the furture of semiconductor industry from 'fabless...

TRANSCRIPT

Mar

vell

Con

fiden

tial ©

2007

The

Futu

re o

f Sem

icon

duct

or In

dust

ry fr

om

“Fab

less

”Pe

rspe

ctiv

e

Roa

wen

Che

n, P

h.D

.

GM

and

VP

of C

onne

ctiv

ity B

usin

ess

Uni

t&

VP

of M

anuf

actu

ring

Ope

ratio

ns

Mar

vell

Sem

icon

duct

or

UC

Ber

kele

y S

olid

-Sta

te S

emin

ar

Feb.

1st, 2

008

2M

arve

ll C

onfid

entia

l ©20

07

Out

line

Intro

duct

ion

Fabl

ess

Bus

ines

s M

odel

Ado

ptio

n

Foun

dry

Tech

nolo

gy a

nd In

dust

ry T

rend

Obs

erva

tion

of th

eFu

ture

of S

emic

ondu

ctor

indu

stry

3M

arve

ll C

onfid

entia

l ©20

07

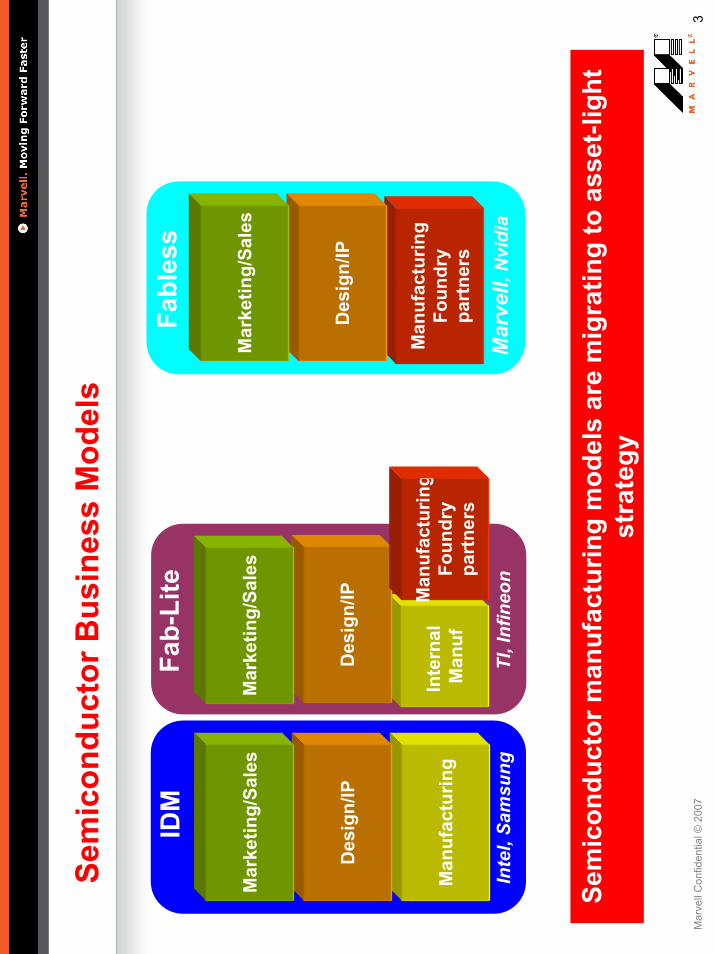

Sem

icon

duct

or B

usin

ess

Mod

els

Man

ufac

turin

gFo

undr

ypa

rtne

rs

Des

ign/

IP

Mar

ketin

g/Sa

les

Fabl

ess

Mar

vell,

Nvi

dia

Man

ufac

turin

g

Des

ign/

IP

Mar

ketin

g/Sa

les

IDM

Inte

l, Sa

msu

ng

Inte

rnal

M

anuf

Des

ign/

IP Man

ufac

turin

gFo

undr

ypa

rtne

rs

Mar

ketin

g/Sa

les

Fab-

Lite

TI, I

nfin

eon

Sem

icon

duct

or m

anuf

actu

ring

mod

els

are

mig

ratin

g to

ass

et-li

ght

stra

tegy

4M

arve

ll C

onfid

entia

l ©20

07

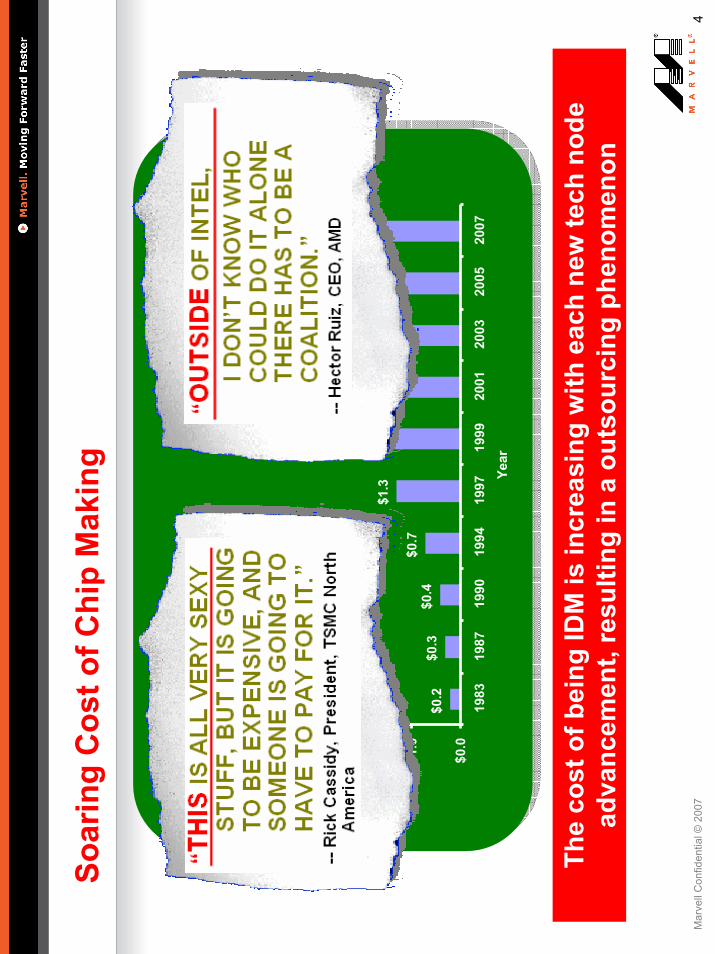

