the international crisis and latin america: growth...

TRANSCRIPT

World Bank Seminar on “Managing Openness:Outward-oriented Growth Strategies after the Crisis”

May 10, 2010Washington, DC

:::

:::The International Crisis and Latin America:Growth Effects and Development Strategies

Vittorio CorboKlaus Schmidt-Hebbel

::: Outline

1. Introduction

2. Data

3. Dating Recessions

4. Growth Model and Empirical Strategy

5. Estimation Results

6. Decomposing the Amplitude of the 1998-99 and 2008-09 Recessions

7. Implications for Policies and Growth Strategies

8. Final Remarks

:::

1. Introduction

::: Is Latin America different now? (1)

• LatAm was hit by both the 1998-1999 Asian Crisis and the 2008-2009 Global Crisis

• Yet significant structural and policy changes were implemented by many countries in LAC during the past decade

• Hence were the effects of the international crises and recessions on LatAm different this time?

::: Is Latin America different now (2)?

• We address this question in four steps:

(1) identification and dating of both recessions

(2) estimation of GDP growth performance based on short and long-term growth factors

(3) decomposition of amplitude of both recessions and the role of individual growth determinants –international factors, structural conditions, and policy responses

(4) main implications of crises for Latin America and some strategies to grow out of the crisis

:::

2. Data

::: Data

• Country Sample

– Seven major LAC countries: Argentina, Brazil, Chile, Colombia, Mexico, Peru and Venezuela (91% of LAC’s GDP in 2008)

• Time Sample

– Quarterly data, 1990:1-2009:4

::: Average GDP Growth in LatAm

Simple average of annualized quarterly GDP growth rates of seven major Latin American countries, based on official GDP series that are seasonally adjusted by national authorities.

::: GDP growth in LatAm countries (1)

::: GDP growth in LatAm countries (2)

::: GDP growth in LatAm countries (3)

::: Average Output Gap in LatAm

Simple average of output gaps of seven major Latin American countries, based on official GDP series that are seasonally adjusted by national authorities and the Baxter-King filter.

:::

3. Dating of Recessions

::: Dating of recessions (1)

• Starting points: based on Calvo (2005) and Eichengreen and O’Rourke (2009)

• Fixed effects panel regression of GDP growth on two dummy variables for two recessions

• Search conducted by extending end-points by several quarters

::: Dating of recessions (2)

• Final dating based on largest and most significant dummy parameter estimates

• Results for average LatAm economy (panel-data!) – different for individual economies

• Final dating of recessions for LatAm:– Asian crisis: 1998q3 – 1999q2– Global crisis: 2008q4 – 2009q2

• Growth lowered by 7.6 and 8.6 p.p. respectively

::: Dating of recessions (3)Estimation Method: Fixed-effects (within) regression

Dependent Variable: Growth of Real GDP

Time Sample: 1990:1-2009:4 (quarterly frecuency)

Countries: ARG - BRA - CHI -COL -MEX - PER - VEN

Global Financial Crisis Period

Asian Crisis Period

Asian Global Asian Global Asian Global

1998q3-1999q2 -0.077*** -0.071*** -0.076*** -0.086*** -0.076*** -0.113***

(-6.333) (-5.358) (-6.317) (-5.820) (-6.290) (-6.658)

1998q2-1999q2 -0.067*** -0.071*** -0.067*** -0.087*** -0.066*** -0.113***

(-5.731) (-5.380) (-5.714) (-5.840) (-5.684) (-6.674)

1998q1-1999q2 -0.065*** -0.072*** -0.064*** -0.087*** -0.064*** -0.114***

(-6.058) (-5.427) (-6.040) (-5.881) (-6.009) (-6.710)

1997q4-1999q2 -0.056*** -0.072*** -0.055*** -0.087*** -0.055*** -0.114***

(-5.470) (-5.419) (-5.451) (-5.874) (-5.417) (-6.704)

1997q3-1999q2 -0.047*** -0.072*** -0.046*** -0.087*** -0.046*** -0.113***

(-4.712) (-5.393) (-4.691) (-5.852) (-4.654) (-6.684)

1997q2-1999q2 -0.035*** -0.071*** -0.035*** -0.086*** -0.034*** -0.113***

(-3.471) (-5.325) (-3.448) (-5.792) (-3.409) (-6.632)

