the indian tractor industry : buckle up for more rough...

TRANSCRIPT

The Indian Tractor Industry : Buckle up for more rough weather ahead

BSE Auto vs. Sensex

Performance (%)

1m 3m 12m

Sensex 6.6% -1.8% -10.5%

BSE Auto 5.4% -4.2% -8.6%

Market data

BSE SENSEX 25285

Nifty 7704

BSE Autos 17541

Tractor Sector Update

Date 22nd Mar’ 2016

MUKESH SARAF [email protected] +91 44 4344 0041

RAMAKRISHNAN SESHAN [email protected] +91 44 4344 0020Find Spark Research on Bloomberg (SPAK <go>),

Thomson First Call, Reuters Knowledge and Factset

As part of our periodic dealer channel check exercise, between Mar 15 – Mar 21, 2016, we interacted with around 75

tractor dealers (across OEMs) operating in key states across India. The objective of the exercise was to gauge thedealer sentiments on the back of the seemingly bottomless spiral the tractor industry finds itself in. We enquired of

the dealers the impact of recent trends and data-points having a bearing on near-term tractor demand including

1) unseasonal rains/hail impacting North and Central India 2) near record-low reservoir levels across the country3) rocketing dealer inventory and discounting levels, juxtaposed against 4) positives of increasing MSPs and

5) improving prospects of non-agri. demand led by increasing investments in the rural sector. Additionally, we also

interacted with industry experts and managements of leading OEMs to the same end. Our findings are as under

No let up in demand weakness expected over the near term: Tractor demand for Mar’16 is expected to be weak,

conforming with trends seen through FY16, capping what has been the worst year for the tractor industry since FY11

Dealers in major tractor markets were pessimistic about prospects of a meaningful pick up in demand over the near term aswell on the back of a combination of factors (covered in greater detail on pages 8-9 of this report) including payment

arrears/stagnant state-advised-prices for sugarcane in UP, unseasonal rain/hail impacting standing rabi crops (importantly,

wheat) in major North and Central Indian states, sustained drought conditions in Maharashtra, lower demand for gaur (gum)in Rajasthan due to fall in crude prices, crash in basmati prices impacting Punjab and Haryana, and true to form, lack of

decisive policy making (potato procurement prices not yet announced) impacting farmers in Orissa.

On the positive side, a relatively better monsoon in UP (the largest tractor market) favorably impacting produce of all majorcrops, increase in procurement of rice by FCI, increase in MSPs, and investments in road projects are bright spots, that

could favorably impact demand, however, these are not expected to nullify impact of the negative demand drivers.

Dealers plagued by elevated channel inventory levels/retail cycles and discounting levels: Dealers inventory levelshave increased from an average of ~40 days to around 60 days currently, driven by increasing push by the OEMs. High

inventory issues were highlighted specifically by dealers in Maharashtra and MP. With sluggish demand, farmers’ bargaining

strength has improved, leading to average discounting levels increasing compared to ~3 years back. Also, the farmers aredemanding a higher credit period from the dealers, elongating the retail cycle which at times goes upto 180 days against an

avg. of ~40 days.

Bright prospects for the small tractor segment (<30HP): Industry experts indicated promising demand for <30Hpsegment due to the following) on an average a 25HP tractor is sufficient for most agri-operations; 2) the haulage capacity of

such a tractor would be around 2.5T-3T, which is the typical load for non-agri operations and the rate per day for 8 hours of

non-agri-operations (Rs.700) is not dependent on tractor HP 3) major OEMs including M&M and International Tractors arelooking to expand their presence in the segment sensing the potential

International Tractors and TAFE said to be the most aggressively growth focused: Dealers of all major OEMs

identified International Tractors and TAFE as the major competitors, characterized by a robust product portfolio andaggressive marketing force. Dealers also indicated that when the imminent launch of lower HP tractors of John Deere takes

place, it could pose a tough competition to the existing players.

Stock Calls: Retain positive stance on VSTT (BUY: TP: Rs. 1,780), basis 15x FY18 EPS; given that it is perfectly poisedto benefit from the increasing demand for <30HP tractors. Reaffirm our call on M&M (ADD; TP: Rs. 1,325), based on SOTP

valuation. We believe that the slowdown will impact volumes of its farm equipments; and auto segment will drive growth.

Pan-India dealer checks across OEMs indicate a weak near demand outlook; expect pain to continue till 1HFY17, at least

Page 1

-20%

-15%

-10%

-5%

0%

5%

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

BSE Auto Sensex

B

The Indian Tractor Industry : Buckle up for more rough weather ahead

Non-applicability of scrappage scheme to tractors continues to be an impediment to replacement sales

Industry experts indicate that if the proposed scrappage norms of CVs more than 10 years old is made applicable to tractors as well, the replacement marketfor tractors would be enhanced by ~ 1.5mn units with immediate effect, providing a boost to tractor volumes, besides curbing pollution. However, OEMs havebeen opposed to classification of tractors as “ Commercial Automobiles”, so as not to lose eligibility for subsidies and other sops, losing out on this significantdemand trigger in the bargain.

Major tractor OEMs face intense competition (particularly in the Western and Northern regions) from the semi-organized, but significant tractorindustry in Rajkot and Saurashtra

Tractor industry in Rajkot is home to around 10-12 players with annual volumes of 12,000 units (primarily sub-20HP). Sources indicate that ~90% of the partsused in manufacturing by these units are sourced locally, which in combination with easy availability of skilled labour reduced the cost of production MajorOEMs including M&M (for mfg. the Yuvraj brand) Escorts (for mfg. the Steeltrac brand) have tied up with these local manufacturers in order to reduce thecost of production.

The net price of the tractor becoming the most (and in some cases, the only) important criterion in the tractor buying process

Dealers indicated that Intense competition, characterized by the entry and growing prominence of several new entrants in the market, coupled with sluggishdemand conditions has meant that farmers are increasingly going bargaining hunting in search of the best deals and add-on, including pressurising thedealer to throw in cash discounts, give higher value for the old tractor, free agricultural implements including trolleys, extended credit periods and so on.

Dealers indicated the concept of brand loyalty is surely disappearing, and given that all OEMs find it equally challenging to provide after sales service(primarily required on-site, in the farms), the same is not a major criterion in the tractor buying process.

Growing trend of farmer loan repayments being mapped to cash flows could ease burden on farmers significantly.

Dealers in UP indicated that a few banks in the region have restructured the loan repayment cycles of farmer loans to coincide with the harvest season,thereby ensuring that he is not strained due to a cash-flow mis-match. In other words, an EMI is converted into a yearly or half yearly repayment of principal(along with interest). Dealers indicated that this trend could spur confidence in farmers in taking up loans to purchase tractors.

Dealer attrition on the rise

Basis our interactions with dealers on the intra-OEM competitive scenario, dealers across states indicated that since it is becoming increasingly unviable tofunction as a tractor dealer, they are witnessing higher instances of dealer attrition

Replacement cycles the best in Punjab and Haryana; followed by UP; augurs well for a pick up in replacement demand in these major markets withdecent monsoon

Dealers in Punjab and Haryana indicated that the replacement cycle is the lowest in India at ~2-3 years, followed by UP at around 3-4 years. We believe thathigh probability of a good monsoon in FY17 coupled with short replacement cycles in major states augurs well for a pick up in demand.

Other takeaways

Despite official figures of ~30% of tractor used for non-agri purposes, dealers indicated that deploying of tractors for non-agri use is not an option, but anecessity if the farmer were to repay his loans. The rate for non-agri use are ~Rs.700/ day (assuming the tractor is driven by the owner). The registrationcosts for agri-use is Rs. 5,500 for a period of 15 years vs. Rs. 36,000 p.a. to register for non-agri use. Hence, farmers register for agri-use and the tractor isused for non-agri purposes for nine months is a year

Pan-India dealer checks across OEMs indicate a weak near demand outlook; expect pain to continue till 1HFY17, at least

Page 2

The Indian Tractor Industry : Buckle up for more rough weather ahead

Tractor volumes at their five year nadir in FY16; demand revival overwhelmingly dependent on normal - good monsoons

Page 3

Water levels of major Indian river basins plummet, reflective of the sub-par monsoons in the past two years; hearteningly, India has seldom

experienced three sub-par monsoons on the trot, historically, raising hopes of a normal monsoon in FY17

Source: Central Water Commission, Spark Capital

Tractor volumes at their lowest 5 year ebb in FY16E; demand revival hinges overwhelmingly on favorable monsoon in FY17

233 265

314 303 305

403

482 537 528

634

551

487

-20%

-10%

0%

10%

20%

30%

40%

-

100

200

300

400

500

600

700

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16E

Volumes (000's nos) Yoy growth (%)

