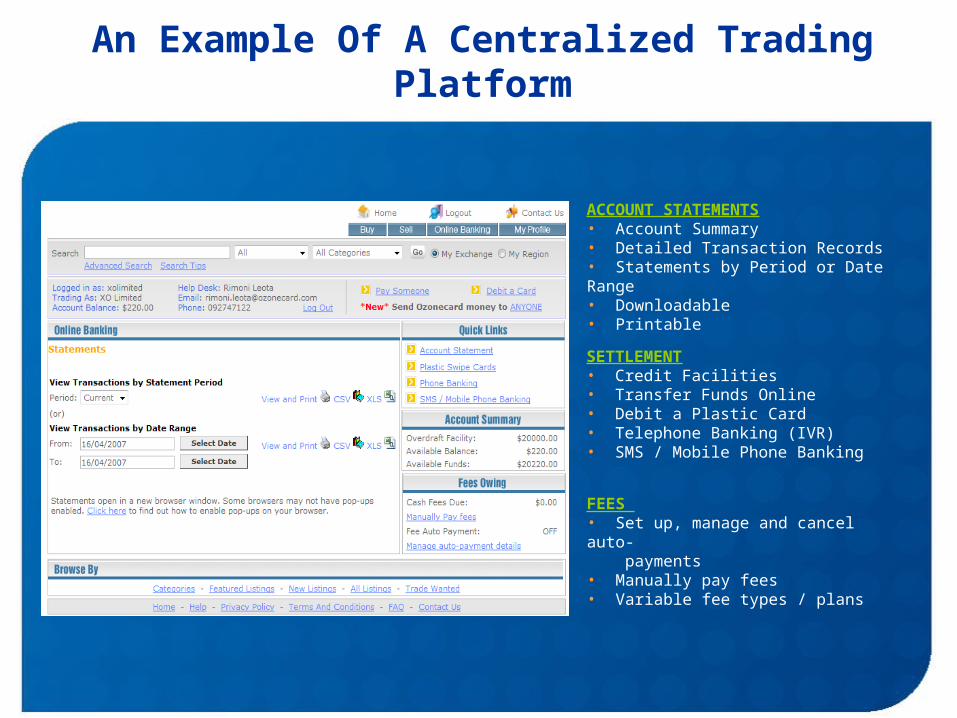

SETTLEMENT• Credit Facilities• Transfer Funds Online• Debit a Plastic Card• Telephone Banking (IVR) • SMS / Mobile Phone Banking

FEES • Set up, manage and cancel auto- payments• Manually pay fees• Variable fee types / plans

ACCOUNT STATEMENTS• Account Summary• Detailed Transaction Records• Statements by Period or Date Range• Downloadable • Printable

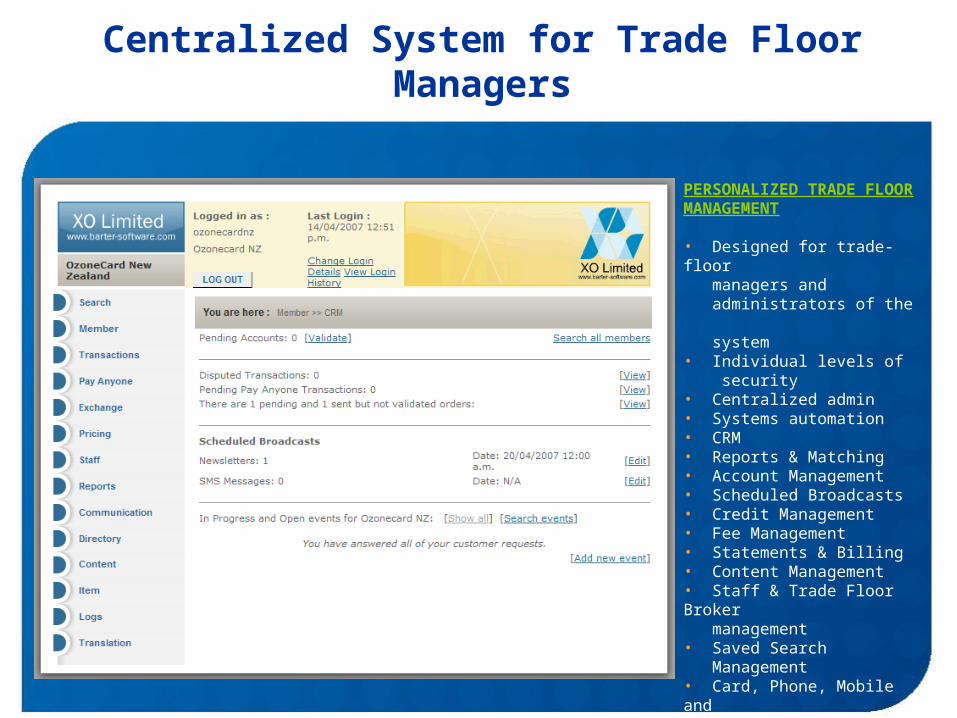

Centralized System for Trade Floor Managers

PERSONALIZED TRADE FLOOR MANAGEMENT

• Designed for trade-floor managers and administrators of the system• Individual levels of security• Centralized admin• Systems automation• CRM• Reports & Matching• Account Management• Scheduled Broadcasts• Credit Management• Fee Management• Statements & Billing• Content Management• Staff & Trade Floor Broker management• Saved Search Management• Card, Phone, Mobile and Internet Banking Systems functionality

Benefits for Borrowers

Overview

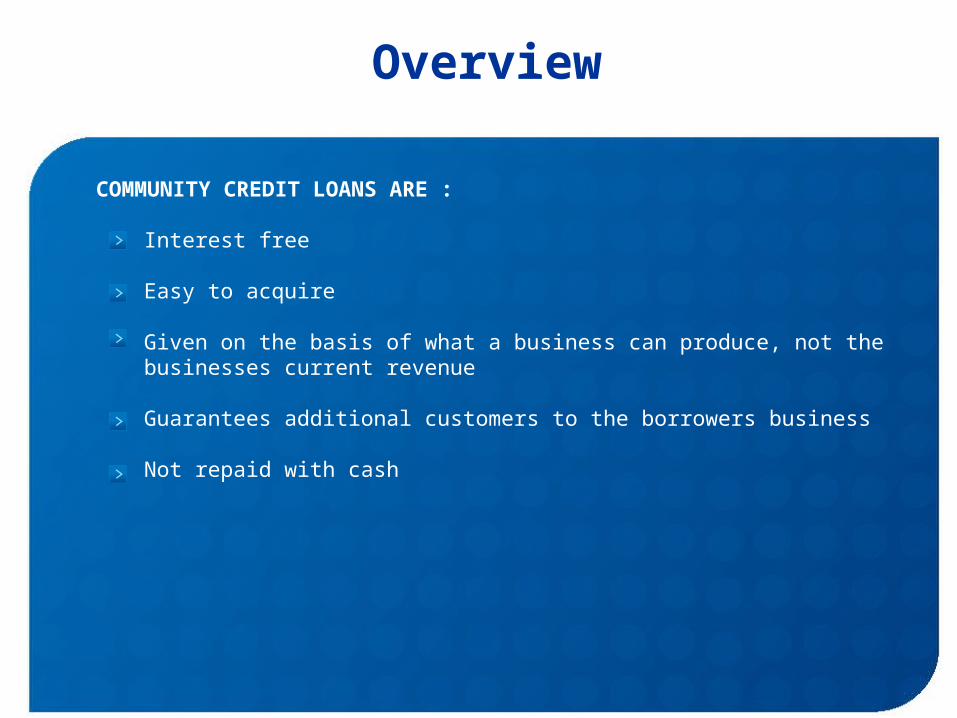

COMMUNITY CREDIT LOANS ARE :

Interest free

Easy to acquire

Given on the basis of what a business can produce, not the businesses current revenue

