the foreclosure crisis the state and federal response

TRANSCRIPT

3/7/2012

1

The Foreclosure Crisis

&

The State and Federal

Response

Fundamental Change in Mortgage

Lending – No UnderwritingWells sues JPMorgan over 800 mortgage loans

Thu, Sep 15 2011

Sept 15 (Reuters) - JPMorgan Chase & Co was sued by Wells Fargo & Co which seeks to force it to buy back more than 800 soured mortgage loans that it oversees as trustee.

In the complaint, Wells Fargo said EMC and its affiliates routinely approved mortgage loans despite "clear defects" in loan applications, including faulty appraisals and inflated borrower incomes.

It also said a forensic review showed that EMC breached representations and warranties on 89 percent of a sample of 948 of mortgage loans.

Market Incentives

“The market is paying me to do a no-income-

verification loan more than it is paying me to

do the full documentation loans.”

– William D. Dallas, Ownit’s founder and CEO• From FHFA Presentation Janet Tavakoli, Tavakoli Structured Finance, Inc.

3/7/2012

2

There are 15 Million Underwater Homeowners

Four million are more than 50% underwater.

The average negative equity is $107,000.

• Source: Equifax, U.S. Gov’t. via Moody’s Analytics From FHFA Presentation Janet Tavakoli, Tavakoli Structured Finance, Inc

Mortgage Servicers’ Work Triples

E.g. Bank of America Home Loan

Servicing

B of A serviced 4 million loans before it bought

Countrywide -

14 million after.

• Presentation Janet Tavakoli, Tavakoli Structured Finance, Inc

3/7/2012

3

The Foreclosure Crisis

ROBOSIGNING

3/7/2012

4

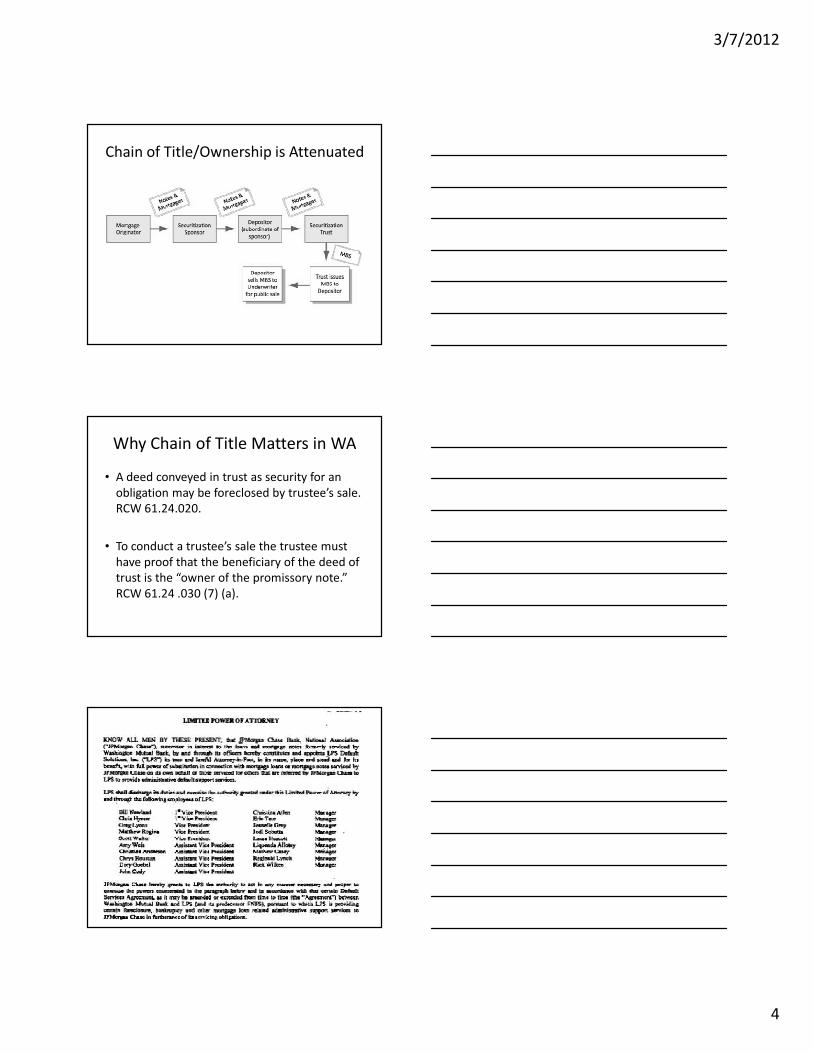

Chain of Title/Ownership is Attenuated

Why Chain of Title Matters in WA

• A deed conveyed in trust as security for an

obligation may be foreclosed by trustee’s sale.

