the lebanon weekly monitor - mofcomimages.mofcom.gov.cn/lb/accessory/201212/1355469125338.pdf ·...

TRANSCRIPT

1Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

Bank Audi sal - Audi Saradar Group - Group Research Department - Bank Audi Plaza - Bab Idriss - PO Box 11-2560 - Lebanon - Tel: 961 1 994 000 - email: [email protected]

CONTACTS

RESEARCH

Treasury & Capital Markets

Micky Chebli(961-1) [email protected]

Nadine Akkawi(961-1) [email protected]

Bechara Serhal(961-1) [email protected]

Private Banking

Toufic Aouad(961-1) [email protected]

Corporate Banking

Khalil Debs(961-1) [email protected]

Marwan Barakat(961-1) [email protected]

Jamil Naayem(961-1) [email protected]

Salma Saad Baba(961-1) [email protected]

Fadi Kanso(961-1) [email protected]

Nathalie Ghorayeb(961-1) [email protected]

Sarah Borgi(961-1) [email protected]

Marc Harb(961-1) [email protected]

Nivine Turyaki(961-1) [email protected]

LEBANON MARKETS: WEEK OF DECEMBER 03 - DECEMBER 09, 2012

The LEBANON WEEKLY MONITOR

Economy___________________________________________________________________________p.2 BANKING ACTIVITY GROWTH SUSTAINS COMPARATIVELY SLOWER PACE The latest statistics published by the Central Bank revealed that banking activity indicators managed to sustain a rising streak during the first ten months of 2012. Yet, the pace at which it is rising remains comparatively slower than that seen during previous years. Also in this issuep.3 External accounts still adversely affected by unstable politico-security conditions p.4 Lebanon’s reduced growth prospects remain amongst its main vulnerabilities, as per Moody’s

Surveys___________________________________________________________________________p.5 LEBANON’S RANK IMPROVES IN TRANSPARENCY INTERNATIONAL’S CORRUPTION PERCEPTION INDEXTransparency International released its 2012 corruption perception index (CPI) in which it revealed that Lebanon’s global rank improved by six notches from last year and its regional one was better by one notch. Also in this issuep.6 Standard Chartered foresees mild recovery for Lebanon in 2013

Corporate News___________________________________________________________________________p.7 CRÉDIT LIBANAIS’ NET PROFITS ALMOST STABLE AT US$ 51.2 MILLION IN THE FIRST NINE MONTHS OF 2012 Crédit Libanais announced net profits of US$ 51.2 million in the first nine months of 2012, up by a mere 0.2% from the first nine months of 2011.

Also in this issuep.7 BBAC’s net profits up by a yearly 22.7% to US$ 34.1 million in the first nine months of 2012p.8 First National Bank’s net profits at US$ 13.3 million in the first nine months of 2012 p.8 EuroMena and Syrian investors acquire Khoury family stake in Khoury Home

Markets In Brief___________________________________________________________________________p.9 NEW RECORD HIGH LEVEL OF BDL’S FOREIGN ASSETSLebanese capital markets saw a rising activity on the equity market, a sustained balanced activity on the FX market, and a local and foreign demand for Lebanese debt papers on the bond market. In details, the BSE price index rose by 0.3%, while the total trading value doubled to reach US$ 10 million due to cross trades on some banking stocks, noting that investors' appetite for Lebanese stocks remained weak within the context of the current prevailing uncertainties despite attractive market pricing ratios on the BSE relative to peer stock exchanges in the region. On the FX market, a balanced activity governed, with the LP/US$ interbank rate hovering between LP 1,510 and LP 1,514. The BDL’s latest bi-monthly balance sheet showed a growth in foreign assets of US$ 797 million during the second half of November 2012, driven by the cash proceeds of the latest Eurobond issue, hitting a new record high level of US$ 35.7 billion. As to the equity market, some local and foreign demand was observed on medium to long-term papers in relatively moderate volumes. This was met by adequate local offer. Lebanon’s five-year CDS spreads ranged between 420 and 440 bps.

2Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

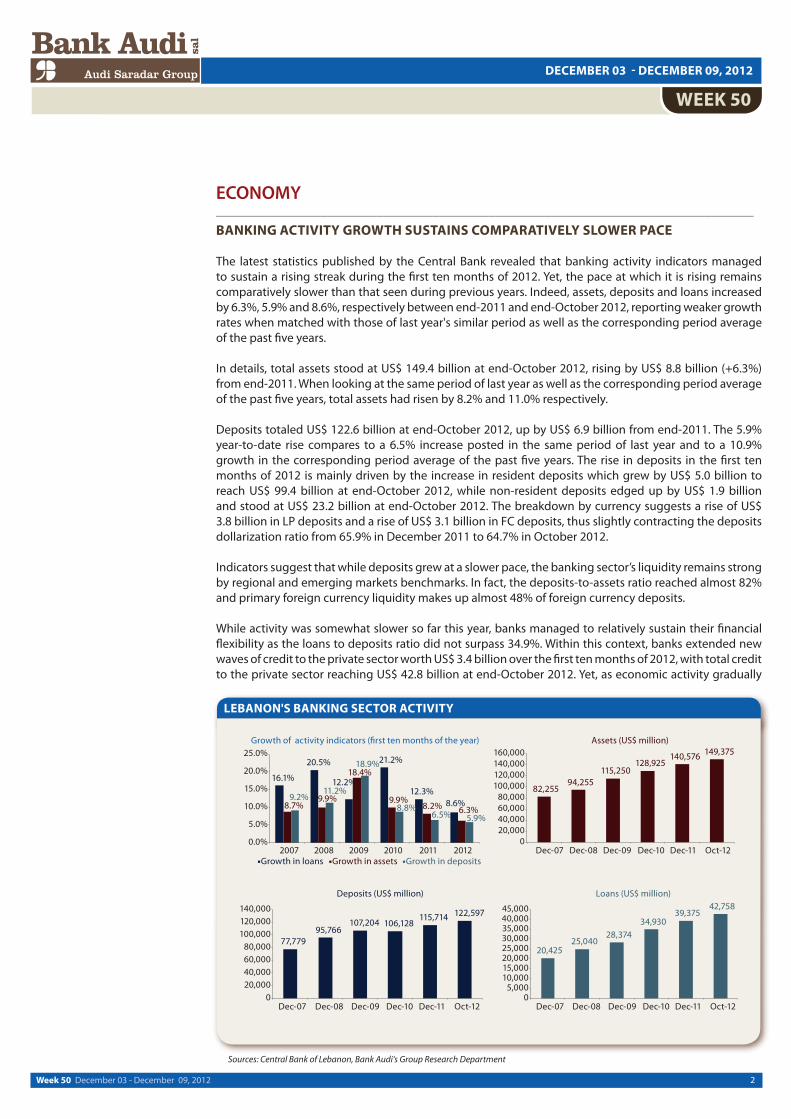

ECONOMY_____________________________________________________________________________BANKING ACTIVITY GROWTH SUSTAINS COMPARATIVELY SLOWER PACE

The latest statistics published by the Central Bank revealed that banking activity indicators managed to sustain a rising streak during the first ten months of 2012. Yet, the pace at which it is rising remains comparatively slower than that seen during previous years. Indeed, assets, deposits and loans increased by 6.3%, 5.9% and 8.6%, respectively between end-2011 and end-October 2012, reporting weaker growth rates when matched with those of last year's similar period as well as the corresponding period average of the past five years.

In details, total assets stood at US$ 149.4 billion at end-October 2012, rising by US$ 8.8 billion (+6.3%) from end-2011. When looking at the same period of last year as well as the corresponding period average of the past five years, total assets had risen by 8.2% and 11.0% respectively.

Deposits totaled US$ 122.6 billion at end-October 2012, up by US$ 6.9 billion from end-2011. The 5.9% year-to-date rise compares to a 6.5% increase posted in the same period of last year and to a 10.9% growth in the corresponding period average of the past five years. The rise in deposits in the first ten months of 2012 is mainly driven by the increase in resident deposits which grew by US$ 5.0 billion to reach US$ 99.4 billion at end-October 2012, while non-resident deposits edged up by US$ 1.9 billion and stood at US$ 23.2 billion at end-October 2012. The breakdown by currency suggests a rise of US$ 3.8 billion in LP deposits and a rise of US$ 3.1 billion in FC deposits, thus slightly contracting the deposits dollarization ratio from 65.9% in December 2011 to 64.7% in October 2012.

Indicators suggest that while deposits grew at a slower pace, the banking sector’s liquidity remains strong by regional and emerging markets benchmarks. In fact, the deposits-to-assets ratio reached almost 82% and primary foreign currency liquidity makes up almost 48% of foreign currency deposits.

While activity was somewhat slower so far this year, banks managed to relatively sustain their financial flexibility as the loans to deposits ratio did not surpass 34.9%. Within this context, banks extended new waves of credit to the private sector worth US$ 3.4 billion over the first ten months of 2012, with total credit to the private sector reaching US$ 42.8 billion at end-October 2012. Yet, as economic activity gradually