72.6%67.2%

93.3%

44.3%

87.9%

35.9%67.2%47.5%

26.9%

69.9%

30.7% 33.8%

13.3%

77.2%

42.3%

60.0%

30.6%

0%

20%

40%

60%

80%

100%

Jul14 Oct14 Jan15 Mar15 Jul15 Oct15 Jan16 Mar16

Ganga Narmada Godavari Krishna Overall

Source: Industry, Spark Capital

The Indian Tractor Industry : Buckle up for more rough weather ahead

The Government has raised the MSPs in 2016 in a bid to revive flagging rural incomes

Source: GoI, Spark Capital

Reservoir levels especially in West & South a cause of concern; increasing MSPs a positive sign

Page 4

1,7101,762

1,886

2,134

2,7222,850 2,892 2,968

1,5571,668

1,784

2,164

2,4472,538 2,589

2,76546.7%

3.1%7.0%

13.2%

27.5%

4.7%1.5% 2.6%

4.5% 7.2% 7.0%

21.2%

13.1%

3.7% 2.0%

6.8%

0%

10%

20%

30%

40%

50%

1,500

1,800

2,100

2,400

2,700

3,000

2009 2010 2011 2012 2013 2014 2015 2016

Avg. Kharif MSP (Rs. Quintal) Avg. Rabi MSP (Rs. Quintal) YoY growth in Kharif MSP % YoY growth in Rabi MSP %

RegionNo. of

reservoirs

Filling position of 91 reservoirs w.r.t. Full reservoir levels as at 10, Mar 2016

100% 91%-99% 81%-90% 71%-80% 61%-70% 51%-60% 41%-50%40% &

belowDeparture from normal levels

North

(HP,Punjab & Rajasthan)6 - - - - - - - 6

HP: -19%; Punjab: -29%, Rajasthan: -

12%East

(Jharkhand,Odisha, Tripura &

W.Bengal)

15 - - - - - 4 3 8Jharkhand: -39%, Orissa: -10%, W.

Bengal:-21%

West

(Guj.& Mah.)27 - - - - - - 5 22 Gujarat: -39%, Maharashtra: -57%

Central

(MP,UP,Uttarakhand & Chh.)12 - - - - - 2 2 8

UP: -15%, Uttarakhand:-46%, MP: 33%

and Chattisgarh: -29%

South

(Karnataka,TN,AP & Kerala),31 - 1 - 1 - 1 2 26

AP: -1%; Telangana:-74%, Karnataka:-

34%, Kerala:-4% and TN: -42%

Overall 91 0 1 0 1 0 7 12 70

The Indian Tractor Industry : Buckle up for more rough weather ahead

Evaluating major factors related to Rural India

1. Monsoon

3. Minimum Support Price

4. FCI’s policy on foodgrains

5. Agri Exports

2. Agri Production

6. Rural wage growth

The worst Monsoon season in six years

with 14% rain deficit

El Nino is weakening; International

climate models suggest neutral 2H 2016

Rabi output fell 9.1% from last year

while Kharif output was down 3%

Rabi output to increase 4% while Kharif

output is likely to rise 3%

Only ~2% increase in MSP of Kharif and

Rabi crops

6.8% hike in MSP for Rabi - highest in 3

yrs, expect 5-8% hike in MSP for Kharif

FCI off-loaded rice and wheat in the

open markets to curb food inflation

Stopped offloading foodgrain stocks in

open markets

Agri exports contracted 27% during

Apr-Dec 2015

Given lower global food prices, agri

exports may continue to suffer in 2016

Rural nominal wage growth has been

muted at ~4% in 2015

No significant change vs. 2015; Rural

wage growth likely to be ~5% in 2016E

2015 2016

7. Govt rural spendMuted govt rural spend at 3.4% during

Apr-Dec 2015

Budget focus on more rural spend,

Expect 20% increase in FY17

8. Cheaper agri importsGlobal food prices fell 20% leading to

cheaper food imports in India

Govt twice hiked custom duty on wheat

after 8 yrs to protect Indian farmers

9. Construction activitiesWeak construction activities as new

home launches fell 30% in Dec quarter

Weak real estate related activities to be

a drag on non-farm rural economy

10. Wealth effect Negative wealth effect at the play as

land prices fell ~20% from the peak

Recent 20% surge in gold prices may

partially offset the -ve wealth effect

Page 5

The Indian Tractor Industry : Buckle up for more rough weather ahead

Zone% of volumes

YTD16FY11 FY12 FY13 FY14 FY15 FY16E

CAGR

(FY11-FY16)

North 24.0% 133,687 140,658 147,626 168,853 155,263 116,264 -2.8%

East 18.7% 74,696 75,933 83,989 103,907 91,492 91,155 4.1%

West 39.1% 178,175 217,670 221,627 275,137 224,504 188,496 1.1%

South 18.2% 93,821 100,420 73,650 85,034 79,126 90,287 -0.8%

Total 100% 480,379 534,681 526,892 632,931 550,385 486,202 0.2%

East and West Zone increase their share in volumes led by Bihar and Rajasthan, resp.; North and South dragged down by U.P. and T.N., resp.

Source: Industry, Spark Capital

27.8% 26.3% 28.0% 26.7% 28.2% 24.0% 23.9%

15.5% 14.2% 15.9% 16.4% 16.6% 18.7% 18.7%

37.1% 40.7%42.1% 43.5% 40.8% 39.1% 38.8%

19.5% 18.8% 14.0% 13.4% 14.4% 18.2% 18.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY11 FY12 FY13 FY14 FY15 YTD16 FY16E

North East West South

Tractor growth in East and West Zone has outperformed the rest of the country over the last 5 years

Page 6

Source: Industry, Spark Capital

The Indian Tractor Industry : Buckle up for more rough weather ahead

State Zone

% of

volumes

YTD16

FY11 FY12 FY13 FY14 FY15 FY16ECAGR

(FY11-FY16)

U.P. North 14.5% 76,981 82,613 84,553 95,660 92,235 70,507 -1.7%

Rajasthan West 12.7% 35,173 53,175 63,275 74,920 64,565 60,530 11.5%

M.P West 9.8% 48,435 50,640 70,815 87,835 63,763 47,203 -0.5%

A.P South 8.5% 44,110 41,958 30,784 44,163 37,028 42,640 -0.7%

Maharashtra West 8.5% 53,616 57,191 44,405 65,631 49,840 41,191 -5.1%

Gujarat West 8.1% 40,951 56,664 43,132 46,751 46,336 39,572 -0.7%

Bihar East 7.3% 27,244 29,162 34,857 40,437 36,092 34,979 5.1%

Karnataka South 6.6% 28,403 31,533 23,745 30,601 33,758 32,695 2.9%

Haryana North 4.5% 24,124 26,040 27,902 35,290 30,626 21,902 -1.9%

Punjab North 3.6% 26,620 25,987 28,234 30,187 26,077 17,545 -8.0%

Chhattisgarh East 3.5% 12,861 13,277 15,815 24,271 20,011 16,930 5.7%

Tamil Nadu South 3.0% 20,638 26,298 18,533 9,886 8,072 14,634 -6.6%

West Bengal East 2.6% 13,045 12,187 12,751 13,760 12,779 12,842 -0.3%

Orissa East 2.6% 11,134 9,233 9,210 12,125 10,878 12,677 2.6%

Others NA 4.3% 18,944 20,895 19,757 22,634 19,403 21,342 2.4%

Total 100% 482,279 536,853 527,768 634,151 551,463 487,189 0.2%

Amongst major states, Rajasthan, Bihar and Karnataka outperform; UP, Mah. and Punjab impacted the most

Page 7

Source: Industry, Spark Capital

The Indian Tractor Industry : Buckle up for more rough weather ahead

State

% of

volumes

YTD16

Major CropsSnippets of dealer interactions on recent happenings

and its impact on near term demand

Uttar

Pradesh 14.5%

Paddy, sugarcane, and

wheat

No hike in state-administered prices for sugarcane (stagnant at Rs.280/quintal), coupled with increasing

arrears of dues to be paid to farmers continue to act as constraints on cash flows. Also, the unseasonal

rains/hail in early March 2016 has flattened wheat crops (due for harvesting).

However, increase in paddy procurement by the FCI in the recent months is a positive sign.

Rajasthan 12.7%Wheat, gaur, soybean

and other pulses

Demand for gaur has significantly suffered on the back of fall in crude prices. (Gaur gum is used as a

thickening agent in the fracking process). Unseasonal rains in early March 2016 have damaged pulses

crops, particularly chana and standing wheat crops

M.P 9.8%

Wheat, soybean,

sugarcane, rice, maize

and cotton

The major produce of wheat and gram, as has been the case with most Northern and Central states has

been severely impacted on account of the unseasonal rains. Few dealers indicated vociferous agitations by

farmers in their networks demanding for government assistance to tide over the damages.

