the eiti process · pdf filethe eiti process 1: establish objectives and work plan 2:...

TRANSCRIPT

THE EITI PROCESS1: Establish objectives and work plan

2: Preliminary or updated scoping

3: Agree TOR for Independent Administrator

4: Appointment of Independent Administrator

5: Confirmation of reporting procedure

6: Data collection, verification, reconciliation

7: Review of draft EITI report

8: Approval and publication of final EITI report

9: Dissemination and promoting public debate

10: Validation

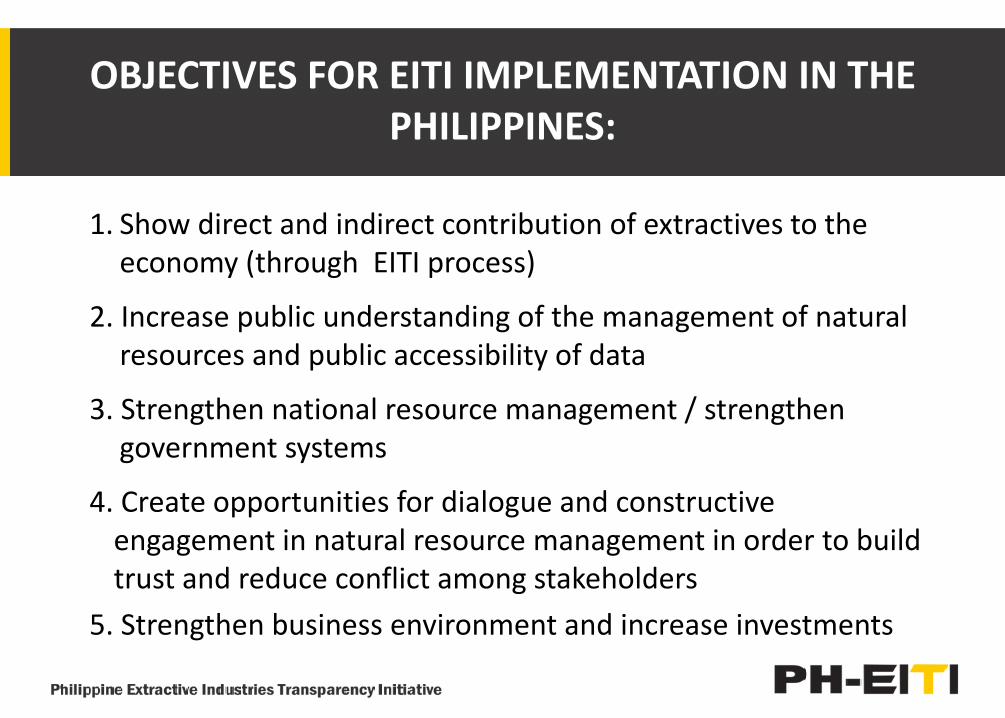

OBJECTIVES FOR EITI IMPLEMENTATION IN THE PHILIPPINES:

1. Show direct and indirect contribution of extractives to the economy (through EITI process)

2. Increase public understanding of the management of natural resources and public accessibility of data

3. Strengthen national resource management / strengthen government systems

4. Create opportunities for dialogue and constructive engagement in natural resource management in order to build trust and reduce conflict among stakeholders