Sources: Central Bank of Lebanon, Bank Audi's Group Research Department

LEBANON'S BANKING SECTOR ACTIVITY

3Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

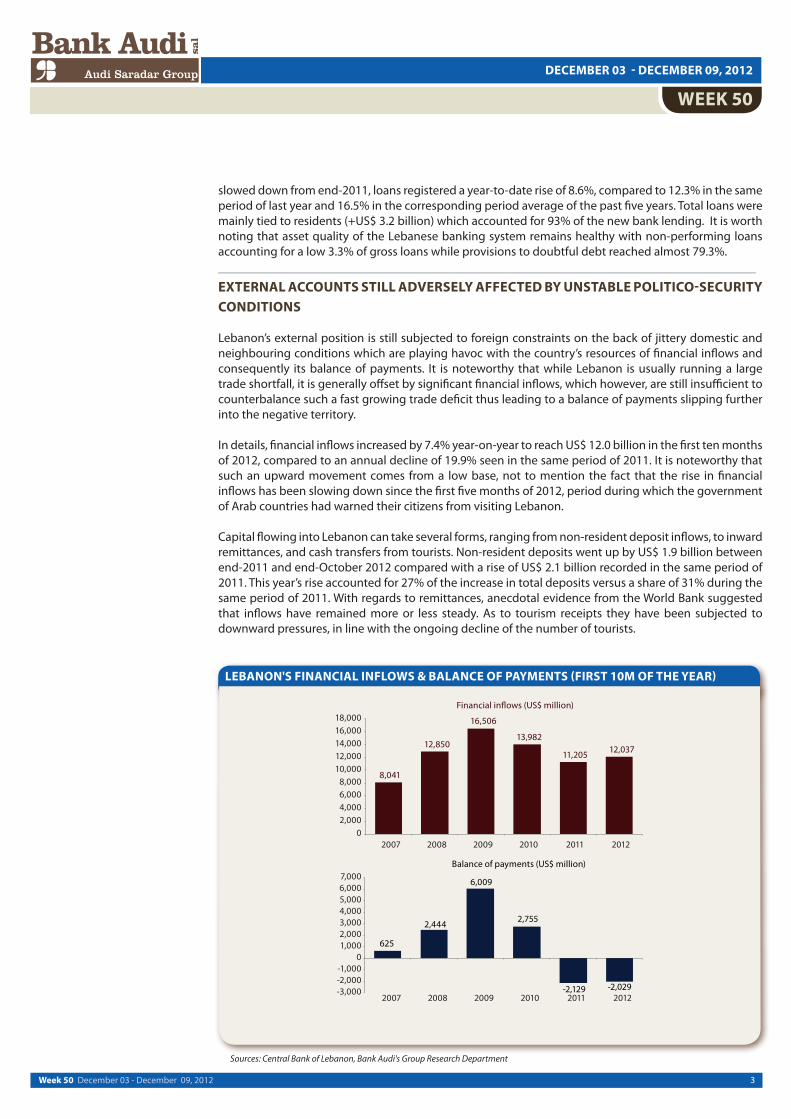

slowed down from end-2011, loans registered a year-to-date rise of 8.6%, compared to 12.3% in the same period of last year and 16.5% in the corresponding period average of the past five years. Total loans were mainly tied to residents (+US$ 3.2 billion) which accounted for 93% of the new bank lending. It is worth noting that asset quality of the Lebanese banking system remains healthy with non-performing loans accounting for a low 3.3% of gross loans while provisions to doubtful debt reached almost 79.3%. _____________________________________________________________________________EXTERNAL ACCOUNTS STILL ADVERSELY AFFECTED BY UNSTABLE POLITICO-SECURITY CONDITIONS

Lebanon’s external position is still subjected to foreign constraints on the back of jittery domestic and neighbouring conditions which are playing havoc with the country’s resources of financial inflows and consequently its balance of payments. It is noteworthy that while Lebanon is usually running a large trade shortfall, it is generally offset by significant financial inflows, which however, are still insufficient to counterbalance such a fast growing trade deficit thus leading to a balance of payments slipping further into the negative territory.

In details, financial inflows increased by 7.4% year-on-year to reach US$ 12.0 billion in the first ten months of 2012, compared to an annual decline of 19.9% seen in the same period of 2011. It is noteworthy that such an upward movement comes from a low base, not to mention the fact that the rise in financial inflows has been slowing down since the first five months of 2012, period during which the government of Arab countries had warned their citizens from visiting Lebanon.

Capital flowing into Lebanon can take several forms, ranging from non-resident deposit inflows, to inward remittances, and cash transfers from tourists. Non-resident deposits went up by US$ 1.9 billion between end-2011 and end-October 2012 compared with a rise of US$ 2.1 billion recorded in the same period of 2011. This year’s rise accounted for 27% of the increase in total deposits versus a share of 31% during the same period of 2011. With regards to remittances, anecdotal evidence from the World Bank suggested that inflows have remained more or less steady. As to tourism receipts they have been subjected to downward pressures, in line with the ongoing decline of the number of tourists.

Sources: Central Bank of Lebanon, Bank Audi's Group Research Department

LEBANON'S FINANCIAL INFLOWS & BALANCE OF PAYMENTS (FIRST 10M OF THE YEAR)

4Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

In parallel, the balance of payments account recorded a cumulative deficit of precisely US$ 2,029 million in the first ten months of 2012. That deficit compares to another shortfall of US$ 2,129 million over the corresponding period of 2011.

The deficit registered in the first ten months of the year is the result of a decline of US$ 2,854 million in net foreign assets of the Lebanese commercial banks, which was coupled with a rise of US$ 825 million in net foreign assets of the Central Bank of Lebanon.______________________________________________________________________________LEBANON’S REDUCED GROWTH PROSPECTS REMAIN AMONGST ITS MAIN VULNERABILITIES, AS PER MOODY’S

In its recent sovereign rating report on Lebanon, Moody’s placed Lebanon’s long-term sovereign foreign currency rating at “B1” with a “stable outlook”.

Lebanon's ratings reflect the country’s dimmed growth prospects, high, yet declining, level of debt coupled with the persistent twin deficits. The resilience of the Lebanese banking sector and its abundant foreign exchange liquidity are deemed as supportive factors for the ratings. Moody’s had previously upgraded Lebanon’s rating to "B1" in April 2010. Since then, improvements in the fiscal metrics were balanced by a weakened economic landscape affected by surrounding conflicts, as per Moody's.

As to Lebanon’s economic strength, Moody’s assesses it to be moderate relative to other sovereigns, reflecting the country’s small size, rising per capita income and fragile economic framework, as well as sensitivity to political factors.

As to institutional strength, Moody’s placed it at low, taking into account the World Bank’s governance indicators and Transparency International’s Corruption Perception Index, among others. The government financial strength was also placed at low, balancing a very high debt burden and large fiscal deficit with a favorable creditor base that poses limited rollover risk.

The fourth and last factor considered by Moody’s is the susceptibility to event risk where it assessed Lebanon at very high risk, reflecting the country’s vulnerability to adverse shocks that could materially impact the government’s creditworthiness.

