the bretton woods system class 14 – tuesday, 1 november 2011 j a morrison 1 jm keynes & hd...

TRANSCRIPT

The Bretton Woods System

Class 14 – Tuesday, 1 November 2011J A Morrison 1

JM Keynes & HD White

Admin• Niall Ferguson's The Ascent of Money

-- available online

2

Lec 14: The Bretton Woods System

I. Keynes’ Revolutionary VisionII. Creation of the Bretton Woods

SystemIII.History of the Bretton Woods

System

3

Lec 14: The Bretton Woods System

I. Keynes’ Revolutionary VisionII. Creation of the Bretton Woods

SystemIII.History of the Bretton Woods

System

4

You’ll remember that JM Keynes had been a virulent critic of the gold standard

since the early 1920s.

By the mid-1930s, the gold standard had once again

become “dead as mutton.”5

But Keynes knew that the revolution might prove only

temporary.

Throughout the 1930s, Keynes worked to refine his perspective and sharpen his

criticisms.6

Let’s turn, then, to consider precisely why Keynes

despised the gold standard so vigorously…

7

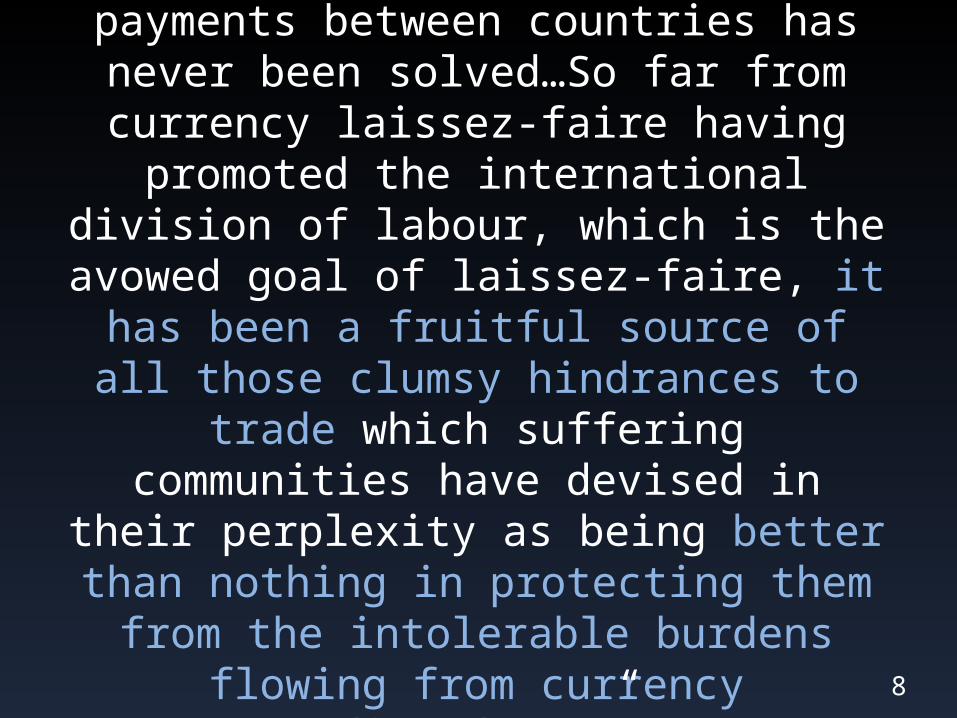

“The problem of maintaining equilibrium in the balance of payments

between countries has never been solved…So far from currency laissez-

faire having promoted the international division of labour, which is the avowed goal of laissez-faire, it has been a fruitful source of all those

clumsy hindrances to trade which suffering communities have devised in their perplexity as being better than nothing in protecting them from the

intolerable burdens flowing from currency disorders.”

-- Keynes (1941)8

So, for Keynes, the central issue was the balance of

payments.

9

What are states’ options for dealing with imbalances of

payments?

(Hint: Friedman in Class 6!)

10

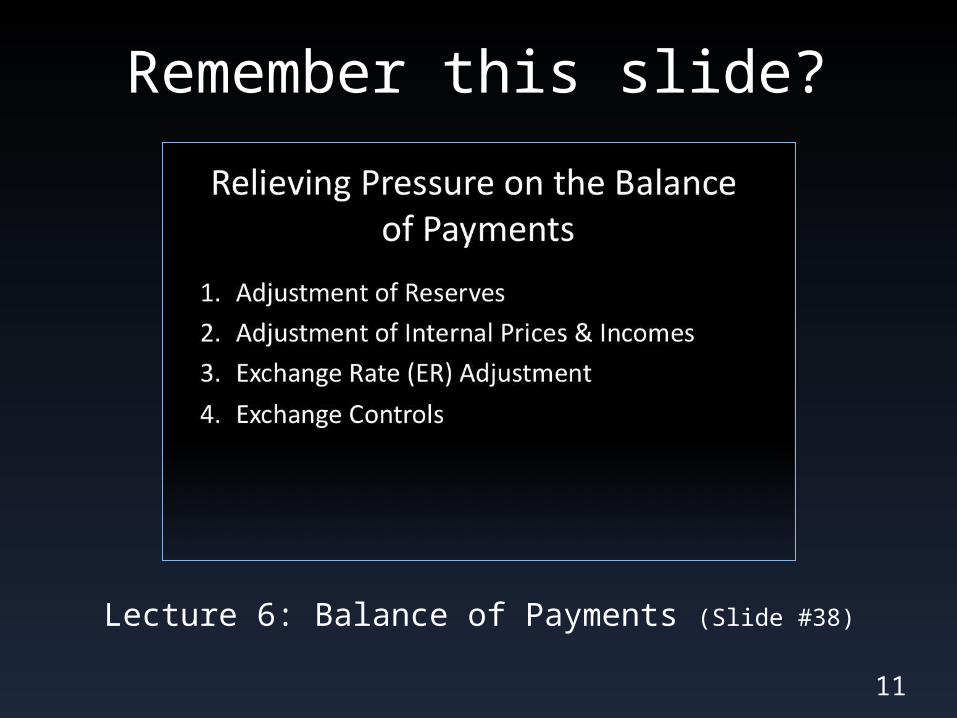

Remember this slide?

11

Lecture 6: Balance of Payments (Slide #38)

