the iam in 2030 · new digital ecosystem key drivers for disruption in the iam value chain source:...

TRANSCRIPT

Pre-Selection of global automotive trends impacting the independent multi-brand aftermarket

10th of June 2016

The IAM in 2030

2

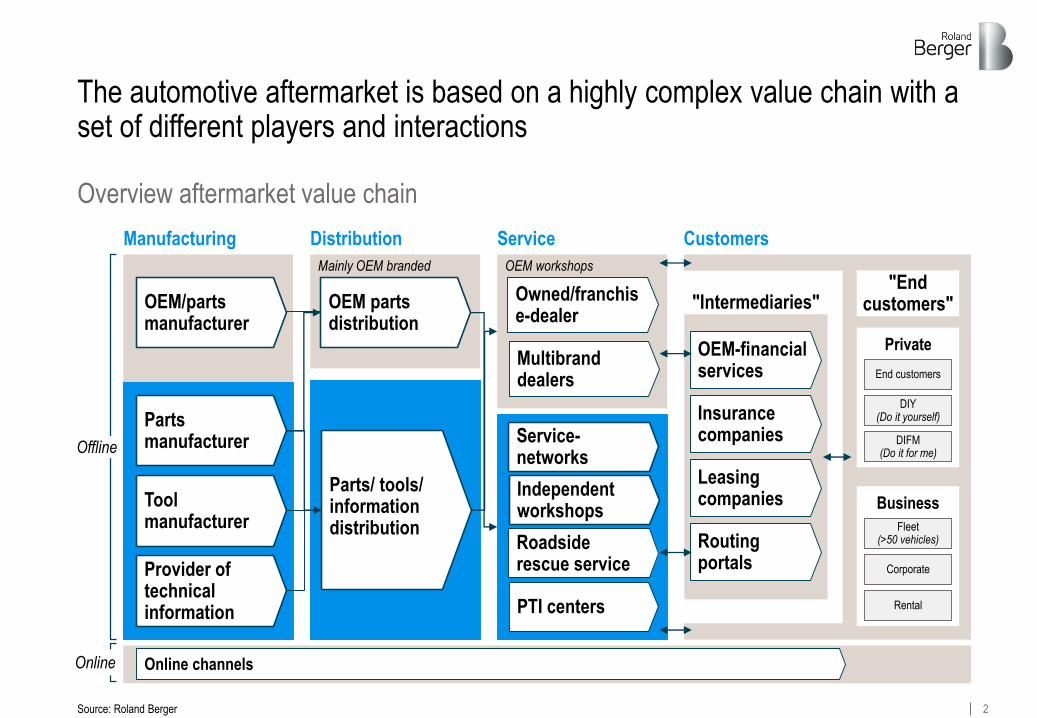

Overview aftermarket value chain

The automotive aftermarket is based on a highly complex value chain with a set of different players and interactions

Source: Roland Berger

Manufacturing

Mainly OEM branded

Distribution

OEM workshops

Service

OEM/parts manufacturer

OEM parts distribution

Owned/franchise-dealer

Multibranddealers

Independent workshops

Service-networks

Offline

Online

Customers

"Intermediaries"

Roadside rescue service

OEM-financial services

Insurance companies

Leasingcompanies

Routing portals

Private

"End customers"

End customers

DIY(Do it yourself)

DIFM(Do it for me)

Business

Fleet(>50 vehicles)

