the global wind outlook - global wind energy council · hydro 17% onshore wind 8% utility-scale pv,...

TRANSCRIPT

Global Wind Power Installations & Financing Outlook Vietnam Wind Power Conference, 2019

Ashish Sethia

June 11, 2019

@asethia@BloombergNEF

1 June 11, 2019

Sustainable materials

& circular economy

BloombergNEFStrategies for a cleaner future Solar Wind Storage Decentralized

energy

Frontier power Heat Impact on

power & utilities

IoT technologies

& platformsAdvanced

analytics

& automation

Digital business

model evolutionDigitialization of

energy, industry

& supply chains

Electrified

transportMobility

services

Connected &

autonomous

vehicles

Impact on

transport

Impact on

oil & power

Carbon Power markets Oil & products

Gas & LNG Chemicals Metals

3D printing &

green manufacturing

Composites, bioplastics &

new materials

Impact on industrials,

utilities & manufacturing

Policy

Economics

& forecasts

Sustainability

Innovation

& tech

Finance

2 June 11, 2019

Source: The Institute of Future, Gartner

Amara’s Law & Hype Cycles“We tend to overestimate the effect of a technology in the short run and

underestimate the effect in the long run”, Roy Amara

3 June 11, 2019

Technology led transitions of the past

Selected technologies’ penetration of U.S. households

Source: Michael Felton, NY tImes, https://www.census.gov/history/pdf/sipp-data-appliances.pdf

4 June 11, 2019

Source: BloombergNEF

How far are we in the energy transition?

Renewable

power (18%)Rooftop

solar (~2%)

Natural gas

power (35%)

Current penetration of selected technologies in power generation, U.S.

5 June 11, 2019

-

200

400

600

800

1,000

1,200

Cumulative GW

Small-scale PV

Utility-scale PV

Offshorewind

Onshorewind

Source: Bloomberg NEF.

Wind and solar are at terawatt scale, storage is accelerating

Global wind and solar installations Global stationary energy storage installations

0

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015 2016 2017 2018

Cumulative GW

EMEA

AMER

APAC

6 June 11, 2019

Source: BloombergNEF Note: the PV LCOE is for a tracking PV system.

PV tracking capacity factors in the US: 14%-30% in 2018 and onshore

wind: 29%-49% in 2018

Source: BloombergNEF Note: PV capacity factors in China: 12%-18%

in 2018, onshore wind 23%-32%. Coal and gas plants LCOEs include

a carbon price.

China U.S.

Utility-scale PV

CCGT

Onshore wind

Coal

0

20

40

60

80

100

2018 2025 2030 2035 2040 2045 2050

LCOE ($/MWh, real 2017)

Utility-scale PV

Onshore wind

CCGT

Coal

0

10

20

30

40

50

60

70

80

2018 2025 2030 2035 2040 2045 2050

LCOE ($/MWh, real 2017)

Tipping point 1: new renewables vs new fossils

7 June 11, 2019

Source: BloombergNEF. Note: PV capacity factors in India: 18%-20%

in 2018, onshore wind 25%-35%.

Source: BloombergNEF Note: the PV LCOE is for a tracking PV system.

PV tracking capacity factors in the US: 14%-30% in 2018 and onshore

wind: 29%-49% in 2018

U.S. India

Tipping point 2: new renewables vs existing fossils

CCGT

Utility-scale PV

Coal

Onshore wind

0

10

20

30

40

50

60

70

80

2018 2025 2030 2035 2040 2045 2050

LCOE vs running costs ($/MWh, 2017 real)

CCGT

Utility-scale PV

Coal

Onshore wind

0

10

20

30

40

50

60

2018 2025 2030 2035 2040 2045 2050

LCOE vs running costs ($/MWh, 2017 real)

8 June 11, 2019

Source: BloombergNEF

Total installed capacity, 2017 (GW) Total installed capacity, 2050 (GW)

79% of new power generating capacity will be renewable

Coal30%

Gas19%

Peaker Gas4%

Oil5%

Nuclear5%

Hydro17%

Onshore wind8%

Utility-scale PV, 4%

6,596GW

Coal5% Gas

9%Peaker

Gas6%

Nuclear2%

Hydro9%

Onshore wind15%

Offshore wind2%

Utility-scale PV

28%

Small-scale PV

12%

16,977GW

Flexible

capacity

9%

Half a decade for the next wind and solar TW

9 June 11, 2019

Source: BloombergNEF

Global investment in power generation by

region, 2018-2050

Asia Pacific investment in power generation by

region, 2018-2050

$0.5

$1.6

$1.9

$1.9

$5.6

ROW

META

AMER

Europe

APAC

Cumulative investment ($tn, 2017 real)