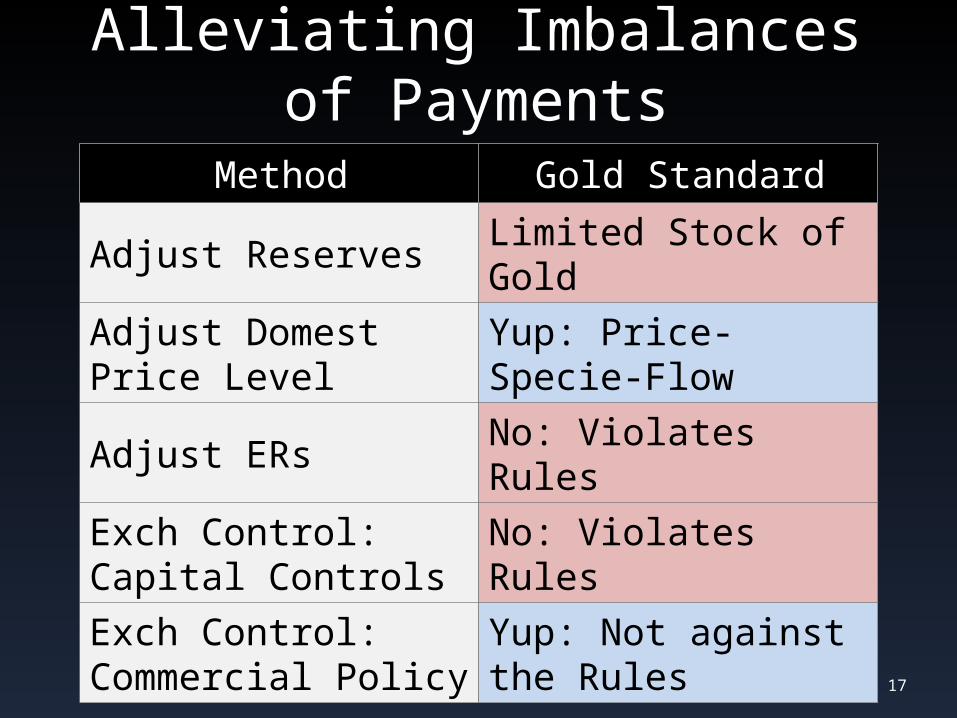

Reconciling the Balance of Payments Under the Gold

Standard

16

1. Adjustment of Reserves2. Adjustment of Internal Prices &

Incomes 3. Exchange Rate (ER) Adjustment4. Exchange Controls

1. Capital Controls: Limit convertibility2. Commercial Policy

But world gold supply is limited.

Alleviating Imbalances of Payments

17

Method Gold Standard

Adjust ReservesLimited Stock of Gold

Adjust Domest Price Level

Yup: Price-Specie-Flow

Adjust ERs No: Violates Rules

Exch Control: Capital Controls

No: Violates Rules

Exch Control: Commercial Policy

Yup: Not against the Rules

Given the finite supply of gold, policymakers on the

GS are essentially forced to choose between sacrificing

control over domestic macroeconomic policy and

enacting commercial policy…

18

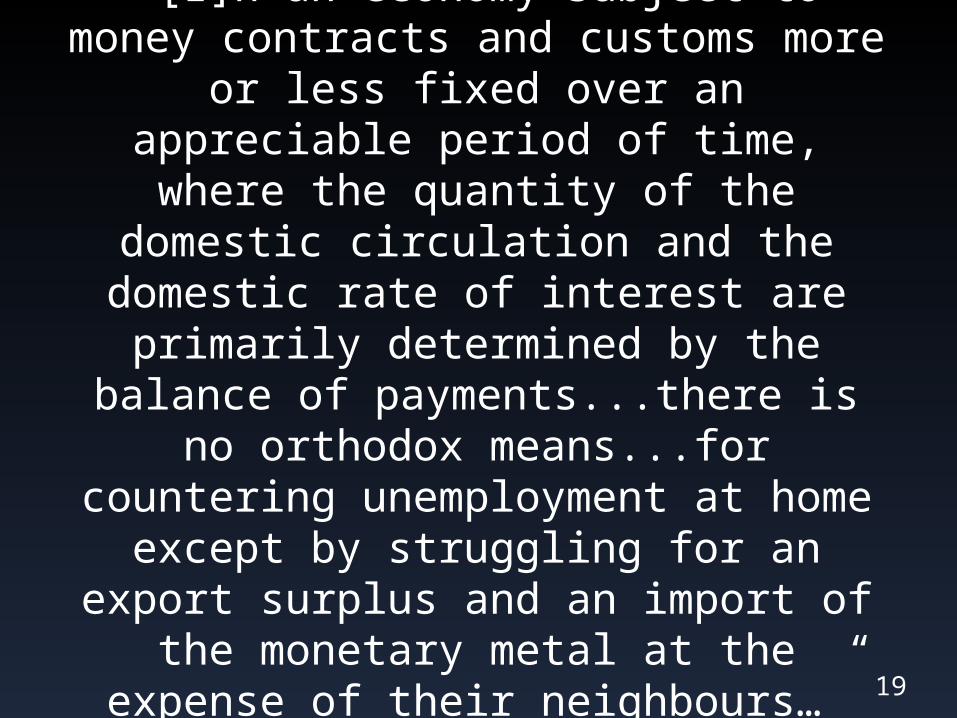

“[I]n an economy subject to money contracts and customs more or less fixed over an appreciable period of

time, where the quantity of the domestic circulation and the domestic

rate of interest are primarily determined by the balance of

payments...there is no orthodox means...for countering unemployment

at home except by struggling for an export surplus and an import of the monetary metal at the expense of

their neighbours…”

-- Keynes, General Theory (Ch 23)19

“Never in history was there a method devised of such efficacy for setting

each country's advantage at variance with its neighbours' as the

international gold (or, formerly, silver) standard. For it made domestic

prosperity directly dependent on a competitive pursuit of markets and a competitive appetite for the precious

metals. ”

-- Keynes, General Theory (Ch 23)

20

21

In other words, the gold standard

creates enormous incentives for

states to enact commercial policy.

Is the gold standard worth sacrificing free

trade?