Soar

ing

Cos

t of C

hip

Mak

ing

$0.2

$0.3

$0.4

$0.7

$1.3

$1.8

$3.0

$3.6

$4.3

$5.0

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

1983

1987

1990

1994

1997

1999

2001

2003

2005

2007

Year

FabCost ($B)D

ata

sour

ce:

UM

C

The

cost

of b

eing

IDM

is in

crea

sing

with

eac

h ne

w te

ch n

ode

adva

ncem

ent,

resu

lting

in a

out

sour

cing

phe

nom

enon

5M

arve

ll C

onfid

entia

l ©20

07

Fab

is s

impl

y un

affo

rdab

le b

y ID

M m

odel

2007

Top

20

Sem

icon

duct

or C

ompa

nies

by

Reve

nue

0510152025303540

Intel

Samsung

Toshiba

TI

STMicro

Hynix

Renesas

Sony

NXP

Infineon

AMD

Qualcomm

NEC

Freescale

Micron

Qimonda

Matsushita

Elpida

Broadcom

Sharp

($B)

Dat

a so

urce

: G

oldm

an S

achs

$7B

reve

nue

requ

ired

to s

uppo

rt 30

0mm

Fab

6M

arve

ll C

onfid

entia

l ©20

07

Why

Fab

less

Bus

ines

s M

odel

Attr

activ

e?

Demand

Y200

0

Dem

and

Cyc

les

Y201

0

Util

izat

ion

wor

sens

du

ring

the

dow

n tim

e,

and…

Fab-

Lite

keep

s in

tern

al c

apac

ity

100%

load

ed,

whi

le…

IDM

cap

acity

bu

ilt fo

llow

s th

e de

man

d bu

t…H

ow to

dis

pose

ex

cess

cap

aciti

esw

hen

tech

nolo

gy

mov

es o

n ?