5. Strengthen business environment and increase investments

EITI IMPLEMENTATION IN THE PHILIPPINES

1. ADMISSION AS A CANDIDATE COUNTRY: MAY 22, 2013

2. FORMATION OF A MULTI-STAKEHOLDER GROUP AND REGULAR MEETINGS/CONSULTATIONS

3. FORMULATION OF OBJECTIVES FOR EITI IMPLEMENTATION

4. ISSUANCE OF EXECUTIVE ORDER NO. 147

5. SUBMISSION OF COUNTRY WORK PLAN TO THE EITI BOARD

6. EXECUTION OF BIR WAIVER

7. DATA GATHERING AND RECONCILIATION

8. OUTREACH ACTIVITIES (ARMM, TEMPLATE WORKSHOP WITH LGU’s)

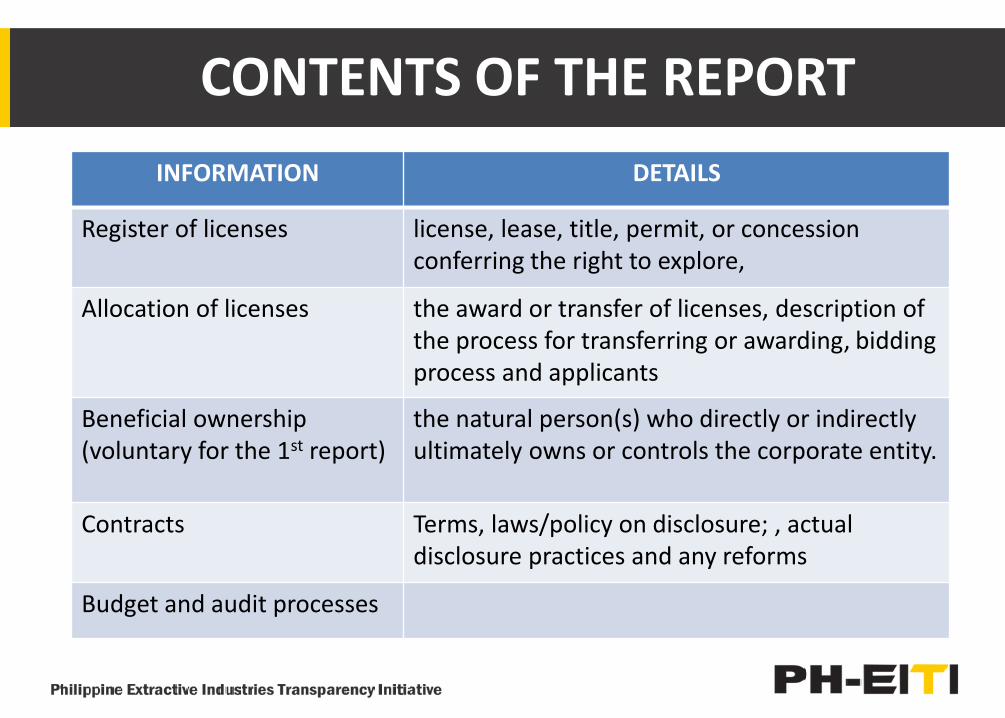

CONTENTS OF THE REPORT

A. CONTEXTUAL INFORMATION

B. REVENUE STREAMS

C. ADDITIONAL INFORMATION AS DETERMINED BY THE MSG

D. IDENTIFICATION OF DISCREPANCIES (IF ANY)

E. RECONCILIATION OF DATA/EXPLANATION FOR DISCREPANCIES

F. RECOMMENDATIONS AND OBSERVATIONS OF THE INDEPENDENT ADMINISTRATOR

EITI STANDARD

EITI REQUIREMENT 3

The EITI requires EITI Reports that includecontextual information about the extractiveindustries.

CONTENTS OF THE REPORT

A. CONTEXTUAL INFORMATION

INFORMATION DETAILS

Legal framework and fiscal regime governing the extractive industries.

the fiscal regime overview of the relevant laws and regulations, roles and responsibilities of the relevant government agencies.

Overview of the extractive industries, including any significant exploration activities.

Size of the extractive industries , estimate of informal sector activity. Total government revenues in absolute terms and as a percentage of total government revenues, exports, employment, key regions of production

Information about the contribution of the extractive industries to the economy for the fiscal year covered by the EITI Report.

CONTENTS OF THE REPORT

INFORMATION DETAILS

Production data for the fiscal year covered by the EITI Report,

Total production volumes and the value of production by commodity, and, when relevant, by state/region; Total export volumes and the value of exports by commodity, and, when relevant, by state/region of origin.

State participation in the extractive industries

prevailing rules and practices regarding the financial relationship between the government and state owned enterprises (SOEs), quasi-fiscal expenditures , government’s level of beneficial ownership, loans granted to mining companies

Distribution of revenues from the extractive industries.

which extractive industry revenues, whether cash or in-kind, are recorded in the national budget or their allocation

Further information on revenue management and expenditures in the EITI Report

description of any extractive revenues earmarked for specific programmes or geographic regions; description of the methods for ensuring accountability and efficiency in their use; description of the country’s budget and audit processes

CONTENTS OF THE REPORT

INFORMATION DETAILS

Register of licenses license, lease, title, permit, or concession conferring the right to explore,

Allocation of licenses the award or transfer of licenses, description of the process for transferring or awarding, bidding process and applicants

Beneficial ownership (voluntary for the 1st report)

the natural person(s) who directly or indirectly ultimately owns or controls the corporate entity.