Maharashtra 8.5%Cotton, sugarcane,

groundnut and sunflower

Dealers in Maharashtra were particularly gloomy about demand prospects as compared to their pan-India

counterparts. Maharashtra faces its second consecutive year of drought with 278 out of 355 talukas

declared drought hit. Dealers in the sugarcane belt indicated that demand has worsened; however, the

demand indicators from dealers in the Vidarbha region was slightly more encouraging as the district was

impacted to a lesser degree by the drought. (Cotton production for the year is expected to register an

increase over the previous year.

Bihar 7.3%Rice, wheat, maize,

potato and pulses

Unseasonal rain and hail storm have caused extensive damage to standing rabi crops, particularly wheat.

masoor (lentils), khesari, pea, mustard and wheat. On a lighter vein, a few dealers indicated that the

government’s decision to classify the “Nilgais’’ as vermin and allow the culling of the same could afford

relife to farmers, on account of major damages done by the animal.

Haryana 4.5%Rice, jowar, bajra, maize,

wheat, and sugarcane

In addition to the common issue of unseasonal rains damaging wheat crop, dealers indicated an

improvement in mining activity on the back of e-auction of mineral mining licences in FY16. Though,

recently, the NGT has issued a notice issued notice to Haryana Govt to take action against illegal sand

mining in the Yamuna Belt. Dealers felt that the impact of the same on demand would not be significant.

Unseasonal rains/hail across major North and Central Indian states have expected to dampen near term tractor demand

Page 8

Source: Industry, Spark Capital

The Indian Tractor Industry : Buckle up for more rough weather ahead

State

% of

volumes

YTD16

Major CropsSnippets of dealer interactions on recent happenings

and its impact on near term demand

Orissa 2.6%Rice, pulses, and

potato

Dealers indicated lack of decisive policy making as an impediment with potato procurement prices not fixed as

yet even though the crop is ready for harvesting

A.P 8.5%

Rice, jowar, bajra,

maize, pulses,

castor, tobacco,

cotton and

sugarcane.

The unseasonal rain led to weaker food grains production in the region. Dealers indicated that unfavorable

prices in addition to rains impacted cotton produce 2015-16. However, tobacco production was supported by

higher global demand and increasing prices (over Rs.140 per kg) due to launch of e-auctioning facility. The AP

govt.’s initiative to interlink rivers and increasing farm ponds under the MNREGA are few positive takeaways to

which could improve the sentiment of farmers.

Punjab 3.6%

Barley, wheat, rice,

maize and

sugarcane.

In addition to the common issue of unseasonal rains damaging wheat crop, dealers indicated that crash in

prices of Basmati due to supply from other non-traditional basmati states impacted prices and farm income.

However, to the positive side, the below par potato crop in other parts of the country have boosted demand for

the rabi potato crop in Punjab, and is expected to favourably impact sentiment.

Gujarat 8.1%

Tobacco, cotton,

groundnuts, rice,

wheat, jowar, bajra

and maize

Attack of pink bollworms coupled with erratic rainfall has reduced cotton yield significantly in 2015-16, lowest in

last 10 years. Consecutive failures have led to decrease in cultivation area leading to fall in Y-o-Y produce of

cotton (8.6% decline), groundnut(4.2%), wheat(15.2%), jowar(58.3%), bajra(4.8%) and rice(31.6%).

Karnataka 6.6%

Rice, ragi, jowar,

maize, pulses,

cashews and

coconut,

Paddy suffered heavy losses in the last two years owing to crop destruction caused by floods and other climatic

fluctuations. Relative absence of mechanisation in jowar cultivation and harvest, coupled with shortage of

labour are also adding to the decline in cultivation. 64 sugar mills have produced 3.6 mt – about 0.2 mt higher

than the corresponding period last year.

West Bengal 2.6% Rice, Potato, Jute The paddy production was impacted by floods, while the rabi potato crop was impacted by unseasonal rains.

Tamil Nadu 3.0%

Paddy, maize,

sugarcane,

groundnut

Two consecutive droughts and the vagaries of the weather have added to the agrarian distress. Lower than

expected cane pricing and increasing acreage of cane production in neighbouring states is expected to reduce

acreage.

Unseasonal rains/hail across major North and Central Indian states have expected to dampen near term tractor demand

Page 9

Source: Industry, Spark Capital

The Indian Tractor Industry : Buckle up for more rough weather ahead

State

% of

volumes

YTD16

Irrigation

Intensity

% of

medium

and large

farmers Soil Type

% of

commercial

usage

% of > 40

HP

Punjab 4% 98% 91% Alluvial 15-20 86%

T.N. 3% 58% 39% Red & Yellow, Alluvial 35-40 87%

A.P. 9% 49% 45% Black, Red & Yellow, Alluvial 40-45 67%

Maharashtra 9% 20% 55% Black, Red & Yellow 30-35 57%

W. Bengal 3% 58% 19% Red & Yellow, Alluvial 60-65 76%

Karnataka 7% 33% 60% Black, Red & Yellow 25-30 59%

Haryana 5% 85% 77% Alluvial 25-30 57%

M.P 10% 34% 66% Black 15-20 59%

Rajasthan 13% 32% 84% Sandy, Alluvial & Black 30-35 44%

U.P. 15% 76% 36% Alluvial 25-30 49%

Orissa 3% 35% 30% Red & Yellow, Alluvial 70-75 48%

Chattisgarh 4% 28% 58% Red & Yellow 35-40 35%

Gujarat 8% 46% 71% Black, Alluvial 10-15 32%

Bihar 7% 62% 24% Alluvial 35-40 27%

Northern states most decoupled from monsoon vagaries ; good monsoon capable of sustaining farm incomes for a longer time

Snippets of interactions with dealers

Industry experts called for an increasing

penetration of irrigation facilities across India,

as a solution to the ills plaguing the tractor

industry. They indicate that irrigation intensity is

the only criterion that differentiates a farmer in

Punjab and UP from the rest of the country.

With assured farm income, a farmer in these

states

In states like Orissa and Bihar, characterised by

more than average land fragmentation, the

prevalence of higher HP tractors is on the back

of greater usage for non-agri purposes.

Dealers in Punjab, Haryana and UP indicated

that given the high irrigation intensity, a good

monsoon will sustain agricultural activities for a

longer period (recharging of ground water and

replenishment of reservoirs) compared to other

states on the back of the highly penetrate

irrigation network in these states.

Dealers explained the prevalence of higher HP

tractors in these states despite presence of

softer soil as being on account of greater

income certainty on the back of the irrigation

network.

Page 10

Source: Industry, Spark Capital

The Indian Tractor Industry : Buckle up for more rough weather ahead

India lags far behind globally in tractor penetration; wide disparity between states in tractor penetration

Country wise penetration of tractors (HP/hectare)

Source: Industry, Spark Capital

State wise penetration of tractors (HP/hectare)

Source: Industry, Spark Capital

9.8

8.27.6

7.0

4.5 4.1 4.1 3.7

2.0 1.9 1.6 1.61.1

0

2

4

6

8

10

12

W. G

erm

any

Italy

UK

Jap

an

Fra

nce

So

uth

Kore

a

Chin

a

Po

lan

d

US

A

Tu

rkey

Th

aila

nd

Vie

tnam

India

1.21.0

0.8

1.3

0.7

0.40.6

1.1

0.8

0.5

2.8

0.8

1.5

2.7

1.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

T.N

A.P

.

Ka

rnata

ka

Guja

rat

Chattis

garh

Jha

rkhand

Orissa

M.P

.

Ma

hara

sh

tra

W. B

engal

Pu

nja

b

Raja

sth

an

U.P

Hary

ana

Bih

ar

India lags significantly behind other

countries in the penetration of tractors, with

the tractor driver HP/Hectare at an abysmal

1.1.

India is impacted by fragmented land

holdings and low penetration of irrigation

facilities, which inhibits certainty of

agricultural income discouraging farmers

from using tractors as a major source of

power on farms.

Punjab and Haryana, which enjoy the

highest penetration of irrigation facilities in

the country, also have the highest

penetration of tractors.

Pulling down the national average are the

states of Maharashtra, West Bengal,

Karnataka, constrained by limited irrigation

penetration.

Page 11

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise irrigation intensity

Source: Industry, Spark Capital

Usage for non-agri purposes

Source: Industry, Spark Capital

98%

85%76%

62%58% 58%

49% 46%

34% 33%28%

35% 32%

20%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Pu

nja

b

Hary

ana

U.P

.

Bih

ar

T.N

.

W. B

engal

A.P

.

Guja

rat

M.P

Ka

rnata

ka

Chattis

garh

Orissa

Raja

sth

an

Ma

hara

sh

tra

Jha

rkhand

72.5%

62.5%

42.5% 37.5% 32.5%27.5%

17.5%12.5%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Orissa

W. B

engal

A.P

.

Bih

ar

T.N

.

Chattis

garh

Raja

sth

an

Ma

hara

sh

tra

Ka

rnata

ka

Hary

ana

U.P

.

Pu

nja

b

M.P

.

Guja

rat

Besides the key northern states of

Punjab, Haryana and UP, the rest of

India lags significantly in the

penetration of irrigation facilities.

