the effect of audit quality with earning management as an...

TRANSCRIPT

The Effect of Audit Quality with Earning Management as an Intervening

Variable on Earning Quality

(Study on Service Company Listed in Indonesia Stock Exchange year 2013-

2015)

Undergraduate Thesis

By:

Melinda Octaviani

1113082100008

ACCOUNTING DEPARTMENT

INTERNATIONAL CLASS PROGRAM

THE FACULTY OF ECONOMICS AND BUSINESSES

SYARIF HIDAYATULLAH STATE ISLAMIC UNIVERSITY

JAKARTA

1437 H /2017 AD

i

CIRCULUM VITAE

DAFTAR RIWAYAT HIDUP

I. PERSONAL IDENTITY

1. Name : Melinda Octaviani

2. Place and Date of Birth : Bogor, 1 October 1995

3. Address : Jl. Ciomas I RT 001/ RW 011 No.14

Kecamatan Ciomas, Kelurahan Ciomas,

Kabupaten Bogor, 16610

4. Phone : 081296151539

5. Email : [email protected]

II. EDUCATION

1. TK Miftahul Salam Bogor 2000-2001

2. SD Rimba Putra Bogor 2001-2006

3. SMP Insan Kamil Bogor 2006-2009

4. SMAS Insan Kamil Bogor 2009-2012

5. S1 Ekonomi Akuntansi UIN Syarif Hidayatullah 2013-2017

III. SEMINAR AND WORKSHOP

1. Seminar by Pusat Pembinaan Profesi Keuangan (PPPK) Sekretariat

Jenderal Kementrian Keuangan and FEB UIN Syarif Hidayatullah

Jakarta. “Sosialisasi Perkembangan Terkini Profesi di Bidang

ii

Akuntansi dan Ujian Sertifikasi Akuntan (CA) dan Akuntan Publik

(CPA)”. 2015.

2. Training “Forensic Audit to Enhance Accountability in the Public

Sector” by The 16th

ATV FEB University of Indonesia.

3. Company Visit “Forensic Audit to Enhance Accountability in the

Public Sector” by The 16th

ATV FEB University of Indonesia.

4. Seminar by U.S. Embassy Jakarta and FEB UIN Syarif Hidayatullah

Jakarta, “Future Business Opportunities in the Global Islamic

Economy”. 2017.

IV. FAMILY BACKGROUND

1. Father : (PURN) Letkol TNI-AD Achmad Ramli (Alm)

2. Mother : Sundus Saleh Sanad

3. Child : 7 from 7 siblings

iii

Pengaruh Kualitas Audit dengan Manajemen Laba sebagai Variabel Intervening

terhadap Kualitas Laba

(Studi pada Perusahaan Jasa yang terdaftar di Bursa Efek Indonesia tahun 2013-

2015)

ABSTRAK

Tujuan penelitian ini adalah untuk memberikan bukti seberapa besar

pengaruh kualitas audit terhadap kualitas laba dengan menggunakan manajemen

laba sebagai variabel intervening. Populasi penelitian adalah perusahaan yang

tercatat di Bursa Efek Indonesia. Sampel penelitian adalah perusahaan jasa yang

tercatat di Bursa Efek Indonesia. Teknik Pengambilan sampel menggunakan metode

purposive sampling dengan sampel sebanyak 30 perusahaan untuk periode 2013

sampai dengan 2015.

Metode analisis data menggunakan analisis jalur dengan menggunakan SPSS

Versi 20. Variabel independen dalam penelitian ini adalah Kualitas Audit yang

diproksikan oleh fee audit, variable dependen adalah kualitas laba dan variabel

intervening adalah manajemen laba.

Hasil penelitian menunjukkan bahwa nilai signifikan 0,652 atas pengaruh

kualitas audit terhadap manajemen laba yang membuktikan tidak ada pengaruh

kualitas audit pada manajemen laba. Dan hasil pengujian hubungan langsung

kualitas audit terhadap kualitas laba menunjukkan hasil lebih besar yaitu 0,330 atau

33% dibandingkan dengan pengaruh tidak langsung melalui manajemen laba yaitu

sebesar -0,014 atau -1,4%, sehingga manajemen laba tidak bisa dijadikan sebagai

variable untuk kualitas audit terhadap kualitas laba.

Keyword: kualitas audit, manajemen laba, kualitas laba.

iv

The Effect of Audit Quality with Earning Management as an Intervening

Variable on Earning Quality

(Study on Service Company Listed in Indonesia Stock Exchange year 2013-2015)

ABSTRACT

The purpose of this study is to provide evidence of how much the effect of

audit quality on earning quality by using earning management as an intervening

variable. The population of the research is Company listed on Indonesian Stock

Exchange. The sample is service companies listed in Indonesian Stock Exchange. The

sampling method is purposive sampling that were sampled are 30 companies for the

period from 2013 to 2015.

A method used of data analysis was path analysis using SPSS version 20.

Independent Variable of the research is audit quality proxies by audit fees, dependent

variable is earning quality and intervening variable is earning management.

The results showed that significant value is 0,652 on the effect of audit quality

towards earning management which proved there is no effect of audit quality on

earning management. And test results direct effect of audit quality on earning quality

is larger result that is 0,330 or 33% compared with the indirect effect of audit quality

on earning quality through earning management which is -0,014 or -1,4%, so earning

management is not an intervening variable for audit quality on earning quality.

Keywords: audit quality, earning management, and earning quality.

v

FOREWORD

Assalamualaikum Wr.Wb

All praise to Allah SWT, the most merciful, seer, hearer, and all above

abundance of grace, for given me your gifts and blessings, so I can finish this thesis.

And also shalawat and salam always gives to our beloved prophet Muhammad SAW

and all his families and friends who always helped him in establishing Dinullah in

this earth. With patience, intelligence, and strong desire from Allah SWT, I am able

to finish this thesis as requirement for bachelor degree in State Islamic University

Syarif Hidayatullah Jakarta.

My very special thanks for my beloved daddy (alm) Achmad Ramli. Thank

you dad for given me your time, attention, prays, support and your patience in

educate me, even now you’re not here anymore for me, but you always be my best

hero ever lived in this world.

And I would like to extend my gratitude for my mom, for your all attention

and prays for me. You’re the one that always have your time to pray for me, devotes

all your love, you always patience facing your annoying and stubborn daughter.

Thanks a lot mom, thank you for being my mother, I always grateful to have you. I

hope I can be the reason of your both, mom and dad, smiles and proud.

On this occasion, with all my humility to thank for all helps, guidance, support,

pray, and spirit both directly and indirectly in completion of this mini thesis, to:

1. For my relatives family. All my brothers and sisters for the support and pray

for my success. Thank you for your all attention and loves for me.

2. Mr. Dr. Arief Mufraini, Lc., M.Si as Dean of Economic Faculty.

3. Mrs. Yessi Fitri, SE., M.Si., Ak., CA as Head of Accounting Major.

4. Mr. Hepi Prayudiawan, SE., MM., Ak., CA as Secretary of Accounting

Major.

vi

5. Mrs. Yulianti SE., M.Si as thesis supervisor. You have given me your time to

guide me to compile this thesis and share your knowledge to me. Thank you

very much for all attention and advice for me, so I can finish this thesis.

You’re the best mentor I’ve ever had.

6. Mr. Hepi Prayudiawan, SE., MM., Ak., CA as academic supervisor for given

me all information and help during lectures and all the support and pray.

7. All lecturers who have taught me patiently, may they have given are recorded

in Allah SWT almighty and all staff UIN Syarif Hidayatullah Jakarta,

8. Special thanks to Mr. Bonik. Thanks a lot for your provided information and

official stuffs that I needed in UIN Syarif Hidayatullah.

9. All my best friends (almh) Indriyanti, Banan , Wulan, Fita, Sisi, Yuli, Denisa,

Tari, Rani, Lia and Disa. Thank you for all time, support, and prays for me.

You’re all the best.

10. All friends in Accounting International Program 2013, Panji, Putra, Raisa,

Aji, Syarah, Ryan, Riski dan Afri. Thank you for every support and pray for

me and all story that we.ve been trough together. I’m really glad to be part of

you all.

11. All friends in International Program.

I am fully aware this mini thesis is still has a lot of flaws and far from

perfect due to many reasons including limited experience and knowledge I

have. Therefore, I expect all suggestion and also criticism from various

parties.