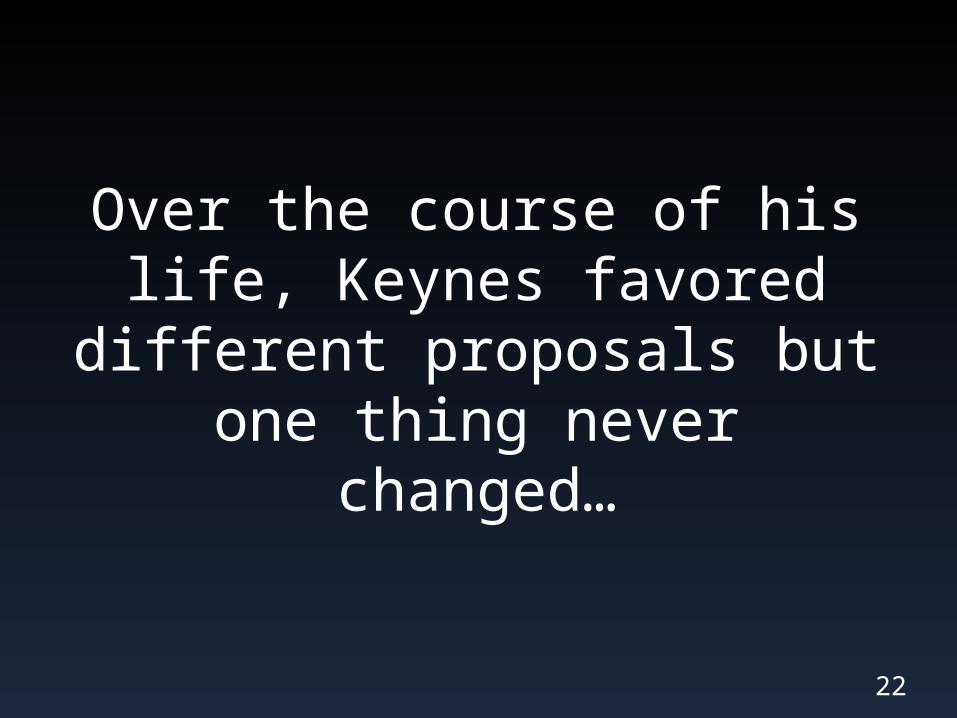

Over the course of his life, Keynes favored different proposals but one thing

never changed…

22

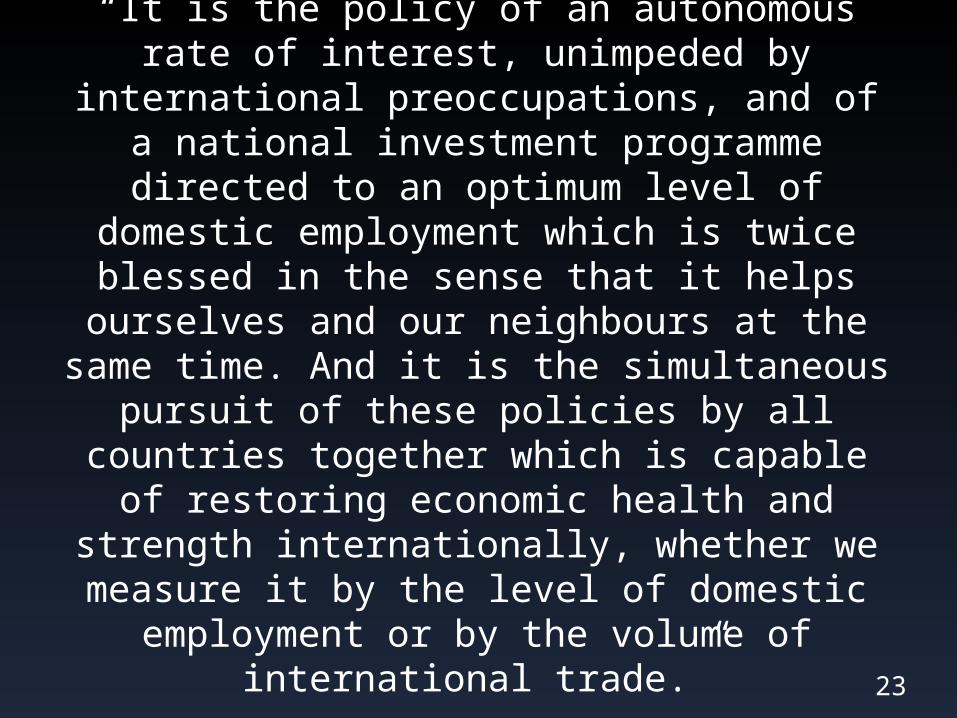

“It is the policy of an autonomous rate of interest, unimpeded by international

preoccupations, and of a national investment programme directed to an

optimum level of domestic employment which is twice blessed in the sense that it helps ourselves and our neighbours at the

same time. And it is the simultaneous pursuit of these policies by all countries together which is capable of restoring

economic health and strength internationally, whether we measure it by

the level of domestic employment or by the volume of international trade.”

-- Keynes, General Theory (Ch 23) 23

Alleviating Imbalances of Payments

24

Method Gold StandardKeynes’

Proposals

Adjust ReservesLimited Stock of Gold

1944

Adjust Domest Price Level

Yup: Price-Specie-Flow

NEVER!!!!!!

Adjust ERsNo: Violates Rules

1923-1926, 1931-1940

Exch Control: Capital Controls

No: Violates Rules

1944

Exch Control: Commercial Policy

Yup: Not against the Rules

1929-1931

Keynes always prioritized internal stability over

external stability…

Find some way—any way!—to alleviate imbalances of

payments other than through domestic macroeconomic

adjustments. 25

During the interwar period, foreign economic policy was

made unilaterally and on an ad hoc basis.

The result was not just a lack of cooperation, but many of

the policies were cross-cutting.

The difficulties of the 1930s were exacerbated. 26

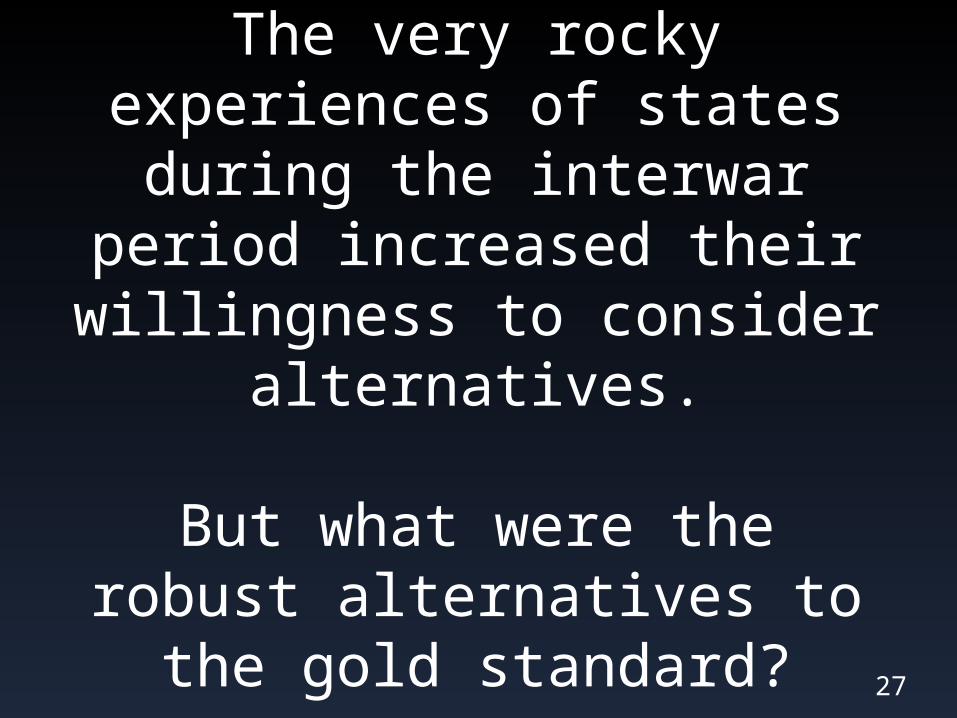

The very rocky experiences of states during the

interwar period increased their willingness to consider

alternatives.

But what were the robust alternatives to the gold

standard?27

Lec 14: The Bretton Woods System

I. Keynes’ Radical VisionII. Creation of the Bretton Woods

SystemIII.History of the Bretton Woods

System

28

II. Creation of the BWS

1. Keynes and White2. Keynes versus White3. The Bretton Woods Conference4. Another Gold Standard System?

29

In the summer of 1941, with the United States far from entering the war and the Axis rolling through the

Soviet Union, JM Keynes and HD White (independently) drafted their plans for the postwar monetary order.

30

John Maynard Keynes (GB)

• 5 June 1883 – 21 April 1946

• Represented British Treasury at Versailles (1919)

• Battled 1925 Return to Gold

• Called for Abandonment of Gold in 1930s

31

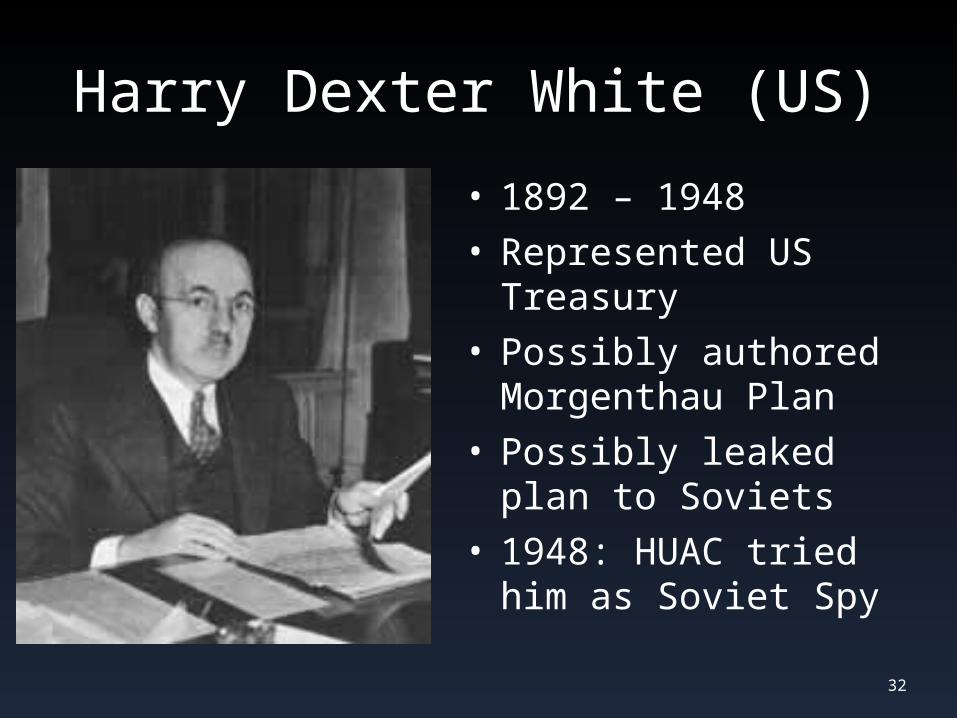

Harry Dexter White (US)