This in turn leaves theses states

entirely dependent on the monsoon,

exposing them to fluctuations in

agricultural output depending on the

vagaries of the monsoon.

It is conventionally believed that

~30% of the tractors are used in non-

agri purposes. Our channel checks

indicate that deploying of tractors for

non-agri use is not an option, but a

necessity if the farmer were to be

able to generate sufficient cash flows

to repay his loans.

The rate for non-agri use is estimated

at ~Rs.700/ day (assuming the tractor

is driven by the owner)

Penetration levels of irrigation leave a lot to be desired; non-agri usage of tractors has never been an option, but a need

Page 12

The Indian Tractor Industry : Buckle up for more rough weather ahead

TAFE and International Tractors gain significant share in the overall market; Escorts falters

Though the 41-50 HP seg. leads in volumes; our checks reveal that the 21-30 HP (within 0-30 HP) segment holds much promise

Source: Industry, Spark Capital

Note: Due to changes made in HP classification made in mid-FY13, data for & prior to FY13 is not comparable with FY14 and beyond

11% 11% 11%

35% 37% 37%

49% 47% 46%

5% 6% 7%

0%

20%

40%

60%

80%

100%

FY14 FY15 FY16E

Upto 30 hp 31-40 hp 41-50 hp 51 hp and above

Overall volumes: 41-50 HP is the largest HP segment; M&M manages to hold its fort amidst intensifying competition

HP

SegmentFY14 FY15 FY16E

CAGR

(FY14-

FY16)

0-30 70,794 59,411 49,462 -16%

31-40 223,085 202,281 170,851 -12%

41-50 286,286 251,627 215,160 -13%

>50 30,972 32,663 30,180 -1%

Total 6,11,137 5,45,982 4,65,653 -13%

Page 13

42.2% 41.8% 40.6% 41.0% 40.1% 41.5%

20.4% 23.3% 25.0% 24.8% 24.4% 23.2%

8.6% 8.3% 9.6% 10.3% 11.9% 11.8%13.2% 11.3% 11.6% 10.7% 10.4% 10.0%8.0% 7.5% 5.7% 5.9% 5.4% 6.2%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16E

Mahindra & Mahindra Ltd. TAFE International Tractors Ltd. Escorts Ltd. Johndeere New Holland India VST Others

Source: Industry, Spark Capital

Pan India, HP

and OEM

share

The Indian Tractor Industry : Buckle up for more rough weather ahead

Shift in Market share in major states

M&M and International tractors have made significant inroads in market share in this segment, Escorts loses big time

35.7% 36.5% 36.5% 37.5% 36.5% 39.0%

19.7% 22.8% 22.4% 21.8% 21.1% 18.7%

12.4% 12.0% 13.7% 14.5% 16.0% 15.9%20.7% 17.6% 16.7% 16.1% 15.7% 15.8%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16E

Mahindra & Mahindra Ltd. TAFE International Tractors Ltd. Escorts Ltd. Johndeere New Holland India VST Others

21% 17% 16% 17%

26%33% 34% 34%

36%40%

34%40%

FY11 FY14 FY15 YTD16

UP

Haryana

Punjab

23%26% 25%

23%

22% 21% 18% 14%

12%15% 14% 13%

21% 17% 16% 17%

25%18% 17% 18%

17%12% 14% 12%

10% 13% 14% 14%

8% 8% 9%

6%

15%16% 16%

18%

FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16

M&M extends its lead in the North Zone, largest market by size; International tractors makes impressive gains

Page 14

Source: Industry, Spark Capital

North Zone

The Indian Tractor Industry : Buckle up for more rough weather ahead

Shift in Market share in major states

Source:: Industry, Spark Capital

East Zone Market share

50.0% 48.2% 47.3% 48.1% 47.9% 48.5%

16.1% 17.9% 19.5% 19.5% 17.8% 16.6%10.7% 11.0% 11.0% 11.9% 13.6% 14.7%11.5% 10.6% 10.5% 9.5% 9.8% 9.8%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16E

Mahindra & Mahindra Ltd. TAFE International Tractors Ltd. Escorts Ltd. Johndeere New Holland India Others

47%44%

45% 46%

49%47% 46% 46%

49%

52% 51% 51%

19%24% 22% 20%

19%

22%20% 19%

21% 18% 16% 16%

16%15%

14%15%

8%

6%7% 7%

4%

1% 2% 2%

53% 54%

51%52% 7%

7% 7%6%

14%8%

11% 10%

9% 11% 13% 13%

11% 11% 12% 13%

11% 12% 14% 14%

11%14% 16% 17%

Bihar

Chattisgarh

Orissa

WB

FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16

The East Zone is the fastest growing tractor market across India; International Tractors gains share from M&M and Escorts

Page 15

East Zone

The Indian Tractor Industry : Buckle up for more rough weather ahead

TAFE makes significant inroads in the share of M&M and Escorts in the West; International tractors gains as well

West Zone Market share

40.0% 40.1% 38.4% 38.4% 37.3% 36.5%

23.7% 26.9% 29.3% 28.8% 29.4% 30.0%

7.3% 6.7% 8.0% 8.8% 10.2% 10.5%12.6% 10.6% 11.0% 10.2% 9.4% 9.4%8.0% 6.6% 5.3% 5.2% 4.1% 4.6%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16E

Mahindra & Mahindra Ltd. TAFE International Tractors Ltd. Escorts Ltd. Johndeere New Holland India VST Others

Shift in Market share in major states

Source: Industry, Spark Capital:

42%43%

45%44%

36% 37%35%

33%

51%47%

46% 46%

28%30%

29% 27%

21%26% 26% 26%

8%11% 11% 11%

26%

30% 29% 29%

46% 46%47%

48%

9%

5% 5% 6%

17%13% 13% 13%

8%

5%3% 3%

17%15% 14% 13%

7% 9% 10% 10%

9% 11%14% 15%

7%10% 12% 13%

5% 5% 6% 6%

FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16

Gujarat

MP

Maharashtra

Rajasthan

Page 16

West Zone

The Indian Tractor Industry : Buckle up for more rough weather ahead

The 2nd fastest growing zone : South Zone saw TAFE extend share gains; only zone where Itnl. Tractors has lost share

South Zone Market share

50.2% 48.9% 48.4% 48.4% 46.9% 48.3%

18.6% 20.7% 23.0% 23.8% 24.0% 21.5%

14.6% 14.4% 10.2% 12.8% 11.4% 12.3%

0%

20%

40%

60%

80%

100%

FY11 FY12 FY13 FY14 FY15 FY16E

M&M TAFE Johndeere Itnl. Tractors Ltd. Escorts Ltd. New Holland India VST Others

Shift in Market share in major states

Source: Industry, Spark Capital:

52%

47% 47% 48%

46%

49%

46%48%

52%51%

53%

52%

20%25% 25% 23%

19%24% 25% 23%

15% 16% 18%16%

16%15%

14% 14%

14%11% 9% 9%

13%10% 9%

14%

10% 13% 14% 14%

8% 8% 9%

6%

15%16% 16%

18%

FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16 FY11 FY14 FY15 YTD16

AP

Karnataka

Tamilnadu

Page 17

South Zone

The Indian Tractor Industry : Buckle up for more rough weather ahead

0-30 HP: Increasing fragmentation and usage for new niche applications expected to propel growth in this segment

0-30HP volumes (FY14-FY16E CAGR: -16%)

Source: Industry, Spark Capital

Market shares in 0-30Hp segment

Source: Industry, Spark Capital

54% 51% 52%

26%22% 17%

6%10%

10%

10% 11% 13%

4% 6% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

M&M TAFE International Tractors VST Others

Small tractors are suitable for the soft soil in regions like

Rajasthan, Haryana, Bihar, Gujarat, Maharashtra and the western

parts of Uttar Pradesh.

However, a new trend is evolving, where tractors with less than 20

HP are being launched by manufacturers for farming smaller plots.

These tractors are targeting specific applications like orchard

farming, inter-cultivation etc. and are also suitable to farmers with

0.8-2.0 hectares (ha) of land.

Given the low tractor penetration in India (in HP terms), and with

around 85% of land holdings being small and marginal (no of

households holding less than 2 ha land), the opportunity in this

space is significant.

M&M, TAFE and VST Tillers have a significant presence in this

segment.