Corporate

Rental

Online channels

Parts/ tools/ information distribution

Parts manufacturer

Toolmanufacturer

Provider of technical information PTI centers

3

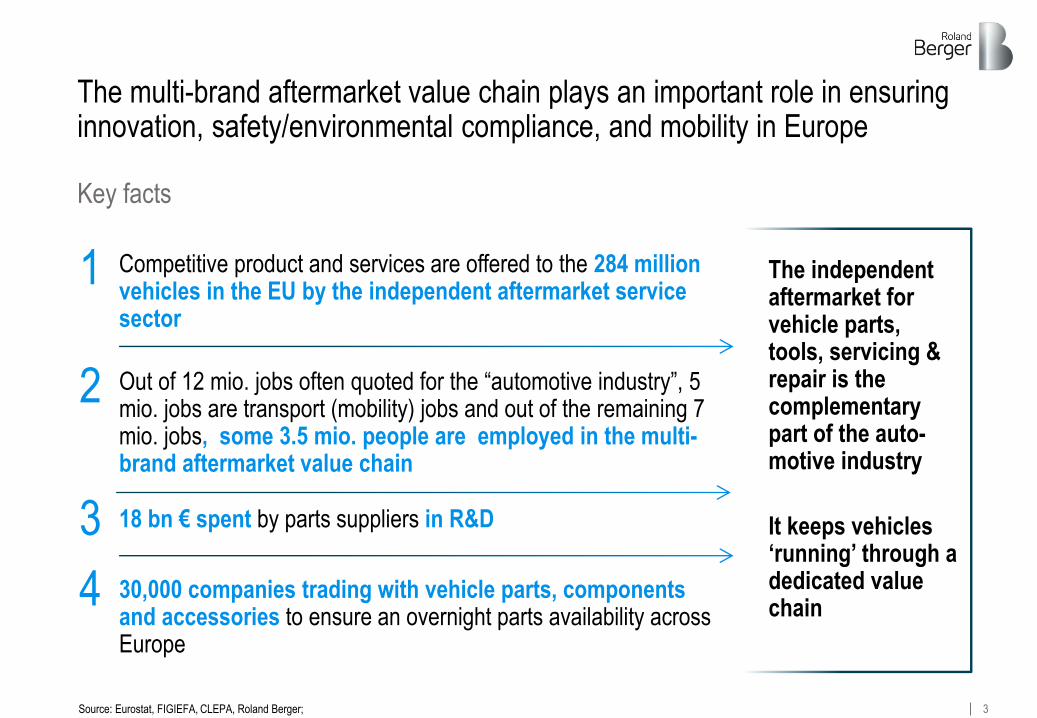

The multi-brand aftermarket value chain plays an important role in ensuring innovation, safety/environmental compliance, and mobility in Europe

Key facts

Source: Eurostat, FIGIEFA, CLEPA, Roland Berger;

The independent aftermarket for vehicle parts, tools, servicing & repair is the complementary part of the auto-motive industry

It keeps vehicles ‘running’ through a dedicated value chain

Competitive product and services are offered to the 284 million vehicles in the EU by the independent aftermarket service sector

1

Out of 12 mio. jobs often quoted for the “automotive industry”, 5 mio. jobs are transport (mobility) jobs and out of the remaining 7 mio. jobs, some 3.5 mio. people are employed in the multi-brand aftermarket value chain

2

18 bn € spent by parts suppliers in R&D 3

30,000 companies trading with vehicle parts, components and accessories to ensure an overnight parts availability across Europe