• 1892 – 1948• Represented US

Treasury• Possibly authored

Morgenthau Plan• Possibly leaked plan

to Soviets• 1948: HUAC tried

him as Soviet Spy

32

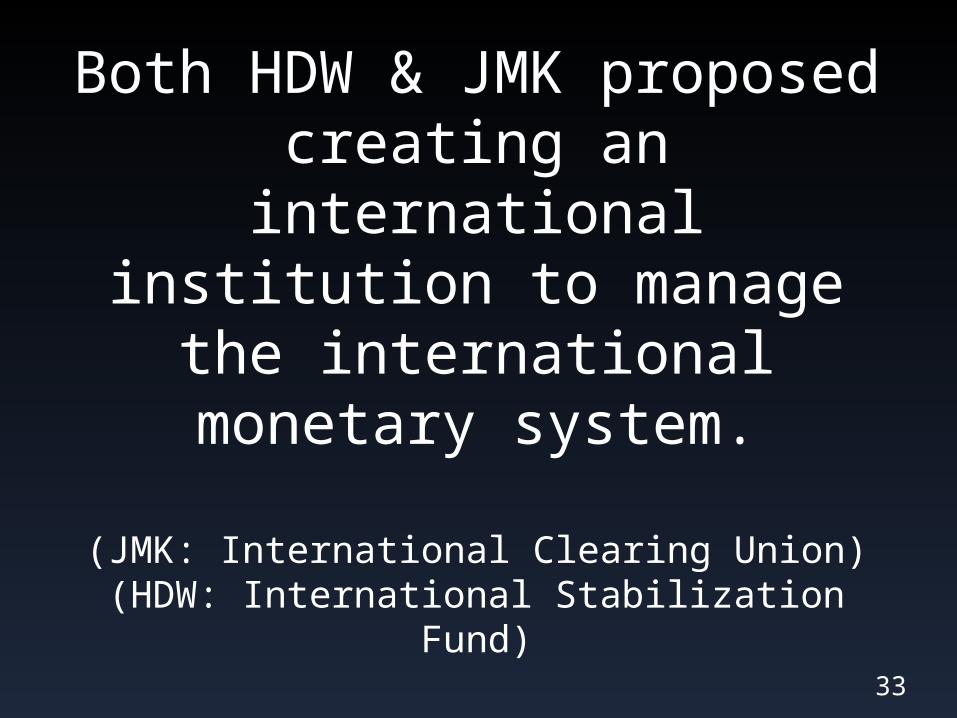

Both HDW & JMK proposed creating an international institution to manage the international monetary

system.

(JMK: International Clearing Union)(HDW: International Stabilization Fund)

33

Functions of the Proposed International Institution

• Multilateral Clearing Mechanism: Centralize Currency Exchange

• Orderly Exchange Rate Regulation• International “Banking” – Distribute

Liquidity– “Creditor” countries acquire extra

reserves– “Debtor” countries lose reserves– Int’l Institution will loan to debtors from

creditors’ accounts 34

Essentials of Proposed Institution

• ER Stability– ERs fixed to gold or currency backed by gold

(e.g. US $)– ERs flexible within very narrow bands– Limited Adjustment: members vote to

determine if there is “fundamental disequilibrium”

– “Scarce currency” exception

• Capital Controls– States encouraged to limit “speculative

flows”

• Facilitator: Make loans for temporary imbalances

35

Alleviating Imbalances of Payments

36

Method Gold Standard Bretton Woods

Adjust ReservesLimited Stock of Gold

IMF will redistribute

Adjust Domest Price Level

Yup: Price-Specie-Flow

Unnecessary!

Adjust ERsNo: Violates Rules

10%, more with authorization

Exch Control: Capital Controls

No: Violates Rules

Please do!

Exch Control: Commercial Policy

Yup: Not against the Rules

No: Promote free trade

Keynes and White broadly agreed on the purpose and

scope of the proposed institution.

But they didn’t agree on all of the specifics of implementation…

37

II. Creation of the BWS

1. Keynes and White2. Keynes versus White• The Bretton Woods Conference• Another Gold Standard System?

38

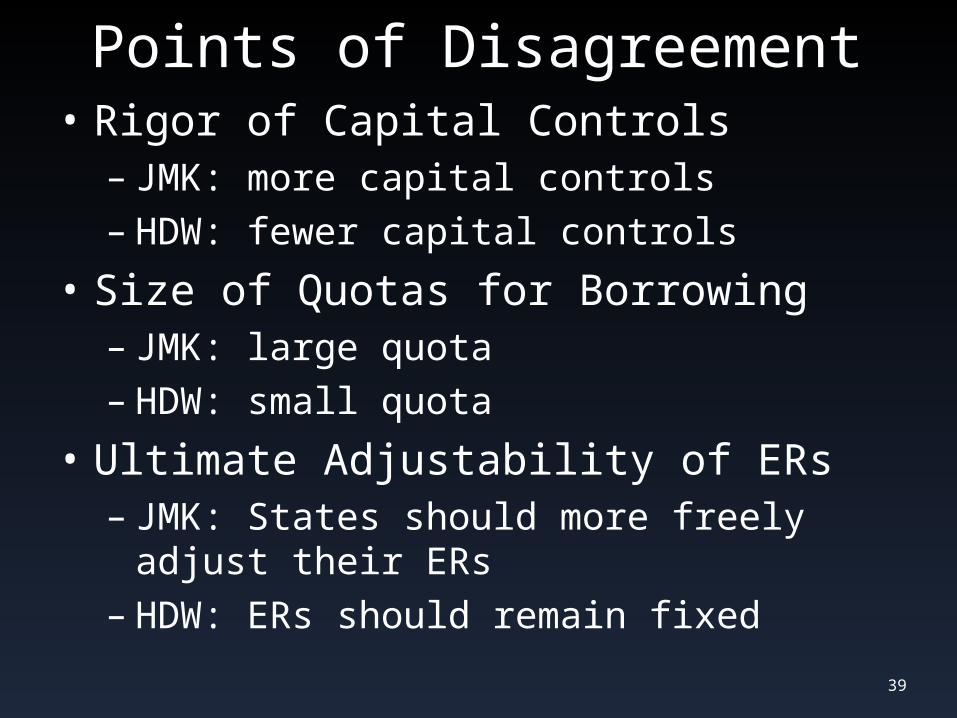

Points of Disagreement• Rigor of Capital Controls– JMK: more capital controls– HDW: fewer capital controls

