the bbwe wine model growth and returns · •summary foster’s strategy • bbwe strategy overview...

TRANSCRIPT

The BBWE Wine Model Growth and Returns

The BBWE Wine Model Growth and Returns

Presentation by Walt Klenz

ABN-AMRO Wine Conference, 24 April 2002

Presentation by Walt Klenz

ABN-AMRO Wine Conference, 24 April 2002

AgendaAgenda

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

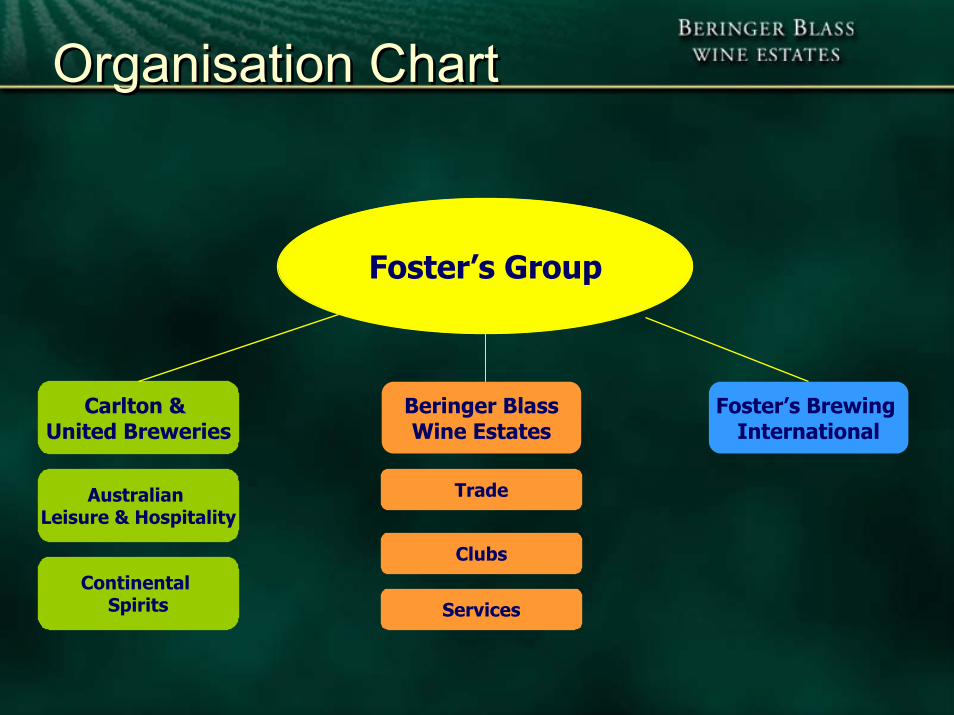

Organisation ChartOrganisation Chart

Foster’s Group

Carlton & United Breweries

Beringer BlassWine Estates

Australian Leisure & Hospitality

Continental Spirits

Foster’s Brewing International

Trade

Clubs

Services

Foster’s Points of DifferenceFoster’s Points of Difference

• Business mix• Steady, non-cyclical returns• Funded recent growth in wine• Beer/wine mix creates value

for shareholders

• Business mix• Steady, non-cyclical returns• Funded recent growth in wine• Beer/wine mix creates value

for shareholders

Share of EBITA & CCE by Product & GeographyFoster’s Business/Geographic MixFoster’s Business/Geographic Mix

EBITA by Product EBITA by Geography

Australia

Int’l

Wine

Other

CCE by Product

Wine

Other

CCE by Geography

AustraliaInt’l

Foster’s Group ReturnsFoster’s Group Returns

11.1

13.8

16.3

13.812.2

13.3

13.210.7

16.5

19.0

1997 1998 1999 2000 2001

Weighted Average Cost Of Capital

Return on Capital Employed

‘ROCE is calculated as EBITA on capital employed’

AgendaAgenda

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

BBWE StrategyBBWE Strategy• International portfolio of premium varietal

wine brands.

• Distribution strength in world’s high-growth premium wine markets.

• 3-channel business model.

= Growth + Returns

• International portfolio of premium varietalwine brands.

• Distribution strength in world’s high-growth premium wine markets.

• 3-channel business model.

= Growth + Returns

Wine GrowthWine GrowthCase Sales, EBITA for Wine Group F97-F01

0

2000

4000

6000

8000

10000

12000

14000

16000

F97 F98 F99 F00 F01

Cases (000s)

0

100

200

300

400

F97 F98 F99 F00 F01

+27% +48%+44%

+27%

+122%CAGR = +56.8%

A$million

F01 includes 9 months’ result for BWE.

Wine ReturnsWine ReturnsAverage ROCE for Wine Group F97-F01

ROCE is calculated as EBITA on capital employed. F01 includes 9 months’ result for BWE.

