the contact lens industry: structure, competition, and

TRANSCRIPT

The Contact Lens Industry: Structure,Competition, and Public Policy

December 1984

NTIS order #PB85-204451

LIBRARYOF TECHNOLOGY ASSESSMENT

HEALTH TECHNOLOGY CASE STUDY 31

The Contact Lens IndustryStructure, Competition, and

Public Policy

This case study was

Federal Policies

DECEMBER 1984

performed

and the

as part of OTA’s Assessment of

Medical Devices Industry

Prepared for OTA by:Leonard G. Schifrin, Ph.D.

Department of Economics, College of William and Mary, Williamsburg, VAand

Department of Preventive Medicine, Medical College of VirginiaVirginia Commonwealth University, Richmond, VA

with

William J. Rich, A.B.Department of Economics, College of William and Mary, Williamsburg, VA

OTA Case Studies are documents containing information on a specific medical tech-nology or area of application that supplements formal OTA assessments. The materialis not normally of as immediate policy interest as that in an OTA Report, nor doesit present options for Congress to consider.

Recommended Citation:Schifrin, Leonard G., with Rich, William J., The Contact Lens Industry: Structure, Com-petition, and Public Policy (Health Technology Case Study 31), OTA-HCS-31, Washington,DC: U.S. Congress, Office of Technology Assessment, November 1984. This case studywas performed as part of OTA’s assessment of Federal Policies and the Medical DevicesIndustry.

Library of Congress Catalog Card Number 84-601157

For sale by the Superintendent of DocumentsU.S. Government Printing Office, Washington, DC 20402

Preface

The Contact Lens Industry: Structure, Com-petition, and Public Policy is Case Study 31 inOTA’s Health Technology Case Study Series. Thiscase study has been prepared in connection withOTA’s project on Federal Policies and the MedicalDevices Industry, which was requested by theSenate Committee on Labor and Human Resourcesand endorsed by the Senate Committee on Veter-ans’ Affairs. A listing of other case studies in theseries is included at the end of this preface.

OTA case studies are designed to fulfill twofunctions. The primary purpose is to provideOTA with specific information that can be usedin forming general conclusions regarding broaderpolicy issues. The first 19 cases in the Health Tech-nology Case Study Series, for example, were con-ducted in conjunction with OTA’s overall projecton The Implications of Cost-Effectiveness Anal-ysis of Medical Technology. By examining the 19cases as a group and looking for common prob-ems or strengths in the techniques of cost-effec-tiveness or cost-benefit analysis, OTA was ableto better analyze the potential contribution thathose techniques might make to the managementof medical technology and health care costs andquality.

The second function of the case studies is toprovide useful information on the specific tech-nologies covered. The design and the funding lev-els of most of the case studies are such that theyshould be read primarily in the context of the as-sociated overall OTA projects. Nevertheless, inmany instances, the case studies do represent ex-pensive reviews of the literature on the efficacy,safety, and costs of the specific technologies ands such can stand on their own as a useful contri-bution to the field.

Case studies are prepared in some instances be-cause they have been specifically requested byCongressional committees and in others becausethey have been selected through an extensive re-view process involving OTA staff and consulta-tions with the congressional staffs, advisory panel the associated overall project, the Health Pro-gram Advisory Committee, and other experts invarious fields. Selection criteria were developedto ensure that case studies provide the following:

● examples of types of technologies by func-

●

●

●

●

●

●

●

tion (preventive, diagnostic, therapeutic, andrehabilitative);examples of types of technologies by physicalnature (drugs, devices, and procedures);examples of technologies in different stagesof development and diffusion (new, emerg-ing, and established);examples from different areas of medicine(e.g., general medical practice, pediatrics,radiology, and surgery);examples addressing medical problems thatare important because of their high frequen-cy or significant impacts (e.g., cost);examples of technologies with associated highcosts either because of high volume (for low-cost technologies) or high individual costs;examples that could provide information ma-terial relating to the broader policy and meth-odological issues being examined in theparticular overall project; andexamples with sufficient scientific literature.

Case studies are either prepared by OTA staff,commissioned by OTA and performed under con-tract by experts (generally in academia), or writ-ten by OTA staff on the basis of contractors’papers.

OTA subjects each case study to an extensivereview process. Initial drafts of cases are reviewedby OTA staff and by members of the advisorypanel to the associated project. For commissionedcases, comments are provided to authors, alongwith OTA’s suggestions for revisions. Subsequentdrafts are sent by OTA to numerous experts forreview and comment. Each case is seen by at least30 reviewers, and sometimes by 80 or more out-side reviewers. These individuals may be fromrelevant Government agencies, professional so-cieties, consumer and public interest groups, med-ical practice, and academic medicine. Academi-cians such as economists, sociologists, decisionanalysts, biologists, and so forth, as appropriate,also review the cases.

Although cases are not statements of officialOTA position, the review process is designed tosatisfy OTA’s concern with each case study’sscientific quality and objectivity. During the vari-ous stages of the review and revision process,therefore, OTA encourages, and to the extentpossible requires, authors to present balanced in-formation and recognize divergent points of view.

,..111

—

Health Technology Case Study Seriesa

Case Study Case study title; author(s); Case Study Case study title; author(s);Series No. OTA publication numberb Series No. OTA publication numberb

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Formal Analysis, Policy Formulation, and End-Stage RenalDisease;

Richard A. Rettig (OTA-BP-H-9(1))C

The Feasibility of Economic Evaluation of Diagnostic Pro-cedures: The Case of CT Scanning;

Judith L, Wagner (OTA-BP-H-9(2))Screening for Colon Cancer: A Technology Assessment;

David M. Eddy (OTA-BP-H-9(3))Cost Effectiveness of Automated Multichannel ChemistryAnalyzers;

Milton C. Weinstein and Laurie A. Pearlman(OTA-BP-H-9(4))

Periodontal Disease: Assessing the Effectiveness and Costs ofthe Keyes Technique;

Richard M. Scheffler and Sheldon Rovin(OTA-BP-H-9(5))

The Cost Effectiveness of Bone Marrow Transplant Therapyand Its Policy Implications;

Stuart O. Schweitzer and C. C. Scalzi (OTA-BP-H-9(6))Allocating Costs and Benefits in Disease Prevention Programs:An Application to Cervical Cancer Screening;

Bryan R. Luce (Office of Technology Assessment)(OTA-BP-H-9(7))

The Cost Effectiveness of Upper Gastrointestinal Endoscopy;Jonathan A. Showstack and Steven A. Schroeder(OTA-BP-H-9(8))

The Artificial Heart: Cost, Risks, and Benefits;Deborah P. Lubeck and John P. Bunker(OTA-BP-H-9(9))

The Costs and Effectiveness of Neonatal Intensive Care;Peter Budetti, Peggy McManus, Nancy Barrand, andLu Ann Heinen (OTA-BP-H-9(10))

Benefit and Cost Analysis of Medical Interventions: The Caseof Cimetidine and Peptic Ulcer Disease;

Harvey V. Fineberg and Laurie A. Pearlman(OTA-BP-H-9(11))

Assessing Selected Respiratory Therapy Modalities: Trends andRelative Costs in the Washington, D.C. Area;

Richard M. Scheffler and Morgan Delaney(OTA-BP-H-9(12))

Cardiac Radionuclide Imaging and Cost Effectiveness;William B. Stason and Eric Fortess (OTA-BP-H-9(13))

Cost Benefit/Cost Effectiveness of Medical Technologies: ACase Study of Orthopedic Joint Implants;

Judith D. Bentkover and Philip G. Drew (OTA-BP-H-9(14))Elective Hysterectomy: Costs, Risks, and Benefits;

Carol Korenbrot, Ann B. Flood, Michael Higgins,Noralou Roos, and John P. Bunker (OTA-BP-H-9(15))

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

The Costs and Effectiveness of Nurse Practitioners;Lauren LeRoy and Sharon Solkowitz (OTA-BP-H-9(16))

Surgery for Breast Cancer;Karen Schachter Weingrod and Duncan Neuhauser(OTA-BP-H-9(17))

The Efficacy and Cost Effectiveness of Psychotherapy;Leonard Saxe (Office of Technology Assessment)(OTA-BP-H-9(18))d

Assessment of Four Common X-Ray Procedures;Judith L. Wagner (OTA-BP-H-9(19))e

Mandatory Passive Restraint Systems in Automobiles: Issuesand Evidence;

Kenneth E. Warner (OTA-BP-H-15(20))f

Selected Telecommunications Devices for Hearing-ImpairedPersons;

Virginia W. Stern and Martha Ross Redden(OTA-BP-H-16(21))g

The Effectiveness and Costs of Alcoholism Treatment;Leonard Saxe, Denise Dougherty, Katharine Esty,and Michelle Fine (OTA-HCS-22)

The Safety, Efficacy, and Cost Effectiveness of TherapeuticApheresis;

John C. Langenbrunner (Office of Technology Assessment

(OTA-HCS-23)Variation in Length of Hospital Stay: Their Relationship toHealth Outcomes;

Mark R. Chassin (OTA-HCS-24)Technology and Learning Disabilities;

Candis Cousins and Leonard Duhl (OTA-HCS-25)Assistive Devices for Severe Speech Impairments;

Judith Randal (Office of Technology Assessment)(OTA-HCS-26)

Nuclear Magnetic Resonance Imaging Technology: A ClinicalIndustrial, and Policy Analysis;

Earl P. Steinberg and Alan Cohen (OTA-HCS-27)Intensive Care Units (ICUs): Clinical Outcomes, Costs, anDecisionmaking;

Robert A. Berenson (OTA-HCS-28)The Boston Elbow;

Sandra J. Tanenbaum (OTA-HCS-29)The Market for Wheelchairs: Innovations and Federal Policy

Donald S. Shepard and Sarita L. Karen (OTA-HCS-30The Contact Lens Industry: Structure, Competition, and PublicPolicy

Leonard G. Schifrin with William J. Rich (OTA-HCS-3)

aAvailable for sale by the Superintendent of Documents, U.S. Government dBackground paper #3 to The Implications of Cost-Effectiveness AnalysisPrinting Office, Washington, DC, 20402, and by the National Technical Medical Technology.Information Service, 5285 Port Royal Rd., Springfield, VA, 22161. Call eBackground Paper #5 to The Implications of Cost-Effectiveness AnalysisOTA’s Publishing Office (224-8996) for availability and ordering infor- Medical Technology.

fBackground paper #1 to OTA’s May 1982 report Technology and Hanmation.bOriginal publication numbers appear in parentheses. capped People.cThe first 17 cases in the series were 17 separately issued cases in Background gBackground Paper #2 to Technology and Handicapped People.Paper #2: Case Studies of Medical Technologies, prepared in conjunctionwith OTA’s August 1980 report The Implications of Cost-Effectiveness Anal-ysis of Medical Technology.

