the european translation industry - facing the future - euatc eeig european economic interest...

TRANSCRIPT

The European Translation IndustryThe European Translation Industry

-- Facing The Future -Facing The Future -

EUATC EEIG

European Economic Interest Grouping

Brussels 2005

Fernand Boucau

Belgian Quality Translation Association

European Union of Associations of Translation Companies

Fernand Boucau

Chairman of BQTA

Belgian Quality Translation Association

Former Chairman and Director of EUATC

European Union of Associations of Translation Companies

Vice-Chairman GET

Guilde Française des Entreprises de Traduction

Chairman of the Telelingua Group

BELGIAN BELGIAN QUALITY TRANSLATION ASSOCIATIONQUALITY TRANSLATION ASSOCIATION

The European Translation Industry

- Facing The Future -

Summary

1. The economic importance of the translation sector. Estimated turnover worldwide and by European country. Forecasts up to 2010. Pages 4 - 22

2. Profile of the translation sector, changes over the last 10 years and problems in the profession. Forecast development by 2010. Pages 23 - 31

3. Conclusions. Pages 32 - 33

1. 1. The economic importance of the translation sector.The economic importance of the translation sector.

- 1999 EC study (based on questionnaires): ‘Evaluation of the economic and social impact of the multilingualism in Europe’, by Bureau Van Dyck Paris.

- Language Translation World Market Assessment’, Allied Business Intelligence, Inc. USA 1999.

- Global Business Confidence Survey Translation’, Common Sense Advisory Inc., USA, 2004.

- Studies by EUATC national Associations: Belgium, UK, Hungary, Spain, Portugal, Germany, Italy, Holland, France, Finland.

1.1. Information sources.

1.2. 1.2. Translation turnover worldwide.Translation turnover worldwide.

1.2.1. Estimates by ‘Common Sense Advisory, Inc.’ USA 2005 in US millions of dollars (copyright).

Annual average growth + 7.5%

Region

% of Total

Market

2005 2006 2007 2008 2009 2010

U.S. 42% 3 696 3 973 4 271 4 592 4 936 5 306

Europe 25

41% 3 608 3 879 4 169 4 482 4 818 5 180

Asia 12% 1 056 1 135 1 220 1 312 1 410 1 516

ROW 5% 440 473 508 547 588 632

Total 100% 8 800 8 987 9 661 10 386 11 165 12 002

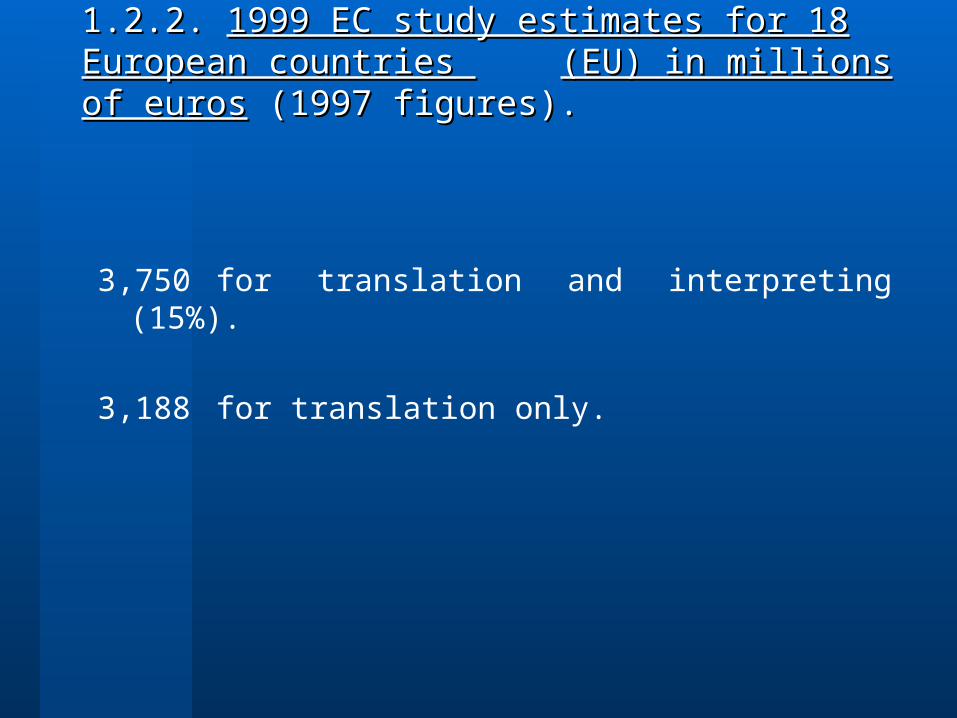

1.1.22..22.. 1999 EC study estimates for 18 European countries 1999 EC study estimates for 18 European countries (EU) in millions of euros(EU) in millions of euros (1997 figures). (1997 figures).