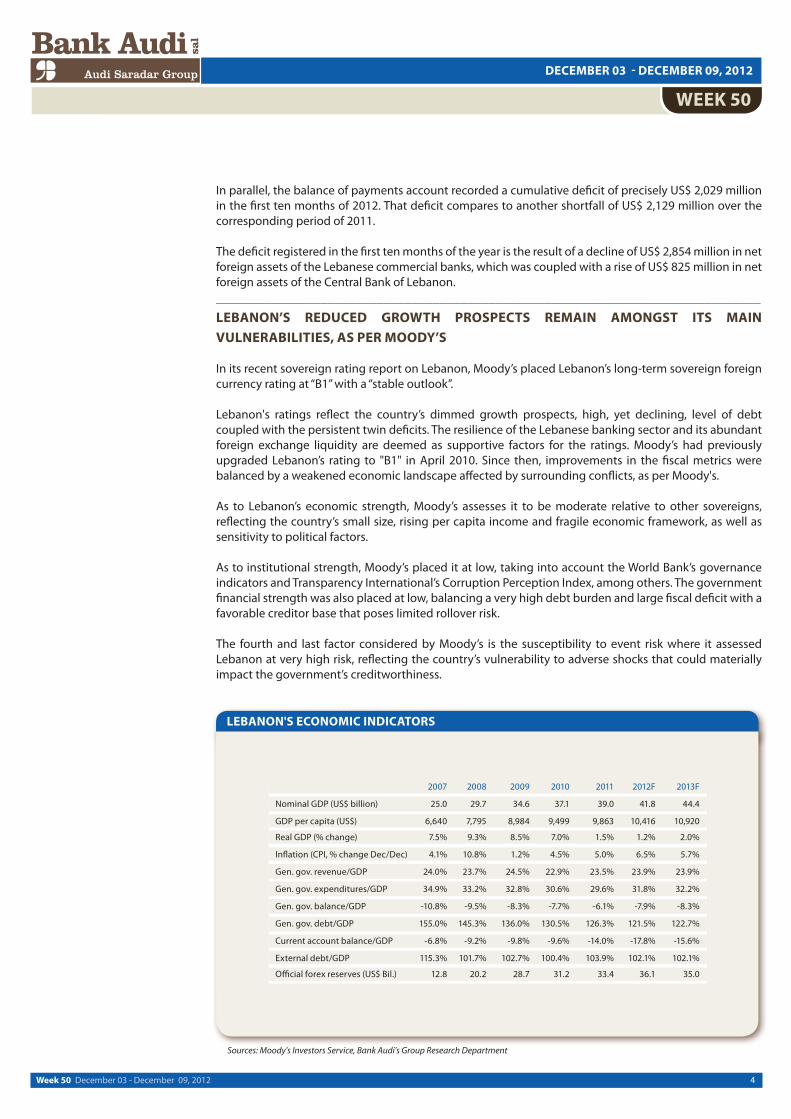

LEBANON'S ECONOMIC INDICATORS

Sources: Moody's Investors Service, Bank Audi's Group Research Department

5Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

SURVEYS_____________________________________________________________________________LEBANON’S RANK IMPROVES IN TRANSPARENCY INTERNATIONAL’S CORRUPTION PERCEPTION INDEX

Transparency International released its 2012 corruption perception index (CPI) in which it revealed that Lebanon’s global rank improved by six notches from last year and its regional one was better by one notch. Worldwide, Lebanon took the 128th position amongst 176 countries this year compared to the 134th one in 2011. In the MENA region, it was ranked 12th out of 17 countries against 13th in last year’s survey. Despite this progress, the need for enforced institutional oversight and legal frameworks coupled with effective regulation remains crucial for Lebanon. In fact, this would enhance the trust in public institutions, sustain economic growth and alleviate social differences as is the case for countries that perform most poorly in the CPI.

The Corruption Perceptions Index ranks countries according to their perceived levels of public-sector corruption and assigns scores ranging from a perfect 100 points for highly clean countries to zero for the most corrupt ones. The surveys and assessments used to compile the index include questions relating to the bribery of public officials, kickbacks in public procurement, embezzlement of public funds, and questions that probe the strength and effectiveness of public-sector anti-corruption efforts.

On a more positive note, Lebanon and Iraq posted the second best annual improvement (up by six notches globally), after Yemen and Libya (up by 8 notches each). It is also worth mentioning that while the average global ranking of MENA countries declined from last year, Lebanon was amongst the few economies to report an improvement. Lebanon’s score reached 30 over 100 this year while that of last year was at 2.5 points out of 10, as per the old methodology. Globally, it outperformed Togo, Cote d’Ivoire and Nicaragua while it came after Mozambique, Sierra Leone and Vietnam. Regionally, Lebanon ranked ahead of Syria, Yemen and Libya while it was surpassed by Morocco, Algeria and Egypt.

RANKING OF MENA COUNTRIES IN THE CPI

Sources: Transparency International, Bank Audi's Group Research Department

6Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

_____________________________________________________________________________STANDARD CHARTERED FORESEES MILD RECOVERY FOR LEBANON IN 2013

In its latest report, Standard Chartered indicated that 2013 should bring a mild recovery for the Lebanese economy, barring net political risks. Accordingly, Lebanon would record a real GDP growth of 2.5% in 2013, up from the 1.5% foreseen for 2012.

According to Standard Chartered, GDP growth drivers in the country (retail demand, tourism, and construction) are volatile, final demand has been affected in 2012, but will gradually recover as resilience and adaptability prevail. According to Standard Chartered, even in a manageable geopolitical environment, tourism is forecasted to suffer in summer 2013, affecting also the construction sector.

Regarding the banking sector, the report considered it to be disconnected from the health of the real economy and the political environment. Indeed, it proved resilient to most political shocks, with low NPLs and loan-to-deposit ratios and available necessary ammunition to support the sovereign debt.

The budget deficit remains a source of worry, with subsidies, mainly those to Electricité du Liban, increasing by 63% year-on-year in the first seven months, and, amidst the inability to increase State revenues as a result of political paralysis. As to the bonds’ markets, Standard Chartered sees limited potential for spreads to tighten from current levels over the next few months.

SELECTED LEBANON MACROECONOMIC INDICATORS

Sources: Standard Chartered Bank, Bank Audi's Group Research Department

7Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

CORPORATE NEWS_____________________________________________________________________________CRÉDIT LIBANAIS’ NET PROFITS ALMOST STABLE AT US$ 51.2 MILLION IN THE FIRST NINE MONTHS OF 2012

Crédit Libanais announced net profits of US$ 51.2 million in the first nine months of 2012, up by a mere 0.2% from the first nine months of 2011.

