the future of oats - poga.ca · why oat prices have spiked since 2003 • 50% increase in...

TRANSCRIPT

The Future of OatsAg Commodity Research –

Oatinsight.comVancouver, Canada

Quarterly CBOT Oat Prices

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

708090

100110120130140150160170180190200210220230240250260270280290300310320330340350360370380390400410420430440450460470480490500

708090

100110120130140150160170180190200210220230240250260270280290300310320330340350360370380390400410420430440450460470480490500Record high

$4.71 1/2

21 of the last 31 quarters have seen price increases

Why Oat Prices Have Spiked Since 2003

• 50% increase in “Managed Money” oat & corn longs

• US grain use for ethanol use up 435%• Increasing incomes in China and India• Chinese consumption of meat up 50%• Global grain supplies not keeping pace

with consumption• Declining world grain stocks

The Future of Oats

“Just the Oat Facts Ma’am

• Oats are viewed by consumers as one of the healthiest foods

• Rising global food demand for oats• Re-confirmation that oats are beneficial for

equine• Highly concentrated market;

• Production, milling & trade• Bio-Fuel crops threatening oat area• The oat future has challenges……………….

World Crop Production

45%39%

26%

9%4% 2% 1% 1%

0%5%

10%15%20%25%30%35%40%45%50%

% o

f tot

al

Number of Countries Growing a Crop

90

7564 59

4231

20 20 20

0102030405060708090

100

World Oat Area and Production

5,000

15,000

25,000

35,000

45,000

55,000

65,000

62 65 68 71 74 77 80 83 86 89 92 95 98 01 04 07 10

thou

sand

s Production

AreaRecord lows

World Oat Production % of Total

16%

12%

4% 4% 4% 4% 3% 3% 3% 2%

22%

0%

5%

10%

15%

20%

25%%

of t

otal

10 countries account for 78%

Changes in World Oat Area

232%222%

144%

38%5% 1%

-1% -23%-57% -63%-100%

-50%0%

50%100%150%200%250%

1961 to 2009

World Yield Change – 1970s to 2000s

93%83%

50%

35%

18% 16%

0%10%20%30%40%50%60%70%80%90%

100%

Corn Wheat Rye Barley Sorghum Oats

World Oat Production

90% of world production

North American and EU Oat Area

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

thou

sand

N. American

EU-27

EU Oat Area – Top 5 Oat Millers

0

100

200

300

400

500

600

700

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Thou

sand

Hec

tare

s

Germany United Kingdom DenmarkSweden Finland

EU Oat Area – Top 5 Oat Milling Countries

600

800

1,000

1,200

1,400

1,600

1,800

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Thou

sand

Hec

tare

s

Record low

US & Canadian Seeded Oat Area

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Thou

sand

acr

es

US

Canada

Record lows

US & Canadian Harvested Area

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

% h

arve

sted

US

Canada

Record lows

Australia and S. American Oat Area

0200400600800

1,0001,2001,4001,6001,8002,000

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

thou

sand

Australia & Oceania

South American

Oat Trade

Oat Trade Highly Concentrated

• Nine countries account for 80% of the world’s oat trade

• 85% of the Exports• Canada, Sweden, Finland and Australia

• 77% of the Imports• US, Germany, Spain & Mexico

Free Flow of Trade?

• No such thing• EU Import Tariffs• US “Avena sterilis” restrictions• Australian import restrictions• Phytosanitary requirements