70,794

59,411

49,462

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

FY14 FY15 FY16E

Overall volumes

Zone wise share in overall volumes

Source: Industry, Spark Capital

35%28% 24%

19%16%

14%

41%49%

51%

6% 6% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 FY16E

North East West South

Page 18

0-30HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in 0-30 HP segment – North

Source: Industry, Spark Capital

60% 57% 55%

27% 29% 31%

10% 11% 10%

3% 3% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

UP Haryana Punjab Others

24,704

16,621

11,976

-

5,000

10,000

15,000

20,000

25,000

30,000

FY14 FY15 FY16E

North Zone total volumes

North Zone volumes (FY14-FY16E CAGR: -30%)

Source: Industry, Spark Capital

State wise share in 0-30 HP segment - East

Source: Industry, Spark Capital

East Zone volumes (FY14-FY16E CAGR: -28%)

Source: Industry, Spark Capital

55% 57% 62%

25% 24% 19%

5% 6% 9%7% 8% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Bihar Chattisgarh West Bengal Jharkhand Orissa Assam

13,179

9,773

6,914

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

FY14 FY15 FY16E

East Zone total volumes

0-30 HP: Increasing fragmentation and usage for new niche applications expected to propel growth in this segment

Page 19

0-30HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in 0-30 HP segment – West

Source: Industry, Spark Capital

West Zone volumes (FY14-FY16E CAGR: -7%)

Source: Industry, Spark Capital

State wise share in 0-30 HP segment - South

Source: Industry, Spark Capital

South Zone volumes (FY14-FY16E CAGR: +15%)

Source: Industry, Spark Capital

30% 37% 35%

11%5% 5%

47% 51% 54%

12% 7% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Gujarat M.P. Maharashtra Rajasthan

28,686 29,176

24,980

22,000

23,000

24,000

25,000

26,000

27,000

28,000

29,000

30,000

FY14 FY15 FY16E

West Zone total volumes

4,225 3,841

5,592

-

1,000

2,000

3,000

4,000

5,000

6,000

FY14 FY15 FY16E

South Zone total volumes

24%16%

26%

43%75% 62%

1%

1% 1%33%

8% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

A.P. Karnataka Kerala T.N.

0-30 HP: Increasing fragmentation and usage for new niche applications expected to propel growth in this segment

Page 20

0-30HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

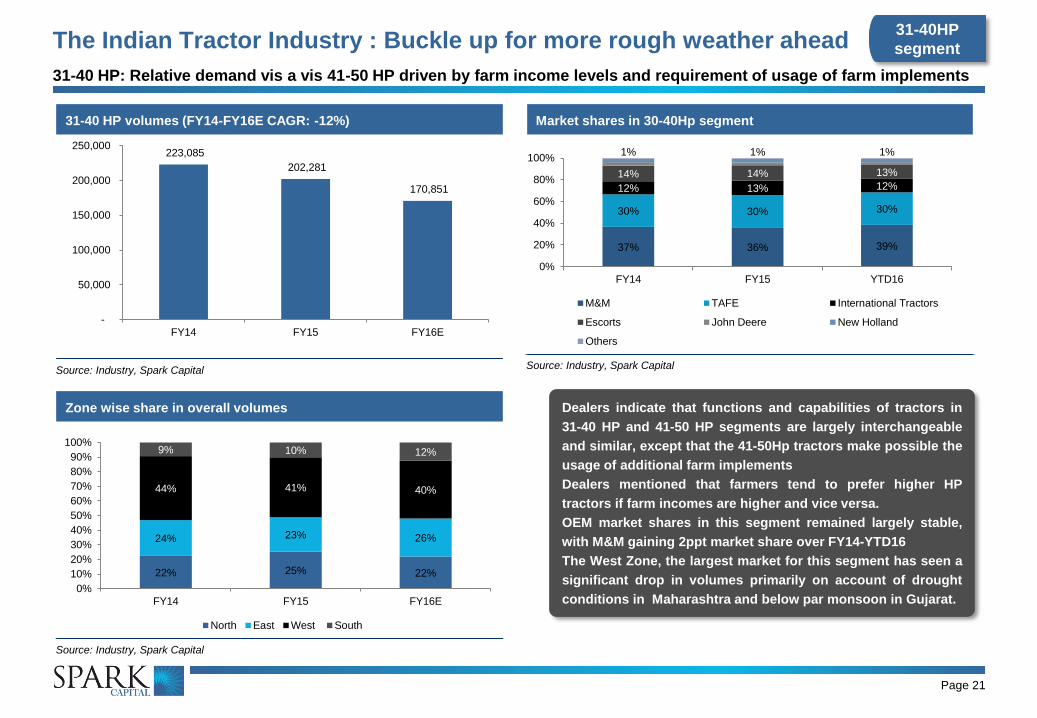

31-40 HP volumes (FY14-FY16E CAGR: -12%)

Source: Industry, Spark Capital

37% 36% 39%

30% 30% 30%

12% 13% 12%14% 14% 13%

1% 1% 1%

0%

20%

40%

60%

80%

100%

FY14 FY15 YTD16

M&M TAFE International Tractors

Escorts John Deere New Holland

Others

Market shares in 30-40Hp segment

Source: Industry, Spark Capital

Dealers indicate that functions and capabilities of tractors in

31-40 HP and 41-50 HP segments are largely interchangeable

and similar, except that the 41-50Hp tractors make possible the

usage of additional farm implements

Dealers mentioned that farmers tend to prefer higher HP

tractors if farm incomes are higher and vice versa.

OEM market shares in this segment remained largely stable,

with M&M gaining 2ppt market share over FY14-YTD16

The West Zone, the largest market for this segment has seen a

significant drop in volumes primarily on account of drought

conditions in Maharashtra and below par monsoon in Gujarat.

Zone wise share in overall volumes

Source: Industry, Spark Capital

22% 25% 22%

24% 23% 26%

44% 41% 40%

9% 10% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 FY16E

North East West South

223,085

202,281

170,851

-

50,000

100,000

150,000

200,000

250,000

FY14 FY15 FY16E

31-40 HP: Relative demand vis a vis 41-50 HP driven by farm income levels and requirement of usage of farm implements

Page 21

31-40HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in 31-40 HP segment – North – Put CAGR

Source: Industry, Spark Capital

North Zone volumes (FY14-FY16E CAGR: -13%)

Source: Industry, Spark Capital

State wise share in 31-40 HP segment - East

Source: Industry, Spark Capital

East Zone volumes (FY14-FY16E CAGR: -10%)

Source: Industry, Spark Capital

50,074 51,291

37,583

-

10,000

20,000

30,000

40,000

50,000

60,000

FY14 FY15 FY16E

54,478

47,484 44,350

-

10,000

20,000

30,000

40,000

50,000

60,000

FY14 FY15 FY16E

75% 77% 78%

17% 16% 15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

U.P. Haryana Punjab Others

44% 45% 45%

22% 22% 21%

11% 13% 13%

12% 13% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Bihar Chattisgarh Others Jharkhand Others

31-40 HP: Relative demand vis a vis 41-50 HP driven by farm income levels and requirement of usage of farm implements

Page 22

31-40HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in 31-40 HP segment – West– Put CAGR

Source: Industry, Spark Capital

West Zone volumes (FY14-FY16E CAGR: -17%)

Source: Industry, Spark Capital

State wise share in 31-40 HP segment - South

Source: Industry, Spark Capital

South Zone volumes (FY14-FY16E CAGR: +1%)

Source: Industry, Spark Capital

97,689

82,990

67,594

-

20,000

40,000

60,000

80,000

100,000

120,000

FY14 FY15 FY16E

20,844

20,516

21,324

20,000

20,200

20,400

20,600

20,800

21,000

21,200

21,400

FY14 FY15 FY16E

22% 23% 25%

37% 33% 25%

6%5%

5%

35% 39% 45%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Gujarat M.P. Maharashtra Rajasthan

58%50% 54%

38% 46% 41%

4% 3% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

A.P Karnataka T.N. Kerala

31-40 HP: Relative demand vis a vis 41-50 HP driven by farm income levels and requirement of usage of farm implements

Page 23

31-40HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

43% 43% 44%

23% 23% 22%

7% 9% 10%11% 10% 10%8% 7% 7%1% 1% 1%

0%

20%

40%

60%

80%

100%

FY14 FY15 YTD16

M&M TAFE International Tractors

Escorts John Deere New Holland

Others

41-50 HP segment: Rising farm incomes and increasing usage of farm implements would drive demand over medium term

