the italian insurance market - ice tokyo

TRANSCRIPT

The Italian Insurance Market2015 figures + 3M16 overview

September 2016

PwC

Italian insurance market snapshots

The Italian Insurance Market • 2015 figures + 3M16 overview

1

PwC

Section 1 – Italian insurance market snapshots

2

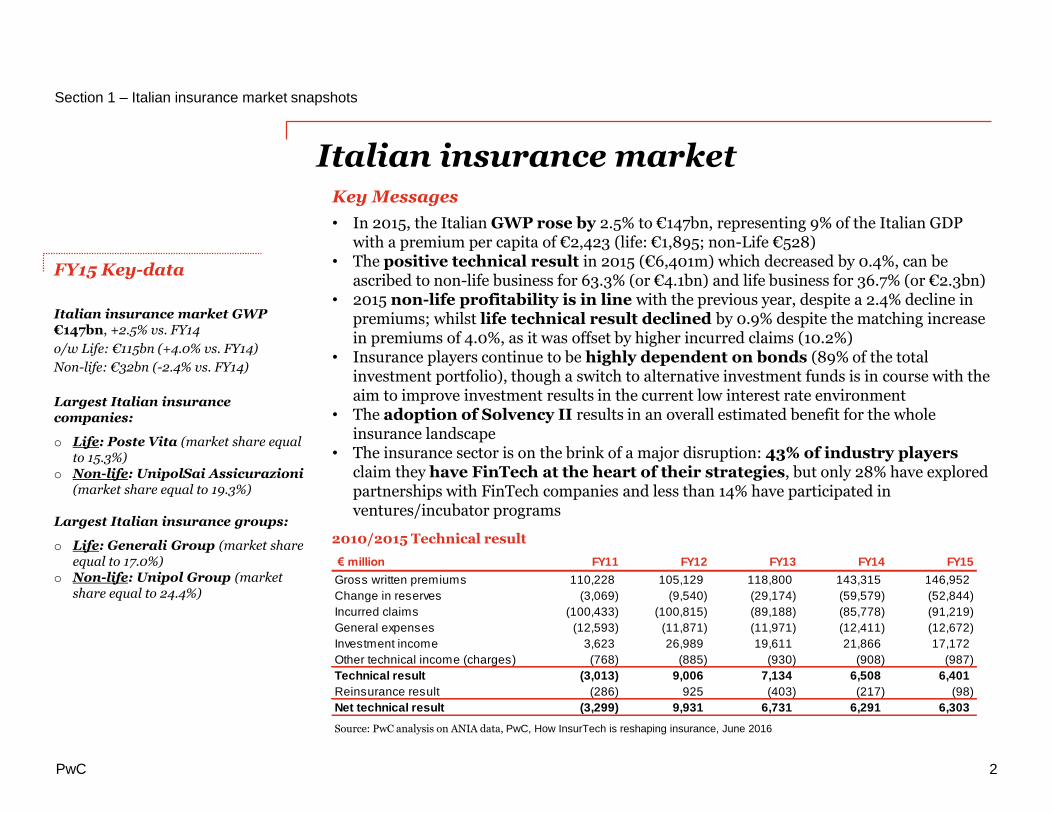

Italian insurance market

FY15 Key-data

Italian insurance market GWP €147bn, +2.5% vs. FY14

o/w Life: €115bn (+4.0% vs. FY14)

Non-life: €32bn (-2.4% vs. FY14)

Largest Italian insurance companies:

o Life: Poste Vita (market share equal to 15.3%)

o Non-life: UnipolSai Assicurazioni (market share equal to 19.3%)

Largest Italian insurance groups:

o Life: Generali Group (market share equal to 17.0%)

o Non-life: Unipol Group (market share equal to 24.4%)

Source: PwC analysis on ANIA data, PwC, How InsurTech is reshaping insurance, June 2016

Key Messages

• In 2015, the Italian GWP rose by 2.5% to €147bn, representing 9% of the Italian GDP with a premium per capita of €2,423 (life: €1,895; non-Life €528)

• The positive technical result in 2015 (€6,401m) which decreased by 0.4%, can be ascribed to non-life business for 63.3% (or €4.1bn) and life business for 36.7% (or €2.3bn)

• 2015 non-life profitability is in line with the previous year, despite a 2.4% decline in premiums; whilst life technical result declined by 0.9% despite the matching increase in premiums of 4.0%, as it was offset by higher incurred claims (10.2%)

• Insurance players continue to be highly dependent on bonds (89% of the total investment portfolio), though a switch to alternative investment funds is in course with the aim to improve investment results in the current low interest rate environment

• The adoption of Solvency II results in an overall estimated benefit for the whole insurance landscape

• The insurance sector is on the brink of a major disruption: 43% of industry players claim they have FinTech at the heart of their strategies, but only 28% have explored partnerships with FinTech companies and less than 14% have participated in ventures/incubator programs

2010/2015 Technical result

€ million FY11 FY12 FY13 FY14 FY15

Gross written premiums 110,228 105,129 118,800 143,315 146,952

Change in reserves (3,069) (9,540) (29,174) (59,579) (52,844)

Incurred claims (100,433) (100,815) (89,188) (85,778) (91,219)

General expenses (12,593) (11,871) (11,971) (12,411) (12,672)

Investment income 3,623 26,989 19,611 21,866 17,172

Other technical income (charges) (768) (885) (930) (908) (987)

Technical result (3,013) 9,006 7,134 6,508 6,401

Reinsurance result (286) 925 (403) (217) (98)

Net technical result (3,299) 9,931 6,731 6,291 6,303

PwC

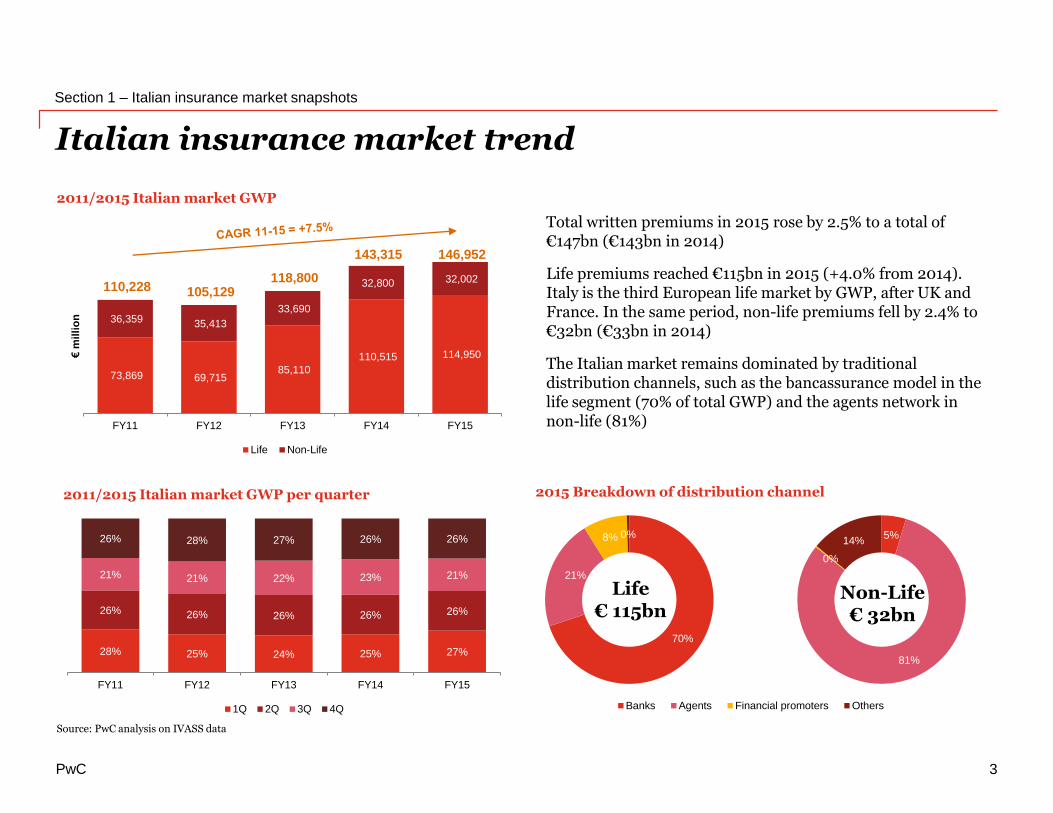

Italian insurance market trend

Section 1 – Italian insurance market snapshots

2011/2015 Italian market GWP

2015 Breakdown of distribution channel2011/2015 Italian market GWP per quarter

Non-life

Source: PwC analysis on IVASS data

Total written premiums in 2015 rose by 2.5% to a total of €147bn (€143bn in 2014)

Life premiums reached €115bn in 2015 (+4.0% from 2014). Italy is the third European life market by GWP, after UK and France. In the same period, non-life premiums fell by 2.4% to €32bn (€33bn in 2014)

The Italian market remains dominated by traditional distribution channels, such as the bancassurance model in the life segment (70% of total GWP) and the agents network in non-life (81%)

73,869 69,715 85,110

110,515 114,950

36,359 35,413

33,690

32,800 32,002 110,228 105,129

118,800

143,315 146,952

FY11 FY12 FY13 FY14 FY15

€m

illi

on

Life Non-Life

28% 25% 24% 25% 27%

26% 26% 26% 26% 26%

21% 21% 22% 23% 21%

26% 28% 27% 26% 26%

FY11 FY12 FY13 FY14 FY15

1Q 2Q 3Q 4Q

Life€ 115bn

Non-Life€ 32bn

70%

21%

8% 0% 5%

81%

0%

14%

5%

81%

0%

14%

Non-Life market - Breakdown per distribution channel FY14

Banks Agents Financial promoters Others

3

PwC

7,084

5,286

4,001

1,426 1,414

7,814

6,073

4,754

2,030 1,943

22.1%

16.5%

12.5%

4.5% 4.4%

24.4%

19.0%

14.9%

6.3% 6.1%

0%

5%

10%

15%

20%

25%

30%

35%

-

3,000

6,000

9,000

12,000

15,000

Mark

et

sh

are

GW

P (€

mil

lio

n)

18,145

15,087

7,709 7,1766,599

19,49418,145

15,087

8,4957,728

15.8%

13.1%

6.7%6.2% 5.7%

17.0%15.8%

13.1%

7.4%6.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

5,000

10,000

15,000

20,000

Mark

et

sh

are

GW

P (€

mil

lio

n)

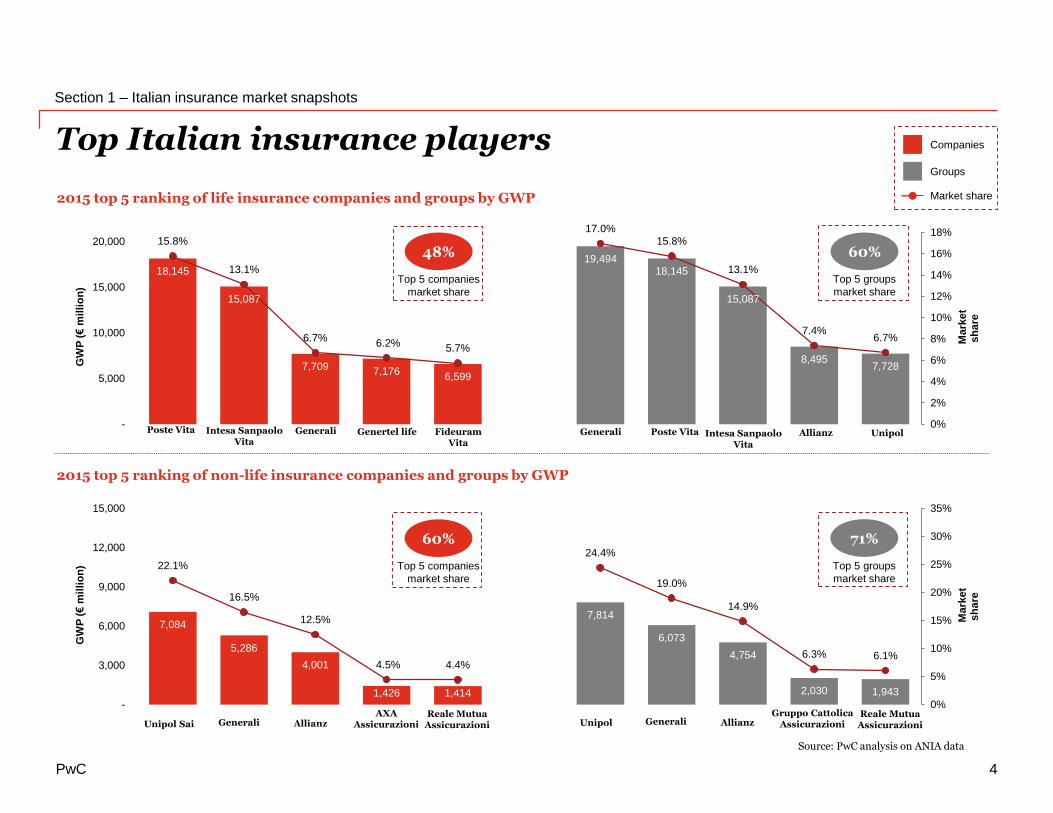

2015 top 5 ranking of life insurance companies and groups by GWP

Top Italian insurance players

Section 1 – Italian insurance market snapshots

4

2015 top 5 ranking of non-life insurance companies and groups by GWP

48%

Top 5 companies

market share

Source: PwC analysis on ANIA data

Poste Vita Genertel lifeIntesa Sanpaolo Vita

Generali FideuramVita

Generali Poste Vita Intesa Sanpaolo Vita

Allianz Unipol

Unipol Sai Generali AllianzAXA

Assicurazioni Unipol Generali AllianzGruppo Cattolica

AssicurazioniReale Mutua

AssicurazioniReale Mutua

Assicurazioni

60%

Top 5 groups

market share

60%

Top 5 companies

market share

71%

Top 5 groups

market share

Companies

Groups

Market share

PwC

191 182229 258

34713 68

4978

3

83

8894

119132

11

10 9

9 9

21

24 27

38 52

319 371

408

502

544

FY11 FY12 FY13 FY14 FY15

€b

illi

on

Investments

Section 1 – Italian insurance market snapshots

5

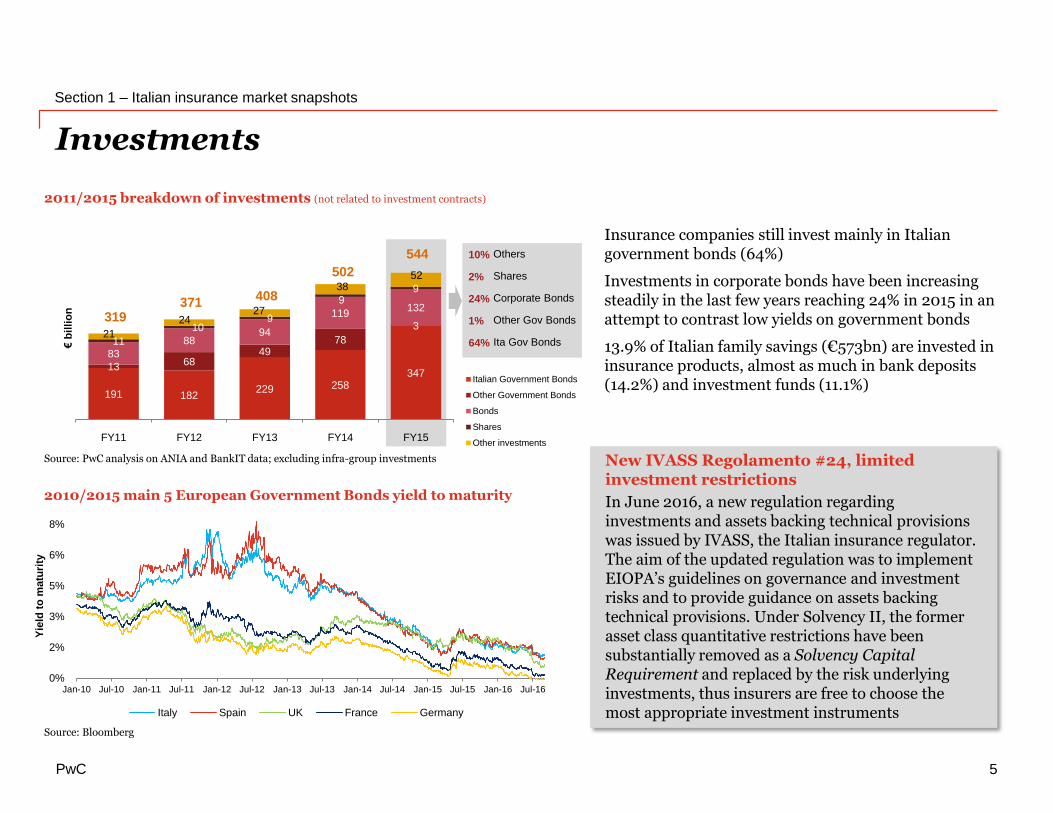

2011/2015 breakdown of investments (not related to investment contracts)

2010/2015 main 5 European Government Bonds yield to maturity

Source: Bloomberg

Source: PwC analysis on ANIA and BankIT data; excluding infra-group investments

64%

1%

24%

2%

10%

51%

15%

24%

2%

8%

Italian Government Bonds

Other Government Bonds

Bonds

Shares

Other investments

Insurance companies still invest mainly in Italian government bonds (64%)

Investments in corporate bonds have been increasing steadily in the last few years reaching 24% in 2015 in an attempt to contrast low yields on government bonds