World Oat Exports

Oat Exports

1,809

321178 149 58 53 51 43 38 29 27

0200400600800

1,0001,2001,4001,6001,8002,000

000

mt

World Oat Imports

Oat Imports

1,727

20987 86 63 62 52 49 38 35 31

0200400600800

1,0001,2001,4001,6001,8002,000

000

mt

World Oat Import Competition

US

Mexico

South Africa

Ecuador

Canada

Finland

Sweden

Australia

Japan

Oat Product Exporters

• Canada• Mainly to US and Mexico

• EU-27• Mainly internal trade from UK, Germany

and Scans• Australia

• Oceania, Asia and sub continent• US

• Canada, Latin America and Asia• Chile

• Latin America

Oat Product Importers

• Mexico• EU-27

• Mainly internal due to Import Tariffs• South America

• Mainly from Chile• Indian Sub Continent, Asia, South Pacific

• Mainly from Australia and the US

Oat Utilization

World Oat Feed and Food Use

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0

10,000

20,000

30,000

40,000

50,000

60,000

60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05 08

Food

use

Feed

Use

Food Use

Feed useThis is lowering

oat area

World Oat Milling Activity

North America1.5 mmt

EU-270.950 mmt

Chile, Brazil, Ecuador & Argentina

0.125 mmt

0.150 mmt

Approx range of oat product

exports

World Oat Milling Breakdown

Canada 18%

US 36%

Europe 34%

Chile 2%

Australia 5%Others 5%

N. American Breakfast Cereal & Snack Bar Sales

2504506508501,0501,2501,4501,6501,8502,050

1,900

1,910

1,920

1,930

1,940

1,950

1,960

1,970

1,980

Hot

Cere

al, B

B &

GB

–00

0 m

t

Cere

al &

SB

–00

0 m

t

Breakfast cereal/SB

Hot cereal, Breakfast & Granola Bars

W. Europe Breakfast Cereal & Hot Cereal Sales

80

90

100

110

120

130

140

150

800850900950

1,0001,0501,1001,1501,2001,2501,300

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Hot C

erea

l –00

0 m

t

Brea

kfas

t Ce

real

–00

0 m

t

Hot Cereal

Breakfast Cereal

W. Europe Breakfast Cereal Per Capita Consumption

2.12.22.22.32.32.42.42.52.52.62.62.7

Kg p

er h

ead

E. Europe Breakfast Cereal & Hot Cereal Sales

10

20

30

40

50

60

70

80

50

100

150

200

250

300

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Hot c

erea

l –00

0 m

t

Brea

kfas

t Ce

real

–00

0 m

t

Hot Cereal

Breakfast Cereal

E. Europe Breakfast Cereal Per capita Consumption

0.00.10.20.30.40.50.60.70.80.9

Kg p

er h

ead

Latin American Breakfast Cereal & Snack Bar Sales

8090100110120130140150160170180

200250300350400450500550600650700

1998 1999 2001 2002 2003 2004 2005 2006 2007 2008 2009

000

mt

Breakfast cereal/SB

Hot cereal, Breakfast & Granola Bars

China Breakfast Cereal Per Capita Consumption

2.6

4.9

0.03163

0.000

0.005

0.010

0.015

0.020

0.025

0.030

0.035

1.52.02.53.03.54.04.55.05.56.06.5

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Kg/h

ead

Western Europe

North America

China

Largest Oat Food Growth Potential

What Does This All Mean

• Continued divergence of oat production & mill demand

• Oat production could very well slide into “grower contract” status

• Higher feed demand (equine) needed to stem oat supply declines

• All the above could threaten CBOT oat futures contract…… and in turn price discovery