1998q3-1999q3 -0.062*** -0.071*** -0.062*** -0.086*** -0.061*** -0.113***

(-5.394) (-5.353) (-5.377) (-5.816) (-5.347) (-6.654)

1998q3-1999q4 -0.049*** -0.071*** -0.049*** -0.086*** -0.049*** -0.112***

(-4.356) (-5.331) (-4.337) (-5.797) (-4.305) (-6.637)

1998q3-2000q1 -0.038*** -0.070*** -0.038*** -0.086*** -0.037*** -0.112***

(-3.407) (-5.295) (-3.386) (-5.765) (-3.352) (-6.609)

1998q3-2000q2 -0.042*** -0.071*** -0.041*** -0.087*** -0.041*** -0.113***

(-4.045) (-5.354) (-4.023) (-5.817) (-3.986) (-6.654)

1998q3-2000q3 -0.042*** -0.072*** -0.041*** -0.087*** -0.041*** -0.113***

(-4.255) (-5.387) (-4.233) (-5.846) (-4.194) (-6.679)

1998q3-2000q4 -0.040*** -0.072*** -0.040*** -0.088*** -0.039*** -0.114***

(-4.330) (-5.406) (-4.307) (-5.863) (-4.266) (-6.693)

Observations

t-stats calculated using robust standard errors in parentheses

*** p<0.01, ** p<0.05, * p<0.1

Estimated Parameters

553

2008q3-2009q2 2008q4-2009q1

Estimated Parameters

553

Estimated Parameters

2008q4-2009q2

553

::: Average GDP growth in LatAm around crises

Global Financial

Crisis

Asian Crisis

:::

4. Growth Model and Empirical Strategy

::: Specification and Data

• Data

– Unbalanced panel of 1990.1–2009.4 quarterly data for seven countries

• Estimation Method

– Multivariate dynamic fixed-effects unbalanced panel-data regressions

::: Literature (1)

• Long-term determinants of growth

– Barro (1991), King and Levine (1993), Easterly and Rebelo (1993), Easterly, Loayza, and Montiel (1997), Levine, Loayza, and Beck (2000), Dollar and Kraay (2002), Calderón, Fajnzylber and Loayza (2004), Barro and Sala-i-Martin (2004), and Calderón, Loayza and Schmidt-Hebbel (2006).

• Short-term determinants of growth

– Every short-term macroeconomic model – including the DSGE models used in short-term macroeconomic analysis and projections.

::: Literature (2)

• Medium-term determinants of growth

– IMF’s WEO (chap. 4, 2009).

• Recession in Latin America

– Österholm and Zettelmeyer (2007), Caruana (2009), Jara, Moreno and Tovar (2009), IADB (2009a), IADB (2009b), IMF (2009a), IMF (2009b), Ocampo (2009), World Bank (2009) and Soto (2010).

::: Behavior of growth in LatAm (1)

• Specification: Multivariate dynamic fixed-effects panel data

regression that nests long and short-term growth determinants and potential interaction effects:

• where:

– y : dependent variable

– X : long-term growth variables

– K : domestic policy variables

– M : structural variables

– Z : foreign cyclical variables

– with interactions between M and Z,

– and allowing for structural breaks in coefficients after 2000

itiMZititZit

MitKitXititit

ZMZ

MKXyy

''

'''1

23

::: Behavior of growth in LatAm (2)

(1) Long-term growth variables• Private Credit, Secondary School Enrollment, Inflation

Rate, Fiscal Balance, and Political Certainty(2) Structural variables• Financial and Trade Openness, Net External Assets,

International Foreign Reserves, and Exchange Rate Regime

(3) Foreign cyclical variables• Channels of transmission: Terms of Trade Growth,

Growth of Trading Partners and of World Exports, Capital Inflows to LatAm, and Sovereign Spreads

(4) Domestic policy variables• Government Consumption and ex-ante Real Interest

Rate(5) Interactions of structural and foreign cyclical

variables

:::