13.9% of Italian family savings (€573bn) are invested in insurance products, almost as much in bank deposits (14.2%) and investment funds (11.1%)

New IVASS Regolamento #24, limited investment restrictions

In June 2016, a new regulation regarding investments and assets backing technical provisions was issued by IVASS, the Italian insurance regulator. The aim of the updated regulation was to implement EIOPA’s guidelines on governance and investment risks and to provide guidance on assets backing technical provisions. Under Solvency II, the former asset class quantitative restrictions have been substantially removed as a Solvency Capital Requirement and replaced by the risk underlying investments, thus insurers are free to choose the most appropriate investment instruments

Ita Gov Bonds

Other Gov Bonds

Corporate Bonds

Shares

Others

0%

2%

3%

5%

6%

8%

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Yie

ld t

o m

atu

rity

Italy Spain UK France Germany

PwC

(2%)

0%

2%

4%

6%

8%

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Yie

ld t

o m

atu

rity

BTP 10Y yield

Inflation rate

Avg segregated funds yield

Section 1 – Italian insurance market snapshots

6

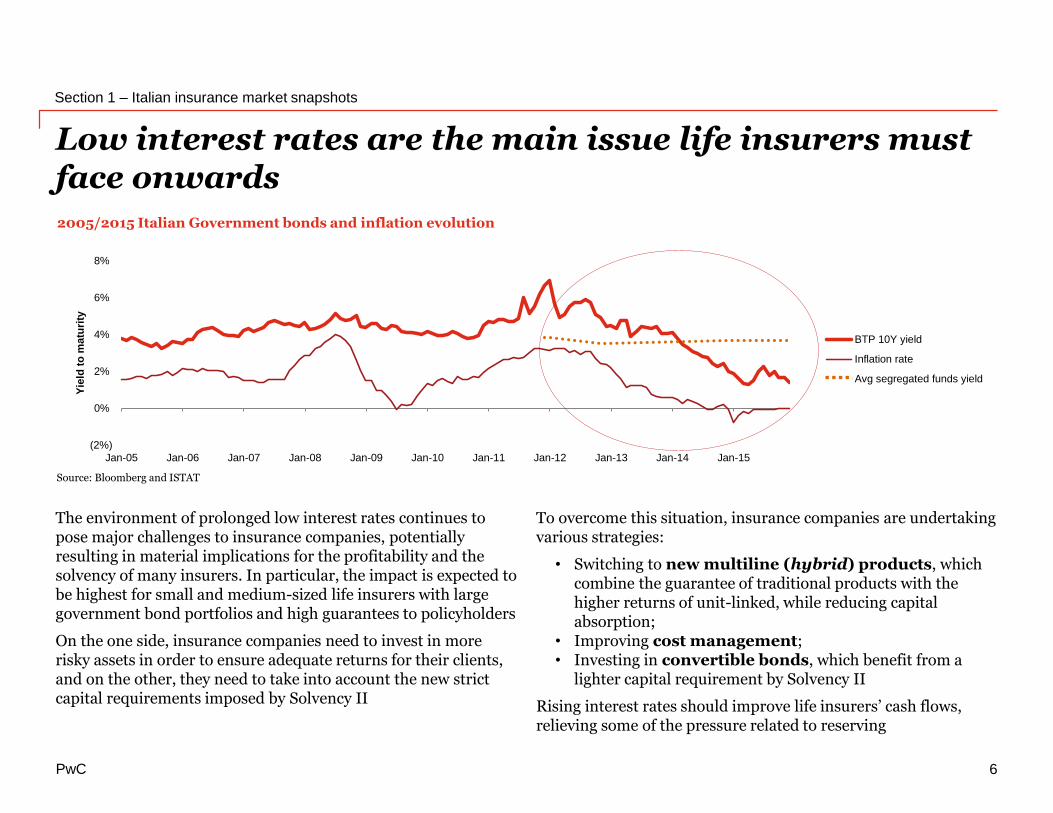

Low interest rates are the main issue life insurers must face onwards

2005/2015 Italian Government bonds and inflation evolution

Source: Bloomberg and ISTAT

The environment of prolonged low interest rates continues to pose major challenges to insurance companies, potentially resulting in material implications for the profitability and the solvency of many insurers. In particular, the impact is expected to be highest for small and medium-sized life insurers with large government bond portfolios and high guarantees to policyholders

On the one side, insurance companies need to invest in more risky assets in order to ensure adequate returns for their clients, and on the other, they need to take into account the new strict capital requirements imposed by Solvency II

To overcome this situation, insurance companies are undertaking various strategies:

• Switching to new multiline (hybrid) products, which combine the guarantee of traditional products with the higher returns of unit-linked, while reducing capital absorption;

• Improving cost management;• Investing in convertible bonds, which benefit from a

lighter capital requirement by Solvency II

Rising interest rates should improve life insurers’ cash flows, relieving some of the pressure related to reserving

PwC

Section 1 – Italian insurance market snapshots

7

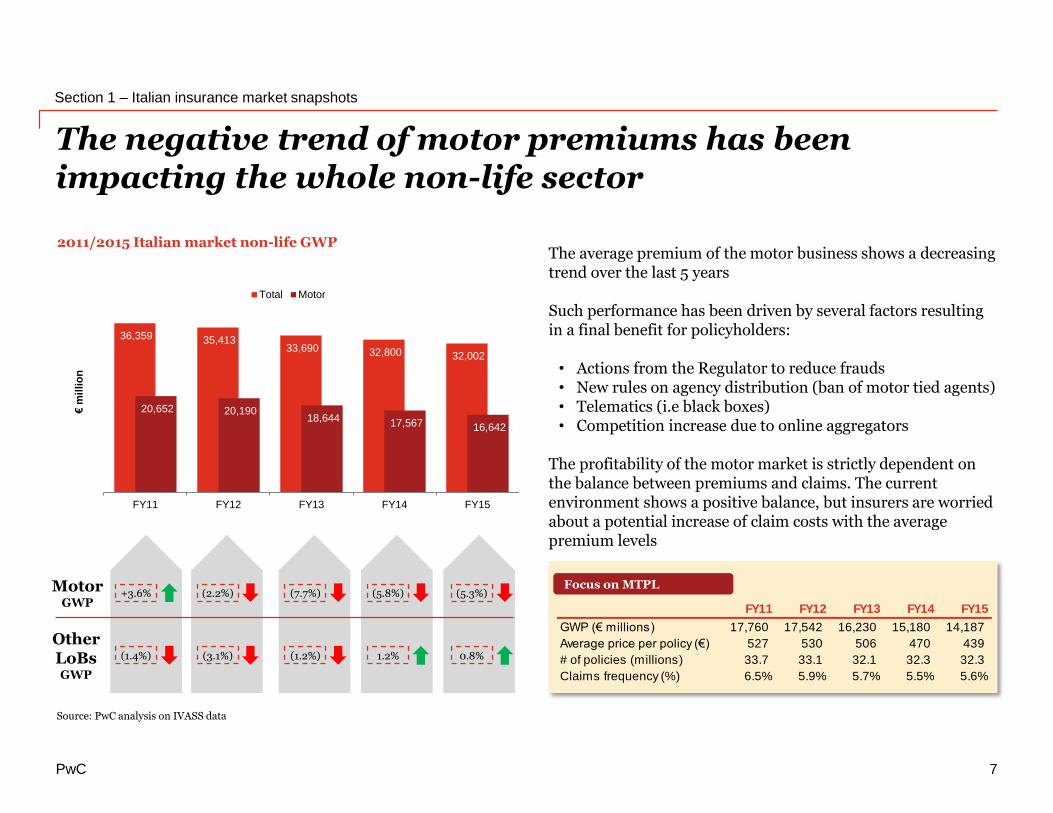

The negative trend of motor premiums has been impacting the whole non-life sector

2011/2015 Italian market non-life GWP

Source: PwC analysis on IVASS data

MotorGWP

OtherLoBsGWP

36,359 35,413 33,690 32,800 32,002

20,652 20,190 18,644 17,567 16,642

FY11 FY12 FY13 FY14 FY15

€m

illi

on

Total Motor

+3.6%

(1.4%)

(2.2%)

(3.1%)

(7.7%)

(1.2%)

(5.8%)

1.2%

(5.3%)

0.8%

The average premium of the motor business shows a decreasing trend over the last 5 years

Such performance has been driven by several factors resulting in a final benefit for policyholders:

• Actions from the Regulator to reduce frauds• New rules on agency distribution (ban of motor tied agents)• Telematics (i.e black boxes)• Competition increase due to online aggregators

The profitability of the motor market is strictly dependent on the balance between premiums and claims. The current environment shows a positive balance, but insurers are worried about a potential increase of claim costs with the average premium levels

FY11 FY12 FY13 FY14 FY15

GWP (€ millions) 17,760 17,542 16,230 15,180 14,187

Average price per policy (€) 527 530 506 470 439

# of policies (millions) 33.7 33.1 32.1 32.3 32.3

Claims frequency (%) 6.5% 5.9% 5.7% 5.5% 5.6%

Focus on MTPL

PwC

Italian life insurance market

The Italian Insurance Market • 2015 figures + 3M16 overview

8

PwC

Section 2 – Italian life insurance market

9

Italian life insurance market

2015 # of companies by GWP

GWP > €5bn €5bn-€1bn

€1bn-€0,1bn

€100m-€50m

< €50m

26

4

16

19

6

FY15 Key-data

Italian life insurance market GWP

€115bn, +4.0% vs. FY14

Life products distributed mainly through banking channel (70%)

Largest life insurance company:

Poste Vita (market share equal to 15%)

Largest life insurance group:

Generali Group (market share equal to 17%)

71 insurance companies operating in the life business (76 in 2014)

2010/2015 Life business technical result

Source: ANIA

Key Messages

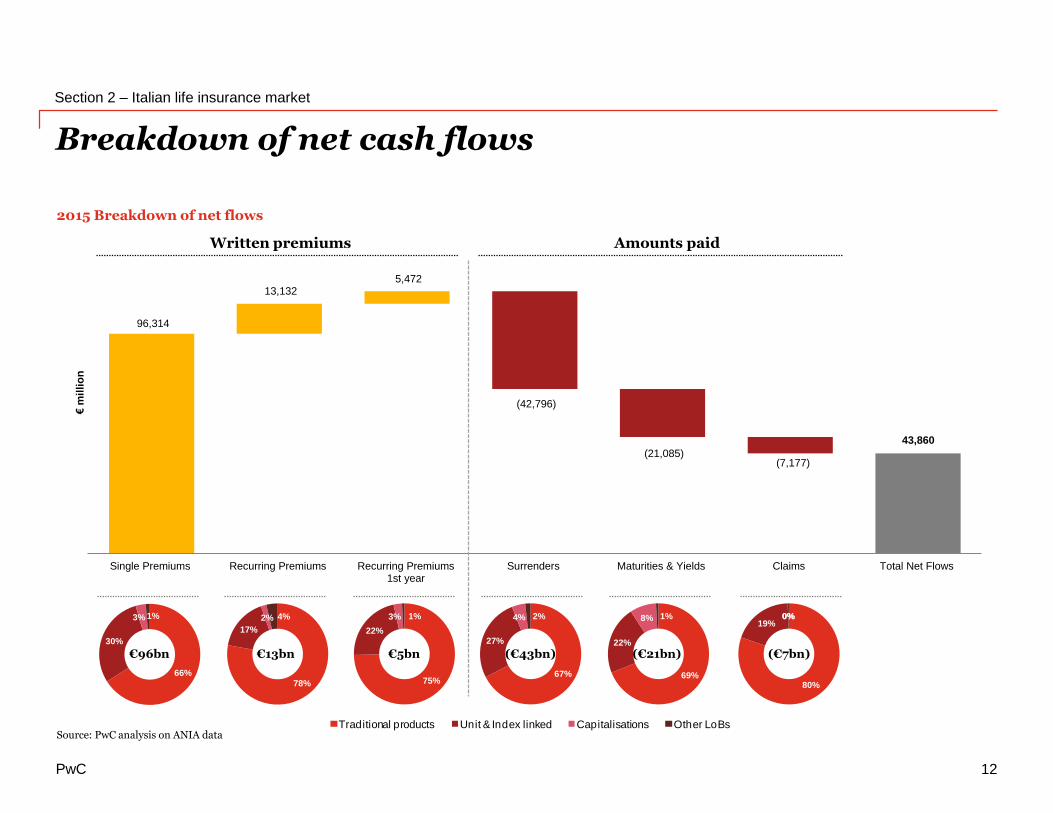

• The GWP of the Italian life insurance market increased by 4.0%, resulting in a record GWP of €115bn and net cash flow of €44bn (€46bn in 2014)

• 2015 technical result was positive (€2.3bn), however 0.9% lower than 2014 (€2.4bn) due to the increase in lapses which offset the increase in written premiums

• Italian families have invested €573bn of their own savings in life insurance products (13.9% of total savings)

• The market still shows a strong predominance of traditional products (68%), even though it decreased compared to 2014 (75%). The low interest rate environment and the introduction of Solvency II are likely to boost investment products, as already indicated by the strong growth of multi-line contracts (€22bn in 2015, an increase of 88% versus 2014), also called hybrid contracts

• Life premium penetration in Italy is 7.0% (premiums/GDP), the second highest in Europe after UK (8.5%)

• With the new solvency regime, the life segment may benefit of a higher solvency capital ratio (151.7%)

€ million FY11 FY12 FY13 FY14 FY15

Gross written premiums 73,869 69,715 85,110 110,515 114,950

Changes in technical provisions (2,547) (10,013) (29,928) (59,967) (53,024)

Lapses (Surrenders/ Maturities/ Claims) (73,971) (75,022) (66,788) (64,577) (71,196)

General expenses (3,832) (3,367) (3,538) (3,812) (3,970)

Investment income 3,019 25,382 18,409 20,588 15,976

Other technical income (charges) (177) (222) (325) (381) (388)

Technical result (3,639) 6,473 2,929 2,369 2,347

Reinsurance result 268 388 369 383 312

Net technical result (3,371) 6,861 3,298 2,752 2,659

PwC

73,869 69,71585,110

110,515 114,950

FY11 FY12 FY13 FY14 FY15

€m

illi

on

2011/2015 Italian market life GWP

Italian life insurance market trend

Section 2 – Italian life insurance market

10

2011/2015 Split between traditional & investment contracts

Source: PwC analysis on IVASS data

77%

73%

76%

75%

68%

23%

27%

24%

25%

32%

0% 20% 40% 60% 80% 100%

FY11

FY12

FY13

FY14

FY15

Traditional contracts Investment contracts

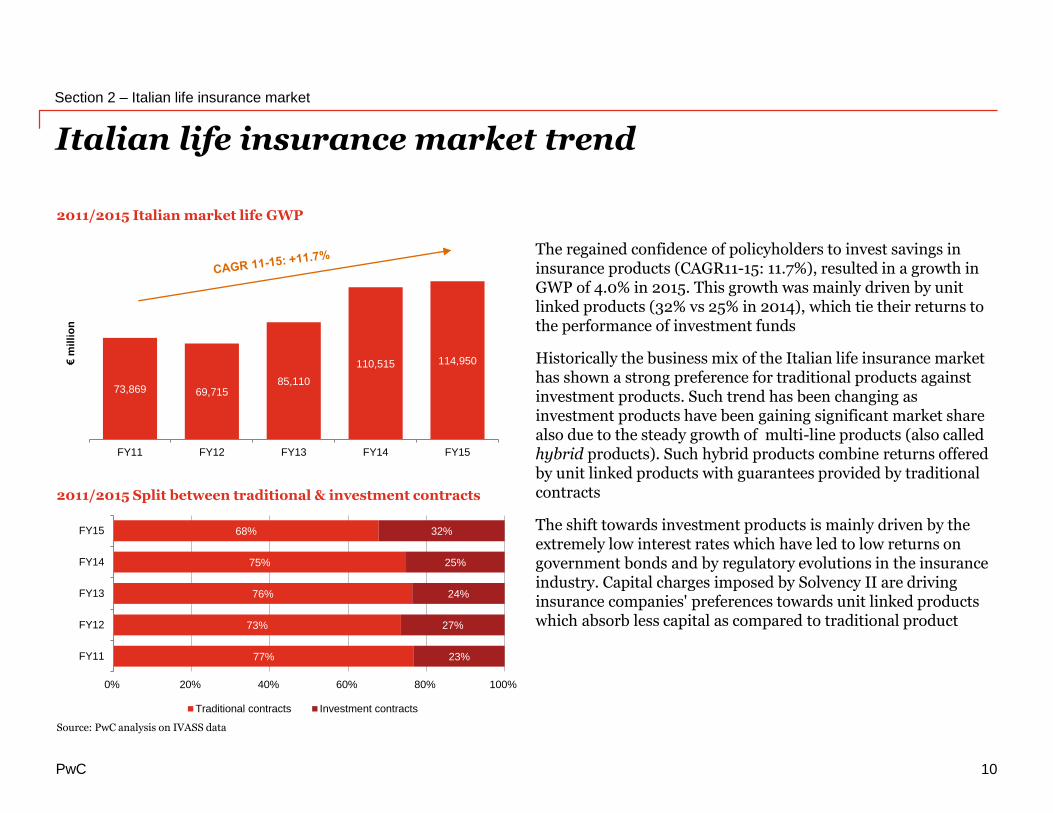

The regained confidence of policyholders to invest savings in insurance products (CAGR11-15: 11.7%), resulted in a growth in GWP of 4.0% in 2015. This growth was mainly driven by unit linked products (32% vs 25% in 2014), which tie their returns to the performance of investment funds