In H

ouse

Cap

acity

Sho

rtage

of

supp

ly d

urin

g bo

om ti

me!

Exce

ss C

apic

ities

Fab-

Lite

com

pani

es

com

plem

ent i

nter

nal c

apac

ity

cons

train

ts w

ith fo

undr

ies,

but…

Flex

ible

Fab

less

Mod

el w

ill P

reva

il !!!

Flex

ible

Fab

less

Mod

el w

ill P

reva

il !!!

7M

arve

ll C

onfid

entia

l ©20

07

Fabl

ess

Sem

icon

duct

or G

row

th

050100

150

200

250

300

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Overall Semiconductor Sales ($B)

0102030405060

Fabless Sales ($B)

over

all s

emic

ondu

ctor

fabl

ess TS

MC

foun

ded

Mar

vell

foun

ded

Fabl

ess

~20%

of

ove

rall

Sem

i

Dat

a so

urce

: EE

Tim

es

8M

arve

ll C

onfid

entia

l ©20

07

Rea

l Men

Sta

rted

to R

ent F

abs

Q1

'07

Ran

kQ

2 '0

7 R

ank

Com

pany

Nam

eQ

1-07

R

venu

e($M

)Q

2-07

R

venu

e($M

)%

of T

otal

11

Inte

l7,

868

7,72

812

.25%

22

Sam

sung

Ele

ctro

nics

4,83

54,

716

7.48

%4

3Te

xas

Inst

rum

ents

2,90

03,

030

4.80

%3

4To

shib

a3,

109

2,51

03.

98%

65

STM

icro

elec

troni

cs2,

276

2,41

83.

83%

86

Ren

esas

Tec

hnol

ogy

1,94

81,

985

3.15

%5

7H

ynix

2,53

91,

963

3.11

%9

8N

XP1,

427

1,47

22.

33%

149

Qua

lcom

m1,

259

1,36

72.

17%

1310

Infin

eon

Tech

nolo

gies

1,28

21,

363

2.16

%Al

l Oth

ers

35,9

7534

,519

54.7

3%To

tal S

emic

ondu

ctor

65,4

1863

,071

100%

Inte

l

Mem

ory

Fab-

lite

Fabl

ess

Dat

a so

urce

: FS

A

Fabl

ess

com

pany

, for

the

first

tim

e, e

nter

sS

emic

ondu

ctor

Top

-10

(Q2

2007

)

9M

arve

ll C

onfid

entia

l ©20

07

Fabl

ess

Com

pani

es: N

o lo

nger

sm

all p

laye

rs

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1000

0

Qualcomm

SanDisk

Nvidia

Broadcom

Marvell

Media Tek

LSI

Xilinx

Avago

Altera

Cirrus Logic

ATI

Sun Micro

Compaq

Level One

ESS

S3

Fab

less

-ers

Revenue($M)

1998

Rev

enue

2007

Rev

enue

Dat

a so

urce

: FS

A

In 1

998,

top

3 fa

bles

sco

mpa

nies

(Alte

ra, Q

ualc

omm

and

Xilin

x)

each

had

~$5

00M

ann

ual r

even

ue; T

oday

in 2

008,

mor

e th

an 1

0 fa

bles

sco

mpa

nies

hav

e ea

ch s

urpa

ssed

$1B

in a

nnua

l rev

enue

10M

arve

ll C

onfid

entia

l ©20

07

Fabl

ess

reve

nue

is m

erel

y ~2

0% o

f Wor

ldw

ide

IC$,

Pot

entia

l G

row

th is

Hug

e

Mem

ory

17.3

%

IDM

Str

ongh

old

IDM

dom

inat

ed

Wire

d C

omm

unic

atio

ns

6.0%

Gra

pc/F

PGA

3.0%

uP/u

CP

16.0

%

Aut

omot

ive

6.4%

Indu

stria

l El

ectr

onic

s 8.