$0.1

$0.2

$0.3

$0.5

$1.6

$2.7

Australia

South Korea

Japan

Southeast Asia

India

China

Cumulative investment ($tn, 2017 real)

Coal Gas Oil Nuclear Hydro Wind Solar Other

Asia needs ~1/2 of global power generation investment

10 June 11, 2019

Source: Bloomberg NEF. Notes: Data for 2008-22 from 3Q 2018 Global Wind Market Outlook; 2023-40 data from New Energy Outlook 2018.

0

20

40

60

80

100

120

140

160

2010 2015 2020 2025 2030 2035 2040

Gigawatts

Commissioning year

Historic

Global onshore wind forecast

11 June 11, 2019

0

20

40

60

80

100

120

140

160

2010 2015 2020 2025 2030 2035 2040

Gigawatts

Commissioning year

HistoricShortterm

189GW

Global onshore wind forecast

Source: Bloomberg NEF. Notes: Data for 2008-22 from 3Q 2018 Global Wind Market Outlook; 2023-40 data from New Energy Outlook 2018.

12 June 11, 2019

0

20

40

60

80

100

120

140

160

2010 2015 2020 2025 2030 2035 2040

Gigawatts

Commissioning year

HistoricShortterm

Mediumterm

330GW

189GW

Global onshore wind forecast

Source: Bloomberg NEF. Notes: Data for 2008-22 from 3Q 2018 Global Wind Market Outlook; 2023-40 data from New Energy Outlook 2018.

13 June 11, 2019

0

20

40

60

80

100

120

140

160

180

2010 2015 2020 2025 2030 2035 2040

Gigawatts

Commissioning year

HistoricShortterm

Mediumterm

Long term

≈1,800GW

330GW

189GW

Global onshore wind forecast

Source: Bloomberg NEF. Notes: Data for 2008-22 from 3Q 2018 Global Wind Market Outlook; 2023-40 data from New Energy Outlook 2018.

14 June 11, 2019

0

20

40

60

80

100

120

140

160

180

2010 2015 2020 2025 2030 2035 2040

Gigawatts

Commissioning year

HistoricShortterm

Mediumterm

Long term

Feed-in-tariffs

Subsidies

Auctions

Hybrid

Economic build

Subsidy-free?

Wind project revenue drivers

Source: Bloomberg NEF. Notes: Data for 2008-22 from 3Q 2018 Global Wind Market Outlook; 2023-40 data from New Energy Outlook 2018.

15 June 11, 2019

Source: BloombergNEF . Note: Chart is for offsite PPAs only. APAC capacity is estimated. Figures are subject to change and may be updated as more

information is made available.

Corporate PPAs create new routes to market

1.5 3.4 2.4 3.9

9.1

0.8

2.32.0

0

12

24

36

48

60

0

3

6

9

12

15

2009 10 11 12 13 14 15 16 17 18 19YTD

Annual volume (GW)

AMER EMEA APAC Cumulative

Cumulative volume (GW)

0.3 0.1 0.3 0.3 1.02.2

4.6 4.26.2

13.4

16 June 11, 2019

MWhCost of

finance

Source: BloombergNEF

All project inputs have combined to drag down prices…

Capex O&M

≈

17 June 11, 2019

Source: BloombergNEF Note: Data shows levelized average winning date by commissioning date. Bids have been levelized to account for

indexation, exchange rate, tariff duration and expected merchant tail.

Competitive auctions have resulted in cost drops

8th capacity auction

25th energy auction

26th energy auction

27th energy auction 28th energy auction

Vietnam FiT

IV

VII & V

IIIII

I

II III IV V

1st auction

3rd auction

0

10

20

30

40

50

60

70

80

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$2017/MWh

Brazil

Vietnam FiT

Germany

India SECI

Mexico

18 June 11, 2019

Source: BloombergNEF

1.501.58

1.831.72

1.481.45

1.24

1.29

1.231.22

1.171.16

1.10

1.20

1.13

1.12

1.03

1.071.02

0.890.89

0.820.78

0.79

0.00.20.40.60.81.01.21.41.61.82.0

1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H 1H 2H

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

$m/MW

Wind turbine prices have declinedGlobal turbine price index by delivery date, 2H 2018

19 June 11, 2019

Source: BloombergNEF Note: Pricing for full-service initial agreements only. This includes routine and unscheduled maintenance, minor and major

component parts and labor.