5. Estimation Results

25

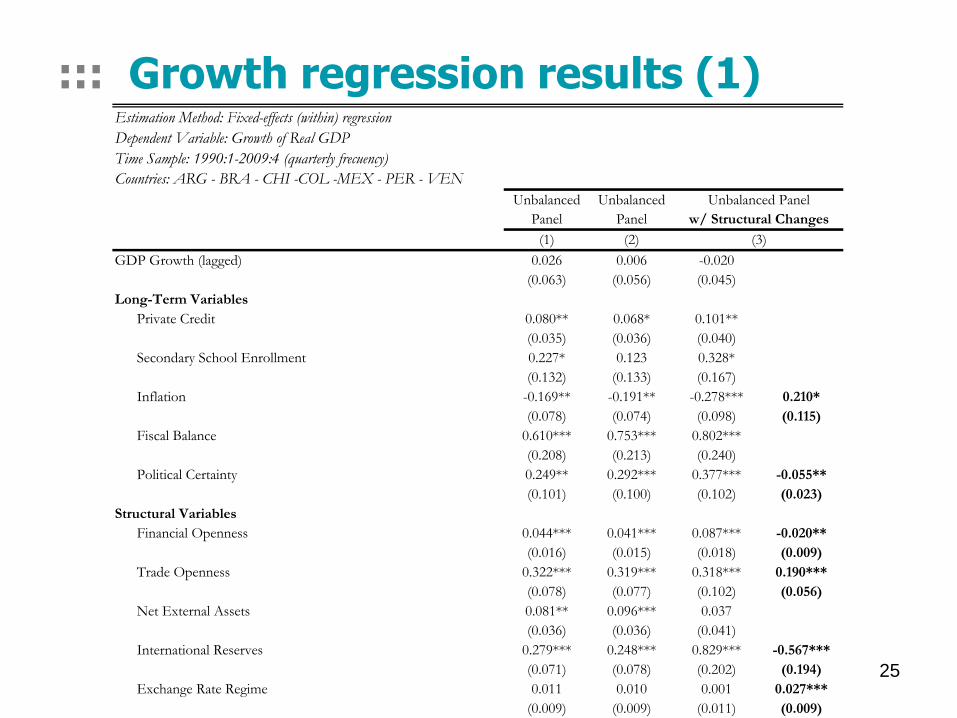

::: Growth regression results (1)Estimation Method: Fixed-effects (within) regression

Dependent Variable: Growth of Real GDP

Time Sample: 1990:1-2009:4 (quarterly frecuency)

Countries: ARG - BRA - CHI -COL -MEX - PER - VEN

Unbalanced Unbalanced

Panel Panel

(1) (2)

GDP Growth (lagged) 0.026 0.006 -0.020

(0.063) (0.056) (0.045)

Long-Term Variables

Private Credit 0.080** 0.068* 0.101**

(0.035) (0.036) (0.040)

Secondary School Enrollment 0.227* 0.123 0.328*

(0.132) (0.133) (0.167)

Inflation -0.169** -0.191** -0.278*** 0.210*

(0.078) (0.074) (0.098) (0.115)

Fiscal Balance 0.610*** 0.753*** 0.802***

(0.208) (0.213) (0.240)

Political Certainty 0.249** 0.292*** 0.377*** -0.055**

(0.101) (0.100) (0.102) (0.023)

Structural Variables

Financial Openness 0.044*** 0.041*** 0.087*** -0.020**

(0.016) (0.015) (0.018) (0.009)

Trade Openness 0.322*** 0.319*** 0.318*** 0.190***

(0.078) (0.077) (0.102) (0.056)

Net External Assets 0.081** 0.096*** 0.037

(0.036) (0.036) (0.041)

International Reserves 0.279*** 0.248*** 0.829*** -0.567***

(0.071) (0.078) (0.202) (0.194)

Exchange Rate Regime 0.011 0.010 0.001 0.027***

(0.009) (0.009) (0.011) (0.009)

Unbalanced Panel

w/ Structural Changes

(3)

26

::: Growth regression results (2)Foreign Cyclical Variables

Terms of Trade Growth 0.012 0.007 0.009

(0.009) (0.009) (0.010)

Growth of Trading Partners 0.221* 0.215 0.224

(0.133) (0.138) (0.137)

Growth of World Exports 0.081*** 0.082*** 0.081***

(0.022) (0.022) (0.021)

Capital Inflows to Latin America 0.573** 0.475** 0.419*

(0.244) (0.239) (0.252)