Wassalamu’alaikum Wr.Wb.

Bogor, June 2017

Melinda Octaviani

vii

TABLE OF CONTENTS

Curriculum Vitae ........................................................................................................ i

Abstrak........................................................................................................................ iii

Abstract ..................................................................................................................... iv

Foreword .................................................................................................................... v

Table of Content ...................................................................................................... vii

List of Tables ............................................................................................................. xi

List of Figures .......................................................................................................... xii

List of Appendixes .................................................................................................. xiii

CHAPTER I INTRODUCTION

A. Background ...................................................................................................... 1

B. Problem Formulation ..................................................................................... 15

C. Purpose and Benefit of Research ................................................................... 16

1. Purposes of Research ......................................................................... 16

2. Benefits of Research .......................................................................... 16

CHAPTER II STUDY LITERATURE

A. Literature …………………………….……………………………............... 19

1. Agency Theory……..…….…………….…………………............... 19

2. Audit Quality ..................................................................................... 21

3. Earning Management ......................................................................... 27

viii

4. Earning Quality .................................................................................. 31

B. Previous Research .......................................................................................... 33

C. Conceptual Framework ……………………..……………………………… 42

1. Variable Interrelation ………………………..……………………... 42

a. Audit Quality and Earning Quality …………………………….. 42

b. Audit Quality and Earning Management …………………..…... 43

c. Earning Management and Earning Quality ……………………. 44

d. Audit Quality and Earning Quality through Earning

Management ……………….…………………………………... 46

2. Research Model ................................................................................. 48

D. Hypotheses ..................................................................................................... 48

CHAPTER III Research Methodology

A. Scope of Research .......................................................................................... 49

B. Sampling Method ........................................................................................... 49

C. Collection Data Method ................................................................................. 50

D. Data Analysis Method ................................................................................... 51

1. Descriptive Statistic ........................................................................... 51

2. Classic Assumption Test .................................................................... 52

3. Coefficient of Determination ............................................................. 55

4. Hypothesis Test ................................................................................. 56

E. Research Variables Operationalization .......................................................... 57

1. Earning Quality (Dependent Variable) .............................................. 57

ix

2. Earning Management (Intervening Variable) .................................... 59

3. Audit Quality (Independent Variable) ............................................... 63

CHAPTER IV FINDING AND ANALAYSIS

A. General Description of Research Object………........................................... 67

1. Research Object Description ............................................................. 67

2. Research Sample Description ............................................................ 68

B. Analysis and Discussion ................................................................................ 70

1. Descriptive Statistic Analysis ............................................................ 70

2. Classic Assumption Test Results ....................................................... 71

a. Normality Test Result .................................................................. 71

b. Multicollonearity Test Result ....................................................... 72

c. Heterocedasticity Test Result ....................................................... 73

d. Autocorrelation Test Result ......................................................... 74

3. Determination Coefficient Test Result .............................................. 75

4. Hypothesis Test Result ...................................................................... 77

a. Significant Partial Test (t-test) ...................................................... 77

5. Interpretation ...................................................................................... 82

a. Effect of Audit Quality on Earning Quality ................................ 82

b. Effect of Audit Quality on Earning Management ........................ 83

c. Effect of Earning Management on Earning Quality.................... 84

d. Effect of Audit Quality on Earning Quality through

Earning Management ................................................................... 84

x

CHAPTER V CONCLUSIONS

A. Conclusions .................................................................................................... 87

B. Implication ..................................................................................................... 88

C. Recommendation ........................................................................................... 89

Reference ................................................................................................................... 91

Appendixes ................................................................................................................ 98