OTA Project Staff for Case Study #31

Roger Herdman, Assistant Director, OTAHealth and Life Sciences Division

Clyde J. Behney, Health Program Manager

Jane E. Sisk, Project Director

Lawrence H. Miike, Senior Associate

Katherine E. Locke, Research Assistant

H. Christy Bergemann, Editor

Virginia Cwalina, Administrative Assistant

Rebecca I. Erickson, Secretary/Word Processor Specialist

Brenda Miller, Word Processor/P. C. Specialist

.-

Advisory Panel for Federal Policies andthe Medical Devices Industry

Richard R. Nelson, ChairInstitute for Social and Policy Studies, Yale University

New Haven, CT

William F. BallhausInternational Numatics, Inc.Beverly Hills, CA

Ruth FarriseyMassachusetts General HospitalBoston, MA

Peter Barton HuttCovington & BurlingWashington, DC

Alan R. KahnConsultantCincinnati, OH

Grace KraftKidney Foundation of the Upper MidwestCannon Falls, MN

Joyce LashofSchool of Public HealthUniversity of CaliforniaBerkeley, CA

Penn LupovichGroup Health AssociationWashington, DC

Victor McCoyParalyzed Veterans of AmericaWashington, DC

Robert M. MoliterMedical Systems DivisionGeneral Electric Co.Washington, DC

Louise B. RussellThe Brookings InstitutionWashington, DC

Earl J. SaltzgiverForemost Contact Lens Service, Inc.Salt Lake City, UT

Rosemary StevensDepartment of History and Sociology of ScienceUniversity of PennsylvaniaPhiladelphia, PA

Allan R. ThiemeAmigo Sales, Inc.Albuquerque, NM

Eric von HippelSloan SchoolMassachusetts Institute of TechnologyCambridge, MA

Edwin C. WhiteheadTechnicon Corp.Tarrytown, NY

Contents

PageCHAPTER 1: SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

CHAPTER 2: THE DEVELOPMENT OF CONTACT LENSES . . . . . . . . . . . . . . . . . . . . 9

CHAPTER 3: TYPES OF CONTACT LENSES AND THEIR CHARACTERISTICS . . 15Hard PMMA Lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Soft Lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Gas-Permeable Lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Present Usage and Future Trends... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

CHAPTER 4: WEARERS, PRICES, AND SOURCES OF PAYMENT . . . . . . . . . . . . . . 23Wearers of Contact Lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Sources of Payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

CHAPTER 5: PRODUCERS OF CONTACT LENSES.. . . . . . . . . . . . . . . . . . . . . . . . . . . 31

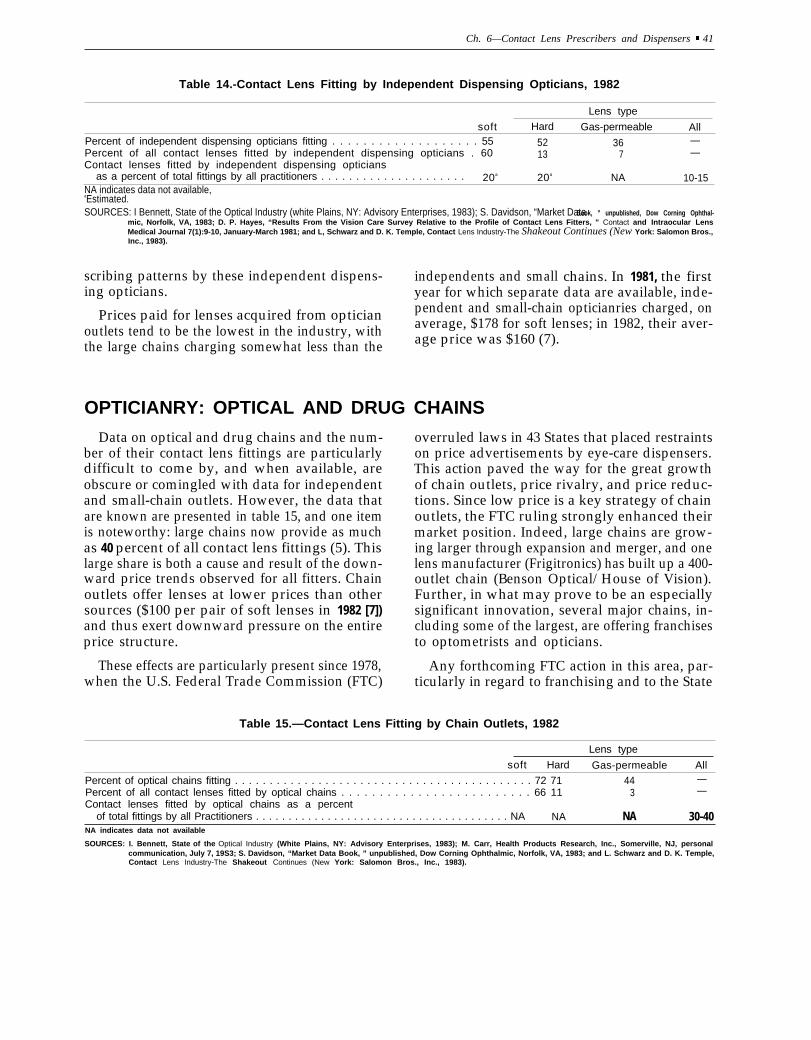

CHAPTER 6: CONTACT LENS PRESCRIBERS AND DISPENSERS. . . . . . . . . . . . . . . 39Ophthalmologists . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Optometrists . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Opticianry: Independent Optical Outlets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Opticianry: Optical and Drug Chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41The Marketing of Contact Lenses to Dispensers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

CHAPTER 7: THE ROLE OF FEDERAL POLICY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47General Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Patents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47The Maintenance of Market Competition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Mergers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48State Commercial Practice Restraints. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

FDA Regulatory Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51The Origins, Development, and Scope of FDA Authority Over Contact Lenses . . . 51The Effects of the Present System of Regulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

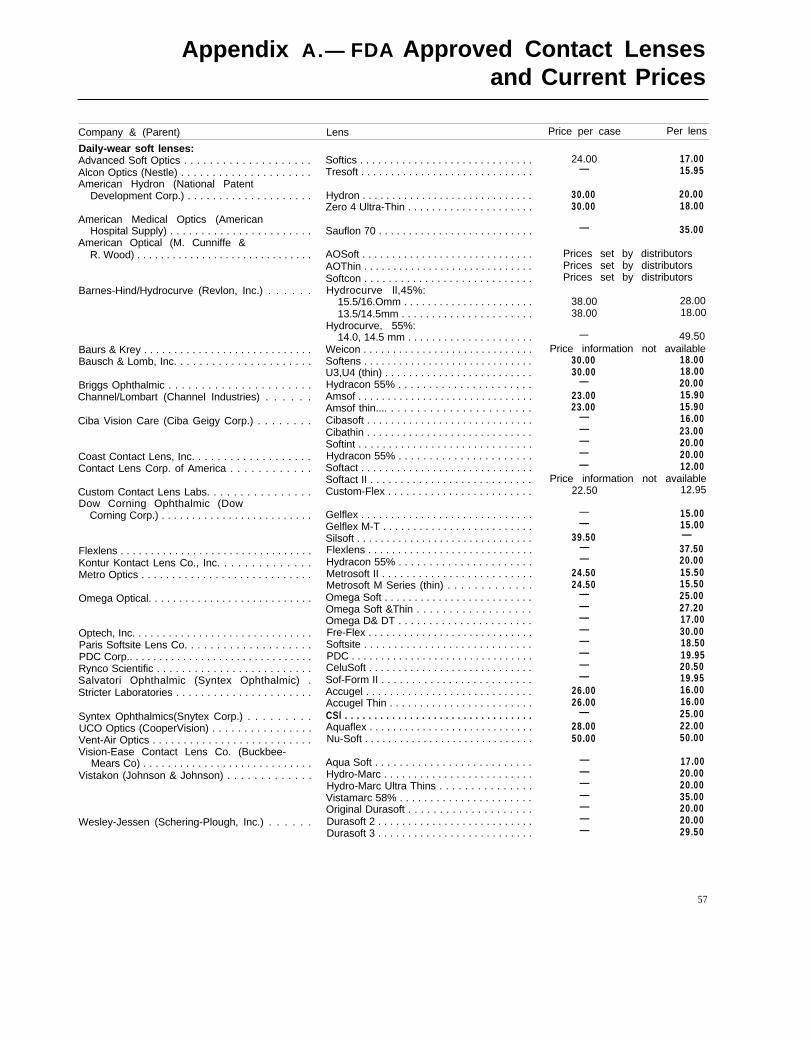

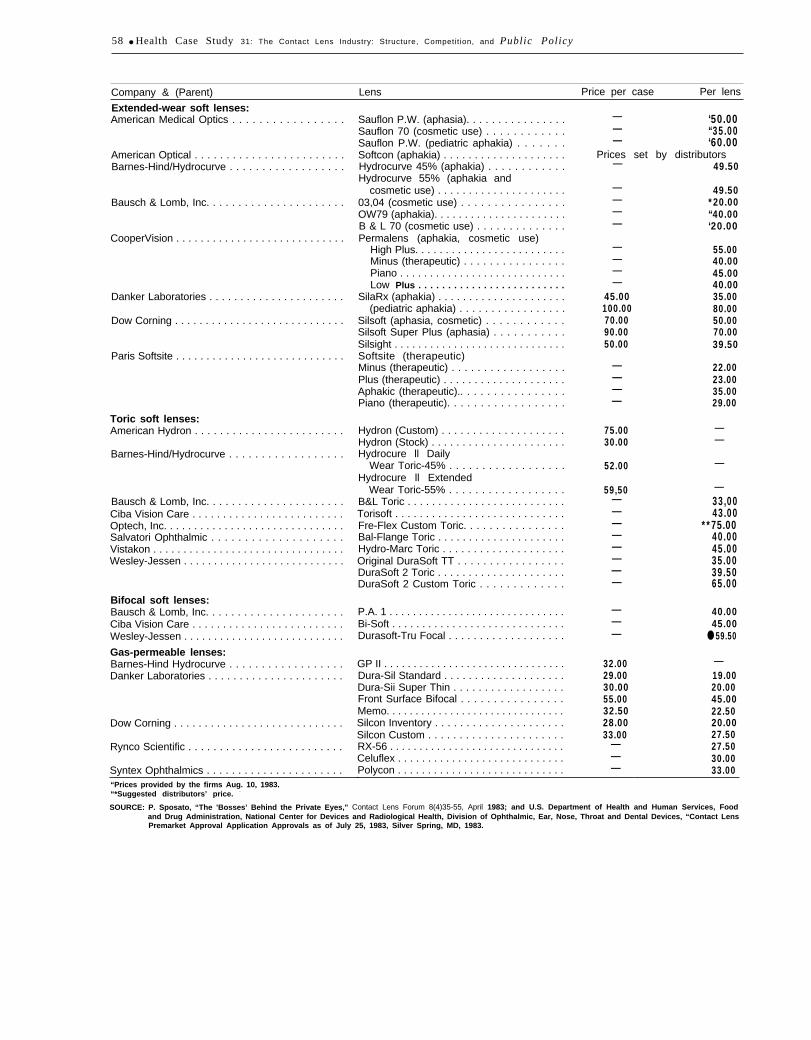

APPENDIX A.– FDA APPROVED CONTACT LENSES AND CURRENT PRICES.. 57

APPENDIX B.– MAJOR CONTACT LENS MANUFACTURERS, METHODS OFENTRY, AND ACQUISITIONS AND LICENSE AGREEMENTS . . . . . . . . . . . . . . . . 59

