the hybrid db/dc plan model: an effective approach for ... hybrid db/dc plan model: an effective...

TRANSCRIPT

The hybrid DB/DC plan model: An effective approach for government pension providers

Historically, state and local governments have successfully relied on defined benefit (DB) pension plans as the fundamental component of a successful employee retirement program. But, in recent years, deep-rooted financial issues have emerged and challenged both the sustainability of some traditional DB plans and the ability of governments to provide required public services.

Given these financial realities, many governments are now examining whether standard 401(k) plans can help, but are finding that these plans have their own shortcomings that make them unsuitable as vehicles for providing adequate and secure retirement income for public employees.

As an alternative, many state and local governments are turning to hybrid DB/DC plan models as a balanced approach to reduce their singular reliance on, and help avoid the financial risks of, the traditional DB plan of the past, while preserving the positive features of those plans. Unlike traditional 401(k)-style defined contribution (DC) plans, which focus on asset accumulation, the new hybrid DB/DC plans should continue to focus on seeking to provide retirement income adequacy and security. The DC components of these hybrid approaches should also include features that mitigate investment and longevity risk for employees while providing funding stability and budgetary predictability for government employers.

Many legislators and other government policy makers remain unfamiliar with how hybrid DB/DC plans can be successfully structured. This paper explores the components and best practice design features of these plans and specific plan provisions to serve as a guide to state and local governments that are considering a hybrid DB/DC solution.

Key principles for effective plan designThere are several principles that should be taken into consideration when designing any government retirement program. Retirement plans should:

W Provide adequate and secure income throughout retirement as a formal primary objective. This supports work force management mandates, including attracting and retaining quality employees and facilitating an orderly transition into retirement.

W Provide full-career employees with a target replacement income from all sources at a level sufficient to maintain the employee’s preretirement standard of living during retirement.

W Recognize the needs of a mobile work force by offering equitable benefits for less than full-career employees in a manner consistent with work force attraction, retention and budget objectives of the employer.

W Take risks into account to create a high degree of certainty that participants will achieve an adequate and secure income throughout retirement. The plan design should address funding-shortfall risk (the risk that total employer and employee funding is not adequate to achieve the desired income replacement objectives); longevity risk (the risk that the retiree will outlive his or her retirement assets); investment risk, including normal market volatility and risk attributable to more severe economic downturns; inflation risk; and annuitization rate risk.

W Recognize that achieving retirement income adequacy and security for employees is a responsibility to be shared between the employer and employees. Employee participation in a primary retirement benefit plan should be mandatory. Both the employer and employees should share in the cost and risk of funding plan benefits.