Sovereign Spreads -0.040 -0.023 -0.039 -0.032

(0.057) (0.058) (0.059) (0.020)

Domestic Policy Variables

Government Consumption 1.386*** 1.362*** 1.516***

(0.328) (0.319) (0.304)

Real Interest Rate -0.168** -0.192*** -0.326*** 0.289**

(0.071) (0.068) (0.077) (0.119)

Interactions

Growth of Trading Partners * Trade Openness 1.170* 0.995

(0.657) (0.607)

Growth of Trading Partners * Financial Openness -0.629* -0.385

(0.332) (0.301)

Capital Inflows to Latin America * Financial Openness -1.232** -0.677

(0.603) (0.609)

Sovereign Spreads * Net External Assets 0.284** 0.377***

(0.125) (0.130)

Constant -0.288** -0.274** -0.497***

(0.122) (0.118) (0.139)

Observations 462 462 462

R-squared 0.670 0.680 0.707

*** p<0.01, ** p<0.05, * p<0.1

Robust standard errors in parentheses

::: Significant growth factors

• Long-term growth determinants: financial depth, school enrollment, inflation (less since 2001), fiscal balance, political certainty (less since 2001)

• Structural variables: financial openness (less since 2001), trade openness (more since 2001), international reserves (less since 2001), exchange rate regime (only since 2001)

• Foreign cyclical variables: foreign trading partners’ growth, world export growth, capital inflows. Note: terms of trade and sovereign spreads not significant!

• Domestic policy variables: government consumption, real interest rate

• Four significant interaction effects• Significant structural breaks in 2001 for 7 variables

:::

6. Decomposing the Amplitude of the 1998-99 and 2008-09 Recessions

::: Dissecting LatAm’s recessions

• Compare LatAm’s growth performance in both recessions

• Decompose amplitude of the recession in both events – the average cumulative GDP decline in 7 individual countries between last quarter before the recession and last quarter of the recession

• Decomposition allows to identify the most relevant recession determinants in both crises

• Within-crisis decomposition:

MZititZitMitKitXitit ZMZMKXy ˆ)'(ˆ'ˆ'ˆ'ˆ'