APPENDIX C.– GLOSSARY OF TERMS AND ACRONYMS . . . . . . . . . . . . . . . . . . . . 62

APPENDIX D.– ACKNOWLEDGMENTS AND HEALTH PROGRAMADVISORY COMMITTEE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

REFERENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

Tables

Table No. Pagel. Summary of the Historical Development of Contact Lenses . . . . . . . . . . . . . . . . . . . 92. Persons Wearing Corrective Lenses: 1966, 1971, and 1977. . . . . . . . . . . . . . . . . . . . . 173. Persons Wearing Corrective Lenses: 1970, 1975, 1978-82 . . . . . . . . . . . . . . . . . . . . . . 184. Share of U.S. Contact Lens Market by Lens Type, 1978-87. . . . . . . . . . . . . . . . . . . . 18

vii

—————

Contents—continuedTable No. Page5.

6.

7.

8.9.

10.

11.

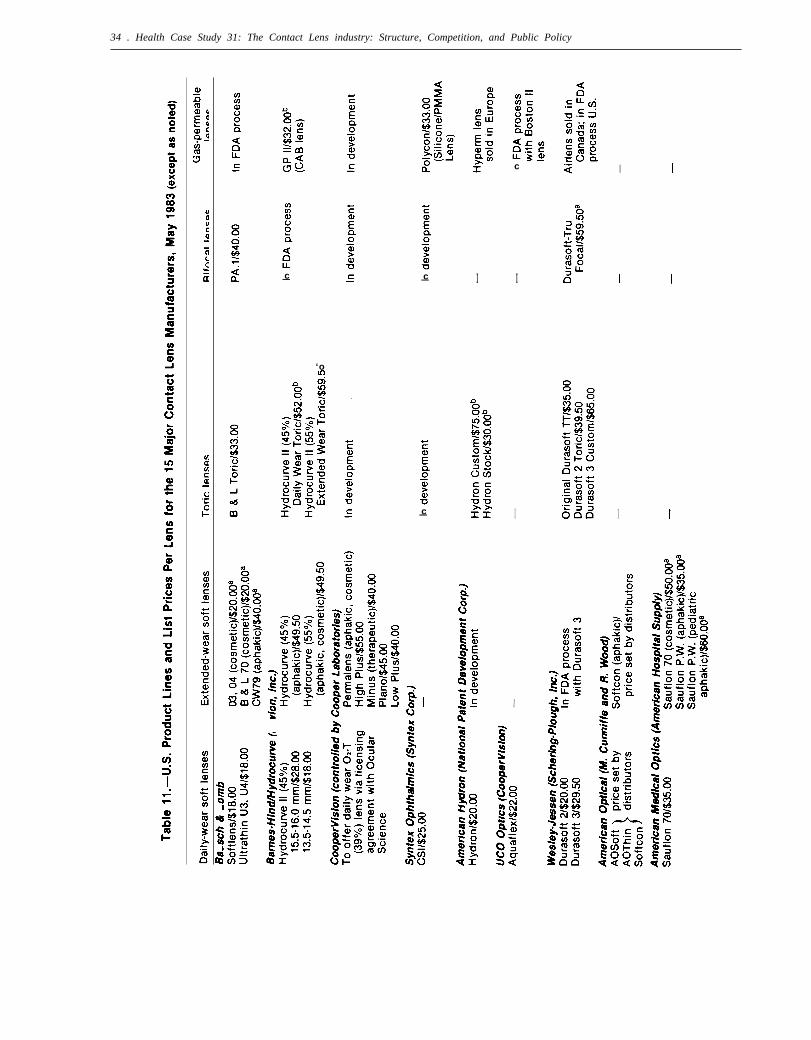

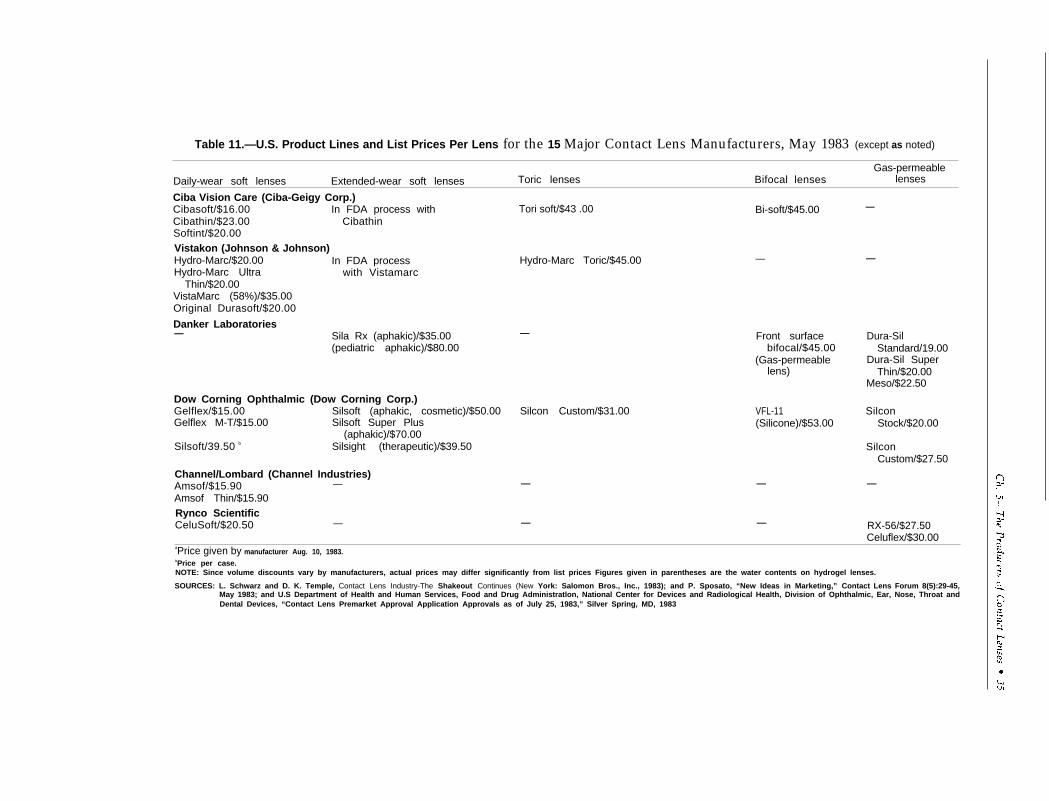

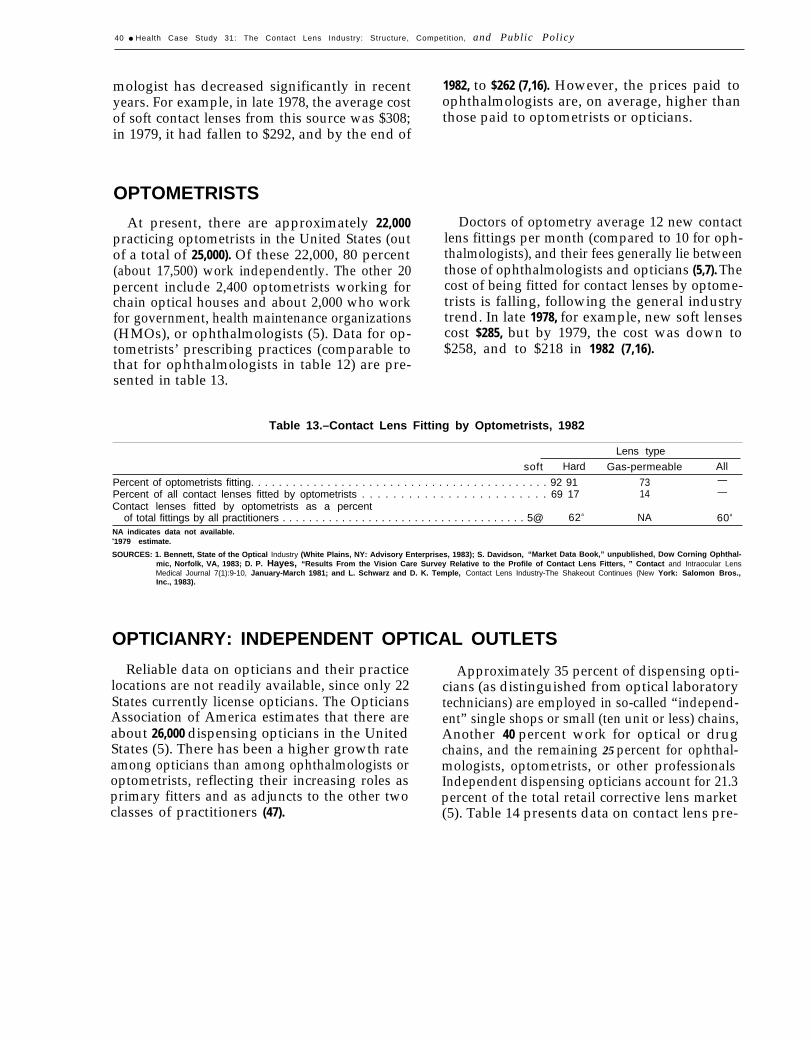

12.13.14.15.16.17.