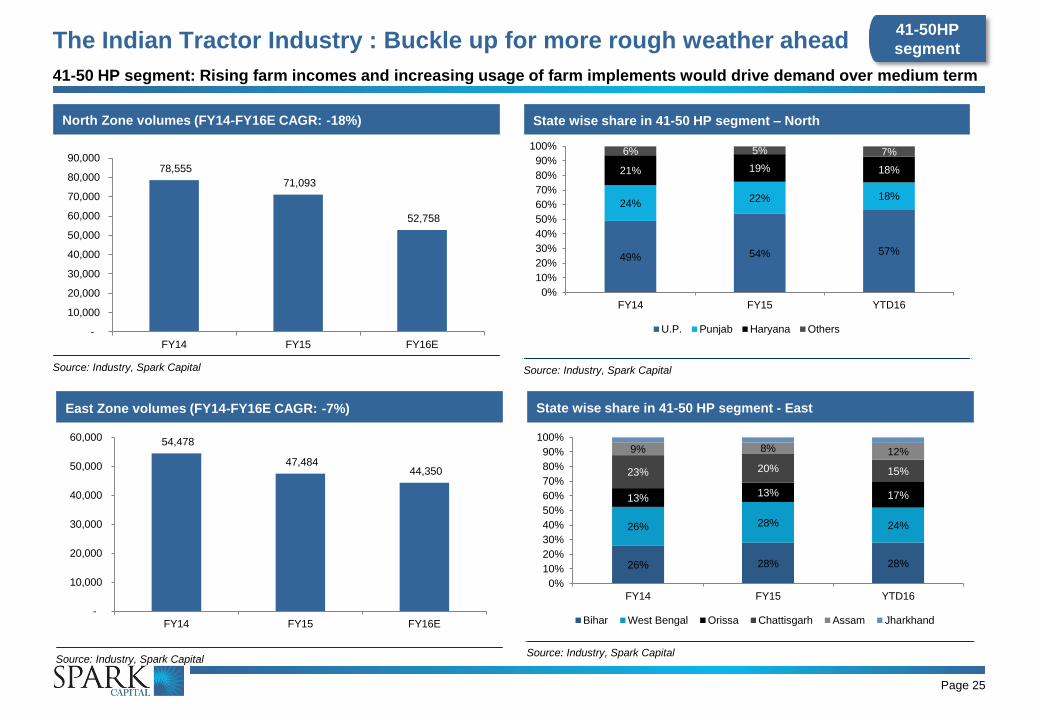

41-50 HP volumes (FY14-FY16E CAGR: -13%)

Source: Industry, Spark Capital

Market shares in 41-50 HP segment

Source: Industry, Spark Capital

Zone wise share in overall volumes

Source: Industry, Spark Capital

22% 25% 22%

24% 23% 26%

44% 41% 40%

9% 10% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 FY16E

North East West South

286,286

251,627

215,160

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

FY14 FY15 FY16E

Demand for 41-50 HP segment tractors have a direct

correlation with rising farm incomes (if incomes are lower, then

31-40Hp tractors are preferred).

Also, 41-50HP tractors enables the usage of a wide array of

farm implements , which would gain traction over the medium

term as farm mechanisation levels improve.

International Tractors was the largest gainer of market share in

this segment, gaining share from OEMs across the board.

The West Zone, the largest market for this segment has seen a

significant drop in volumes primarily on account of drought

conditions in Maharashtra and below par monsoon in Gujarat

Page 24

41-50HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in 41-50 HP segment – North

Source: Industry, Spark Capital

North Zone volumes (FY14-FY16E CAGR: -18%)

Source: Industry, Spark Capital

State wise share in 41-50 HP segment - East

Source: Industry, Spark Capital

East Zone volumes (FY14-FY16E CAGR: -7%)

Source: Industry, Spark Capital

78,555

71,093

52,758

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

FY14 FY15 FY16E

54,478

47,484 44,350

-

10,000

20,000

30,000

40,000

50,000

60,000

FY14 FY15 FY16E

49% 54% 57%

24%22% 18%

21% 19% 18%

6% 5% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

U.P. Punjab Haryana Others

26% 28% 28%

26% 28% 24%

13%13% 17%

23% 20% 15%

9% 8% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Bihar West Bengal Orissa Chattisgarh Assam Jharkhand

41-50 HP segment: Rising farm incomes and increasing usage of farm implements would drive demand over medium term

Page 25

41-50HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in 41-50 HP segment – West

Source: Industry, Spark Capital

West Zone volumes (FY14-FY16E CAGR: -17%)

Source: Industry, Spark Capital

State wise share in 41-50 HP segment - South

Source: Industry, Spark Capital

South Zone volumes (FY14-FY16E CAGR: -5%)

Source: Industry, Spark Capital

97,689

82,990

67,594

-

20,000

40,000

60,000

80,000

100,000

120,000

FY14 FY15 FY16E

55,564

50,060 50,458

47,000

48,000

49,000

50,000

51,000

52,000

53,000

54,000

55,000

56,000

FY14 FY15 FY16E

11% 15% 13%

33% 32% 30%

30% 26% 25%

26% 28% 31%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Gujarat M.P. Maharashtra Rajasthan

52% 49% 47%

34% 38%32%

13% 13%21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

A.P Karnataka T.N. Kerala

41-50 HP segment: Rising farm incomes and increasing usage of farm implements would drive demand over medium term

Page 26

41-50HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

> 50 HP segment – a niche segment with limited applications in non-agri segment; growth expected to be muted

>50HP volumes (FY14-FY16E CAGR: -1%)

Source: Industry, Spark Capital

Market shares in >50HP segment

Source: Industry, Spark Capital

Zone wise share in overall volumes

Source: Industry, Spark Capital

22% 25% 22%

24% 23% 26%

44% 41% 40%

9% 10% 12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 FY16E

North East West South

30,972

32,663

30,180

28,500

29,000

29,500

30,000

30,500

31,000

31,500

32,000

32,500

33,000

FY14 FY15 FY16E

18% 16%27%

24% 26%26%

36% 31%23%

13% 12% 10%

6% 10% 5%2% 3% 5%

0%

20%

40%

60%

80%

100%

FY14 FY15 YTD16

John Deere M&M International Tractors

New Holland Escorts TAFE

Others

Dealers indicated that the market for the >50HP segment is

expected to remain limited as for Indian conditions, a 41-50HP

tractor is more amenable and versatile with capabilities of

being used in the non-agro segment as well.

Also, the price gap between a 41-50HP segment and >50 HP

segment was indicated as being significant to convince

farmers to purchase the latter.

John Deere was the largest gainer of market share in this

segment, gaining share particularly from International tractors.

Page 27

>50HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in >50 HP segment – North – Put CAGR

Source: Industry, Spark Capital

North Zone volumes (FY14-FY16E CAGR: -5%)

Source: Industry, Spark Capital

State wise share in >50HP segment - East

Source: Industry, Spark Capital

East Zone volumes (FY14-FY16E CAGR: +16%)

Source: Industry, Spark Capital

15,520

16,256

13,947

12,500

13,000

13,500

14,000

14,500

15,000

15,500

16,000

16,500

FY14 FY15 FY16E

2,713

3,226

3,637

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY14 FY15 FY16E

41% 41% 39%

30% 30% 32%

25% 26% 24%

4% 4% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Punjab U.P. Haryana Others

28% 34%47%

42% 35%27%

12% 14% 11%

12% 9% 8%

6% 7% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

West Bengal Chattisgarh Bihar Orissa Others

> 50 HP segment – a niche segment with limited applications in non-agri segment; growth expected to be muted

Page 28

>50HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

State wise share in >50 HP segment – West– Put CAGR

Source: Industry, Spark Capital

West Zone volumes (FY14-FY16E CAGR: -5%)

Source: Industry, Spark Capital

State wise share in >50 HP segment - South

Source: Industry, Spark Capital

South Zone volumes (FY14-FY16E CAGR: 8%)

Source: Industry, Spark Capital

8,338

8,500

7,457

6,800

7,000

7,200

7,400

7,600

7,800

8,000

8,200

8,400

8,600

FY14 FY15 FY16E

4,401

4,681

5,139

4,000

4,200

4,400

4,600

4,800

5,000

5,200

FY14 FY15 FY16E

12% 12% 17%

32% 29%34%

41% 45%32%

15% 14% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

Gujarat M.P. Maharashtra Rajasthan

46%37% 42%

43%51%

32%

11% 11%25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY14 FY15 YTD16

A.P Karnataka T.N. Kerala

> 50 HP segment – a niche segment with limited applications in non-agri segment; growth expected to be muted

Page 29

>50HP

segment

The Indian Tractor Industry : Buckle up for more rough weather ahead

OEM sales by HP category

M&M: While 41-50HP is the major segment, increasing focus on 0-

30 HP segment

Source: Industry, Spark Capital

International Tractors Ltd: Increasing focus on 41-50HP and 0-30HP

Source: Industry, Spark Capital

40%31% 33% 34%

42%51% 49% 48%

8% 3% 4% 4%

10% 15% 14% 13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 YTD16

31-40 hp 41-50 hp 51 hp and above Upto 30 hp

43% 41% 40% 39%

30% 35% 36% 38%

21% 17% 16% 14%

6% 7% 9% 9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 YTD16

31-40 hp 41-50 hp 51 hp and above Upto 30 hp

Page 30

In a bid to tap the growing tractor rental business in India,

Mahindra & Mahindra (M&M), has set up of a new startup

venture called Trringo, the first ever organised rental service

for the sector.

Based on a franchisee model aimed at increasing farm

mechanisation levels in India through easy availability of

tractors to farmers who cannot afford to purchase them,

Trringo would use technology to create a sharing

infrastructure in the deep rural pockets of India.