RCW 61.24.020.

• To conduct a trustee’s sale the trustee must

have proof that the beneficiary of the deed of

trust is the “owner of the promissory note.”

RCW 61.24 .030 (7) (a).

3/7/2012

5

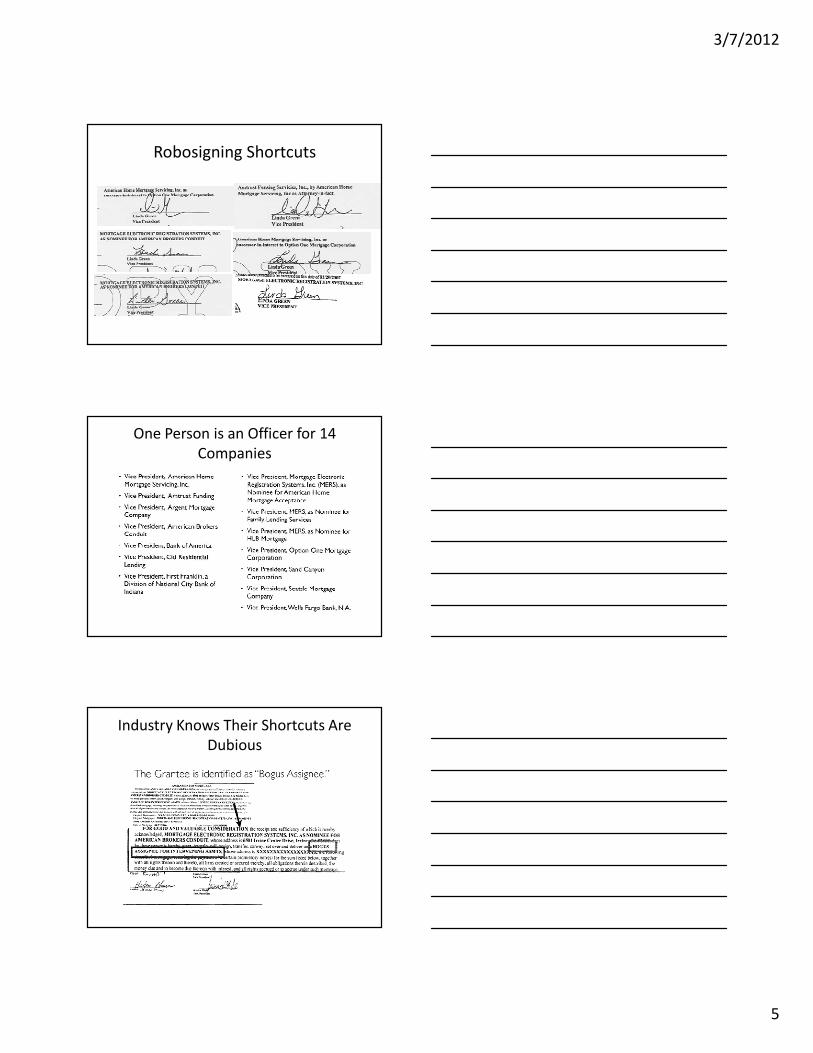

Robosigning Shortcuts

One Person is an Officer for 14

Companies

Industry Knows Their Shortcuts Are

Dubious

3/7/2012

6

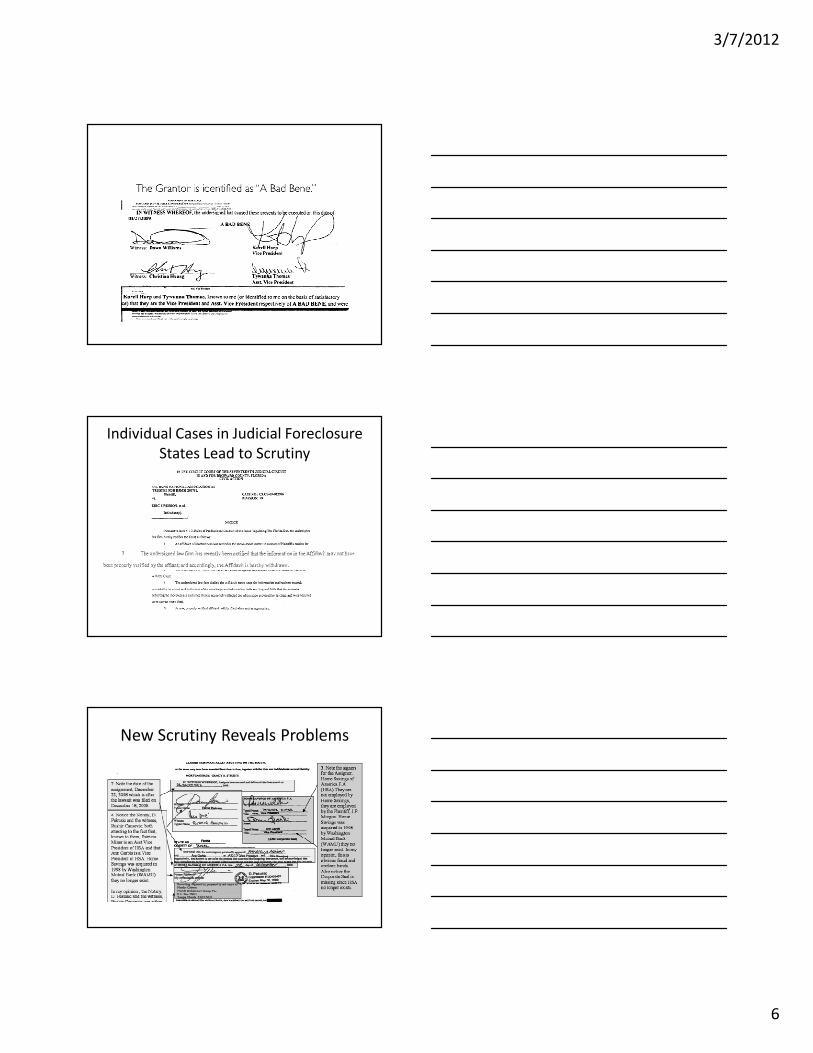

Individual Cases in Judicial Foreclosure

States Lead to Scrutiny

New Scrutiny Reveals Problems

3/7/2012

7

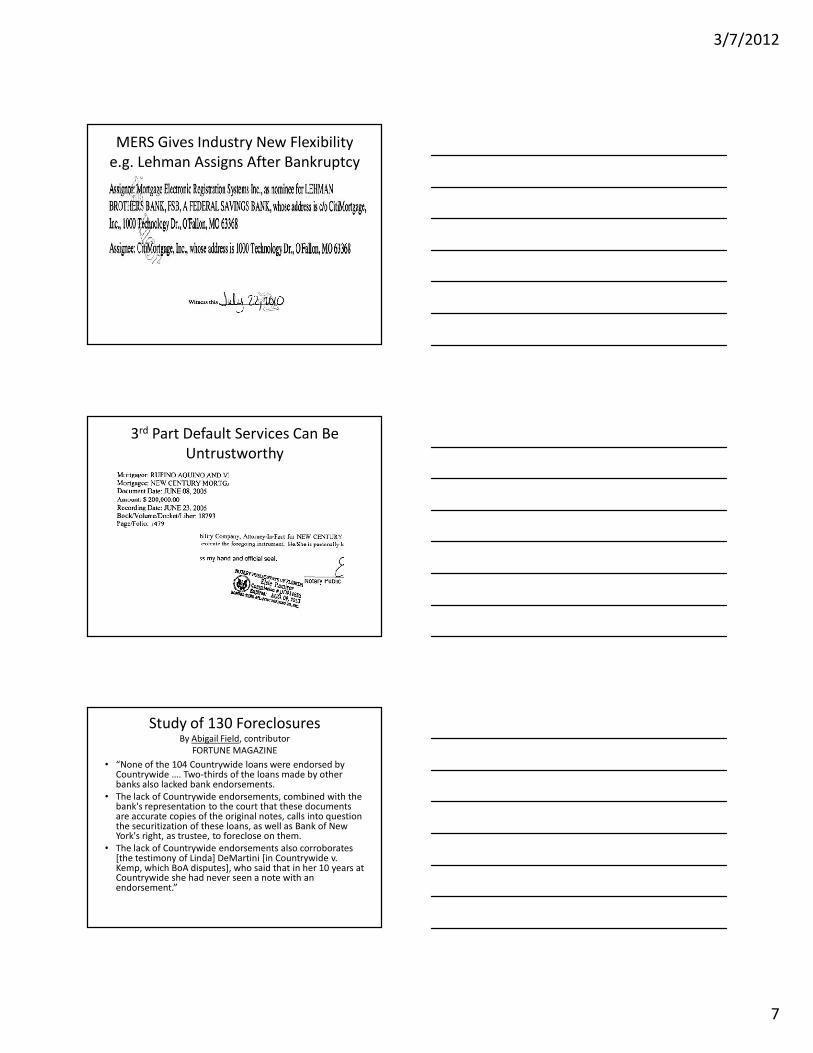

MERS Gives Industry New Flexibility

e.g. Lehman Assigns After Bankruptcy

3rd Part Default Services Can Be

Untrustworthy

Study of 130 ForeclosuresBy Abigail Field, contributor

FORTUNE MAGAZINE

• “None of the 104 Countrywide loans were endorsed by Countrywide …. Two-thirds of the loans made by other banks also lacked bank endorsements.

• The lack of Countrywide endorsements, combined with the bank's representation to the court that these documents are accurate copies of the original notes, calls into question the securitization of these loans, as well as Bank of New York's right, as trustee, to foreclose on them.

• The lack of Countrywide endorsements also corroborates [the testimony of Linda] DeMartini [in Countrywide v. Kemp, which BoA disputes], who said that in her 10 years at Countrywide she had never seen a note with an endorsement.”