4

4

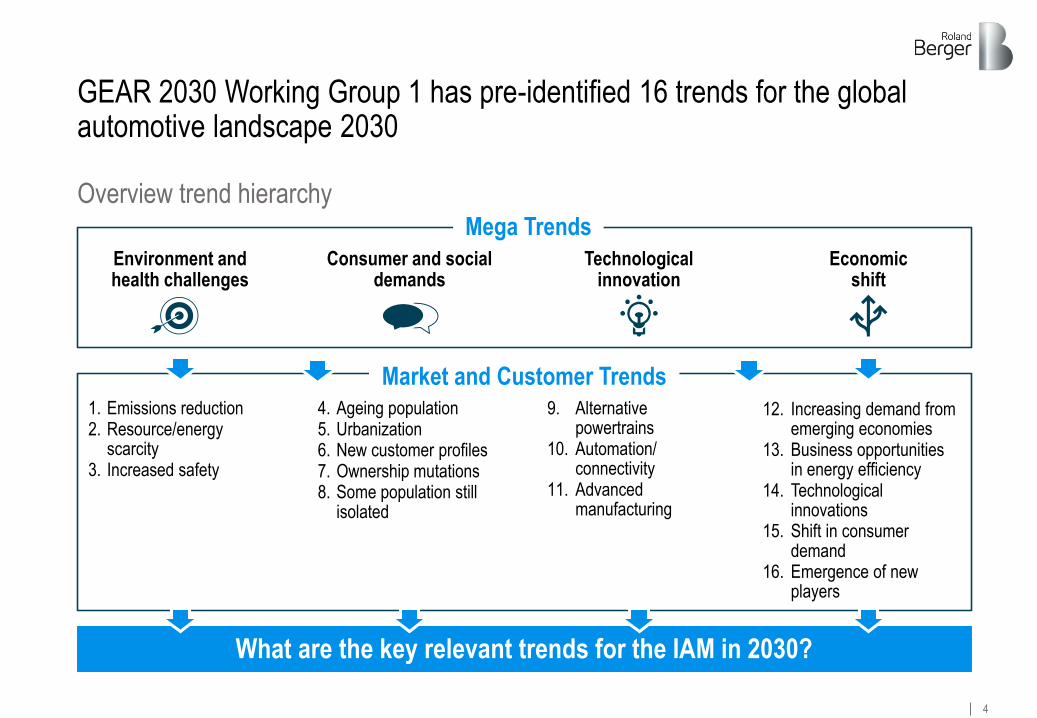

GEAR 2030 Working Group 1 has pre-identified 16 trends for the global automotive landscape 2030

Overview trend hierarchyMega Trends

Market and Customer Trends

What are the key relevant trends for the IAM in 2030?

Environment and health challenges

Consumer and social demands

Economicshift

Technological innovation

1. Emissions reduction2. Resource/energy

scarcity3. Increased safety

4. Ageing population5. Urbanization6. New customer profiles7. Ownership mutations8. Some population still

isolated

9. Alternative powertrains

10. Automation/ connectivity

11. Advanced manufacturing

12. Increasing demand from emerging economies

13. Business opportunities in energy efficiency

14. Technological innovations

15. Shift in consumer demand

16. Emergence of new players

5

Change of customer structure

Powertrain technology

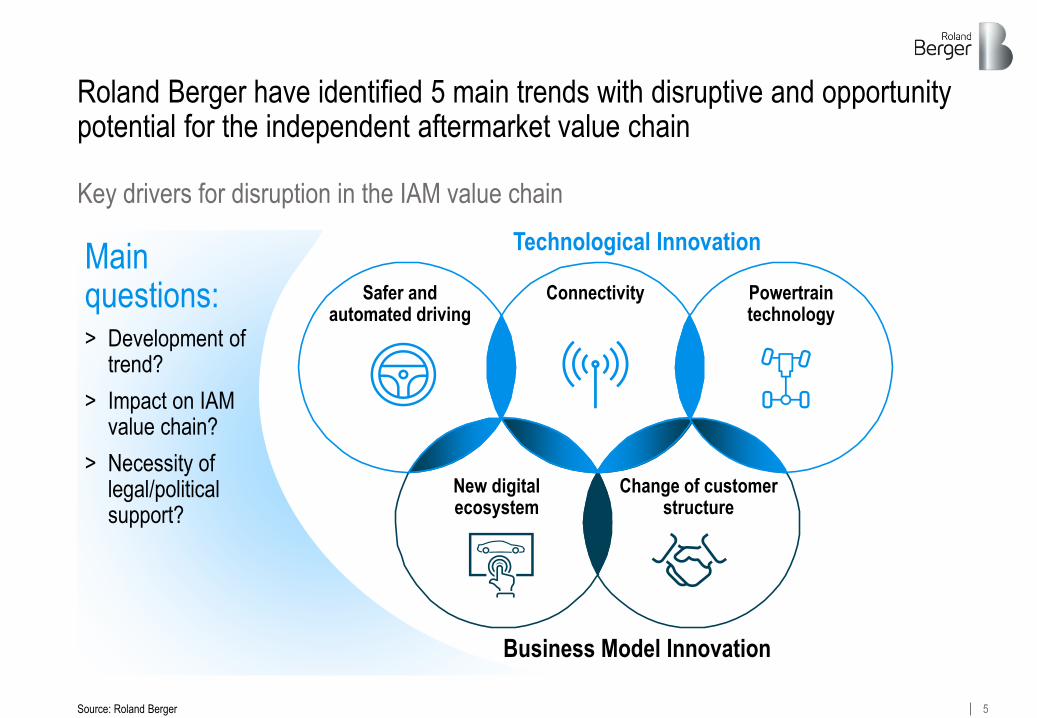

Roland Berger have identified 5 main trends with disruptive and opportunity potential for the independent aftermarket value chain

Main questions:> Development of

trend?

> Impact on IAM value chain?

> Necessity oflegal/political support?