6%

Wire

less

C

omm

unic

atio

ns

19.1

%

Con

sum

er

Elec

tron

ics

19.5

%St

orag

e/Pr

inte

r4.

3%

Fabl

ess

Stro

ngho

ld20

07$2

60 B

illio

n20

0720

07$2

60 B

illio

n$2

60 B

illio

n

Dat

a so

urce

: iS

uppl

i

Fabl

ess

com

pany

gro

ws

from

trad

ition

al tr

ench

, it i

s in

evita

ble

to

inva

de in

to ID

M p

ie. W

irele

ss a

nd C

onsu

mer

ele

ctro

nics

are

two

likel

y ar

eas

11M

arve

ll C

onfid

entia

l ©20

07

Proc

ess

Tech

nolo

gy is

no

long

er D

iffer

entia

tor …

.

Foun

dry

is w

ell i

n pa

ce w

ith

indu

stry

tech

nolo

gy ro

adm

apFo

undr

y is

wel

l in

pace

with

in

dust

ry te

chno

logy

road

map

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7 19

9419

9619

9820

0020

0220

0420

06Ye

ar

Linewidth (um)

ITR

S R

oadm

apFo

undr

y

Dat

a so

urce

: Gar

tner

SiTe

chno

logy

itse

lf no

lo

nger

a k

ey

diffe

rent

iato

r for

IDM

’s

Tech

nolo

gy is

mor

e st

anda

rdiz

ed

Foun

dry

tech

nolo

gy is

th

e de

-fact

or p

roce

ss

choi

ce to

day

for m

ost o

f se

mic

ondu

ctor

co

mpa

nies

Foun

dry

proc

ess

tech

nolo

gy is

the

lead

ing-

edge

.

SiTe

chno

logy

itse

lf no

lo

nger

a k

ey

diffe

rent

iato

r for

IDM

’s

Tech

nolo

gy is

mor

e st

anda

rdiz

ed

Foun

dry

tech

nolo

gy is

th

e de

-fact

or p

roce

ss

choi

ce to

day

for m

ost o

f se

mic

ondu

ctor

co

mpa

nies

Foun

dry

proc

ess

tech

nolo

gy is

the

lead

ing-

edge

.

12M

arve

ll C

onfid

entia

l ©20

07

Foun

dry

Tech

nolo

gy in

Par

with

Indu

stry

Lea

der

TSM

C a

nd In

tel f

eatu

red

2007

IE

DM

with

2 m

ost s

igni

fican

t pa

pers

TSM

CTr

aditi

onal

SiO

2 G

ate

Oxi

de w

/ N

itrid

atio

nIm

mer

sion

Lith

o (1

93nm

w/ 1

.35

Max

NA

)U

ltra

Low

-K (K

=2.5

5)

Inte

lH

igh-

K M

etal

Gat

e (d

ual W

F ga

te

met

al)

Dry

Lith

o (1

93nm

w/ 0

.92

NA

)

Foun

dry

proc

ess

choi

ce is

m

ore

cost

-effe

ctiv

e an

d di

vers

ified

13M

arve

ll C

onfid

entia

l ©20

07

32nm

and

bey

ond?

Waf

er P

rice

(8”

equi

vale

nt)

Tech

nolo

gy N

ode

0.25

µm0.

18µm

0.13

µm90

nm65

nm45

nm

1.25

-1.

35x

each

new

nod

e

Waf

er C

ost

(8”

equi

vale

nt)

Tech

nolo

gy N

ode

0.25

µm0.

18µm

0.13

µm90

nm65

nm45

nm

Cu/

Low

-k

Hig

h-k

Met

al G

ate

imm

ersi

onA

SP o

f Con

sum

er IC

’s

Tech

nolo

gy N

ode

0.25

µm0.

18µm

0.13

µm90

nm65

nm45

nm

Con

sum

ers/

B2B

exp

ect 2

x re

duct

ion

in c

ost p

er fu

nctio

n ea

ch n

ode

Perf

orm

ance

/Po

wer

Tech

nolo

gy N

ode

0.25

µm0.