3/7/2012

8

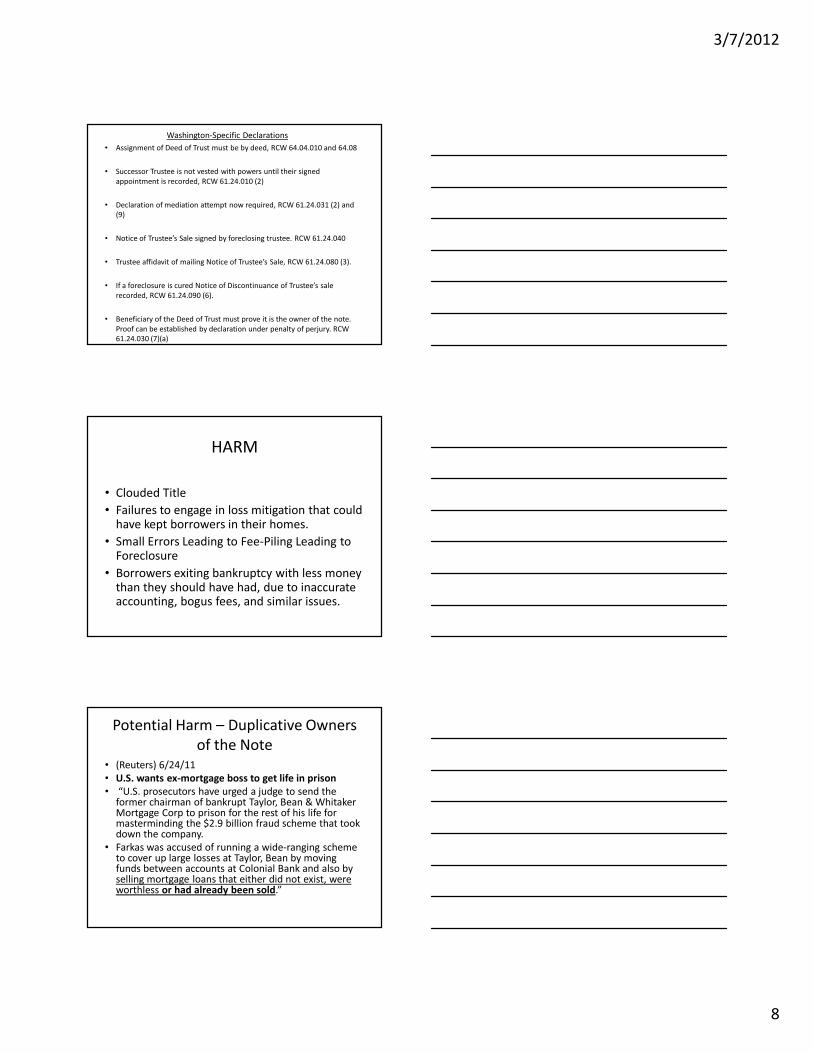

Washington-Specific Declarations

• Assignment of Deed of Trust must be by deed, RCW 64.04.010 and 64.08

• Successor Trustee is not vested with powers until their signed

appointment is recorded, RCW 61.24.010 (2)

• Declaration of mediation attempt now required, RCW 61.24.031 (2) and

(9)

• Notice of Trustee’s Sale signed by foreclosing trustee. RCW 61.24.040

• Trustee affidavit of mailing Notice of Trustee’s Sale, RCW 61.24.080 (3).

• If a foreclosure is cured Notice of Discontinuance of Trustee’s sale

recorded, RCW 61.24.090 (6).

• Beneficiary of the Deed of Trust must prove it is the owner of the note.

Proof can be established by declaration under penalty of perjury. RCW

61.24.030 (7)(a)

HARM

• Clouded Title

• Failures to engage in loss mitigation that could have kept borrowers in their homes.

• Small Errors Leading to Fee-Piling Leading to Foreclosure

• Borrowers exiting bankruptcy with less money than they should have had, due to inaccurate accounting, bogus fees, and similar issues.

Potential Harm – Duplicative Owners

of the Note• (Reuters) 6/24/11

• U.S. wants ex-mortgage boss to get life in prison

• “U.S. prosecutors have urged a judge to send the former chairman of bankrupt Taylor, Bean & Whitaker Mortgage Corp to prison for the rest of his life for masterminding the $2.9 billion fraud scheme that took down the company.

• Farkas was accused of running a wide-ranging scheme to cover up large losses at Taylor, Bean by moving funds between accounts at Colonial Bank and also by selling mortgage loans that either did not exist, were worthless or had already been sold.”

3/7/2012

9

The Foreclosure Crisis

Loan servicing Issues

Major Problems

• Failure to Respond to

Consumer/Attorneys/Counselors