xi

LIST OF TABLES

No. Description Page

2.1 Previous Research .......................................................................................... 34

3.1. Variable Operationalization ........................................................................... 66

4.1. Detail of Research Sample ............................................................................. 67

4.2. Research Sample............................................................................................ 69

4.3. Research Sample Distribution ………………………………………..……. 70

4.4. Descriptive Statistic Analysis in Period 2013-2015...................................... 70

4.5. Klomogorov-Smirnov Test Result................................................................. 72

4.6 Multicollonearity Test Result ........................................................................ 73

4.7. Autocorrelation Test Result........................................................................... 75

4.8. Coefficient of Determination Equation I Test Result.................................... 76

4.9. Coefficient of Determination Equation II Test Result ………………...…… 76

4.10. Direct Regression Test Result ....................................................................... 79

4.11. Regression I Test Result ……........................................................................ 80

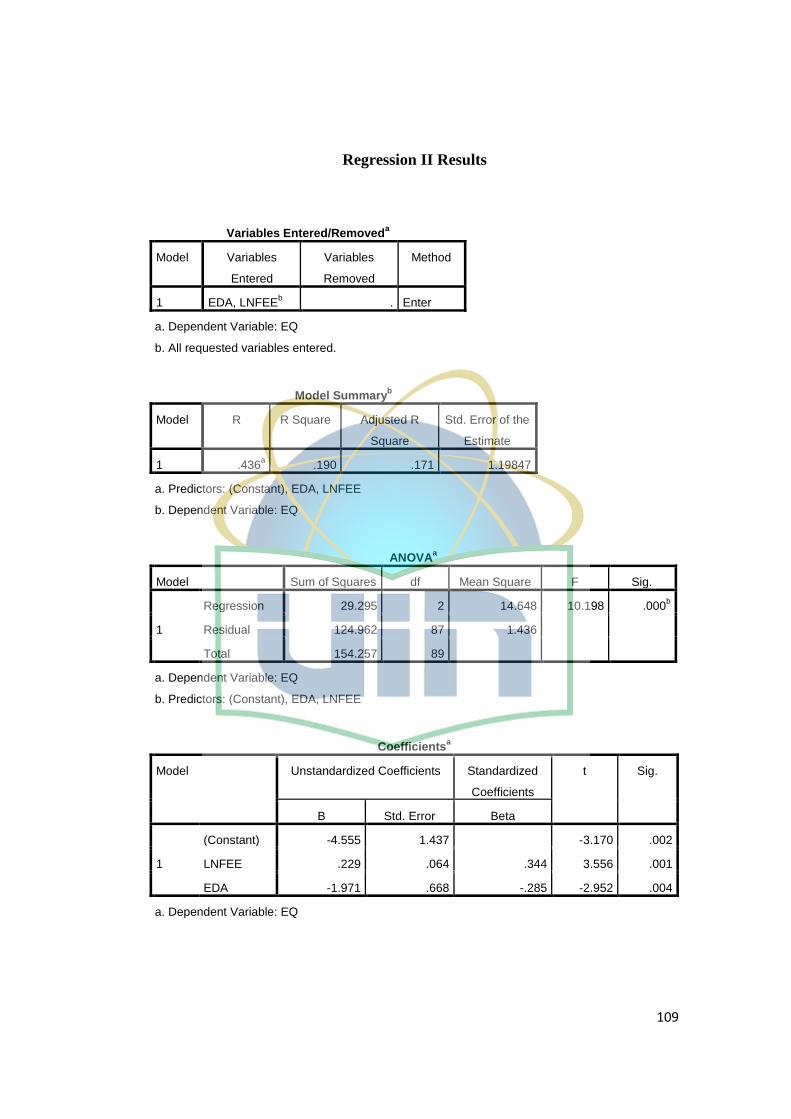

4.12. Regression II Test Result ............................................................................... 81

xii

LIST OF FIGURES

No. Description Page

2.1. Research Model ............................................................................................. 48

4.1. Scatterplot Graphic........................................................................................ 74

4.2. Path Analysis Result...................................................................................... 82

xiii

LIST OF APPENDIXES

No. Description Page

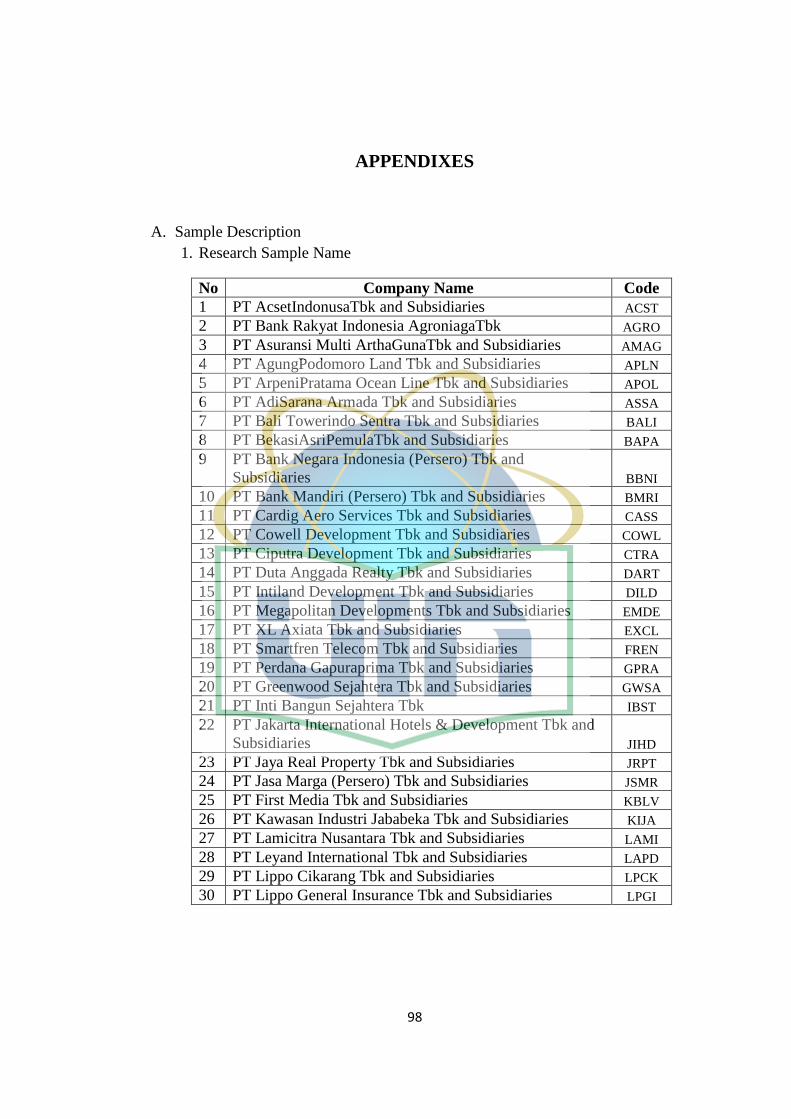

1. Sample Data Description ..................................................................................... 98

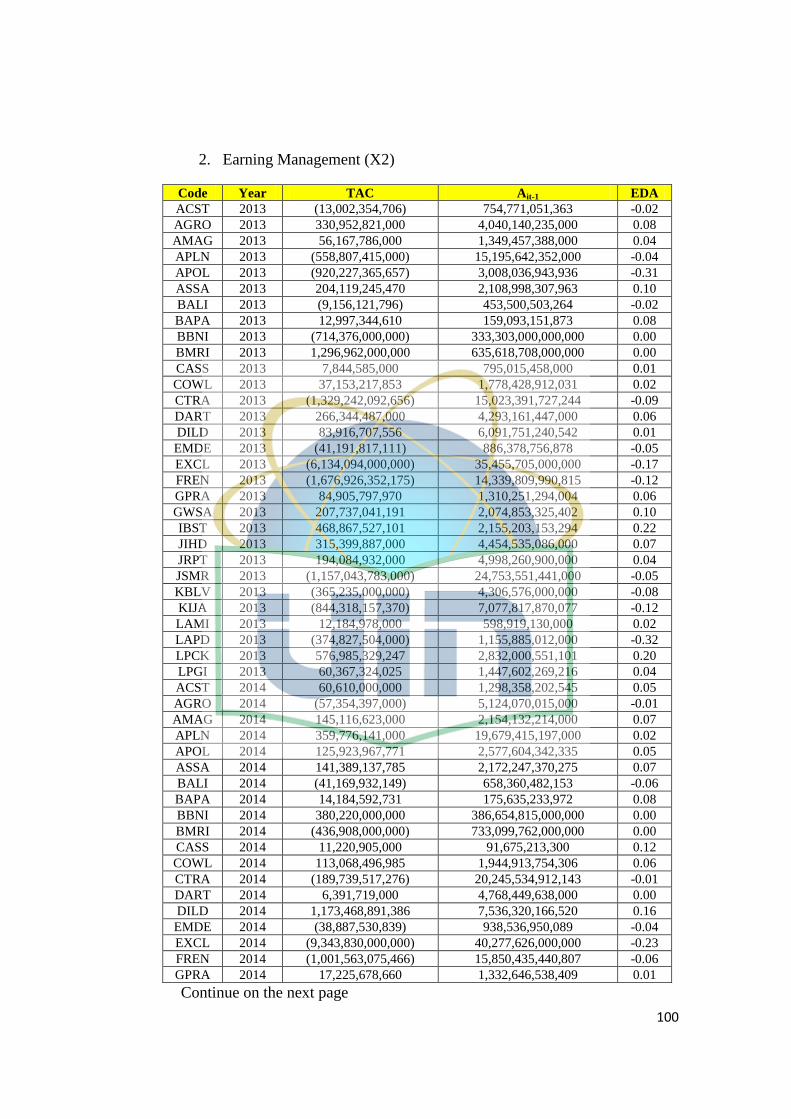

2. Raw Data Description ………………………………………………………….. 98

3. SPSS Output Result ........................................................................................... 104

1

CHAPTER I

INTRODUCTION

A. Background

A company’s number one goal is to make money. Not only have

profit at the end of every accounting period, but they also want the

company financial statements to look as good as they can. The main

purpose of a company when it’s established is to gain revenue or earning

as much as possible. The earnings of a company can be seen from the

financial statement of the company. Public companies have an obligation

to submit periodic financial statements, namely annual reports and mid

financial statements or quarterly financial report which is in Indonesia is

every 4 months (divided into quarterly 1, 2, and 3). The annual financial

statement submitted to Badan Pengawas Pasar Modal (Bapepam) and

should be announced to the public. Financial statement is a tool to deliver

financial information regarding the management’s responsibility of their

performance (Novianti, 2012).However, because of many interests of

individuals within the company, cannot be ensured if the financial

statement made is truly what is happened. So it becomes a doubt for users

of financial statements, especially investors, the quality of the financial

statements which in this case is the earnings. Thus, it’s necessary to have

2

evidence that can ensure the quality of earnings of the company to be

reliable, this is called earnings quality.

Because of management actions which reported earnings that do

not describe the actual condition of the company resulted in profit

generated becomes questionable quality. This phenomenon can be

detrimental to many users of financial statements. Each party has their

own interest from the financial statement (Novianti, 2012). In accordance

with Schipper and Vincent (2003) mentioned, that earning quality in

particular and quality of financial statement in general is important for

those who use the financial statement due to contract purposes and

investments decision making. Novianti (2012) stated the importance of

earning information has expressly mentioned in Statement of Financial

Accounting Concept (SAFC) No. 1 which states that in addition to

assessing the performance of management, earnings also help estimate the

earnings capacity representatively, as well as to assess the risks in the

investment or credit (FASB, 1985). Earnings information reported by the

company’s management will be used by investors to take decision whether

to invests their money or not, also forecasting the future earnings.

Investors buy shares when they believe that earning in the future can

increase the share price (Libby, et al., 2008).

With the importance of earning quality that exists in the financial

statement, then it is necessary to ensure that financial statement presented

fairly by management. But on the other hand if the company is in bad

3

condition and the financial statements is worst, to keep the company and

the investors, the management is required to always produce the

interesting financial statements for shareholders and it could make the

management acted dishonestly and manipulate the results of financial

statement. In addition to the company's interests in order not to lose the

trust of shareholders, also for the benefit of themselves in order to

complete their task. The idea that the management can take action only

provides benefits for himself based on an assumption that states everyone

has the behavior of selfish or self-interested behavior. The desire,

motivation and utilities are not the same between management and

shareholders raises the possibility of management acts detrimental to

shareholders, among others behave unethically and tend to do the

accounting fraud. This conflict can result in the nature of management

which reporting profits opportunistically to maximize his personal gain. If

this occurs would resulting poor quality of earnings (Rachmawati and

Triatmoko, 2007).