Commenced operations at its new plant at Hoshiarpur, Punjab,

with an installed capacity of 200,000 units p.a. (up from current

capacities of 65,000 units p.a., which would be discontinued)

Claimed to be the world’s largest integrated unit, the plant is

expected to enhance the company’s reach in the South andin

the export markets.

It plans to introduce five products for TN (and South) , the GT

26, GT 30 for sugarcane and orchard farms and the DI 750,

Rx750 and the Rx47 – four-wheel drive models for puddling

and haulage applications.

Also plans to launch a 250 HP tractor next year in the global

markets.

Recent updates

OEM

updates

The Indian Tractor Industry : Buckle up for more rough weather ahead

OEM sales by HP category

Escorts: More focussed on the Big tractor segments (>40HP)

Source: Industry, Spark Capital

TAFE: Focussing big on the 41-50HP segment

Source: Industry, Spark Capital

63%

43% 45% 47%

21%45% 45% 44%

0%0% 1% 1%17%

12% 10% 8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 YTD16

31-40 hp 41-50 hp 51 hp and above Upto 30 hp

44% 47% 50% 47%

51% 50% 43% 47%

3% 3% 6% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 YTD16

31-40 hp 41-50 hp 51 hp and above Upto 30 hp

Page 31

No recent tractor segment specific updates

Escorts recently launching a new category of tractors called

“ANTI LIFT TRACTORS. specifically for commercial haulage

operators, are available in two models: ALT 4000 and ALT 3500,

in 37HP and 41 HP

Recent updates

OEM

updates

The Indian Tractor Industry : Buckle up for more rough weather ahead

New Holland: Volumes derived primarily from the 41-50Hp segment

Source: Company, Spark Capital

John Deere: The biggest >51HP player; expected to increase focus

on lower HP segments

Source: Company, Spark Capital

22% 21% 24% 25%

64% 67% 61% 58%

14% 12% 15% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 YTD16

31-40 hp 41-50 hp 51 hp and above

25% 20% 18% 16%

55% 65% 64%54%

20% 15% 18%30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY13 FY14 FY15 YTD16

31-40 hp 41-50 hp 51 hp and above

OEM sales by HP category

Page 32

Tractor maker John Deere India is aiming for a 10 per cent

jump in exports at 27,500 units this fiscal on likely increase in

demand for its new models in countries like the US and

Thailand.

Industry sources indicated that on the back of slowing demand

in India, it is expected that one of its plants near Pithampur is

expected to cater almost entirely to the export markets .

Tractors with advanced features which are now being exported

are expected to be introduced domestically over the medium

term

No recent tractor segment specific updates

Recent updates

OEM

updates

The Indian Tractor Industry : Buckle up for more rough weather ahead

Existing models across HP categories

Upto 20 HP

Yuvraj 15HP Shakti Mt 180D

Shakti Mt 180D - Jai

21 to 30 HP

Mahindra 245 DI MF 1030 Baaghban Shakti VT 224 - Ajai Powertrac Diesel Saver

Mahindra 255 DI DI 730 Shakti MT 270 - Viraat

Mahindra 265 DI (New) Shakti VT 224

31 to 40 HP

Mahindra 265 Power MF 1035 DI 734 3032 5036 Farmtrac XP

Mahindra 275 ECO TAFE 35 DI 35 3030 5039 Powertrac DS Plus

Mahindra 275 DI Eicher 333 3510 5038

Mahindra 295 Eicher 364 3037

Mahindra 415 (New) Eicher 368 4010

Swaraj 735

41 to 50 HP

Mahindra 475 MF 241 DI 740 3230 5041 Farmtrac Jai Kisan

Mahindra 575 MF 7250 DI 745 4510 5042 Powertrac Euro Series

Mahindra 595 MF 245 DI 42 4710 5045

Arjun 555 MF 5245 DI 47 3600 5050

TAFE 45 3630

Eicher 480

Eicher 485

Eicher 5150

Eicher 5660

>50 HP

Arjun Novo 605 MF 5245 DI 750 3630 (SPL) 5055 5055 Farmtrac Executive

Arjun International MF 9000 DI 60 5500 5310 5310

Mahindra 555 MF 9500 Worldtrac 75 6500 5060 5060

Arjun Novo 605 4WD

(New)TAFE 5450 Worldtrac 90 7500 5065 5065

Page 33

The Indian Tractor Industry : Buckle up for more rough weather ahead

Change in estimates – M&M and VST Tillers

Page 34Page 34

Volume estimates FY16E FY17E FY18E

Volume YoY % Volume YoY % Volume YoY %

Power Tillers 27,000 17% 31,051 15% 34,777 12%

Tractors 7,400 11% 8,880 20% 10,390 17%

Volume Estimates

FY15 FY16E FY17E FY18E

Automotive 4,64,842 488,109 595,545 659,544

% growth -8% 5% 22% 11%

Farm Equipment - tractor segment 236,426 212,269 222,089 249,156

% growth -12% -10% 5% 12%

TOTAL 701,268 700,378 817,633 908,700

% growth -9.0% 0% 17% 11%

SOTP Valuation

Basis

Mar’18PAT/

Market Cap

(Rs. mn)

PE (x)Discount

(%)

Eq Value

(Rs. mn)

Rs. per

share

M&M + MVML Core PAT 41,176 14x - 576,464 928

Listed subsidiaries &

holdings

Market Cap

/ book value308,485 20% 246,788 396

1,325

VST Tillers & Tractors

Mahindra & Mahindra (M&M + MVML)

Key estimate revision

FY17E FY18E

Old New Change Old New Change

Revenue 441,888 434,537 -1.7% 498797 490,194 -1.7%

EBITDA 58,329 56,490 -3.2% 65,841 64,706 -1.7%

Margin (%) 13.20% 13.0% -20 bps 13.20% 13.20% 0 bps

PAT 37,984 36,633 -3.6% 44,060 43,226 -1.9%

PAT Margin 8.60% 8.43% -17 bps 8.83% 8.82% -1 bps

EPS 61.7 59.0 -3.6% 71.5 69.6 -1.9%

All figures in Rs. mn, except EPS, which is in Rs.

Key estimate revision

FY16E FY17E

Old New Change Old New Change

Revenue 6,329 6,329 n/a 7,508 7,508 n/a

EBITDA 1,125 1,125 n/a 1,336 1,336 n/a

Margin (%) 17.8% 17.8% n/a 17.8% 17.8% n/a

PAT 736 736 n/a 884 884 n/a

PAT Margin 11.6% 11.6% n/a 11.8% 11.8% n/a

EPS 85.2 85.2 n/a 102.3 102.3 n/a

All figures in Rs. mn, except EPS, which is in Rs.

The Indian Tractor Industry : Buckle up for more rough weather ahead

Financial summary – VST Tillers

Page 35

Abridged Financial Statements - Standalone Key metrics

Rs. mn FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E

Profit & Loss Growth ratios

Revenues 5,516 6,329 7,508 8,679 Revenues -12% 15% 19% 16%

Manufacturing & Other Expenses 4,514 5,204 6,171 7,134 EBITDA -17% 12% 19% 16%

EBITDA 1,002 1,125 1,336 1,545 PAT -16% 6% 20% 16%

Depreciation 94 116 131 149 Margins

EBIT 908 1,009 1,205 1,396 EBITDA 18.2% 17.8% 17.8% 17.8%

Net Interest Exp / (inc) 21 22 22 22 EBIT 16.5% 15.9% 16.1% 16.1%

Profit Before Tax 1,005 1,083 1,300 1,507 PAT 12.6% 11.6% 11.8% 11.8%

Tax 311 347 416 482 Leverage & WC ratios

Adj. Net Profit 694 736 884 1,024 Debt to equity (x) - - - -

Balance Sheet (Rs. mn) Current ratio (x) 2.1 2.4 2.4 2.4

Shareholders Equity 3,635 4,207 4,893 5,688 Debtor days (Sales) 62 63 63 63

Loan funds - - - - Inventory days (COGS) 66 72 72 72

Deferred Tax Liability (Net) 47 46 46 46 Creditor Days (COGS) 56 51 51 50

Sources of Funds 3,683 4,253 4,939 5,734 Performance & turnover ratios

Net block 1,347 1,421 1,590 1,741 RoCE 20.7% 18.9% 19.6% 19.5%

Capital WIP 21 - - - RoAE 20.5% 18.8% 19.4% 19.4%

Current assets, loans & advances 2,402 2,762 3,479 4,290 Total asset turnover (x) 1.4 1.4 1.4 1.4

Current liabilities & provisions 1,039 1,095 1,294 1,461 Fixed asset turnover (x) 3.2 3.3 3.4 3.5

Net Current Assets 1,363 1,667 2,184 2,829 Valuation metrics

Application of funds 3,683 4,253 4,939 5,734 Current price (Rs.)