• Failure to engage in loss mitigation efforts

• False statements to courts, foreclosure

authorities, and the United States as insurer

or guarantor (HUD/GSEs/FDIC)

• A federal review of foreclosure claims filed in

bankruptcy courts shows servicers routinely

filing facially deficient claims.

3/7/2012

10

Servicing Errors

Consumer returns the loan modification paperwork

and is told by bank they are approved.

Another part of the bank does not approve it and

does not notify the consumer, refuses to put in

writing what has occurred, allows collection calls

and letters to continue, default fees and costs

accrue, and then the bank forecloses or requires

the consumer to re-qualify for the loan

modification.

Foreclosure Fee Problems

• In re Lafferty, Case No. 11-50918 (Bankr. S.D.

Ohio) (Huntington National Bank): The

servicer filed its first claim claiming

$52,042.58 arrearage. After the debtor

objected, the claim was reduced to $3,156.02.

Other Fee Problems

Servicer charged 44 inspections over 79 months and all

were charged while debtor was making regular

payments.

3/7/2012

11

Modification Confusion

• Consumer was being reviewed for loan

modification and told by her servicer that no

foreclosure sale scheduled – home sold at

foreclosure sale the next day.

• Servicer advises consumer to stop making

monthly payments in order to qualify for a

loan modification.

• Charging late fees while consumer is making timely trial modification payments

• Inaccurate increases in escrow for real property taxes

• Charging for force placed insurance when insurance in place and outrageous fees

• Failure to post payments accurately or in wrong order of payment

• Excessive or unsubstantiated fees including property inspection and maintenance