Contracts Terms, laws/policy on disclosure; , actual disclosure practices and any reforms

Budget and audit processes

EITI STANDARD

EITI Requirement 4:

The EITI requires the production of comprehensiveEITI Reports that include full government disclosureof extractive industry revenues and disclosure of allmaterial payments to government by oil, gas andmining companies.

CONTENTS OF THE REPORT

B. REVENUE STREAMS

A description of each revenue stream, relatedmateriality definitions and thresholds should beincluded in the EITI Report, as well as optionsconsidered and the rationale for establishing thedefinitions and thresholds.

CONTENTS OF THE REPORT

B. REVENUE STREAMS

• the host government’s production entitlement (governmentshare);

• national state-owned company production entitlement (share ofPMDC and PNOC);

• taxes

• Royalties (IP royalties, royalties in mineral reservations);

• Dividends (for GOCCs) ;

• bonuses, such as signature, discovery and production bonuses(for oil explorations as stated in service contracts);

CONTENTS OF THE REPORT

• licence fees, rental fees, entry fees and other considerations forlicences and/or concessions; (occupation fees)

• Social expenditures (SDMP, AEPEP, CDP, MRF, RCF,CLRF, voluntaryCSR, MMTF, FMRDF)

• Transportation (wharfage fees)

• Subnational payments (business tax, RPT, mayor’s permit,occupation fees, local wharfage fees, toll fees, extraction fees,local fees and taxes,

• Subnational transfers share of LGUs in national wealth

• Other material payments: BOC payments e.g. customs duties,VAT on imported materials

ADDITIONAL INFORMATION (as decided by the MSG)

1. Incentives regime

2. Special Funds (PD 910)

3. Country’s mineral potential

4. Reconciliation of export data

ADDITIONAL INFORMATION (as decided by the MSG)

5. Additional contextual information:

• Company profile (including information on MOA with IPs)

• Employment (nature of employment, gender, IP)

• Gross Production/Tonnage

• Pricing

• Suppliers/contractors

• Additional information for SDMP (planned vs spent, operating cost, partner organizations)

CONTENTS OF THE REPORT

C. IDENTIFICATION OF DISCREPANCIES/ RECONCILIATION OF DATA

EITI Requirement 5.3: the IndependentAdministrator should prepare an EITI Report thatcomprehensively reconciles the informationdisclosed by the reporting entities, identifying anydiscrepancies.

CONTENTS OF THE REPORT

D. RECOMMENDATIONS and OBSERVATIONS OF THE IA:

1. Examination of audit and assurance procedures

2. Assessment on comprehensiveness and reliability of data

3. Gaps and weaknesses in the reporting procedure (companies and agencies who failed to comply and impact on comprehensiveness)

CONTENTS OF THE REPORT

4. Documentation of auditing of financial statements of reporting entities

5. Recommendations for strengthening the reporting process (e.g. auditing process, compliance with international standards)

THE PHILIPPINE EITI REPORT

YEAR COVERED: 2012

DEADLINE: DECEMBER 2014

LEVEL OF DETAIL:Per revenue stream, per company, per commodity, per project

REPORTING COMPANIES: 39 LARGE SCALE METALLIC MINING COMPANIES; 11 OIL AND GAS COMPANIES1 COAL company1 additional mining company in ARMM

THE PHILIPPINE EITI REPORT

WHO SHOULD REPORT?