Guarantees additional customers to the borrowers business

Not repaid with cash

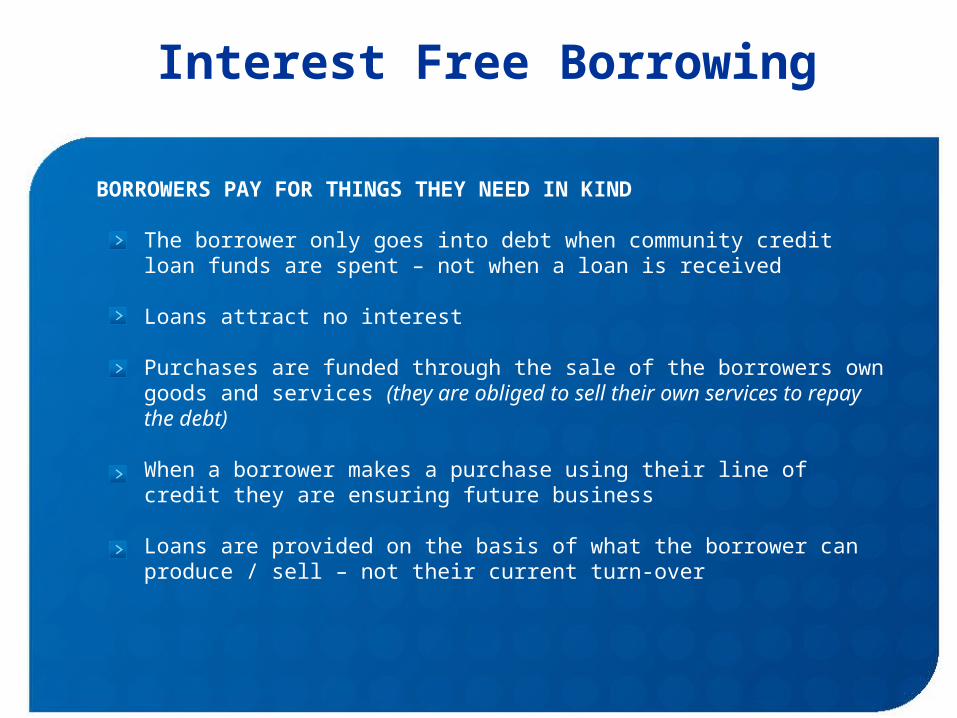

Interest Free Borrowing

BORROWERS PAY FOR THINGS THEY NEED IN KIND

The borrower only goes into debt when community credit loan funds are spent – not when a loan is received

Loans attract no interest

Purchases are funded through the sale of the borrowers own goods and services (they are obliged to sell their own services to repay the debt)

When a borrower makes a purchase using their line of credit they are ensuring future business

Loans are provided on the basis of what the borrower can produce / sell – not their current turn-over

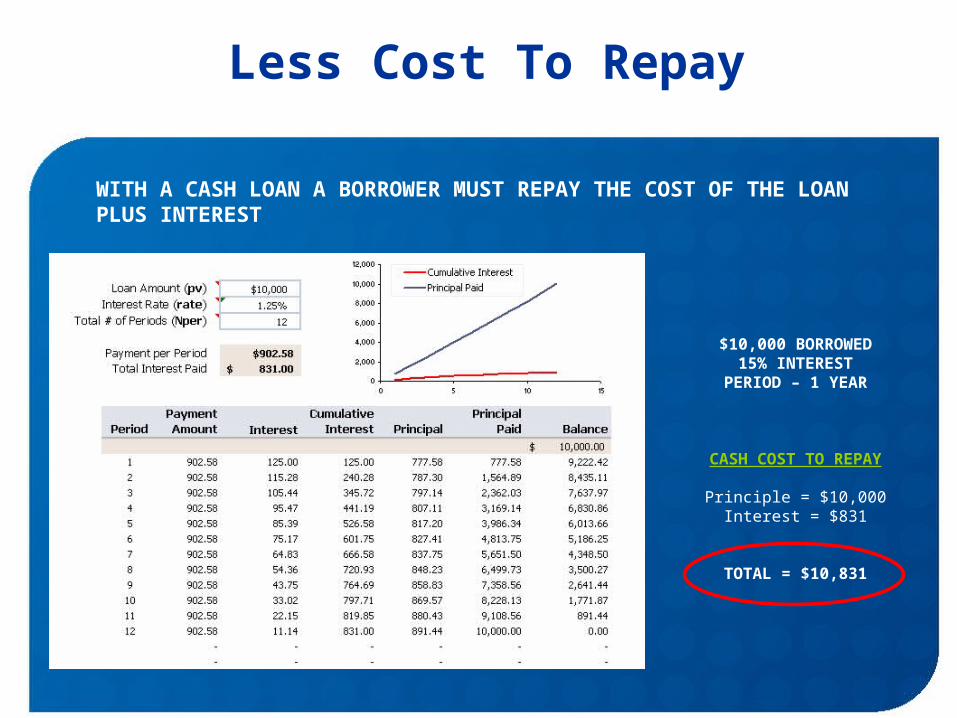

Less Cost To Repay

WITH A CASH LOAN A BORROWER MUST REPAY THE COST OF THE LOAN PLUS INTEREST

$10,000 BORROWED15% INTEREST

PERIOD – 1 YEAR

CASH COST TO REPAY

Principle = $10,000Interest = $831

TOTAL = $10,831

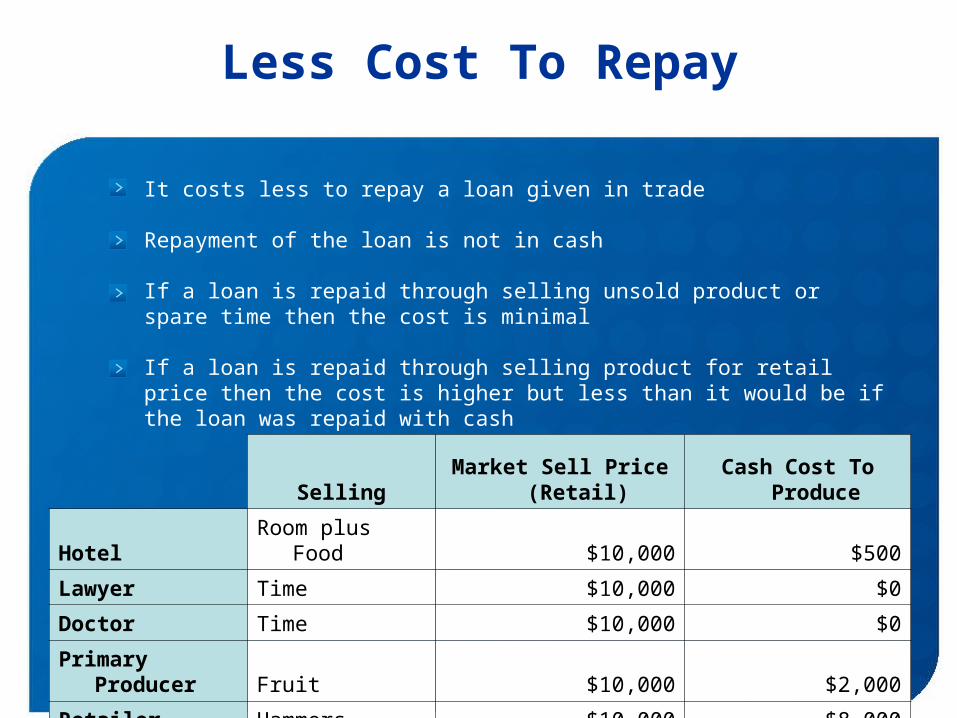

Less Cost To Repay

It costs less to repay a loan given in trade

Repayment of the loan is not in cash

If a loan is repaid through selling unsold product or spare time then the cost is minimal

If a loan is repaid through selling product for retail price then the cost is higher but less than it would be if the loan was repaid with cash