Court Reaction

3/7/2012

12

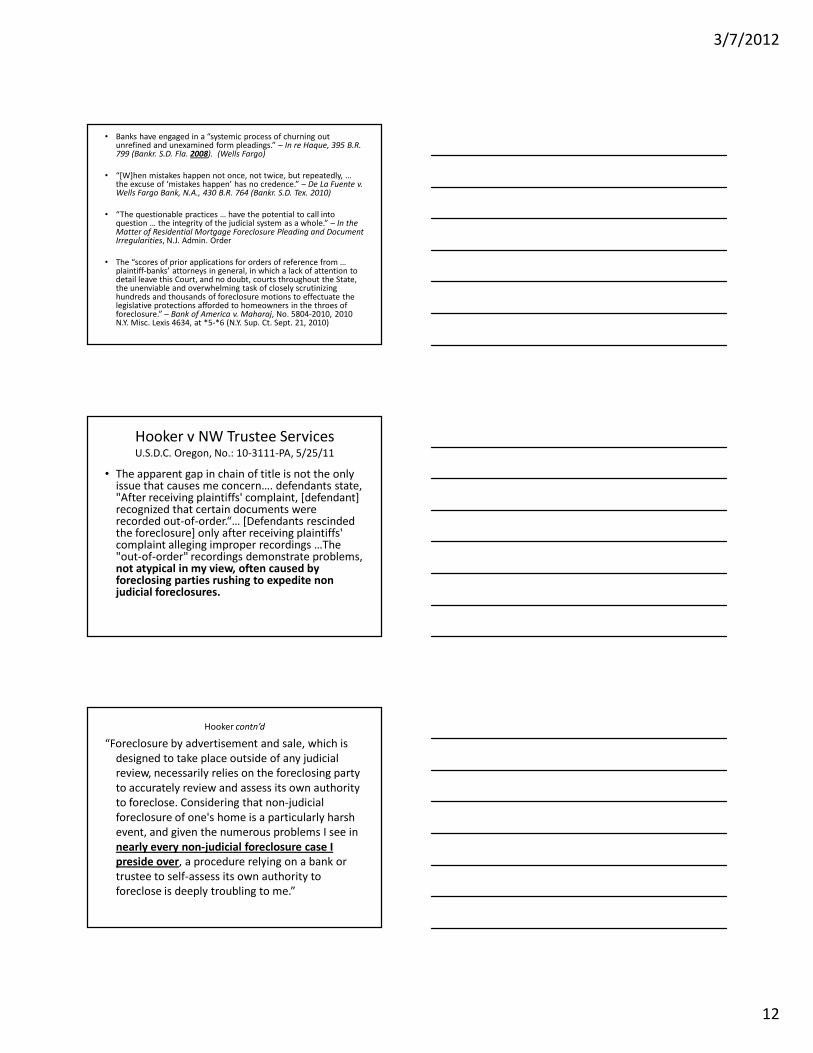

• Banks have engaged in a “systemic process of churning out unrefined and unexamined form pleadings.” – In re Haque, 395 B.R. 799 (Bankr. S.D. Fla. 2008). (Wells Fargo)

• “[W]hen mistakes happen not once, not twice, but repeatedly, … the excuse of ‘mistakes happen’ has no credence.” – De La Fuente v. Wells Fargo Bank, N.A., 430 B.R. 764 (Bankr. S.D. Tex. 2010)

• “The questionable practices … have the potential to call into question … the integrity of the judicial system as a whole.” – In theMatter of Residential Mortgage Foreclosure Pleading and DocumentIrregularities, N.J. Admin. Order

• The “scores of prior applications for orders of reference from … plaintiff-banks’ attorneys in general, in which a lack of attention to detail leave this Court, and no doubt, courts throughout the State, the unenviable and overwhelming task of closely scrutinizing hundreds and thousands of foreclosure motions to effectuate the legislative protections afforded to homeowners in the throes of foreclosure.” – Bank of America v. Maharaj, No. 5804-2010, 2010 N.Y. Misc. Lexis 4634, at *5-*6 (N.Y. Sup. Ct. Sept. 21, 2010)

Hooker v NW Trustee ServicesU.S.D.C. Oregon, No.: 10-3111-PA, 5/25/11

• The apparent gap in chain of title is not the only issue that causes me concern…. defendants state, "After receiving plaintiffs' complaint, [defendant] recognized that certain documents were recorded out-of-order.“… [Defendants rescinded the foreclosure] only after receiving plaintiffs' complaint alleging improper recordings …The "out-of-order" recordings demonstrate problems, not atypical in my view, often caused by foreclosing parties rushing to expedite non judicial foreclosures.