Taruno (2013) mentioned that reporting financial scandal have

been a lot going on, in abroad there are a lot of accounting scandals by

doing management earnings, among others Enron, Merck, World Com and

majority other companies in the United States. Some of the cases occurred

in Indonesia such as PT. Lippo Tbk and PT. Kimia Farma Tbk also

involves financial reporting originated from detected manipulation. PT

Kimia Farma Tbk case proved overstated their net income from the initial

4

reported 132 billion Indonesian Rupiahs and that report was audited by

Hans Tuanakotta & Mustofa (HTM). But Ministry of State-Owned

Enterprise of Republic of Indonesia (BUMN) and Bapepam assessed that

net earnings is too large and contains elements of manipulating act. The

real earnings were only 99.56 billion Indonesian Rupiahs or 24.7% lower

than initial profit. Cases like this that make the shareholders doubted the

quality of presented earnings. It is made should there is third party who

can ensure the financial statement is presented fairly (Media: Kompasiana,

2015).

Trusted party that is able to ensure the financial statement is an

independent party that is auditor. Auditors are expected to provide

information stating that the report made by the management has been

fairly presented or not. Because, according to government regulations from

Finance Ministry of Indonesia No: KEP-346/BL/2011 announced that

public company in Indonesia should report periodic financial statement

and annual reports to Badan Pengawas Pasar Modal (Bapepam) which

must be accompanied by an opinion of public accountants who audited the

financial statements. Auditors with carry out a series of audit process, if

found any material misstatement in the financial statement, the auditor

have a right to give justification recommendations.This makes the

company requires the services of a public accountant (now called as an

auditor). An auditor provides audit services on the client's financial

statements to provide assurance to users of financial statements that the

5

financial statements have been prepared in accordance with accounting

standards so that financial statements can be relied upon in making

decisions. The decision makers of course expect the best results of the

audit so as to make them believe the decision they should take. Audit

services is a means of monitoring the possibility of conflict of interest

between the owner and managers and the shareholders with a number of

different ownership and can reduce the information asymmetry between

managers and stakeholders of the company to allow outsiders to check the

validity of financial statements (Jensen and Meckling, 1976).

In principle, an audit is supposed to improve earnings quality.

However, it is unclear which earnings attributes are considered by auditors

as being indicative of high earnings quality and it is unclear which

financial statement users benefit the most from having an audit (Lenox

et.al. 2015).High quality information is important in making good

judgments and decisions. It’s important for many participants in the

financial reporting process: investors (e.g., where and how much to invest,

what is the investment risk), regulators (e.g., what is the quality of

financial reporting standards), auditors (e.g., what is the quality of

financial statements and audit performed), lenders (e.g., what is the credit

quality of an entity), etc. It’s used in many investment decision and

valuation models. There is no single definition of the quality of earnings,

as well as there is no single measure of this concept. According to the

Statement of Financial Accounting Concepts No.1, higher earning quality

6

provide more information about the features of a firm’s financial

performance that are relevant to a specific decision made by a specific

decision-maker.

In general, the earnings quality can be looked at as the quality of

information. High quality information is precise (accurate), relevant,

comparable, unbiased, and timely. The concept of the quality of

information is especially applicable in the context of capital markets. For

example, from the precision perspective, the quality of earnings is high

when earnings precisely reflect the underlying (i.e., true) operating risk

and environment, business performance, and reporting quality of an entity.

Dechow et.al. (2010) define the high-quality earnings number is one that

accurately reflects the company’s current operating performance, is a good

indicator of future operating performance, and is a useful summary

measure for assessing firm value. From that, Dechow et.al. (2010) define

earnings to be of high quality when the earnings number accurately

annuitizes the intrinsic value of the firm. Interest of knowing the quality of

earning is not only for investors but also to regulators, standard setters,

credit rating agencies, analysts, accounting researchers, and many other

participants in the financial reporting process. As the result, there are

numerous benchmarks and views used to measure the quality of earnings.

Earnings quality can be viewed from such perspectives as (but this

is not an exhaustive list):

7

1. Analyst expertise

2. Auditor independence

3. Balance sheet

4. Decision usefulness

5. Earnings management

6. Financial analysis/reporting

7. International Measurement

For instance, from the decision usefulness perspective, the quality

of earnings is how precisely the earnings reflect the changes in the wealth

of a company. From the financial analysis perspective, the earnings quality

is how precisely the earnings measure the value of the company and how

accurately they (earnings) represent the firm’s current and future

performance. Determining earnings quality and its implications for firm

value is complex. Understanding a company’s quality of earnings requires

expertise in finance, accounting, and corporate strategy and a strong

knowledge of the industry in which the company operates and the

governance mechanisms monitoring and rewarding employees and

managers.

As a result of failures occurred to business organizations and the

subsequent collapse and bankruptcy of large and multinational firms, such

as Enron, WorldCom, and other firms, and based on the clear relationship

of these collapses with manipulating the accounts of these firms, doubts

emerged among users of financial information regarding the credibility of

8

this announced information, where they depend on, in decision making.

This incredibility and unreliability raise many questions, including the

managements of these firms, and the effectiveness of accounting

standards, and the applied procedures in firms. Auditors' responsibility and

credibility, audit process, and audit quality, became questionable directly

next to these collapses (Almomani, et al., 2015). Because of increasing

number of collapsed firms, and losses incurred by investors and creditors,

the issue of earnings quality became the focus of different interested

groups of people. The issue of earnings quality stems its importance from

the quality of reported earnings by business organizations in the financial

and investments decisions that investors, creditors, and other users depend

on, in taking decisions. Eisa (2008) in Almomani (2015) stated that

earnings quality is used in performance evaluation of firms, and in

determining the fair value of these firms. Moreover earnings quality is

important in future estimations and contracting. Dechow and Schrand

(2004) explained that earnings quality is strongly associated with quality

of financial reports, where this quality of earnings can be achieved when

firms adhere to the legal, professional, and control standards. Business

organizations are required to issue reliable, free of errors and misstatement

information, to provide a good base for the evaluation of current operating

performance of firms, and to be appropriate for the estimation of its future

operating performance, and for the determinations of the fair value of

firms. Penman (2003), demonstrated that earnings quality is associated

9

with accounting profits, realized cash flows, so quality of earnings is

achieved when the reported income reflects the actual profits, where future

expected profits can be accurately estimated.

Nowadays, auditors encounter several types of pressure by users of

accounting information in order to improve the quality of audit, because of

several financial problems exist in periodic financial reports. Audit

profession is required these days to concentrate on efficient and qualified

work force, to provide audit services with high quality, and to be able to

reveal any incorrect practices that managements take to affect the

accounting measurement. Audit report is considered one among the most

important inputs for the decision making process. In addition, audit quality

is a primary requirement for different groups of users. Actually, audit

quality is difficult because of its difference in nature, to provide trust with

audit reports and financial statements (Scott and Pitman, 2005). Audit

quality means that audit profession has the ability to detect the significant

errors, and limits information inconsistency between managements and

shareholders, so it can protect the behalves of shareholders. Audit

profession is expected to provide highly efficient services and to keep the

trust of its services in minds of interested people (Eisa, 2008 in Almomani

2015).

After all, the financial statements are what potential investors and

creditors look at when they make the decision whether or not to lend the

company money or to become an investor. This is where the concept of

10

earnings management comes into play. As a result, these effects of

management interventions are reflected in the reported income, and led to

a situation where income does not represent the actual situation, especially

when managements' awards depend on the reported income. Earnings

quality means that the reported income is actual and not overstated or

manipulated, and at the same time reflects the actual economic events

occurred in the entity during the accounting period (Bellovary et al.,

2005). And because of that there is a potential action that maybe done by

the management to arrange the earning based on their own interest or

usually called as earning management. The definition of earnings

management in a nutshell, is the creative use of different accounting

techniques to make financial statements look better. Earnings management

is a global phenomenon in financial reporting or reporting of information

related to profits. The purpose of earnings management is to demonstrate

reasonable earnings quality that meets either the shareholders’

expectations, or the requirement of obtaining relevant authorization from

regulators (Ahmadpour and Shahsavari, 2016). But a lot of case proved

that management acts opportunistic earning management by increasing or

decreasing the accrual number of income statement which causes earning

information is not appropriate with actual company’s performance (Azhar,

2013).