Cash Flows (Rs. mn) Shares outstanding (mn) 8.6 8.6 8.6 8.6

Cash flows from operations 260 499 746 876 Market capitalisation (Rs. mn) 13,175 13,175 13,175 13,175

Capex (227) (170) (300) (300) Enterprise value (Rs. mn) 12,991 13,031 12,750 12,373

Free Cash Flow 32 329 446 576 EV/EBIDTA (x) 13.0 11.6 9.5 8.0

Cash flows from investments (129) (382) (300) (300) Adj. Per-share earnings (Rs.) 80.3 85.2 102.3 118.6

Cash flows from financing (173) (156) (165) (198) Price-earnings multiple (x) 19.0 17.9 14.9 12.9

Closing cash and cash equivalents 179 144 425 803 Dividend yield (%) 1.0% 1.0% 1.3% 1.5%

1525

The Indian Tractor Industry : Buckle up for more rough weather ahead

Financial summary – M&M

Page 36

Abridged Financial Statements (M&M + MVML) Key metrics

Rs. mn FY15 FY16E FY17E FY18E FY15 FY16E FY17E FY18E

Revenues 372,236 383,445 434,537 490,194 Revenues -4.1% 3.0% 13.3% 12.8%

Manufacturing & Other Expenses 326,203 331,609 378,047 425,488 EBITDA -12.3% 12.6% 9.0% 14.5%

EBITDA 46,033 51,836 56,490 64,706 PAT -18.4% 5.2% 9.2% 18.0%

Depreciation 10,980 11,904 13,332 14,415

EBIT 46,611 47,969 51,998 60,015 EBITDA 12.4% 13.5% 13.0% 13.2%

Interest Exp / (inc) 3,039 2,304 2,138 1,181 EBIT 12.5% 12.5% 12.0% 12.2%

Profit Before Tax 43,572 45,664 49,860 58,834 PAT 8.6% 8.7% 8.4% 8.8%

Tax 9,339 12,114 13,228 15,608 Leverage & WC ratios

Adj. Net Profit 31,883 33,550 36,633 43,226 Debt to equity (x) 0.2 0.2 0.1 0.0

Current ratio (x) 1.2 1.2 1.2 1.2

Shareholders Equity 198,769 222,004 248,322 281,233 Debtor days (Sales) 24 25 25 25

Loan funds 30,382 35,000 22,000 9,500 Inventory days (COGS) 40 50 45 45

Sources of funds 229,152 257,004 270,322 290,733 Creditor Days (COGS) 83 90 85 85

Net block 79,019 87,115 93,783 99,368 Performance & turnover ratios

Investments 104,133 112,133 120,133 128,133 RoACE 17.0% 16.0% 14.7% 16.0%

Capital WIP 21,788 26,788 31,788 31,828 RoAE 17.1% 15.9% 15.6% 16.3%

Current assets, loans & advances 145,528 155,350 158,446 178,196 Total asset turnover (x) 1.2 1.2 1.2 1.3

Current liabilities & provisions 121,316 124,381 133,827 146,791 Fixed asset turnover (x) 3.9 3.6 3.6 3.8

Net Current Assets 24,212 30,969 24,619 31,405 Valuation metrics

Application of funds 229,152 257,004 270,322 290,733 Current price (Rs.)

Shares outstanding (mn) 621 621 621 621

Cash flows from operations 57,171 43,009 55,004 61,410 Market capitalisation (Rs. mn) 761,411 761,411 761,411 761,411

Capex (20,346) (25,000) (25,000) (20,040) Enterprise value (Rs. mn) 770,740 773,470 762,829 739,782

Free cashflow 20,975 10,009 22,004 33,370 EV/EBIDTA (x) 16.7 14.9 13.5 11.4

Cash flows from investments 7,436 (33,000) (33,000) (28,040) Per-share earnings (Rs.) 51.8 54.5 59.5 70.2

Cash flows from financing (22,054) (8,121) (24,363) (22,823) Price-earnings multiple (x) 23.7 22.5 20.6 17.5

Cash at the end of the year 21,053 22,941 20,582 31,129 Dividend yield (%) 1.1% 1.1% 1.1% 1.1%

Profit & Loss Growth ratios

Margins

Balance Sheet (Rs. mn)

Cash Flows (Rs. mn)

1,226

The Indian Tractor Industry : Buckle up for more rough weather ahead

Spark Disclaimer

Spark Capital Advisors (India) Private Limited (Spark Capital) and its affiliates are engaged in investment banking, investment advisory and institutional equities and

infrastructure advisory services. Spark Capital is registered with SEBI as a Stock Broker and Category 1 Merchant Banker.

We hereby declare that our activities were neither suspended nor we have defaulted with any stock exchange authority with whom we are registered in the last five years. We

have not been debarred from doing business by any Stock Exchange/SEBI or any other authorities, nor has our certificate of registration been cancelled by SEBI at any point of

time.

Spark Capital has a subsidiary Spark Investment Advisors (India) Private Limited which is engaged in the services of providing investment advisory services and is registered

with SEBI as Investment Advisor. Spark Capital has also an associate company Spark Infra Advisors (India) Private Limited which is engaged in providing infrastructure

advisory services.

This document does not constitute or form part of any offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction.

This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document should

be construed as investment or financial advice, and nothing in this document should be construed as an advice to buy or sell or solicitation to buy or sell the securities of

companies referred to in this document.

Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies

referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. This

document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published,

copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to or use by any person or entity who is a citizen or resident of or located in

any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Spark Capital

and/or its affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to

a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such applicable restrictions. This

material should not be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

Spark Capital makes no representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information and opinions contained in this

document. Spark Capital , its affiliates, and the employees of Spark Capital and its affiliates may, from time to time, effect or have effected an own account transaction in, or

deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit

investment banking or other business from, any company referred to in this report.

This report has been prepared on the basis of information, which is already available in publicly accessible media or developed through an independent analysis by Spark

Capital. While we would endeavour to update the information herein on a reasonable basis, Spark Capital and its affiliates are under no obligation to update the information.

Also, there may be regulatory, compliance or other reasons that prevent Spark Capital and its affiliates from doing so. Neither Spark Capital nor its affiliates or their respective

directors, employees, agents or representatives shall be responsible or liable in any manner, directly or indirectly, for views or opinions expressed in this report or the contents

or any errors or discrepancies herein or for any decisions or actions taken in reliance on the report or the inability to use or access our service in this report or for any loss or

damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits that may arise from or in connection with the use of

or reliance on this report.

Absolute

Rating

Interpretation

BUY Stock expected to provide positive returns of >15% over a 1-year horizon REDUCEStock expected to provide returns of <5% – -10% over a 1-year

horizon

ADDStock expected to provide positive returns of >5% – <15% over a 1-year

horizonSELL Stock expected to fall >10% over a 1-year horizon

Disclaimer

Page 37

The Indian Tractor Industry : Buckle up for more rough weather ahead

Disclaimer (Cont’d)

Spark Capital and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency,

Spark Capital has incorporated a disclosure of interest statement in this document. This should however not be treated as endorsement of views expressed in this report:

Disclosure of interest statement Yes/No

Analyst financial interest in the company No

Group/directors ownership of the subject company covered No

Investment banking relationship with the company covered No

Spark Capital’s ownership/any other financial interest in the company covered No

Associates of Spark Capital’s ownership more than 1% in the company covered No

Any other material conflict of interest at the time of publishing the research report No

Receipt of compensation by Spark Capital or its Associate Companies from the subject company covered for in the last twelve months:

Managing/co-managing public offering of securities

Investment banking/merchant banking/brokerage services

products or services other than those above

in connection with research report

No

Whether Research Analyst has served as an officer, director or employee of the subject company covered No

Whether the Research Analyst or Research Entity has been engaged in market making activity of the Subject Company; No

Analyst Certification of Independence

The views expressed in this research report accurately reflect the analyst’s personal views about any and all of the subject securities or issuers; and no part of the research

analyst’s compensations was, is or will be, directly or indirectly, related to the specific recommendation or views expressed in the report.

Additional Disclaimer for US Institutional Investors

This research report prepared by Spark Capital Advisors (India) Private Limited is distributed in the United States to US Institutional Investors (as defined in Rule 15a-6 under

the Securities Exchange Act of 1934, as amended) only by Auerbach Grayson, LLC, a broker-dealer registered in the US (registered under Section 15 of Securities Exchange

Act of 1934, as amended). Auerbach Grayson accepts responsibility on the research reports and US Institutional Investors wishing to effect transaction in the securities

discussed in the research material may do so through Auerbach Grayson. All responsibility for the distribution of this report by Auerbach Grayson, LLC in the US shall be borne

by Auerbach Grayson, LLC. All resulting transactions by a US person or entity should be effected through a registered broker-dealer in the US. This report is not directed at you

if Spark Capital Advisors (India) Private Limited or Auerbach Grayson, LLC is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available

to you. You should satisfy yourself before reading it that Auerbach Grayson, LLC and Spark Capital Advisors (India) Private Limited are permitted to provide research material

concerning investment to you under relevant legislation and regulations;

Page 38