::: Recessions in LatAm

Cumulative GDP growth rates during recessions

Asian Global Financial

Crisis Crisis

1998q3-1999q2 2008q4-2009q2

Argentina -5,20% -1,55%

Brazil -1,03% -3,99%

Chile -3,88% -4,40%

Colombia -6,82% -0,87%

Mexico 3,37% -11,09%

Peru 1,15% -3,64%

Venezuela -8,51% -3,59%

Simple Average -2,99% -4,16%

Weighted Average -1,15% -5,24%

Amplitude of GDP Growth Decline

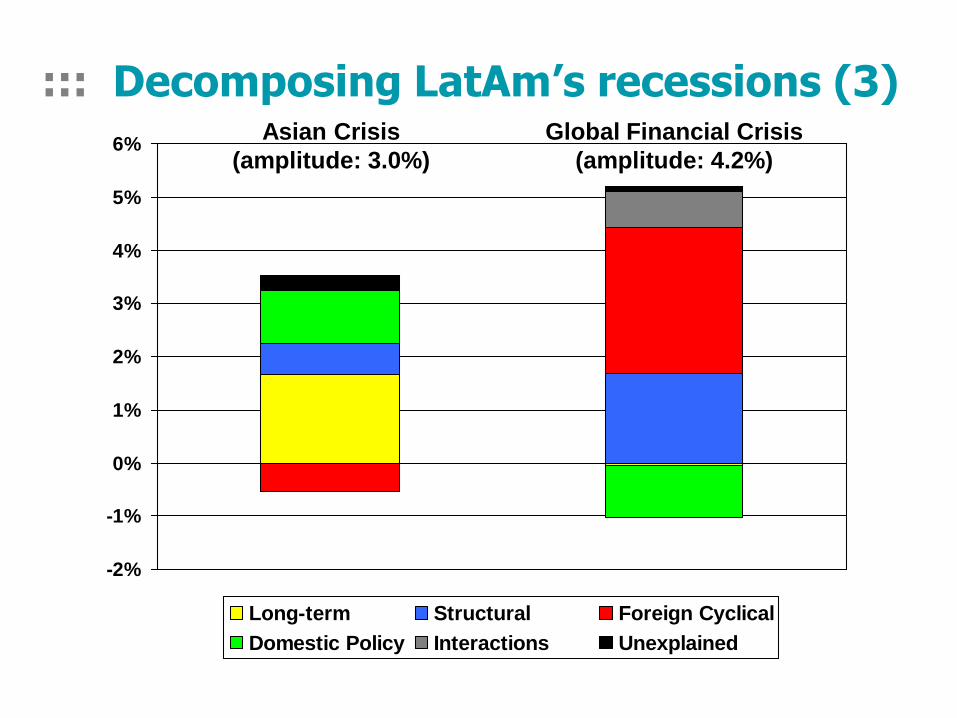

::: Decomposing LatAm’s recessions (1)

Asian Global Financial

Crisis Crisis

1998q3-1999q2 2008q4-2009q2

Amplitude of GDP Growth Decline -2.99% -4.16%

NO Changes YES

Sources:

Long-Term Variables -1.68% 0.77% 0.05%

Private Credit 0.24% 0.44% 0.44%

Inflation 0.65% 0.97% -0.73% 0.24%

Secondary School Enrollment -0.14% 0.15% 0.15%

Fiscal Balance -1.17% -0.73% -0.73%

Political Certainty -1.26% -0.06% 0.01% -0.05%

Structural Variables -0.57% 0.59% -1.70%

Financial Openness 0.73% -0.60% 0.14% -0.46%

Trade Openness -0.53% -1.32% -0.79% -2.11%

Net External Assets -0.08% 0.08% 0.08%

International Reserves -0.68% 2.43% -1.64% 0.79%

Exchange Rate Regime -0.01% 0.00% 0.00% 0.00%

Structural Changes

::: Decomposing LatAm’s recessions (2)Foreign Cyclical Variables 0.54% -2.60% -2.74%

Terms of Trade Growth 0.02% -0.32% -0.32%

Growth of Trading Partners 0.26% -1.36% -1.36%

Growth of World Exports 0.53% -0.05% -0.05%

Capital Inflows to Latin America -0.05% -0.68% -0.68%

Sovereign Spreads -0.22% -0.19% -0.14% -0.33%

Domestic Policy Variables -0.99% -0.14% 0.99%

Government Consumption 0.69% 1.12% 1.12%

Real Interest Rate -1.68% -1.26% 1.13% -0.13%

Interactions -0.02% -0.67% -0.67%

Growth of Trading Partners * Trade Openness 0.00% -0.19% -0.19%

Growth of Trading Partners * Financial Openness 0.10% -0.35% -0.35%

Capital Inflows to Latin America * Financial Openness -0.09% -0.10% -0.10%

Sovereign Spreads * Net External Assets -0.02% -0.03% -0.03%

Structural Changes post-2000 -2.02%

Explained Variation -2.72% -4.07% -4.07%

Unexplained Variation -0.26% -0.09% -0.09%

Total Variation -2.99% -4.16% -4.16%

::: Decomposing LatAm’s recessions (3)

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Long-term Structural Foreign Cyclical

Domestic Policy Interactions Unexplained

Global Financial Crisis

(amplitude: 4.2%)

Asian Crisis

(amplitude: 3.0%)

• (Unweighted) average amplitude of both recessions was larger this time – a cumulative -3.0% vs. -4.2%

• Our explained variation is -2.7% for 1998-99 and -4.1% for 2008-09

• 1998-99 recession: largely due to domestic factors, NOT to foreign cyclical variables:– Lower inflation and rising financial openness dampened the

recession

– Higher political uncertainty and rising country risk spreads deepened the recession

– Positive growth of world GDP and exports dampened the recession

– Fiscal policy (higher fiscal balance and government consumption) deepened the recession

– Higher interest rates and lower international reserves, in defense of non-flexible exchange-rate regimes, contributed strongly to the recession

::: Explaining LatAm’s recessions (1)

• 2008-09 recession: in contrast to 1998-09, largely due to the world recession, i.e., foreign cyclical variables

– All five foreign cyclical variables contributed to the recession, jointly they explain 2.7% of 4.1%

– Collapsing growth of LatAm’s trading partners made the largest contribution

– Declining trade – through lower trade openness and negative world trade growth – deepened significantly the recession

– Lower inflation and rising international reserves dampened the recession

– Fiscal policy (lower fiscal balance + higher government consumption) was largely neutral for growth

– Monetary policy: 2009 nominal interest rate reductions were more than offset by inflation decline; hence real interest rates increased. But their effect on growth is close to nil after 2001.