Safer and automated driving

Connectivity

New digitalecosystem

Key drivers for disruption in the IAM value chain

Source: Roland Berger

Technological Innovation

Business Model Innovation

6

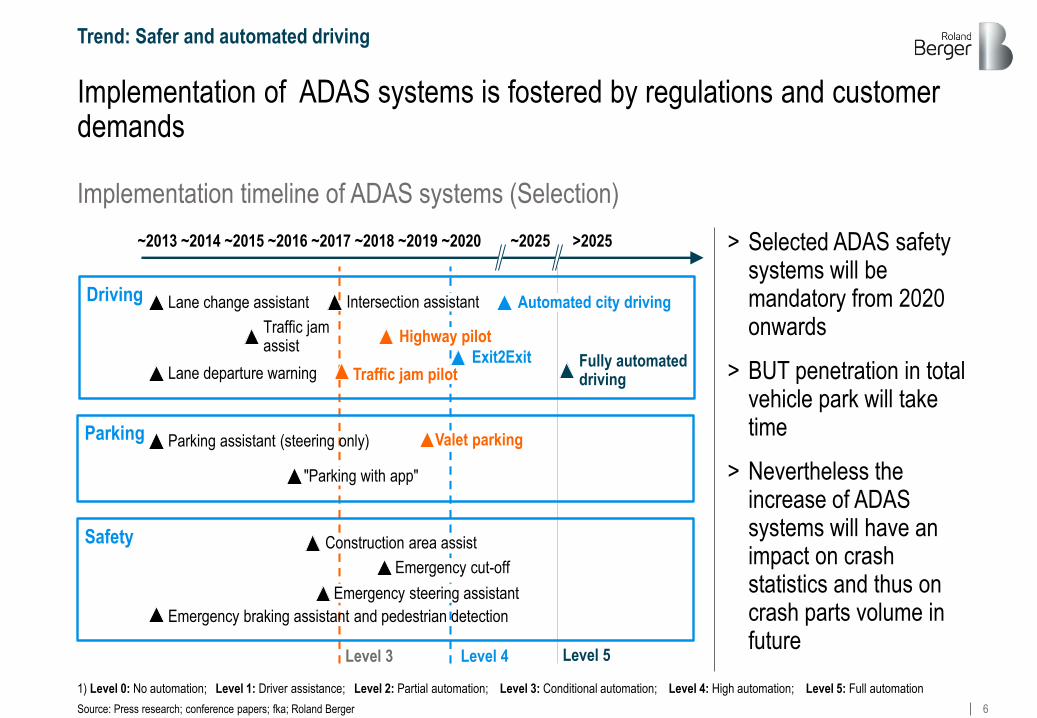

Implementation timeline of ADAS systems (Selection)

Implementation of ADAS systems is fostered by regulations and customer demands

Level 3 Level 4

~2013 ~2020~2016~2014 ~2015 ~2017 ~2018 ~2019 ~2025 >2025

Parking assistant (steering only) Valet parking

"Parking with app"

Emergency braking assistant and pedestrian detection

Emergency steering assistant

Emergency cut-off

Lane change assistant Automated city driving

Lane departure warning

Intersection assistant

Highway pilot

Traffic jam pilotFully automateddriving

Parking

Safety

Driving

Construction area assist

Traffic jamassist

Exit2Exit

Level 5

1) Level 0: No automation; Level 1: Driver assistance; Level 2: Partial automation; Level 3: Conditional automation; Level 4: High automation; Level 5: Full automation

Source: Press research; conference papers; fka; Roland Berger

Trend: Safer and automated driving

> Selected ADAS safety systems will be mandatory from 2020 onwards

> BUT penetration in total vehicle park will take time

> Nevertheless the increase of ADASsystems will have an impact on crash statistics and thus on crash parts volume in future

7

Only minor share of sold vehicles will be Level 4 or higher equipped in 2025, which is a prerequisite for automated driving

> In 2025, 50% of new vehicle sales will be at least Level 1 equipped

> Minor share of vehicles will be Level 3 and higher equipped

> Fully automated driving is expected in 2025-2030

Development of car production differentiated by HAD-Level des [Mio. units]

Level 0

2025

Level 1

Level 2

Level 3

21.7

5.0

3.3

9.5

20.7

3.7

0.1

2020

11.6

8.1

0.7 0.4

2016

19.6

15.8

3.8

CAGR2020-2025

-22.4%

3.4%

-

59.6%

50.2%

Total 0.9%

Europe

Source: IHS figures, adapted by Roland Berger expert judgment (scenario based)