O&M prices are falling too

39.1

50.6

45.0

51.1

35.4

50.0

28.8

21.3

26.4

20.518.1

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Thousand $/MW/yr

Full-service initial O&M contract pricing

20 June 11, 2019

Source: BloombergNEF

75MW

299MW

0%

10%

20%

30%

40%

50%

60%

70%

1980 1990 2000 2010 2020 2030 2040

Year

Capacity Factor (%)

Global forecast

Operational projects

weightedaverage

Onshore wind capacity factors are rising 1% point year-on-year

Historic and forecast onshore wind gross capacity factors

21 June 11, 2019

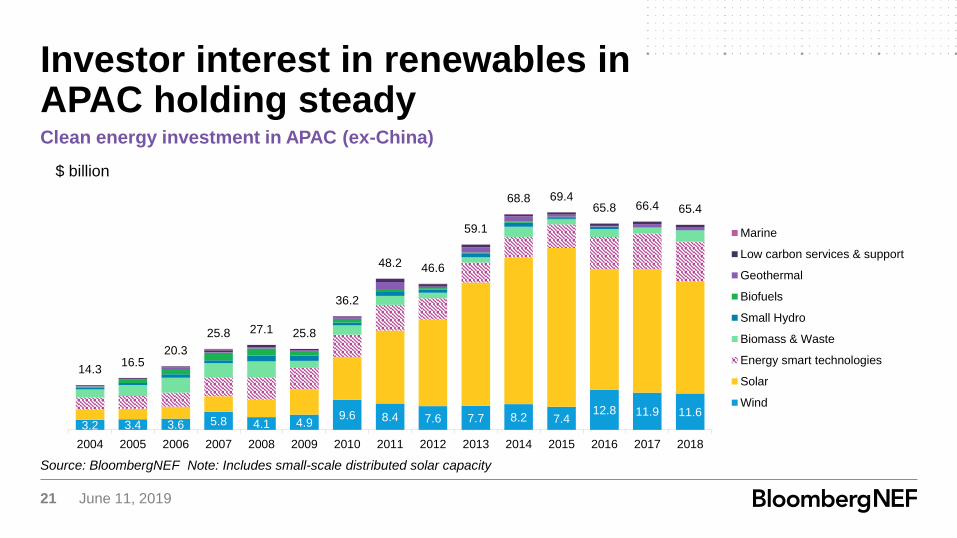

Source: BloombergNEF Note: Includes small-scale distributed solar capacity

Investor interest in renewables in APAC holding steadyClean energy investment in APAC (ex-China)

3.2 3.4 3.6 5.8 4.1 4.99.6 8.4 7.6 7.7 8.2 7.4

12.8 11.9 11.6

14.316.5

20.3

25.8 27.1 25.8

36.2

48.2 46.6

59.1

68.8 69.465.8 66.4 65.4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

$ billion

Marine

Low carbon services & support

Geothermal

Biofuels

Small Hydro

Biomass & Waste

Energy smart technologies

Solar

Wind

22 June 11, 2019

Source: Bloomberg Note: Reflective of fixed-for-floating swap rates.

Cheap debt is helping

Swap rates for select tenors and countries

23 June 11, 2019

Source: BloombergNEF Green Bonds Tool

4.214.7

37.3

51.7

103.1

173.6182.1

0

20

40

60

80

100

120

140

160

180

200

2012 2013 2014 2015 2016 2017 2018

$ billionHealth care

Consumer staples

Technology

Materials

Consumer discretionary

Industrial

U.S. municipal

Energy

Utilities

Government

Financial

Green bond issuance growing

24 June 11, 2019

Source: BloombergNEF Note: includes renewable energy and energy efficiency

Clean energy IPOs still too far and few

0

2

4

6

8

10

12

14

16

18

20

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

$bn

EMEA

APAC

AMER

25 June 11, 2019

Source: BloombergNEF Note: includes renewable energy and energy efficiency

But clean energy M&A rising steadily

0

20

40

60

80

100

120

140

160

180

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18

$bn

APAC

EMEA

AMER

26 June 11, 2019

0.0

10.0

20.0

30.0

40.0

50.0

60.0

0 20 40 60 80 100 120 140 160 180 200

Brazil

India

Canada

Mexico

Spain

Peru

Denmark

Uruguay

Italy

France

Panama

Estonia

Poland

Vietnam

Kenya

South Korea

Indonesia

$0/MWhRange 1H 2018 (mid) Mid

Source: BloombergNEF. Note: LCOE for a project starting construction in 2H 2018.