Thus, earnings management has much in common with earnings

quality (represented by accruals quality, earnings persistence, earnings

11

predictability, and earnings smoothness in our study). For instance, highly

managed earnings can yield low quality earnings (Lo, 2008), as the

“artificial” information may lead to an incorrect decision. However, the

absence of earnings management is insufficient to guarantee high quality

earnings, because other factors (such as capital market and management

compensation) contribute to the quality of earnings (Lo, 2008). Earning

management is the use of accounting techniques to produce financial

reports that present an overly positive view of a company’s business

activities and financial position. Healy and Wahlen (1999) describe

earnings management (EM) as an action of managers to adjust financial

reports using their judgment in order to influence contractual outcomes

that based upon reported accounting data or to mislead stakeholder about

firm’s performance.

The influence of audit quality towards the earning quality and

earning management is also important to know because audit quality needs

to be in accordance with certain accounting rules and it adds value if the

quality enables financial statements to reflect the economic performance

position of a firm and ensure that good performing firms can be

distinguished from bad performing firms. In theory, a firm should select

accounting methods and make estimations which best reflects the

economical position. In practice this means that audit firms must be

independent from the client, due to the liability and disciplinary sanctions.

Because there is room for subjectivity when expressing an opinion on a

12

financial statement, the probability that an audit firm discovers a material

error or the risk that the audit firm will report these errors and signals are a

couple of the many contributing factors when it comes to audit quality

(DeAngelo, 1981).

As Velury & Jenkins (2008) states, earnings quality is influenced

by the audit quality, because a high level of audit quality leads to a higher

degree of earnings quality. But other research that is Pupperhart (2012)

provided evidence that high audit quality is not significant associated with

high earnings quality. Also research done by Gerayli et al. (2011) which

use discretionary accruals as a measure of earning management reveal that

discretionary accruals are negatively related to auditor size and auditor

industry specialization which are the measurement of audit quality. Their

findings also support our hypothesis of the negative association between

auditor independence and discretionary accruals. Overall, this study

provides evidence that firms which are audited by high quality auditors are

more likely to have less discretionary accruals. Other research that tested

the influences between audit quality, earning management and earning

quality is the main reference of this study it’s Almomani (2015) also tested

the quality of audit to earning quality, He stated that audit quality have

significant relations with quality of earnings. And also there are some

researches that tested the quality of audit on earning managements.

Research done by Nawaiseh (2016) stated that the audit quality which is

used audit tenure, audit fees and international big auditing firms as proxies

13

have significant relations with earning management. But founded that are

no relationship is found between leverage, return of asset (ROA), cash

flow/total assets (CFO) towards earning management.

As there has been a collection of massive accounting fraud, for

example: Enron (special purpose entities to hide debt), WorldCom (of

misstatements) and Parmalat (for cash balance overstatements), critics

conclude that there was a correlation of various factors which have

contributed to these accounting scandals. A few of the factors that

contributed to the collapse of these firms included poor corporate

governance, management compensation packages and also a decline in

audit quality, with the adverse consequences of poor earnings quality. This

has been the subject of significant debate among academics, practitioners

and regulators. However, the empirical evidence on earnings quality is

sparse and controversial. Examining one factor of lower earnings quality

that has an impact on information asymmetry (e.g. a decline in audit

quality) is one of the focuses in this research. Lower earnings quality

increases the adverse selection risk and lowers liquidity in financial

markets, especially for public firms where earnings represent the principal

source of information for market participants (Pupperhart, 2012).

Based on the above, researchers are motivated to do this study

because the first quality of earnings of a company plays a very important

for shareholders and creditors for decision making. With the good quality

of earnings they can easily made decision whether to make investment for

14

investor or give loan for the creditors. Second, this study also test about is

the earning management effect earning quality or not because earning

management can change the value of confident of this quality of earning if

don’t done fairly. And last, earning management can influenced (based on

the previous researches) the quality of audit if the auditor doesn’t know

nor can’t find that the management do the illegal or unfairly earning

management. Based on those reasons, the researchers conducted a study

entitled “The Effects of Audit Quality with Earning Management as an

Intervening Variable on Earning Quality.”

This research is an extension of the previous research done by

Taruno (2013), Almomani (2015), and Nawaiseh (2016). The differences

of this study with the previous research are as follows:

1. The variable used in previous research is audit quality

which is influenced the earning quality. Moreover, in this

study, the researcher add one variable its earning

management as an intervening variable to expand the scope

of discussion and get more complex (Almomani, 2016). In

addition, the management manages the earnings to profit-

motivated, and implies earnings management reduces the

information content of accounting items. On the other hand,

some researchers have informative look-out earnings

management, and these are considered as a way to raise

awareness of favorable financial conditions to shareholders,

15

that it is done by management involvement in the process

of income determination (Subramanyam, 1996, pp.249–

281). So it should be expected that earnings management

not only does not reduce the income information content,

but it also helps investors in the better interpretation of

reported items (Ahmadpour and Shahsavari, 2016).

2. The population of this study is Services Company Listed in

Indonesia Stock Exchange at the period 2014-2015

suggested by previous research to study in other countries.

Meanwhile, the study population before is the entire

industry in Amman, Jordan.

B. Problem Formulation

From the background above, the problem formulation that will

identify in this research are:

1. How much audit quality effect the earning quality?

2. How much audit quality effect the earning management?

3. How much earning management effect the earning quality?

4. How much audit quality effect the earning quality through

earning management?

16

C. Purposes and Benefits

1. Purposes of Research

Based on the problems formulation above, the purposes of

the research are:

a. To test and analyze the effects of audit quality

towards earning quality.

b. To test and analyze the effects of audit quality

towards the earning management.

c. To test and analyze the effects of earning

management towards the earning quality.

d. To test and analyze the effects of audit quality

towards the earning quality through the earning

management.

2. Benefits of Research

a. Theoretical Contributions

1) Student Accounting Department, this study is useful

as reference material for future research and

comparative increase knowledge.

2) Society, as information facilities about the earning

management, audit quality and the earning quality

and also to add the knowledge about auditing which

may be useful in the future.

17

3) Subsequent researchers, as a reference for those

parties who will carry out further research on this

topic.

4) The author, as a means to broaden insight and make

reference to auditing, especially on the earning

management, audit quality and also about the

earning quality which is expected to be useful for

writers in the future.

b. Practical contribution

1) Auditor and Public Accountant Office (KAP), a

review which is expected to be used as information

to improve the audit quality so can influence the

earning quality of the client’s company.

2) Company or User, expected to be useful in

assessing the quality of audit and that influence to

the earning quality of company.

3) Indonesian Institute of Accountants (IAI), the

research is expected to contribute positively so that

it can be used as a basis for considering audit

activity especially about the audit quality and the

effect to earning quality and earning management.

4) Indonesian Institute of Certified Public Accountants

(Certified), as additional information about audit

18

quality and earning management and their influence

to the earning quality of company.

19

CHAPTER II

STUDY LITERATURE

A. Literature

1. Agency Theory

Agency theory explains the existence of a contract between

the agent (management) and the principal (shareholders) which the

agent received a mandate to manage the company of the principal.

Jensen and Meckling (1976) an agency relationship as a contract

under which one or more persons (the principal(s)) engage another

person (the agent) to perform some service on their behalf which

involves delegating some decision making authority to the agent. If

both parties to the relationship are utility maximizers, there is good

reason to believe that the agent will not always act in the best

interests of the principal.

The principal can limit divergences from his interest by

establishing appropriate incentives for the agent and by incurring

monitoring costs designed to limit the aberrant activities of the

agent. In addition in some situations it will pay the agent to expend

resources (bonding costs) to guarantee that he will not take certain

actions which would harm the principal or to ensure that the

principal will be compensated if he does take such actions.

20

However, it is generally impossible for the principal or the agent at

zero cost to ensure that the agent will make optimal decisions from

the principal’s viewpoint. In most agency relationships the

principal and the agent will incur positive monitoring and bonding

costs (non-pecuniary as well as pecuniary), and in addition there

will be some divergence between the agent’s decisions and those

decisions which would maximize the welfare of the principal

(Jensen & Meckling, 1976).

Agency costs arise in any situation involving cooperative

effort by two or more people even though there is no clear-cut

principal-agent relationship. Viewed in this light it is clear that our

definition of agency costs and their importance to the theory of the

firm bears a close relationship to the problem of shirking and

monitoring of team production. Since the relationship between the

stockholders and the managers of a corporation fits the definition

of a pure agency relationship, it should come as no surprise to

discover that the issues associated with the “separation of

ownership and control” in the modern diffuse ownership

corporation are intimately associated with the general problem of

agency (Jensen & Meckling, 1976).