Contact Lens Wearers, Percent of Population, by Sex and Age,1965-66, 1971, and 1979-80. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Purchase or Repair of Contact Lenses per 1,000 Population at DifferentFamily Income Levels, 1977 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Average Soft Contact Lens List and Total Fitting Prices, per Pair, 1971-82,Selected Years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Market Shares and Concentration Ratios, Soft Lenses, 1978-82 . . . . . . . . . . . . . . . . 31Market Shares and Concentration Ratios, Gas-Permeable Lenses, 1979-82 . . . . . . . 31Worldwide Sales, Profit, and R&D Data of the 17 Major Firms in theContact Lens Industry, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33U.S. Product Lines and List Prices Per Lens for the 15 Major Contact LensManufacturers, May 1983 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34Contact Lens Fittingly Ophthalmologists, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Contact Lens Fitting by Optometrists, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Contact Lens Fitting by Independent Dispensing Opticians, 1982 .........,., . . . 41Contact Lens Fitting by Chain Outlets, 1982. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Major Optical Chains and Number of Outlets, 1982 . . . . . . . . . . . . . . . . . . . . . . . . . . 42Contact Lens Fitting by Opticians: Survey of State Limitations . . . . . . . . . . . . . . . . 49

. . .Viii

OTA Note

These case studies are authored works commissioned by OTA. Each authoris responsible for the conclusions of specific case studies. These cases are not state-ments of official OTA position. OTA does not make recommendations or endorseparticular technologies. During the various stages of review and revision, therefore,OTA encouraged the authors to present balanced information and to recognizedivergent points of view.

25-339 0 - 84 - 2 : QL 3

1

Summary

This study presents an analysis of the contactlens industry in the United States, emphasizingthe role of economics and public policy in shap-ing past and future development. The analysis fol-lows the general format usually employed in suchindustry studies: 1) the evolution and present con-figuration of the structural and institutional fea-tures, including public policy, that define the con-tact lens industry; 2) the corporate strategies andpolicies conditioned by this operational context;and 3) the end results of these strategies and pol-icies in terms of the technical improvement of con-tact lenses, the ways of making them, and theprices at which they are sold.

In following this general format, the study isboth descriptive and analytical. The descriptiveaspects include the historical evolution of contactlenses (ch. 2); the range of available lens types(ch. 3); the characteristics of wearers of contactlenses, how much they spend, and the sources ofpayment for these contact lenses expenditures (ch.4); the firms that make contact lenses (ch. 5); theeye-care professionals who represent the bridgebetween makers and users by prescribing and fit-ting contact lenses, and toward whom lens man-ufacturers direct most of their marketing efforts(ch. 6); and the regulatory context within whichthe entire manufacturing and selection processtakes place (ch. 7).

The first part of the analysis relates structureto behavior, or the influence that the number, size,market power, and policies of the makers of con-tact lenses have on their incentives and behaviorregarding competition in product developmentand price.

The second part of the analysis focuses on therole played by public policy in influencing thiscompetition, either directly or indirectly. Themore important elements of public policy affect:1) mergers, 2) market entry, 3) competition in theprofessional prescribing and fitting of contactlenses, and 4) the payment mechanism in the pur-chasing process.

Why is it important to know these features ofthe contact lens industry and how public policyaffects the industry’s operation, when the indus-try is quite small, with annual domestic sales atthe manufacturers’ level currently running about$350 million? First, the analysis of any industry,however small, provides another economic casestudy that adds to our knowledge of how indus-try structure and public policy affect the competi-tive behavior of firms in the marketplace. Second,the contact lens industry gives every indicationof growing considerably in the relatively nearfuture; thus, its record in product improvementand pricing will be increasingly important rela-tive to the full range of goods and services pro-duced in the economy. Third, the study of the ef-fects of public policy regarding the contact lensindustry can provide guidelines for the formula-tion of sound policies in the future toward thisindustry, and, in turn, by serving as a case study,for the formulation of effective policies to influ-ence the activities and performance results of otherindustries, both inside and outside the medicalsector.

Contact lenses are of three types, although thedistinctions between the types could conceivablydisappear in the future. The first type of moderncontact lens was the hard “PMMA” (for “poly-methylmethacrylate”) lens, made of plexiglass-type plastics. The advantages of this type are rela-tive rigidity (where flexing may be a problem),smallness, lightness, safety (minimal risk to theeyes), ease of precision-machining, ease of main-tenance, and durability. Their major disadvan-tage is that they are impermeable to oxygen andinterfere with the flow of oxygen to the cornea.For a sizable proportion of potential wearers, thisproblem may actually deter the wearing of PMMAlenses; for others, wearing time becomes limitedto a usual daily maximum of 8 to 16 hours.PMMA lens wearers may also incur “spectacleblur” when switching from lenses to glasses.

The second type of contact lens is made fromwater-absorbing plastics caIled “hydrogels” (mostly

3

4 ● Health case study 31: The Contact Lens Industry : Structure, competition, and Public Policy

“HEMA’’-for “hydroxyethylmethacrylate’’—hy-drogels, but other hydrogel materials are alsopopular) or soft silicone. Their water absorbencyand resulting softness make them considerablymore easy to adapt to and more comfortable forlonger periods, but the same characteristics makethem fragile, provide less acute vision correction,and may increase the likelihood of eye infectionsfrom handling and wearing.

The third type of lenses is gas permeable. Theselenses have much of the superior optical and ease-of-care qualities of hard lenses because of theirrigidity, and the comfort of soft lenses becausethey are oxygen permeable.

About 120 million people in the United Stateswear corrective eyeglasses and another 16 millionto 18 million use contact lenses, either exclusivelyor interchangeably with eyeglasses. Among allU.S. contact lens wearers, the use of hard lensesis declining and the use of soft and gas permeablelenses is increasing. For new fittings, hard lensesrepresent a minor share, soft lenses predominate,and gas permeable are the fastest growing. Forboth new fittings and replacements together, softlenses represent upwards of 75 percent of the totalmarket, probably their peak figure. Hard lenseshave 15 percent or less of the market, and gaspermeable at least 10 percent.

In the future, soft and gas-permeable lenses willaccount for almost all lens sales, perhaps aboutequally. There are some signs that a hybrid typeof lens, combining the best qualities of each type,may be emerging. If so, then this fourth type willbe “the” contact lens of the future. Whether ornot this hybrid is developed, contact lenses maybecome as common or even more common amethod of vision correction than eyeglasses, astheir comfort, wearability, applications, and ef-fectiveness continue to increase.

At present, contact lenses are particularly usefulin the correction of single vision problems, essen-tially myopia (nearsightedness) and hypermetropia(farsightedness). They are also useful in the cor-rection of astigmatism (a vision defect usuallyresulting from an irregular, nonsymmetrical con-formation of the cornea, which results in a lackof sharpness or evenness of focus) and presbyopia(the loss of flexibility in refocusing from near to

far objects, and vice versa) for which bifocal ormultifocal corrective lenses or monovision cor-rection is employed. These “disorders of refrac-tion and accommodation” rank very high amongphysical problems, as evidenced by patient visitsto all eye-care professional practitioners.

Certain interesting features exist in the patternof contact lens wearers. Unlike eyeglasses, con-tact lenses have been a “younger person’s” prod-uct. The traditional wearer has been the youngadult female. However, as the therapeutic applica-tions of contact lenses expand and consumer tastesare altered (partly by increased direct advertis-ing by manufacturers), contact lens usage amongmales and among older persons is increasingrapidly and the traditional orientation toward theyoung adult female is disappearing.

The absolute price of contact lenses of all typeshas fallen significantly in the past decade, a timeof high general inflation. Soft lens wholesale pricesnow are about half their mid-1970s level, and totalfitting prices are half or less of their early 1970slevel. Lens price reductions have resulted fromlarge-scale entry, excess capacity, and vigorousprice competition among manufacturers, particu-larly in the soft lens group. Total-fitting price re-ductions reflect these cuts in lens prices and theexpanded competition among lens fitters, particu-larly the large chain optical houses. Continuedprice competition is likely, and further price de-clines, if less dramatic, may occur in the future.

Unlike many categories of health care expend-itures, the largest proportion of payments for cor-rective lenses comes from patients, rather thanfrom private or public insurance. Although anumber of major collectively bargained employ-ment contracts provide vision-care benefits, suchcoverage applies only to a small proportion of allworkers, provides mainly for eyeglasses, and pro-vides only partial payment for contact lenseswhen they are covered. In the public sector, con-tact lenses are insured only for therapeutic, notcosmetic, use. (In a strict sense, all contact lensesthat offer vision correction or eye protection are“therapeutic” in use. However, contact lenses thatprovide correction or protection not achievablethrough the use of eyeglasses are commonly con-sidered “therapeutic” in use while those afford-

Ch. I—Summary ● 5

ing benefits also attainable through the wearingof eyeglasses are considered “cosmetic,” since, itis believed, the choice of contact lenses in the lattercases is made on the basis of appearance con-siderations. ) In practice, this means that contactlenses are provided under Medicare, Medicaid,and other public programs mainly in relation tocataract or other eye surgery. As a result of thisminimal role of third-party payment in the totalsource-of-payment pattern, insurance as a wholeand public programs in particular have little dis-cernible effect on contact lens usage, development,prices, or resource allocation patterns.

Although a large number of firms produce con-tact lenses, the manufacture of both soft and gaspermeable lenses is concentrated among a veryfew large firms. However, because of many fac-tors—e.g., the similarity of lenses within eachtype, the considerable substitutability and re-sulting competition among types, and excesscapacity—competition is active in both productdevelopment and price. Where market power ismost evenly distributed (hard lenses), price com-petition is greatest. Where large firms dominatebut are surrounded by a fringe of smaller firms(soft lenses), price competition is high. Where onlya few firms are in the market and one predomi-nates (gas permeable lenses), price competition,among groups if not within this group, is at leastobservable.

Yet public policy has not had benign effects onmarket competition. As a result, the degree ofcompetition is probably less than it otherwisewould be, and the gap between the actual and po-tential levels may widen in the future. To thepresent, the history of this industry shows theimportant role of small firms as generators of in-novational progress, service, and price rivalry.Yet the sector most open to small firms—hardroses - is becoming less important as time passes.n the soft-lens area, energetic small firms haveDifficulty entering the market, and mergers andacquisitions by large firms may eliminate manyof them. And small firms have the greatest diffi-culty in entering the fastest growing marketarea —gas-permeable lenses. The greatest poten-tial obstacle to the attainment of optimal prod-uct and price competition in the future is the U.S.Food and Drug Administration’s premarketing

approval policies, which have been especiallyburdensome to smaller firms. Restrictive marketapproval policies may be wise for significantlynew lens types, but once their effectiveness andsafety become established, more flexible approachestoward minor or closely similar new develop-ments seem warranted.

