icds - sirc of icai · ix borrowing costs- ca tg suresh- 98840 20900 icds sirc of icai - icds - ca...

TRANSCRIPT

IX Borrowing Costs- CA TG SURESH- 98840

20900

ICDS

SIRC of ICAI - ICDS - CA T G

SURESH

Borrowing Costs

Applicability:

Only for computation of income chargeable under the

head

• Profits and gains of business or profession or

• Income from other sources

Not for the purpose of maintenance of books of account.

SIRC of ICAI - ICDS - CA T G

SURESH

Borrowing Costs

Issue :

Entities borrow in order to finance their activities. They

incur borrowing cost.

• Is Always expensed out (or)

• Are there circumstances to justify capitalisation

SIRC of ICAI - ICDS - CA T G

SURESH

Borrowing Costs

Arguments For

• Better matching of cost to

benefit

• Inter-firm comparison

• Interest is treated like any

other production cost

Arguments Against

Benefit is the use of money

hence it should be charged

to revenue for the period in

which it uses the cash

Assets held at different cost

based on method of

financing

SIRC of ICAI - ICDS - CA T G

SURESH

Borrowing Costs

In case of conflict between Act and ICDS, Act will prevail

SIRC of ICAI - ICDS - CA T G

SURESH

Borrowing Costs

Relevant Provisions of the Income tax Act

1. Sec 36(1)(iii)

2. Expl 8 to Sec 43 (1)

3. Sec 43 A

(iii) the amount of the interest paid in respect of

capital borrowed for the purposes of the business or

profession :

Deduction u/s 36(1)(iii) will be allowed as deduction

irrespective of whether the asset is put to use or not. No

distinction between Revenue or capital in 36(1)(iii)

Monnet industries 350 ITR 304 DCIT V Core health

care (SC) Vardhaman polytex 25 taxman 281 SIRC of ICAI - ICDS - CA T G

SURESH

Borrowing Costs

Explanation 8.—For the removal of doubts, it is hereby

declared that where any amount is paid or is payable as

interest in connection with the acquisition of an asset,

so much of such amount as is relatable to any period

after such asset is first put to use shall not be included,

and shall be deemed never to have been included, in

the actual cost of such asset.

SIRC of ICAI - ICDS - CA T G

SURESH

Meaning of Borrowing cost

Interest and other costs incurred in connection with the

borrowing.

Includes:

Commitment charges on borrowings;

• Amortised discounts or premiums

• Amortised ancillary costs;

• Finance charges in respect of assets acquired under

finance leases.

SIRC of ICAI - ICDS - CA T G

SURESH

AS vs ICDS

AS-16

Provides that borrowing

costs may include exchange

rate differences to the

extent they are regarded as

an adjustment to interest

costs.

ICDS-IX

This provision has been

removed in the ICDS.

Exchange differences arising

from foreign currency

borrowings are added or

reduced from the actual

cost of the asset on

payment basis u/s 43 A

SIRC of ICAI - ICDS - CA T G

SURESH

Meaning of Qualifying asset

Tangible Assets

Land, building, machinery, plant or furniture

Intangible Assets

Know-how, patents, copyrights, trade marks, licences,

franchises or any other business or commercial right

Inventories

If it requires a period of 12 months or more to bring them to

a saleable condition.

Capitalisation in the context of inventory means addition of

borrowing cost to the cost of inventory.

SIRC of ICAI - ICDS - CA T G

SURESH

AS vs ICDS

AS-16

QA is an asset that

necessarily takes a

substantial period of time

to get ready for its

intended use or sale.

ICDS-IX

Except Inventory no time

limit is prescribed for QA.

SIRC of ICAI - ICDS - CA T G

SURESH

Treatment of Borrowing cost

On Qualifying Asset will be added to the cost of Qualifying

asset.

On Other than Qualifying asset

Treated as per the provisions of the Income tax Act .

Note: The amount of borrowing costs eligible for

capitalisation shall be determined in accordance with this

ICDS.