SellingMarket Sell Price

(Retail)Cash Cost To

Produce

Hotel Room plus Food $10,000 $500

Lawyer Time $10,000 $0

Doctor Time $10,000 $0

Primary Producer Fruit $10,000 $2,000

Retailer Hammers $10,000 $8,000

Less Cost To Repay

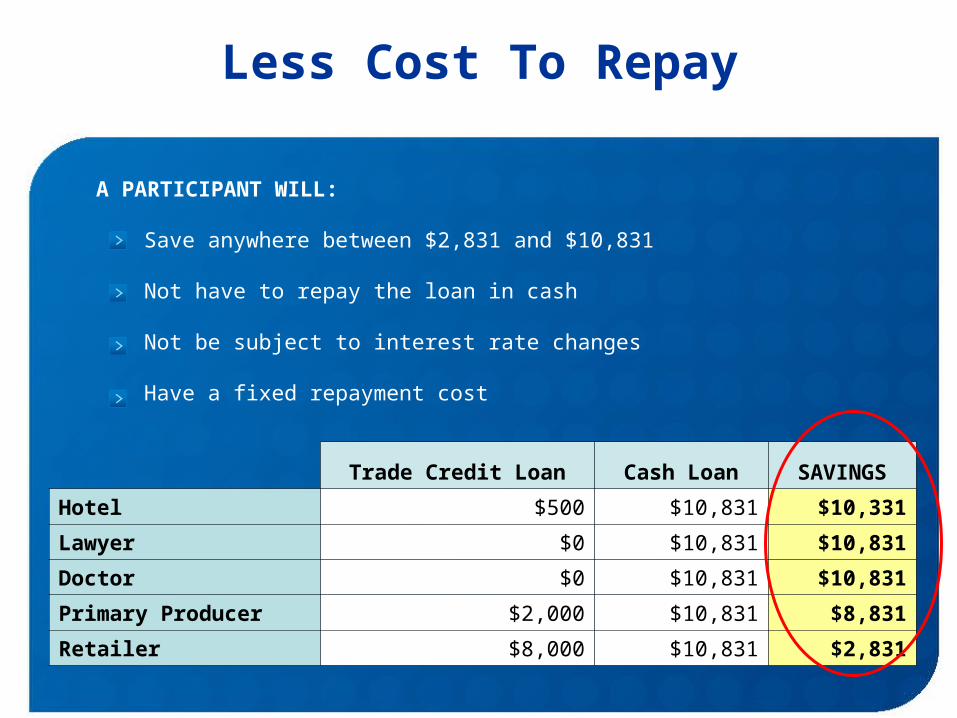

A PARTICIPANT WILL:

Save anywhere between $2,831 and $10,831

Not have to repay the loan in cash

Not be subject to interest rate changes

Have a fixed repayment cost

Trade Credit Loan Cash Loan SAVINGS

Hotel $500 $10,831 $10,331

Lawyer $0 $10,831 $10,831

Doctor $0 $10,831 $10,831

Primary Producer $2,000 $10,831 $8,831

Retailer $8,000 $10,831 $2,831

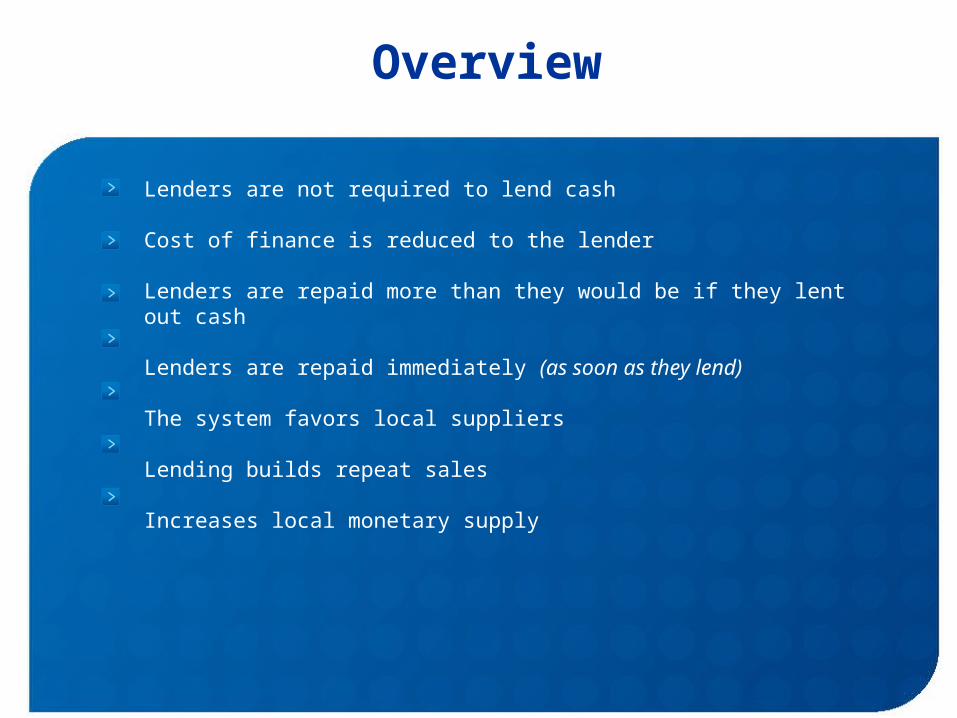

Benefits for Lenders

Overview

Lenders are not required to lend cash

Cost of finance is reduced to the lender

Lenders are repaid more than they would be if they lent out cash

Lenders are repaid immediately (as soon as they lend)

The system favors local suppliers

Lending builds repeat sales

Increases local monetary supply

No Cash Lending

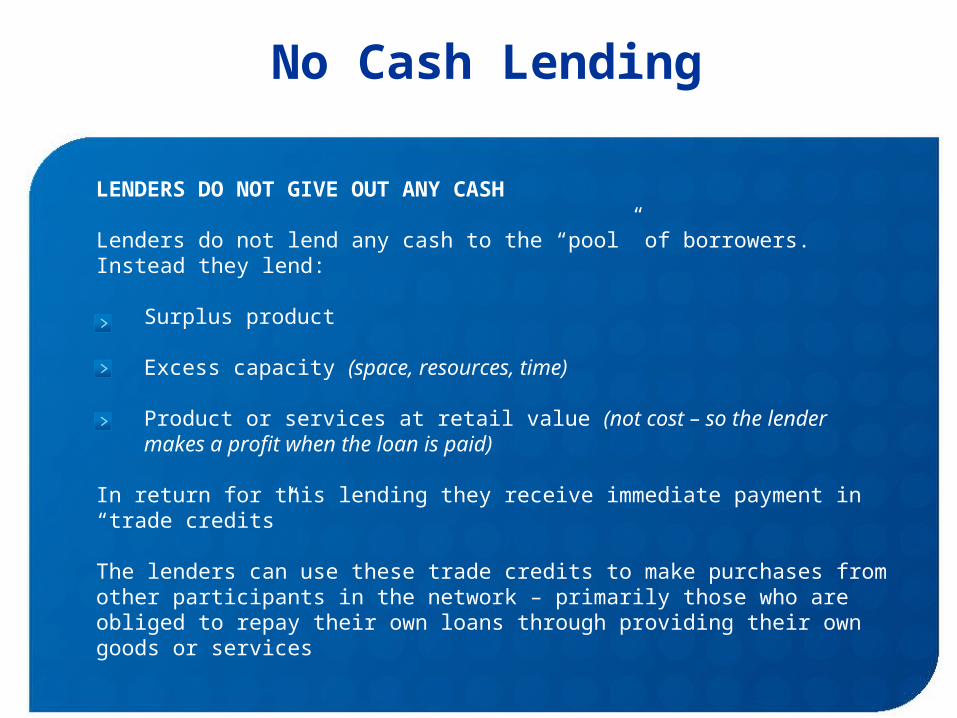

LENDERS DO NOT GIVE OUT ANY CASH

Lenders do not lend any cash to the “pool” of borrowers. Instead they lend:

Surplus product

Excess capacity (space, resources, time)

Product or services at retail value (not cost – so the lender makes a profit when the loan is paid)

In return for this lending they receive immediate payment in “trade credits”

The lenders can use these trade credits to make purchases from other participants in the network – primarily those who are obliged to repay their own loans through providing their own goods or services