Net interest income amounted to US$ 94.7 million in the aforementioned period of 2012, rising by 4.8% from US$ 90.3 million recorded in the same period of 2011. Net fee and commission income totaled US$ 25.9 million in the first nine months of 2012 against US$ 22.4 million a year earlier.

Total operating income reached US$ 136.9 million in the first nine months of 2012, up by 13.0% year-on-year. Net operating income increased from US$ 124.2 million in the first nine months of 2011 to US$ 136.8 million in the same period of this year.

Crédit Libanais’ total operating expenses were higher by 19.1% annually to reach US$ 79.5 million in the first nine months of 2012, of which staff expenses totaling US$ 46.0 million (+17.2% year-on-year) and administrative and other expenses amounting to US$ 28.2 million (+21.0% year-on-year). The cost-to-income ratio reached 57.7% in the first nine months of 2012, against 54.8% in the same period of 2011.

Total assets stood at US$ 7.7 billion at end-September 2012, up by 7.6% from US$ 7.2 billion at end-2011. The Bank’s return on average assets remained almost unchanged annually, moving from 1.0% in the first nine months of 2011 to 0.9% in the same period of this year. Net loans and advances rose by 11.5% from US$ 2.0 billion at end-2011 to US$ 2.2 billion at end-September 2012. Crédit Libanais’ NPL-to-total loans ratio declined from 4.8% in the first nine months of 2011 to 4.6% in the same period of this year.

Customer deposits totaled US$ 6.7 billion at end-September 2012 against US$ 6.3 billion at end-2011. Shareholder’s equity posted an increase of 8.0% from US$ 488.7 million at end-2011 to reach US$ 527.9 million at end-September 2012. Return on average equity went down by from 14.0% in the first nine months of 2011 to 13.2% in the same period of this year. _____________________________________________________________________________BBAC’S NET PROFITS UP BY A YEARLY 22.7% TO US$ 34.1 MILLION IN THE FIRST NINE MONTHS OF 2012

BBAC’s net profits recorded an annual improvement of 22.7% to reach US$ 34.1 million in the first nine months of 2012, against US$ 27.8 million in the same period of 2011. It is worth noting that net provisions for credit losses moved from US$ 6.1 million in the first nine months of 2011 to US$ 2.8 million in the same period of this year.

Net interest income edged up by 25.9% from US$ 48.9 million in the first nine months of 2011 to US$ 61.6 million in the first nine months of this year. Net fee and commission income increased by 5.5% to US$ 12.6 million in the first nine months of 2012, from US$ 11.9 million a year earlier. Net operating income moved from US$ 75.6 million in the first nine months of 2011 to US$ 86.9 million in the same period of this year. BBAC’s interest margin was up from 1.6% in the first nine months of 2011 to 1.9% in the same period of this year.

Total operating expenses progressed by 11.0% annually to US$ 47.1 million in the first nine months of 2012, of which staff expenses amounting to US$ 24.8 million (+14.9% year-on-year) and administrative and other expenses totaling US$ 20.3 million (+7.2% year-on-year). Staff expenses accounted for 52.6% of operating expenses in the first nine months of 2012, against a share of 50.8% seen in the same period of 2011. The cost-to-income ratio declined from 61.1% in the first nine months of 2011 to 56.0% in the corresponding period of 2012.

Total assets stood at US$ 4.7 billion at end-September 2012, up by 8.8% from US$ 4.3 billion at end-2011. Loans and advances amounted to US$ 1.2 billion at end-September 2012, up by 9.3% from US$ 1.1 billion at end-2011. The return on average assets ratio was up from 0.9% in the first nine months of 2011 to 1.0% in the same period of this year.

8Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

Customer deposits reached US$ 4.2 billion at end-September 2012, up by 8.8% from US$ 3.8 billion at end-2011. Shareholders equity moved from US$ 319.1 million at end-2011 to US$ 373.1 million at end-September 2012. BBAC’s return on average equity rose from 11.8% in the first nine months of 2011 to 12.9% in the same period of this year.

The Bank’s loans-to-assets ratio increased from 23.8% in the first nine months of 2011 to 24.9% in the same period of this year. Its loans-to-deposits ratio moved from 27.5% in the aforementioned period of 2011 to 28.3% in the corresponding period of this year. _____________________________________________________________________________FIRST NATIONAL BANK’S NET PROFITS AT US$ 13.3 MILLION IN THE FIRST NINE MONTHS OF 2012

First National Bank announced consolidated net profits of US$ 13.3 million in the first nine months of 2012, up by 23.7% from US$ 10.7 million in the same period of 2011. Net provisions for operating expenses went up by more than two folds annually to US$ 4.0 million in the aforementioned period of 2011.

Net interest income increased by 21.9% from US$ 33.7 million in the first nine months of 2011 to US$ 41.1 million in the first nine months of 2012, while net commission earnings were almost constant over the covered period, reaching US$ 3.9 million in the first nine months of 2012.

Total operating income increased by a yearly 20.7% to reach US$ 51.0 million in the first nine months of 2012. Total operating expenses increased by 14.4%, moving from US$ 27.3 million in the first nine months of 2011 to US$ 31.3 million in the corresponding period of 2012, of which staff expenses amounted to US$ 16.6 million, up by 8.8% year-on-year, and other operating expenses totaled US$ 12.7 million, up by a yearly 23.8%.

Total assets reached US$ 3.3 billion at end-September 2012, against US$ 2.8 billion at year-end 2011. Loans to customers reached US$ 845.7 million at end-September 2012, against US$ 779.2 million at year-end 2011.