Level 4

Trend: Safer and automated driving

8

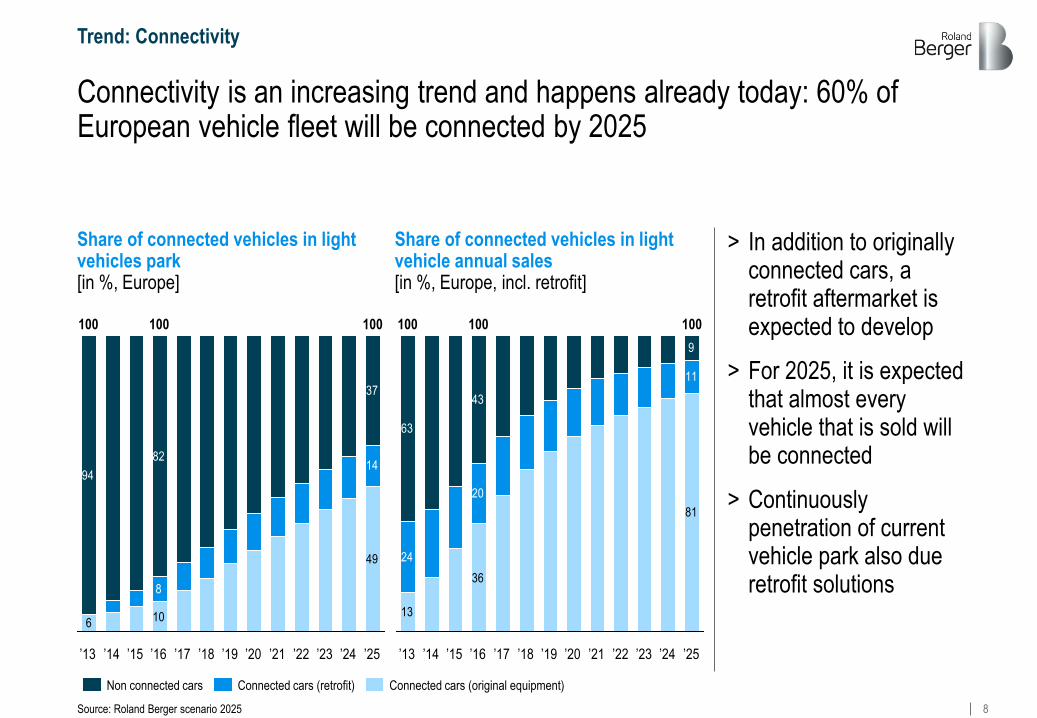

81

36

13

11

20

24

9

43

63

’25

100

’24’23’22’21’20’19’18’17’16

100

’15’14’13

100

10

49

6

8

1482

37

94

’21’20’19’18’17’16

100

’15’14’13

100

’25

100

’24’23’22

Connectivity is an increasing trend and happens already today: 60% of European vehicle fleet will be connected by 2025

> In addition to originally connected cars, a retrofit aftermarket is expected to develop

> For 2025, it is expected that almost every vehicle that is sold will be connected

> Continuously penetration of current vehicle park also due retrofit solutions

Source: Roland Berger scenario 2025

Trend: Connectivity

Share of connected vehicles in light vehicles park [in %, Europe]

Share of connected vehicles in light vehicle annual sales[in %, Europe, incl. retrofit]

