the new axis of financial reporting - ind as and icds

TRANSCRIPT

THE POWER OF BEING UNDERSTOOD

THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS

BRINGING EXPERT GLOBAL ANDLOCAL KNOWLEDGE TO YOURENVIRONMENT

RSM in India

Consistently ranked amongst India�s top six accounting and consulting groups (International Accounting Bulletin, September 2015) Nationwide presence through offices in 12 key cities across India Multi-disciplinary personnel strength of over 1,200

rsmindia.in

RSM Seventh largest global audit, tax and consulting network (with total fee income of US$ 4.4 bn) and the sixth largest provider of tax services by revenue globally Firms in 120 countries and in each of the top 40 major business centres throughout the world Combined staff of over 37,500 in over 740 offices across the Americas, Europe, MENA, Africa and Asia Pacific

rsm.global

THE NEW AXIS OF FINANCIAL REPORTING- IND AS AND ICDS

| The New Axis of Financial Reporting � Ind AS and ICDS RSM

About this publication

The publication 'The New Axis of Financial Reporting � Ind AS and ICDS' is prepared by RSM Astute Consulting Pvt. Ltd. (the Indian member of RSM) to provide readers a broad understanding of applicability of Ind AS and Income Computation and Disclosure Standards (ICDS) and some key differences with IFRS and Indian Standards. The publication is general in nature and does not cover all the requirements of Ind AS / (ICDS). The publication does not focus on other regulatory requirements that an Indian Entity needs to comply with. The preparation of financial statements complying with Ind AS is the responsibility of the management of the relevant entity and accordingly this publication does not replace the need for professional judgment which may be necessary for application of relevant standards and other disclosure requirements.

Although the publication has been compiled by RSM Astute Consulting Pvt. Ltd., the views expressed are those of RSM Astute - IFRS Champions.

The copyright in this published work shall belong to and vest in RSM Astute Consulting Pvt. Ltd. and all rights are reserved. Every effort has been made to ensure the contents are accurate and current. Information in this publication is no way intended to replace or supersede specific independent or other professional, legal, tax or accounting advice. This publication cannot and should not be relied upon for taking actions or decisions without appropriate professional advice. While all reasonable care has been taken in preparation of this publication, we accept no responsibility for any liability arising from any statements or errors contained in this publication.

Happy Reading!

|The New Axis of Financial Reporting � Ind AS and ICDS RSM

Table of Contents

Chapter 1 : Introduction 1Chapter 2 : Applicability of Ind AS 5Chapter 3 : Ind AS Vs. IFRS Vs. Indian GAAP (AS) 9 3.1 Ind AS Vs. IFRS and Indian GAAP (AS) � Listing 10 3.2 Ind AS Vs. IFRS � Carve-outs 13 3.3 Ind AS Vs. AS - Key Differences 22Chapter 4 : Ind AS Vs. ICDS � Key Differences 75 4.1 Brief Background of ICDS 76 4.2 Comparison of ICDS and Ind AS 76 4.3 Comparative list of ICDS Vs. corresponding Ind AS 77 4.4 Key differences � ICDS Vs. Ind AS 77Chapter 5 : First Time Adoption of Indian Accounting Standards (Ind AS 101) 96 5.1 Scope of Ind AS 101 97 5.2 Certain Key Aspects 97 5.2.1 Opening Ind AS balance sheet and accounting policies 97 5.2.2 Exceptions to the principles that an entity�s opening Ind AS balance sheet shall fully comply with each Ind AS effective at the reporting date 98 5.2.3 Exemptions from retrospective application of some aspects of other Ind AS 99 5.2.4 Exemptions from the requirements of certain Ind ASs 100 5.2.5 Comparative information 101 5.2.6 Explanation for transition to Ind AS 101 5.2.7 Use of fair value as deemed cost 102 5.2.8 Use of deemed cost for investments in subsidiaries, joint ventures and associates 102 5.2.9 Derecognition of financial assets and financial liabilities 103 5.2.10 Hedge accounting 103 5.2.11 Non-controlling interest 104 5.2.12 Interim financial reports 105 5.2.13 Presentation and disclosures 105Chapter 6 : Frequently Asked Questions (FAQs) by First Time Adopters of Ind AS 107 6.1 From which date Ind AS will be applicable in India? 108 6.2 Which entities in India need to comply with Ind AS with effect from 1 April 2016? 108 6.3 If an unlisted company has net worth less than Rs. 250 crores as at 31 March 2014, can Ind AS become applicable to it in future? 108

Table of Contents

6.4 What is the date of transition to Ind AS? 108 6.5 If the date of transition to Ind AS is 1 April 2015, what GAAP the Indian company needs to follow for the year 2015-2016? 109 6.6 What are the components of a complete set of Ind AS financial statements? 109 6.7 What would entity need to do in converting financial statements as per Indian GAAP to Ind AS financial statements? 109 6.8 Can any entity prepare Ind AS financial statements for period longer / shorter than one year? If yes, what are the disclosures required? 110 6.9 Which Ind AS would an entity need to comply with in its first Ind AS financial statements? 110 6.10 If an entity presents interim financial information for part of the period covered by its first Ind AS financial statements, what additional disclosures are required? 111 6.11 What is offsetting? 111

| The New Axis of Financial Reporting � Ind AS and ICDS RSM

Terms DefinitionAFS Available for saleAS Accounting Standards notified vide Companies (Accounting Standards) Rules, 2006BS Balance SheetCFS Consolidated Financial StatementsCGU Cash Generating UnitEPS Earning Per ShareFASB Financial Accounting Standards BoardFIFO First-In First-OutGAAP Generally Accepted Accounting PrinciplesGCA Going Concern AssumptionIAS The International Accounting StandardsIASB The International Accounting Standards BoardICAI The Institute of Chartered Accountants of IndiaICDS Income Computation and Disclosure StandardsIFRIC The International Financial Reporting Interpretations Committee IFRS The International Financial Reporting StandardsIND AS Indian Accounting Standards notified vide Companies (Accounting Standards) Rules, 2015MCA Ministry of Corporate Affairs NRV Net Realisable ValueOCI Other Comprehensive IncomeP&L Profit and LossPPE Property, Plant and EquipmentSFS Separate Financial StatementsSIC Standing Interpretations CommitteeSMC Small and Medium-Sized CompaniesSME Small and Medium-Sized EntitiesWAV Weighted Average Cost

Abbreviations

|The New Axis of Financial Reporting � Ind AS and ICDS RSMBack to Content

1.0 INTRODUCTION

Back to Content

The financial reporting for Indian companies is set to change completely from financial year 2016-17 with India moving towards IFRS - the most commonly used global financial reporting standards. From the financial year 2016-17, companies whose equity or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having net worth of Rs. 500 crores or more (about US$ 75 million) as well as unlisted companies having net worth of Rs. 500 crores or more (about US$ 75 million) would be required to adopt Ind AS i.e. the Indian Accounting Standards which have been converged with the IFRS with certain minimal exceptions. This requirement will also be applicable to the holding, subsidiary, joint venture or associate companies of companies covered above. From the financial year 2017-18, companies whose equity or debt securities are listed or are in the process of listing on any stock exchange in India or outside India irrespective of net worth and all other companies having net worth of Rs. 250 crores or more (about US$ 38 million) would be required to adopt Ind AS. This is perhaps the most significant change in respect of financial reporting in the history of corporate India and will have far reaching implications in terms of assets, liabilities, income and expenses, disclosures and will also impact tax on book profits.

The term International Financial Reporting Standards (IFRSs) includes IFRSs, IASs and interpretations originated by the IFRIC or its predecessor, the former Standing Interpretations Committee (SIC). IFRS are increasingly being recognised as Global Reporting Standards for financial statements. �National GAAP� is becoming rare. As global capital markets become increasingly integrated, many countries are moving to IFRS. More than 130 countries such as European Union, Australia, New Zealand and Russia currently permit the use of IFRS in their countries.