SIRC of ICAI - ICDS - CA T G

SURESH

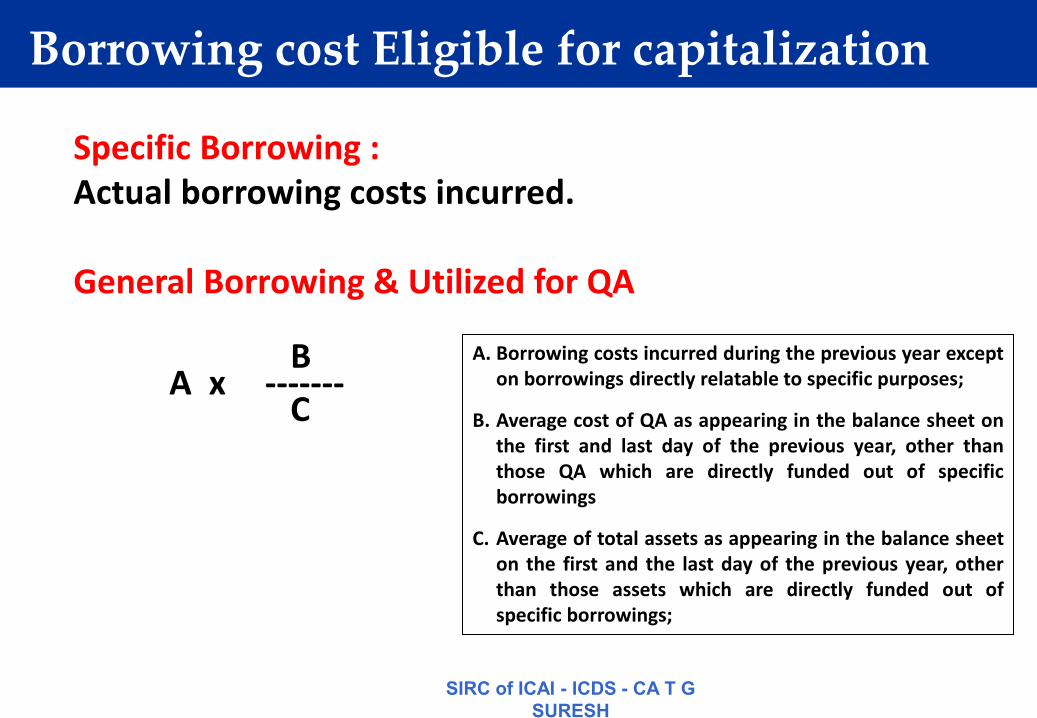

Borrowing cost Eligible for capitalization

Specific Borrowing :

Actual borrowing costs incurred.

General Borrowing & Utilized for QA

B A x ------- C

A. Borrowing costs incurred during the previous year except

on borrowings directly relatable to specific purposes;

B. Average cost of QA as appearing in the balance sheet on

the first and last day of the previous year, other than

those QA which are directly funded out of specific

borrowings

C. Average of total assets as appearing in the balance sheet

on the first and the last day of the previous year, other

than those assets which are directly funded out of

specific borrowings;

SIRC of ICAI - ICDS - CA T G

SURESH

AS vs ICDS

AS-16

Judgment to be used for

determining whether

general borrowings have

been utilized to fund

Qualifying Assets.

ICDS-IX

Provides a specific formula

for capitalizing borrowing

costs relating to general

borrowings.

SIRC of ICAI - ICDS - CA T G

SURESH

Commencement of Capitalization

Specific borrowing

From the date on which funds are borrowed;

General borrowing

From the date on which funds were utilised.

SIRC of ICAI - ICDS - CA T G

SURESH

Cessation of Capitalization

In case of tangible and Intangible assets

when such asset is first put to use;

In case of Inventory

when substantially all the activities necessary to prepare

such inventory for its intended sale are complete.

These will apply if the construction is done in parts and the

part completed is capable of being used while construction

continues for other parts.