Reducing the Cost of Finance

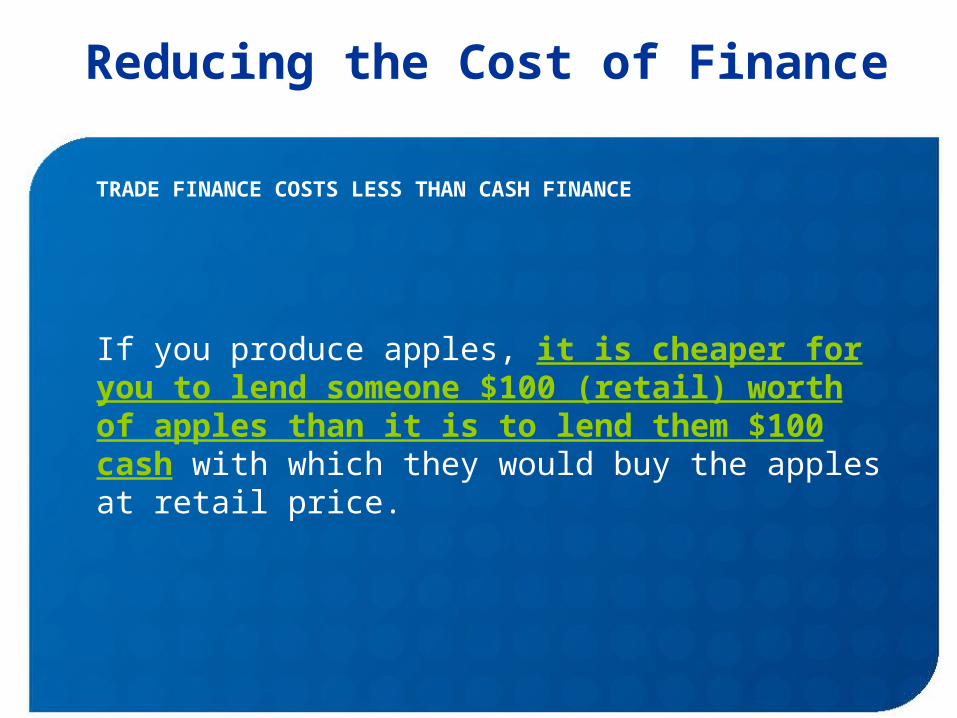

TRADE FINANCE COSTS LESS THAN CASH FINANCE

If you produce apples, it is cheaper for you to lend someone $100 (retail) worth of apples than it is to lend them $100 cash with which they would buy the apples at retail price.

Reducing the Cost of Finance

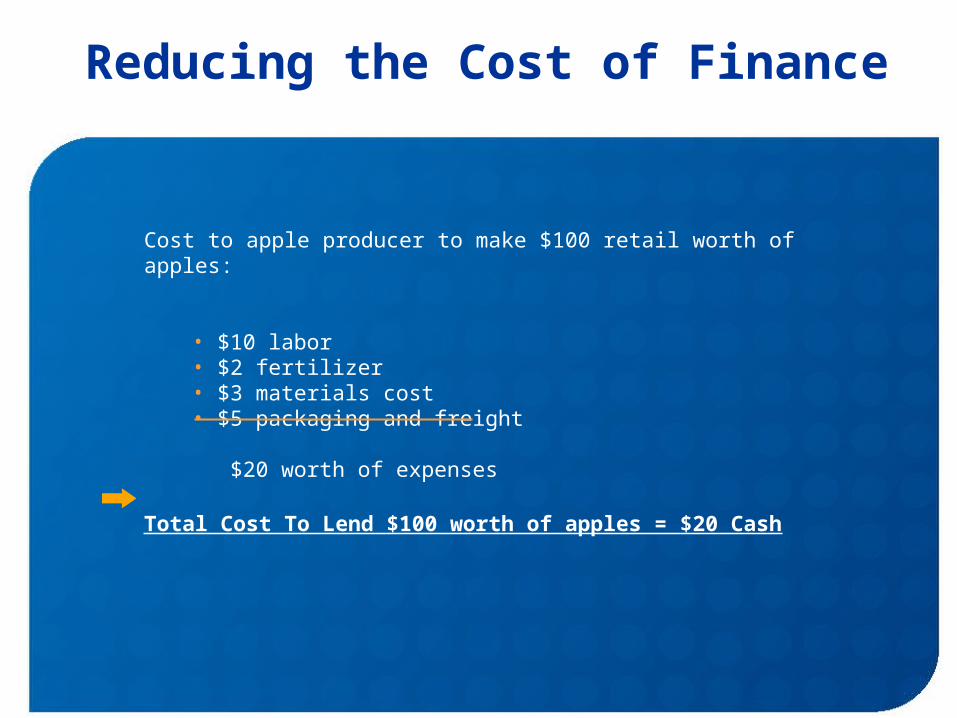

Cost to apple producer to make $100 retail worth of apples:

• $10 labor• $2 fertilizer• $3 materials cost• $5 packaging and freight

$20 worth of expenses

Total Cost To Lend $100 worth of apples = $20 Cash

Reducing the Cost of Finance

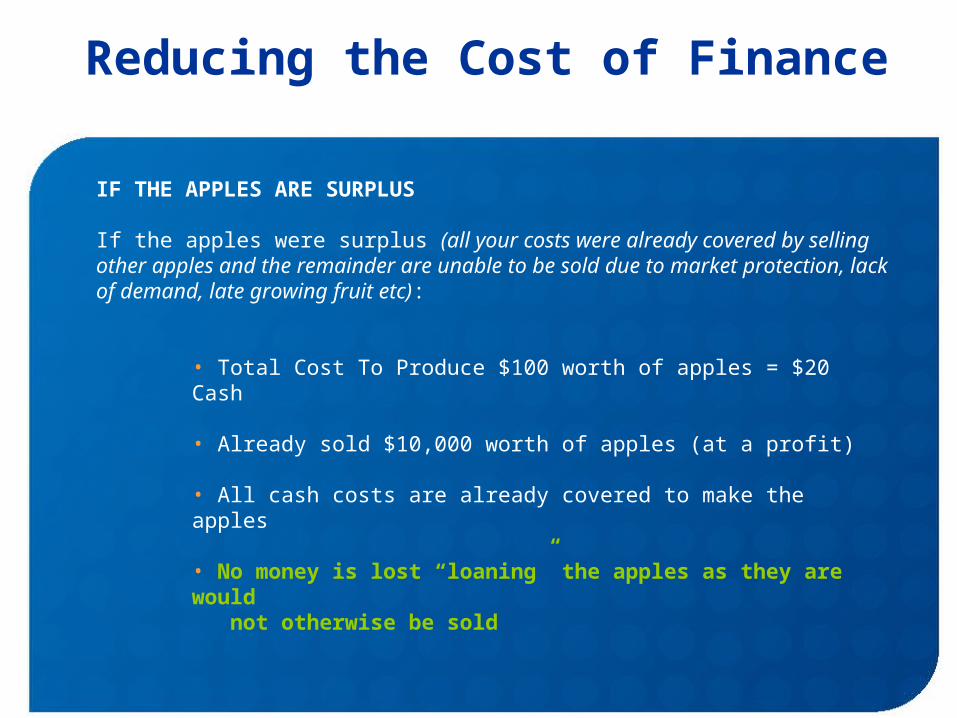

IF THE APPLES ARE SURPLUS

If the apples were surplus (all your costs were already covered by selling other apples and the remainder are unable to be sold due to market protection, lack of demand, late growing fruit etc):

• Total Cost To Produce $100 worth of apples = $20 Cash

• Already sold $10,000 worth of apples (at a profit)