The study also examines the role of contact lensprescribers and dispensers (ophthalmologists, op-tometrists, and opticians) in the eye-care field.Ophthalmologists are medical doctors specializ-ing in eye care, and vision correction is a largepart of their activity. There are about 12,500ophthalmologists in the United States, of whom11,000 are involved in regular patient care. Op-tometrists, who are licensed to measure and fitcorrective lenses, outnumber ophthalmologists byroughly two-to-one, and fit proportionally morecorrective lenses. Opticians are usually limited tomaking contact lenses or to fitting them under thesupervision of an optometrist or ophthalmologist,but in some States they may measure for and fitcorrective lenses. There are an estimated 26,000dispensing opticians. Recent action by the U.S.Federal Trade Commission (FTC), however, hasexpanded the competitive roles of these dispens-ing opticians. The FTC requires all lens prescribersto provide copies of the prescription to the pa-tient, Thus, patients may take these prescriptionselsewhere, including to opticianries, for filling andfitting. State prohibitions against price competi-tion by corrective lens dispensers are also nolonger enforceable, and opticians have begun tocompete on the basis of price to fill corrective lensprescriptions written by others. Large chains, withinhouse optometrists and opticians, have been themost vigorously price competitive, both for fullprescribing and fitting, and for filling prescriptionsbrought in by patients. Accordingly, public pol-icy has been successful in providing strong com-petition in the fitting of contact lenses, which isdirectly advantageous to patients in the forms ofexpanded choices and lower prices, and indirectlyadvantageous by exerting a strong counteractingforce on any market power among lens manufac-turers.

Other Federal policies—tax, import, researchfunding, procurement—seem to have little, if any,effect on the contact lens industry. Patent policy

Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

is somewhat more important, but not critically approval requirements could suggest adjustmentsso. More importantly, the procompetitive effects in policies that would make mergers somewhatof enhancing competition among dispensers could more difficult to accomplish and market entrybe maximized subject, of course, to the mainte- considerably easier. Adoption of more flexiblenance of high-quality care. An assessment of the policies of premarket approval merits particulareffects of unhindered mergers and premarketing attention.

2.The Development of Contact Lenses1

The oft-told history of the development of con-tact lenses is an interesting one, and its highlightsare presented in table 1. The history usually beginswith the theories of Leonardo da Vinci that awater-filled glass “half circle” could neutralize therefractive (light bending) power of the cornea andsubstitute the refractive power of the curved glassto improve the clarity of the image received bythe retina. Leonardo suggested at least two dem-onstrations of his theory: 1) a water-filled glassbowl in which the person placed his or her face(presumably for brief periods) and looked throughthe bottom, and 2) a water-filled glass hemisphereactually worn over the eye and remarkably likea contact lens. His ideas far exceeded the abilityof his times to actually implement them. How-ever, he had correctly identified several key prin-ciples of contact lenses; neutralizing the refrac-tion of the natural cornea by means of an artificialsurface; substituting the refractive powers of a

1Except as noted, this discussion was drawn from: Graham, 1981(15); Lowther, 1982 (21); and Ruben, 1976 (30).

curved, clear lens in its place; and positioning thatlens directly on the eye.

Almost a century and a half later, the philos-opher-mathematician René Descartes suggestedplacing a lens at the end of a water-filled tube,the other end of which was placed on the corneaof the eye. His concept was not really practicalas such tubes would require external support, buttime has shown that his idea of placing the lensonly over the cornea instead of including the sclera(white portion of the eye), as Leonardo had pro-posed, was most perceptive.

In 1801, Thomas Young, an English scientist,actually made a rudimentary set of contact lenseson the model of Descartes. Using wax, he affixedwater-filled lenses to his eyes, neutralizing his ownrefractive power, then corrected for it with anotherpair of lenses. His optic device affirmed the prin-ciples formulated by both Leonardo and Descartes.

Next in the progression of the science of con-tact lenses was Sir John Herschel, an English

Table 1 .—Summary of the Historical Development of Contact Lenses

Year Individual(s) Development

1508163618011827

188718881888

1936

1938194719471950

196019681971

Leonardo da Vinci . . . . . . .René Descartes . . . . . . . . .Thomas Young . . . . . . . . . .John Herschel . . . . . . . . . .

F. A. Muller. . . . . . . . . . . . .A. E. Fick . . . . . . . . . . . . . .E. Kalt . . . . . . . . . . . . . . . . .

W. Feinbloom . . . . . . . . . . .

Mullen and Obrig . . . . . . . .N. Bier . . . . . . . . . . . . . . . . .K. Tuohy . . . . . . . . . . . . . . .Butterfield . . . . . . . . . . . . . .

Wichterle and Lim . . . . . . .

Bausch & Lomb . . . . . . . . .1970s J. DeCarle . . . . . . . . . . . . . .1970s Rynco Scientific . . . . . . . .1970s1978 Danker Laboratories . . . . .1979 Syntex Ophthalmic . . . . .

Described glass contact lensTube of water used to neutralize the corneaUsed Descartes’ principle to study the eyeDescribed how a contact lens could be ground; concept

of molding the eyeFitted a glass blown lens for a patient to protect the eyeDescribed first glass lens to be worn to correct visionDesigned and fitted glass corneal lenses; Used

ophthalmometer to fit lensesMade lens with glass central optic and plastic surround

(first plastic used in contact lens)First all-plastic (PMMA) contact lensFenestrated minimum-clearance haptic lensAll-plastic corneal lensDesigned corneal lens to parallel the cornea; used

peripheral curvesHydrogel polymers for contact lensesU.S. FDA became involved in regulating contact lensesFirst hydrogel lens approved in United StatesExtended wear with high water content hydrogel lensesUse of CAB polymer for contact lensesFirst clinical marketing of soft silicone lensesU.S. FDA approval of CAB lensesU.S. FDA approval of a PMMA-silicone copolymer lens

SOURCE: G. E. Lowther, Contact Lenses: Procedures and Techniques (Boston, MA: Butterworths, 1982)

9

10 ● Health Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

—

astronomer, who in the 1820s suggested principlesfor accurate lens grinding and fitting. His first con-tribution was to suggest grinding the inside cur-vature of a glass lens to conform as closely as pos-sible to an irregularly surfaced cornea, and theoutside curvature of the same lens to duplicatea normal cornea. He also proposed taking an ac-tual mold of the eye to use in rendering an ac-curate interior curvature fit and using a gel-likefilling for the cavity between the cornea and in-terior curve.

The actual making of contact lenses becamepossible as the necessary technological capabil-ities slowly emerged. The development of anes-thesia in 1884 allowed for making a mold of theshape of the eye, as proposed by Herschel. Ad-vances in optics, particularly precision glass blow-ing and lens grinding, made possible the accurateduplication in glass of the curvatures of the eye.Usable lenses thus were developed, but their firstapplications were for pathological conditions ofthe eye (as opposed to correcting a refraction er-ror), since only the correction of severe problemsjustified the wearing of these large, heavy, anduncomfortable devices, which were tolerable onlyfor brief periods. In Germany, F. A. Muller, amaker of artificial glass eyes, made a transparentlens in 1887 to protect a diseased eye that seemsto have worked for many years.

The following year, two important develop-ments occurred. A. E. Fick, a Swiss physician,employed a small glass bowl—more accurately,a segment of a glass sphere “bounded by concen-tric and parallel sphere segments’’—to correctrefractive errors. These appear to be the first truecontact lenses, and Fick went on to design anduse both corneal and scleral lenses. Concomitantadvances in lens making, led by the Zeiss enter-prise in Germany, made Fick’s work possible andallowed for further experimentation with contactlenses in Germany, Switzerland, and France. Forthe most part, however, such lenses were notcomfortable enough for much use in other thanpathological conditions such as keratoconus,where the pressure of the lens might help suppressthe conical distention of the cornea and protectit; other severe distortions of the cornea in whichcorrection by the use of spectacles was not possi-

ble; and in cases where the cornea needed pro-tection from infections and encrustations of theeyelids.

By the end of the 19th century, then, a plateauhad been reached in the progress of contact lenses.Fairly well-fitting and carefully made glass con-tact lenses were available but were used on alimited scale only for occasional therapeutic pur-poses. Glass, even thin-blown or finely ground,is relatively heavy. Thus, small lenses would notadhere reliably to the surface of the eye, and largelenses which extended under the eyelids impededthe lubrication of the cornea and the flow of ox-ygen (and carbon dioxide) because they wereessentially impermeable. The results of wearingthese large, scleral lenses were: discomfort, irrita-tion, swelling, and perhaps infection or otherdamage; the need for continuous and usually notsuccessful artificial lubrication of the eye; and/ora cycle of short-term wearing and longer rest peri-ods. Additionally, wearing highly fragile lensesin the eye was considerably dangerous, and theglass material itself was affected by tears. Theregular use of contact lenses for simple vision cor-rection, although nearer to reality than before,was not yet feasible. The development of contactlenses thus remained static at this point, waitingfor supporting technology to catch up.

This catchup took another half-century and ap-peared in the form of plastics, which overcamesome of the more serious limitations of glasslenses. Feinbloom, in the United States, was thefirst to use plastic in contact lenses. In 1936, heproduced a scleral lens by bonding the glass cor-neal portion to an opaque, molded resin scleralband. Obrig and Mullen, also working in theUnited States, made the first all-plastic sclerallenses in 1938, using a new material, polymethyl-methacrylate (PMMA), which was particularlyeasy to shape to ultra-thin dimensions and greatlysuperior to glass in safety, lightness, and work-ability. The step from plastic scleral to plastic cor-neal lenses was a short but difficult and impor-tant one and was accomplished by Tuohy in 1947,and the modern era of contact lenses had begun.

Tuohy and others, including Butterfield, madegreat progress in both the construction and de-sign of corneal plastic contact lenses. The results

Ch. 2—The Development of Contact Lenses ● 11

were a small, light lens of high optical quality anda design that conformed very closely to the shapeof the central cornea, but with a slight “stand off”at the edges for better tear spreading for greaterlubrication and oxygen delivery to the cornea. Asa result, PMMA or “hard” corneal contact lensesfor correcting refractive errors became commer-cially practical in the early 1950s, and for the nexttwo decades, they were virtually the only typeof lenses used.

The search for new lens materials and designswas partly spurred by the wide range of correc-tive and therapeutic requirements that one mate-rial and a few design configurations were unlikelyto serve, but more so by the limitations of PMMAfor routine refractive corrections. A serious limita-tion of PMMA is that because it is nonpermeable,oxygen-bearing tears may not be able to diffusethrough the lens to reach the cornea in sufficientquantity. Without oxygen, the cornea swells andmakes lens-wearing difficult. For many people,natural blinking and movement of the lens allowfor an oxygen supply adequate for upwards of 16hours of wear, so-called “daily” wear. But formany others, shorter wearing times and higherlevels of discomfort can be expected, perhaps tothe point of their forgoing lenses totally, especiallysince many wearers of contact lenses choose themover glasses essentially for cosmetic reasons.

If PMMA lenses represent the first generationof modern contact lenses, “soft” lenses, designedlargely to overcome the limitations of hard PMMAlenses, represent the second generation. For themost part, soft lenses are made of hydrophilic(water-absorbing) plastic materials called “hydro-gels.” The basic hydrogel plastic is hydroxyethyl-methacrylate (HEMA), although new hydrogelmaterials and other soft-lens plastics have recentlybeen developed. These plastics absorb water (asmuch as 85 to 90 percent by weight) and becomesoft and flexible in proportion to their absorbency.In 1960, Wichterle and Lim, Czechoslovakianchemists working with Dreifus, an ophthalmolo-gist, researched hydrogels, and with Dreifus beganto formulate hydrophilic contact lenses.