Customer deposits amounted to US$ 2.6 billion at end-September 2012, rising from US$ 2.3 billion at year-end 2011. Shareholders’ equity amounted to US$ 201.7 million at end-September 2012, up by 12.6% from end-2011. _____________________________________________________________________________EUROMENA AND SYRIAN INVESTORS ACQUIRE KHOURY FAMILY STAKE IN KHOURY HOME

Khoury Home Group announced that the Khoury family has sold all its shares in the entity to its two other shareholders.

Shares in the group were owned by the Khoury family (55%), Moussa Farhan (24%), and private equity firm EuroMena II (21%). The transaction included all companies of the group, which amount to around 27 entities.

The Khoury family has signed a Memorandum of Understanding, with a term sheet, with both partners Farhan and EuroMena II. This transaction is part of a larger one including real estate assets and other obligations and shares in other companies, as per newswires.

Farhan and EuroMena II will join their shares in one holding company that will control the majority of the group’s shares. The remaining shares will be held by a number of individual investors. The group will soon be forming a new board of directors with a new chairman. The partners already appointed a COO and a CFO eight months ago. Khoury Home is expected to keep its brand name and identity, at least for the near term. A change in the brand might occur along with regional expansion, as per newswires.

9Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

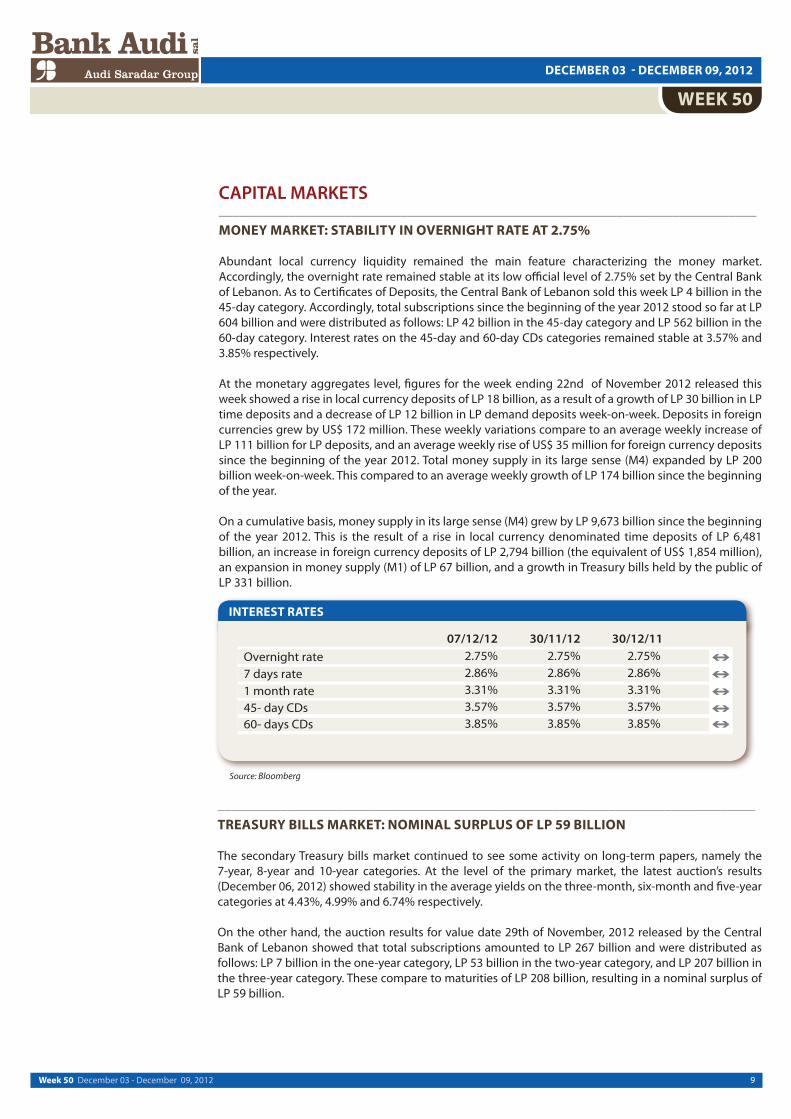

CAPITAL MARKETS_____________________________________________________________________________MONEY MARKET: STABILITY IN OVERNIGHT RATE AT 2.75%

Abundant local currency liquidity remained the main feature characterizing the money market. Accordingly, the overnight rate remained stable at its low official level of 2.75% set by the Central Bank of Lebanon. As to Certificates of Deposits, the Central Bank of Lebanon sold this week LP 4 billion in the 45-day category. Accordingly, total subscriptions since the beginning of the year 2012 stood so far at LP 604 billion and were distributed as follows: LP 42 billion in the 45-day category and LP 562 billion in the 60-day category. Interest rates on the 45-day and 60-day CDs categories remained stable at 3.57% and 3.85% respectively.

At the monetary aggregates level, figures for the week ending 22nd of November 2012 released this week showed a rise in local currency deposits of LP 18 billion, as a result of a growth of LP 30 billion in LP time deposits and a decrease of LP 12 billion in LP demand deposits week-on-week. Deposits in foreign currencies grew by US$ 172 million. These weekly variations compare to an average weekly increase of LP 111 billion for LP deposits, and an average weekly rise of US$ 35 million for foreign currency deposits since the beginning of the year 2012. Total money supply in its large sense (M4) expanded by LP 200 billion week-on-week. This compared to an average weekly growth of LP 174 billion since the beginning of the year.