IFRSs are accounting standards for reporting financial results and are applicable to general purpose financial statements and other financial reporting of all profit- oriented entities. Profit-oriented entities includes those engaged in commercial, industrial, financial and similar activities, whether organized in corporate or in other forms also includes mutual insurance companies, other mutual co-operative entities, etc. developed and approved by IASB (International Accounting Standard Board).

Chapter 1 Introduction

|The New Axis of Financial Reporting � Ind AS and ICDS 2RSMBack to Content

Chapter 1 Introduction

IASB is also working with FASB on joint project to align IFRS and US GAAP along with other projects to improve IFRS requirements. As a result, IFRS have under gone significant changes in recent past and more changes would be implemented in future.

The legal recognition to the Accounting Standards in India was accorded for the companies in the Companies Act, 1956, by introduction of Section 211(3C) whereby it is required that the companies shall follow the Accounting Standards notified by the Central Government. The Accounting Standards were notified by Ministry of Corporate Affairs (MCA) vide the Companies (Accounting Standards) Rules, 2006 under the Companies Act, 1956. This Rule contained the standards to be applied by companies for preparation of general purpose financial statements for accounting periods commencing on or after 7 December 2006.

In February 2011, MCA had hosted 35 Ind AS (Indian Accounting Standards, which are converged with IFRS) on its website. However, date for implementation of these Ind AS by Indian companies was not notified.

In February 2015, MCA notified the Companies (Indian Accounting Standards) Rules2015. These rules require select class of companies and their auditors to comply with the Ind AS in specified manner. Other companies not required to comply with Ind AS are required to comply with Accounting Standards as specified in Annexure to the Companies (Accounting Standards) Rules, 2006.

Sub-section (1) of Section 145 of the Income-tax Act, 1961 (�the Act�) provides that the income chargeable under the head �Profits and gain of business or profession� or �Income from other sources� shall [subject to the provisions of sub-section (2)] be computed in accordance with either cash or mercantile system of accounting regularly employed by the assessee. Sub-section (2) of Section 145 provides that the Central Government may notify Income Computation and Disclosure Standards (ICDS) for any class of assessees or for any class of income. 10 ICDS were notified and are effective from 1 April 2015 and accordingly applicable from the assessment year 2016-17 onwards.

| The New Axis of Financial Reporting � Ind AS and ICDS 3 RSMBack to Content

What is Ind AS?

Ind AS stands for Indian Accounting Standards as notified by MCA vide Companies (Indian Accounting Standards) Rules, 2015. These are standards converged with International Financial Reporting Standards (IFRS).

Since India has not adopted IFRS as issued by IASB, Ind AS were formulated. In principle, Ind AS are very much same as IFRS, but with some exceptions (carveouts).

Ind AS are not approved by IASB, but are approved / notified by MCA for implementation by select class of Indian companies.

It can also be noted that the 39 Ind AS as notified by MCA in February 2015 are not same as 35 Ind AS published in February 2011.

The notified Ind AS would be mandatorily applied by select class of companies from financial year 2016-17, with comparatives for previous year ending 31 March 2016 or thereafter.

IFRS stands for �International Financial Reporting Standards� and includes International Accounting Standards (IAS) until they are replaced by any IFRS and interpretations originated by the IFRIC or its predecessor, the former Standing Interpretations Committee (SIC).

Chapter 1 Introduction

|The New Axis of Financial Reporting � Ind AS and ICDS 4RSMBack to Content

2.0 APPLICABILITY OF IND AS

Back to Content

Ind AS are applicable to companies meeting specified criteria as under:

Particulars Phase I (FY 2016-17) Phase II (FY 2017-18)

Covered companies

Year in which Ind AS to be applied

Comparative figures for preceding accounting period

a) Companies whose equity or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having net worth of Rs. 500 crores or more

Accounting period beginning on or after 1 April 2016

Required for period ending on 31 March 2016 or thereafter

a) Companies whose equity or debt securities are listed or are in the process of listing on any stock exchange in India or outside India and having net worth less than Rs. 500 crores

Accounting period beginning on or after 1 April 2017

Required for period ending on 31 March 2017 or thereafter

b) Companies not covered in (a) above and having net worth of Rs. 500 crores or more

b) Companies not covered in (a) above and having net worth of Rs. 250 crores or more but less than Rs. 500 crores

c) Holding, subsidiary, joint venture or associate companies of companies covered above

c) Holding, subsidiary, joint venture or associate companies of companies covered above

Notes:

1. Ind AS shall be applicable to both, standalone and consolidated financial statements of the company.

2. Any company may comply with the Ind AS for financial statements for accounting periods beginning on or after 1 April 2015, with the comparatives for the periods ending on 31 March 2015 or thereafter. Such company would prepare its financial statements as per Ind AS consistently.

3. Companies whose securities are listed or are in the process of being listed on SME exchange without initial public offering need not apply Ind AS.

Chapter 2 Applicability of Ind AS

|The New Axis of Financial Reporting � Ind AS and ICDS 6RSMBack to Content

4. 'Net Worth' means the aggregate value of the paid-up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation.

5. For the purpose of applicability of Ind AS the net worth shall be calculated in accordance with the standalone financial statements of the company as on 31 March 2014 or the first audited financial statements for accounting period which ends after that date.

6. Companies which are not in existence as on 31 March 2014 or an existing company falling under any of the thresholds specified in subsequent year, the net worth shall be calculated on the basis of first audited financial statements ending after 31 March 2014.

7. Overseas subsidiary, associates, joint venture and other similar entities of an Indian company may prepare its standalone financial statements in accordance with the requirements of the specific jurisdiction.

8. Once a company starts following Indian Accounting Standards (Ind AS) either voluntarily or mandatorily), it shall be required to follow the Indian Accounting Standards (Ind AS) for all the subsequent financial statements.

9. Once Indian Accounting Standards (Ind AS) are applied voluntarily, it shall be irrevocable and such companies shall not be required to prepare another set of financial statements in accordance with Accounting Standards specified in Annexure to Companies (Accounting Standards) Rules, 2006.

10. Ind AS are intended to be in conformity with the provisions of applicable laws. However, if due to subsequent amendments in the law, a particular Ind AS is found not to be inconformity with such law, the provisions of the said law shall prevail and the financial statements shall be prepared in conformity with such law.

Chapter 2 Applicability of Ind AS

| The New Axis of Financial Reporting � Ind AS and ICDS 7 RSMBack to Content

11. Ind AS are intended to apply only to items which are material.

Exemptions: The insurance companies, banking companies and non-banking finance companies shall not be required to apply Ind AS for preparation of their financial statements either voluntarily or mandatorily. It is expected that a separate roadmap would be announced by MCA for implementation of Ind AS by these classes of companies in near future.

Chapter 2 Applicability of Ind AS

|The New Axis of Financial Reporting � Ind AS and ICDS 8RSMBack to Content

3.0 IND AS VS. IFRS VS. INDIAN GAAP (AS)

Back to Content

3.1 Ind AS Vs. IFRS and Indian GAAP (AS) � Listing

As at 30 September 2015, 39 Ind AS corresponding to related IFRS have been notified. There are 43 IFRS of which 3 standards though issued would be applicable from future dates. Similarly there are 28 AS that are applicable as on this date.