A. Contextual Information: PSA, BOI, DOLE, MGB, DOE, PNOC, PMDC, DBM, BLGF, COA, COMPANIES

B. Revenue streams: MGB, DOE, BIR, LGU, BLGF, PPA, BOC, NCIP, COMPANIES

C. State-owned Enterprises (GOCC): PMDC, PNOC

REPORTING COMPANIES

A.MINING

1. Apex Mining Company, Inc.

2. Benguet Nickel Mines, Inc. (Benguet Corporation)

3. Berong Nickel Corporation

4. Cagdianao Mining Corporation

5. Carmen Copper Corporation (Atlas Consolidated Mining and Development Corporation)

6. Citinickel Mines and Development Corporation

7. CTP Construction and Mining Corporation

8. Eramen Minerals, Inc.

9. Filminera Resources Corporation

10. Hinatuan Mining Corporation

A.MINING

11. Lepanto Consolidated Mining Company

12. LNL Archipelago Minerals Incorporated

13. Mt. Sinai Mining Exploration and Development Corporation

14. Oceana Gold (Philippines), Inc.

15. Philex Mining Corporation

16. Philsaga Mining Corporation

17. Platinum Group Metals Corporation

18. Rapu-Rapu Minerals, Inc.

19. Rio Tuba Nickel Mining Corporation

20. SR Metals, Incorporated

REPORTING COMPANIES

A.MINING

21. Taganito Mining Corporation

22. TVI Resource Development

23. Zambales Diversified Metals Corporation

24. Adnama Mining Resources Incorporated

25. Cambayas Mining Corporation

26. Carrascal Nickel Corporation

27. Greenstone Resources Corporation

28. Johson Gold Mining Corporation

29. Krominco, Inc.

30. Leyte Iron Sand Corporation

REPORTING COMPANIES

REPORTING COMPANIES

A.MINING

31. Marcventures Mining and Development

32. Ore Asia Mining and Development Corporation

33. Oriental Synergy Mining Corporation

34. Philippine Mining Development Corporation (PMDC)

35. AAM-PHIL Natural Resources Exploration and Development Corporation

36. Shenzhou Mining Group Corporation

37. Shuley Mine Incorporated

38. Pacific Nickel Philippines, Inc.

39. Sino Steel Phils. H.Y. Mining Corporation

Note: Coal and Additional mining company in ARMM for engagement

REPORTING COMPANIES

B. OIL AND GAS

1. Shell Philippines Exploration B.V (SPEX)

2. Chevron Malampaya LLC

3. Philippine National Oil Company (PNOC) - Exploration Corporation

4. The Philodrill Corporation

5. Oriental Petroleum & Minerals Corporation

6. Nido Petroleum Phils. Pty. Ltd.

7. Alcorn Gold Resources Corporation

8. Trans Asia Oil & Energy Development Corporation

9. Galoc Production Company

10. Forum Energy Philippines Corporation

11. Forum Pacific Incorporated

REPORTING COMPANIES

C. STATE OWNED ENTERPRISES (GOCC):

1.Philippine Mining Development Company (PMDC)

2.Philippine National Oil Company (PNOC)

WHAT DO EITI REPORTS TELL US?

1. How much are we getting fromextractive industries?

Taxes,Timor Leste

EITI Requirement 4.1.b

Source: EITI INTERNATIONAL

SECRETARIAT. (2014). Establishing the scope

of the EITI Report [Presentation]. Port

Moresby.