Although hydrogels have become the main typeof contact lenses currently on the market, theywere not a practical alternative to hard lenses for

a decade or more after their invention. Being softand permeable, they were comfortable on the eye,but their water content made them difficult tohandle, of poor optical quality, and raised ques-tions about the absorption of infectious bacteria.However, within several years, improved mate-rials and lens designs were formulated. After afew years of experimentation and improvement,Wichterle granted to National Patent Develop-ment Corp. (NPD), a U.S. firm, exclusive West-ern Hemisphere rights to the new hydrogel ma-terials and to a novel molding process, now called“spin casting, “ for the fabrication of hydrogel con-tact lenses. NPD, in turn, licensed Bausch &Lomb Inc. to use these product and process pat-ents. In 1971, after considerable improvementand careful testing, Bausch & Lomb obtained ap-proval from the U.S. Food and Drug Adminis-tration to sell hydrogel lenses in the United States.After several years, other firms began to obtainsimilar approvals for their hydrogel lenses, andmany firms are now in the market.

Today, there are more than 30 manufacturersof soft lenses (31,48). For any given use, differentbrands of lenses may differ slightly in design andhydrophilic capacity, some higher for greatercomfort and permeability, others lower for greaterdurability and visual acuity. Soft lenses are nowavailable for a wide variety of vision problemsand for extended wear.

The decade of the 1970S thus marked the in-troduction, acceptance, and ultimate dominanceof soft lenses over the older PMMA hard lenses,but as the decade ended a new type of lens, per-haps a third generation, was introduced. This lensis a gas-permeable hard lens, made of eithercellulose acetate butyrate (CAB), PMMA-siliconecombinations, or pure silicone. These lenses allowoxygen to reach the cornea through the lens assoft lenses do, while also offering the opticalclarity and ease of handling of hard lenses. In1979, the first gas-permeable hard lenses were ap-proved for use in the United States, and recently,others have followed. Currently, in addition tothe wide range of soft lenses available or beingtested, experimentation with newer gas-permeablehard lenses, including extended wear lenses, isactive.

12 ● Health Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

The history of the development of contactlenses is considerably more detailed and complexthan is suggested by a discussion of its significantdevelopments or a chronological listing of itshighlights. Today’s wide range of precision-made,carefully fitted, and extensively used contactlenses represents the contributions of a large num-ber of scientific areas and industrial sectors whichplayed key roles. These include: physics, biology,and chemistry and their continually expandingtheoretical and empirical foundations; precisionglassmaking, which made possible early lenses of

thin optical glass; the plastics industry, which hasdeveloped an expanded inventory of sophisticatedpolymer plastics that are the foundation of today’scontact lenses; the precision machine tool indus-try, which has provided ultra-fine grinding,lathing, and molding machines for lens finishing;the optical instruments industry, for its provisionof precise ophthalmic measurement and exami-nation technology and eye-care practitioners andtechnical personnel, who have utilized the newtechnologies and encouraged their continuedevolution.

3 ■

Types of Contact Lenses andTheir Characteristics1

The basic categories of contact lenses currentlyin use are the original hard (polymethylmethacry-late [PMMA]) lenses, soft hydrogels (hydro-xymethylmethacrylate [HEMA] and other mate-rials), and gas-permeable hard lenses (cellulose

HARD PMMA LENSES

As discussed in the previous chapter, hardPMMA lenses were the first lenses introducedonto the market, and corneal PMMA lenses simi-lar to those currently in use have been availablesince the early 1950s. Compared to later types oflenses, PMMA lenses can be difficult to adapt to,and perhaps as many as half of the people fitteddo not become long-term wearers. Since PMMAis not water- or gas-permeable, wearers must relyon the “tear pump” action of the eye to provideoxygen to the covered portion of the cornea. Asthe wearer blinks, tear interchange occurs fromoutside the lens to beneath it, providing the nec-essary oxygen. Although hard lenses are verysmall and cover only a portion of the cornea,many persons may not be able to provide enoughtears for comfortable wear. Others may “get by”for 8 to 12 hours but beyond that time, they suf-fer from dryness, swelling, and discomfort of theeye. Thus, hard lenses are, at best, “daily” wearlenses, but for many people they are very com-fortable for that duration.

The positive characteristics of PMMA lenses arenumerous. PMMA is made by annealing, a proc-ess of successive heating and cooling, which leavesit free of toxic chemicals. It thus is an inert mate-

‘This discussion of lens types and characteristics is drawn from:Aquavella and Gullapali, 1980 (3); Check, 1982 (8); ConsumerReports, 1980 (9); Dixon, 1982 (13); Feldman, 1981 (14); Kersley,1980 (19); and Morrison, 1976 (27).

acetate butyrate [CAB], PMMA-silicone, andsilicone). There are variations within each group,but their respective properties are similar enoughto consider them as essentially the same type oflenses.

rial and safe for use in the eye. It can be moldedor lathed into lenses with a high degree of preci-sion. Once made, PMMA lenses can be reworkedand modified to customize them to an individual’srequirements. The result is a safe lens of excellentvisual properties which very closely conforms topatient requirements. PMMA lenses require min-imal use of cleaning, soaking, and wetting solu-tions. They may be tinted to reduce excessive lightsensitivity, to make them easier to find whendropped, or for appearance reasons. They aredurable, can be renewed by polishing away mi-nor surface scratches, and often last 5 to 7 yearsor more. Last, they tend to be cheaper than otherlens types, because they are an older product withmany small suppliers and little difference amongdifferent brands.

Despite attempts to improve their permeabilityby drilling small holes in the lenses (“fenestra-tion”), adding hydrogel to the PMMA, or othermodifications, impermeability remains the majorshortcoming of rigid PMMA lenses. Because ofthis impermeability, they cannot cover much ofthe cornea and therefore must be small. They mustbe light and thin to adhere to the eye, which pre-cludes their use for correcting corneal astigmatismbeyond a moderately severe degree.

In summation, then, hard lenses are effectivefor daily wear for those persons who have nor-mal or better tearing action and who have mainlysingle vision refractive problems, such as near-

15

16 ● Health Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

sightedness (myopia) and farsightedness (hyper-metropia). They are not suitable for those withpoor tearing action, high corneal oxygen need,

SOFT LENSES

Soft lenses differ from PMMA lenses in manyways. Their basic soft quality comes from theirwater absorbency. They are usually gas-perme-able, allowing oxygen transport to the cornea.This softness and permeability make them con-siderably more comfortable than hard lenses, andmany wearers can adapt to them almost at once.These qualities can be of great advantage towearers, but they come at the expense of somevisual clarity. Soft lenses, which may containanywhere from 30 to 90 percent water, can bevery flexible, but what is called their “bag ofwater” nature has an effect on refraction, yieldingless clear images than provided by hard lenses.Additionally, high water content lenses are usu-ally fragile and easily torn. Reducing the watercontent in order to increase acuity and durability,however, sacrifices comfort. Reducing the plasticcontent to increase acuity by making a thinnerlens usually increases fragility. These tradeoffs arethe major problem with soft lenses. Further, theselenses cannot be easily modified. The extensive,but limited, inventories of ready-made lenses andthe lack of post-prescription customizing cannotpossibly meet the exact needs of all wearers. Still,lenses are readily available for the most commonrefractory corrections and may be available forless common corrections. For most wearers theoriginal fit is close enough, and the flexibility ofthe lens provides an additional, built-in elementof modification.

The comfort and permeability of soft lensesallow for uses beyond the correction of near-sightedness and farsightedness. Some brands havebeen approved by FDA for 15-day and even 30-day extended wear. Extended-wear lenses offerparticular benefits to those who find lens inser-tion and removal difficult, such as persons withextremely poor eyesight or troubled by arthritisor unsteadiness of the hand. Extended-wear softlenses, therefore, are often used by persons with

difficult multifocal correction requirements, orwho are unable to follow a daily regimen of care,insertion, and removal.

aphakia (i.e., those who have undergone lensremoval, usually due to cataracts) who may notsee well enough without contact lenses to insertthem properly, and are of particular value to olderpersons.

The larger size of soft lenses offers anotheradvantage. They can overlap comfortably ontothe scleral portion of the eye and under the lid,which stabilizes the lenses. This allows a softbifocal or multifocal lens to be tried in those casesof presbyopia (loss of flexibility in adjusting fromfar to near vision, usually associated with age)where hard PMMA bifocals have not proven suc-cessful. Multifocal soft lens are still problemati-cal for most users, particularly as other alterna-tives exist, such as bifocal eyeglasses; single visionlens-eyeglass combinations; and an unmatchedpair of monovision contact lenses, one correct-ing for nearsightedness, the other for farsighted-ness. The stability of soft lenses has also led tothe recent introduction of soft toric lenses, whichare used to correct for uneven focusing of the eye(so-called “corneal astigmatism”).

Special problems associated with soft lensesrelate to their hydrogel construction, fluid con-tent, and extended-wear functions. The potentialexists for the accumulation of both surface depos-its and bacteria, and the latter, particularly, wasthought to be a serious problem. As a result,special cleaning methods are used, and disinfec-tion techniques are also necessary. First, “hot”methods of disinfection (e.g., boiling), and then“cold” methods (chemical solutions) were devel-oped and appear to be equally effective in pre-venting serious problems that might otherwise de-velop in wearing waterlogged lenses for longperiods of time. However, these cleaning anddisinfection methods are costly, raising the ex-pense of maintaining soft lenses to upwards of$100 a year or more and stimulating the growthof a sizable lens care products industry (31).

Ch. 3—Types of Contact Lenses and Their Characteristics ● 17

GAS= PERMEABLE LENSES

Gas-permeable lenses are the newest type to ap- care. Their rigidity helps to correct astigmatism,pear and are made of either CAB, a PMMA- they are small but easy to handle, and they havesilicone combination, or pure silicone. They are recently become available in tints. Of the threerigid lenses, with the optical properties of PMMA types of gas-permeable lenses, the PMMA-siliconelenses, but approach soft lenses in comfort because combination is the most preferred at present, butof their permeability. They take more getting used the pure silicone lens has proved popular sinceto than soft lenses do but require considerably less its introduction.