3,750 for translation and interpreting (15%).

3,188 for translation only.

1.2.3. 1.2.3. Estimates and forecasts by ‘Allied Business Estimates and forecasts by ‘Allied Business Intelligence, Inc.’1999. USA, in millions of USD.Intelligence, Inc.’1999. USA, in millions of USD.

Total translation market 1999 2004

worldwide 11,600 16,100

Breakdown of world market 1999 2004

World Global 11,600 16,100

Human Translation 7,600 9,300

Software Localization 3,000 5,200

Website Localization 640 1,162

Machine Translation 324 447

Human Translation 1999 2004World 7,600 9,300Europe (32%) 2,400 3,200Asia 1,800 2,300North America 1,400 1,600Latin America 558 636USSR 472 543Africa 802 825Oceania 162 185

1.2.4. 1.2.4. Conclusions (in millions of euros)Conclusions (in millions of euros)

The translation market worldwide is estimated at:

7,300 in 2005 by ‘Common Sense Advisory, Inc.’

9,500 in 1999 by ‘Allied Business Intelligence, Inc.’

13,200 in 2004 by ‘Allied Business Intelligence, Inc.’ (forecast)

In these figures, Europe is estimated at (millions of euros):In these figures, Europe is estimated at (millions of euros):

2,850 (USD 3,608) by ‘Common Sense Advisory, Inc.’

in 2005.

3,712 (USD 2,400) by ‘Allied Business Intelligence, Inc.’

in 1999.

5,150 in 2004 (forecast by Allied Business Intelligence, Inc.).

3,188 in 1997 by the EC for 18 countries (not including interpreting).

4,777 in 2004 for 18 countries (not including interpreting).

(forecast based on EC report of 1999).

FFirst finding:irst finding:

At a European and a worldwide level, major variations are apparent in the figures in various studies and estimates. This can be explained by the fact that there are no reliable official statistics (with the exception of Belgium and Finland) and we are forced to rely on estimates.

The translation industry is an important economic player at a global level:

- Worldwide, in 2005 it represents a total turnover of 10,250 million euros.This figure is the average from the two USA studies quoted and appears reasonable.

- The translation industry is an essential resource in promoting international communication and globalisation.

- The translation industry has grown rapidly over the past 20 years.

This growth will continue and all the forecasts indicate: average annual growth of 5 to 7.5% between 2005 and 2010.

SecondSecond finding: finding:

The translation industry is a major employer.

- According to the EC: 82,000 jobs in 1997 in the 18 countries plus 17,700 ‘captive jobs’.

2005 forecast, i.e. 8 years later: 110,000 jobs,+ Russia, + 7 countries,+ captive jobs.

- In 1999, a study by ABI (‘Allied Business Intelligence, Inc.’) estimated that there were.43,222 full-time translators in Europe and 79,488 part-time translators.

ThirdThird finding: finding:

In 1999, the ABI estimated that there were 142,580 (full-time) and 261,180 (part-time) translators in the world.

However, these figures do not include IT staff, the many production staff and other specialists employed full time by the translation industry, in particular by translation companies.

In 2005, we can therefore estimate that there are around 250,000 people working in the global translation industry, including 110,000 in Europe (plus Russia + new European countries 25) + captive in-house translators.

According to these estimates, the number of people employed by the translation industry represented approximately €50,000 per job.

1.1.33. The European translation market by country.. The European translation market by country.

The figures include translation and localisation, they do not include interpreting and in-house translators (captive).

Our references are the EC study of 1999 and the market studies and information provided by the national associations of translation companies (EUATC members) in:

Belgium UK

Hungary Spain

Portugal Germany

Italy Holland

France Finland.