Hooker contn’d

“Foreclosure by advertisement and sale, which is

designed to take place outside of any judicial

review, necessarily relies on the foreclosing party

to accurately review and assess its own authority

to foreclose. Considering that non-judicial

foreclosure of one's home is a particularly harsh

event, and given the numerous problems I see in

nearly every non-judicial foreclosure case I

preside over, a procedure relying on a bank or

trustee to self-assess its own authority to

foreclose is deeply troubling to me.”

3/7/2012

13

•

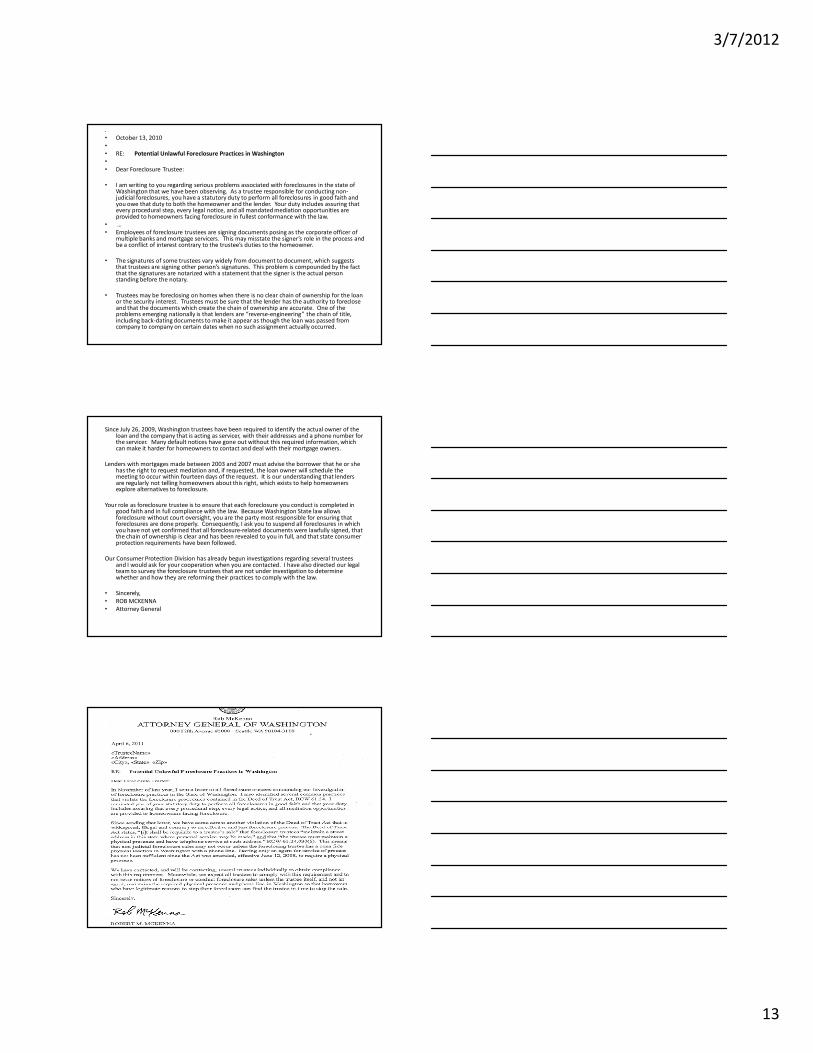

• October 13, 2010

•

• RE: Potential Unlawful Foreclosure Practices in Washington

•

• Dear Foreclosure Trustee:

• I am writing to you regarding serious problems associated with foreclosures in the state of Washington that we have been observing. As a trustee responsible for conducting non-judicial foreclosures, you have a statutory duty to perform all foreclosures in good faith and you owe that duty to both the homeowner and the lender. Your duty includes assuring that every procedural step, every legal notice, and all mandated mediation opportunities are provided to homeowners facing foreclosure in fullest conformance with the law.

• …

• Employees of foreclosure trustees are signing documents posing as the corporate officer of multiple banks and mortgage servicers. This may misstate the signer’s role in the process and be a conflict of interest contrary to the trustee’s duties to the homeowner.

• The signatures of some trustees vary widely from document to document, which suggests that trustees are signing other person’s signatures. This problem is compounded by the fact that the signatures are notarized with a statement that the signer is the actual person standing before the notary.