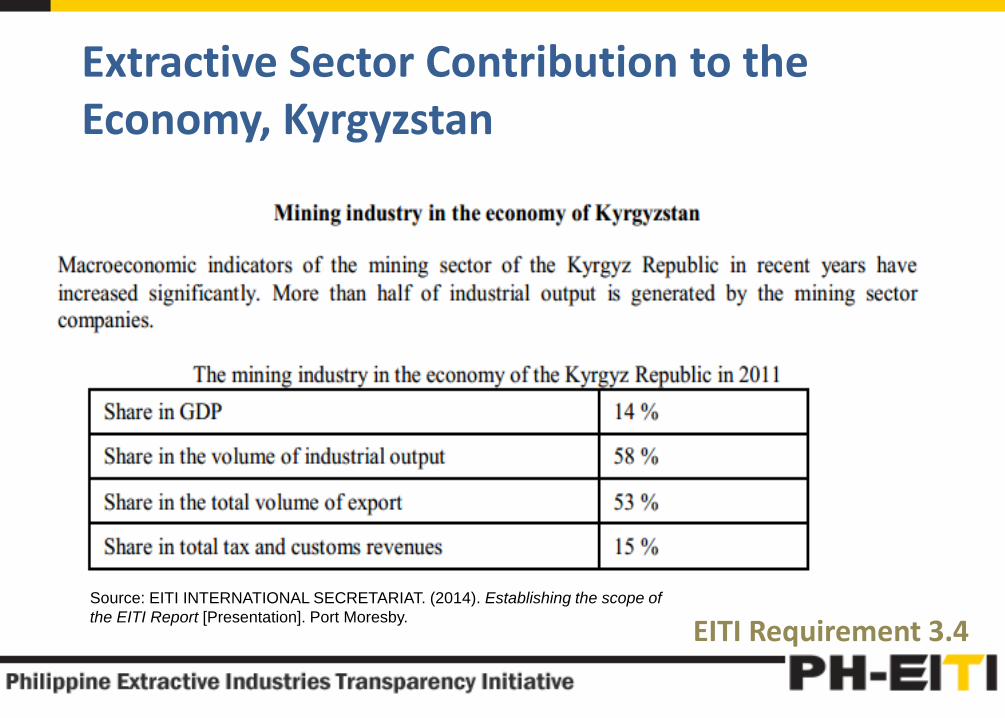

Extractive Sector Contribution to the Economy, Kyrgyzstan

EITI Requirement 3.4Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of

the EITI Report [Presentation]. Port Moresby.

Contribution to the Economy,Trinidad and Tobago

EITI Requirement 3.4

Source: EITI INTERNATIONAL SECRETARIAT. (2014).

Establishing the scope of the EITI Report

[Presentation]. Port Moresby.

Energy Sector Contribution toEconomy (2007-2011), Trinidad and Tobago

Source: TRINIDAD AND TOBAGO EITI. (2013). Trinidad and Tobago EITI Report 2010-11: Making Sense of

T&T’s Energy Dollars.

EITI-Reported Government Receipts as Percentage of Total Production Value, Average

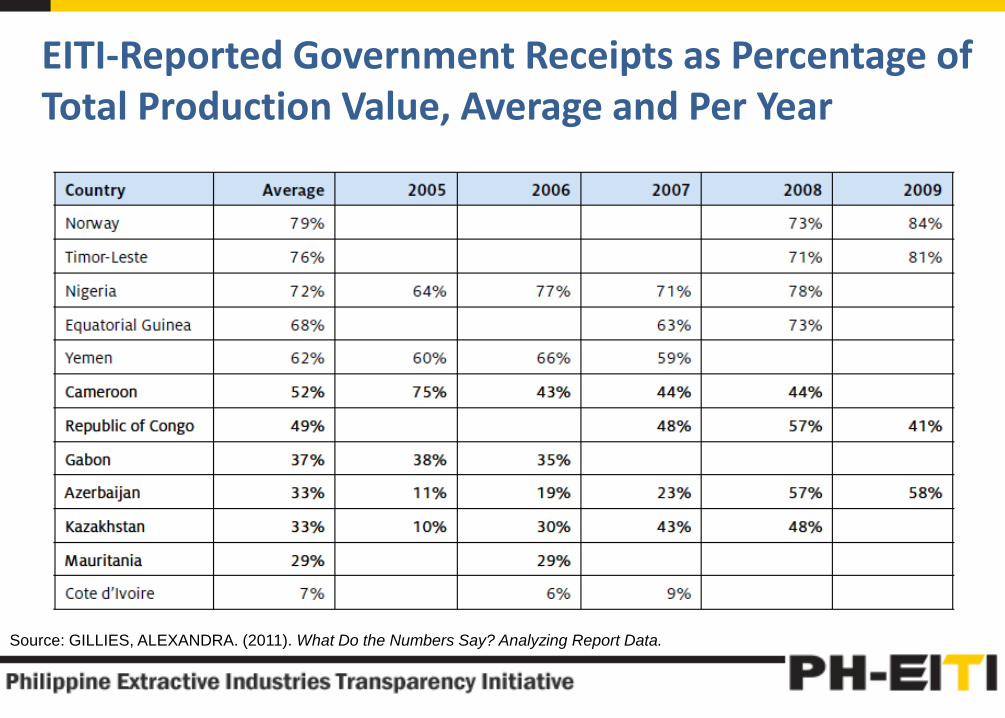

Source: GILLIES, ALEXANDRA. (2011). What Do the Numbers Say? Analyzing Report Data.

EITI-Reported Government Receipts as Percentage of Total Production Value, Average and Per Year

Source: GILLIES, ALEXANDRA. (2011). What Do the Numbers Say? Analyzing Report Data.

Export Data, Iraq

EITI Requirement 3.5

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report [Presentation]. Port Moresby.

WHAT DO EITI REPORTS TELL US?