• Size of Quotas for Borrowing– JMK: large quota– HDW: small quota

• Ultimate Adjustability of ERs– JMK: States should more freely adjust

their ERs– HDW: ERs should remain fixed

39

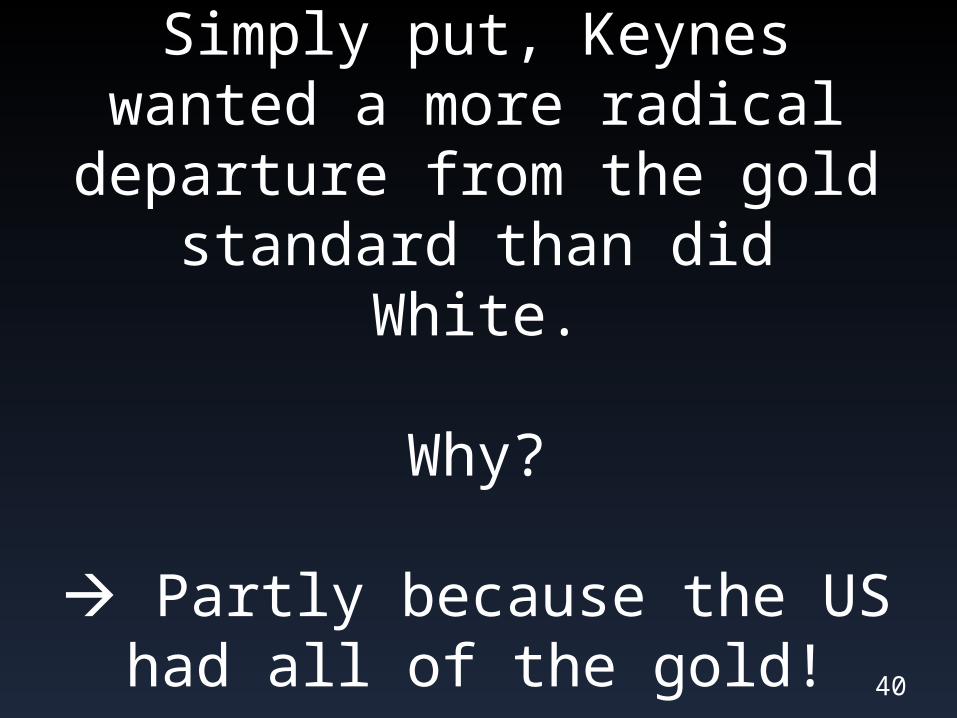

Simply put, Keynes wanted a more radical departure

from the gold standard than did White.

Why?

Partly because the US had all of the gold!

40

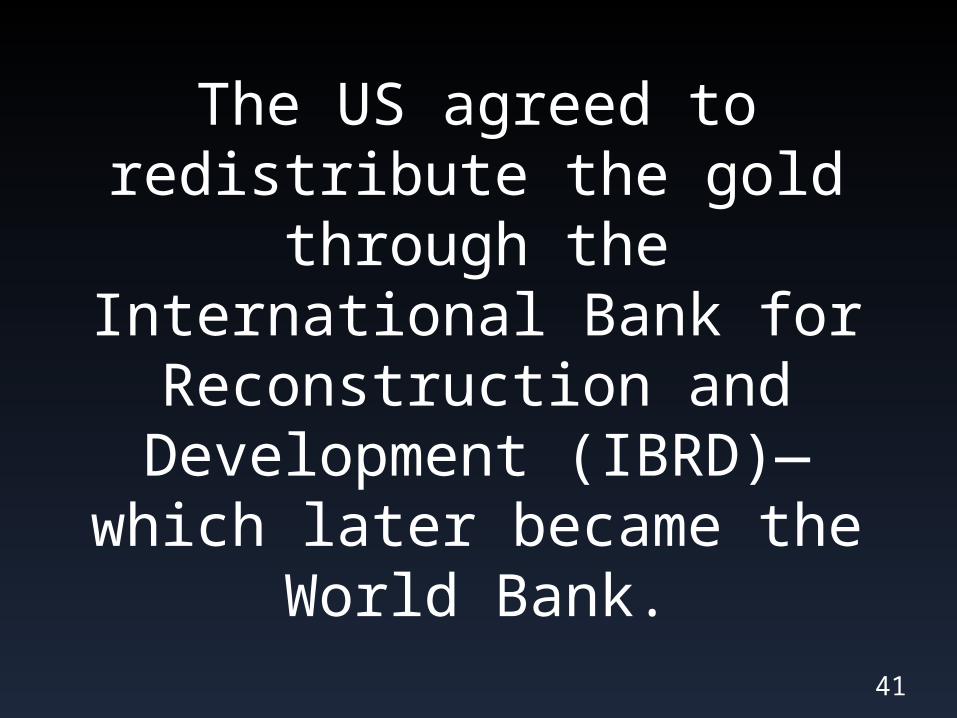

The US agreed to redistribute the gold

through the International Bank for Reconstruction and Development (IBRD)—which

later became the World Bank.

41

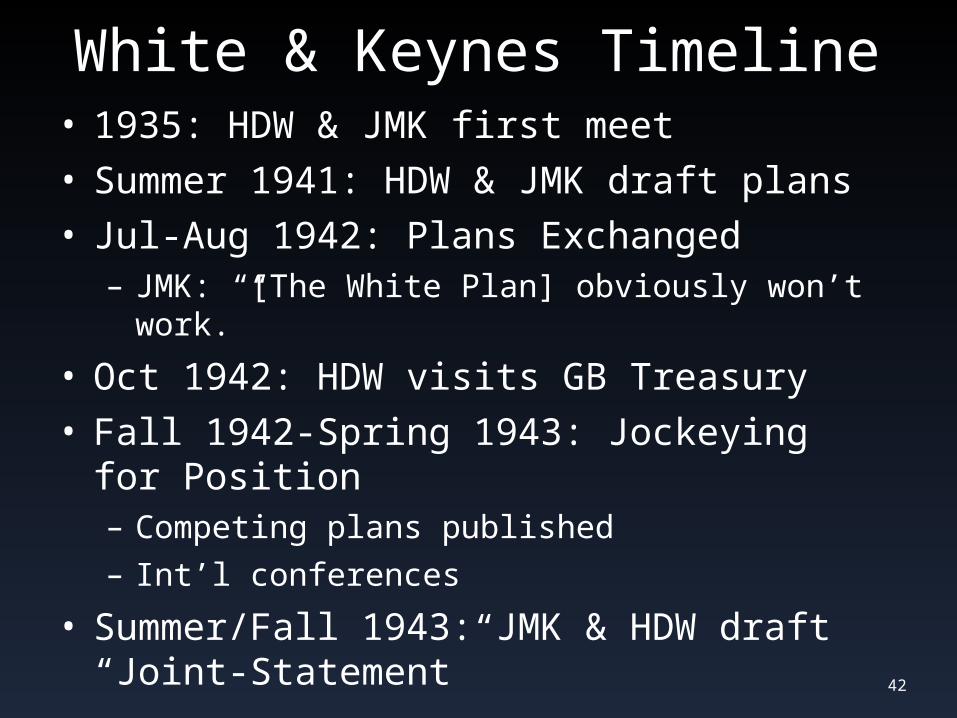

White & Keynes Timeline• 1935: HDW & JMK first meet• Summer 1941: HDW & JMK draft plans• Jul-Aug 1942: Plans Exchanged– JMK: “[The White Plan] obviously won’t work.”

• Oct 1942: HDW visits GB Treasury• Fall 1942-Spring 1943: Jockeying for

Position– Competing plans published– Int’l conferences

• Summer/Fall 1943: JMK & HDW draft “Joint-Statement”

42

Ultimately, things looked more like White’s Plan than

that of Keynes.

This isn’t surprising given the asymmetry of bargaining power.

43

And Keynes was content…

44

“the Harry White Plan is not a firm offer.

The real risk is that there will be no plan at all and that Congress will run

away from their own proposal. No harm…if the Americans work up a

certain amount of patriotic fervour for their own version. Much can be done in detail hereafter to improve it. The great thing at this stage is that they should get thoroughly committed to

there being some plan…”--Keynes to Phillips, April 1943

45

II. Creation of the BWS

1. Keynes and White2. Keynes versus White3. The Bretton Woods Conference• Another Gold Standard System?

46

By the autumn of 1943, Britain and the United States had sorted out

essentially all of the details for the International

Monetary Fund.