Connected cars (original equipment)Connected cars (retrofit)Non connected cars

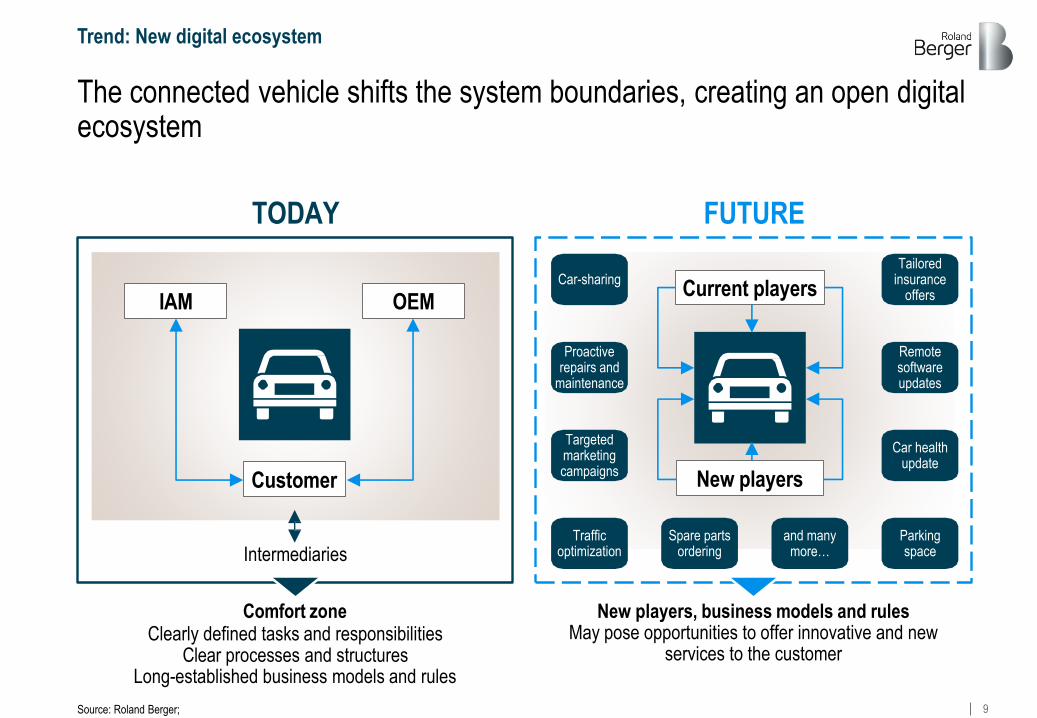

9

The connected vehicle shifts the system boundaries, creating an open digital ecosystem

Trend: New digital ecosystem

Source: Roland Berger;

TODAY

Comfort zoneClearly defined tasks and responsibilities

Clear processes and structuresLong-established business models and rules

New players, business models and rulesMay pose opportunities to offer innovative and new

services to the customer

Intermediaries

Tailored insurance

offers

Customer

IAM OEM

FUTURE

New players

Current players

Remote software updates

Car health update

Parking space

and many more…

Spare parts ordering

Car-sharing

Proactive repairs and

maintenance

Targeted marketing campaigns

Traffic optimization

10

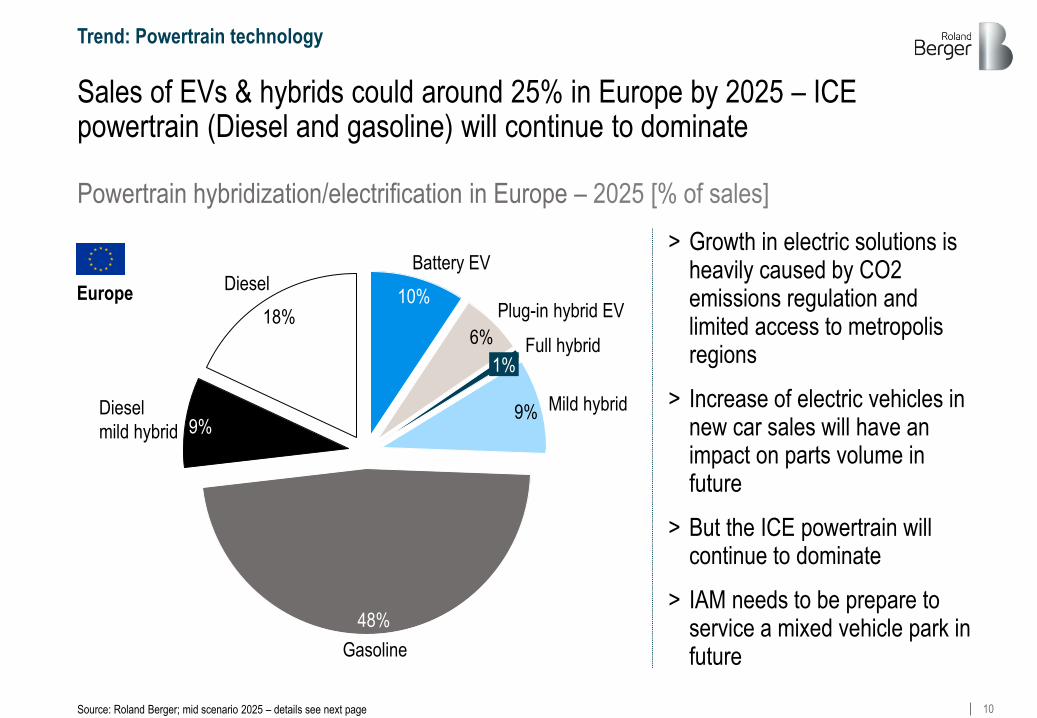

Sales of EVs & hybrids could around 25% in Europe by 2025 – ICE powertrain (Diesel and gasoline) will continue to dominate