Historically the business mix of the Italian life insurance market has shown a strong preference for traditional products against investment products. Such trend has been changing as investment products have been gaining significant market share also due to the steady growth of multi-line products (also called hybrid products). Such hybrid products combine returns offered by unit linked products with guarantees provided by traditional contracts

The shift towards investment products is mainly driven by the extremely low interest rates which have led to low returns on government bonds and by regulatory evolutions in the insurance industry. Capital charges imposed by Solvency II are driving insurance companies' preferences towards unit linked products which absorb less capital as compared to traditional product

PwC

21,78517,251 20,297

27,49331,972

40,34035,444

42,593

55,59961,626

56,19550,522

62,168

82,356 86,100

73,86969,715

85,110

110,515114,950

3M11 3M12 3M13 3M14 3M15 6M11 6M12 6M13 6M14 6M15 9M11 9M12 9M13 9M14 9M15 12M11 12M12 12M13 12M14 12M15

€m

illi

on

Traditional products Unit & Index linked Capitalisations Others (sickness or mutual funds)

Breakdown by quarter of Italian life insurance market

Section 2 – Italian life insurance market

11

2011/2015 GWP breakdown by quarter

2011/2015 Annual, single and recurring premiums

-21%+18%

+35%

-12%+20%

+31%

-10%+23%

+32%

-6% +6%

+30%

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

+16%

+11%

+5%

+4%

08%

09%

07%

06%

05%

79%

78%

81%

84%

84%

13%

13%

12%

10%

11%

0% 20% 40% 60% 80% 100%

FY11

FY12

FY13

FY14

FY15

Annual premiums Single premiums Recurring premiums

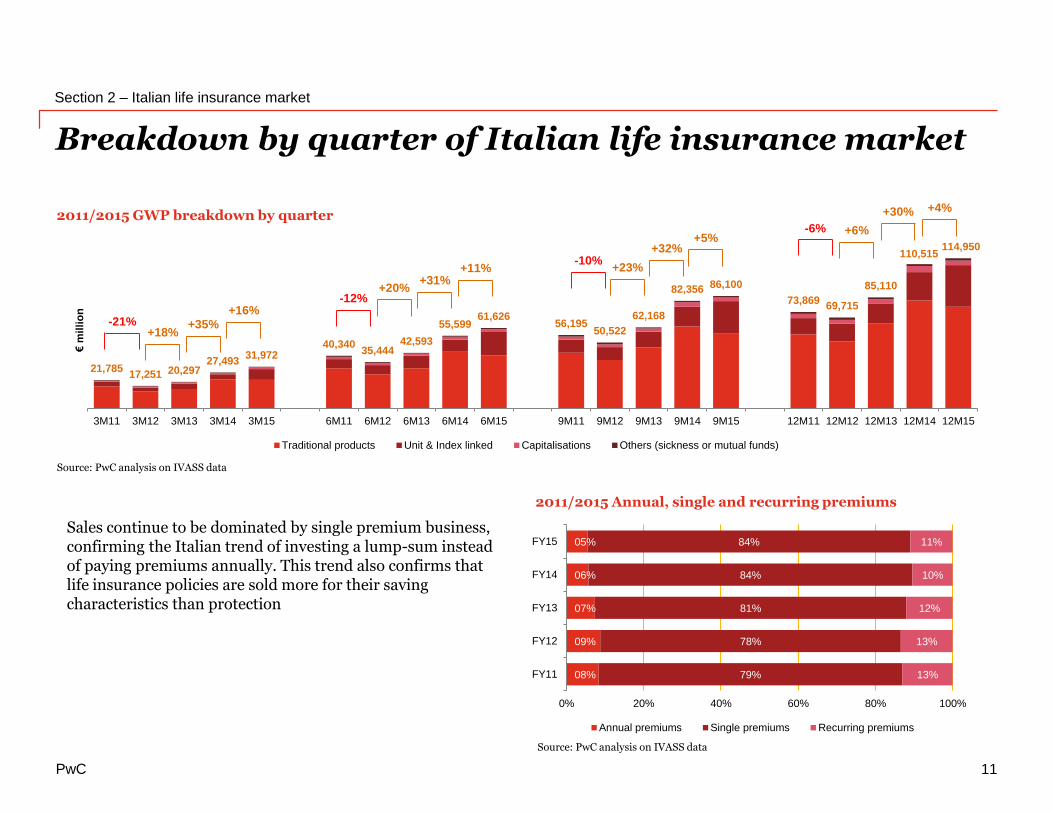

Sales continue to be dominated by single premium business, confirming the Italian trend of investing a lump-sum instead of paying premiums annually. This trend also confirms that life insurance policies are sold more for their saving characteristics than protection

PwC

96,314

43,860

(7,177)

(42,796)

(21,085)

13,132 5,472

Single Premiums Recurring Premiums Recurring Premiums1st year

Surrenders Maturities & Yields Claims Total Net Flows

€m

illi

on

Breakdown of net cash flows

80%

19% 0% 0%

67%

27%

4% 2%

75%

22%

3% 1%

78%

17%

2% 4%

66%

30%

3% 1%

41%

46%

9%4%

Traditional products Unit & Index linked Capitalisations Other LoBs

Section 2 – Italian life insurance market

12

2015 Breakdown of net flows

Written premiums Amounts paid

Source: PwC analysis on ANIA data

€96bn €13bn €5bn (€43bn) (€21bn) (€7bn)

69%

22%

8% 1%

PwC

28,724

14,464

(137)

809 43,860

Traditional products Unit & Index linked Capitalisations Other LoBs Total Net Flow

€m

illi

on

Breakdown of net cash flows by LoB

Section 2 – Italian life insurance market

13

2015 Breakdown of net flows by LoB

Source: PwC analysis on ANIA data

GWP

Redemptions

Maturities

Claims

Net flows €28,724m Net flows €14,464m Net flows (€137m)

Traditional Unit & Index linked Capitalisation

77,870

(28,847)

(14,536)

(5,763)

31,838

(11,376)

(4,611)

(1,387)

3,483

(1,842)

(1,774)

(4)

€ million € million € million

Traditional productsUnit & Index linkedCapitalisationsOther Lobs

65%33%0%2%

LoBs contribution to Net Flow

PwC

5.14 3.32

7.83

4.76

12.3%

16.5%

13.3% 13.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

-

1

2

3

4

5

6

7

8

9

10

11

12

Traditional products Unit & Index linked Capitalisations Life LoBsTotal

Average duration (years) Lapse index (%)

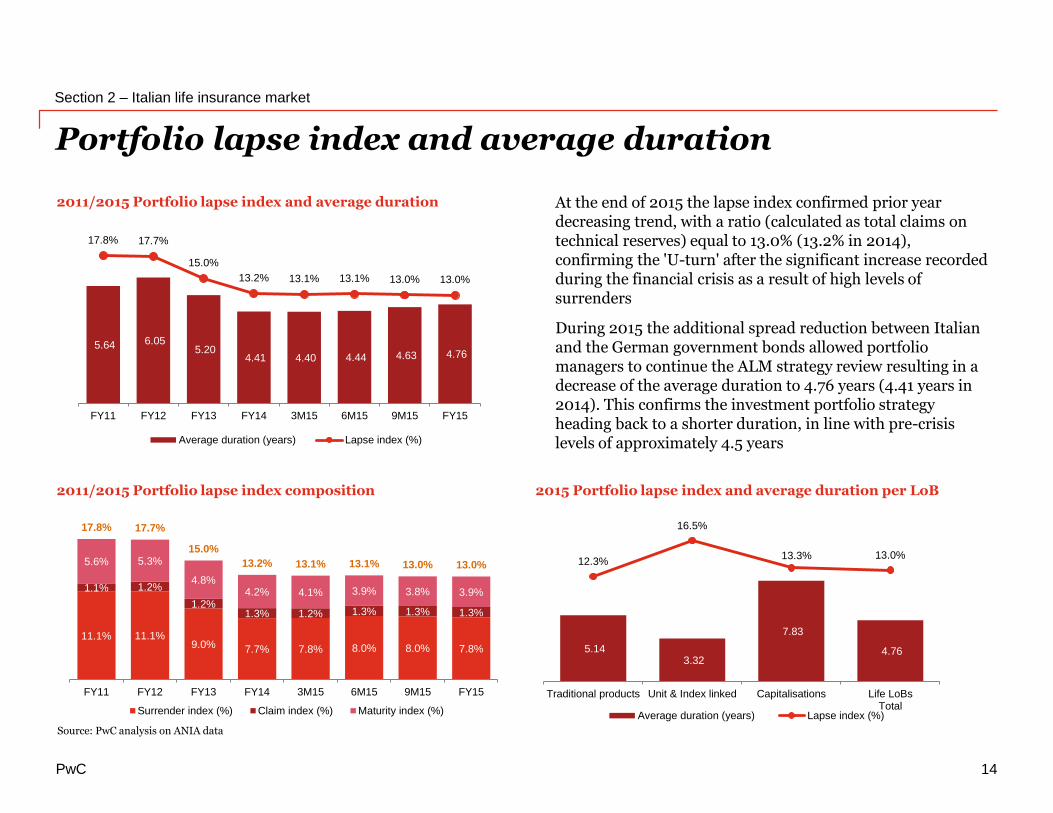

Portfolio lapse index and average duration

Section 2 – Italian life insurance market

14

At the end of 2015 the lapse index confirmed prior year decreasing trend, with a ratio (calculated as total claims on technical reserves) equal to 13.0% (13.2% in 2014), confirming the 'U-turn' after the significant increase recorded during the financial crisis as a result of high levels of surrenders

During 2015 the additional spread reduction between Italian and the German government bonds allowed portfolio managers to continue the ALM strategy review resulting in a decrease of the average duration to 4.76 years (4.41 years in 2014). This confirms the investment portfolio strategy heading back to a shorter duration, in line with pre-crisis levels of approximately 4.5 years

2015 Portfolio lapse index and average duration per LoB

2011/2015 Portfolio lapse index and average duration

2011/2015 Portfolio lapse index composition

Source: PwC analysis on ANIA data

5.64 6.05 5.20

4.41 4.40 4.44 4.63 4.76

17.8% 17.7%

15.0%

13.2% 13.1% 13.1% 13.0% 13.0%

0%

5%

10%

15%

20%

-

1

2

3

4

5

6

7

8

FY11 FY12 FY13 FY14 3M15 6M15 9M15 FY15

Average duration (years) Lapse index (%)

11.1% 11.1%9.0% 7.7% 7.8% 8.0% 8.0% 7.8%

1.1% 1.2%

1.2%1.3% 1.2% 1.3% 1.3% 1.3%

5.6% 5.3%

4.8%4.2% 4.1% 3.9% 3.8% 3.9%

17.8% 17.7%

15.0%

13.2% 13.1% 13.1% 13.0% 13.0%

FY11 FY12 FY13 FY14 3M15 6M15 9M15 FY15

Surrender index (%) Claim index (%) Maturity index (%)

PwC

Distribution channel and investments overview

Section 2 – Italian life insurance market

15

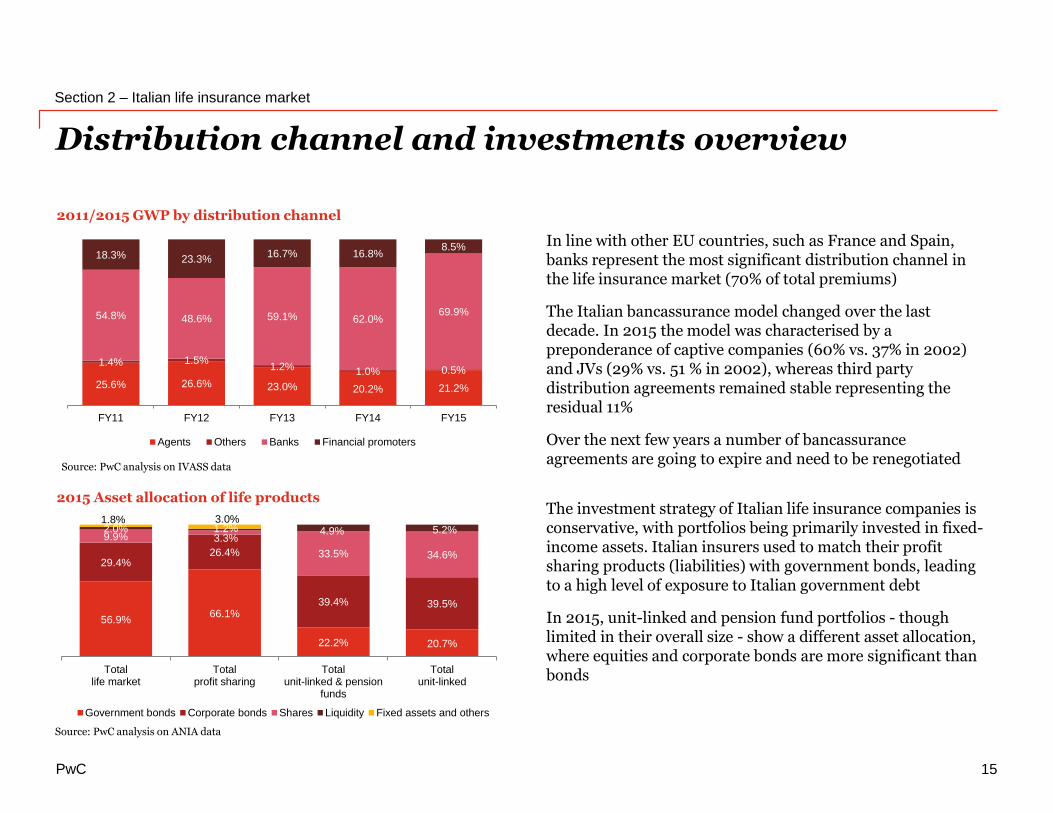

2011/2015 GWP by distribution channel

2015 Asset allocation of life products

Source: PwC analysis on IVASS data

Source: PwC analysis on ANIA data

25.6% 26.6% 23.0% 20.2% 21.2%

1.4% 1.5%1.2% 1.0% 0.5%

54.8% 48.6% 59.1% 62.0%69.9%

18.3% 23.3%16.7% 16.8%

8.5%

FY11 FY12 FY13 FY14 FY15

Agents Others Banks Financial promoters

56.9%66.1%

22.2% 20.7%

29.4%26.4%

39.4% 39.5%

9.9% 3.3%

33.5% 34.6%

2.0% 1.2% 4.9% 5.2%1.8% 3.0%

Totallife market

Totalprofit sharing

Totalunit-linked & pension

funds

Totalunit-linked

Government bonds Corporate bonds Shares Liquidity Fixed assets and others

In line with other EU countries, such as France and Spain, banks represent the most significant distribution channel in the life insurance market (70% of total premiums)

The Italian bancassurance model changed over the last decade. In 2015 the model was characterised by a preponderance of captive companies (60% vs. 37% in 2002) and JVs (29% vs. 51 % in 2002), whereas third party distribution agreements remained stable representing the residual 11%

Over the next few years a number of bancassuranceagreements are going to expire and need to be renegotiated

The investment strategy of Italian life insurance companies is conservative, with portfolios being primarily invested in fixed-income assets. Italian insurers used to match their profit sharing products (liabilities) with government bonds, leading to a high level of exposure to Italian government debt

In 2015, unit-linked and pension fund portfolios - though limited in their overall size - show a different asset allocation, where equities and corporate bonds are more significant than bonds

PwC

Life insurance solvency margin

Section 2 – Italian life insurance market

16

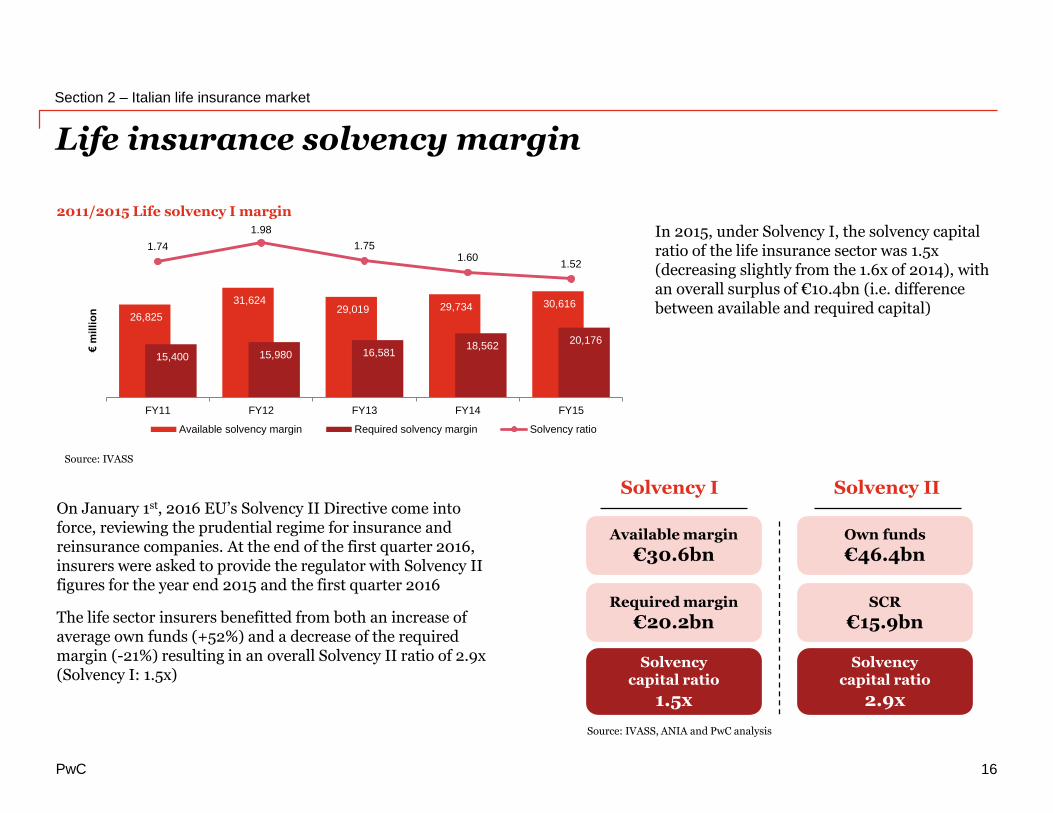

On January 1st, 2016 EU’s Solvency II Directive come into force, reviewing the prudential regime for insurance and reinsurance companies. At the end of the first quarter 2016, insurers were asked to provide the regulator with Solvency II figures for the year end 2015 and the first quarter 2016