::: Explaining LatAm’s recessions (2)

:::

7. Implications for Policies and Growth Strategies

• Most LatAm countries carried out important policy and institutional reforms aimed at strengthening their macro fundamentals.

– improving their fiscal accounts, putting in place inflation targeting monetary frameworks -to reduce inflation towards single digit annual levels- and introducing more flexible exchange rate regimes

– public debt to GDP ratios have improved as well as the stock of gross external debt to GDP ratio

– when the global financial crisis struck, the size of their macroeconomic imbalances were manageable

– therefore, domestic policy did not amplify the recession this time

::: Policies and Growth Strategies (1)

• In spite of the progress that has been achieved, Latin America has still a pending agenda:

1. to raise in a sustainable way its rate of growth

2. to make further progress in reducing poverty

3. improving its income distribution

• Limited state capacity

– public policies are unpredictable, slow to be implemented and costly for businesses

– the merit system is not common in the public sector

– public services are of low quality

– investor protection leaves much room to be improved

– enforcement of contracts is expensive and slow

::: Policies and Growth Strategies (2)

• Raising Total Factor Productivity– LatAm still has in place important entry and exit barriers to

business, limiting the process of creative destruction

– rigid labor laws (including high minimum wages) distort wages

– limitations to adjust working hours and high firing costs– These restrictions complicate participation of low-skilled workers

in formal labor markets, especially low-skilled youth and mothers

• LatAm still ranks very low in internationaleducation achievement tests.

• Policy reforms focused at reaising labor rpoductivity and productive efficiency are key for raising aggregate income and income of the poor and unskilled in particular, contributing to lower poverty and improved income distribution.

::: Policies and Growth Strategies (3)

:::

8. Final Remarks

::: Is LatAm different now? (1)

• On average, yes

• LatAm has improved its macro policy framework: – Strengthening macro regimes by shifting from less

discretion to more rules– Exchange-rate regime: adopting (largely dirty) floating

ER regimes (effective dampener of foreign shocks)– Strengthening monetary policy regime by adopting

fuller-fledged versions of flexible IT

• LatAm has also improved structural conditions:– strengthened global links through trade and financial

openness– strengthened external positions, especially foreign

reserve positions (consistent with dirty floats)

::: Is LatAm different now? (2)

• More openness has contributed to higher growth but partly exposed the region to the effects of adverse foreign shocks

• However: LatAm is still very heterogeneous, exhibiting large (and possibly increasing) heterogeneity in regimes and policies, as well as in performance records

• LatAm still faces a long agenda of economic and institutional reforms to spur growth, raise its resilience to foreign shocks, and defeat proverty.

::: Is LatAm different now? (3)

(1) Continue improving macro-financial policy framework

• Adopt full-fledged IT (or PLT), clean up dirty ER floats, adopt fiscal rules and policy regimes (independent fiscal councils)

• Adopt the world’s (still evolving) best practice in macro-prudential regulation

(2) Deepen globalization

• Strengthen unilateral trade and financial integration into world markets

• Maintain plain level field: resist Tobin taxes on portfolio flows, subsidies to FDI, trade protection, picking sector winners

(3) Deepen and widen structural reforms: micro incentives, education, labor markets, government reform – in support of higher long-term growth

:::

9. Appendix

::: Long-term growth determinants

Note: Simple averages for seven major Latin American economies.

::: Structural growth determinants

Note: Simple averages of seven major Latin American economies.

::: Foreign cyclical variables

Note: Simple averages of seven major Latin American economies.

::: Domestic policy variables

Note: Simple averages of seven major Latin American economies.

World Bank Seminar on “Managing Openness:Outward-oriented Growth Strategies after the Crisis”

May 10, 2010Washington, DC

:::

:::The International Crisis and Latin America:Growth Effects and Development Strategies

Vittorio CorboKlaus Schmidt-Hebbel