Powertrain hybridization/electrification in Europe – 2025 [% of sales]

Europe

Gasoline

48%

Mild hybrid9%

Full hybrid1%

Plug-in hybrid EV

6%

Battery EV

10%

9%Diesel

mild hybrid

18%

Diesel

Trend: Powertrain technology

> Growth in electric solutions is heavily caused by CO2 emissions regulation and limited access to metropolis regions

> Increase of electric vehicles in new car sales will have an impact on parts volume in future

> But the ICE powertrain will continue to dominate

> IAM needs to be prepare to service a mixed vehicle park in future

Source: Roland Berger; mid scenario 2025 – details see next page

11

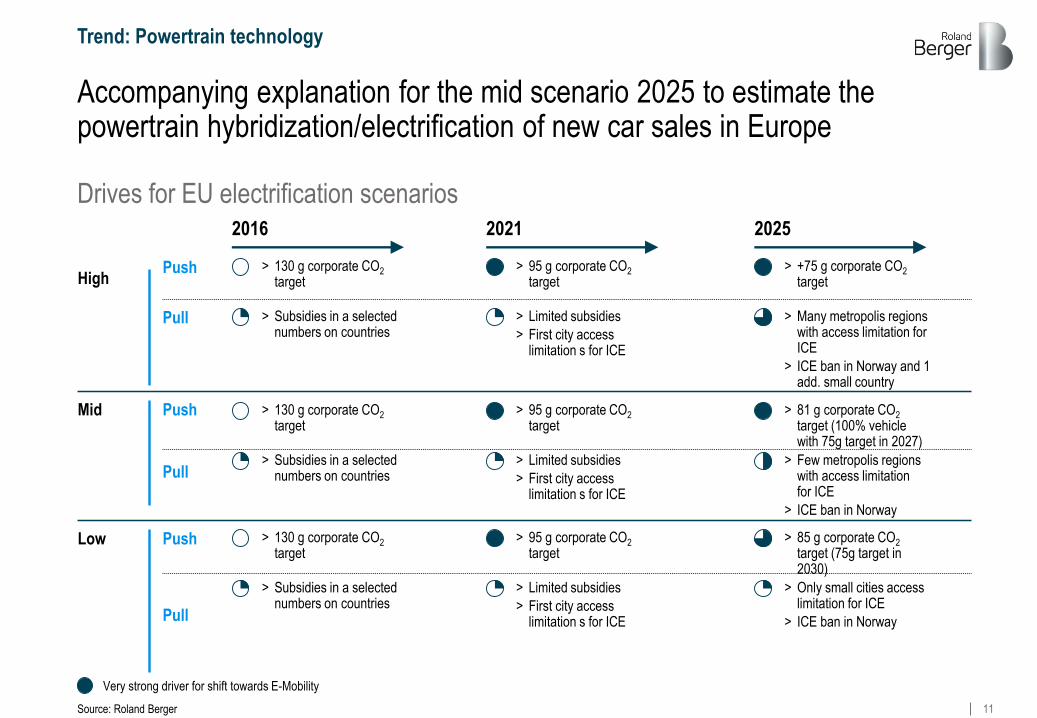

Accompanying explanation for the mid scenario 2025 to estimate the powertrain hybridization/electrification of new car sales in Europe

Very strong driver for shift towards E-Mobility

2016 2021 2025

Push > 130 g corporate CO2

target> 95 g corporate CO2

target> +75 g corporate CO2

target

Pull > Subsidies in a selected numbers on countries

> Limited subsidies

> First city access limitation s for ICE

> Many metropolis regions with access limitation for ICE

> ICE ban in Norway and 1 add. small country

Push

Pull

Push

Pull

Drives for EU electrification scenarios

Source: Roland Berger

High

Mid

Low

> 130 g corporate CO2

target> 95 g corporate CO2

target> 81 g corporate CO2

target (100% vehicle with 75g target in 2027)

> Subsidies in a selected numbers on countries

> Limited subsidies

> First city access limitation s for ICE

> Few metropolis regions with access limitation for ICE

> ICE ban in Norway

> 130 g corporate CO2

target> 95 g corporate CO2

target> 85 g corporate CO2

target (75g target in 2030)