1999 EC Report1999 EC Report

Country Turnover in millions of euros

Turnover in %

turnover / inhabitant in euros

turnover / GNP in thousands

Germany 1 050 27.9 12.8 0.56 Austria + Lichtenstein 75 2.0 9.3 0.41 Belgium + Luxembourg 206 5.5 19.4 0.89 Denmark 95 2.5 17.9 0.67 Spain 205 5.5 5.2 0.44 Finland 105 2.8 20.4 1.00 France 575 15.3 9.8 0.47 Greece 35 0.9 3.3 0.32 Ireland 20 0.5 5.4 0.30 Italy 450 12.0 7.8 0.45 Norway + Iceland 95 2.5 20.2 0.73 Netherlands 235 6.4 15.0 0.73 Portugal 85 2.1 19.1 0.95 United Kingdom 290 7.7 4.9 0.26 Sweden 229 6.4 25.8 1.18 Total/average 3,750 100.0 9.9 0.52

1999 EC report1999 EC report

Translation turnover only (excluding interpreting 15%)Translation turnover only (excluding interpreting 15%)

*Forecast including average growth of +/- 5%.

Country Turnover in millions of

euros 1997

Forecast ( +8 years)

in millions of euros 2004*

Germany 892 1,338 Austria + Lichtenstein 64 96

Belgium + Luxembourg 175 262 Denmark 81 121

Spain 174 261 Finland 89 133 France 490 735 Greece 30 45 Ireland 17 24 Italy 381 571

Norway + Iceland 81 121 Netherlands 200 300

Portugal, 72 108 United Kingdom 247 370

Sweden 195 292 Total 3,188 4,777

Belgian translation market (code NACE-BEL74 832)Belgian translation market (code NACE-BEL74 832)Turnover in millions of Turnover in millions of €€ (not incl (not incl.. interpreting) based on VAT interpreting) based on VAT

declarationsdeclarations INS (Institut National de Statistique)INS (Institut National de Statistique)

Source: BQTA

Belgian Quality Translation Association

1995 81,295 100%

1996 93,475

1997 105,519

1998 124,088

1999 126,019

2000 134,231

2001 140,513 173%

2002 144,625 181%

2003 152,875 197%

2004 169,833 202%

Comparison of forecast turnover in 2004 (millions ofComparison of forecast turnover in 2004 (millions of.. €€) from the ) from the EC study with estimated figures based on studies by national EC study with estimated figures based on studies by national

associations of translation companies that are members of EUATC associations of translation companies that are members of EUATC (non-captive market and not including interpreting)(non-captive market and not including interpreting)

Country EC Nat. association of translation companies

Belgium 262,000Incl. European Institutions

169,833Not incl. European Institutions

BQTA

UK 370,000 300,000 to 480,000 ATC

France 735,000 300,000 to 500,000 CNET

Germany 1,338,000 500,000 to 700,000 QSD

Hungary - 28,000 MFE

Portugal 108,000 91,000 APET

Spain 261,000 247,000 ACT

Italy 571,000 676,000 Federcentri SEB

Holland 300,000 115,000 ATA (EIM)

Finland 133,000 61,166 SKTOL

22.. Profile of the translation sector.Profile of the translation sector.

Changes over the last 10 years.Changes over the last 10 years.

Problems in the profession.Problems in the profession.

Forecast development by 2010.Forecast development by 2010.

2.1. Profile, characteristics 2.1. Profile, characteristics && development of the translation sector. development of the translation sector.

2.1.1. The translation industry is one of the most fragmented service sectors in the world.

There are 100,000 freelance translators in Europe and over 200,000 in the world.

2.1.2.The last 25 years has seen, in parallel to freelancers, the emergence and rapid growth of multilingual translation companies, whose share of the worldwide translation market already accounts for 20%, a figure that will gradually increase to 50% (increase in the number of languages for each project).

There are an estimated (EUATC base = 400 companies) 1,500 translation companies in Europe and 3,000 worldwide. Their average turnover is in the region of 300,000 € per company, i.e. a worldwide turnover of close to 1,000 million €, plus 1 billion €, i.e. the turnover of the 15 biggest translation companies in the world.(Source: ‘Common Sense Advisory, Inc.’).

In other words, a total of 2 billion € for translation companies throughout the world (total market 10 billion €).