LCOEs in leading markets at $40-50/MWh

2H 2018 onshore wind LCOE

27 June 11, 2019

Source: BloombergNEF Note: Survey done in 2018.

Risks remain even in high-deployment markets

Financiers Risks IPPs

Financiers that ranked the parameter among the top two risks

IPPs that ranked the parameter among the top two risks

Curtailment - grid or offtake

Regulatory risks

Payment delays

Resource estimation errors

Land acquisition risks

Forex risks

Plant downtime

71% 86%

43% 71%

57% 14%

14% 0%

14% 29%

0% 0%

0% 0%

Perception of risk in Indian renewables projects

28 June 11, 2019

The Bloomberg NEF ("BNEF"), service/information is derived from selected public sources. Bloomberg Finance L.P. and its affil iates, in providing the

service/information, believe that the information it uses comes from reliable sources, but do not guarantee the accuracy or completeness of this information, which is

subject to change without notice, and nothing in this document shall be construed as such a guarantee. The statements in this service/document reflect the current

judgment of the authors of the relevant articles or features, and do not necessarily reflect the opinion of Bloomberg Finance L.P., Bloomberg L.P. or any of their

affiliates (“Bloomberg”). Bloomberg disclaims any liability arising from use of this document, its contents and/or this service. Nothing herein shall constitute or be

construed as an offering of financial instruments or as investment advice or recommendations by Bloomberg of an investment or other strategy (e.g., whether or not

to “buy”, “sell”, or “hold” an investment). The information available through this service is not based on consideration of a subscriber’s individual circumstances and

should not be considered as information sufficient upon which to base an investment decision. You should determine on your own whether you agree with the

content. This service should not be construed as tax or accounting advice or as a service designed to facilitate any subscriber’s compliance with its tax, accounting or

other legal obligations. Employees involved in this service may hold positions in the companies mentioned in the services/information.

The data included in these materials are for illustrative purposes only. The BLOOMBERG TERMINAL service and Bloomberg data products (the “Services”) are

owned and distributed by Bloomberg Finance L.P. (“BFLP”) except that Bloomberg L.P. and its subsidiaries (“BLP”) distribute these products in Argentina, Australia

and certain jurisdictions in the Pacific islands, Bermuda, China, India, Japan, Korea and New Zealand. BLP provides BFLP with global marketing and operational

support. Certain features, functions, products and services are available only to sophisticated investors and only where permitted. BFLP, BLP and their affiliates do

not guarantee the accuracy of prices or other information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial

instruments by BFLP, BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not

to “buy”, “sell” or “hold” an investment. Information available via the Services should not be considered as information suff icient upon which to base an investment

decision. The following are trademarks and service marks of BFLP, a Delaware limited partnership, or its subsidiaries: BLOOMBERG, BLOOMBERG ANYWHERE,

BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG PROFESSIONAL, BLOOMBERG TERMINAL and BLOOMBERG.COM. Absence of any trademark

or service mark from this list does not waive Bloomberg's intellectual property rights in that name, mark or logo. All rights reserved. © 2019 Bloomberg.

Copyright and disclaimer

Coverage.

Clean energy

Advanced transport

Commodities

Digital industry

Bloomberg NEF (BNEF) is a leading provider

of primary research on clean energy,

advanced transport, digital industry,

innovative materials, and commodities.

BNEF’s global team leverages the world’s

most sophisticated data sets to create clear

perspectives and in-depth forecasts that

frame the financial, economic and policy

implications of industry-transforming trends

and technologies.

BNEF research and analysis is accessible via

web and mobile platforms, as well as on the

Bloomberg Terminal.