The life sector insurers benefitted from both an increase of average own funds (+52%) and a decrease of the required margin (-21%) resulting in an overall Solvency II ratio of 2.9x (Solvency I: 1.5x)

Available margin

€30.6bn

Required margin

€20.2bn

Own funds

€46.4bn

SCR

€15.9bn

Solvencycapital ratio

1.5x

Solvencycapital ratio

2.9x

In 2015, under Solvency I, the solvency capital ratio of the life insurance sector was 1.5x (decreasing slightly from the 1.6x of 2014), with an overall surplus of €10.4bn (i.e. difference between available and required capital)

26,825

31,624 29,019 29,734 30,616

15,400 15,980 16,581 18,562

20,176

1.74

1.98

1.751.60

1.52

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

FY11 FY12 FY13 FY14 FY15

€m

illi

on

Available solvency margin Required solvency margin Solvency ratio

Source: IVASS

2011/2015 Life solvency I margin

Source: IVASS, ANIA and PwC analysis

Solvency I Solvency II

PwC

60%

40%

Traditional Unit & Index Linked

11% 72% 17%

Others Banks Financial promoters

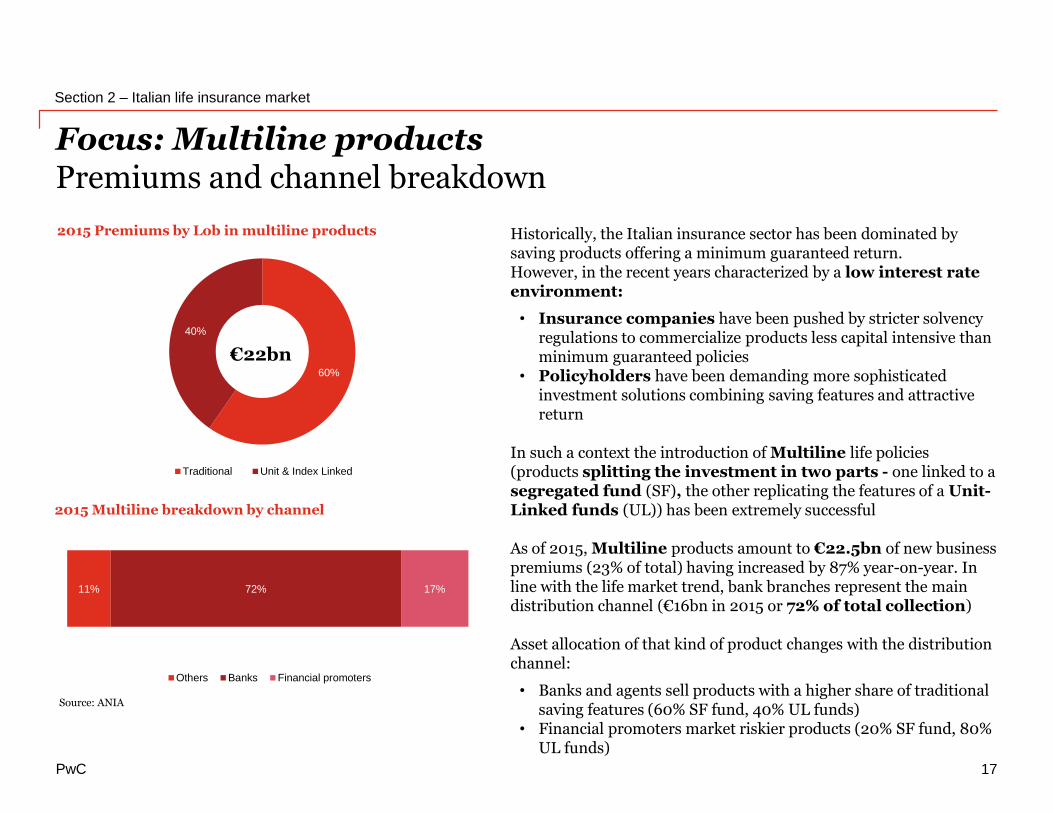

Focus: Multiline productsPremiums and channel breakdown

Section 2 – Italian life insurance market

2015 Multiline breakdown by channel

2015 Premiums by Lob in multiline products

Source: ANIA

17

€22bn

Historically, the Italian insurance sector has been dominated by saving products offering a minimum guaranteed return.However, in the recent years characterized by a low interest rate environment:

• Insurance companies have been pushed by stricter solvency regulations to commercialize products less capital intensive than minimum guaranteed policies

• Policyholders have been demanding more sophisticated investment solutions combining saving features and attractive return

In such a context the introduction of Multiline life policies(products splitting the investment in two parts - one linked to asegregated fund (SF), the other replicating the features of a Unit-Linked funds (UL)) has been extremely successful

As of 2015, Multiline products amount to €22.5bn of new business premiums (23% of total) having increased by 87% year-on-year. In line with the life market trend, bank branches represent the main distribution channel (€16bn in 2015 or 72% of total collection)

Asset allocation of that kind of product changes with the distribution channel:

• Banks and agents sell products with a higher share of traditional saving features (60% SF fund, 40% UL funds)

• Financial promoters market riskier products (20% SF fund, 80% UL funds)

PwC

Italian non-life insurance market

The Italian Insurance Market • 2015 figures + 3M16 overview

18

PwC

> €1bn €1bn-€0.3bn

€0.3bn-€0.1bn

€100m-€50m

< €50m

Section 3 – Italian non-life insurance market

19

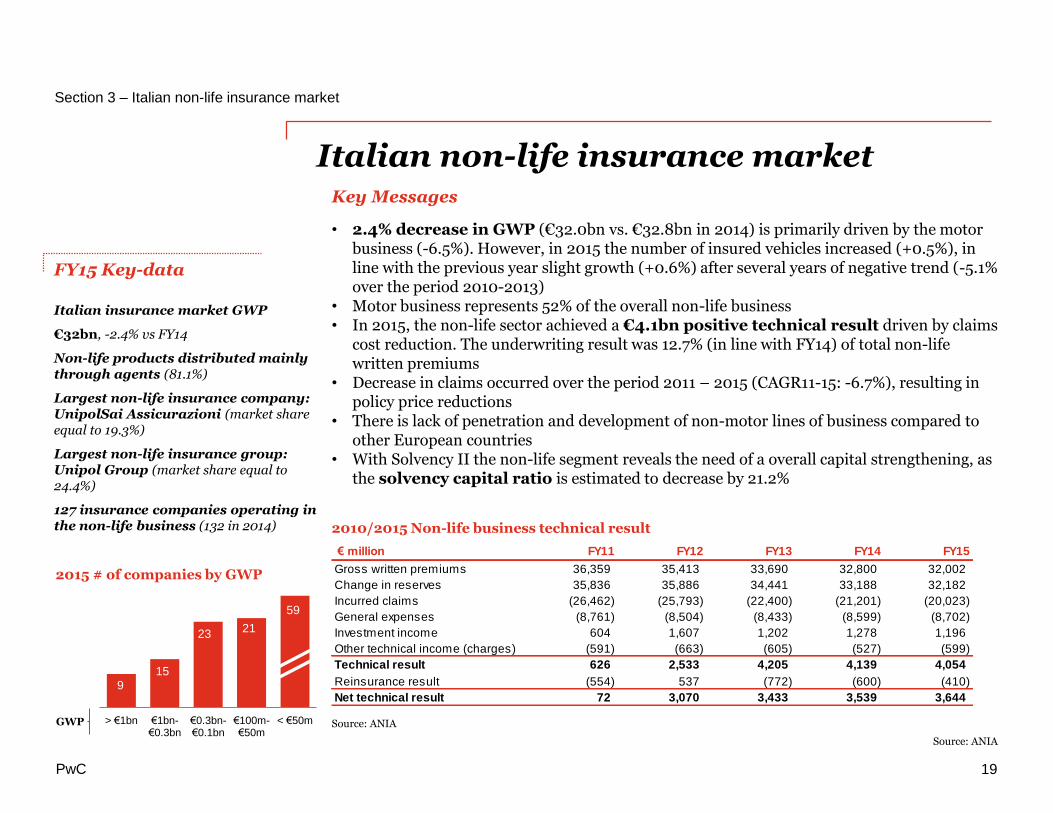

Italian non-life insurance market

FY15 Key-data

Italian insurance market GWP

€32bn, -2.4% vs FY14

Non-life products distributed mainly through agents (81.1%)

Largest non-life insurance company: UnipolSai Assicurazioni (market share equal to 19.3%)

Largest non-life insurance group: Unipol Group (market share equal to 24.4%)

127 insurance companies operating in the non-life business (132 in 2014)

2015 # of companies by GWP

GWP

2010/2015 Non-life business technical result

Source: ANIA

23 21

59

159

Source: ANIA

Key Messages

• 2.4% decrease in GWP (€32.0bn vs. €32.8bn in 2014) is primarily driven by the motor business (-6.5%). However, in 2015 the number of insured vehicles increased (+0.5%), in line with the previous year slight growth (+0.6%) after several years of negative trend (-5.1% over the period 2010-2013)

• Motor business represents 52% of the overall non-life business• In 2015, the non-life sector achieved a €4.1bn positive technical result driven by claims

cost reduction. The underwriting result was 12.7% (in line with FY14) of total non-life written premiums

• Decrease in claims occurred over the period 2011 – 2015 (CAGR11-15: -6.7%), resulting in policy price reductions

• There is lack of penetration and development of non-motor lines of business compared to other European countries

• With Solvency II the non-life segment reveals the need of a overall capital strengthening, as the solvency capital ratio is estimated to decrease by 21.2%

€ million FY11 FY12 FY13 FY14 FY15

Gross written premiums 36,359 35,413 33,690 32,800 32,002

Change in reserves 35,836 35,886 34,441 33,188 32,182

Incurred claims (26,462) (25,793) (22,400) (21,201) (20,023)

General expenses (8,761) (8,504) (8,433) (8,599) (8,702)

Investment income 604 1,607 1,202 1,278 1,196

Other technical income (charges) (591) (663) (605) (527) (599)

Technical result 626 2,533 4,205 4,139 4,054

Reinsurance result (554) 537 (772) (600) (410)