A comparative listing of accounting standards under Ind AS, IFRS and AS, as at 30 September 2015 is given hereunder:

ASAS 1 - Disclosure of Accounting Policies

IFRSInd ASIAS 1 - Presentation of Financial Statements

Ind AS 1 - Presentation of Financial Statements

AS 2 - Valuation of Inventories

IAS 2 - InventoriesInd AS 2 - Inventories

AS 3 - Cash Flow Statements

IAS 7 - Statements of Cash Flows

Ind AS 7 - Statement of Cash Flows

AS 5 - Net Profit or Loss for the period, Prior period items and Changes in Accounting policies

IAS 8 - Accounting Policies, Changes in Accounting estimates and errors

Ind AS 8 - Accounting policies, Changes in Accounting estimates and errors

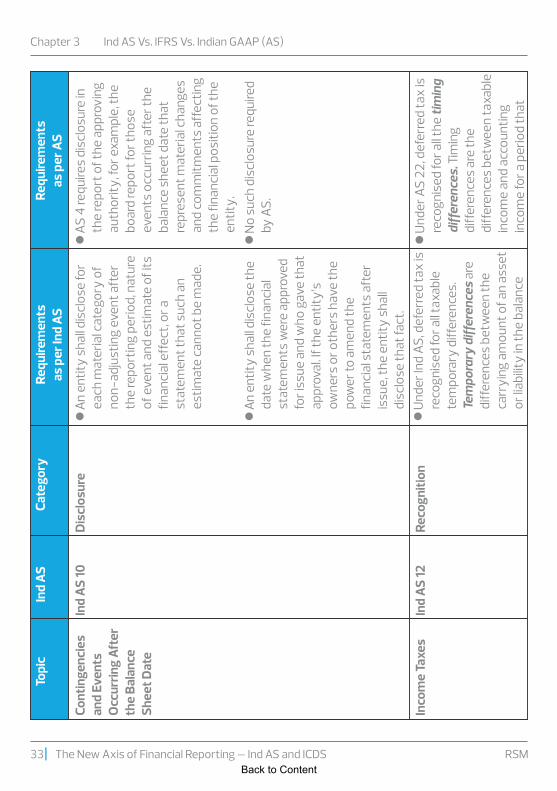

AS 4 � Contingencies and event occurring after the balance sheet date

IAS 10 - Events After the Balance Sheet Date

Ind AS 10 � Event after the reporting period

AS 7 - Construction Contracts

IAS 11 - Construction Contracts (will be superseded by IFRS 15 � Revenue from Contract with Customers)

AS 22 - Accounting for Taxes on Income

IAS 12 - Income TaxesInd AS 12 - Income Taxes

AS 10 � Accounting for Fixed AssetsAS 6 - Depreciation Accounting

IAS 16 - Property, Plant and Equipment

Ind AS 16 - Property, Plant and Equipment

AS 19 � LeasesIAS 17 - LeasesInd AS 17 - Leases

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

AS 9 - Revenue Recognition

IAS 18 - Revenue (will be superseded by

|The New Axis of Financial Reporting � Ind AS and ICDS 10RSM

Ind AS 115 - Revenue from Contract with Customers

Back to Content

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

ASIFRSInd ASIFRS 15 � Revenue from Contract with Customers)

AS 15 - Employee BenefitsIAS 19 - Employee Benefits

Ind AS 19 - Employee Benefits

AS 12 - Accounting for Government Grants

IAS 20 - Accounting for Government Grants and Disclosure of Government Assistance

Ind AS 20 - Accounting for Government Grants and Disclosure of Government Assistance

AS 11 - The Effects of Changes in Foreign Exchange Rates

IAS 21 - The Effect of Changes in Foreign Exchange Rates

Ind AS 21 - The Effects of Changes in Foreign Exchange Rates

AS 16 - Borrowing CostsIAS 23 - Borrowing CostsInd AS 23 - Borrowing Costs

AS 18 - Related Party Disclosures

IAS 24 - Related Party Disclosures

Ind AS 24 - Related Party Disclosures

IAS 26 - Accounting and Reporting by Retirement Benefit PlansIAS 27 - Separate Financial Statements

Ind AS 27 - Separate Financial Statements

AS 23 - Accounting for Investments in Associates in Consolidated Financial Statements

IAS 28 - Investments in Associates and Joint Ventures

Ind AS 28 - Investments in Associates and Joint Ventures

IAS 29 - Financial Reporting in Hyperinflationary Economies

Ind AS 29 - Financial Reporting in Hyperinflationary Economies

AS 27 - Financial reporting of Interests in Joint Ventures

IAS 32 - Financial Instruments - Presentation

Ind AS 32 - Financial Instruments - Presentation

AS 20 - Earnings per share

IAS 33 - Earnings per share

Ind AS 33 - Earnings per share

| The New Axis of Financial Reporting � Ind AS and ICDS 11 RSMBack to Content

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

ASIFRSInd ASAS 25 - Interim Financial Reporting

IAS 34 - Interim Financial Reporting

Ind AS 34 - Interim Financial Reporting

AS 28 - Impairment of Assets

IAS 36 - Impairment of Assets

Ind AS 36 - Impairment of Assets

AS 29 - Provisions, Contingent Liabilities and Contingent Assets

IAS 37 - Provisions, Contingent Liabilities and Contingent Assets

Ind AS 37 - Provisions, Contingent Liabilities and Contingent Assets

AS 26 - Intangible AssetsIAS 38 - Intangible AssetsInd AS 38 - Intangible Assets

AS 13 - Accounting for Investments

IAS 39 - Financial instruments - Recognition and Measurement

AS 13 - Accounting for Investments

IAS 40 - Investment Property

Ind AS 40 - Investment Property

IAS 41 - AgricultureInd AS 41 - AgricultureIFRS 1 - First Time Adoption of International Financial Reporting Standards

Ind AS 101 - First Time Adoption of Indian Accounting Standards

IFRS 2 - Share based payment

Ind AS 102 - Share based payment

AS 14 - Accounting for Amalgamations

IFRS 3 - Business combinations

Ind AS 103 - Business Combinations

IFRS 4 - Insurance Contracts

Ind AS 104 - Insurance Contracts

IFRS 5 - Non Current Assets Held for Sale and Discontinued Operations

AS 24 � Discontinued Operations

Ind AS 105 - Non Current Assets Held for Sale and Discontinued Operations

IFRS 6 - Exploration for and evaluation of Mineral Resources

Ind AS 106 - Exploration for and evaluation of Mineral Resources

IFRS 7 - Financial Instruments - Disclosures

Ind AS 107 - Financial Instruments - Disclosures

AS 17 � Segment Reporting

IFRS 8 - Operating Segments

Ind AS 108 - Operating Segments

|The New Axis of Financial Reporting � Ind AS and ICDS 12RSMBack to Content

IFRS 9 - Financial Instruments (effective from 1 Jan 2018)

Ind AS 109 � Financial Instruments

AS 21 - Consolidated Financial Statements

IFRS 10 - Consolidated Financial statements

Ind AS 110 � Consolidated Financial Statements

AS 27 - Financial reporting of Interests in Joint Ventures

IFRS 11 - Joint Arrangements

Ind AS 111 � Joint Arrangements

IFRS 12 - Disclosure of Interests in other entities

Ind AS 112 � Disclosure of Interest in other entities

IFRS 13 - Fair value measurement

Ind AS 113 � Fair value measurement

IFRS 14 - Regulatory Deferral Accounts (effective from 1 Jan 2016)

Ind AS 114 � Regulatory Deferral Accounts

AS 7 - Construction ContractsAS 9 - Revenue Recognition

IFRS 15 - Revenue from Contracts with Customers (effective from 1 Jan 2018)

Ind AS 115 � Revenue from Contracts with Customers

Chapter 3

ASIFRSInd AS

Standards that would be mandatory from a future datea

Standards that would be superseded

No corresponding Standards

3.2 Ind AS Vs. IFRS � Carve-outs

India has not adopted IFRS as issued by IASB, instead IFRS converged standards (Ind AS) were formulated and notified. Though in principle, Ind AS�s are similar to IFRS, certain differences still exist which are popularly called carve-outs. In order to facilitate easy comparison and understanding, at the end of each Ind AS an Appendix is given summarizing the differences, if any, between Ind AS and corresponding IFRS

A brief summary of significant carve-outs (differences between IFRS and Ind AS) is as follows:

Ind AS Vs. IFRS Vs. Indian GAAP (AS)

| The New Axis of Financial Reporting � Ind AS and ICDS 13 RSMBack to Content

IFRS

Ind

ASPa

rtic

ular

sBa

lanc

e sh

eet

Ind

AS-1

Te

rmin

olog

y

used

Stat

emen

t of f

inan

cial

pos

ition

(SO

FP)

Stat

emen

t of p

rofit

and

loss

Stat

emen

t of p

rofit

or l

oss

(SO

PL) a

nd o

ther

co

mpr

ehen

sive

inco

me(

SOCI

)Ap

prov

al o

f fin

anci

al s

tate

men

ts fo

r iss

ueAu

thor

izat

ion

of fi

nanc

ial s

tate

men

ts fo

r iss

ueTr

ue a

nd fa

ir vi

ewFa

ir pr

esen

tatio

nIn

d AS

requ

ires

all e

ntiti

es to

use

term

inol

ogy

for t

he ti

tle o

f the

fina

ncia

l sta

tem

ents

as

give

n in

the

stan

dard

IAS

1 giv

es th

e op

tion

to in

divi

dual

ent

ities

to

follo

w d

iffer

ent t

erm

inol

ogy

for t

he ti

tle o

f the

fin

anci

al s

tate

men

ts

Ind

AS 1

allo

ws

only

sin

gle

stat

emen

t app

roac

h fo

r pre

sent

ing

stat

emen

t of p

rofit

and

loss

and

ot

her c

ompr

ehen

sive

inco

me,

i.e. c

ompo

nent

s of

pro

fit o

r los

s an

d co

mpo

nent

s of

oth

er

com

preh

ensi

ve in

com

e sh

all b

e pr

esen

ted

as a

pa

rt o

f the

sta

tem

ent o

f pro

fit a

nd lo

ss.

Pres

enta

tion

of

Fina

ncia

l St

atem

ents

IAS

1 pro

vide

s an

opt

ion

eith

er to

follo

w th

e si

ngle

sta

tem

ent a

ppro

ach

or to

follo

w th

e tw

o st

atem

ent a

ppro

ach

i.e. e

ntity

may

eith

er

pres

ent a

sin

gle

stat

emen

t of

prof

it or

loss

and

ot

her c

ompr

ehen

sive

inco

me

pres

ente

d in

two

sect

ion

or p

rese

nt s

epar

ate

stat

emen

t of p

rofit

or

loss

whi

ch s

hall i

mm

edia

tely

pre

cede

the

stat

emen

t pre

sent

ing

com

preh

ensi

ve in

com

e,

whi

ch s

hall b

egin

with

pro

fit o

r los

s.O

nly

natu

re-w

ise

clas

sific

atio

n of

exp

ense

is

allo

wed

.Ex

pens

es c

lass

ifica

tion

base

d on

eith

er n

atur

e or

func

tion

is a

llow

ed.

Long

term

loan

s ne

ed n

ot b

e cl

assi

fied

as

curr

ent l

iabi

litie

s on

acc

ount

of b

reac

h of

a

mat

eria

l pro

visi

on, f

or w

hich

the

lend

er h

as

agre

ed to

wai

ve b

efor

e th

e ap

prov

al o

f fin

anci

al

stat

emen

ts fo

r iss

ue.

Und

er IF

RS, e

ntiti

es n

eed

to c

lass

ify s

uch

long

te

rm lo

an a

s cu

rren

t, ev

en if

the

lend

er a

gree

d,

afte

r the

repo

rtin

g pe

riod

and

befo

re th

e au

thor

isat

ion

of th

e fin

anci

al s

tate

men

ts fo

r is

sue,

not

to d

eman

d pa

ymen

t as

a co

nseq

uenc

e of

the

brea

ch.

Ind

AS 7

doe

s no

t pro

vide

an

optio

n to

cla

ssify

th

e in

tere

st p

aid

and

inte

rest

/ d

ivid

ends

St

atem

ent o

f Ca

sh F

low

IAS

7 gi

ves

an o

ptio

n to

cla

ssify

the

inte

rest

pai

d an

d in

tere

st /

divi

dend

s re

ceiv

ed a

s ite

m o

f

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

|The New Axis of Financial Reporting � Ind AS and ICDS 14RSMBack to Content

IFRS

Ind

ASPa

rtic

ular

sre

ceiv

ed a

s ite

m o

f ope

ratin

g ca

sh fl

ows

and

requ

ires

thes

e ite

m to

be

clas

sifie

d as

item

of

finan

cing

act

ivity

and

inve

stin

g ac

tivity

re

spec

tivel

y.

oper

atin

g ca

sh fl

ows.

Ind

AS 7

requ

ires

divi

dend

pai

d to

be

clas

sifie

d as

an

item

of f

inan

cing

act

ivity

onl

y.IA

S 7

give

s an

opt

ion

to c

lass

ify th

e di

vide

nd

paid

as

an it

em o

f ope

ratin

g ac

tivity

.

Even

ts a

fter

the

Repo

rtin

g Pe

riod

Whe

n an

ent

ity b

reac

hes

a m

ater

ial p

rovi

sion

of

a lo

ng-t

erm

loan

arr

ange

men

t on

or b

efor

e th

e en

d of

the

repo

rtin

g pe

riod

with

the

effe

ct th

at

the

liabi

lity

beco

mes

pay

able

on

dem

and

on th

e re

port

ing

date

and

if th

e le

nder

, bef

ore

the

appr

oval

of t

he fi

nanc

ial s

tate

men

ts fo

r iss

ue,

agre

es to

wai

ve th

e br

each

, it s

hall b

e co

nsid

ered

as

an a

djus

ting

even

t.

Whe

n an

ent

ity b

reac

hes

the

prov

isio

n of

a lo

ng

term

loan

arr

ange

men

t on

or b

efor

e th

e en

d of

th

e re

port

ing

perio

d w

ith th

e ef

fect

that

liabi

lity

beco

mes

pay

able

on

dem

and,

an

agre

emen

t by

the

lend

er a

fter

the

repo

rtin

g pe

riod

and

befo

re

the

auth

roris

atio

n of

the

finan

cial

sta

tem

ents

fo

r iss

ue, n

ot to

dem

and

paym

ent i

s no

t co

nsid

ered

as

an a

djus

ting

even

t.

Leas

esIn

d AS

17 e

scal

atio

n of

ope

ratin

g le

ase

rent

als

that

are

in lin

e w

ith th

e ex

pect

ed g

ener

al

infla

tion,

the

incr

ease

s in

the

rent

als

shal

l not

be

stra

ight

line.

IAS

17 re

quire

s re

cogn

ition

of o

pera

ting

leas

e ex

pens

es /

inco

me

on s

trai

ght l

ine

basi

s un

less

an

othe

r sys

tem

atic

bas

is is

mor

e re

pres

enta

tive

of th

e tim

e pa

tter

n of

the

user

�s

bene

fit.

Empl

oyee

Be

nefit

sIn

d AS

19 re

quire

s th

e ra

te u

sed

to d

isco

unt

post

-em

ploy

men

t ben

efit

oblig

atio

ns to

be

dete

rmin

ed b

y re

fere

nce

to m

arke

t yie

lds

on

gove

rnm

ent b

onds

. How

ever

, sub

sidi

arie

s,

asso

ciat

es, jo

int v

entu

res

and

bran

ches

do

mic

iled

outs

ide

Indi

a sh

all d

isco

unt p

ost-

empl

oym

ent b

enef

it ob

ligat

ions

aris

ing

on

acco

unt o

f pos

t-em

ploy

men

t ben

efit

plan

s

IAS

19 ra

te u

sed

to d

isco

unt p

ost-

empl

oym

ent

bene

fit o

blig

atio

ns a

re d

eter

min

ed b

y re

fere

nce

to m

arke

t yie

lds

on th

e hi

gh q

ualit

y co

rpor

ate

bond

s. G

over

nmen

t bon

ds y

ield

can

be

used

on

ly w

here

ther

e is

no

deep

mar

ket o

f hig

h qu

ality

cor

pora

te b

onds

.

| The New Axis of Financial Reporting � Ind AS and ICDS 15 RSM

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

Back to Content

IFRS

Ind

ASPa

rtic

ular

sus

ing

the

rate

det

erm

ined

by

refe

renc

e to

m

arke

t yie

lds

on h

igh

qual

ity c

orpo

rate

bon

ds.