• All cash costs are already covered to make the apples

• No money is lost “loaning” the apples as they are would

not otherwise be sold

Reducing the Cost of Finance

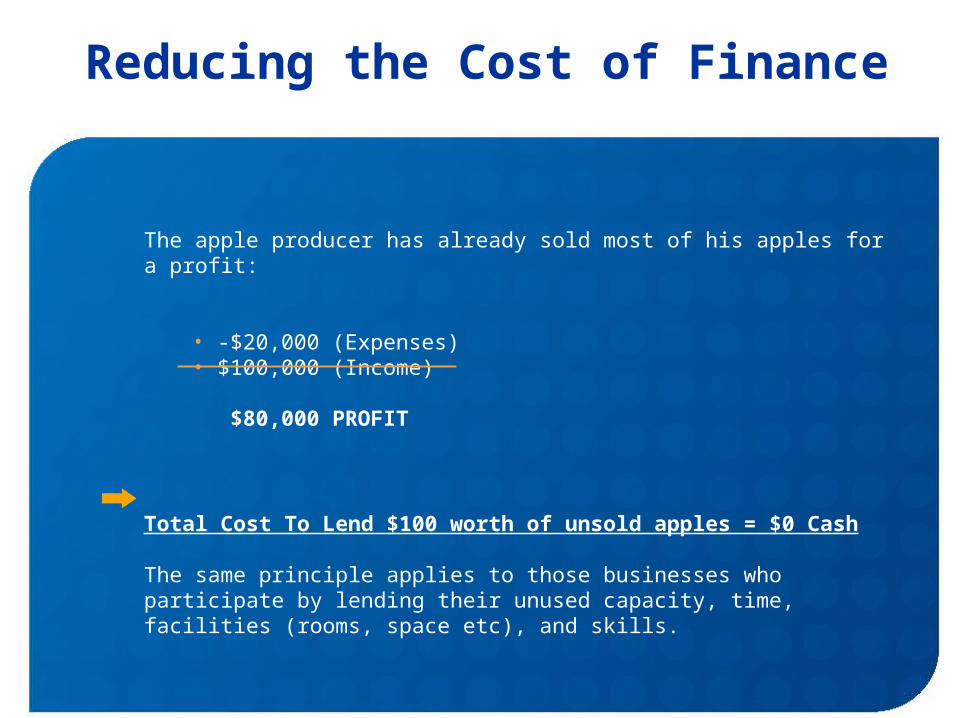

The apple producer has already sold most of his apples for a profit:

• -$20,000 (Expenses)• $100,000 (Income)

$80,000 PROFIT

Total Cost To Lend $100 worth of unsold apples = $0 Cash

The same principle applies to those businesses who participate by lending their unused capacity, time, facilities (rooms, space etc), and skills.

Reducing the Cost of Finance

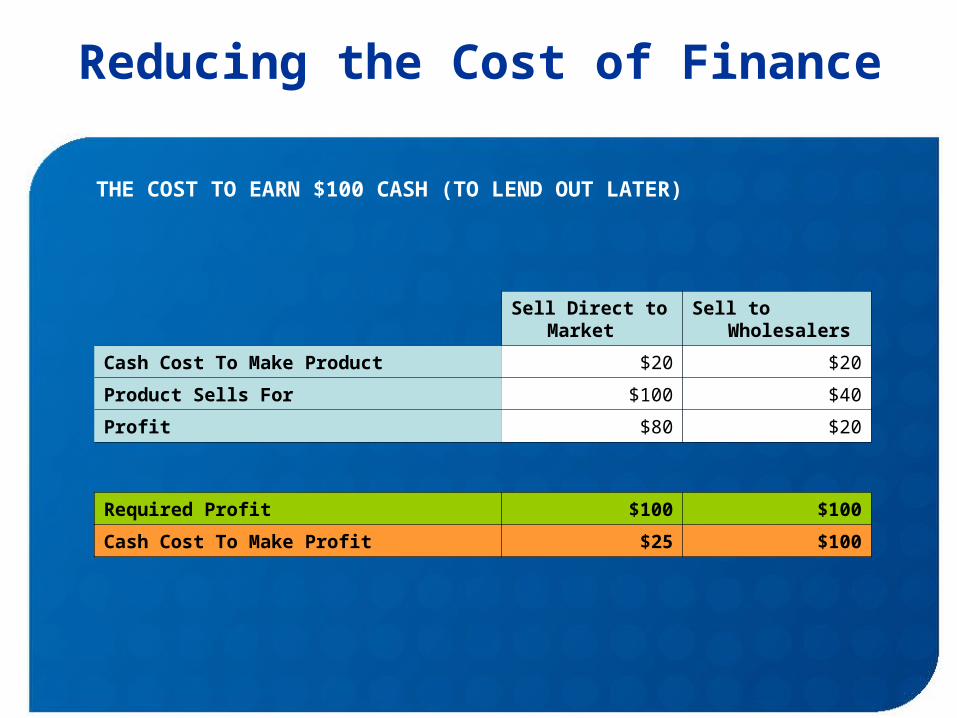

THE COST TO EARN $100 CASH (TO LEND OUT LATER)

Sell Direct to Market

Sell to Wholesalers

Cash Cost To Make Product $20 $20

Product Sells For $100 $40

Profit $80 $20

Required Profit $100 $100

Cash Cost To Make Profit $25 $100

Lenders are Repaid More

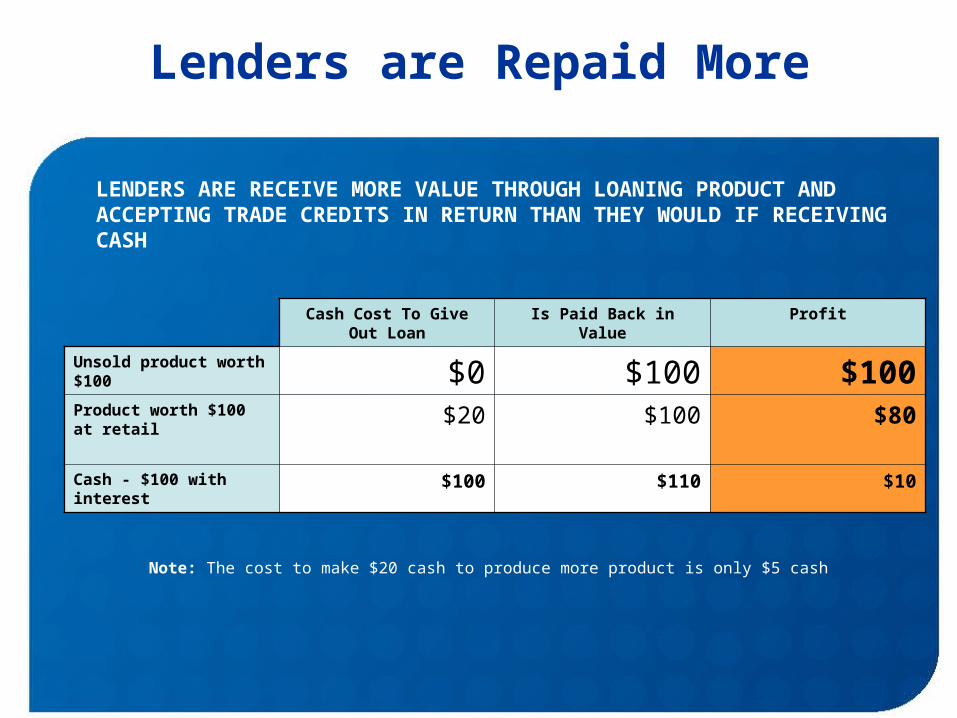

LENDERS ARE RECEIVE MORE VALUE THROUGH LOANING PRODUCT AND ACCEPTING TRADE CREDITS IN RETURN THAN THEY WOULD IF RECEIVING CASH