Net technical result 72 3,070 3,433 3,539 3,644

PwC

20,652

5,208 4,989

2,933 2,577

20,190

5,113 4,917

2,939 2,254

18,644

5,031 4,947

2,848 2,221

17,567

5,030 5,072

2,831 2,301

16,642

5,105 5,019

2,871 2,364

Motor Accident & Sickness Fire & other damages General TPL Other

€m

illi

on

FY11 FY12 FY13 FY14 FY15

36,35935,413

33,69032,800

32,002

FY11 FY12 FY13 FY14 FY15

€m

illi

on

2011/2015 Italian market non-life GWP

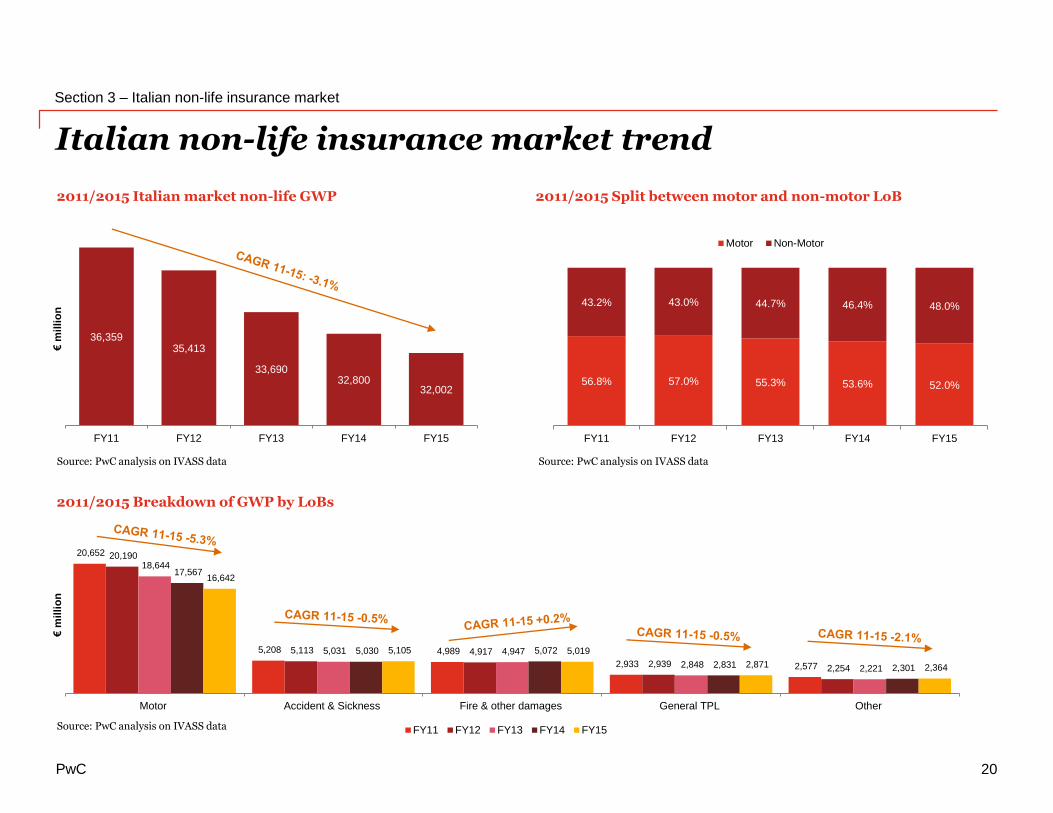

Italian non-life insurance market trend

Section 3 – Italian non-life insurance market

20

2011/2015 Breakdown of GWP by LoBs

2011/2015 Split between motor and non-motor LoB

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

56.8% 57.0% 55.3% 53.6% 52.0%

43.2% 43.0% 44.7% 46.4% 48.0%

FY11 FY12 FY13 FY14 FY15

Motor Non-Motor

PwC

8,791 8,687 8,198 7,967 7,804

18,385 18,059 17,159 16,515 16,090

25,713 25,168 23,988 23,153 22,619

36,359 35,413 33,690 32,800 32,002

3M11 3M12 3M13 3M14 3M15 6M11 6M12 6M13 6M14 6M15 9M11 9M12 9M13 9M14 9M15 12M11 12M12 12M13 12M14 12M15

€m

illi

on

Motor Accident & Sickness Fire & other damages General TPL Other

-2.6%

-2.1%

-1.8%

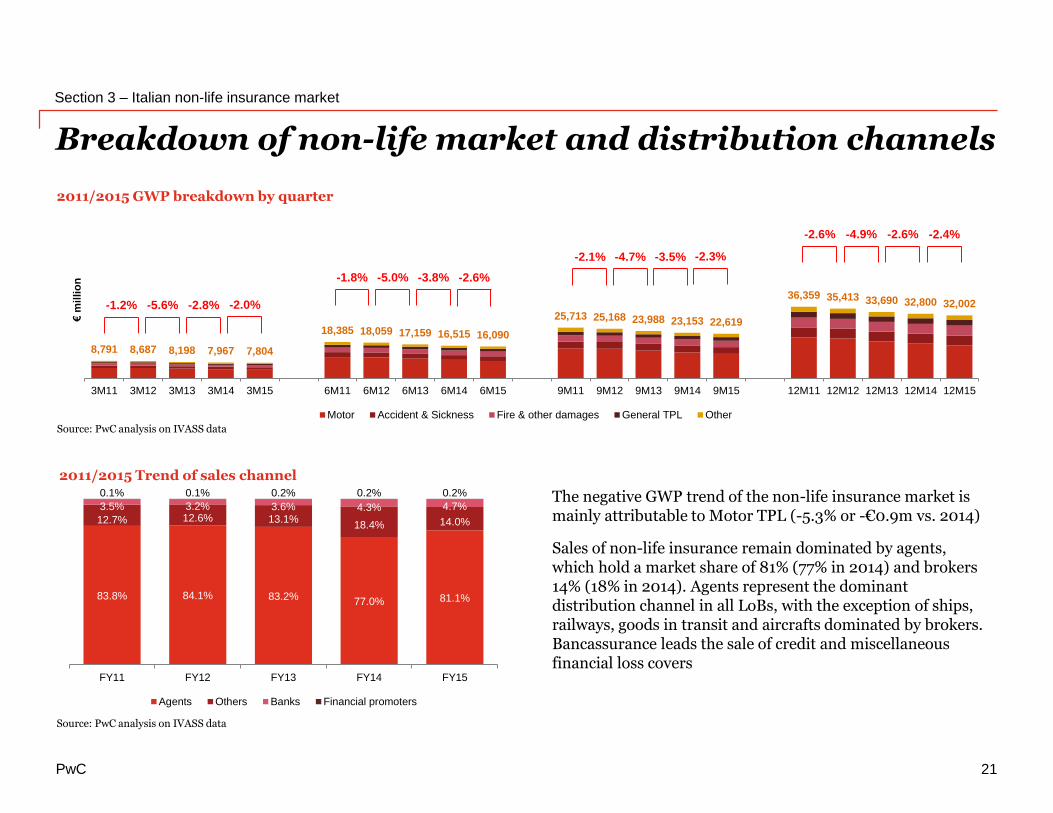

Breakdown of non-life market and distribution channels

Section 3 – Italian non-life insurance market

21

2011/2015 Trend of sales channel

2011/2015 GWP breakdown by quarter

-1.2% -5.6% -2.8%

-3.8%-5.0%

-3.5%-4.7%

-2.6%-4.9%

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

-2.0%

-2.6%

-2.3%

-2.4%

83.8% 84.1% 83.2%77.0% 81.1%

12.7% 12.6% 13.1%18.4% 14.0%

3.5% 3.2% 3.6% 4.3% 4.7%

0.1% 0.1% 0.2% 0.2% 0.2%

FY11 FY12 FY13 FY14 FY15

Agents Others Banks Financial promoters

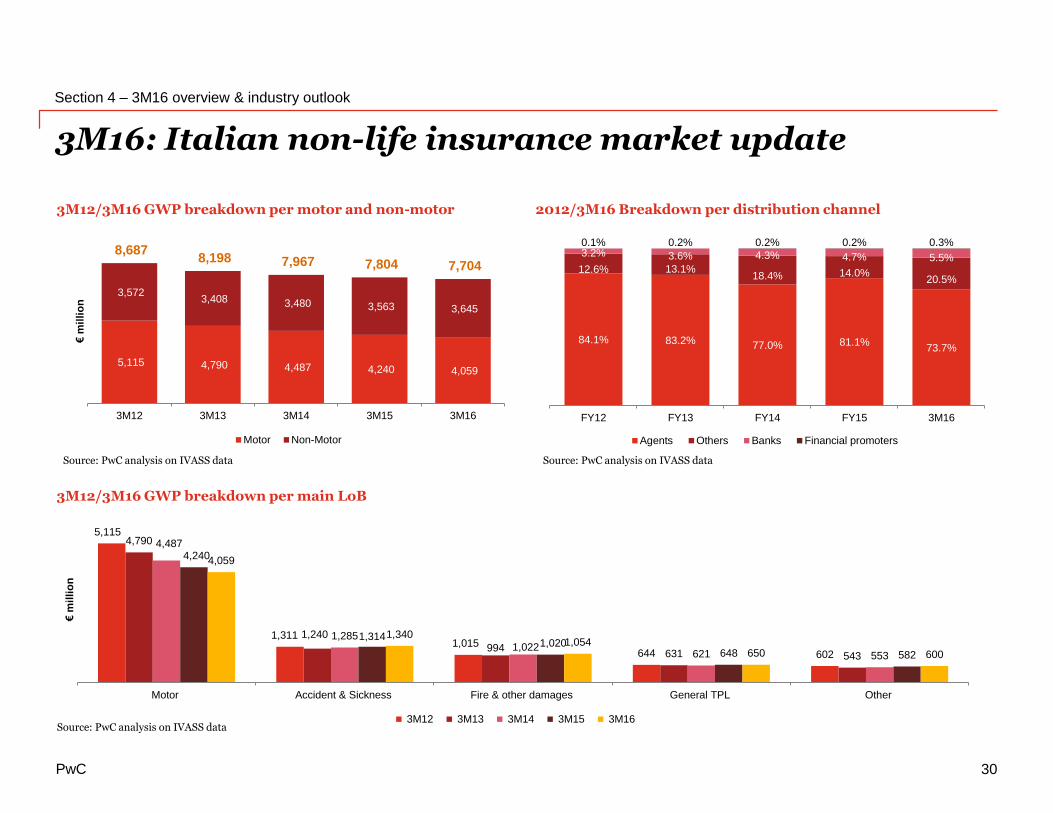

The negative GWP trend of the non-life insurance market is mainly attributable to Motor TPL (-5.3% or -€0.9m vs. 2014)

Sales of non-life insurance remain dominated by agents, which hold a market share of 81% (77% in 2014) and brokers 14% (18% in 2014). Agents represent the dominant distribution channel in all LoBs, with the exception of ships, railways, goods in transit and aircrafts dominated by brokers. Bancassurance leads the sale of credit and miscellaneous financial loss covers

PwC

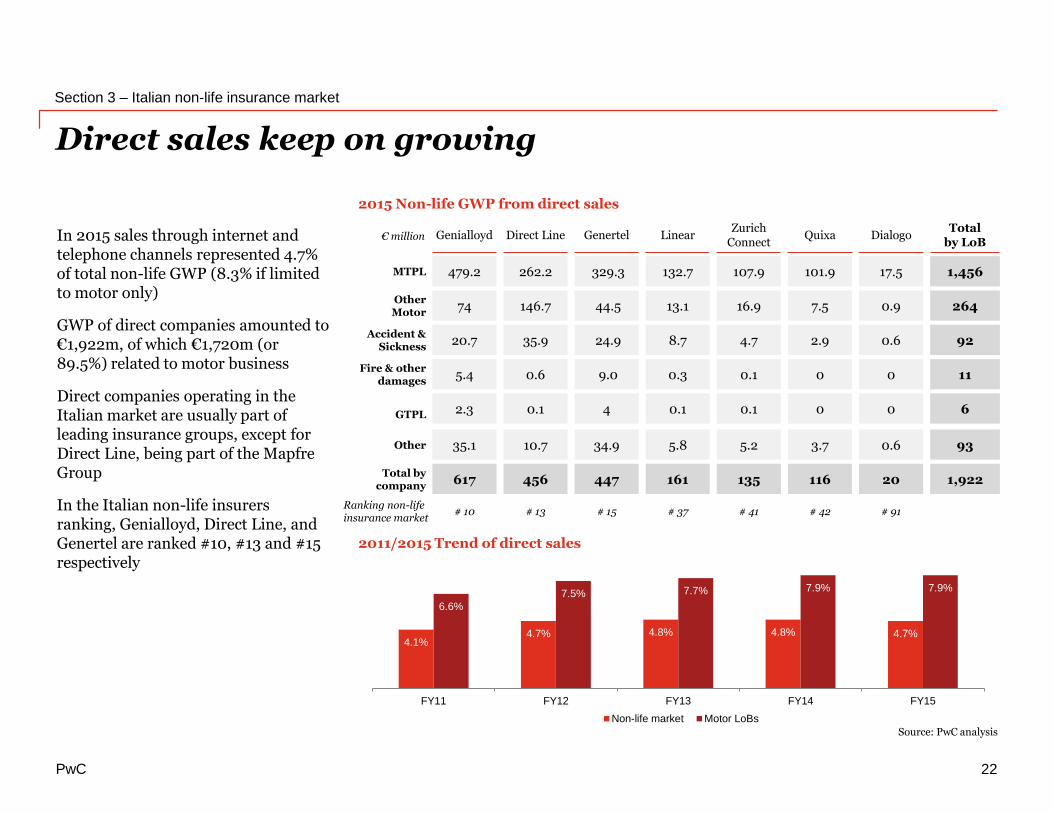

Direct sales keep on growing

Section 3 – Italian non-life insurance market

22

€ million Genialloyd Direct Line Genertel LinearZurich

ConnectQuixa Dialogo

Totalby LoB

479.2 262.2 107.9132.7329.3 101.9 17.5 1,456MTPL

74 146.7 16.913.144.5 7.5 0.9 264Other Motor

20.7 35.9 4.78.724.9 2.9 0.6 92Accident &

Sickness

5.4 0.6 0.10.39.0 0 0 11Fire & other

damages

2.3 0.1 0.10.14 0 0 6GTPL

35.1 10.7 5.25.834.9 3.7 0.6 93Other

617 456 135161447 116 20 1,922Total by

company

Ranking non-life insurance market

# 10 # 13 # 15 # 37 # 41 # 42 # 91

2015 Non-life GWP from direct sales

2011/2015 Trend of direct sales

Source: PwC analysis

4.1%4.7% 4.8% 4.8% 4.7%

6.6%

7.5% 7.7% 7.9% 7.9%

FY11 FY12 FY13 FY14 FY15

Non-life market Motor LoBs

In 2015 sales through internet and telephone channels represented 4.7% of total non-life GWP (8.3% if limited to motor only)

GWP of direct companies amounted to €1,922m, of which €1,720m (or 89.5%) related to motor business

Direct companies operating in the Italian market are usually part of leading insurance groups, except for Direct Line, being part of the Mapfre Group

In the Italian non-life insurers ranking, Genialloyd, Direct Line, and Genertel are ranked #10, #13 and #15 respectively

PwC

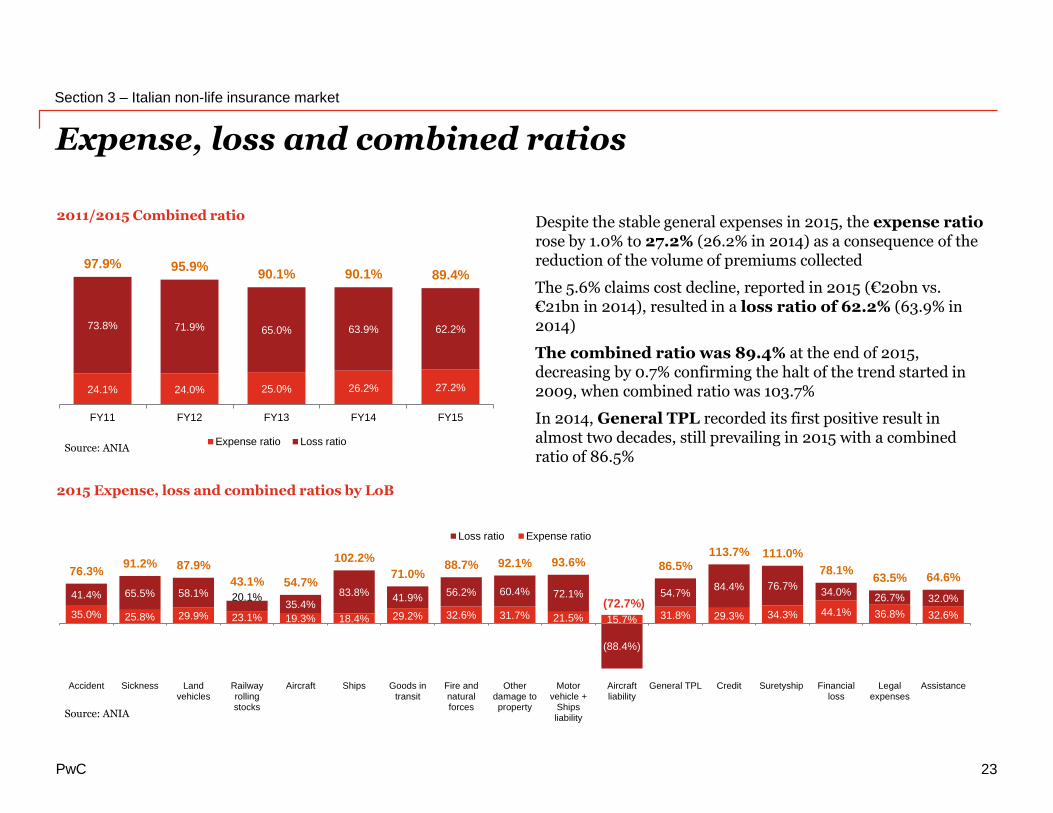

Expense, loss and combined ratios

Section 3 – Italian non-life insurance market

23

2011/2015 Combined ratio

2015 Expense, loss and combined ratios by LoB

Source: ANIA

Source: ANIA

35.0% 25.8% 29.9% 23.1% 19.3% 18.4% 29.2% 32.6% 31.7% 21.5% 15.7% 31.8% 29.3% 34.3% 44.1% 36.8% 32.6%

41.4% 65.5% 58.1% 20.1% 35.4%

83.8% 41.9%

56.2% 60.4% 72.1%

(88.4%)

54.7% 84.4% 76.7%

34.0% 26.7% 32.0%

76.3% 91.2% 87.9%

43.1% 54.7%

102.2%

71.0% 88.7% 92.1% 93.6%

(72.7%)

86.5%

113.7% 111.0%

78.1% 63.5% 64.6%

Accident Sickness Landvehicles

Railwayrollingstocks

Aircraft Ships Goods intransit

Fire andnaturalforces

Otherdamage toproperty

Motorvehicle +

Shipsliability

Aircraftliability

General TPL Credit Suretyship Financialloss

Legalexpenses

Assistance

Loss ratio Expense ratio

24.1% 24.0% 25.0% 26.2% 27.2%

73.8% 71.9% 65.0% 63.9% 62.2%

97.9% 95.9% 90.1% 90.1% 89.4%

FY11 FY12 FY13 FY14 FY15

Expense ratio Loss ratio

Despite the stable general expenses in 2015, the expense ratio rose by 1.0% to 27.2% (26.2% in 2014) as a consequence of the reduction of the volume of premiums collected

The 5.6% claims cost decline, reported in 2015 (€20bn vs. €21bn in 2014), resulted in a loss ratio of 62.2% (63.9% in 2014)

The combined ratio was 89.4% at the end of 2015, decreasing by 0.7% confirming the halt of the trend started in 2009, when combined ratio was 103.7%

In 2014, General TPL recorded its first positive result in almost two decades, still prevailing in 2015 with a combined ratio of 86.5%

PwC

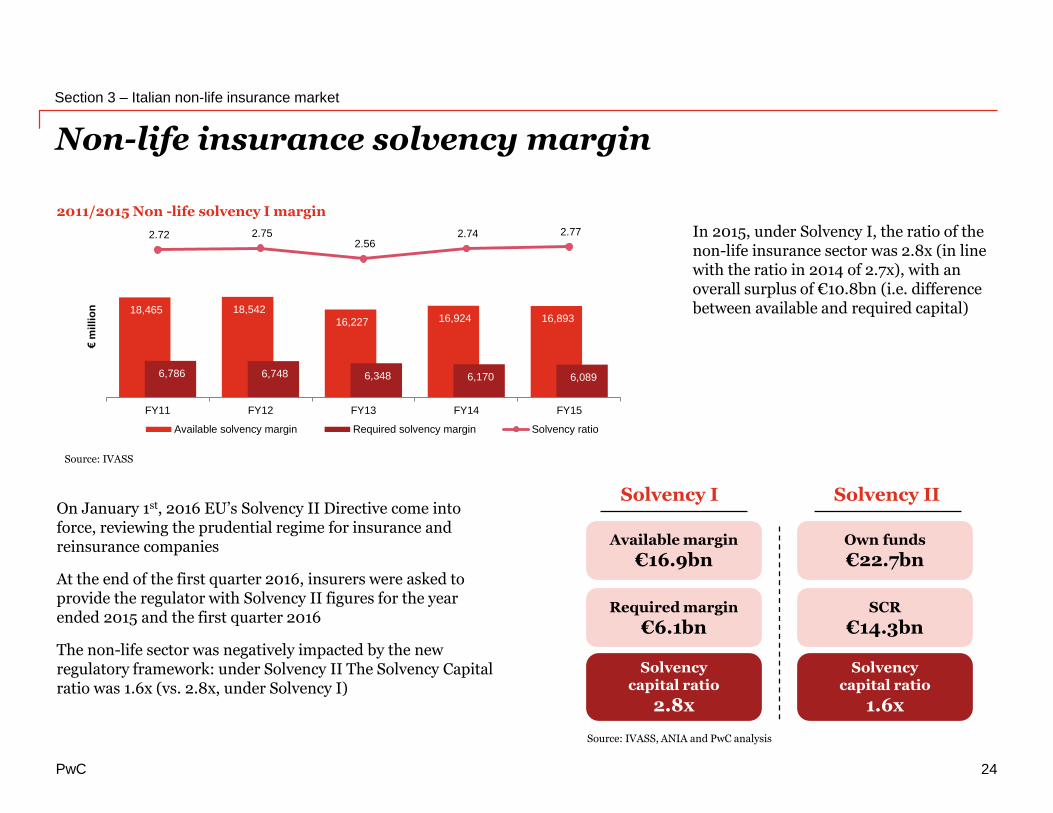

Non-life insurance solvency margin

Section 3 – Italian non-life insurance market

24

In 2015, under Solvency I, the ratio of the non-life insurance sector was 2.8x (in line with the ratio in 2014 of 2.7x), with an overall surplus of €10.8bn (i.e. difference between available and required capital)

On January 1st, 2016 EU’s Solvency II Directive come into force, reviewing the prudential regime for insurance and reinsurance companies

At the end of the first quarter 2016, insurers were asked to provide the regulator with Solvency II figures for the year ended 2015 and the first quarter 2016

The non-life sector was negatively impacted by the new regulatory framework: under Solvency II The Solvency Capital ratio was 1.6x (vs. 2.8x, under Solvency I)