2. How do local communities benefitfrom extractive operations withintheir localities?

EITI Requirement 4.1.e

Social Payments, Kazakhstan

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report

[Presentation]. Port Moresby.

Direct Sub-national Payments, Sierra Leone

EITI Requirement 4.2.d

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report [Presentation]. Port Moresby.

Sub-national Transfers, Peru

EITI Requirement 4.2.eSource: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report

[Presentation]. Port Moresby.

WHAT DO EITI REPORTS TELL US?

3. How are environmental funds and social development funds managed?

Environmental Protection and Remediation Activities, Mongolia

Source: MONGOLIA EITI (2013). Mongolia Seventh EITI Reconciliation Report – 2012.

Environmental protection and remediation activities by extractive company, Mongolia

Source: MONGOLIA EITI (2013). Mongolia Seventh EITI Reconciliation Report – 2012.

WHAT DO EITI REPORTS TELL US?

4. What do mining, oil and gas contracts say?

WHAT DO EITI REPORTS TELL US?

5. Who are the major players in the extractive sector? Where are operations found?

License Allocations, Afghanistan

EITI Requirement 3.10

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing

the scope of the EITI Report [Presentation]. Port Moresby.

License Holders, Norway

EITI Requirement 3.9

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report [Presentation]. Port Moresby.

Licensed Areas, Trinidad and Tobago

Source: TRINIDAD AND TOBAGO EITI.

(2013). Trinidad and Tobago EITI Report 2010-

11: Making Sense of T&T’s Energy Dollars.

WHAT DO EITI REPORTS TELL US?

6. Does the government collection tally with company payments? If not, what accounts for the discrepancy?

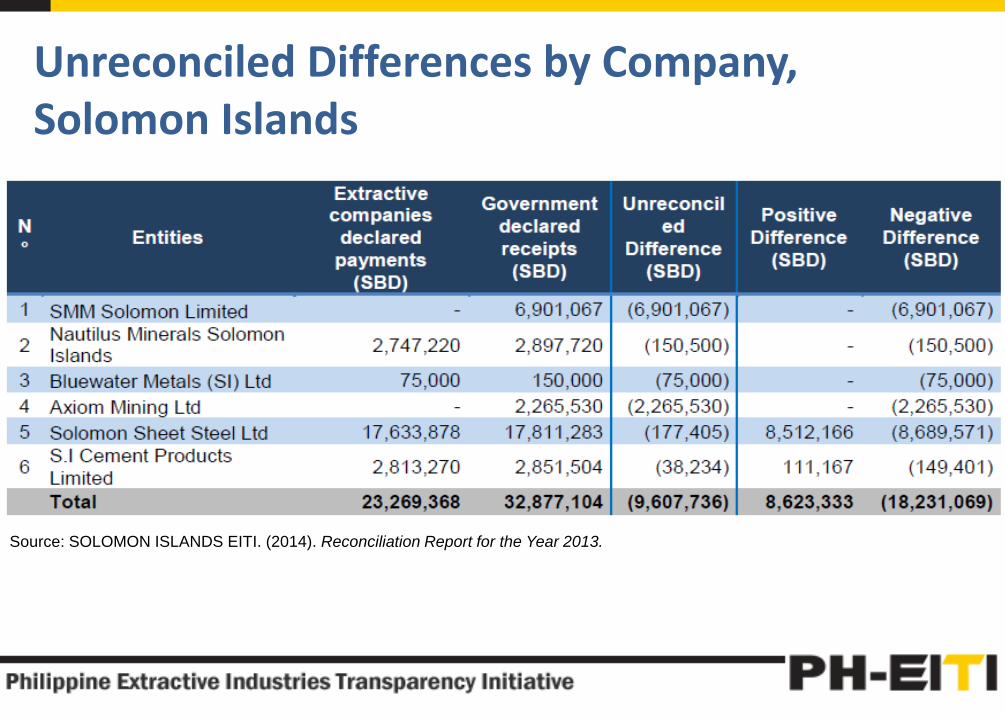

Unreconciled Differences by Company, Solomon Islands

Source: SOLOMON ISLANDS EITI. (2014). Reconciliation Report for the Year 2013.

Unreconciled differences by Agency/Tax, Solomon Islands

Source: SOLOMON ISLANDS EITI. (2014).