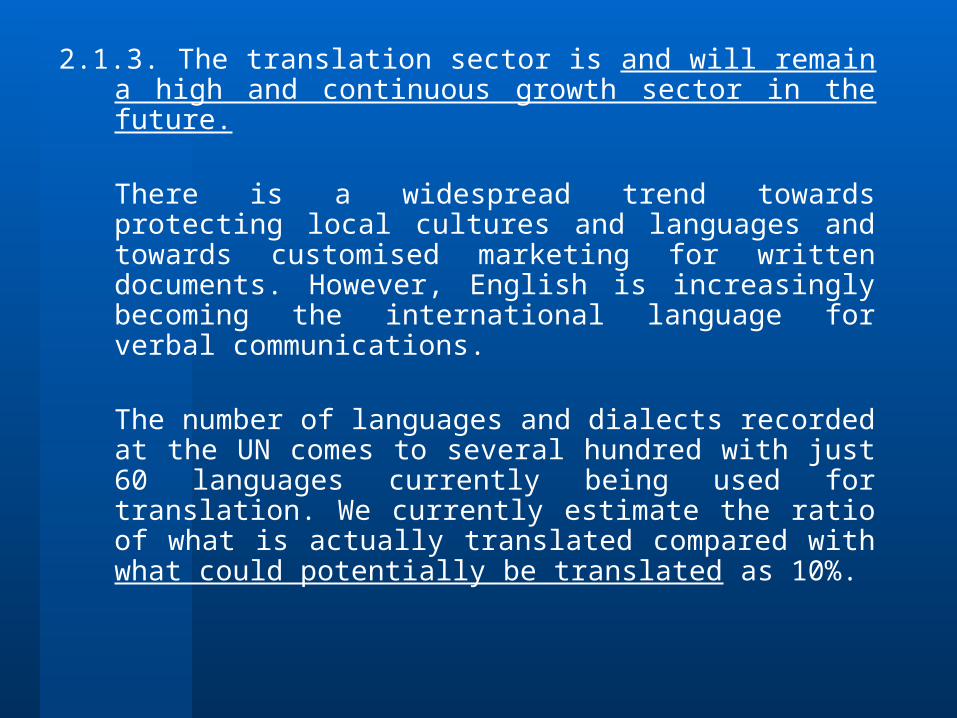

2.1.3. The translation sector is and will remain a high and continuous growth sector in the future.

There is a widespread trend towards protecting local cultures and languages and towards customised marketing for written documents. However, English is increasingly becoming the international language for verbal communications.

The number of languages and dialects recorded at the UN comes to several hundred with just 60 languages currently being used for translation. We currently estimate the ratio of what is actually translated compared with what could potentially be translated as 10%.

2.1.4. The translation sector offers jobs with high levels of knowledge and training (linguistic and technological mix).

2.1.5. The last 5 years have seen intense competition between translation companies, with significant and continuous erosion of margins.

Companies and groups of independent translators sometimes sell at a loss and often at cost price (Internet).

This situation threatens companies’ profitability and quality as well as placing pressure on the sales prices of the freelancers who work with the translation companies.

2.1.6. The image of translation is not positive, it is viewed as

a commodity.

Price takes precedence over quality.

Companies do not view translation as a strategic element, they do not understand the full complexity of the process.

Companies use translation as an expensive method of communication rather than an investment.

2.1.7. The development of production tools (translation memories, terminological management and project management software) is a technical characteristic of the sector and this trend will increase.

2.1.8. The translation sector is unorganised and there is

no unity.

There is no ongoing and structured contact between the FIT (organisation for freelance translators) and EUATC (European association of translation companies). However, they share many common objectives and interests. This ‘unorganised’ aspect has a very negative effect on the image of the translation sector.

2.1.9. Consolidation in the translation market through acquisitions of translation companies has been a major development over the past 10 years. The market is experiencing a period of great upheaval.

Lionsbridge’s acquisition of Bowne brings the group's total turnover to 340 million euros (i.e. 3.4% of the total global market).The combined turnover of the 15 biggest translation companies in the world is somewhere around 1,000 million euros, representing 10% of the world market and 50% of the market for translation companies.

The structure of the global translation market therefore resembles a pyramid with rapidly changing segments. The consequences of this situation are already becoming apparent.

2.1.10. Translation is an industry where customers demand quality. With the exception of the EN(CEN)standard due to be introduced in 2006, there is no specific quality standard for the translation industry.

The new EN(CEN) standard is a step in the right direction.ISO is a general procedure that can be applied to all industries and all sectors and is therefore useful in encouraging the translation sector – driven by EUATC – to introduce specific EN(CEN)standards.

However, ISO also intends to develop a new ISO standard specifically for translation. We must hope that the ISO project considers the basic EN(CEN)standard to avoid duplicating standards throughout the world.

EUATC must work with ISO and gain acceptance for the EN(CEN)standard as one of the foundations for discussion of the new ISO project.