> Subsidies in a selected numbers on countries

> Limited subsidies

> First city access limitation s for ICE

> Only small cities access limitation for ICE

> ICE ban in Norway

Trend: Powertrain technology

12

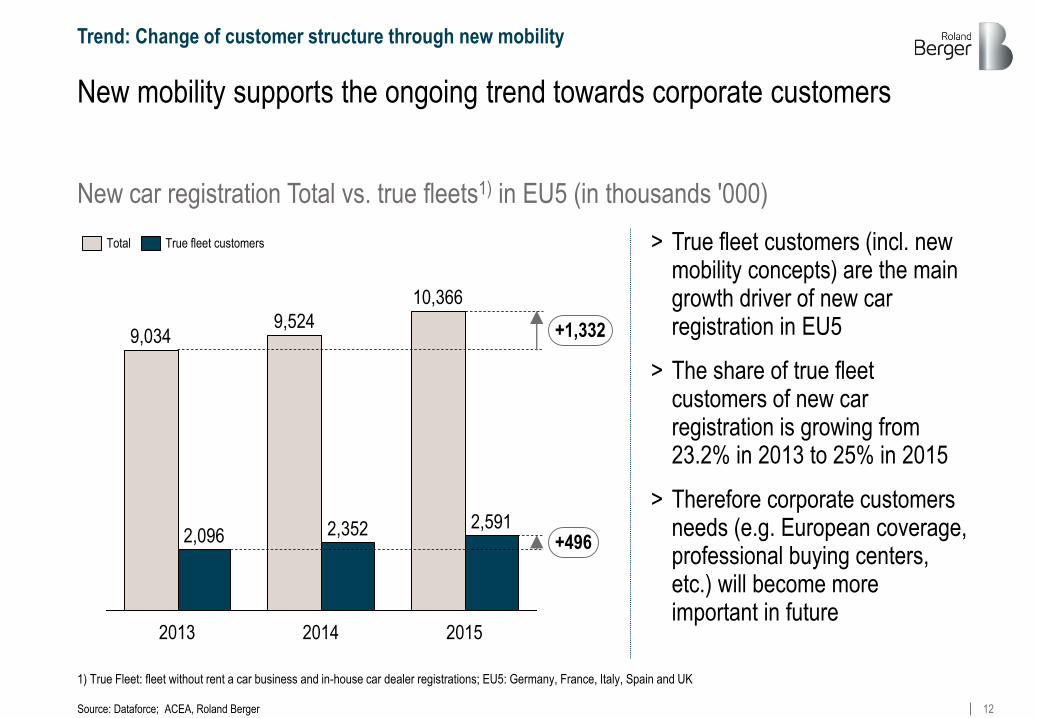

New car registration Total vs. true fleets1) in EU5 (in thousands '000)

New mobility supports the ongoing trend towards corporate customers

Source: Dataforce; ACEA, Roland Berger

Trend: Change of customer structure through new mobility

> True fleet customers (incl. new mobility concepts) are the main growth driver of new car registration in EU5

> The share of true fleet customers of new car registration is growing from 23.2% in 2013 to 25% in 2015

> Therefore corporate customers needs (e.g. European coverage, professional buying centers, etc.) will become more important in future

1) True Fleet: fleet without rent a car business and in-house car dealer registrations; EU5: Germany, France, Italy, Spain and UK

9,524

2,352

2015

2,591

2014

10,366

2,096

2013

9,034

+496

+1,332

True fleet customersTotal

13

New mobility concepts will change the customer structure towards a higher share of corporate customers – Need to find answers to more EU-wide and globally structured customers.

Going forward – Key points to be considered

Connectivity is a increasing trend and happens already today – New business models, players and rules will arise, creating new ecosystems. This engenders the need for the aftermarket supply chain to offer and innovate new services to be part of the future ecosystem

ICE powertrain will continue to dominate in future; electric powertrains will play a minor role – IAM needs to be prepared to service a mixed vehicle park in future

Implementation of ADAS systems is fostered by regulations and customer demands – And will have an impact on crash statistics and thus on crash part volume in future

Summary

Source: Roland Berger

5

1

2

3

4

Only minor share of vehicles will be Level 4 or higher equipped in 2025 – Thus fully automated driving is not expected before 2025