Available margin

€16.9bn

Required margin

€6.1bn

Own funds

€22.7bn

SCR

€14.3bn

Solvencycapital ratio

2.8x

Solvencycapital ratio

1.6x

18,465 18,542

16,227 16,924 16,893

6,786 6,748 6,348 6,170 6,089

2.72 2.75 2.56

2.74 2.77

0.0

0.5

1.0

1.5

2.0

2.5

3.0

-

5,000

10,000

15,000

20,000

25,000

30,000

FY11 FY12 FY13 FY14 FY15

€m

illi

on

Available solvency margin Required solvency margin Solvency ratio

2011/2015 Non -life solvency I margin

Source: IVASS

Source: IVASS, ANIA and PwC analysis

Solvency I Solvency II

PwC

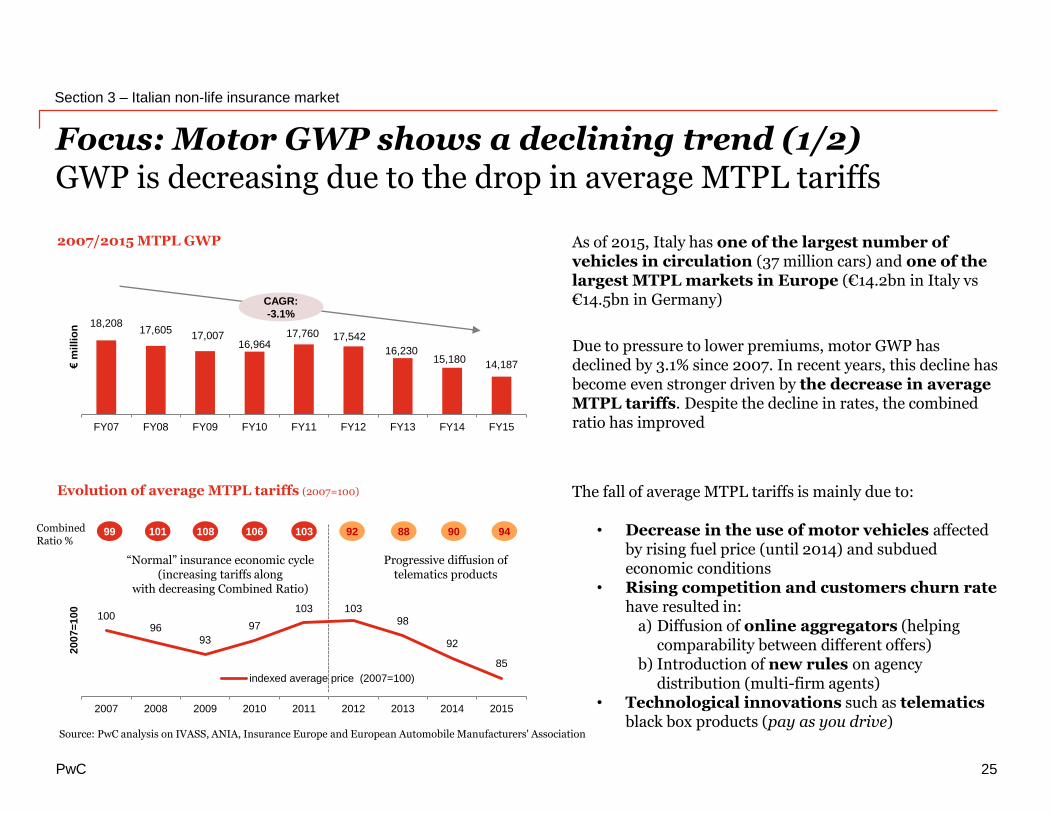

Section 3 – Italian non-life insurance market

25

Focus: Motor GWP shows a declining trend (1/2)GWP is decreasing due to the drop in average MTPL tariffs

As of 2015, Italy has one of the largest number of vehicles in circulation (37 million cars) and one of the largest MTPL markets in Europe (€14.2bn in Italy vs €14.5bn in Germany)

Due to pressure to lower premiums, motor GWP has declined by 3.1% since 2007. In recent years, this decline has become even stronger driven by the decrease in average MTPL tariffs. Despite the decline in rates, the combined ratio has improved

2007/2015 MTPL GWP

Evolution of average MTPL tariffs (2007=100)

18,20817,605

17,00716,964

17,760 17,542

16,23015,180

14,187

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

€m

illi

on

The fall of average MTPL tariffs is mainly due to:

• Decrease in the use of motor vehicles affected by rising fuel price (until 2014) and subdued economic conditions

• Rising competition and customers churn ratehave resulted in:

a) Diffusion of online aggregators (helping comparability between different offers)

b) Introduction of new rules on agency distribution (multi-firm agents)

• Technological innovations such as telematics black box products (pay as you drive)

Source: PwC analysis on IVASS, ANIA, Insurance Europe and European Automobile Manufacturers' Association

99 101 108 106 103 92 88 90

CAGR:

-3.1%

Combined Ratio %

Progressive diffusion of telematics products

“Normal” insurance economic cycle (increasing tariffs along

with decreasing Combined Ratio)

10096

93

97

103 10398

92

85

2007 2008 2009 2010 2011 2012 2013 2014 2015

2007=

100

indexed average price (2007=100)

94

PwC

Focus: Motor GWP shows a declining trend (2/2) The progressive diffusion of “Black Box” is one of the key drivers

Section 3 – Italian non-life insurance market

26

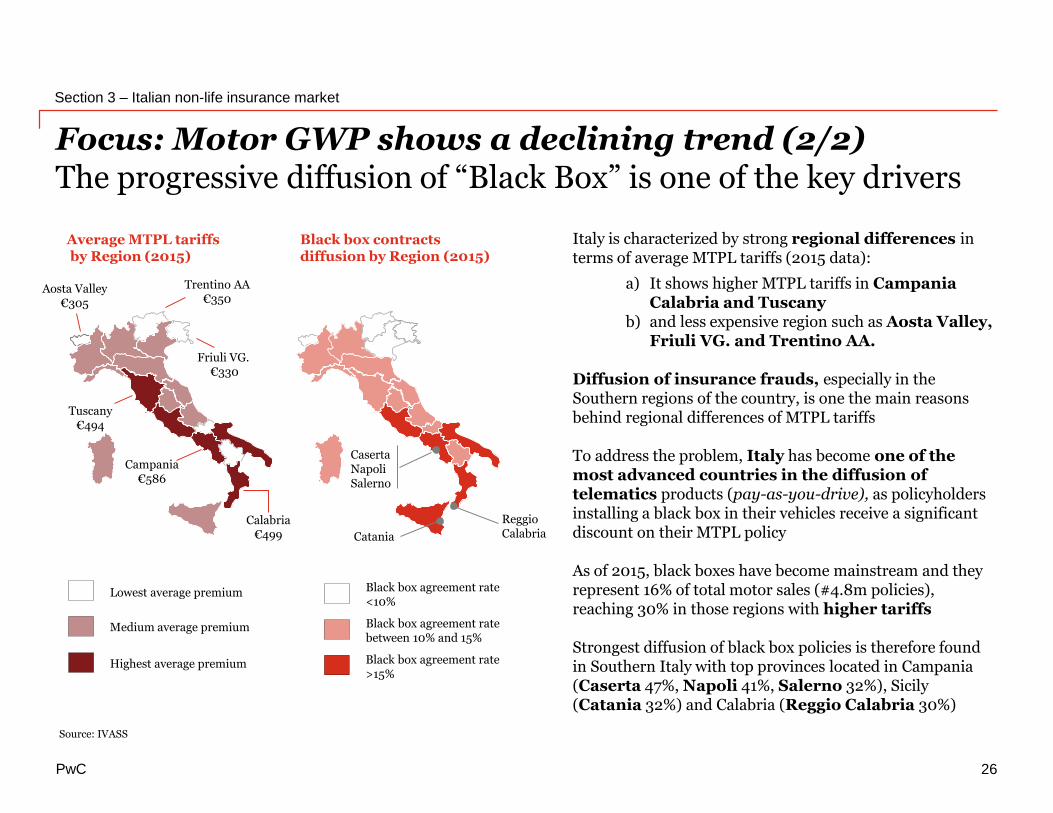

Source: IVASS

Average MTPL tariffs by Region (2015)

Campania€586

Medium average premium

Lowest average premium

Black box agreement rate between 10% and 15%

Black box agreement rate <10%

Black box agreement rate >15%

Highest average premium

Black box contracts diffusion by Region (2015)

Italy is characterized by strong regional differences in terms of average MTPL tariffs (2015 data):

a) It shows higher MTPL tariffs in Campania Calabria and Tuscany

b) and less expensive region such as Aosta Valley, Friuli VG. and Trentino AA.

Diffusion of insurance frauds, especially in the Southern regions of the country, is one the main reasons behind regional differences of MTPL tariffs

To address the problem, Italy has become one of the most advanced countries in the diffusion of telematics products (pay-as-you-drive), as policyholders installing a black box in their vehicles receive a significant discount on their MTPL policy

As of 2015, black boxes have become mainstream and they represent 16% of total motor sales (#4.8m policies), reaching 30% in those regions with higher tariffs

Strongest diffusion of black box policies is therefore found in Southern Italy with top provinces located in Campania (Caserta 47%, Napoli 41%, Salerno 32%), Sicily (Catania 32%) and Calabria (Reggio Calabria 30%)

Friuli VG.€330

Calabria€499

Aosta Valley€305

Tuscany€494

CasertaNapoliSalerno

Reggio CalabriaCatania

Trentino AA€350

PwC

3M16 overview & industry outlook

The Italian Insurance Market • 2015 figures + 3M16 overview

27

PwC

17,251 20,29727,493

31,972 30,331

8,6878,198

7,967

7,8047,704

25,93728,495

35,46039,776 38,035

3M12 3M13 3M14 3M15 3M16

€m

illi

on

Life Non-Life

47% 53%

3M16: Insurance market trend update

Section 4 – 3M16 overview & industry outlook

28

3M16 Italian Life & non-Life GWP breakdown per LoB

3M12/3M16 Italian market GWP

Life€30.3bn

Non-life€7.7bn

74%

21%

4% 2%

Traditional productsUnit & Index linkedCapitalizationsOthers (Mutual funds & Sickness)

58%

42%

Non-life market - Breakdown per motor and non-motor 3M13

Motor

Non-Motor

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

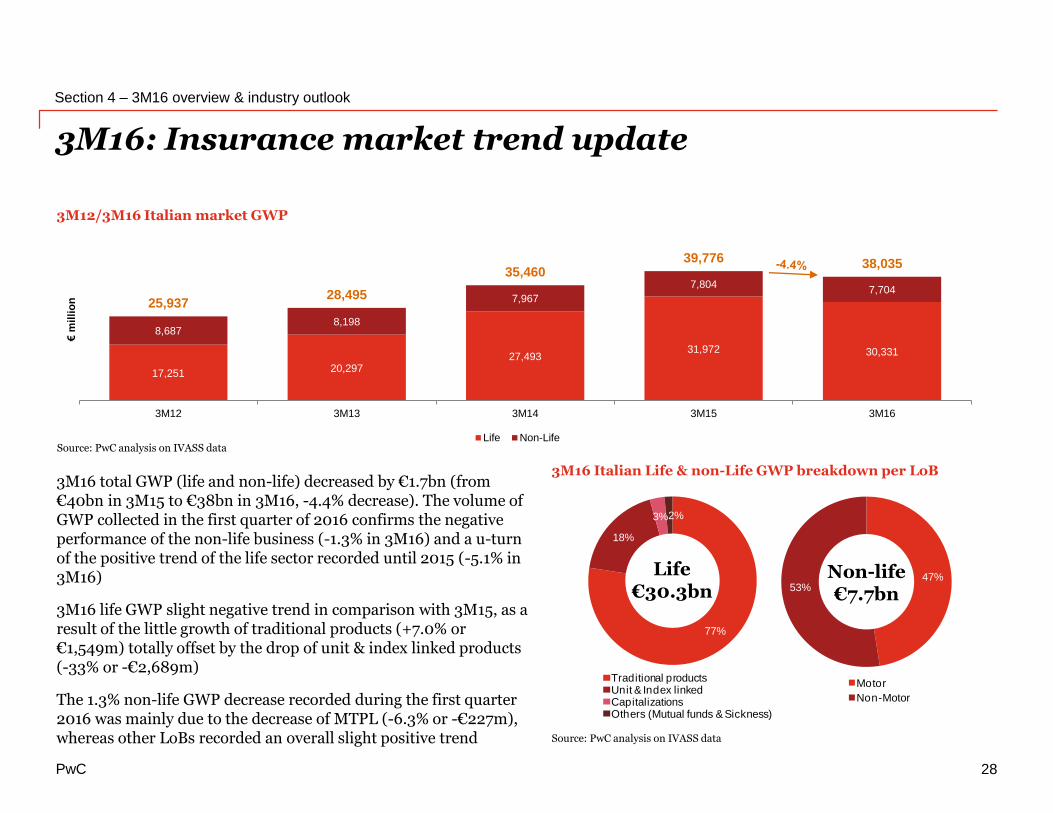

3M16 total GWP (life and non-life) decreased by €1.7bn (from €40bn in 3M15 to €38bn in 3M16, -4.4% decrease). The volume of GWP collected in the first quarter of 2016 confirms the negative performance of the non-life business (-1.3% in 3M16) and a u-turnof the positive trend of the life sector recorded until 2015 (-5.1% in 3M16)

3M16 life GWP slight negative trend in comparison with 3M15, as a result of the little growth of traditional products (+7.0% or €1,549m) totally offset by the drop of unit & index linked products(-33% or -€2,689m)

The 1.3% non-life GWP decrease recorded during the first quarter 2016 was mainly due to the decrease of MTPL (-6.3% or -€227m), whereas other LoBs recorded an overall slight positive trend

77%

18%

3% 2%

PwC

73%

76%

75%

68%

78%

27%

24%

25%

32%

22%

0% 20% 40% 60% 80% 100%

FY12

FY13

FY14

FY15

3M16

Traditional contracts Investment contracts

3M16: Italian life insurance market update

Section 4 – 3M16 overview & industry outlook

29

2012/3M16 Breakdown per channel2012/3M16 Breakdown per type of policies

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

26.6% 23.0% 20.2% 21.2% 18.3%

1.5% 1.2% 1.0% 0.5% 1.7%

48.6% 59.1% 62.0% 69.9%

64.8%

23.3% 16.7% 16.8%

8.5% 15.2%

FY12 FY13 FY14 FY15 3M16

Agents Others Banks Financial promoters

3M12/3M16 Life GWP quarter breakdown per LoB

13,043

3,074

691 443

14,981

4,183

769 364

22,345

3,856

940 354

21,945

8,208

1,403418

23,494

5,519

856 461

Traditional products Unit & Index linked Capitalisations Others (Mutual funds & Sickness)

€m

illi

on

3M12 3M13 3M14 3M15 3M16

PwC

5,115 4,790 4,487 4,240 4,059

3,572 3,408 3,480 3,563 3,645

8,687 8,198 7,967 7,804 7,704

3M12 3M13 3M14 3M15 3M16

€m

illi

on

Motor Non-Motor

5,115

1,3111,015

644 602

4,790

1,240

994631 543

4,487

1,2851,022

621 553

4,240

1,3141,020

648 582

4,059

1,3401,054

650 600

Motor Accident & Sickness Fire & other damages General TPL Other

€m

illi

on

3M12 3M13 3M14 3M15 3M16

3M16: Italian non-life insurance market update

Section 4 – 3M16 overview & industry outlook

30

2012/3M16 Breakdown per distribution channel

3M12/3M16 GWP breakdown per main LoB

3M12/3M16 GWP breakdown per motor and non-motor

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

Source: PwC analysis on IVASS data

84.1% 83.2% 77.0% 81.1%73.7%

12.6% 13.1%18.4% 14.0%

20.5%

3.2% 3.6% 4.3% 4.7% 5.5%

0.1% 0.2% 0.2% 0.2% 0.3%

FY12 FY13 FY14 FY15 3M16

Agents Others Banks Financial promoters

PwC

Industry outlook

Section 4 – 3M16 overview & industry outlook

31

2016 Non-life GWP outlook

2016 Life GWP outlook

Source: PwC analysis on ANIA data

Source: PwC analysis on ANIA data

114,950

104,653

Actual

2015

30,331

Forecast

2016

Actual

3M16

-5.1%

vs. 3M15

€m

illio

n

Actual

2015

Forecast

2016

Actual

3M16

32,00231,846

7,704

-1.3%

vs. 3M15

29% of 2016 forecast

24% of 2016 forecast

€m

illio

n

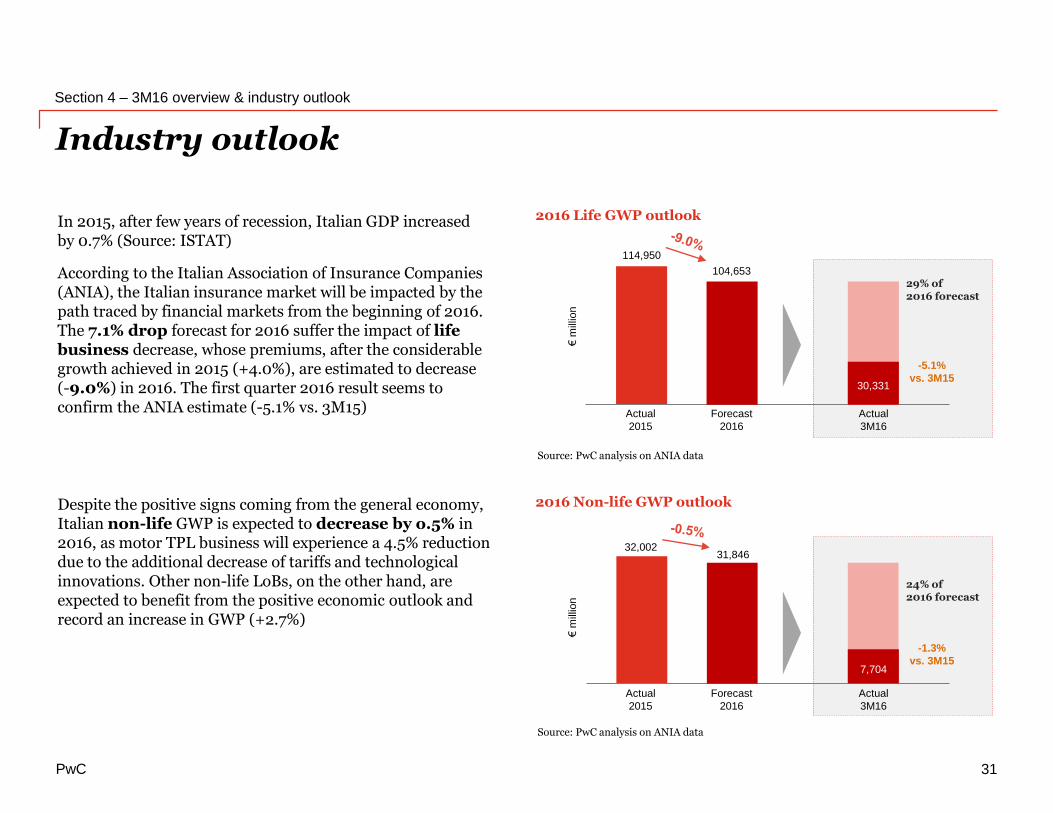

In 2015, after few years of recession, Italian GDP increased by 0.7% (Source: ISTAT)