Gov

ernm

ent

Gra

nts

Ind

AS 2

0 re

quire

s m

easu

rem

ent o

f non

-m

onet

ary

gove

rnm

ent g

rant

s on

ly a

t the

ir fa

ir va

lue.

IAS

20 g

ives

an

optio

n to

mea

sure

non

-m

onet

ary

gove

rnm

ent g

rant

s ei

ther

at t

heir

fair

valu

e or

at n

omin

al v

alue

.In

d AS

20

does

not

per

mit

dedu

ctio

n of

the

gran

t in

arriv

ing

at th

e ca

rryi

ng a

mou

nt o

f the

as

set.

Thus

gra

nts

rela

ted

to a

sset

s, n

eeds

to

be a

ccou

nted

as

defe

rred

inco

me

only

.

IAS

20 g

ives

an

optio

n to

pre

sent

the

gran

ts

rela

ted

to a

sset

s, in

clud

ing

non-

mon

etar

y gr

ants

at f

air v

alue

in th

e ba

lanc

e sh

eet e

ither

by

set

ting

up th

e gr

ant a

s de

ferr

ed in

com

e or

by

dedu

ctin

g th

e gr

ant i

n ar

rivin

g at

the

carr

ying

am

ount

of t

he a

sset

.Ef

fect

s of

Ch

ange

s in

Fo

reig

n Ex

chan

ge R

ate

Whe

n th

ere

is a

cha

nge

in fu

nctio

nal c

urre

ncy,

In

d AS

21 r

equi

res

disc

losu

re o

f tha

t fac

t and

the

reas

on fo

r the

cha

nge.

Add

ition

ally

Ind

AS 2

1 re

quire

s di

sclo

sure

of t

he d

ate

of c

hang

e in

fu

nctio

nal c

urre

ncy.

Whe

n th

ere

is a

cha

nge

in fu

nctio

nal c

urre

ncy,

IA

S 21

requ

ires

disc

losu

re o

f tha

t fac

t and

the

reas

on fo

r the

cha

nge

only

.

Ind

AS 2

1 has

bee

n am

ende

d to

sco

pe o

ut th

e lo

ng-t

erm

fore

ign

curr

ency

mon

etar

y ite

ms

for

whi

ch a

n en

tity

has

opte

d fo

r the

exe

mpt

ion

give

n in

Ind

AS 10

1.

IAS

21 d

o no

t pro

vide

for s

uch

scop

e ex

clus

ion

for l

ong-

term

fore

ign

curr

ency

mon

etar

y ite

ms.

Rela

ted

Part

y D

iscl

osur

esD

iscl

osur

e re

quire

men

t of I

nd A

S 24

, do

not

appl

y in

circ

umst

ance

s w

here

pro

vidi

ng s

uch

disc

losu

res

wou

ld c

onfli

ct w

ith th

e re

port

ing

entit

y�s

dutie

s of

con

fiden

tialit

y as

spe

cific

ally

re

quire

d in

term

s of

a s

tatu

te o

r by

any

regu

lato

r or s

imila

r com

pete

nt a

utho

rity

and

a st

atut

e or

a re

gula

tor o

r sim

ilar c

ompe

tent

IAS

24 d

oes

not p

rovi

de fo

r suc

h sc

ope

excl

usio

n.

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

|The New Axis of Financial Reporting � Ind AS and ICDS 16RSMBack to Content

IFRS

Ind

ASPa

rtic

ular

sau

thor

ity g

over

ning

an

entit

y pr

ohib

its th

e en

tity

to d

iscl

ose

cert

ain

info

rmat

ion

requ

ired

by th

e st

anda

rd.

Sepa

rate

Fi

nanc

ial

Stat

emen

ts

The

Com

pani

es A

ct m

anda

tes

prep

arat

ion

of

sepa

rate

fina

ncia

l sta

tem

ents

by

each

co

mpa

ny. A

ccor

ding

ly In

d AS

27

has

rem

oved

re

quire

men

t of d

iscl

osin

g th

e re

ason

for

prep

arin

g se

para

te fi

nanc

ial s

tate

men

ts if

not

re

quire

d by

law

.

IAS

27 re

quire

s ce

rtai

n cl

ass

of e

ntity

bei

ng a

Pa

rent

or i

nves

tor w

ith jo

int c

ontr

ol o

f or

sign

ifica

nt in

fluen

ce o

ver,

an in

vest

ee to

di

sclo

se th

e re

ason

for p

repa

ring

sepa

rate

fin

anci

al s

tate

men

ts if

not

requ

ired

by la

w

Def

initi

on o

f clo

se m

embe

rs o

f the

fam

ily o

f a

pers

on a

s pe

r IFR

S is

am

ende

d to

incl

ude

brot

her,

sist

er, f

athe

r and

mot

her.

Clo

se m

embe

rs o

f the

fam

ily o

f a p

erso

n ar

e th

ose

fam

ily m

embe

rs w

ho m

ay b

e ex

pect

ed to

in

fluen

ce, o

r be

influ

ence

d by

, tha

t per

son

in

thei

r dea

lings

with

the

entit

y in

clud

ing:

(a) t

hat i

ndiv

idua

l�s d

omes

tic p

artn

er a

nd

ch

ildre

n,

(b) c

hild

ren

of th

e in

divi

dual

�s d

omes

tic p

artn

er;

an

d(c

) dep

enda

nts

of th

e in

divi

dual

or t

he

in

divi

dual

�s d

omes

tic p

artn

er.

Opt

ion

to u

se th

e eq

uity

met

hod

to a

ccou

nt fo

r in

vest

men

t in

subs

idia

ry, jo

int v

entu

re a

nd

asso

ciat

es in

sep

arat

e fin

anci

al s

tate

men

ts is

no

t giv

en in

Ind

AS 2

7.

IAS

27 a

llow

s th

e en

titie

s to

use

the

equi

ty

met

hod

to a

ccou

nt fo

r inv

estm

ent i

n su

bsid

iarie

s, jo

int v

entu

res

and

asso

ciat

es in

th

eir S

epar

ate

Fina

ncia

l Sta

tem

ents

(SFS

).

Inve

stm

ents

in

Ass

ocia

tes

and

Join

t Ven

ture

s

Ind

AS 2

8 re

quire

s us

e of

uni

form

acc

ount

ing

polic

ies,

unl

ess,

in c

ase

of a

n as

soci

ate,

it is

im

prac

ticab

le.

IAS

28 re

quire

s an

inve

stor

to m

ake

appr

opria

te

adju

stm

ents

to th

e as

soci

ate�

s fin

anci

al

stat

emen

ts to

con

form

them

to th

e in

vest

or�s

ac

coun

ting

polic

ies

for r

epor

ting

like

| The New Axis of Financial Reporting � Ind AS and ICDS 17 RSM

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

Back to Content

IFRS

Ind

ASPa

rtic

ular

s

Exce

ss o

f the

ent

ity�s

sha

re o

f the

net

fair

valu

e of

the

inve

stee

�s id

entif

iabl

e as

sets

and

lia

bilit

ies

over

the

cost

of t

he in

vest

men

t is

reco

gnis

ed d

irect

ly in

equ

ity a

s ca

pita

l res

erve

.