On a cumulative basis, money supply in its large sense (M4) grew by LP 9,673 billion since the beginning of the year 2012. This is the result of a rise in local currency denominated time deposits of LP 6,481 billion, an increase in foreign currency deposits of LP 2,794 billion (the equivalent of US$ 1,854 million), an expansion in money supply (M1) of LP 67 billion, and a growth in Treasury bills held by the public of LP 331 billion.

_____________________________________________________________________________TREASURY BILLS MARKET: NOMINAL SURPLUS OF LP 59 BILLION

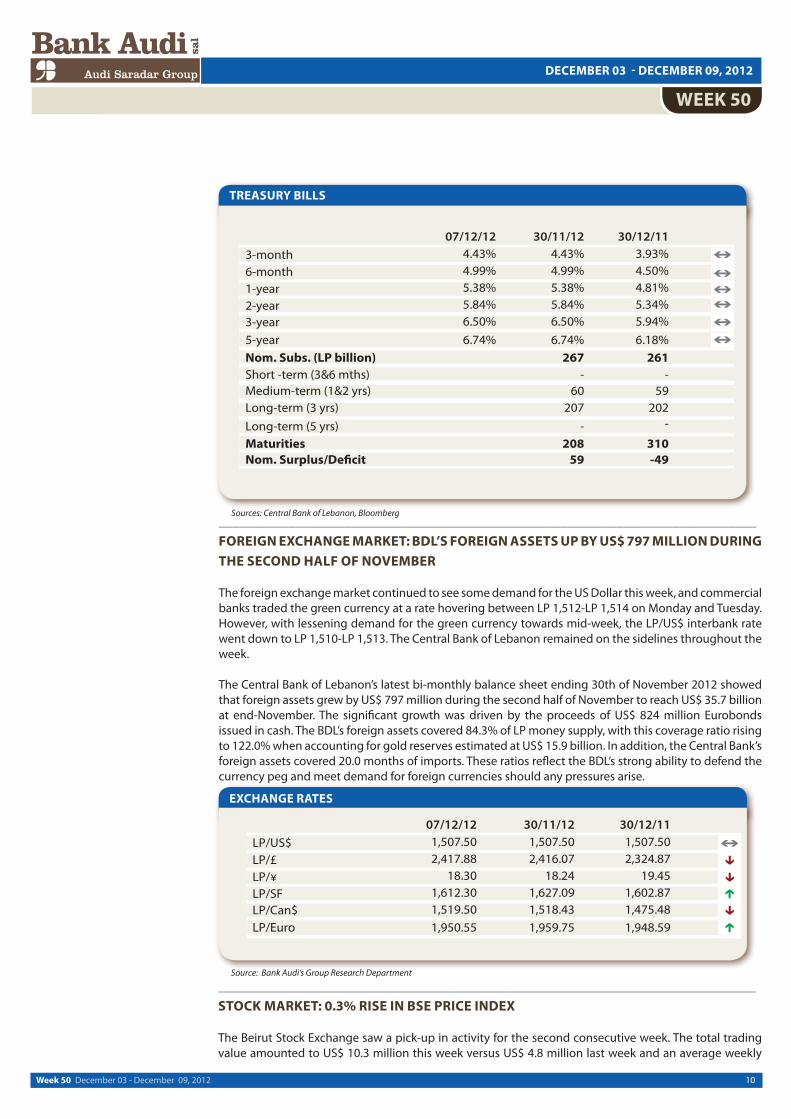

The secondary Treasury bills market continued to see some activity on long-term papers, namely the 7-year, 8-year and 10-year categories. At the level of the primary market, the latest auction’s results (December 06, 2012) showed stability in the average yields on the three-month, six-month and five-year categories at 4.43%, 4.99% and 6.74% respectively.

On the other hand, the auction results for value date 29th of November, 2012 released by the Central Bank of Lebanon showed that total subscriptions amounted to LP 267 billion and were distributed as follows: LP 7 billion in the one-year category, LP 53 billion in the two-year category, and LP 207 billion in the three-year category. These compare to maturities of LP 208 billion, resulting in a nominal surplus of LP 59 billion.

INTEREST RATES

Source: Bloomberg

10Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

TREASURY BILLS

Sources: Central Bank of Lebanon, Bloomberg_____________________________________________________________________________FOREIGN EXCHANGE MARKET: BDL’S FOREIGN ASSETS UP BY US$ 797 MILLION DURING THE SECOND HALF OF NOVEMBER

The foreign exchange market continued to see some demand for the US Dollar this week, and commercial banks traded the green currency at a rate hovering between LP 1,512-LP 1,514 on Monday and Tuesday. However, with lessening demand for the green currency towards mid-week, the LP/US$ interbank rate went down to LP 1,510-LP 1,513. The Central Bank of Lebanon remained on the sidelines throughout the week.

The Central Bank of Lebanon’s latest bi-monthly balance sheet ending 30th of November 2012 showed that foreign assets grew by US$ 797 million during the second half of November to reach US$ 35.7 billion at end-November. The significant growth was driven by the proceeds of US$ 824 million Eurobonds issued in cash. The BDL’s foreign assets covered 84.3% of LP money supply, with this coverage ratio rising to 122.0% when accounting for gold reserves estimated at US$ 15.9 billion. In addition, the Central Bank’s foreign assets covered 20.0 months of imports. These ratios reflect the BDL’s strong ability to defend the currency peg and meet demand for foreign currencies should any pressures arise.