---------------------------------------------------------------------------

200,000 freelance translators

8,000 million.euros directly

80% of the worldwide market

(trend < )

3,000 translationcompanies

2,000 million.€ 20% of the worldwide

Market (trend > )

EstimateEstimate - - Worldwide translation market (10,000 million Worldwide translation market (10,000 million €€))

Estimated breakdown of the 20% share of the worldwide market, Estimated breakdown of the 20% share of the worldwide market, i.e. 2,000 million i.e. 2,000 million €€ between translation companies between translation companies

Worldwide market for translation companies: 2,000 million €. 20 companies account for 1,000 million €100 companies account for 500 million € (average 5 million €)2,880 companies account for 500 million € (average 174,000 €)

----------------------------------------------------- 500 million.euros

2,880 translation companies

1 000 million €20

translation companies -----------------------------------

500 million.euros100 translation companies

2.2. 2.2. Problems in the translation sector.Problems in the translation sector.

2.2.1.The constant increase in the number of translation companies is resulting in a situation where supply continuously exceeds demand.

Consequences: erosion of margins, risks in terms of quality, unfair competition by the Internet.

This is an unhealthy situation and is abnormal because the translation sector is not yet ‘mature’.

Anyone can set up a translation company.

2.2.2.There is no unity in the translation sector.

There is no ongoing and structured contact at the highest level between FIT and EUATC.

However, these two organisations have many common interests to defend.

2.2.3. The image of translation is not positive.

Companies view it as a cost rather than an investment.

Translation is not regarded as strategic by companies.

Its image has become that of a ‘commodity’.

The customer considers the price before quality and technology.

Translation users do not understand the complexity of the process.

2.2.4. The first specific translation quality standard will not come into force until 2006 (CEN standard).

It is a step in the right direction, but not enough.

2.2.5. Lack of official statistics for the translation sector.

We are reduced to estimates, despite the fact that this is an essential sector for Europe and for communication in a globalised world.

2.2.6. Translation companies do not have enough knowledge of or pay sufficient attention to their profitability.

The vast majority of translation companies have low profits and make do with this situation. This is dangerous for their future and for the sector.

In-depth management of supply and the definition of an ‘average minimum gross margin’ are essential objectives to be set each year.

The only way to ensure survival is through a healthy and prosperous financial situation. Companies must learn to say no to customers who demand discount prices.

33. . Conclusions.Conclusions.3.1. EUATC is asking the European Commission to propose and obtain

approval from the Council of Ministers for an official statistics programme for the translation sector in the 25 countries of the Union.

The sector plays a major role in promoting the unity and economic development of the Community, in particular through exports.

3.2. We must educate customers; to help them understand the complex

process involved in producing a high-quality translation; and also to view translation as an investment and not just a cost. Contacts are to be taken with translation companies associations in USA, Canada, with FIT, with organizations like LISA and GALA, in order to create and finance a common action plan.

3.3. We need to educate translation companies.

With regard to an appropriate level of profitability to ensure their survival: managing margins to cover actual costs, refusing to discount prices and sell at a loss.

We need to implement entry barriers for new translation companies: skill, quality standards, effective financial management. Action plan to be defined.

In a recent article, John Freivalds (Multilingual Computing and Technology) wrote: “World trade depends on what the industry does. Content needs to be translated as well as localized to facilitate the movement of goods and services. The value of these services far exceeds what the size of the industry is perceived to be. And it is the message that we need to keep in front of the marketplace.”

3.4. The image of the sector must be improved by creating unity in the translation sector. FIT and EUATC must establish ongoing contact structures at the highest level. FIT and EUATC are in the same boat and share many common interests.

3.5.The first EN – CEN European standard specifically for

the translation industry will come into effect in 2006. We need to play an active role in the drawing up of the future ISO standard for the translation sector.

3.6.Translation assistance technologies are expected to

develop in terms of reducing costs, in particular for major multilingual projects, thanks to new and more effective software. This is what we hope with regard to SDL which has taken over Trados.

3.7. Large companies in the sector are being created through external growth, i.e. through acquisitions.

The consequences of this significant consolidation are:

Today:

1. The major companies have a high production capacity that the others cannot match and therefore

monopolise big projects.

2. Many customers do not like having just one supplier, which means that the big consolidated companies must expect to lose some of their customers to the medium-sized or smaller companies.

In the future:

1. This consolidation may stabilise and improveprices, which in general are currently at the

same levels as 1995. Pressure on margins may slow down, in the interests of the companies and freelance translators.

2. This consolidation will increase.

3. We can expect a more extensive range of services from the big companies.

***********************