Exce

ss o

f the

ent

ity�s

sha

re o

f the

net

fair

valu

e of

the

inve

stee

�s id

entif

iabl

e as

sets

and

lia

bilit

ies

over

the

cost

of t

he in

vest

men

t is

reco

gnis

ed in

pro

fit o

r los

s.

Fina

ncia

l Re

port

ing

in

Hyp

erin

flatio

n-ar

y Ec

onom

ies

Ind

AS 2

9 re

quire

s an

add

ition

al d

iscl

osur

e re

gard

ing

the

dura

tion

of th

e hy

perin

flatio

nary

si

tuat

ion

exis

ting

in th

e ec

onom

y.

IAS

29 d

oes

not r

equi

re s

uch

a di

sclo

sure

.

Fina

ncia

l In

stru

men

ts:

Pres

enta

tion

As

an e

xcep

tion

to th

e de

finiti

on o

f �fin

anci

al

liabi

lity�

, Ind

AS 3

2 co

nsid

ers

the

equi

ty

conv

ersi

on o

ptio

n em

bedd

ed in

a c

onve

rtib

le

bond

den

omin

ated

in fo

reig

n cu

rren

cy to

ac

quire

a fi

xed

num

ber o

f ent

ity�s

ow

n eq

uity

in

stru

men

ts a

s an

equ

ity in

stru

men

t if t

he

exer

cise

pric

e is

fixe

d in

any

cur

renc

y.

This

exc

eptio

n to

the

defin

ition

of �

finan

cial

lia

bilit

y� is

not

pro

vide

d in

IAS

32.

Earn

ings

per

Sh

are

Ind

AS 3

3 is

app

licab

le to

all c

ompa

nies

that

ha

ve o

rdin

ary

shar

es a

nd a

re re

quire

d to

app

ly

Ind

AS.

IAS

33 is

app

licab

le to

ent

ity/

grou

p w

ith a

pa

rent

:i)

Who

se o

rdin

ary

shar

es o

r pot

entia

lly

or

dina

ry s

hare

s ar

e tr

aded

in p

ublic

mar

ket

(a

dom

estic

or f

orei

gn s

tock

exc

hang

e or

an

ov

er-t

he�

coun

ter m

arke

t, in

clud

ing

loca

l

and

regi

onal

mar

kets

); or

ii)

That

file

s or

is in

the

proc

ess

of fi

ling,

its

fin

anci

al s

tate

men

ts w

ith a

sec

uriti

es

co

mm

issi

on o

r oth

er re

gula

tory

tran

sact

ions

and

oth

er e

vent

s in

sim

ilar

circ

umst

ance

s.

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

|The New Axis of Financial Reporting � Ind AS and ICDS 18RSMBack to Content

IFRS

Ind

ASPa

rtic

ular

s

Inta

ngib

le

Ass

ets

Ind

AS 3

8 al

low

s on

ly fa

ir va

lue

for r

ecog

nisi

ng

the

inta

ngib

le a

sset

and

gra

nt in

acc

orda

nce

with

Ind

AS 2

0.

With

rega

rd to

the

acqu

isiti

on o

f an

inta

ngib

le

asse

t by

way

of a

gov

ernm

ent g

rant

, IAS

38,

Inta

ngib

le A

sset

s, p

rovi

des

the

optio

n to

an

entit

y to

reco

gnis

e bo

th a

sset

and

gra

nt in

itial

ly

at fa

ir va

lue

or a

t a n

omin

al a

mou

nt p

lus

any

expe

nditu

re th

at is

dire

ctly

att

ribut

able

to

prep

arin

g th

e as

set f

or it

s in

tend

ed u

se.

Ind

AS 3

3 re

quire

s EP

S re

late

d in

form

atio

n to

be

disc

lose

d bo

th in

con

solid

ated

fina

ncia

l st

atem

ents

and

sep

arat

e fin

anci

al

stat

emen

ts.

IAS

33 p

rovi

des

that

whe

n an

ent

ity p

rese

nts

both

con

solid

ated

fina

ncia

l sta

tem

ents

and

se

para

te fi

nanc

ial s

tate

men

ts, it

may

giv

e EP

S re

late

d in

form

atio

n in

con

solid

ated

fina

ncia

l st

atem

ents

onl

y.In

d AS

33

requ

ires

amou

nt o

f inc

ome

or

expe

nse

debi

ted

or c

redi

ted

to s

ecur

ities

pr

emiu

m a

ccou

nt/o

ther

rese

rves

(whi

ch is

ot

herw

ise

requ

ired

to b

e re

cogn

ised

in p

rofit

or

loss

in a

ccor

danc

e w

ith In

d A

ss) t

o be

adj

uste

d fr

om p

rofit

or l

oss

from

con

tinui

ng o

pera

tions

fo

r the

pur

pose

of c

alcu

latin

g ba

sic

EPS.

Such

situ

atio

n is

not

cov

ered

und

er IA

S 33

.

The

amor

tizat

ion

met

hod

spec

ified

in th

e st

anda

rd d

oes

not a

pply

to a

mor

tizat

ion

of

inta

ngib

le a

sset

s ar

isin

g fr

om s

ervi

ce

conc

essi

on a

rran

gem

ents

in re

spec

t of t

oll

road

s re

cogn

ised

in th

e fin

anci

al s

tate

men

ts o

f en

tity

befo

re t

he b

egin

ning

of t

he fi

rst I

nd A

S re

port

ing

perio

d of

the

entit

y.

IAS

38 d

oes

not c

onta

in s

uch

exem

ptio

n.

or

gani

satio

n fo

r the

pur

pose

of i

ssui

ng

or

dina

ry s

hare

s in

a p

ublic

mar

ket.

| The New Axis of Financial Reporting � Ind AS and ICDS 19 RSM

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

Back to Content

IFRS

Ind

ASPa

rtic

ular

sIn

vest

men

t Pr

oper

tyA

s pe

r Ind

AS

40 In

vest

men

t pro

pert

ies

are

acco

unte

d on

ly b

ased

on

the

cost

mod

el. F

air

valu

e m

odel

is n

ot p

erm

itted

.

IAS

40 p

erm

its b

oth

cost

mod

el a

nd fa

ir va

lue

mod

el (e

xcep

t in

som

e si

tuat

ions

) for

m

easu

rem

ent o

f inv

estm

ent p

rope

rtie

s af

ter

initi

al re

cogn

ition

.

Ind

AS a

lso

prov

ides

cer

tain

opt

iona

l exe

mpt

ion

rela

ting

to th

e lo

ng-t

erm

fore

ign

curr

ency

m

onet

ary

item

s an

d se

rvic

e co

nces

sion

ar

rang

emen

ts re

latin

g to

toll r

oads

.

IFRS

doe

s no

t pro

vide

any

opt

iona

l exe

mpt

ion

rela

ting

to th

e lo

ng-t

erm

fore

ign

curr

ency

m

onet

ary

item

s an

d se

rvic

e co

nces

sion

ar

rang

emen

ts re

latin

g to

toll r

oads

.

Firs

t-tim

e ad

optio

nA

s pe

r Ind

AS

101 a

n en

tity�

s fir

st In

d AS

fin

anci

al s

tate

men

ts a

re th

e fir

st a

nnua

l fin

anci

al s

tate

men

ts in

whi

ch th

e en

tity

adop

ts

Ind

ASs.

The

firs

t-tim

e ad

opte

r sha

ll acc

ount

for

the

resu

lting

cha

nge

in th

e re

tain

ed e

arni

ngs

as

at th

e tr

ansi

tion

date

exc

ept i

n ce

rtai

n sp

ecifi

c in

stan

ces

whe

re it

requ

ires

adju

stm

ent i

n Ca

pita

l res

erve

to th

e ex

tent

suc

h ad

just

men

t am

ount

doe

s no

t exc

eed

the

bala

nce

avai

labl

e in

Cap

ital r

eser

ve.