18µm

0.13

µm90

nm65

nm45

nm

Velo

city

sat

urat

ion,

Mob

ility

deg

rada

tion,

Vd

dsc

alab

ility

, Var

iatio

ns; P

hysi

cs

With

all

thes

e bo

unda

ry c

ondi

tions

, RO

I bey

ond

32nm

m

ay b

e qu

estio

nabl

e

14M

arve

ll C

onfid

entia

l ©20

07

Futu

re T

rend

s of

Sem

icon

duct

or In

dust

ry

Thre

e ty

pes

of S

emic

ondu

ctor

pla

yers

in th

e fu

ture

Inte

lM

emor

yFa

bles

s/Fo

undr

yTS

MC

dom

inan

ce, s

tand

ardi

zatio

n of

CM

OS

proc

ess

offe

rs“D

evic

e sc

alin

g”di

min

ishi

ng a

nd “

dim

ensi

on s

calin

g”sl

ow if

not

sto

pC

onso

lidat

ion

is in

evita

ble,

big

bec

omes

big

ger,

econ

omic

sca

les

win

Inno

vatio

n an

d co

llabo

ratio

n ar

e ou

r hop

es fo

r fut

ure

succ

ess

ofIC

–in

nova

tions

nev

er d

ie. S

ome

pote

ntia

l top

ics

are

Non

-CM

OS

tech

nolo

gies

at m

atur

e pr

oces

s no

de. E

.g.,

Ultr

a-H

V po

wer

de

vice

(ene

rgy

effic

ient

), M

EMS…

.etc

.H

ow to

redu

ce h

igh

mas

k co

st (c

ritic

al fo

r inn

ovat

ive

desi

gns

tofly

)B

reak

thro

ugh

in n

ano-

devi

ces

com

patib

le w

ith c

urre

nt C

MO

S Si

infr

astr

uctu

reTo

p re

sear

ch in

mec

hani

cal/t

herm

al a

spec

ts o

f pac

kagi

ngD

esig

n fo

r Man

ufac

turin

g (D

FM) a

mus

t for

45n

m a

nd b

eyon

d

15M

arve

ll C

onfid

entia

l ©20

07

Sum

mar

y

Fab

cost

s sh

arpl

y in

crea

se d

urin

g th

e la

st d

ecad

e, te

chno

logy

br

ings

onl

y in

crem

enta

l ben

efit

whi

ch m

ay n

ot ju

stify

the

high

fin

anci

al ri

sk o

f ow

ning

fab.

Pro

cess

Tec

hnol

ogy

beco

mes

st

anda

rdiz

ed.

Ana

lysi

s of

the

fabl

ess/

foun

dry

busi

ness

mod

el il

lust

rate

s th

at it

is

the

pref

erre

d m

odel

for c

ompa

nies

to e

xcel

in th

e se

mic

ondu

ctor

in

dust

ry, w

ith th

e hi

ghes

t fle

xibi

lity

to a

ddre

ss d

ynam

ic m

arke

ts

IDM

’sar

e tr

ansi

tioni

ng in

to fa

blite

or fa

bles

sso

mew

here

in b

etw

een

65nm

and

32n

m

As

fabl

ess

beco

mes

mai

nstr

eam

, par

adig

m s

hift

dem

ands

in

nova

tion

and

colla

bora

tion

amon

g su

pply

-cha

ins,

to fu

rthe

r low

er

the

cost

of I

C’s

and

acc

eler

ate

the

grow

th o

f sem

icon

duct

or

indu

stry

16M

arve

ll C

onfid

entia

l ©20

07

Para

digm

Shi

ft

““ Onl

y R

eal M

en h

ave

Onl

y R

eal M

en h

ave

Fabs

Fabs

””Je

rry

Sand

ers

III, C

EO o

f AM

D, c

irca.

199

1Je

rry

Sand

ers

III, C

EO o

f AM

D, c

irca.

199

1

““ Onl

y R

eal M

en G

o O

nly

Rea

l Men

Go

Fabl

ess

Fabl

ess ””

Mar

vell

Con

fiden

tial ©

2007

Than

k Yo

u