According to the Italian Association of Insurance Companies (ANIA), the Italian insurance market will be impacted by the path traced by financial markets from the beginning of 2016. The 7.1% drop forecast for 2016 suffer the impact of life business decrease, whose premiums, after the considerable growth achieved in 2015 (+4.0%), are estimated to decrease (-9.0%) in 2016. The first quarter 2016 result seems to confirm the ANIA estimate (-5.1% vs. 3M15)

Despite the positive signs coming from the general economy, Italian non-life GWP is expected to decrease by o.5% in 2016, as motor TPL business will experience a 4.5% reduction due to the additional decrease of tariffs and technological innovations. Other non-life LoBs, on the other hand, are expected to benefit from the positive economic outlook and record an increase in GWP (+2.7%)

PwC

M&A activity

The Italian Insurance Market • 2015 figures + 3M16 overview

32

PwC

M&A Transactions

Section 5 – M&A activity

33

# Year Target Bidder Stake %Deal Size

(€m)

1 2016 Old Mutual Wealth Italy SpA Cinven Partners LLP 100% 278

2 2015 C.B.A. Vita SpA HDI Assicurazioni SpA n.a. n.a.

3 2015 ERGO Previdenza SpA Cinven Partners LLP n.a. n.a.

4 2014 Carige Vita Nuova Apollo Global Management 100% 170

5 2013 Eurovita Assicurazioni JC Flowers 80% 47

6 2012 Chiara Vita Helvetia Holding AG 30% 23

7 2011 Bipiemme Vita SpA Covea 81% 243

8 2011 BNL Vita SpA Cardif Assicurazioni SpA 51% 325

9 2010 Aviva Life SpA Aviva Italia Holding SpA 50% 30

10 2010 Arca Vita Unipol 60% 270

Life market – Recent Italian transactions

Non-life market - Recent Italian transactions

Source: PwC analysis on Mergermarket data

# Year Target Bidder Stake %Deal Size

(€m)

1 2016 Ergo Assicurazioni Darag AG n.a. 50

2 2016 Filo Diretto Nobis Assicurazioni 100% n.a.

3 2015 InChiaro Assicurazioni SpA HDI Assicurazioni SpA 49% n.a.

4 2015 ERGO Assicurazioni SpA Cinven Partners LLP n.a. n.a.

5 2014 Carige Assicurazioni Apollo Global Management 100% 140

6 2014 RSA (Italian branches) ITAS Mutua 100% 24

7 2014 Direct Line (Italy & Germany) Mapfre 100% 550

8 2014 Cargeas Assicurazioni SpA Ageas NV/BNP Paribas Cardif SA 50% -1 75

9 2014 Milano Assicurazioni SpA Allianz €1.1bn portfolio* 440

10 2013 Fata Assicurazioni Danni Cattolica Assicurazioni 100% 179

11 2012 Fondiaria-SAI Group Unipol 42% 954

* renewal rights on an insurance portfolio + 729 agencies

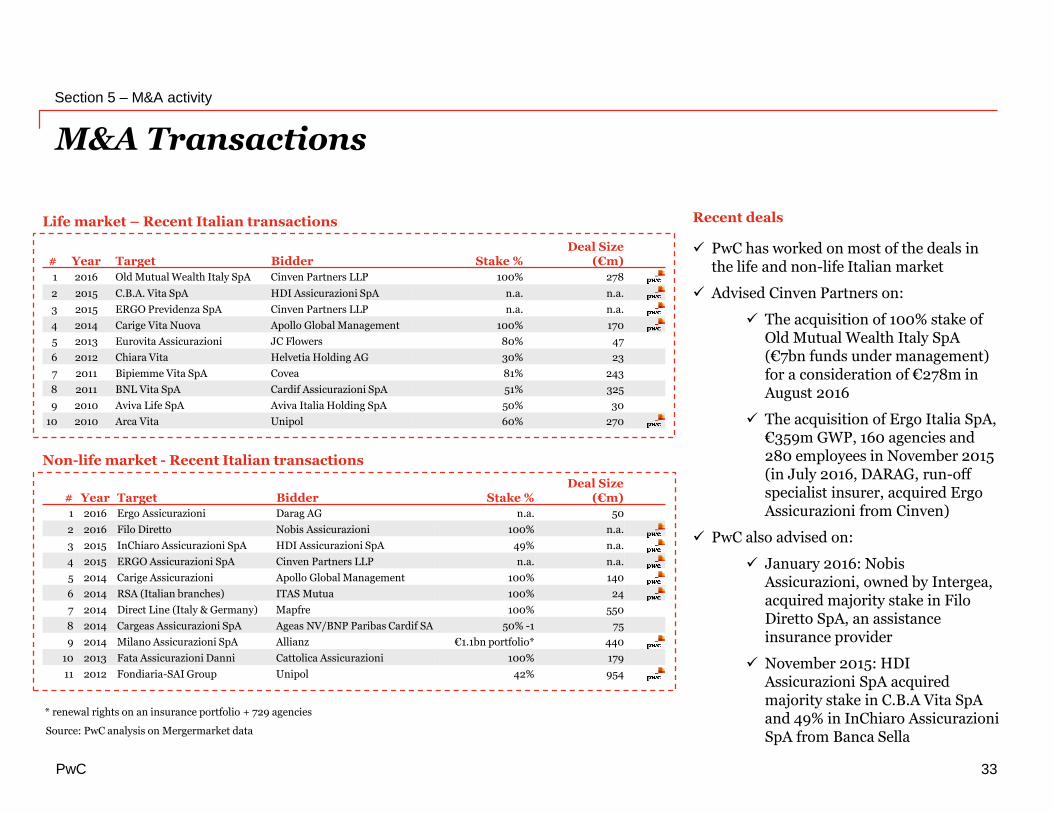

Recent deals

PwC has worked on most of the deals in the life and non-life Italian market

Advised Cinven Partners on:

The acquisition of 100% stake of Old Mutual Wealth Italy SpA (€7bn funds under management) for a consideration of €278m in August 2016

The acquisition of Ergo Italia SpA, €359m GWP, 160 agencies and 280 employees in November 2015 (in July 2016, DARAG, run-off specialist insurer, acquired Ergo Assicurazioni from Cinven)

PwC also advised on:

January 2016: Nobis Assicurazioni, owned by Intergea, acquired majority stake in Filo Diretto SpA, an assistance insurance provider

November 2015: HDI Assicurazioni SpA acquired majority stake in C.B.A Vita SpA and 49% in InChiaro Assicurazioni SpA from Banca Sella

PwC

The Italian insurance market in the European context

The Italian Insurance Market • 2015 figures + 3M16 overview

34

PwC

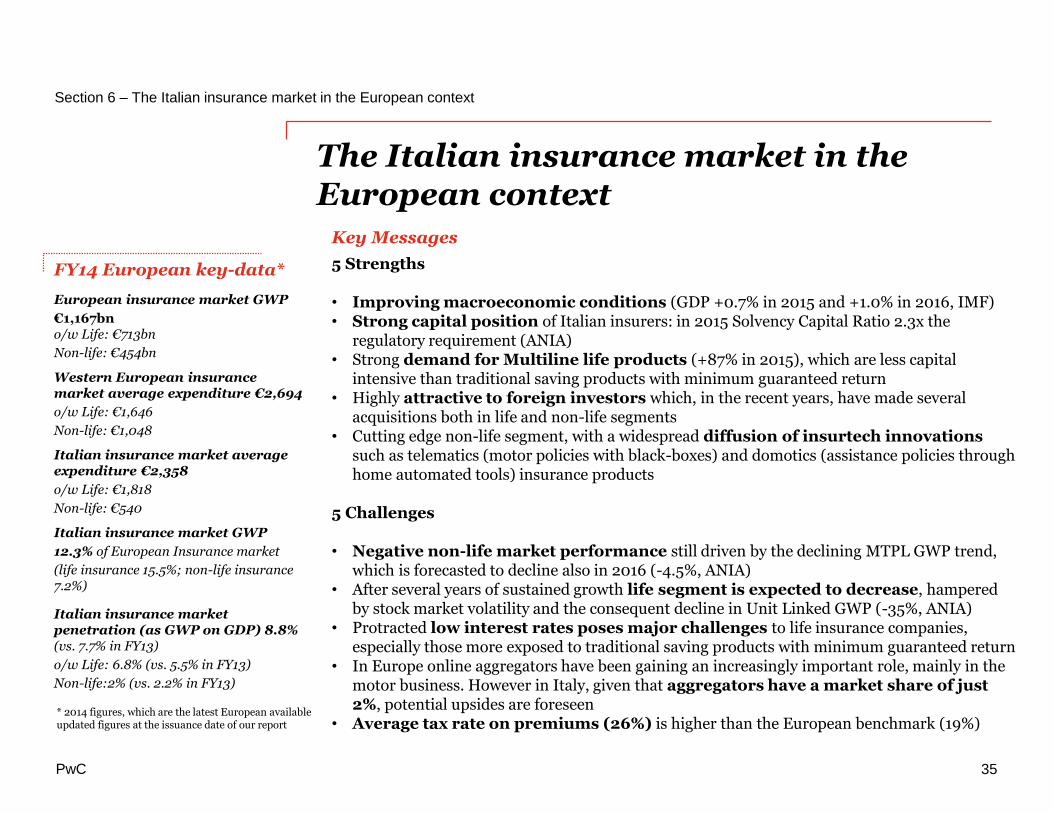

FY14 European key-data*

European insurance market GWP

€1,167bno/w Life: €713bn

Non-life: €454bn

Western European insurance market average expenditure €2,694

o/w Life: €1,646

Non-life: €1,048

Italian insurance market average expenditure €2,358

o/w Life: €1,818

Non-life: €540

Italian insurance market GWP

12.3% of European Insurance market

(life insurance 15.5%; non-life insurance 7.2%)

Italian insurance market penetration (as GWP on GDP) 8.8% (vs. 7.7% in FY13)

o/w Life: 6.8% (vs. 5.5% in FY13)

Non-life:2% (vs. 2.2% in FY13)

Section 6 – The Italian insurance market in the European context

35

The Italian insurance market in the European context

Key Messages

5 Strengths

• Improving macroeconomic conditions (GDP +0.7% in 2015 and +1.0% in 2016, IMF)• Strong capital position of Italian insurers: in 2015 Solvency Capital Ratio 2.3x the

regulatory requirement (ANIA)• Strong demand for Multiline life products (+87% in 2015), which are less capital

intensive than traditional saving products with minimum guaranteed return• Highly attractive to foreign investors which, in the recent years, have made several

acquisitions both in life and non-life segments• Cutting edge non-life segment, with a widespread diffusion of insurtech innovations

such as telematics (motor policies with black-boxes) and domotics (assistance policies through home automated tools) insurance products

5 Challenges

• Negative non-life market performance still driven by the declining MTPL GWP trend, which is forecasted to decline also in 2016 (-4.5%, ANIA)

• After several years of sustained growth life segment is expected to decrease, hampered by stock market volatility and the consequent decline in Unit Linked GWP (-35%, ANIA)

• Protracted low interest rates poses major challenges to life insurance companies, especially those more exposed to traditional saving products with minimum guaranteed return

• In Europe online aggregators have been gaining an increasingly important role, mainly in the motor business. However in Italy, given that aggregators have a market share of just 2%, potential upsides are foreseen

• Average tax rate on premiums (26%) is higher than the European benchmark (19%)* 2014 figures, which are the latest European available updated figures at the issuance date of our report

PwC

90 74 70 85111

0

143 124 113 119 129

0

90 87 87 91 94

022 22 19 18 17 0

27 30 27 26 250

159 167 173 184 17636

36 3534

33

0

6264 66 67

68

0

88 91 94 97 99

0

56 57 56 57 56

0

29 30 30 29 29

0

67 67 6969

66

126110 105

119143

205188 179 186 197

179 178 182 187 193

78 79 75 75 7456 60 57 55 54

227 234 242 253241

FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14

€b

illi

on

Life market Non-life market

France Germany Netherlands Spain United KingdomItaly

European insurance market

Section 6 – The Italian insurance market in the European context

36

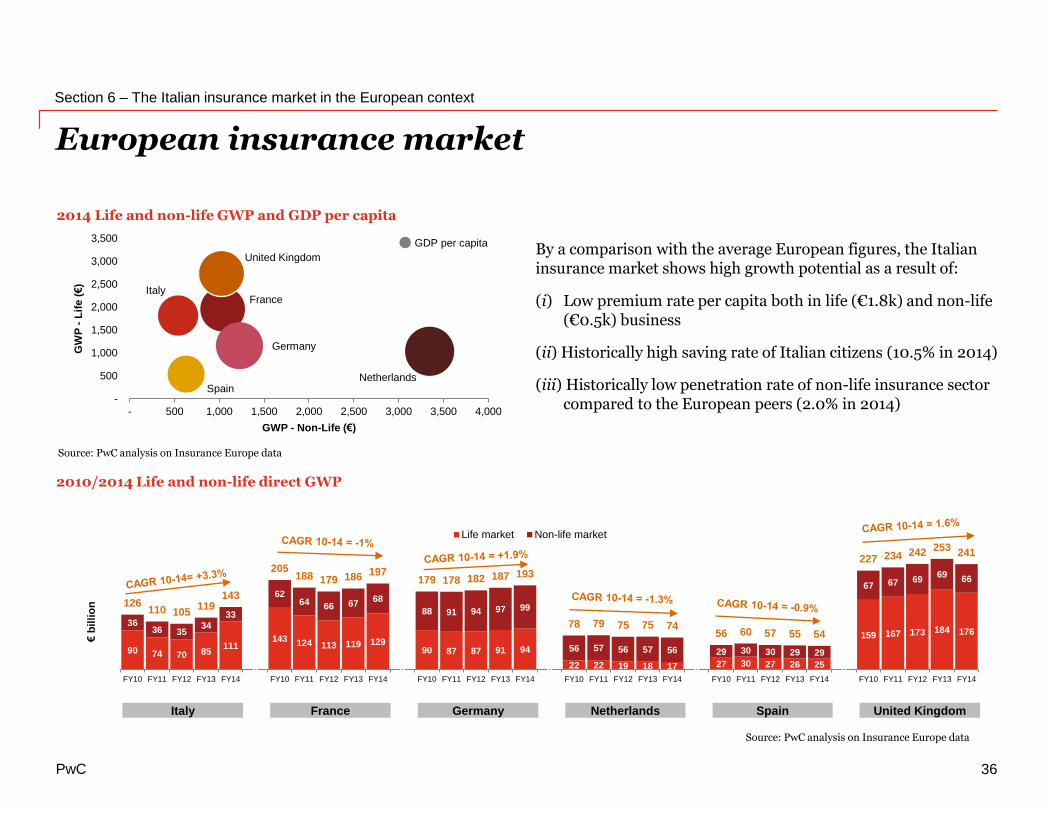

By a comparison with the average European figures, the Italian insurance market shows high growth potential as a result of:

(i) Low premium rate per capita both in life (€1.8k) and non-life (€0.5k) business

(ii) Historically high saving rate of Italian citizens (10.5% in 2014)

(iii) Historically low penetration rate of non-life insurance sector compared to the European peers (2.0% in 2014)

2010/2014 Life and non-life direct GWP

2014 Life and non-life GWP and GDP per capita

Source: PwC analysis on Insurance Europe data

Source: PwC analysis on Insurance Europe data

GDP per capita

ItalyFrance

Germany

NetherlandsSpain

United Kingdom

-

500

1,000

1,500

2,000

2,500

3,000

3,500

- 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

GW

P -

Lif

e (

€)

GWP - Non-Life (€)

PwC

4.4%

5.6%

3.3% 3.2%2.6%

9.0%

5.5% 5.8%

3.3%2.9%

2.5%

8.5%

6.8%

6.0%

3.2%

2.4% 2.3%

n.a.