• Trustees may be foreclosing on homes when there is no clear chain of ownership for the loan or the security interest. Trustees must be sure that the lender has the authority to foreclose and that the documents which create the chain of ownership are accurate. One of the problems emerging nationally is that lenders are “reverse-engineering” the chain of title, including back-dating documents to make it appear as though the loan was passed from company to company on certain dates when no such assignment actually occurred.

Since July 26, 2009, Washington trustees have been required to identify the actual owner of the loan and the company that is acting as servicer, with their addresses and a phone number for the servicer. Many default notices have gone out without this required information, which can make it harder for homeowners to contact and deal with their mortgage owners.

Lenders with mortgages made between 2003 and 2007 must advise the borrower that he or she has the right to request mediation and, if requested, the loan owner will schedule the meeting to occur within fourteen days of the request. It is our understanding that lenders are regularly not telling homeowners about this right, which exists to help homeowners explore alternatives to foreclosure.

Your role as foreclosure trustee is to ensure that each foreclosure you conduct is completed in good faith and in full compliance with the law. Because Washington State law allows foreclosure without court oversight, you are the party most responsible for ensuring that foreclosures are done properly. Consequently, I ask you to suspend all foreclosures in which you have not yet confirmed that all foreclosure-related documents were lawfully signed, that the chain of ownership is clear and has been revealed to you in full, and that state consumer protection requirements have been followed.

Our Consumer Protection Division has already begun investigations regarding several trustees and I would ask for your cooperation when you are contacted. I have also directed our legal team to survey the foreclosure trustees that are not under investigation to determine whether and how they are reforming their practices to comply with the law.

• Sincerely,

• ROB MCKENNA

• Attorney General

3/7/2012

14

Mortgage Debacle Costs Banks $66B

By James Sterngold - Sep 16, 2011

Faulty mortgages and foreclosure abuses have

cost the nation’s five biggest home lenders at

least $65.7 billion, according to a tally by

Bloomberg News, and new claims may push

the industrywide total to twice that amount.

MultiState Investigation

• Washington was 1 of 7 States Investigating and

Negotiating

• Started With 3 Years of Servicing Investigations,

Then 10 Months of Negotiations

• Focused on 5 Banks – Could Be More to Come

• Partnered with State Bank Regulators – including

WA DFI, and US DoJ, HUD and Treasury

– (other actions by OCC, Federal Reserve)

MULTISTATE SETTLEMENT

• $25 Billion in:

–Sanctions

–Homeowner Relief (rough est. $10 b. in principal reduction, $3 b. refi program, $7 b. other loan mod and foreclosure relief)

– Hard Money to States - $5 b.

• Court Ordered Servicing Standards

• Monitor and State Committee (Monitor is

Joseph Smith, former NC Banking Commissioner)

3/7/2012

15

Washington State• $54 million in direct payments to WA:

– About 10% Penalties to General Fund and $5 million for Costs, Fees, Monitoring and Enforcement

– Remaining Distributed by Committee of Legislators and Stakeholders

• Relief to Homeowners Through Bank “Work-Offs”: – Principal Reductions (60%), Loan Modifications, Cash-For-

Keys (still computing – $17 billion nationally, rough est. $483 mill. in WA benefits over 3 years, plus foreclosure payments, Military pay from Feds)

– $3 billion nationally to refi those with negative equity, rough est. $83 mill. for WA, )

• Mandatory Servicing Standards – Enforceable by Several Agencies (not just federal bank regulators)

Misconceptions

• Does NOT Release Banks or Individuals From

Criminal Prosecution, Fair Lending Laws, Other

Regulatory Actions

• Does NOT Waive Homeowners’ Individual

Claims and Defenses

• Does NOT Waive Claims Regarding MERS,

Securitizations, Servicer/Investor Abuse

• Does NOT Allow HAMP Double-counting

Other WA State Actions

• State of Wash. v. ReconTrust Company, (U.S.D.C.

W.Wa. No: 2:11-cv-1460)

• Investigating 17 Foreclosure Trustees

• Law Reform:

– Certified Questions re: MERS in Bain and Selkowitz

– Klem v. Quality Loan Servicing, Div. 1

• Enforcement of the Deed of Trust Act and Mediation Provisions

• Foreclosure Rescue Cases