Because of this potential conflict of agency, an agent

(management) who knows more internal information about the

company than the principal must provide information about the

21

condition of the company, especially which is mandatory and also

voluntary as specified minimum additional disclosures.

Information asymmetry occurs between management by the

owners provide the opportunity for the manager to act

opportunistically that for sake of personal gain. Under such

circumstances the manager can use the information learned to

manipulate financial reporting by way of earnings management

(Azhar, 2013) or as Subramanyam (1996) called as opportunistic

earnings management which means managers apply it to maximize

their own interests and not the interests of the company and the

investors.

Therefore necessary to have an independent party that can

be trusted entirely by the principal and the party is the auditors.

Auditors are expected to ascertain whether the financial statements

presented by management was fair or not because the principal

interest in this case is the profits from the company so that the

auditor is expected or even to be able to ensure the quality of the

profit generated by the management.

2. Audit Quality

Audit quality now is no longer a new concept under the

scope of auditing. Not only the complete all procedures of audit

that can guarantee that the audit have a good quality but also other

factors. The important thing to know first is the definition of audit

22

quality. There are many different definitions but none of them has

achieved universal acceptance. It can even be argued that quality

itself is a concept that cannot be comprehensively defined

(Pitkänen, 2016). Probably the most used definition of audit quality

is created by DeAngelo (1981) which defines audit quality to be

the market-assessed joint probability of discovering an error in the

financial statements and reporting it to the stakeholders. In this

definition quality requires both competence and independence from

the auditor. Without adequate competence the auditor might not be

able to detect the error so irregularities and without high level of

independence auditor might not be willing to report his findings

truthfully. With adequate independence and competence the

auditor should be able to find the material misstatements and report

them, thus completing the audit with high quality.

Malihi et al. (2012) provides further explanation that audit

quality could be a function of the auditor’s ability to detect material

misstatements and reporting the errors. Together with other similar

definitions, they all emphasize on two of the most important

aspects of audit quality, namely auditor ability or auditor effort,

and auditor independence. Therefore, this stream of definitions is

mainly about the auditors’ quality. Another stream of defining

audit quality focuses on the accuracy of the information reported

by the auditors. Titman and Trueman (1986) suggest that high

23

audit quality would improve the reliability of financial statement

information and allows investors to make more precise estimate of

the firm’s value. Schauer (2002) also advises that “a higher quality

audit increases the probability that the financial statements more

accurately reflect the financial position and results of operations of

the entity being audited”. In other words, audit quality is part of the

quality of accounting information disclosed (Clinch et al., 2010).

The audit process is considered a key important element in

the structure of financial statements because it tests whether the

financial information is in an independent and objective form, in

order to increase the credibility of this information. The most

important factor of audit quality is the ability of an auditor to detect

errors and other significant misstatements and reducing the level of

accounting information inconsistency between shareholders and

management (Almomani, 2015).Quality auditor is when the auditor

can give accurate information. Accurate information is information

that can pin point the value of the company. DeAngelo (1981)

defines quality audit as the probability that an auditor discovered

and reported about the existence of a breach in the accounting

system of its clients. Qualified auditors should provide proper

information, not only wore a higher fee so the choice was really

reflects the information contained in the company. In Indonesia

24

there are called as Big4 audit firms. Here is a list of the firm that

belongs to the group Big Four in Indonesia:

a) Public Accountant Firm of Osman Bing Satrio and

Partners affiliated with Deloitte.

b) Public Accountant Firm of Tanudiredja, Wibisana,

and Fellow affiliated with Price Waterhouse

Coopers (PWC).

c) Public Accountant Firm of Purwanto, Suherman,

Surja affiliated with Ernst & Young (EY).

d) Public Accountant Firm of Siddharta and Widjaja

affiliated with KPMG.

There are a lot of proxies’ uses to measure the audit quality.

Which is in DeAngelo (1981) stated audit firm size as a

measurement of audit quality. Research did by Almomani (2015)

use several measurements which are audit office size, auditors’

fees, period of customer retention, type of auditor’s opinion, and

the specialization in client’s industry. The study finds that auditor

fees have most important significant effect on earning quality,

followed by auditors’ opinion, where others factors has no

significant effect on earning quality. Ahmed (2012) in Almomani

(2015) used audit fees, audit office size, client's retention period,

association with international audit fees and professional

qualification of audit office employees, as features of audit quality.

25

The features of audit quality that used by Hamdan (2012) in

Nawaiseh (2016) include audit office size, audit fees, client's

retention period, audit office specialization with the industry of the

client, and association between audit office and the international

offices of auditing.

From that several proxies of measuring the audit quality,

this research will use the auditor fees as a measurement of audit

quality. Besides of many research done using the auditor fees as a

measurement or proxy of audit quality (Ahmed, 2012 in

Almomani, 2015, Hamdan and Ijaela 2012, and Nawaiseh 2016),

already proved that auditor fees as a measurement of audit quality

is significantly influence the earning quality. Hamdan and Ijaela

(2012) in Nawaiseh (2016) investigate the existence of earnings

management practices and earnings quality in the industrial public

companies listed in Amman Stock Exchange (ASE), and tests the

impact of auditing quality characteristics (the audit office size, the

connection with global offices, client retention period, auditing

fees, and specialty in client’s industry) on reducing earnings

management practices, and enhancement earnings quality. Data of

45 companies of the industrial sector for the period 2001-2006

were arranged. The most important conclusion of that study was;

the industrial public companies listed in (ASE) have practiced

earnings management each year during the study period, the study

26

itself cannot prove the earnings quality in the companies of the

industrial sector.

Beatty (1989) argued that the nature and extent of agency

costs vary across organizations and this variation may lead CPA

firms to differentiate the quality of their services. Auditing firms

which have relatively greater investments in reputation capital have

greater incentives to maintain this reputation. Beatty (1989) further

proposed that the accounting information disclosed in the financial

statements audited by high reputation firms would be more precise

than that audited by firms with lower investments in reputation, as

this is one manner in which such firms can protect their reputation

capital. Copley (1991) stated that it seems reasonable that

differences in audit quality would be reflected in audit fees.

Specifically, independent-audit consumers, seeking higher levels of

audit quality, will be required to pay a premium price. Audit fees

were regressed against variables intended to measure the marginal

cost of performing the audit. Beatty (1989) argued that the residual

reflects the price paid to a particular audit firm above or below the

average price paid for auditor reputation. Beatty also stated that

financial reports audited by high reputation firms are more precise,

allowing investors to reduce risk by more precisely estimating the

distribution of firm value.

27

3. Earning Management

Scott (2000: 296) states that the selection of accounting

policies done by manager for a particular purpose is called earnings

management. Related to earning information, Statement of

Financial Accounting Concept (SFAC) No.1 states that such

information is a major concern for assessing the performance or

accountability of management. Besides earnings information also

helps users of financial statements in assessing the company's

earnings power in the future. Therefore, management has a

tendency to take action to provide an attractive financial statement

(Guna and Herawati, 2010). Kitiwong et.al. (2012) stated there are

several definitions of earning management and most widely used

definitions of earnings management are Schipper’s (1989) and

Healy and Wahlen’s (1999) definitions. The definitions indicate

that a management’s incentive to exercise earnings management,

its intent to influence reported earnings, and its use of judgment in

the financial reporting process are the main criteria for defining an

activity as earnings management. However, these two definitions

do not indicate how earnings management is associated with

generally accepted accounting principles (hereafter GAAP),

especially whether it is allowed by GAAP. Therefore it is difficult

to distinguish earnings management from a misstatement resulting

from error and/or fraud. Dechow and Skinner (2000) opines that

28

earnings management is the use of accounting choices which are

allowed by GAAP; conversely, fraudulent accounting is those

which do not comply with GAAP. Managed earnings are earnings

which do not result from a neutral treatment but from the use of

aggressive accounting or conservative accounting. In doing so, a

management has to alter real events or to choose accounting

choices. Kitiwong et.al., (2012) states adopting conservative or

aggressive accounting practices through purposely selecting

accounting estimations and assumptions is far preferable to through

structuring real transactions because, as remarked by Goncharov

(2005), operating earnings management is more costly than

accounting earnings management since it affects real cash flows.