PRESENT USAGE AND FUTURE TRENDS

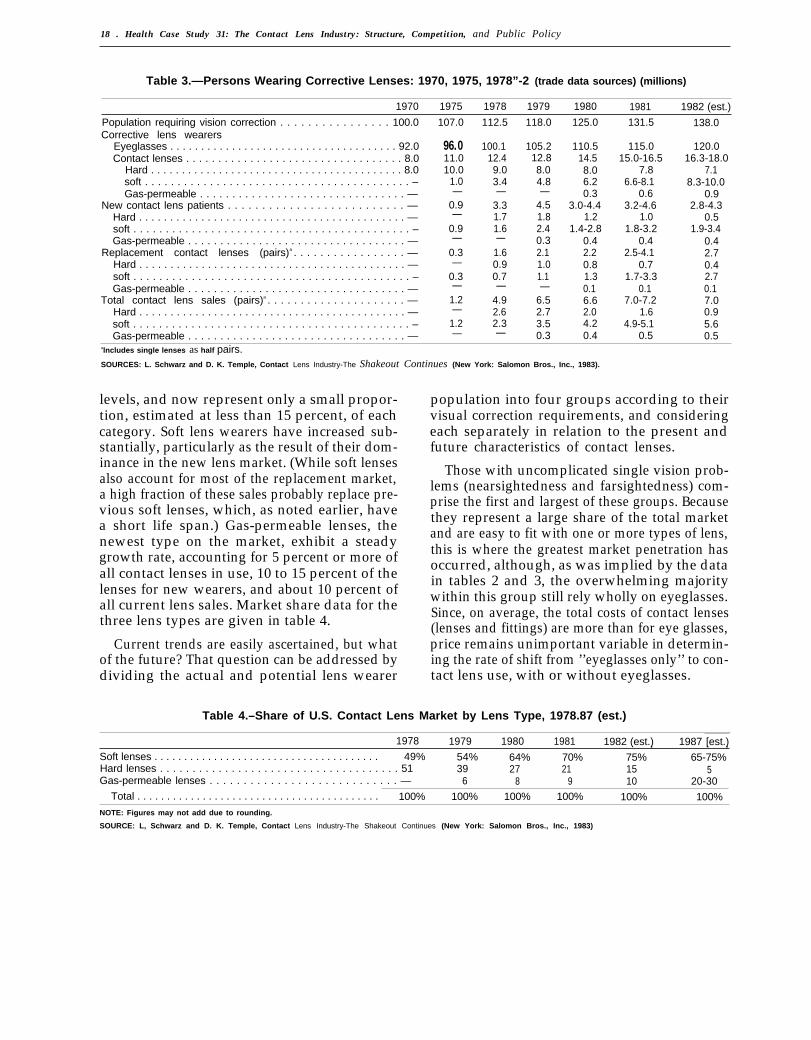

Both governmental and trade sources providedata on current levels and trends in contact lensuse, but they are in some disagreement. Com-parisons of the data in table 2, which contains esti-mates from the National Health Survey on cor-rective lens usage in 1966, 1971, and 1977, andthat of table 3, which contains estimates from in-dustry sources for the period 1970-82, show that,where the two sets overlap, the governmental sta-tistics are considerably more conservative. For ex-ample, the National Health Survey estimates oftotal lens wearers in 1971 and 1977 are 2.4 mil-lion and 7.0 million persons, respectively; thetrade data for 1970 and 1975 suggest that therewere 8.0 million and 11.0 million lens wearers inthose years. The wide gap between these two setsof estimates is explainable if the National HealthSurvey data relate to those who wear contactlenses, and the industry data, to those who havepurchased them. In any case, caution is called forin making definitive statements about rates ofsales and levels of usage of contact lenses. Thesubsequent analysis of trends and levels of con-tact lens wear derives mainly from the data intable 3, which are more detailed and current, ifhigher, than the data in table 2.

The numbers of eyeglass and contact lenswearers appear to have grown at fairly steadyrates since 1979, with eyeglass wearers increas-ing by about 5 million per year and contact lenswearers by about 1.5 million per year. Since thenumber of new contact lens patients per year iswell above 1.5 million, it appears that substan-tial attrition or failure rates do occur. The stablegrowth rate among lens wearers, however, may

Table 2.—Persons Wearing Corrective Lenses:1966, 1971, and 1977

1966 1971 1977

In millionsPopulation 3 years and over . . . . . . . . 178.9 191.6 202.9

Wearing corrective lenses. . . . . . . . 86.0 94.3 103.3Eyeglasses only . . . . . . . . . . . . . . 84.2 90.3 96.3Contact lenses, with

or without eyeglasses . . . . . . . 1.8 2.4 7.0

PercentagesPercent of population wearing lenses 48.1 49.2 50.9

Eyeglasses only . . . . . . . . . . . . . . 47.1 47.1 47.5Contact lenses, with

or without eyeglasses . . . . . . . 1.0 1.3 3.5SOURCES: 1966: U.S. Department of Health, Education, and Welfare, Character-

istics of Persons With Corrective Lenses, United States: July 1965-June 1966, Vital and Health Statistics, series 10, No. 53, prepared byM. M. Hannaford, DHEW publication No. (PHS) 1000 (Washington, DC:U.S. Government Printing Office, June 1969). 1971 and 1977: U.S. De-partment of Commerce, Bureau of the Census, Statistical Abstractof the United States, 1982-83 (103 cd.), Washington, DC, 1983.

be only a temporary phenomenon. Since new (asopposed to replacement) contact lenses are expen-sive and usually represent an alternative to eye-glasses for cosmetic reasons, it is likely that therecession of the early 1980s had a significant neg-ative effect on lens purchases. Additionally, thesales data probably do not yet reflect the ultimateacceptance levels of recent contact lens inno-vations.

Perhaps the more meaningful implications ofthe data relate to patterns among contact lenstypes rather than to aggregated totals. Here, thedata tell a less ambiguous story. The older hardlenses are declining in total usage, having droppedfrom 10 million to 7.1 million wearers between1975 and 1982. Each year they have accountedfor a declining share of both new and replacement

18 . Health Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

Table 3.—Persons Wearing Corrective Lenses: 1970, 1975, 1978”-2 (trade data sources) (millions)

1970 1975 1978 1979 1980 1981 1982 (est.)

Population requiring vision correction . . . . . . . . . . . . . . . . 100.0Corrective lens wearers

Eyeglasses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92.0Contact lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.0

Hard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8.0soft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . –Gas-permeable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

New contact lens patients . . . . . . . . . . . . . . . . . . . . . . . . . . —Hard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —soft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . –Gas-permeable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

Replacement contact lenses (pairs)a . . . . . . . . . . . . . . . . . —Hard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —soft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . –Gas-permeable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

Total contact lens sales (pairs)a . . . . . . . . . . . . . . . . . . . . . —Hard . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —soft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . –Gas-permeable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . —

107.0

96.011.010.0

1.0—

0.9—

0.9—

0.3—

0.3—

1.2—

1.2—

112.5

100.112.49.03.4—

3.31.71.6—

1.60.90.7—

4.92.62.3—

118.0

105.212.88.04.8—

4.51.82.40.32.11.01.1—

6.52.73.50.3

125.0

110.514.58.06.20.3

3.0-4.41.2

1.4-2.80.42.20.81.30.16.62.04.20.4

131.5

115.015.0-16.5

7.86.6-8.1

0.63.2-4.6

1.01.8-3.2

0.42.5-4.1

0.71.7-3.3

0.17.0-7.2

1.64.9-5.1

0.5

138.0

120.016.3-18.0

7.18.3-10.0

0.92.8-4.3

0.51.9-3.4

0.42.70.42.70.17.00.95.60.5

alncludes single lenses as half pairs.SOURCES: L. Schwarz and D. K. Temple, Contact Lens Industry-The Shakeout Continues (New York: Salomon Bros., Inc., 1983).

levels, and now represent only a small propor-tion, estimated at less than 15 percent, of eachcategory. Soft lens wearers have increased sub-stantially, particularly as the result of their dom-inance in the new lens market. (While soft lensesalso account for most of the replacement market,a high fraction of these sales probably replace pre-vious soft lenses, which, as noted earlier, havea short life span.) Gas-permeable lenses, thenewest type on the market, exhibit a steadygrowth rate, accounting for 5 percent or more ofall contact lenses in use, 10 to 15 percent of thelenses for new wearers, and about 10 percent ofall current lens sales. Market share data for thethree lens types are given in table 4.

Current trends are easily ascertained, but whatof the future? That question can be addressed bydividing the actual and potential lens wearer

population into four groups according to theirvisual correction requirements, and consideringeach separately in relation to the present andfuture characteristics of contact lenses.

Those with uncomplicated single vision prob-lems (nearsightedness and farsightedness) com-prise the first and largest of these groups. Becausethey represent a large share of the total marketand are easy to fit with one or more types of lens,this is where the greatest market penetration hasoccurred, although, as was implied by the datain tables 2 and 3, the overwhelming majoritywithin this group still rely wholly on eyeglasses.Since, on average, the total costs of contact lenses(lenses and fittings) are more than for eye glasses,price remains unimportant variable in determin-ing the rate of shift from ’’eyeglasses only’’ to con-tact lens use, with or without eyeglasses.

Table 4.–Share of U.S. Contact Lens Market by Lens Type, 1978.87 (est.)

1978 1979 1980 1981 1982 (est.) 1987 [est.)Soft lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. , . ,49% 54% 64% 70% 75% 65-75%

Hard lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51 39 27 21 15 5Gas-permeable lenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 6 8 9 10 20-30

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100% 100% 100% 100% 100% 100%NOTE: Figures may not add due to rounding.

SOURCE: L, Schwarz and D. K. Temple, Contact Lens Industry-The Shakeout Continues (New York: Salomon Bros., Inc., 1983)

Ch. 3–Types of Contact Lenses and Their Characteristics “ 19

The second and third components of the totalmarket also are large, but the difficulties in de-veloping wearable lenses have left most of thismarket untapped. These two groups are, respec-tively, the moderate-to-severe astigmatic, andthose with presbyopia, for which bifocal or multi-focal corrective lenses are usually employed.

By and large, the use of contact lenses in thesethree groups can be considered “cosmetic,” since,with some exceptions, eyeglasses readily affordsatisfactory levels of correction. For the fourthmarket segment, however, contact lenses can beconsidered therapeutic, since, using the same cri-terion, eyeglasses have limited capability for cor-rection. In this group are those who suffer fromcorneal abnormalities such as keratoconus andother pathological conditions such as trachoma,corneal ulcers, and scarred corneas (20).

Projections for contact lens use for the short-run future can be made by extrapolating currentmarket trends; for the medium-run future by esti-mating the effects of changes currently underwayor impending but which have not yet materializedas strong market factors; and for the long-runfuture by predicting the effects of changes thattoday may be only hypotheses, concepts, or ideas.