SIRC of ICAI - ICDS - CA T G

SURESH

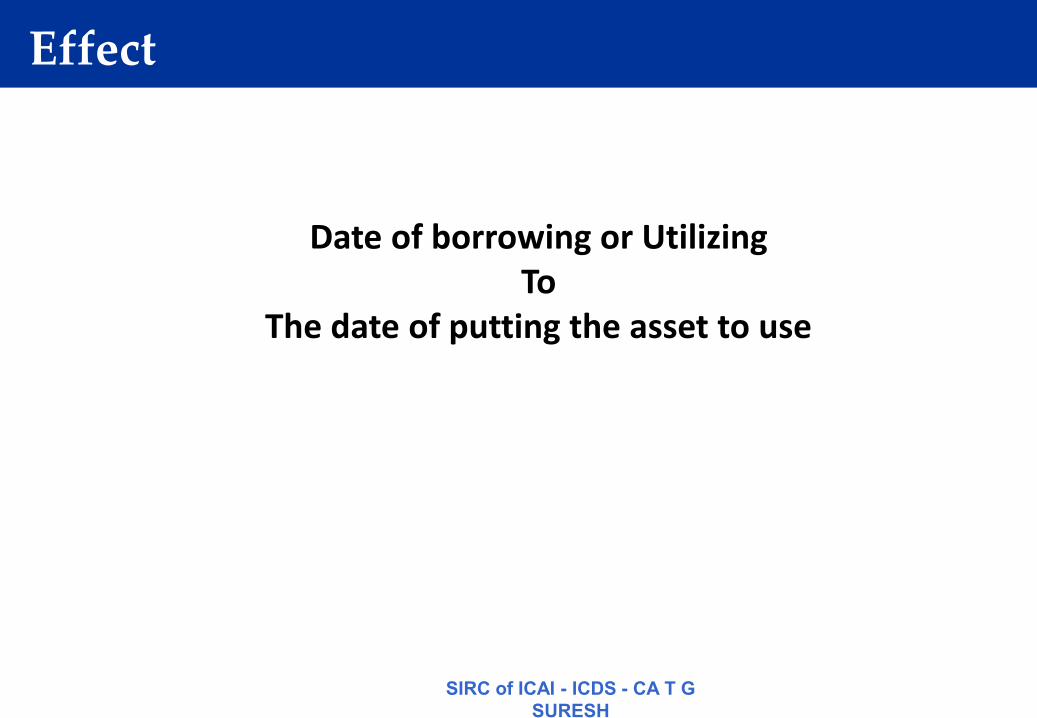

Effect

Date of borrowing or Utilizing

To

The date of putting the asset to use

SIRC of ICAI - ICDS - CA T G

SURESH

AS vs ICDS

AS-16

Borrowing costs on QA

should be capitalised when

it is probable that they will

result in future economic

benefits and can be reliably

measured.

ICDS-IX

This provision is removed.

SIRC of ICAI - ICDS - CA T G

SURESH

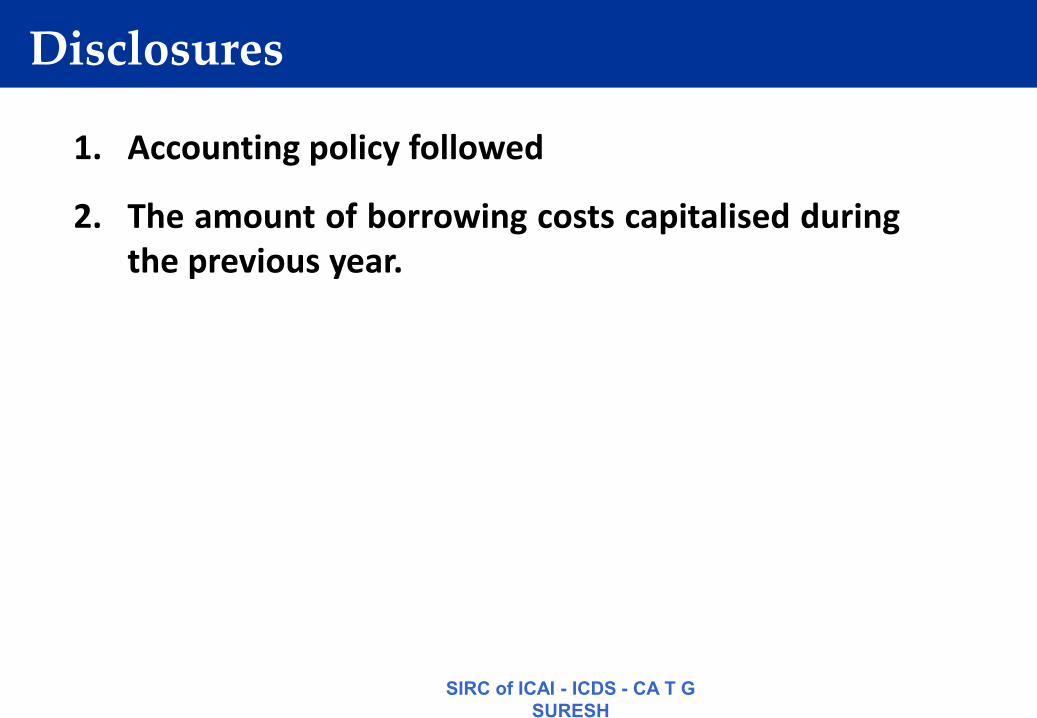

Disclosures

1. Accounting policy followed

2. The amount of borrowing costs capitalised during

the previous year.

SIRC of ICAI - ICDS - CA T G

SURESH

AS vs ICDS

AS-16

Income on temporary

investments of funds

borrowed should be

reduced from borrowing

costs eligible for

capitalization.