Earnings management techniques are also divided into real

operating decisions and pure financial reporting decisions

(Schipper 1989, Peasnell, Pope and Young 2000, Ewert and

Wagenhofer 2005, and Kitiwong et al., 2012). Schipper (1989)

points out that real earnings management is designed to manage the

timing of decision-making on a company’s investments and

production while accounting earnings management is designed to

select accounting techniques allowed by GAAP. Ewert and

Wagenhofer (2005) explain that the management’s interpretation of

accounting standards with intent to make existing standards apply

to existing accounting events and transactions and/or with intent to

29

shift partial earnings between periods is one form of earnings

management. In terms of real earnings management, manager is

required to organize transactions or alter the timing of transactions

to help him/her transform bad news into good news.

The direction of earnings management can be in two

directions, income-increasing earnings management and income-

decreasing earnings management. These depend on a

management’s purpose in managing earnings. Empirical studies

document that management incentive to achieve high rewards, to

take advantage of specific circumstances and to report desirable

numbers are the major causes of earnings management. For

example, in order to maximize bonuses, management’s decision-

making to manage reported earnings upwards or downwards

depends on bonus conditions and the level of pre-managed

earnings. However he/she tends to reduce reported earnings in

order to maximize compensation in the future or to boost future

earnings. A management is likely to use income-decreasing

earnings management with the aim of gaining a government

assistance and protection, deferring earnings to the lower tax rate

period, writing all accruals off before a management’s leaving and

decreasing stock price before a management buyout. He/she

however attempts to report earnings upwards so as to increase

stock prices before stock-to-stock mergers. Smoothing reported

30

earnings is one form of earnings management; it occurs when a

management intentionally fights to smooth a fluctuation of

reported earnings. It leads a management to use income-increasing

and/or income-decreasing accruals. Avoiding reporting losses or

earnings drops and achieving analysts’ forecasts are also key

drivers that induce a management to engage in income-increasing

earnings management (Kitiwong et al., 2012).

Earnings management have been considered as one of the

methods used by the business leaders to mislead their stakeholders

to report unrealistic numbers, despite the various check and

balances (e.g. corporate governance code) on the process.

Nawaiseh (2016) stated that Investors in a company have vital

interest in the earnings reports, and company managers used

earnings management as a strategy to deliberately manipulate

company earnings to match a predetermined target and involves the

planning and execution of certain activities that manipulate or

smooth income, achieve high earnings level and sway the

company’s stock price. That is why “the position” of earning

management is between legal and illegal because if the

management do earning management for only their own interest

but not do it rightly, that earning management is done illegally and

influence the earning reports of a company.

31

In sum, earnings management occurs when management

intends to alter the neutral reporting process in order to report what

he/she wants, rather than to report neutral earnings. However,

neutral earnings (Dechow and Skinner, 2000) or un-managed

earnings (Burgstahler and Dichev, 1997) or real/true earnings

(Copeland, 1968) are difficult to measure and define. This leads to

the problem of how managed earnings are distinguished from

neutral earnings. In essence, discretionary accruals, abnormal

accruals or managed accruals are used to estimate managed

earnings (Kitiwong et al., 2012).

4. Earning Quality

Earnings quality is a central topic in financial accounting

research. Dechow et.al (2010) define earning quality is higher

quality earnings provide more information about the features of a

firm’s financial performance that are relevant to a specific decision

made by a specific decision-maker. And recording to Schipper and

Vincent (2003) the definition of earning quality is an expansion,

where income statement was reported appropriately and in which

there a change of economic assets out of the transactions with the

owner. The terms “quality of earnings” and “earnings quality” have

no single, agreed-upon meaning. Both terms are used when making

accounting choices; considering the business cycle, including

timing of transactions; and discussing earnings management. Some

32

use “quality of earnings” to mean the degree to which

management’s choices of accounting estimates can affect reported

income (these choices occur every period). Some who refer to

“earnings quality” suspect that manager usually will make choices

that enhance current earnings and present the firm in the best light,

regardless of the firm’s ability to generate future, similar earnings

(Weil, 2009).

Dechow and Schrand (2004) stated that the objectives of

financial analysis are to evaluate the performance of the company,

to assess the extent to which current performance is indicative of

future performance, and based on this analysis, to determine

whether the current stock price reflects intrinsic firm value. From

this perspective, a high-quality earnings number is one that

accurately reflects the company’s current operating performance, is

a good indicator of future operating performance, and is a useful

summary measure for assessing firm value. We define earnings to

be of high quality when the earnings number accurately annuitizes

the intrinsic value of the firm. Such earnings are referred to as

“permanent earnings” in the accounting literature (e.g., Black

1980; Beaver 1998; Ohlson and Zhang 1998). Another way to

think about this concept is that earnings are of high quality when

return on equity is a good measure of the internal rate of return on

the company’s current portfolio of projects. An earnings number

33

that represents the annuity of expected future cash flows is likely to

be both persistent and predictable. Persistence and predictability in

earnings alone, however, are not sufficient to indicate that earnings

are high quality. Managers often want earnings to be highly

persistent and predictable because these characteristics can

improve their reputations with analysts and investors. If such

earnings do not annuitize the intrinsic value of the firm, however,

the earnings are low quality. Earnings quality can vary among

companies as a function of accruals even in the absence of

intentional earnings manipulation. Unlike the determination of cash

flows, the determination of earnings requires estimations and

judgments, and some companies require more forecasts and

estimates than others (Dechow and Schrand, 2004).

B. Previous Research

Below are the results from several researches from several

researchers which became the references of this study. The results can be

seen in Table.2.1 below:

34

Table.2.1

Previous Research

No Title

(Researcher,

year)

Research Methodology Research Results

Differentiation Similarities

1 The Impact of

Audit Quality

Features on

Enhancing

Earnings

Quality: The

Evidence of

Listed

Manufacturing

Firms at Amman

Stock Exchange

(Mohammad

Abdallah

Almomani,

2015)

Not use earning

management as

an intervening

variable and

evidence is not

from Indonesia

Stock

Exchange. The

study use

indicators of

quality of audit,

audit office

size, period of

customer's

retention, type

of auditor's

opinion, and the

specialization in

client's industry,

were used to

measure audit

quality

Use audit

quality and

earning

quality as

variables,

used audit

fees as an

audit quality

measurement

and also use

earning of

continuity as a

measurement

of earning

quality and

also used

hypotheses

testing

The study finds

that the earnings of

listed

manufacturing

firms at Amman

Stock Exchange

are with good

quality, and that

there is a linear

relationship

between external

audit quality and

the quality of

reported earnings.

Auditors' fees have

most important

significant effect

on earnings

quality, followed

by auditors'

opinion, where

others factors has

no significant

effect on earnings

quality.

2 Impact of

External Audit

Quality on

Earnings

Management by

Banking Firms:

Evidence from

Jordan

(Mohammad

Ebrahim

Nawaiseh, 2016)

Not use earning

quality as

dependent

variable and not

use earning

management as

an intervening

variable, used

Audit tenure

(AT) and the

international big

audit firms

(INT) as audit

quality

Use audit

quality and

earning

management

as variables,

used audit

fees as audit

quality

measurement

and used

discretionary

accruals as a

measurement

of earning

Audit tenure (AT),

audit fees (AF),

and the

international big

audit firms (INT)

have significant

relations with

earning

management. It

means, future

earning

management

forecast is

predictable based

Continue on the next page

35

Table.2.1 (Continuous)

No Title

(Researcher,

year)

Research Methodology Research Results

Differentiation Similarities

measurements management on audit quality

leading indicators

(audit tenure, audit

fee, and

international big

audit firms). In

addition to

company size, that

is, when external

auditing is

conducted, earning

management

mitigates.