In the short run, current trends are likely to con-tinue. Contact lens wearers will increase steadily,if slowly, as a percentage of the total vision-corrected population. Soft and gas-permeable lenswearers will grow and hard lens wearers will de-cline as percentages of the total contact lens-wearing population. Sales of soft lenses will growas the currently strong competition in innovationand improvement creates increasingly satisfactoryproducts for those who have not yet adoptedlenses or have failed with hard lenses. The uniquequalities of soft lenses will make them increasinglyattractive to those persons with visual problemsnot resolvable with hard or the earlier soft lenses.Accordingly, growth in the use of soft lenses islikely, perhaps at a rate of 10 to 15 percent peryear as their uses for single vision problems,astigmatism, presbyopia, and therapeutic applica-tions expand. Further, as the majority of lenswearers shifts to soft lenses, their fairly short aver-age duration (9 to 18 months) will generate a verysizable replacement lens market.

The use of gas-permeable lenses will also growrapidly as users of hard lenses switch over, non-users adopt them, and those who might otherwiseselect soft lenses are attracted by the lower long-term costs (from less frequent replacement andsimpler care procedures), and excellent vision cor-rection of the gas-permeables. An additional at-traction is that these lenses, unlike the soft ones,can be readily custom-fitted. Thus, over the next5 years gas-permeable contact lenses will contrib-ute substantially to the decline of hard lenses andmay also take part of the market that wouldotherwise be won by soft lenses. Their percent-age growth rate will be especially impressive,given the present small base against which thatrate will be calculated.

Beyond the extension of present trends into theshort-run, certain projections for the medium-runfuture can be made if one looks at forces of changecurrently in their incipiency. At present, softlenses are fragile and not reworkable. However,promising advances in plastics and in lens manu-facturing technology will result in more durableand more precisely fit soft lenses. Combined withtheir comfort and extended-wear capabilities,these improvements will enable soft lenses to pro-tect their market position relative to gas-perme-able lenses. As long as they remain distinguish-able lens types, both soft and gas-permeable lenseswill grow steadily in use. Together, they will ren-der hard lenses obsolete, and each will find itsrespective market position. Soft lenses will be theproduct of choice for those with single visionproblems who place a high premium on comfortand extended wear, and they will be especiallyuseful for presbyopia and for conditions not cor-rectable with eyeglasses. On the other hand,gas-permeable lenses will be attractive to the singlevision problem wearer who finds them sufficientlycomfortable and prefers their overall economy,ease of application, and current availability intints.

The recent introduction of extended-wear gas-permeable lenses, however, provides a strong hintthat the eventual merging of the two main typesof lenses has begun and that the future will bringa new, hybrid type of lens combining the bestfeatures of both. But in the long run, many other

20 . Health Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

changes which today may only be in their basicresearch stages will play prominent roles, and allpredictions are very uncertain. However, basedon what is on the horizon today, the long-runfutures of both soft and gas-permeable lenses lookpromising, possibly more so for soft lenses, if thedistinction continues. New soft lens develop-ments, such as optically superior, nontoxic ma-terials requiring minimal care even in extendeduse, and lens-making methods that allow moreexact fitting and duplication, can be expected.And as new manufacturing methods—e.g., im-provements of today’s low-cost spin-castingmethod—reduce costs, the popularity of softlenses should increase. Accordingly, the lens ofthe future may well be a low-cost, easy-to-wear,visually near-perfect, extended-wear, disposablelens.

A hybrid lens that provides the best qualitiesof both soft and gas-permeable lenses is a distinctpossibility, as mentioned. If it develops, then the

terms soft and (hard) gas-permeable will be ob-solete. An additional quality of the lens of thefuture will be durability, which may make lensesstill more affordable by reducing replacementcosts, and may increase their attractiveness tousers by making them more interchangeable witheyeglasses, since they will be able to be handledmore often without damage.

Finally, in the past, many of the important de-velopments in contact lenses originated from awide range of scientific and industrial sources.This lesson of the long-term past is particularlyapplicable to the long-term future. The technol-ogies of electronics, imaging, optics, and all ofthe other sciences are expanding exponentially.In the long run, then, contact lenses will makesubstantial gains as a form of corrective eyewear.Given their potential development, it is at leastconceivable to project their displacement of eye-glasses as the dominant method of vision correc-tion in the not-too-distant future.

4.Wearers, Prices, and Sources of Payment

WEARERS OF CONTACT LENSES

“Disorders of refraction and accommodation, ”according to the U.S. Public Health Service,ranked 14th among the 20 most common reasonsfor visiting a physician but accounted for only 1.4percent of all visits to non-Federal, office-basedphysicians in 1981 (52). Unlike other diagnosticcategories, however, refractive examinations andcorrective-lens prescribing and fitting can be ob-tained from eye-care professionals other than phy-sicians (i. e., optometrists and, in some States, op-ticians). In fact, optometrists represent abouttwo-thirds of those professionals legally permittedto examine eyes and prescribe corrective lenses,and they prescribe approximately three-fourthsof all corrective lenses and 60 percent of all con-tact lenses (5,12). If all such eye care were pro-vided by ophthalmologists, refractive disorderswould rank among the top three reasons forvisiting a physician, either closely followinghypertension and normal pregnancy or leadingthem, depending on the adjustment factor cho-sen. Accordingly, it is not surprising that over halfof the population 3 years old and above wear cor-rective lenses and that about 15 million personswear contact lenses.

In table 5, data from three National HealthSurvey studies of corrective lens wearers arepresented. These data, for 1965-66, 1971, and1979-80, show some interesting patterns andtrends among users. In each of the study periods,contact lens wearing was at least twice as preva-lent among females, overall, as among males. Fur-ther, lens wearing is most common among youngadults, tapering to low levels at middle age andbeyond. This pattern is almost totally the oppositeof the age-related frequency of use of eyeglasses.(However, in 1979-80, lens wearing in the 65 andover group, both males and females, rose sharply. )Third, over the covered period, lens wearing in-creased at every age level for both males andfemales. Thus, the general view of contact lensesas primarily a “younger female” product has sub-

Table 5.—Contact Lens Wearers, Percentof Population, by Sex and Age,

1965-66, 1971, and 1979.80

Percent of population 3years and over wearing

contact lenses

Sex and age group 1965-66 1971 1979-80

Both sexes:All ages, 3 and over. . . . . . . . .3-16 . . . . . . . . . . . . . . . . . . . . . . .17-24 . . . . . . . . . . . . . . . . . . . . . .25-44 . . . . . . . . . . . . . . . . . . . . . .45-54 . . . . . . . . . . . . . . . . . . . . . .55-64 . . . . . . . . . . . . . . . . . . . . . .65 and over . . . . . . . . . . . . . . . .

Male:All ages, 3 and over. , . . . . . . .3-16 . . . . . . . . . . . . . . . . . . . . . . .17-24 . . . . . . . . . . . . . . . . . . . . . .25-44 . . . . . . . . . . . . . . . . . . . . . .45-54 . . . . . . . . . . . . . . . . . . . . . .55-64 . . . . . . . . . . . . . . . . . . . . . .65 and over . . . . . . . . . . . . . . . .

Female:All ages, 3 and over. . . . . . . . .3-16 . . . . . . . . . . . . . . . . . . . . . . .17-24 . . . . . . . . . . . . . . . . . . . . . .25-44 . . . . . . . . . . . . . . . . . . . . . .45-54 . . . . . . . . . . . . . . . . . . . . . .55-64 . . . . . . . . . . . . . . . . . . . . . .65 and over . . . . . . . . . . . . . . . .

1.00.33.71.30.40.3—

0.6—2.00.90.3

1.30.45.21.70.5——

2.10.66.63.00.70.70.7

1.20.33.41.80.50.70.7

2.90.99.54.20.90.60.7

4.51.09.47.72.11.64.3

2.80.65.34.41.41.44.6

6.21.5

13.310.72.71.94.0

SOURCES: 1965-66: U.S. Department of Health, Education, and Welfare,Characteristics of Persons With Corrective Lenses, United StatesJuly 1965-June 1966, Vital and Health Statistics, series 10, No. 53,prepared by M. M. Hannaford, DHEW publication No. (PHS) 1000(Washington, DC: US. Government Printing Office, June 1969) 1971:U.S. Department of Health, Education, and Welfare, Characteristicsof Persons With Corrective Lenses, United States: 1971, Vital andHealth Statistics, series 10, No. 93, prepared by M. H. Wilder, DHEWpublication no. (HRA) 75-1520, Washington, DC, 1974. 1979-60: R. Hol-Iander, U.S. Department of Health and Human Services, Public HealthService, Rockville, MD, personal communication, June 30, 1983.

stantial validity, but the pattern presently ischanging in substantial ways and will be con-siderably different in the future. The currentchanges, particularly the increasing use of con-tact lenses by older persons, are attributable toyounger lens wearers’ moving through the agespectrum; the development of newer types ofbifocal and toric lenses, which relate especiallyto the vision problems of older persons; and the

23

25-339 0 - 84 - 5 : QI, 3

—

24 ● Health Case Study 31: The Contact Lens Industry: Structure, Competition, and Public Policy

growth in soft and extended-wear lenses, whichparticularly help older persons, whose eyes areless accommodating to contact lenses than arethose of younger persons. Further, differences inthe rates of lens usage by women and men are nar-rowing, and in new fits the differences will soonbe eliminated. Accordingly, the lens market willno longer be dominated by the young adult femalewearer; the traditional patient base will expandwidely; and all groups except perhaps children willbecome important users.

Although as large a part of the population withvision correction suffers from presbyopia as fromsingle-vision problems, lens wearing is much moreprevalent among the latter group. As lenses forall users improve, the greatest relative growth willbe for presbyopes and astigmatic, but contactlenses will continue to be prescribed most fre-quently for single-vision problems. Within thesingle-vision category, about 60 percent havemyopia, 40 percent hyperopia. In addition, therelative use of contact lenses for those with myopiaruns somewhat higher than among those withhyperopia. Therefore, at least through the 1980s,the largest absolute volume of sales will continueto be for the correction of myopia, followed byhyperopia, with presbyopic use gaining quicklyand perhaps passing hyperopia before the 1980shave ended.

Additional data from the National Health Ex-penditures Survey (51) show contact lens use tobe relatively more common in suburban than ru-ral or inner-city areas, among whites than non-whites (particularly blacks and Hispanics), andalso to be positively associated with the educa-tional level of the family head. All of these cor-relations are explainable in terms of the higher in-come levels among suburban residents, whites,and the more educated. (Other features in the pat-tern of contact lens use show that lenses are moreoften worn by white-collar and service workersthan by blue-collar or farm workers. These dif-ferences may also be explainable in part by in-come differentials, but probably more so by thegreater proportion of women employed in thewhite-collar and service sectors, and perhaps alsoby the actual physical conditions of each type ofwork. ) In other words, contact lenses are a “nor-mal” economic good, with purchases expanding

as income expands, or in economists’ parlance,with a positive income elasticity of demand.