Note: The cost to make $20 cash to produce more product is only $5 cash

Cash Cost To Give Out Loan

Is Paid Back in Value Profit

Unsold product worth $100 $0 $100 $100Product worth $100 at retail

$20 $100 $80

Cash - $100 with interest

$100 $110 $10

Benefits For All Participants

Overview

Increased monetary circulation

Increased local wealth

More self-employment opportunities

Recession proofing

Increased purchasing power

Socio-economic wellbeing in cash poor communities

Use of assets which would otherwise be lost

New opportunities are created

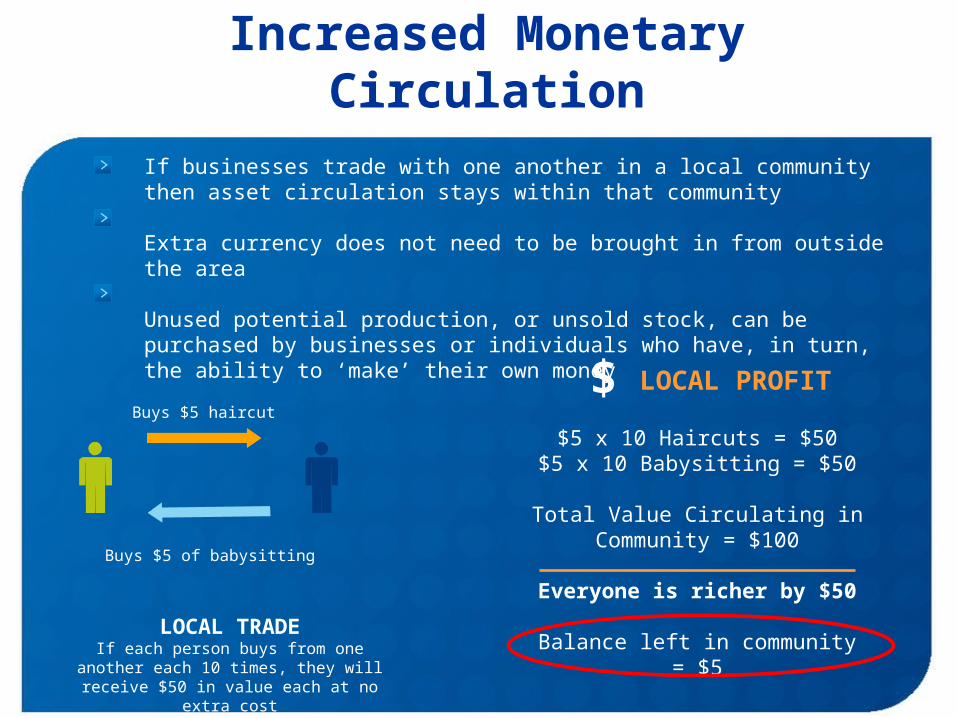

Increased Monetary Circulation

If businesses trade with one another in a local community then asset circulation stays within that community

Extra currency does not need to be brought in from outside the area

Unused potential production, or unsold stock, can be purchased by businesses or individuals who have, in turn, the ability to ‘make’ their own money

Buys $5 haircut

Buys $5 of babysitting

LOCAL TRADEIf each person buys from one another each 10 times, they will receive $50 in

value each at no extra cost

$5 x 10 Haircuts = $50$5 x 10 Babysitting = $50

Total Value Circulating in Community = $100

Everyone is richer by $50

Balance left in community = $5

$ LOCAL PROFIT

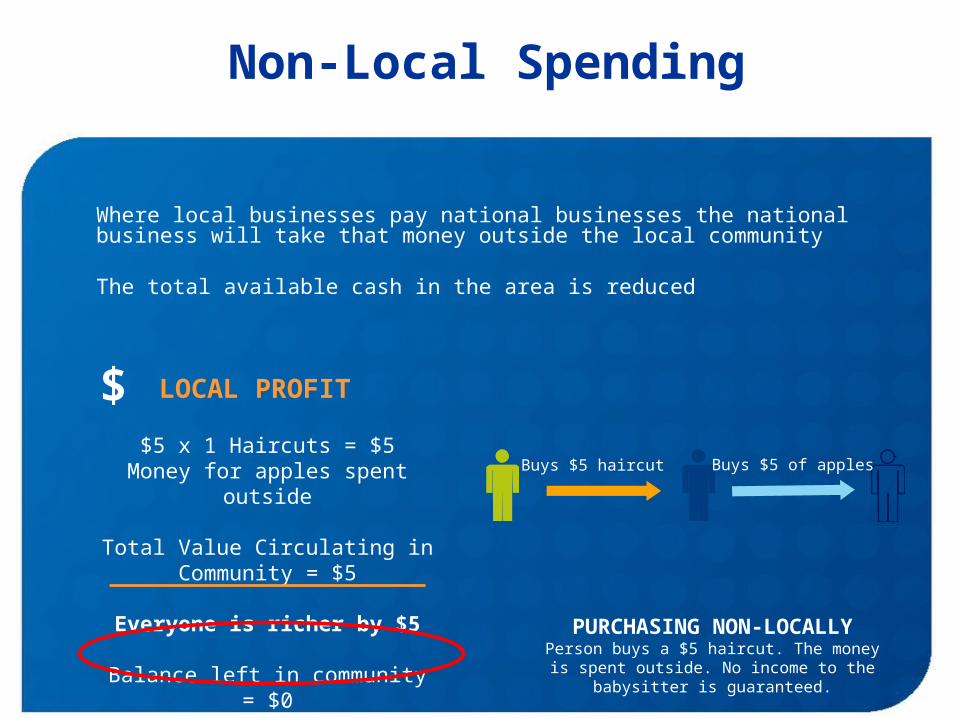

Non-Local Spending

Where local businesses pay national businesses the national business will take that money outside the local community

The total available cash in the area is reduced

PURCHASING NON-LOCALLYPerson buys a $5 haircut. The money is

spent outside. No income to the babysitter is guaranteed.

Buys $5 haircut Buys $5 of apples

$ LOCAL PROFIT

$5 x 1 Haircuts = $5Money for apples spent outside

Total Value Circulating in Community = $5

Everyone is richer by $5

Balance left in community = $0

Increased Local Wealth

Community wealth is not related to the amount of cash in a community, but the amount of assets, capacity and skills

Spending locally ensures that more money stays within the community

Participants can save more without reducing how much is spent

Participants can spend regardless of the amount of cash in the community or other external economic factors

Efficiency

Wastage is not primarily created because of over-consumption, it is created because of over-production and inefficient use of what is produced (throwing away instead of on-selling or recycling)

Both unsold products and services can be on-sold without loosing their value

Time / excess capacity are a priceless non-recoverable, non-recyclable limited commodities; selling under-utilized time and capacity means greater wealth for the seller and buyer

The perceived value of goods may be higher were a tradable currency is readily available

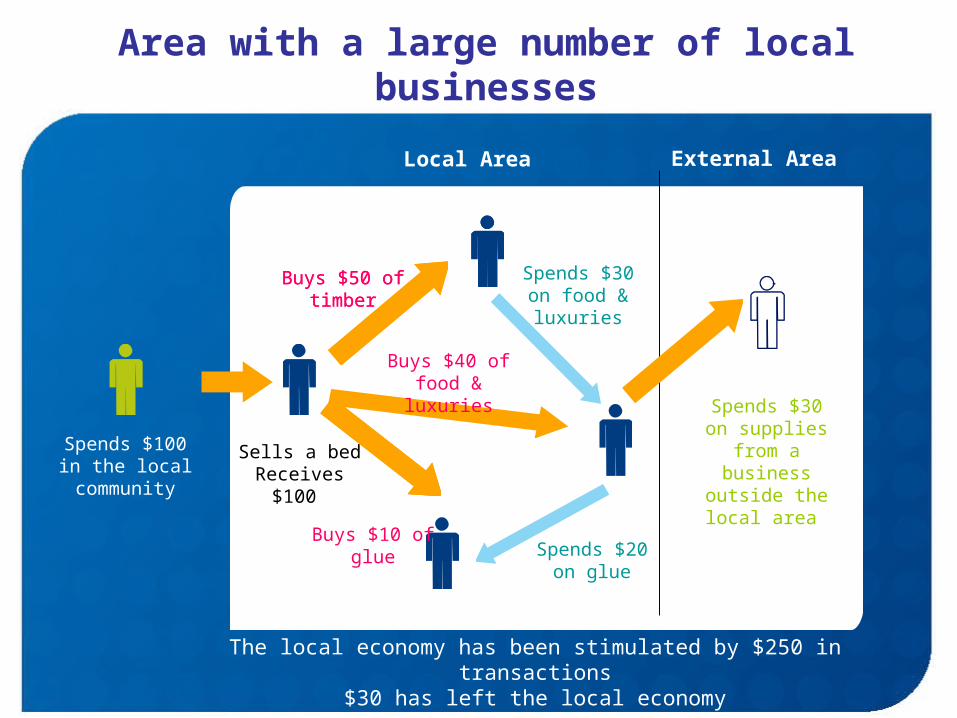

Local Area

Spends $100 in the local

community

Sells a bed Receives $100

Buys $50 of timber

Buys $10 of glue

Buys $40 of food & luxuries

Spends $30 on supplies from a

business outside the local area

External Area

The local economy has been stimulated by $250 in transactions$30 has left the local economyThere is still $70 left locally