The hybrid DB/DC plan model | July 2012 2

The hybrid DB/DC plan model

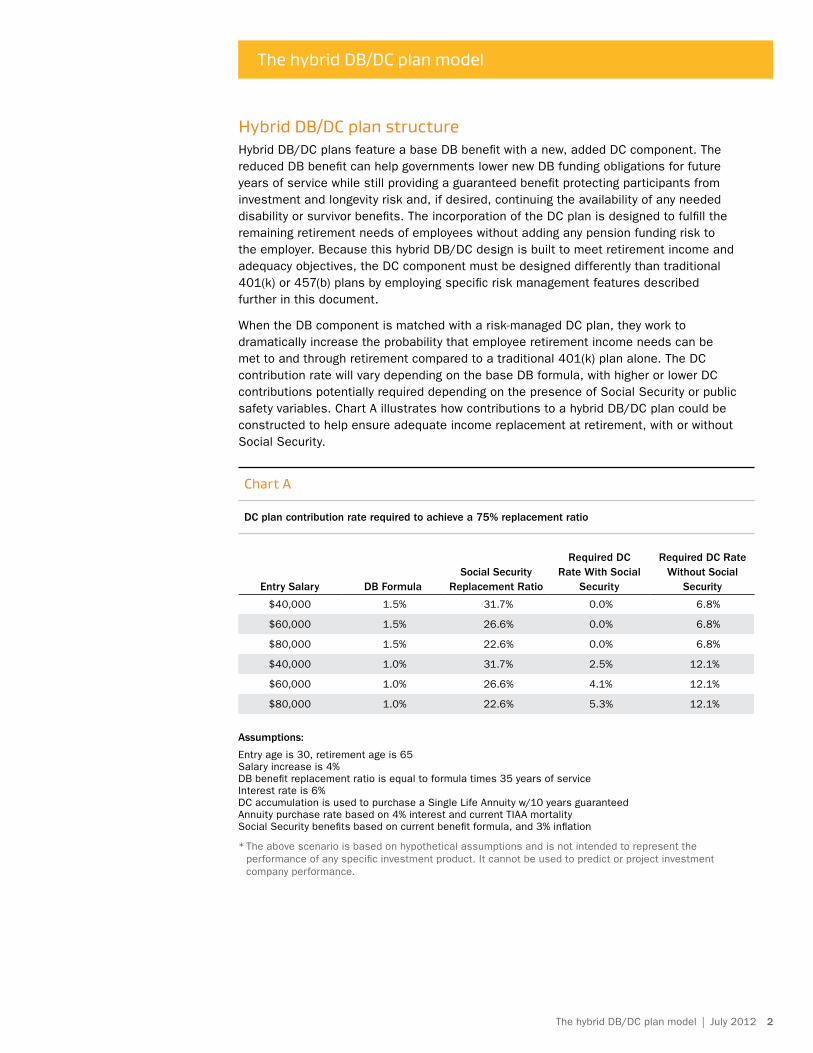

Chart A

DC plan contribution rate required to achieve a 75% replacement ratio

Entry Salary DB FormulaSocial Security

Replacement Ratio

Required DC Rate With Social

Security

Required DC Rate Without Social

Security

$40,000 1.5% 31.7% 0.0% 6.8%

$60,000 1.5% 26.6% 0.0% 6.8%

$80,000 1.5% 22.6% 0.0% 6.8%

$40,000 1.0% 31.7% 2.5% 12.1%

$60,000 1.0% 26.6% 4.1% 12.1%

$80,000 1.0% 22.6% 5.3% 12.1%

Assumptions:

Entry age is 30, retirement age is 65 Salary increase is 4% DB benefit replacement ratio is equal to formula times 35 years of service Interest rate is 6% DC accumulation is used to purchase a Single Life Annuity w/10 years guaranteed Annuity purchase rate based on 4% interest and current TIAA mortality Social Security benefits based on current benefit formula, and 3% inflation

* The above scenario is based on hypothetical assumptions and is not intended to represent the performance of any specific investment product. It cannot be used to predict or project investment company performance.

Hybrid DB/DC plan structureHybrid DB/DC plans feature a base DB benefit with a new, added DC component. The reduced DB benefit can help governments lower new DB funding obligations for future years of service while still providing a guaranteed benefit protecting participants from investment and longevity risk and, if desired, continuing the availability of any needed disability or survivor benefits. The incorporation of the DC plan is designed to fulfill the remaining retirement needs of employees without adding any pension funding risk to the employer. Because this hybrid DB/DC design is built to meet retirement income and adequacy objectives, the DC component must be designed differently than traditional 401(k) or 457(b) plans by employing specific risk management features described further in this document.

When the DB component is matched with a risk-managed DC plan, they work to dramatically increase the probability that employee retirement income needs can be met to and through retirement compared to a traditional 401(k) plan alone. The DC contribution rate will vary depending on the base DB formula, with higher or lower DC contributions potentially required depending on the presence of Social Security or public safety variables. Chart A illustrates how contributions to a hybrid DB/DC plan could be constructed to help ensure adequate income replacement at retirement, with or without Social Security.

The hybrid DB/DC plan model | July 2012 3

The hybrid DB/DC plan model

Implementing a hybrid DB/DC plan designThe hybrid DB/DC plan is not intended to replace an existing DB plan, rather, the new hybrid DB/DC plan would continue to use the existing DB plan for the reduced DB benefit. The DC component would operate concurrently with the modified existing DB plan. Depending on the specific state or local government’s objectives and legal environment, the hybrid DB/DC plan could be open only to new employees, or to both new employees and select current employees.

Some governments have reservations about migrating from the traditional DB structure to a hybrid DB/DC format. Plan sponsors cite fears of an increased risk of non-participation, or that a wide selection of investment choices in the DC component may confuse participants.