IFRS

1 pr

ovid

es v

ario

us e

xam

ples

of f

irst I

FRS

finan

cial

sta

tem

ents

. It a

lso

prov

ides

exa

mpl

es

of in

stan

ces

whe

n an

ent

ity d

oes

not a

pply

IF

RS 1.

The

firs

t-tim

e ad

opte

r sha

ll acc

ount

for

the

resu

lting

cha

nge

in th

e re

tain

ed e

arni

ngs

as

at th

e tr

ansi

tion

date

exc

ept i

n ce

rtai

n sp

ecifi

c in

stan

ces

whe

re it

requ

ires

adju

stm

ent i

n th

e go

odw

ill.

Busi

ness

Co

mbi

natio

nsIn

cas

e of

bus

ines

s co

mbi

natio

ns o

f ent

ities

un

der c

omm

on c

ontr

ol In

d AS

103

prov

ides

that

su

ch b

usin

ess

com

bina

tion

tran

sact

ions

sho

uld

be a

ccou

nted

for u

sing

the

pool

ing

of in

tere

st

met

hod.

IFRS

3 e

xclu

des

from

its

scop

e bu

sine

ss

com

bina

tions

of e

ntiti

es u

nder

com

mon

con

trol

.

Ind

AS 10

3 re

quire

s th

e ba

rgai

n pu

rcha

se to

be

reco

gnis

ed in

oth

er c

ompr

ehen

sive

inco

me

and

accu

mul

ated

in e

quity

as

capi

tal r

eser

ve, u

nles

s th

ere

is n

o cl

ear e

vide

nce

for t

he u

nder

lyin

g

IFRS

3 re

quire

s ba

rgai

n pu

rcha

se g

ain

aris

ing

on

busi

ness

com

bina

tion

to b

e re

cogn

ized

in p

rofit

or

loss

.

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

|The New Axis of Financial Reporting � Ind AS and ICDS 20RSMBack to Content

IFRS

Ind

ASPa

rtic

ular

s re

ason

for c

lass

ifica

tion

of th

e bu

sine

ss

com

bina

tion

as a

bar

gain

pur

chas

e, in

whi

ch

case

, it s

hall b

e re

cogn

ised

dire

ctly

in e

quity

as

capi

tal r

eser

ve.

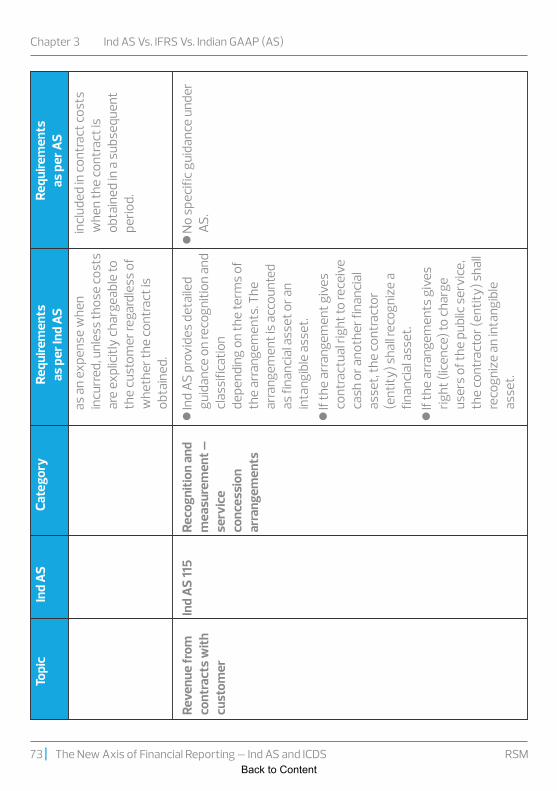

Reve

nue

from

co

ntra

cts

with

cu

stom

er

Und

er In

d AS

115,

pen

altie

s sh

ould

be

acco

unte

d fo

r as

per t

he s

ubst

ance

of t

he c

ontr

act.

Whe

re

the

pena

lty is

inhe

rent

in th

e de

term

inat

ion

of

tran

sact

ion

pric

e, it

sho

uld

form

par

t of v

aria

ble

cons

ider

atio

n, o

ther

wis

e th

e sa

me

shou

ld n

ot

be c

onsi

dere

d fo

r det

erm

inin

g th

e co

nsid

erat

ion

and

the

tran

sact

ion

pric

e sh

ould

con

side

red

as

fixed

.

IFRS

15 a

mou

nt o

f con

side

ratio

n, a

mon

g ot

her

thin

gs, c

an v

ary

beca

use

of p

enal

ties.

As

such

pe

nalti

es a

re re

quire

d to

be

cons

ider

ed in

de

term

inat

ion

of tr

ansa

ctio

n pr

ice.

Ind

AS 11

5 re

quire

s an

ent

ity to

pre

sent

se

para

tely

the

amou

nt o

f exc

ise

duty

incl

uded

in

the

reve

nue

reco

gnis

ed in

the

stat

emen

t of

prof

it an

d lo

ss.

IFRS

15 d

oes

not r

equi

re s

uch

disc

losu

re.

Ind

AS 11

5 re

quire

s to

pre

sent

reco

ncilia

tion

of

the

amou

nt o

f rev

enue

reco

gnis

ed in

the

stat

emen

t of p

rofit

and

loss

with

the

cont

ract

ed

pric

e sh

owin

g se

para

tely

eac

h of

the

adju

stm

ents

mad

e to

the

cont

ract

pric

e sp

ecify

ing

the

natu

re a

nd a

mou

nt o

f eac

h su

ch

adju

stm

ent s

epar

atel

y.

IFRS

15 d

oes

not r

equi

re s

uch

disc

losu

re.

| The New Axis of Financial Reporting � Ind AS and ICDS 21 RSM

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

Back to Content

3.3

Ind

AS V

s. A

S -

Key

Diff

eren

ces

Th

e ac

coun

ting

stan

dard

s as

spe

cifie

d in

the

Anne

xure

to th

e Co

mpa

nies

(Ind

ian

Acco

untin

g St

anda

rds)

Rul

es,

20

15 a

re c

alle

d th

e In

dian

Acc

ount

ing

Stan

dard

s (In

d AS

). T

he A

ccou

ntin

g st

anda

rds

as s

peci

fied

in A

nnex

ure

to

the

Com

pani

es (A

ccou

ntin

g St

anda

rds)

Rul

es, 2

006

are

refe

rred

as

AS in

this

sec

tion.

A

sum

mar

y of

key

diff

eren

ces

betw

een

som

e of

the

Ind

AS a

nd A

S is

giv

en h

ereu

nder

: Requ

irem

ents

as

per

AS

Cate

gory

Topi

c

Gen

eral

In

d AS

gen

eral

ly d

eals

with

pres

enta

tion

of fi

nanc

ial

st

atem

ents

.

Ind

ASRe

quire

men

ts

as p

er In

d AS

Ind

AS 1

Scop

e

AS

1 dea

ls o

nly

with

disc

losu

re o

f acc

ount

ing

po

licie

s.

Com

plia

nce

with

G

AA

P

Ent

ities

sho

uld

mak

e an

ex

plic

it an

d un

rese

rved

st

atem

ent i

n th

e no

tes

that

th

e fin

anci

al s

tate

men

ts

com

ply

with

Ind

AS.

Ind

AS 1

Pres

enta

tion

and

Dis

clos

ure

T

here

is a

pre

sum

ptio

n th

at

finan

cial

sta

tem

ents

sho

uld

be p

repa

red

in c

ompl

ianc

e w

ith A

S to

giv

e a

true

and

fa

ir vi

ew.

A

n en

tity

cann

ot d

escr

ibe

finan

cial

sta

tem

ents

as

com

plyi

ng w

ith In

d AS

un

less

they

com

ply

with

all

the

requ

irem

ents

of e

ach

appl

icab

le s

tand

ard

and

inte

rpre

tatio

n.