Moreover, no

relationship is

found between

Leverage, ROA,

CFO, and Earning

management

3 The effect of

Audit Quality on

Earning Quality

provided by

Dutch public and

private firms

(Mariska

Pupperhart,

2012)

Not use earning

management as

an intervening

variable, used

utilizing

conservatism as

a measure of

earnings quality

and auditor size

as a measure of

audit quality

Use audit

quality and

earning

quality as

variables also

use public

companies as

sample of

study

High audit quality

enhances

confidence in the

integrity of the

financial reporting

and reduces the

risk attached,

which lead to high

earnings quality

4 Impact of Audit

Quality on

Earnings

Management:

Evidence from

Iran

(Mahdi Safari

Gerayli,

Abolfazl

Earning quality

is not use as

variables and

use earning

management

not as

intervening

variable, used

auditor size,

Use audit

quality and

earning

management

as variables,

used

discretionary

accruals as a

measurement

The results reveal

that discretionary

accruals are

negatively related

to auditor size and

auditor industry

specialization The

study also findings

the negative

Continue on the next page

36

Table.2.1 (Continuous)

No Title

(Researcher,

year)

Research Methodology Research Results

Differentiation Similarities

Momeni

Yanesari, and

Ali Reza

Ma'atoofi, 2011)

auditor industry

specialization

and auditor

Independence

as measurement

of audit quality

of earning

management

association

between auditor

independence and Discretionary

Accruals. Overall,

this study provides

evidence that firms

which are audited

by high quality

auditors are more

likely to have less

Discretionary

accruals

5 Earnings

management and

the effect of

earnings quality

in relation to

stress level and

bankruptcy level

of Chinese listed

firms

(Feng Li, Indra

Abeysekera, and

Shiguang Ma,

2011)

Not use audit

quality as

variable and not

use earning

management as

intervening

variable, used

measurements

of earning

quality by four

separate

earnings

attributes:

accruals quality,

earnings

persistence,

earnings

predictability,

and earnings

smoothness

Use earning

management

and earning

quality as

variables and

using

Discretionary

Accruals as a

measurement

of earning

management

The study finds

that the stressed/

bankrupt firms

prefer

opportunistic

earnings

management; the

non-stressed /non-

bankrupt firms are

more likely to

choose more

efficient earnings

management than

the stressed/ non-

Bankrupt firms.

They find that

earnings

management

performs better

than earnings

quality in

predicting future

profitability. And

they also find that

the earnings

quality has

deteriorated over

Continue on the next page

37

Table.2.1 (Continuous)

No Title Research Methodology Research

Results Differentiation Similarities

the sample

period; the

number of

stressed/

bankrupt firms

increased and the

number of non-

stressed/non-

bankrupt firms

decreased

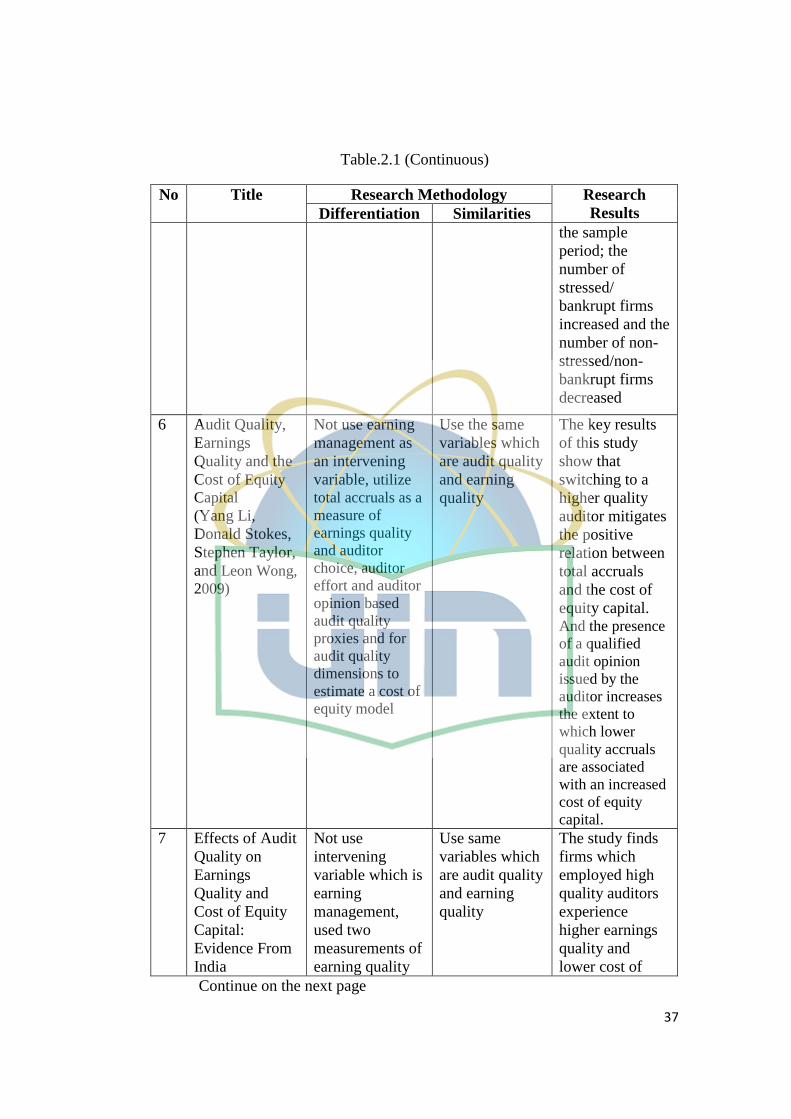

6 Audit Quality,

Earnings

Quality and the

Cost of Equity

Capital

(Yang Li,

Donald Stokes,

Stephen Taylor,

and Leon Wong,

2009)

Not use earning

management as

an intervening

variable, utilize

total accruals as a

measure of

earnings quality

and auditor

choice, auditor

effort and auditor

opinion based

audit quality

proxies and for

audit quality

dimensions to

estimate a cost of

equity model

Use the same

variables which

are audit quality

and earning

quality

The key results

of this study

show that

switching to a

higher quality

auditor mitigates

the positive

relation between

total accruals

and the cost of

equity capital. And the presence

of a qualified

audit opinion

issued by the

auditor increases

the extent to

which lower

quality accruals

are associated

with an increased

cost of equity

capital.

7 Effects of Audit

Quality on

Earnings

Quality and

Cost of Equity

Capital:

Evidence From

India

Not use

intervening

variable which is

earning

management,

used two

measurements of

earning quality

Use same

variables which

are audit quality

and earning

quality

The study finds

firms which

employed high

quality auditors

experience

higher earnings

quality and

lower cost of

Continue on the next page

38

Table.2.1 (Continuous)

No Title

(Researcher,

year)

Research Methodology Research

Results Differentiation Similarities

(Noor Houqe,

Kamran

Ahmed, and

Tony Van, )

which one is

income

smoothing,

using

discretionary

accruals as a

measurement of

earning quality,

and also use cost

of equity capital

as variable

equity capital.

The study result

show that audit

quality will have

a positive effect

on earnings

quality (reducing

discretionary

accruals) and

income

smoothing.

8 The influence

of Corporate

Governance

towards Earning

Quality:

Earning

Management as

an Intervening

Variable

(Singgih Aji

Taruno, 2013)

Not use audit

quality as a

variable, using

corporate

governance

mechanism

(proportion of

independent

board

commissaries

and institutional

ownerships) as

variable

Use earning

quality as

independent

variable and

also use earning

management as

an intervening

variable, use

annual report as

sample, using

same collection

data method

through

documentary

method and also

use path

analysis as an

analysis method

Partial test

results shows

that corporate

governance

mechanisms

affect the quality

of earnings but

do not affect the

earnings

management.

The test results

of path analysis

showed that

earnings

management is

not an

intervening

variable between

corporate

governance

mechanisms on

the quality of

earnings,

because the

direct effect is

greater than the

indirect effects

through earning

management

Continue on the next page

39

Table.2.1 (Continuous)

No Title

(Researcher,

year)

Research Methodology Research

Results Differentiation Similarities

9 Earnings

Management,

Audit Quality

and Legal

Environment:

An International

Comparison

(Mehmet Ünsal

Memiş & Emin

Hüseyin

Çetenak, 2012)

Not use earning

quality as

variable, not use

earning

management as

an intervening

variable, and

using Big4 and

non-Big4 audit

firms as audit

quality proxy

Use audit

quality and

earning

management as

variables, using

discretionary

accruals as a

measurement of

earning

management

From 8 emerging

countries as

samples, only for

Brazilian and

Mexican

companies, there

is significant

relationship

between the

discretionary

accruals and

audit quality. For

the other

countries there is

not significant

relationship.

Along with

results, the big

four auditors do

not constrain the

earnings

management

incentives in

every emerging

Country

10 Earnings

management

and the effect of

earnings quality

in relation to