2011/12 Oat Outlook

Canada Oat Stocks to Usage-Ratio

32%

23%

35%

25%

27%

13%

29%

31%

11%

28%

13%

41%

37%

18%

25%

87/8

888

/89

89/9

090

/91

91/9

292

/93

93/9

494

/95

95/9

696

/97

97/9

898

/99

99/0

000

/01

01/0

202

/03

03/0

404

/05

05/0

606

/07

07/0

808

/09

09/1

010

/11F

11/1

2F

Avg 28%

Canadian End Stocks Near Record Low

-

200

400

600

800

1,000

1,200

1,400

1,600

79/8

080

/81

82/8

282

/83

83/8

484

/85

85/8

686

/87

87/8

888

/89

89/9

090

/91

91/9

292

/93

93/9

494

/95

95/9

696

/97

97/9

898

/99

99/0

000

/01

01/0

202

/03

03/0

40/

405

05/0

606

/07

07/0

808

/09

09/1

010

/11F

Avg 1,000

Record High 1,523

345

535

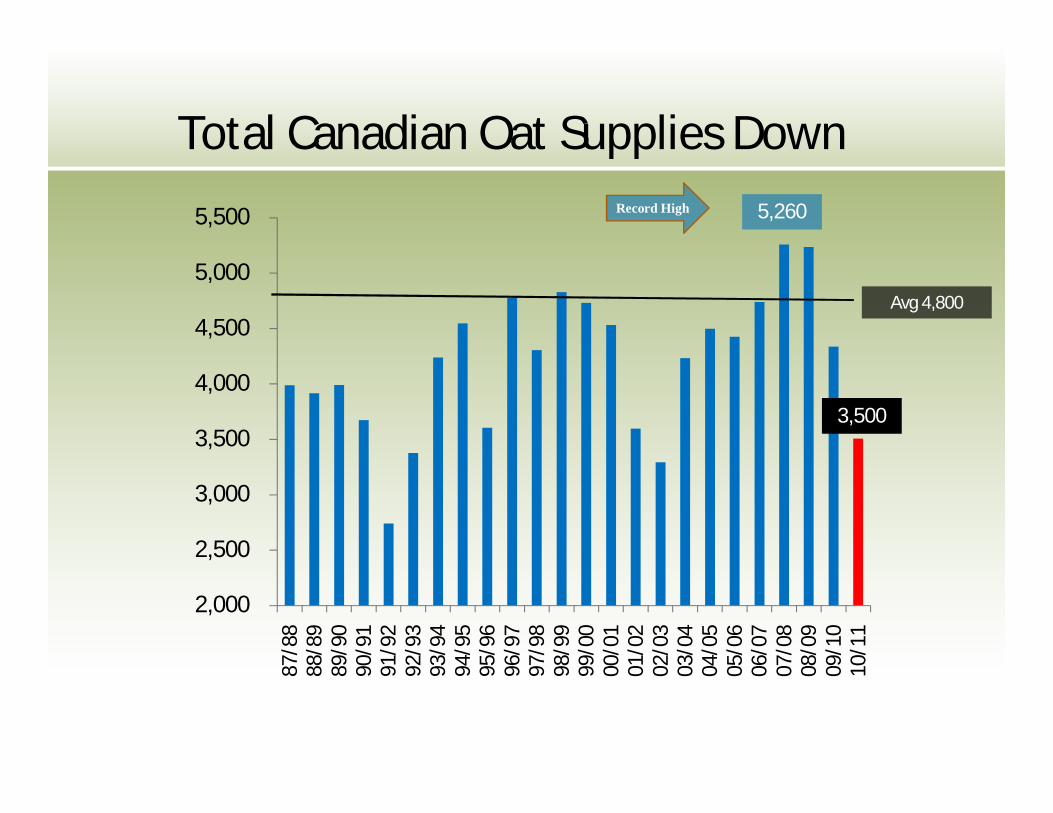

Total Canadian Oat Supplies Down

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

87/8

888

/89

89/9

090

/91

91/9

292

/93

93/9

494

/95

95/9

696

/97

97/9

898

/99

99/0

000

/01

01/0

202

/03

03/0

404

/05

05/0

606

/07

07/0

808

/09

09/1

010

/11

Avg 4,800

Record High

3,500

5,260

Mpls/Duluth Oat Stocks

20,000

22,000

24,000

26,000

28,000

30,000

32,000

34,000

36,000

38,000

Sep/08 Feb/09 Jul/09 Dec/09 May/10 Oct/10 Mar/11

This “Backstop” has a price?

28,865

Net Farm Returns E. Saskatchewan

223 222

173 166

130 129 129 123 12191

$0

$50

$100

$150

$200

$250

Malt Barley

Canola Spring Wheat

Canary Seed

CPS Wheat

Feed Peas

Feed Barley

Flax Oats Large Green Lentils

$CDN

per

acr

e

Net Farm Returns S. Manitoba

232 220 215

179 166136 136 126 125 117

$0

$50

$100

$150

$200

$250

$CDN

per

acr

e

2011 Canadian Oat Production Outlook Scenarios

2010 5 yr avg 2011Seeded acreage changes

000 mt -bu/ac Unchg 5% 10% 15%

Planted 3,737 4,633 3,737 3,924 4,111 4,298Abandonment 67% 75% 75%

Harvested 2,347 3,497 2,803 2,943 3,083 3,223Yield 77.5 71.3 71.3Production 2,798 3,811 3,082 3,236 3,390 3,544Change prod 284 438 592 746

Canadian Oat End Stocks Expected Rise

535

795

-

200

400

600

800

1,000

1,200

1,400

1,600

79/8

080

/81

82/8

282

/83

83/8

484

/85

85/8

686

/87

87/8

888

/89

89/9

090

/91

91/9

292

/93

93/9

494

/95

95/9

696

/97

97/9

898

/99

99/0

000

/01

01/0

202

/03

03/0

40/

405

05/0

606

/07

07/0

808

/09

09/1

0F10

/11F

11/1

2F5

yr a

vg

1.0 mmtAverage

CBOT Continuous Monthly Oats

$0.00$0.50$1.00$1.50$2.00$2.50$3.00$3.50$4.00$4.50$5.00

Mar

/89

Mar

/91

Mar

/93

Mar

/95

Mar

/97

Mar

/99

Mar

/01

Mar

/03

Mar

/05

Mar

/07

Mar

/09

Mar

/11

$3.47

Record High 4.72

Duluth Milling Quality Cash Oat Basis

-$0.80

-$0.60

-$0.40

-$0.20

$0.00

$0.20

$0.40

$0.60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

5 yr avg$.15

Current$.05

Looking Forward

• Increasing food use of oats into 2015• Oat area threaten by Bio-fuel crops• Research funding seriously lagging other

crops• Increasing equine feed use good for milling

• – “push the price envelope”• Removal of EU Tariffs• Removal of “Avena sterilis” in US…….

tolerance?

OatInsight.comThe source for oat information