However, plan sponsors can establish plan features at the outset that will ensure participation and adequacy of contributions. They can also adopt investment structures that help ensure and support appropriate investment decision-making.

There are three key aspects of plan design that must incorporate proper risk-management techniques. These are:

1. Investment - One concern with the hybrid DB/DC structure is that the plan may burden participants with investment decision-making and may lead them to make poor decisions about how to invest their retirement accounts. Since employees need to properly diversify their investments, and rebalance their portfolios regularly to maintain a prudent asset mix, these aspects need to be incorporated in plan features. With the proper plan architecture, plan sponsors can support wise participant decision-making, by offering:

W A limited lower-cost investment menu that would include no more than 15 -20 preselected options representing the various asset classes.

W Automatic or default asset allocation vehicles such as lifecycle or target date funds that provide an age-appropriate asset allocation.

W Individual investment advice to help educate participants and enhance their decision-making prowess.

2. Communication, Education and Advice - While every person’s journey toward financial well-being differs, there are often common steps along the way. Communications and educational tools that are targeted to specific life stages and events ensure that participants receive the right information in the right format at the right level of engagement. Supplementing this communication with expert financial advice, at no additional cost to the participant, is also critical - ensuring that participants have access to an experienced, objective advisor can help ensure that participants stay on the right path to and through retirement. This is particularly true for public safety officers and others with more complex financial planning needs.

3. Distribution at Retirement - Retirement income employees will not outlive.1 Too many standard 401(k)-style retirement plan models focus exclusively on asset accumulation, and fail to include payout features that help ensure that retirees will not outlive their savings. The new hybrid DB/DC plan should include:

W A mechanism to automatically convert a sufficient portion of an employee’s DC account balance to a low-cost annuity upon retirement, to guarantee lifetime income.

W Restrictions to prevent employees from taking large early distributions from their plan, thus preventing “leakage” from their accounts and helping employees retain sufficient assets for retirement.

The hybrid DB/DC plan model

(07/12)C3729

The hybrid DB/DC plan model

A long-term perspectiveState and local governments and their employees can be well served by the hybrid DB/DC plan model, so long as these plans are constructed to meet the objectives of a risk-managed retirement program. Given the career mobility of employees, the funding issues associated with many DB plans and the need for lifetime financial security, the move to a hybrid DB/DC model is a natural evolution in state and local government core pension plan design.

1 Subject to the issuer’s claims-paying ability.2 Source: LIMRA, Not-for-Profit Market Survey, first-quarter 2012 results. Average assets per participant based

on full-service business. Highest account balances is not indicative of investment returns.

For the latest quarterly data on TIAA-CREF, please visit: www.tiaa-cref.org/public/about/identity/get_to_know_us/company-stats-facts/

You should consider the investment objectives, risks, charges and expenses carefully before investing. Please call 877 518-9161, or go to tiaa-cref.org for a current prospectus that contains this and other information. Please read the prospectus carefully before investing.Annuity contracts and certificates are issued by Teachers Insurance and Annuity Association (TIAA) and College Retirement Equities Fund (CREF), New York, NY. TIAA-CREF Individual & Institutional Services, LLC and Teachers Personal Investors Services, Inc., members FINRA, distribute securities products.

For Institutional Investor Use Only. Not for Use with or Distribution to the Public.

© 2012 Teachers Insurance and Annuity Association-College Retirement Equities Fund (TIAA-CREF), 730 Third Avenue, New York, NY 10017

To learn moreWe would like you to learn more about how TIAA-CREF can help your government develop and implement a retirement plan for your employees. For more information please visit www.tiaa-cref.org/government or contact:

Why TIAA-CREF?With our long experience and considerable expertise, TIAA-CREF is uniquely qualified to provide public policy makers and government leaders with sound guidance on the important considerations for the design of effective retirement programs for their employees. In fact, we were recently selected by the State of Rhode Island to manage their new hybrid retirement plan.

Today our commitment to retirement preparedness is stronger than ever. Our risk-managed DC retirement plan offerings have been successful across a broad array of market segments. In addition, in a recent survey of 30 companies, TIAA-CREF participants had the highest average retirement account balances.2