47

After GB and the US had reached agreement, the

rest of the world was invited to Bretton Woods, NH, in July 1944 for the United Nations Monetary and Financial Conference.

48

49

Mount Washington Hotel, Bretton Woods, NH

Keynes and White dominated the conference.

Essentially nothing was changed from their earlier

agreement.

And all but 1—the USSR—of the 45 invited nations eventually signed on. 50

The International Monetary Fund and the International

Bank for Reconstruction and Development (precursor to

the World Bank) were created with a ceremonial

signing 27 December 1945.51

II. Creation of the BWS

1. Keynes and White2. Keynes versus White3. The Bretton Woods Conference4. Another Gold Standard System?

52

Keynes had originally proposed that gold be replaced with a new international currency (“unitas”).

Unitas could be linked to gold but its supply would be regulated by

the IMF.

Combined with IMF reserve management and periodic ER

adjustments, Keynes believed this would prevent states from fighting

over a limited supply of gold. 53

The US, however, liked the idea of continuing to use gold or “any

currency backed by gold” as the Nth Currency.

After all, the US had all of the gold!

The US did not want to cede control over its extensive reserves

to an international regime.

As with trade, the US got its way.54

The textbooks suggest that “under the Bretton Woods

system, the world was on a gold standard once

removed.” (Colander 2006, 482)

So, was the BWS really just a modified GS?

55

It depends on your preferred emphasis.

56

The BWS formally preserved a special role for gold.

But it substantively recognized—for perhaps the

first time—the priority of internal over external

stability.57

Remember Keynes’s insight: the informal “rule of the gold standard game” was that states would use their monetary policies to initiate internal adjustment to maintain

external balance.

By contrast, the informal “rule of the BWS game” was that the IMF

would facilitate external adjustment, freeing monetary

policy to focus on internal macroeconomic objectives. 58

Lec 14: The Bretton Woods System

I. Keynes’ VisionII. Creation of the Bretton Woods

SystemIII.History of the Bretton Woods

System

59

Notice the familiar pattern with the creation of the

postwar order:

Great Britain and the United States forge an agreement

(biased towards the US) and the countries outside the

Soviet orbit sign on…60

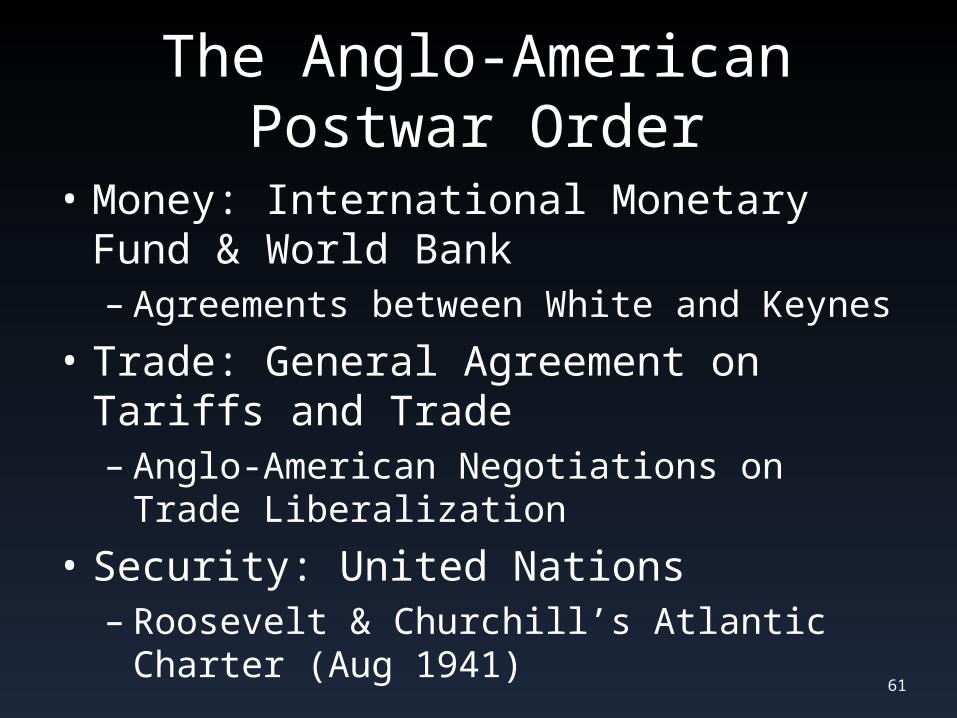

The Anglo-American Postwar Order

• Money: International Monetary Fund & World Bank– Agreements between White and Keynes

• Trade: General Agreement on Tariffs and Trade– Anglo-American Negotiations on Trade

Liberalization

• Security: United Nations– Roosevelt & Churchill’s Atlantic Charter

(Aug 1941) 61

The early history of the IMF was also defined by Anglo-

American relations in 1947…

62

Britain’s Postwar Financial Position

• 1938-1947– British money supply tripled– But GDP only doubled (to £10.5bn)

• Private and official gold & dollars down 50%

• Overseas sterling balances > £3.5bn• UK Reserves: Just over £0.5bn

In sum: maintaining convertibility at the prewar parity was going to be very, very difficult

63

Restoring Convertibility

• US feared Imperial Preference• US demanded Britain restore

convertibility ensure level field for US exporters

• Keynes resisted– GB needed Imperial Preference to resolve

BoP– Negotiated US loan to build up reserves

• JMK: getting the loan was “absolute hell”• Easter Sunday, 1946: Keynes died– (First heart attacks had been at Bretton

Woods)64

Sterling Crisis of 1947

• Anglo-American Loan– GB gets $3.75bn loan from US – But GB must restore convertibility

immediately (5 years earlier than required by BWS)

• 15 July 1947: Pound is convertible at $4.03– Devalued from pre-WWI parity of $4.86; but

still overvalued

• Results– Loan exhausted within weeks (not decade as

planned) GB suspended convertibility again

65

The 1947 Sterling Crisis unambiguously confirmed the financial weakness of western

Europe.

The BWS required countries to have either gold or dollars, but

Europe had neither.

The postwar order depended on the US remedying this

“dollar gap.” 66

The Sterling Crisis inspired political pressure in US to (1) allow greater devaluations in Europe; and (2) furnish more

robust aid.