N

on-c

ompl

ianc

e w

ith a

ny o

f th

e ap

plic

able

AS

need

s to

be

dis

clos

ed in

the

finan

cial

st

atem

ents

.

Com

pone

nts

of

Fina

ncia

l st

atem

ents

Fi

nanc

ial s

tate

men

ts

com

pris

e of

1.

Bala

nce

shee

t as

at th

e en

d

Ind

AS 1

Pres

enta

tion

and

Dis

clos

ure

T

he re

quire

men

ts fo

r the

fin

anci

al s

tate

men

ts a

re s

et

out u

nder

the

Act s

uch

as

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

|The New Axis of Financial Reporting � Ind AS and ICDS 22RSMBack to Content

Requ

irem

ents

as

per

AS

Cate

gory

Topi

cIn

d AS

Requ

irem

ents

as

per

Ind

AS

of

the

perio

d 2.

Sta

tem

ent o

f pro

fit a

nd lo

ss

for t

he p

erio

d3.

Sta

tem

ent o

f cha

nges

in

equi

ty fo

r the

per

iod

4. S

tate

men

t of c

ash

flow

for

the

perio

d 5.

Not

es c

ompr

isin

g a

sum

mar

y of

sig

nific

ant

acco

untin

g po

licie

s an

d ot

her e

xpla

nato

ry

info

rmat

ion

6. C

ompa

rativ

e in

form

atio

n in

re

spec

t of t

he p

rece

ding

pe

riod

7. B

alan

ce s

heet

as

at th

e be

ginn

ing

of th

e pr

eced

ing

perio

d w

hen

an e

ntity

ap

plie

s an

acc

ount

ing

polic

y re

tros

pect

ivel

y or

mak

es

rest

atem

ent o

r rec

lass

ifies

in

its

finan

cial

sta

tem

ents

.

Sc

hedu

le III

of t

he

Com

pani

es A

ct, 2

013.

Fi

nanc

ial s

tate

men

ts u

nder

th

e Co

mpa

nies

Act

, 201

3 in

clud

e:

- Ba

lanc

e sh

eet

- St

atem

ent o

f Pro

fit a

nd

Loss

- Ca

sh fl

ow s

tate

men

t (no

t m

anda

tory

for O

ne P

erso

n Co

mpa

ny, S

mal

l Com

pany

an

d D

orm

ant C

ompa

ny)

- Ac

coun

ting

polic

ies

and

Not

es to

fina

ncia

l st

atem

ents

.

Fair

pres

enta

tion

In

ext

rem

ely

rare

ci

rcum

stan

ces

in w

hich

m

anag

emen

t con

clud

es

Ind

AS 1

Pres

enta

tion

and

Dis

clos

ure

D

epar

ture

s fr

om A

S is

pe

rmitt

ed if

requ

ired

by la

w.

| The New Axis of Financial Reporting � Ind AS and ICDS 23 RSM

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

Back to Content

Requ

irem

ents

as

per

AS

Cate

gory

Topi

cIn

d AS

Requ

irem

ents

as

per

Ind

AS

re

quire

men

t in

an In

d AS

w

ould

be

so m

isle

adin

g th

at

it w

ould

con

flict

with

the

obje

ctiv

e of

fina

ncia

l st

atem

ents

set

out

in th

e Fr

amew

ork,

the

entit

y sh

all

depa

rt fr

om th

at

requ

irem

ent i

f the

rele

vant

re

gula

tory

fram

ewor

k re

quire

s, o

r oth

erw

ise

does

no

t pro

hibi

t, su

ch a

de

part

ure.

In

d AS

pre

scrib

es

disc

losu

res

in c

ase

an e

ntity

de

part

s fr

om a

requ

irem

ent

of In

d AS

.Ca

pita

l

An

entit

y sh

all d

iscl

ose

info

rmat

ion

that

ena

bles

us

ers

of it

s fin

anci

al

stat

emen

ts to

eva

luat

e th

e en

tity�

s ob

ject

ives

, pol

icie

s an

d pr

oces

ses

for m

anag

ing

capi

tal.

Ind

AS 1

Dis

clos

ure

A

S do

es n

ot re

quire

suc

h a

disc

losu

re.

Extr

a-or

dina

ry it

ems

A

n en

tity

shal

l not

pre

sent

an

y ite

ms

of in

com

e or

ex

pens

es a

s ex

trao

rdin

ary

item

s in

the

sepa

rate

of

Ind

AS 1

Dis

clos

ure

A

n en

tity

shou

ld d

iscl

ose

in

stat

emen

t of p

rofit

and

loss

an

y in

com

e or

exp

ense

s th

at a

rise

from

eve

nts

or

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

|The New Axis of Financial Reporting � Ind AS and ICDS 24RSMBack to Content

Requ

irem

ents

as

per

AS

Cate

gory

Topi

cIn

d AS

Requ

irem

ents

as

per

Ind

AS

Com

para

tives

A

n en

tity

shal

l dis

clos

e co

mpa

rativ

e in

form

atio

n in

re

spec

t of p

revi

ous

perio

d fo

r al

l am

ount

s re

port

ed in

cu

rren

t per

iod�

s fin

anci

al

stat

emen

ts.

A

n en

tity

shal

l als

o in

clud

e co

mpa

rativ

e in

form

atio

n fo

r na

rrat

ive

and

desc

riptiv

e in

form

atio

n w

hen

it is

re

leva

nt to

an

un

ders

tand

ing

of th

e

Ind

AS 1

Dis

clos

ure

A

n en

tity

shal

l dis

clos

e on

e ye

ar o

f com

para

tives

for a

ll nu

mer

ical

info

rmat

ion

in th

e fin

anci

al s

tate

men

ts.

tr

ansa

ctio

ns th

at a

re c

lear

ly

dist

inct

from

the

ordi

nary

ac

tiviti

es o

f the

ent

erpr

ise

and,

ther

efor

e, a

re n

ot

expe

cted

to re

cur

freq

uent

ly o

r reg

ular

ly a

s ex

trao

rdin

ary

item

s.

The

nat

ure

and

the

amou

nt

of e

ach

extr

aord

inar

y ite

m

shou

ld b

e se

para

tely

di

sclo

sed

in th

e pr

ofit

and

loss

acc

ount

in a

man

ner

that

its

impa

ct o

n cu

rren

t pr

ofit

or lo

ss c

an b

e pe

rcei

ved.

pr

ofit

and

loss

or i

n th

e no

tes.

| The New Axis of Financial Reporting � Ind AS and ICDS 25 RSM

Chapter 3 Ind AS Vs. IFRS Vs. Indian GAAP (AS)

Back to Content

Requ

irem

ents

as

per

AS

Cate

gory

Topi

cIn

d AS

Requ

irem

ents

as

per

Ind

AS

Cons

iste

ncy

of

pres

enta

tion

cr

itica

l judg

emen

ts a

nd

estim

ates

mad

e by

the

man

agem

ent i

n ap

plyi

ng

acco

untin

g po

licie

s.

Ind

AS 1

Pres

enta

tion

and

disc

losu

re

No

such

requ

irem

ent.

Prev

ious

yea

rs fi

gure

s ar

e re

grou

ped

/rec

lass

ified

to

corr

espo

nd w

ith th

e cu

rren

t ye

ar�s

cla

ssifi

catio

n /

disc

losu

re.

estim

ates

sp

ecifi

cally

requ

ires

such

di

sclo

sure

.

A

n en

tity

shal

l ret

ain

the

pres

enta

tion

and

clas

sific

atio

n of

item

s in

the

finan

cial

sta

tem

ents

from

on

e pe

riod

to a

noth

er

unle

ss th

e ch

ange

is

requ

ired

by In

d AS

or d

ue to

chan

ge in

nat

ure

of th

e en

tity�

s op

erat

ion

havi

ng

rega

rds

to th