ICDS-IX

SC In Tuticorin Alakli &

Chemical 227 ITR 172 has

held that Interest Income

will be taxable under IOS

To align with judicial

precedents, this provision

is removed.

SIRC of ICAI - ICDS - CA T G

SURESH

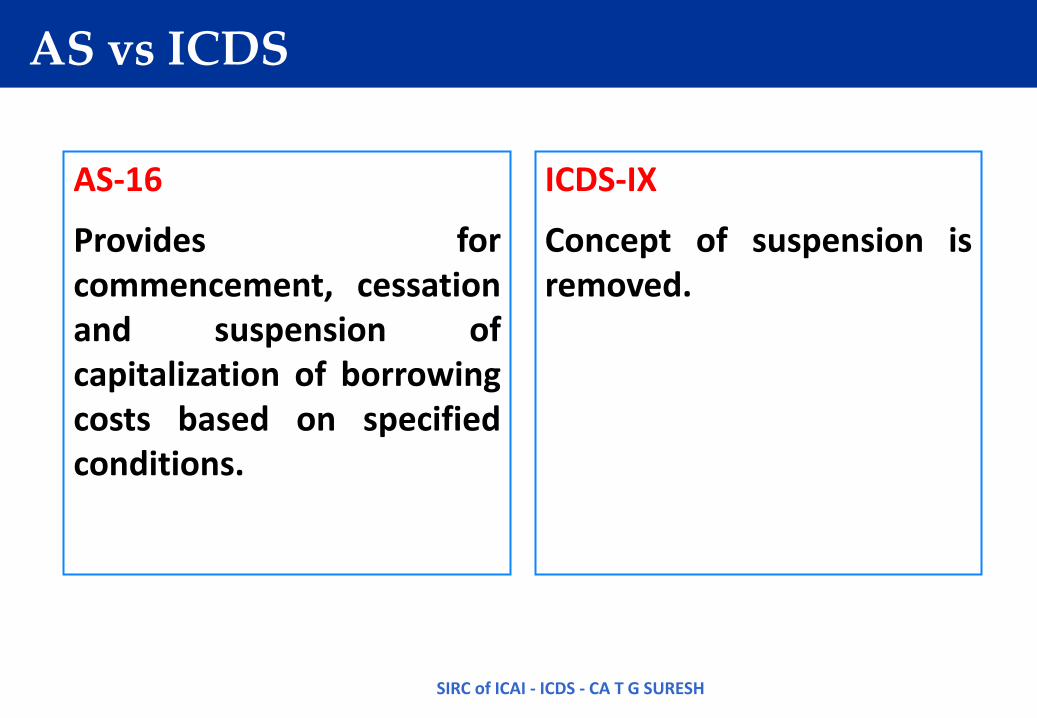

AS vs ICDS

AS-16

Provides for

commencement, cessation

and suspension of

capitalization of borrowing

costs based on specified

conditions.

ICDS-IX

Concept of suspension is

removed.

SIRC of ICAI - ICDS - CA T G SURESH

22

Clarifications from CBDT Question 20 : There arc specific provisions

in the Act read with Rules under which a

portion of borrowing cost may get

disallowed under sections like 14A, 43B,

40(a)(1), 40(a)(ia), 40A(2)(b), etc of the Act.

Whether borrowing costs to be capitalized

under ICDS-IX should exclude portion of

borrowing costs which gets disallowed

under such specific provisions?

SIRC of ICAI - ICDS - CA T G

SURESH

23

Clarifications from CBDT Answer : Since specific provisions of the Act

override the provisions of ICDS, it is clarified

that borrowing costs to be considered for

capitalization under ICDS-IX shall exclude those

borrowing costs which are disallowed under

specific provisions of the Act. Capitalization of

borrowing cost shall apply for that portion of the

borrowing cost which is otherwise allowable as

deduction under the Act.

SIRC of ICAI - ICDS - CA T G

SURESH

24

Clarifications from CBDT

Question 21 : Whether bill discounting

charges and other similar charges would

fall under the definition of borrowing cost?

Answer : The definition of borrowing cost is an

inclusive definition. Bill discounting charges

and other similar charges are covered as

borrowing cost.

SIRC of ICAI - ICDS - CA T G

SURESH

25

Clarifications from CBDT

Question 22 : How to allocate borrowing

costs relating to general borrowing

as computed in accordance with formula

provided under Para 6 of ICDS-IX to

different qualifying assets?

Answer : The capitalization of general

borrowing cost under ICDS-IX shall be done on

asset-by-asset basis.

SIRC of ICAI - ICDS - CA T G

SURESH