Spends $20 on glue

Spends $30 on food & luxuries

Area with a large number of local businesses

Buys $50 of timber

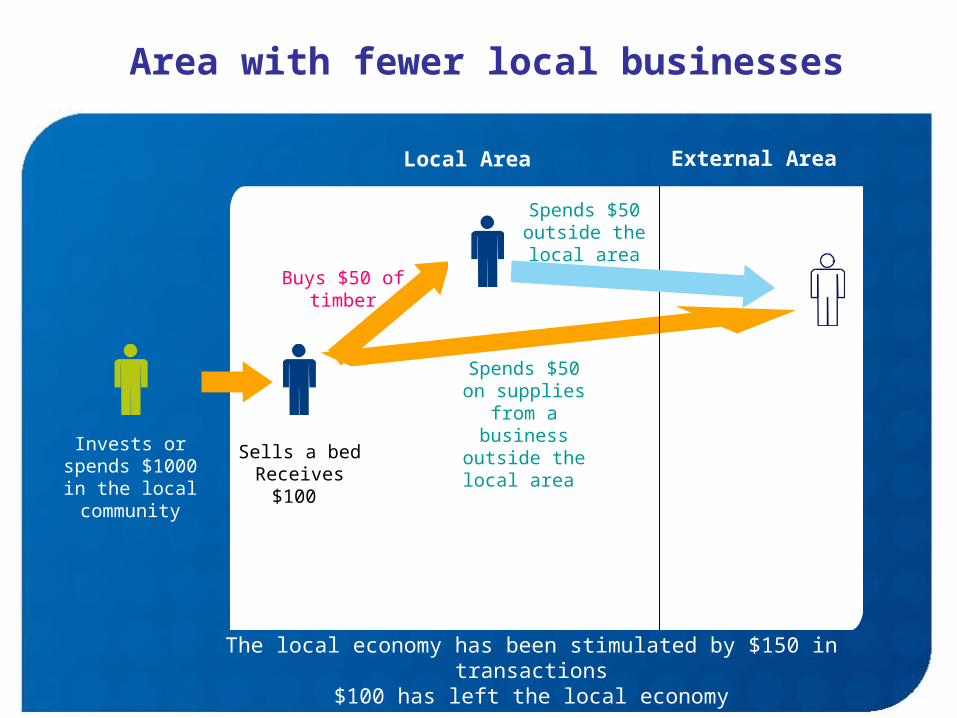

Local Area

Invests or spends $1000 in the local

community

Sells a bed Receives $100

Buys $50 of timber

Spends $50 on supplies from a

business outside the local area

External Area

The local economy has been stimulated by $150 in transactions$100 has left the local economyThere is no money left locally

Spends $50 outside the local area

Area with fewer local businesses

Examples From Across The Globe

Argentina - $6 Billion in Trade

In 2003 in Argentina, various currencies were in general circulation:

Argentine Pesos

U. S. Dollars

Provincial Currencies (up to 20 kinds in circulation)

Trueque Notes / Creditos (community credit currencies - about 100 types in use)

Argentina - Provincial Currencies

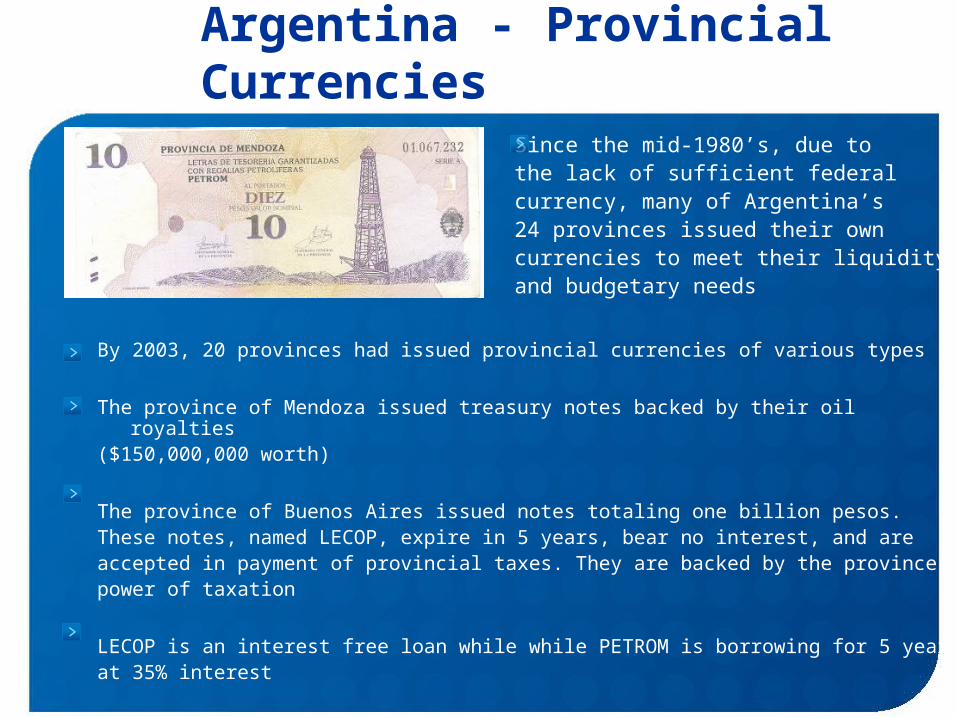

By 2003, 20 provinces had issued provincial currencies of various types

The province of Mendoza issued treasury notes backed by their oil royalties($150,000,000 worth)

The province of Buenos Aires issued notes totaling one billion pesos. These notes, named LECOP, expire in 5 years, bear no interest, and are accepted in payment of provincial taxes. They are backed by the province’spower of taxation

LECOP is an interest free loan while while PETROM is borrowing for 5 yearsat 35% interest

Since the mid-1980’s, due to the lack of sufficient federal currency, many of Argentina’s 24 provinces issued their own currencies to meet their liquidity and budgetary needs

Argentina – Trueque / Creditos

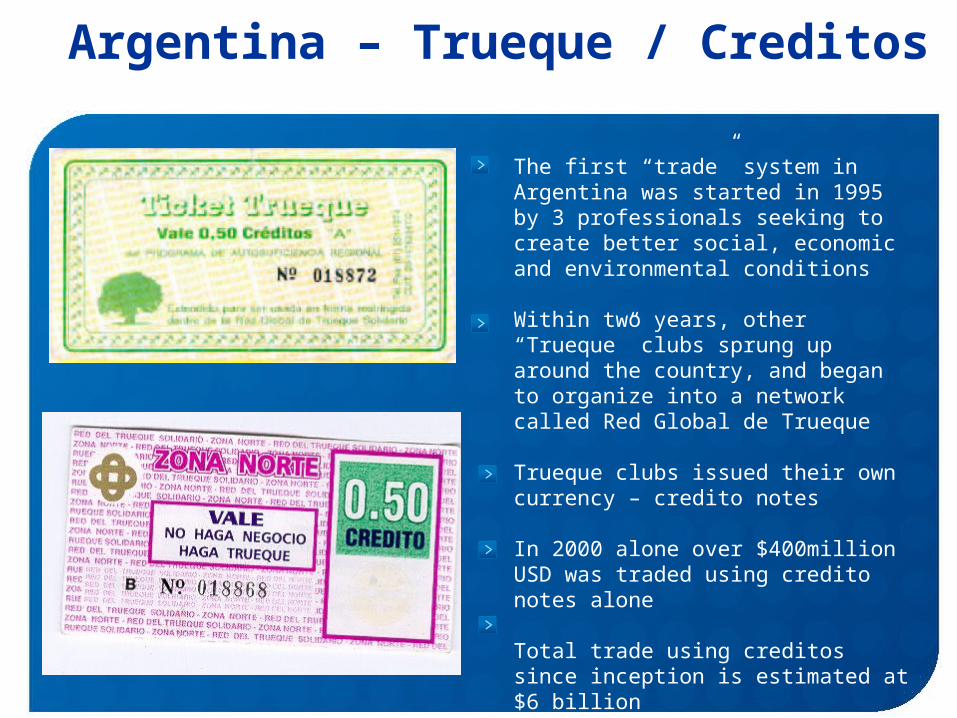

The first “trade” system in Argentina was started in 1995 by 3 professionals seeking to create better social, economic and environmental conditions