Reconciliation Report for the Year 2013.

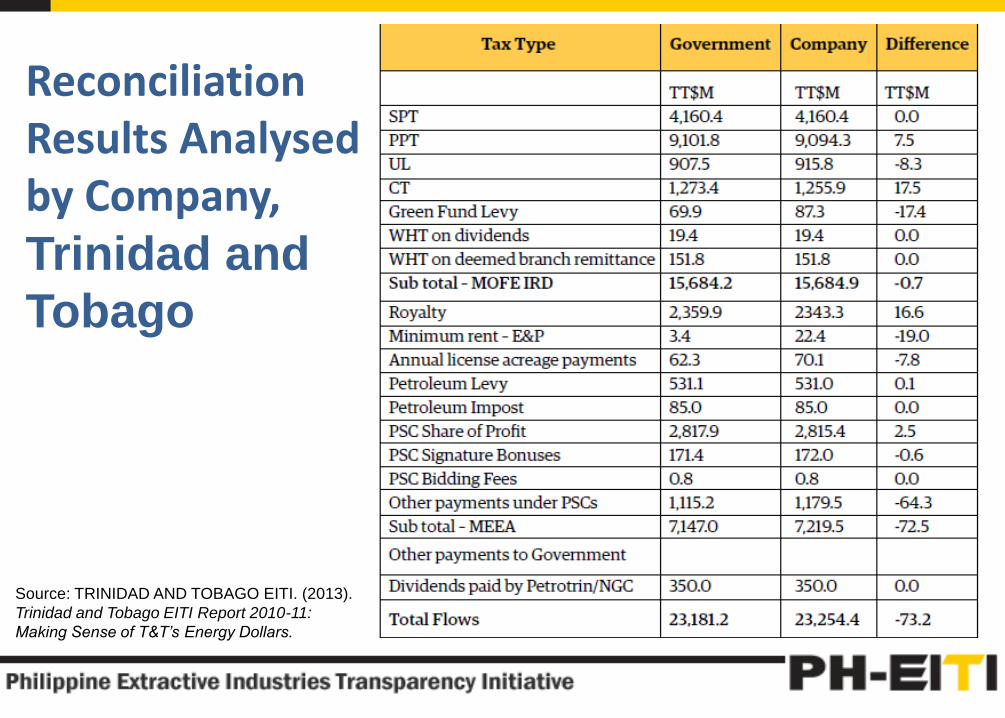

Reconciliation Results Analysedby Company, Trinidad and

Tobago

Source: TRINIDAD AND TOBAGO EITI. (2013).

Trinidad and Tobago EITI Report 2010-11:

Making Sense of T&T’s Energy Dollars.

Recovering Missing Payments, Nigeria

Source: EITI INTERNATIONAL

SECRETARIAT. (2014). Progress

Report 2014: Making Transparency

Matter.

WHAT DO EITI REPORTS TELL US?

7. How are revenues allocated? Do they go to intended beneficiaries?

Revenue Management and Expenditures, Trinidad and Tobago

EITI Requirement 3.8

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report [Presentation]. Port Moresby.

Revenue Allocations, Ghana

EITI Requirement 3.7

Source: EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report [Presentation]. Port Moresby.

CONCLUSION

WE WANT OUR EITI REPORT TO BE:1. CREDIBLE

2. COMPREHENSIVE

3. COMPREHENSIBLE

4. ABLE TO CONTRIBUTE TO PUBLIC DEBATE

REFERENCES

EITI INTERNATIONAL SECRETARIAT. (2014). Establishing the scope of the EITI Report [Presentation]. Port Moresby.

EITI INTERNATIONAL SECRETARIAT. (2014). Progress Report 2014: Making Transparency Matter.

GILLIES, ALEXANDRA. (2011). What Do the Numbers Say? Analyzing Report Data.

MONGOLIA EITI (2013). Mongolia Seventh EITI Reconciliation Report – 2012.

SOLOMON ISLANDS EITI. (2014). Reconciliation Report for the Year 2013.

TRINIDAD AND TOBAGO EITI. (2013). Trinidad and Tobago EITI Report 2010-11: Making Sense of T&T’s Energy Dollars.

PH - EITI Secretariat

Contact Details:

Telephone:+632 525 04 87

www.ph-eiti.org

THANK YOU!!!