Client enquiries:

Bloomberg Terminal: press <Help> key twice

Email: [email protected]

Learn more:

about.bnef.com | @BloombergNEF

30 June 11, 2019

Appendix

31 June 11, 2019

Source: BloombergNEF

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1970 1980 1990 2000 2010 2020 2030 2040 2050

Historical world power

generation mix

NEO2018 power generation

mix

Coal

Gas

Oil

Hydro

Nuclear Wind

Solar

Other

48% solar and wind

64% renewables

29% fossil fuels

50% wind and solar generation by 2050

32 June 11, 2019

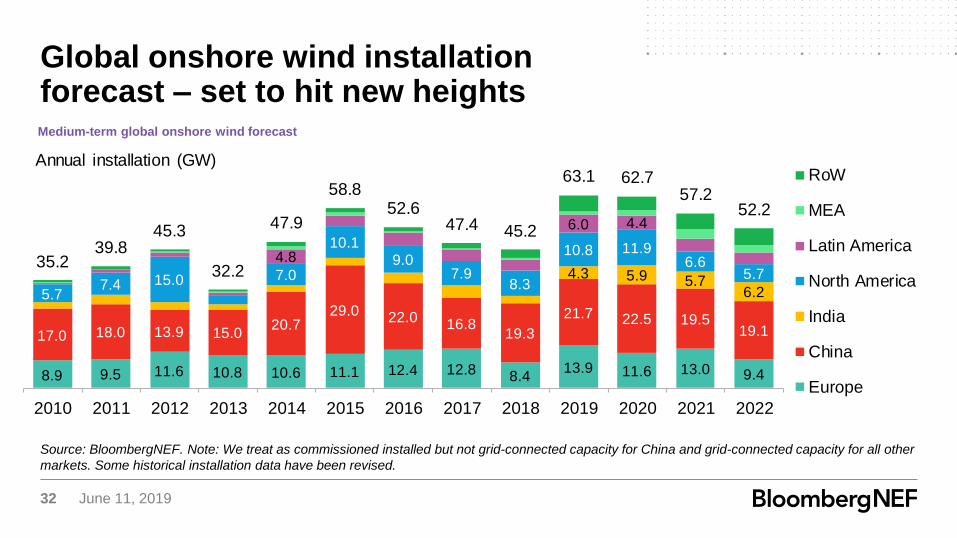

8.9 9.5 11.6 10.8 10.6 11.1 12.4 12.8 8.413.9 11.6 13.0 9.4

17.0 18.0 13.9 15.020.7

29.0 22.0 16.819.3

21.7 22.5 19.519.1

4.3 5.9 5.76.25.7

7.4 15.0 7.0

10.19.0

7.98.3

10.8 11.96.6

5.74.8

6.0 4.4

35.239.8

45.3

32.2

47.9

58.852.6

47.4 45.2

63.1 62.757.2

52.2

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Annual installation (GW)RoW

MEA

Latin America

North America

India

China

Europe

Source: BloombergNEF. Note: We treat as commissioned installed but not grid-connected capacity for China and grid-connected capacity for all other

markets. Some historical installation data have been revised.

Global onshore wind installation forecast – set to hit new heightsMedium-term global onshore wind forecast

33 June 11, 2019

Source: BloombergNEF

Vietnam forecastVietnam installation forecast

30 15

-

89

24 30 39

138

458

300

250 280

-

50

100

150

200

250

300

350

400

450

500

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Annual installation (MW)

Estimate

Announced

Permitted

Financing secured

Commissioned

34 June 11, 2019

Source: BloombergNEF

Getting the admin process right is key (and hard!)

CfD Round 1

Round 3

Round 4

2014 auction

2016 auction

2016 auction 2017 tender

IV

VII & V

II III

Round 1

Round 2

Auction 1

Auction 2

Dumat Al Jandal LCOE bid

2018 auction

0

10

20

30

40

50

60

70

80

90

100

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

$2017/MWh

U.K. South Africa Italy Morocco Turkey

Germany France Greece Saudi Arabia Poland

35 June 11, 2019

Source: BloombergNEF. Note: Only includes onshore wind capacity.

Consolidation has made the turbine market more global

Global onshore turbine manufacturers market share

70%75%

82%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018

Other

Windey

Guodian UP

Nordex

Ming Yang

Enercon

Envision

Siemens Gamesa

GE

Goldwind

Vestas

Top 10

36 June 11, 2019

Source: BloombergNEF.

Smart auctions design can help markets respond