Within two years, other “Trueque” clubs sprung up around the country, and began to organize into a network called Red Global de Trueque

Trueque clubs issued their own currency – credito notes

In 2000 alone over $400million USD was traded using credito notes alone

Total trade using creditos since inception is estimated at $6 billion

Argentina – Economic Success

From an economic perspective the system has been extremely successful

Despite the fact that it is a paper-based, easily forged, and labour intensive to use, there are now over 6 million participants

The system has made a significant difference in the lives of the people who trade regularly

Many people now earn the majority of their income in ‘creditos’ and researchers believe that household consumption can be doubled (from US$300 to US$600 equivalent) (ibid; Primavera, 2000)

The system is strongly supported by the Argentine government who view it as not only a way to allow people to subsist in times of economic crisis but also to reintegrate with the formal economy (Garcia, 2000; Krauss, 2001)

Argentina – Trading Mechanism

Anyone can join so long as they attend two meetings to learn about the system and agree to abide by trading rules

New members are given a loan of 50 creditos - equivalent to around $50 - to begin trading

People set their own prices and the currency is not for accumulation, but purely for trade

Creditos are generally used at large markets where participants have stalls selling not only food and consumables, but also lawyers, dentists, hairdressers and even masseurs

Because of the lack of ready cash many of these small businesses would find no other means of marketing their services

Switzerland – The WIR

Switzerland – $1 Billion Per Annum

Founded in 1934 by Werner Zimmermann and Paul Enz

Aimed at small and medium-sized businesses were especially hard hit at that time by the depression following the stock market crash of 1929

Sales had receded massively, and many employees had lost their jobs. There were no signs of a recovery....

The new self-help organization was intended to provide a remedy. It started with 16 members and an initial capital of SFr 42,000....

After the war membership rolls grew rapidly

The WIR Cooperative now numbers over 62,000 members, who amongst themselves create transactions worth approximately SFr 1.65 billion (1.3 Billion US DOLLARS) annually

Switzerland – Foundations

In October 1934 the WIR Economic Circle Cooperative was brought to life by 16 founding members operating with start-up capital of SFr 42,000

By early 1935 there were already 1700 participants

By the end of the year 3,000

Operating within the framework of a solidarity-oriented self-help organization, members were expected to draw as much as possible on other members to cover their goods-and-services needs, in order to trigger additional turnover within the Circle

Before long the catalogue of offered goods and services covered 850 categories

Already in the first year of operation, turnover surpassed one million francs, this amounting to ten times the volume of WIR accounts

In the absence of the Circle, the majority of these sales would either never have come about at all, or would have gone to outsiders

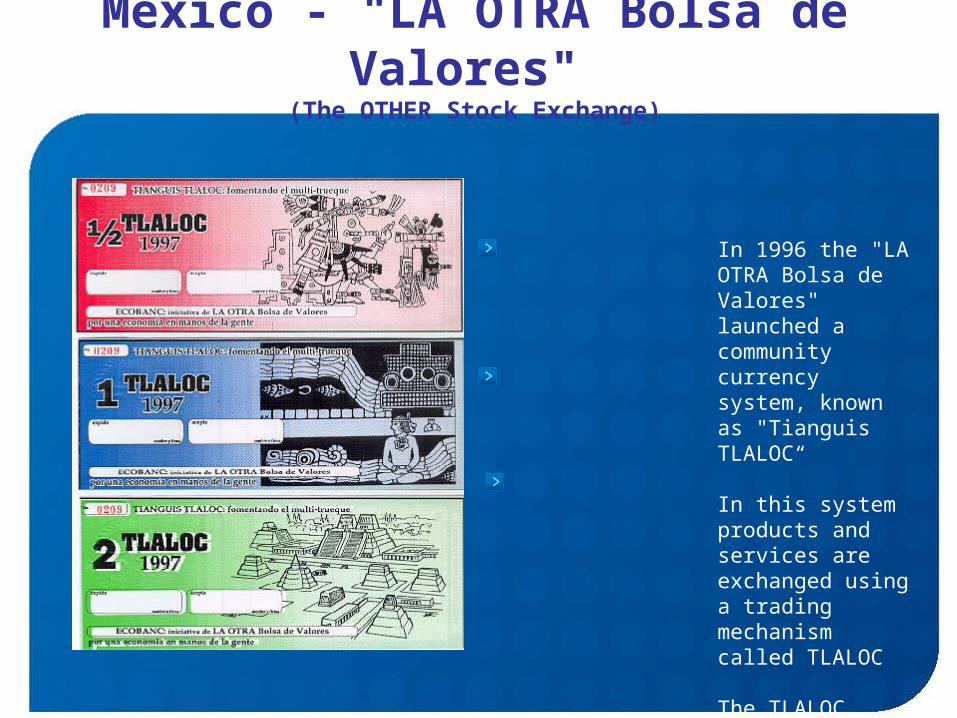

Mexico - "LA OTRA Bolsa de Valores"

(The OTHER Stock Exchange)

In 1996 the "LA OTRA Bolsa de Valores" launched a community currency system, known as "Tianguis TLALOC“

In this system products and services are exchanged using a trading mechanism called TLALOC

The TLALOC allows for the exchange of goods and services where no assets and skills still exist but cash is hard to come by

Mexico - Foundations

"LA OTRA Bolsa de Valores" (THE OTHER Stock Exchange) is a magazine that represents a network of many grassroots organisations and NGOs in Mexico.

Triggered by the Mexican crisis, with its persistent social and economic impacts at the grassroots level, the "LA OTRA Bolsa de Valores" created a platform in which causes and impacts of the financial crisis and its alternatives could be discussed

"We were deeply interested in the money issue, trying to understand why civil society and many NGOs, and, indeed,

practically all individuals and communities, can not overcome their dependency on it.

Money has caused frequent bubbles, it leads to various crises, we are all competing for it and are divided by it. The financial crisis caused a slump in economic activity, high unemployment and severe poverty, while people,

their labour and capabilities, and local resources were still available."

Luis Lopezllera Mendez, Editor of LA ORTA Bosla de Valores and president of Promocion del Desarrollo Popular (Promotion of Popular Development, Civil

Association) – a 40 year old NGO

Mexico – Trading Mechanism

Members have accounts where local trades are recorded, but also may choose to use notes as the medium of exchange

The TLALOC bill represents one hour of work and has an equivalent of approximately $3 USD

Every member of the network of producers, servers and consumers has signed a letter of agreement and has received 15 and a half Tlalocs to start trading products and services with other members of the Tianguis (social market and network)

He or she also receives 50 Tequios (tokens) ("Tequio" is an Aztec word meaning "communal effort")

It is recommended that members accept at least 30% of the price of a transaction in Tlalocs and Tequios

Pesos are accepted, but the policy is to increase the use of Tlaloc as much as possible

Mexico – ‘The Trade Floor’

Members are all from the same economic region within Mexico City

Every member of the network is given space in a quarterly directory where offers and demands for goods and services are publicized

There are approximately 150 registered units (micro-enterprises) as members, which can consist of several individuals

Monthly fairs are organized to allow producers and consumers to meet face to face and trade goods and services