Italy France Germany Netherlands Spain UnitedKingdom

FY12 FY13 FY14

2012/2014 Ratio of non-life premiums to GDP

2.3%

3.3% 3.5%

9.4%

2.9%3.5%

2.2%

3.4% 3.5%

8.9%

3.0% 3.3%

2.0%

3.3% 3.4%

8.1%

2.9%

n.a.

Italy France Germany Netherlands Spain UnitedKingdom

FY12 FY13 FY14

European insurance premiums penetration

Section 6 – The Italian insurance market in the European context

37

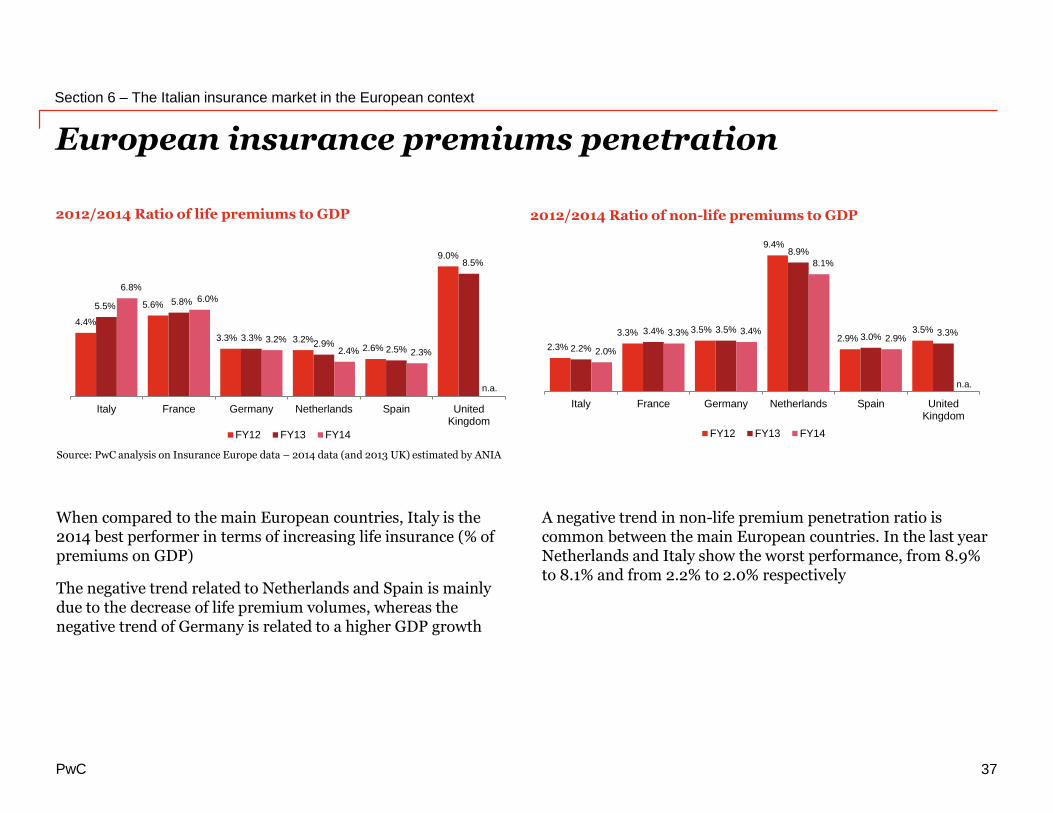

2012/2014 Ratio of life premiums to GDP

When compared to the main European countries, Italy is the 2014 best performer in terms of increasing life insurance (% of premiums on GDP)

The negative trend related to Netherlands and Spain is mainly due to the decrease of life premium volumes, whereas the negative trend of Germany is related to a higher GDP growth

Source: PwC analysis on Insurance Europe data – 2014 data (and 2013 UK) estimated by ANIA

A negative trend in non-life premium penetration ratio is common between the main European countries. In the last year Netherlands and Italy show the worst performance, from 8.9% to 8.1% and from 2.2% to 2.0% respectively

PwC

Distribution channels

Section 6 – The Italian insurance market in the European context

38

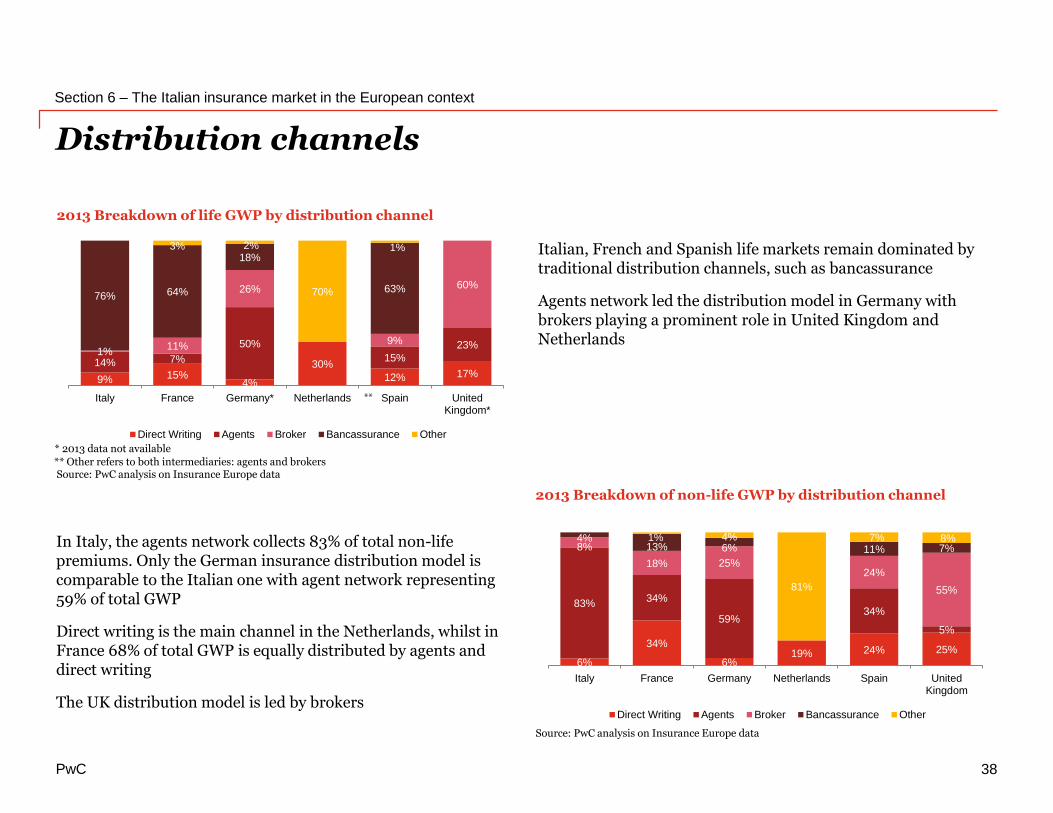

Italian, French and Spanish life markets remain dominated by traditional distribution channels, such as bancassurance

Agents network led the distribution model in Germany with brokers playing a prominent role in United Kingdom and Netherlands

In Italy, the agents network collects 83% of total non-life premiums. Only the German insurance distribution model iscomparable to the Italian one with agent network representing 59% of total GWP

Direct writing is the main channel in the Netherlands, whilst in France 68% of total GWP is equally distributed by agents and direct writing

The UK distribution model is led by brokers

2013 Breakdown of life GWP by distribution channel

2013 Breakdown of non-life GWP by distribution channel

Source: PwC analysis on Insurance Europe data

7%

6%

34%

6%19% 24% 25%

83%34%

59%34%

5%

8%

18% 25%24%

55%

4%13% 6% 11% 7%1% 4%

81%

7% 8%

Italy France Germany Netherlands Spain UnitedKingdom

Direct Writing Agents Broker Bancassurance Other

Source: PwC analysis on Insurance Europe data

* 2013 data not available

** Other refers to both intermediaries: agents and brokers

9% 15%4%

30%

12% 17%14% 7%

50%

15%

23%1%

11%

26%

9%

60%76% 64%

18%

63%

3% 2%

70%

1%

Italy France Germany* Netherlands Spain UnitedKingdom*

Direct Writing Agents Broker Bancassurance Other

**

PwC

Average GWP per insurance company

Section 6 – The Italian insurance market in the European context

39

2012/2014 Number of insurance companies

2012/2014 Average GWP per insurance company

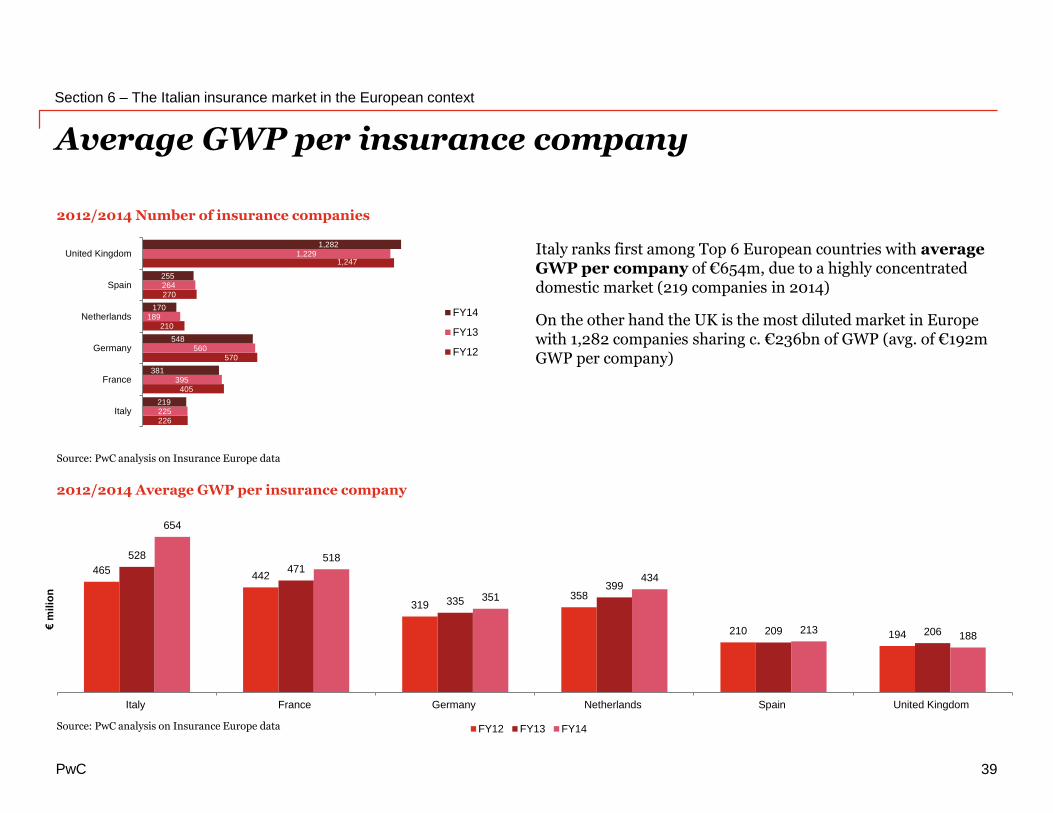

Italy ranks first among Top 6 European countries with average GWP per company of €654m, due to a highly concentrated domestic market (219 companies in 2014)

On the other hand the UK is the most diluted market in Europe with 1,282 companies sharing c. €236bn of GWP (avg. of €192m GWP per company)

Source: PwC analysis on Insurance Europe data

Source: PwC analysis on Insurance Europe data

226

405

570

210

270

1,247

225

395

560

189

264

1,229

219

381

548

170

255

1,282

Italy

France

Germany

Netherlands

Spain

United Kingdom

FY14

FY13

FY12

465442

319358

210 194

528

471

335

399

209 206

654

518

351

434

213188

Italy France Germany Netherlands Spain United Kingdom

€m

ilio

n

FY12 FY13 FY14

PwC

13.5% 13.7% 14.9% 14.3% 14.0% 14.2%

3.8% 3.3% 3.3% 3.1% 3.1% 3.1%

40.7% 40.5% 40.8% 42.1% 42.3% 42.7%

12.4% 12.0% 10.6% 11.0% 10.6% 9.9%

22.7% 24.0% 24.3% 23.4% 23.1% 23.4%

6.9% 6.6% 6.1% 6.1% 6.8% 6.6%

FY08 FY09 FY10 FY11 FY12 FY13

Equities and Participations Real Estate Bonds Loans Investment Funds Other

0.4 0.4 0.5 0.5 0.5

1.5 1.51.7 1.7

1.9

0.8 0.8 0.9 0.9 1.1

0.3 0.3 0.4 0.3 0.40.2 0.2 0.2 0.2 0.2

1.6 1.6 1.7 1.8 1.9

0.1 0.1 0.1 0.1 0.1

0.2 0.2

0.20.2

0.2

0.6 0.60.7 0.7

0.8

0.0 0.0 0.0 0.1 0.1

0.0 0.0 0.0 0.0 0.0

0.1 0.1 0.10.1

0.1

0.5 0.5 0.5 0.6 0.6

1.7 1.71.9

1.9

2.1

1.4 1.51.6 1.6

1.8

0.4 0.40.4 0.4 0.5

0.2 0.2 0.2 0.2 0.2

1.7 1.7 1.81.9 2.0

FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14 FY10 FY11 FY12 FY13 FY14

€tr

illi

on

Life market Non-life market

France Germany Netherlands Spain United KingdomItaly

Investments portfolio

Section 6 – The Italian insurance market in the European context

40

2008/2013 Breakdown of investments

2010/2014 Investments portfolio

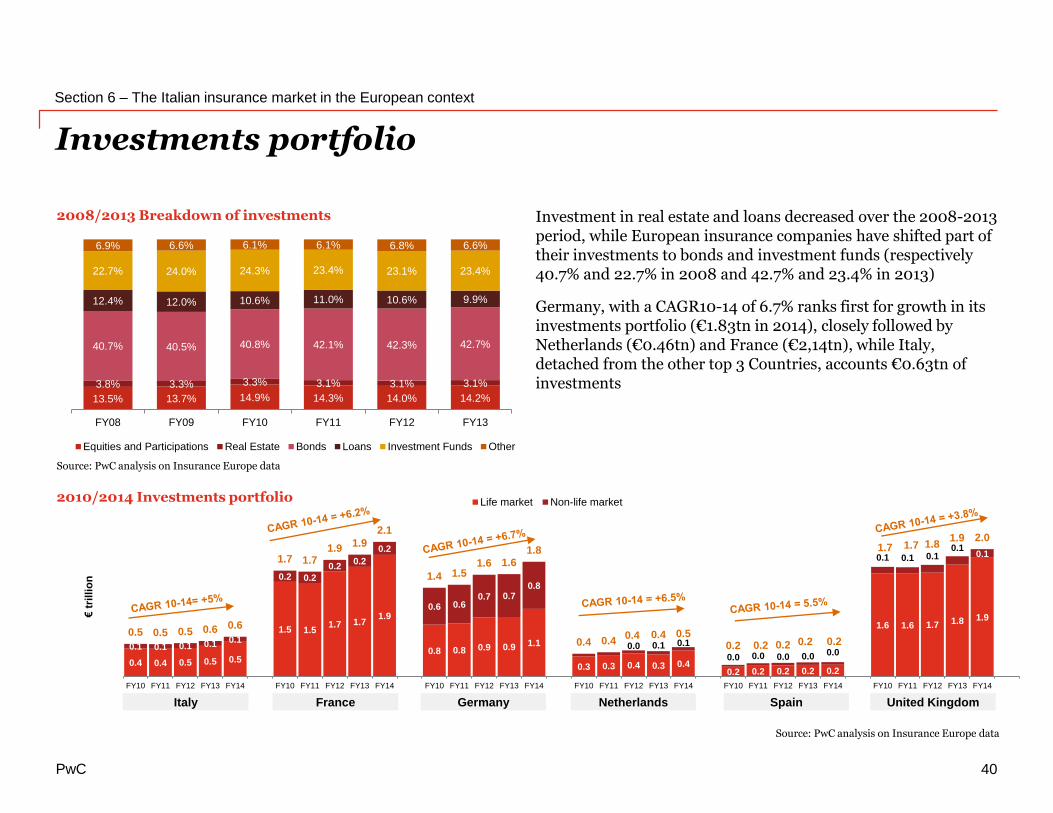

Investment in real estate and loans decreased over the 2008-2013 period, while European insurance companies have shifted part of their investments to bonds and investment funds (respectively40.7% and 22.7% in 2008 and 42.7% and 23.4% in 2013)

Germany, with a CAGR10-14 of 6.7% ranks first for growth in its investments portfolio (€1.83tn in 2014), closely followed by Netherlands (€0.46tn) and France (€2,14tn), while Italy,detached from the other top 3 Countries, accounts €0.63tn of investments

Source: PwC analysis on Insurance Europe data

Source: PwC analysis on Insurance Europe data

Our contacts

© 2016 PricewaterhouseCoopers Advisory SpA. All rights reserved. In this document, “PwC” refers

to PricewaterhouseCoopers Advisory SpA which is a member firm of PricewaterhouseCoopers

International Limited, each member firm of which is a separate legal entity.

Emanuele GrassoPartner | Financial Services

+39 02 7785 372+39 348 [email protected]

Liana VojkollariSenior Manager | Financial Services

+39 02 7785 008+39 346 [email protected]

Gabriele PicutiSenior Associate | Financial Services

+39 345 [email protected]

Marco FalcheroDirector | Financial Services

+39 02 7785 951+39 335 [email protected]