67

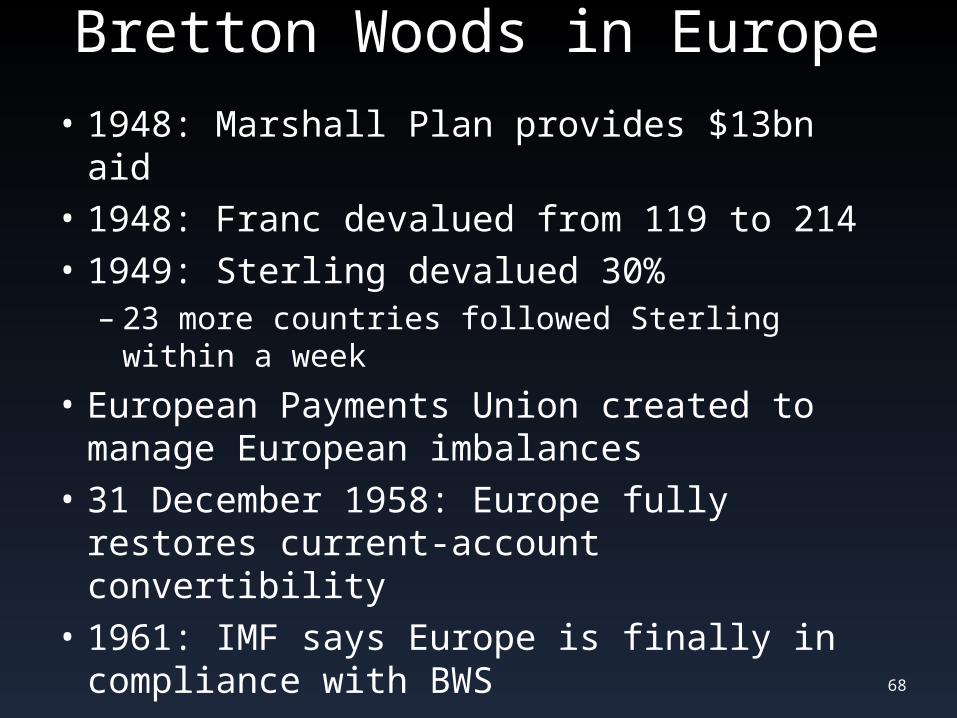

Bretton Woods in Europe

• 1948: Marshall Plan provides $13bn aid• 1948: Franc devalued from 119 to 214• 1949: Sterling devalued 30%– 23 more countries followed Sterling within

a week

• European Payments Union created to manage European imbalances

• 31 December 1958: Europe fully restores current-account convertibility

• 1961: IMF says Europe is finally in compliance with BWS

68

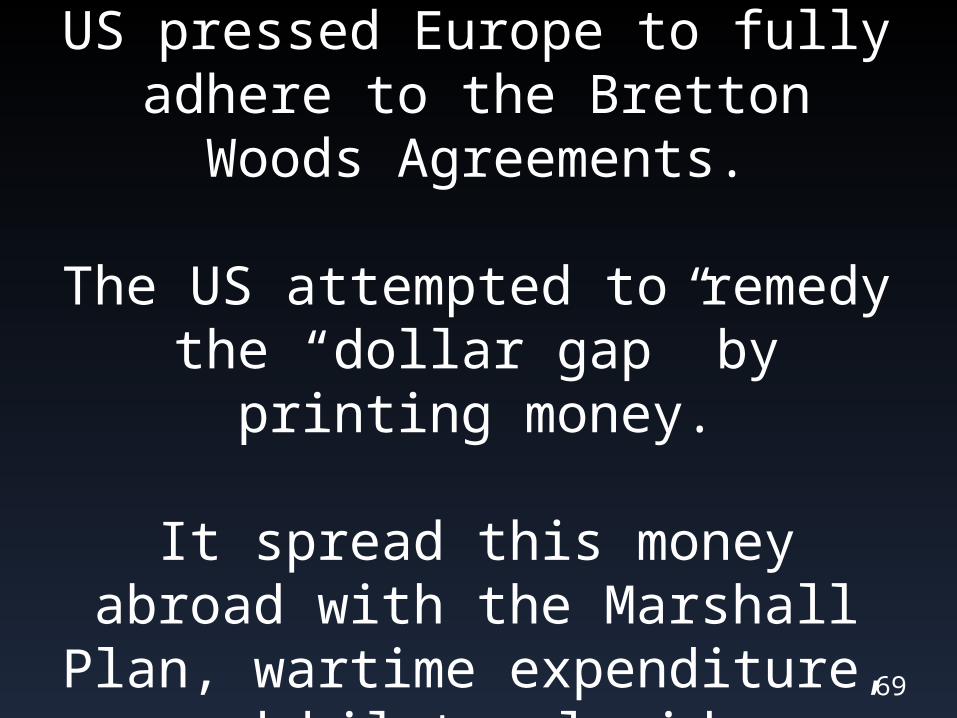

Throughout the 1950s, the US pressed Europe to fully adhere

to the Bretton Woods Agreements.

The US attempted to remedy the “dollar gap” by printing

money.

It spread this money abroad with the Marshall Plan,

wartime expenditure, and bilateral aid.

69

The Changing US Position• Changing Reserves– 1948: US has 2/3rds of global reserves– 1958: US has ½ of global reserves

• 1949-1950: US current-account surplus dropped by > 50%, to $3bn/year

• By early 1960s, US is consistently running trade deficits

• 1960: US foreign monetary liabilities exceed US gold reserves

• 1963: US liabilities to foreign monetary authorities exceed US gold reserves

70

The Vietnam War and the Great Society deepened these

trends.

By the late 1960s, “dollar gap” had given way to “dollar glut.”

The market price of gold rose well above $35/oz and the holders of dollars became

concerned. 71

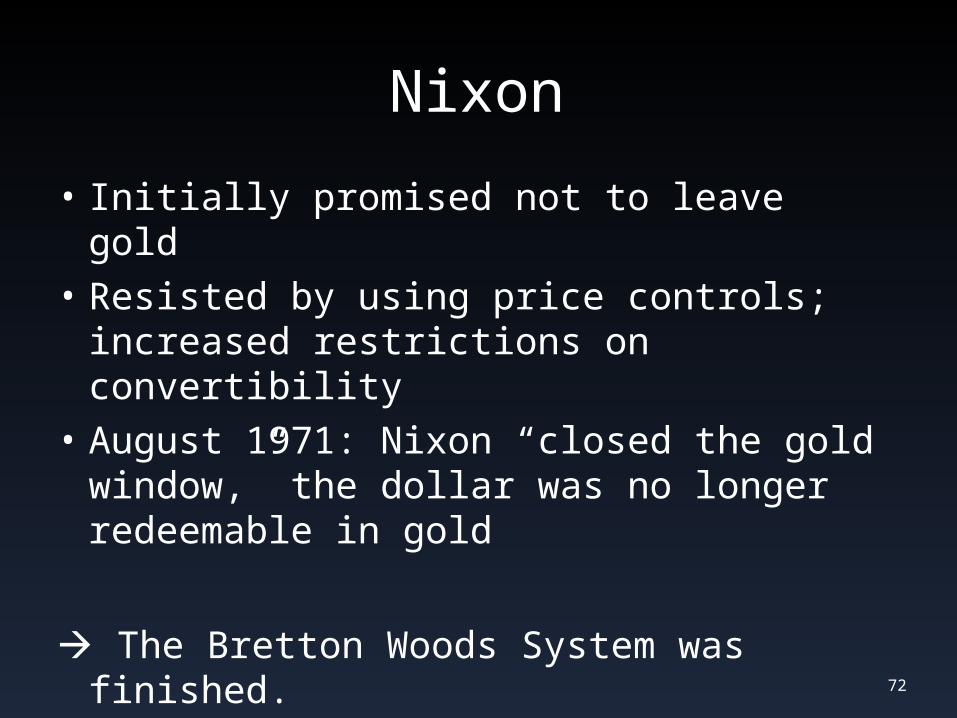

Nixon

• Initially promised not to leave gold• Resisted by using price controls;

increased restrictions on convertibility

• August 1971: Nixon “closed the gold window,” the dollar was no longer redeemable in gold

The Bretton Woods System was finished.

72

[Bonus Slides]

73

Reconciling Imbalances of Payments...