EXCHANGE RATES

Source: Bank Audi’s Group Research Department

_____________________________________________________________________________STOCK MARKET: 0.3% RISE IN BSE PRICE INDEX

The Beirut Stock Exchange saw a pick-up in activity for the second consecutive week. The total trading value amounted to US$ 10.3 million this week versus US$ 4.8 million last week and an average weekly

11Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

EUROBONDS INDICATORS

Source: Bank Audi’s Group Research Department

AUDI INDICES FOR BSE

Sources: Beirut Stock Exchange, Bank Audi’s Group Research Department

trading value of US$ 7.7 million since the beginning of the year 2012. The average daily trading value increased from US$ 954 thousand last week to US$ 2,060 thousand this week, which resulted into a 116.0% surge in the trading volume index to close at 86.60.

Solidere shares accounted for 27.6% of activity. Solidere “A” share price edged down by 0.1% to US$ 12.26, while Solidere “B” share price increased by 0.8% to close at US$ 12.30. The banking shares captured 72.3% of the total trading value. Bank Audi’s “listed” share price rose by 1.8% to close at US$ 5.60. BLOM’s “listed” share price remained stable at US$ 7.40, and BLOM’s GDR price stood unchanged at US$ 7.80. Byblos Bank’s “listed” share price went up by 0.7% to US$ 1.51. Among the other listed securities, Holcim’s share price decreased by 1.9% to US$ 15.25.

All in all, the performance of the Beirut Stock Exchange was less favorable than that of other Arabian and emerging markets, as reflected by a 1.3% rise in the S&P Pan-Arab Composite Index and a 1.5% increase in the S&P Emerging Market Composite Index.

_____________________________________________________________________________BOND MARKET: AVERAGE SPREAD WIDENS BY 6 BPS WEEK-ON-WEEK

The Eurobond market saw some local trading activity on the US Dollar-denominated and Euro-denominated papers maturing in 2018, in addition to some local activity on papers maturing in 2023 and 2027. In parallel, foreign market players showed some demand for papers maturing in 2020 and 2027 that was met by adequate local offer. The average yield remained relatively stable at 4.43%, while the average spread widened by 6 bps to 355 bps due to declines in international benchmark yields. For instance, the five-year US Treasuries yield retreated slightly from 0.63% to 0.60% week-on-week. As to the cost of insuring debt, Lebanon’s five-year CDS spreads ranged between 420 and 440 bps versus 410-430 bps in the previous week.

12Week 50 December 03 - December 09, 2012

DECEMBER 03 - DECEMBER 09, 2012

WEEK 50

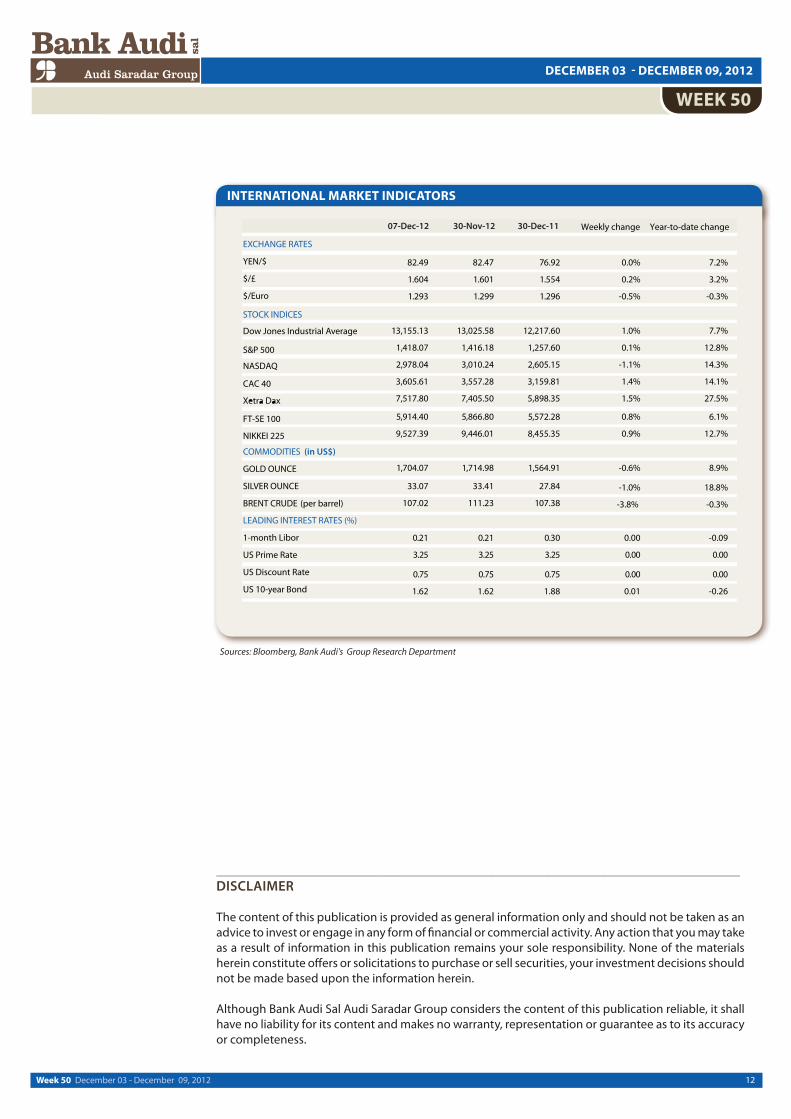

INTERNATIONAL MARKET INDICATORS

Sources: Bloomberg, Bank Audi's Group Research Department

___________________________________________________________________________DISCLAIMER

The content of this publication is provided as general information only and should not be taken as an advice to invest or engage in any form of financial or commercial activity. Any action that you may take as a result of information in this publication remains your sole responsibility. None of the materials herein constitute offers or solicitations to purchase or sell securities, your investment decisions should not be made based upon the information herein.

Although Bank Audi Sal Audi Saradar Group considers the content of this publication reliable, it shall have no liability for its content and makes no warranty, representation or guarantee as to its accuracy or completeness.