73

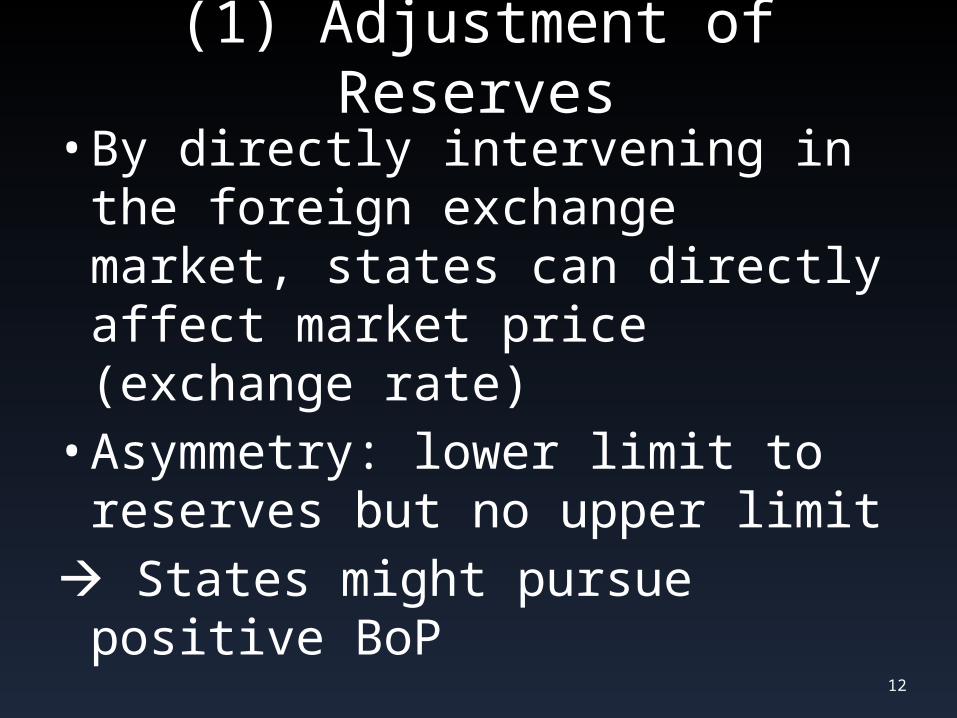

(1) Adjustment of Reserves

• By directly intervening in the foreign exchange market, states can directly affect market price (exchange rate)• Asymmetry: lower limit to

reserves but no upper limit States might pursue positive

BoP12

(2) Adjustment of Internal Prices & Incomes

• Uses price-specie-flow– imbalance inflation/deflation– Change in price levels counters

imbalanced demand

• Problem: domestic price levels are subjected to global economic forces– Politicians don’t like saying they

can’t/won’t redress unemployment problems!

13

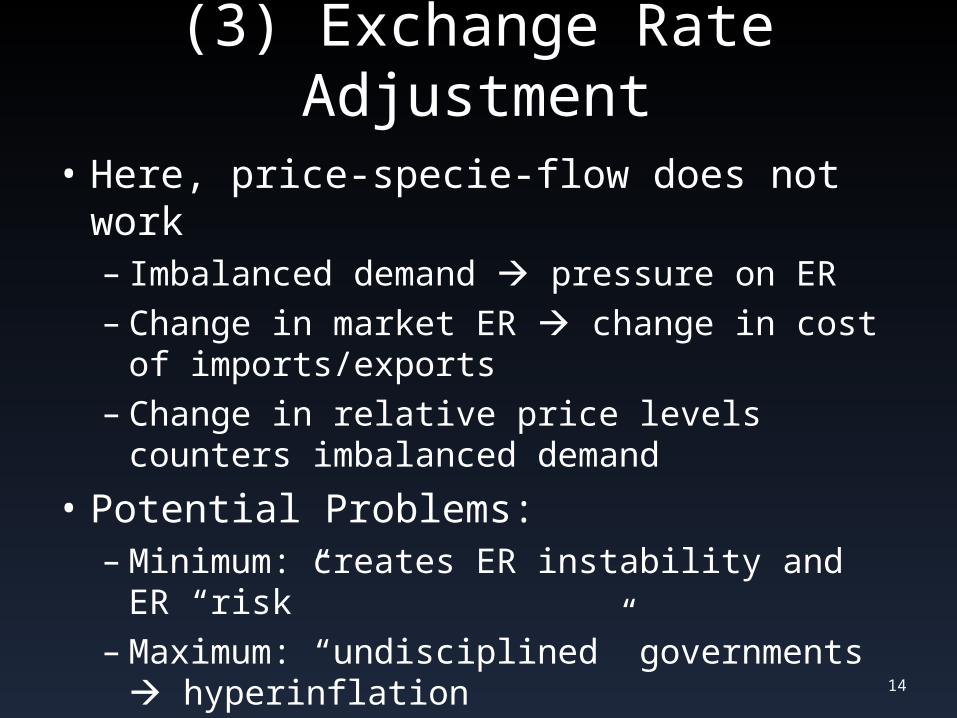

(3) Exchange Rate Adjustment

• Here, price-specie-flow does not work– Imbalanced demand pressure on ER– Change in market ER change in cost

of imports/exports– Change in relative price levels counters

imbalanced demand

• Potential Problems: –Minimum: creates ER instability and ER

“risk”–Maximum: “undisciplined” governments

hyperinflation 14

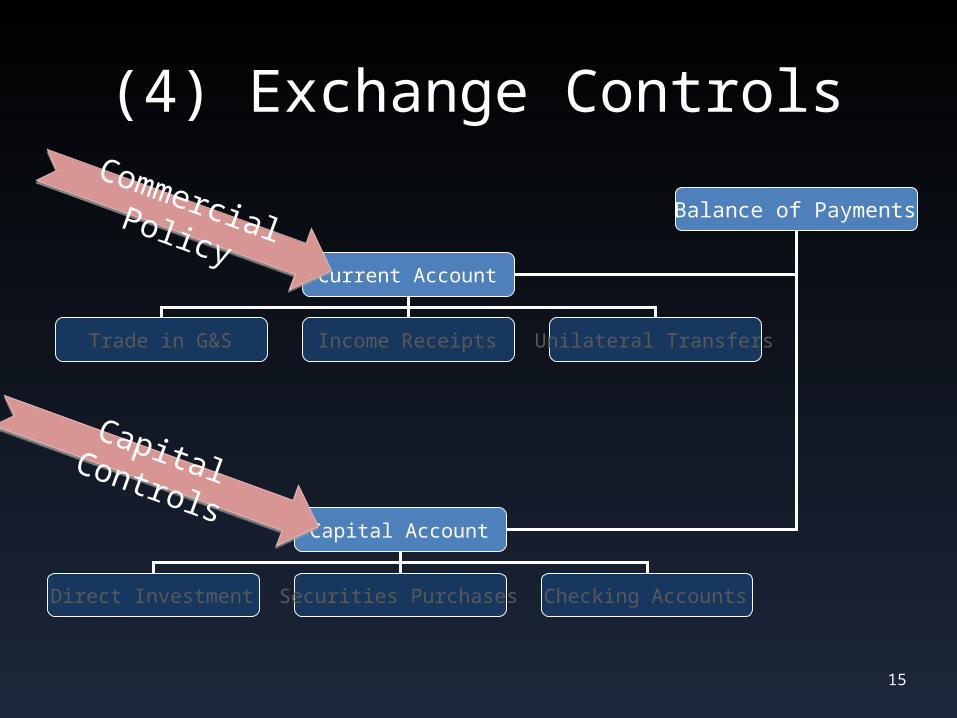

15

(4) Exchange Controls

Balance of Payments

Current Account

Capital Account

Trade in G&S Income Receipts Unilateral Transfers

Direct Investment Securities Purchases Checking Accounts

Commercial Policy

Capital Controls

Was the BWS “knave proof”?

73

Remember that one of the principal motivations for

pegging a currency to gold was to tie policymakers’

hands—to make the monetary system “knave-

proof”—to prevent excessive monetary growth.

74

Judged by this standard, how effectively did the BWS

mimic the GS?

(Consider the course of the dollar between 1945 and 1971.)

75