9.910.29.0

12.3

13.7

F97 F98 F99 F00 F01

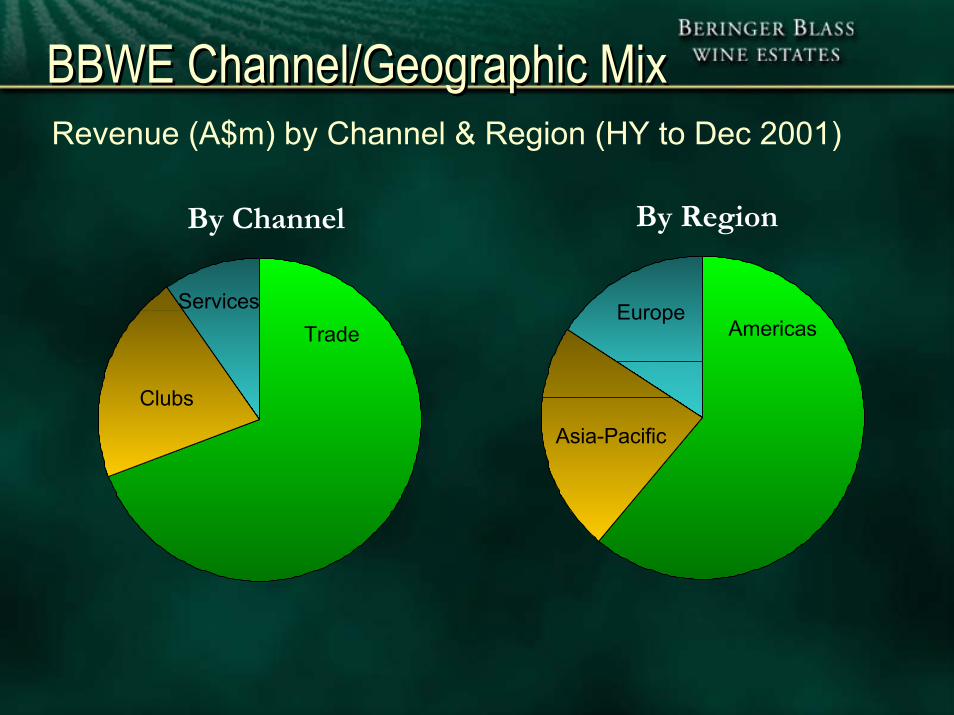

BBWE Channel/Geographic MixBBWE Channel/Geographic MixRevenue (A$m) by Channel & Region (HY to Dec 2001)

By Channel By Region

Trade Americas

Clubs

Services

Asia-Pacific

Europe

BBWE StructureBBWE StructureWalt Klenz

Managing Director

Jim WatkinsPresident Americas

Jamie OdellMD Trade Asia

Pacific

John PhilipsMD Europe, Middle

East, Africa

Pete ScottCFO

Mark EmersonGlobal Wine

Clubs

Global Wine Services

AgendaAgenda

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

Trade ChannelTrade Channel

• Priority focus, accounting for over two-thirds of total wine EBITA.

• Regional structure.• Global brands

- Wolf Blass- Beringer

• Key markets- North America- Australia/Asia Pacific- UK, Europe.

• Priority focus, accounting for over two-thirds of total wine EBITA.

• Regional structure.• Global brands

- Wolf Blass- Beringer

• Key markets- North America- Australia/Asia Pacific- UK, Europe.

Trade InitiativesTrade Initiatives• Improve ROCE by expanding

outsourcing model and continuing to build/leverage brand equity.

• Grow $US6-8 category in US.• Grow Australian brand set in

North America.• Grow core brands in

Australia.• Improve market share in

UK/Europe.

• Improve ROCE by expanding outsourcing model and continuing to build/leverage brand equity.

• Grow $US6-8 category in US.• Grow Australian brand set in

North America.• Grow core brands in

Australia.• Improve market share in

UK/Europe.

Trade Point of DifferenceTrade Point of Difference

• Geographic diversification/balance.

• Strong market share in North America and Asia Pacific, with upside potential in Europe.

• Portfolio targeted at high-value end of bottled wine market.

• Geographic diversification/balance.

• Strong market share in North America and Asia Pacific, with upside potential in Europe.

• Portfolio targeted at high-value end of bottled wine market.

Global Wine BrandsGlobal Wine BrandsWolf Blass• #3 brand by value in Australia.• #1 Australian brand in Canada,

HK, Singapore; #3 in Ireland.• Growth potential in U.S, UK,

mainland Europe.• Leveraging super-premium brand

equity.

Wolf Blass• #3 brand by value in Australia.• #1 Australian brand in Canada,

HK, Singapore; #3 in Ireland.• Growth potential in U.S, UK,

mainland Europe.• Leveraging super-premium brand

equity.

Global Wine BrandsGlobal Wine BrandsBeringer• Spans all price points of target

market in U.S.• Only winery to have both a red

and a white wine named “Wine of the Year” by Wine Spectator.

• Dominates blush category with leading market share.

• Exports growing.

Beringer• Spans all price points of target

market in U.S.• Only winery to have both a red

and a white wine named “Wine of the Year” by Wine Spectator.

• Dominates blush category with leading market share.

• Exports growing.

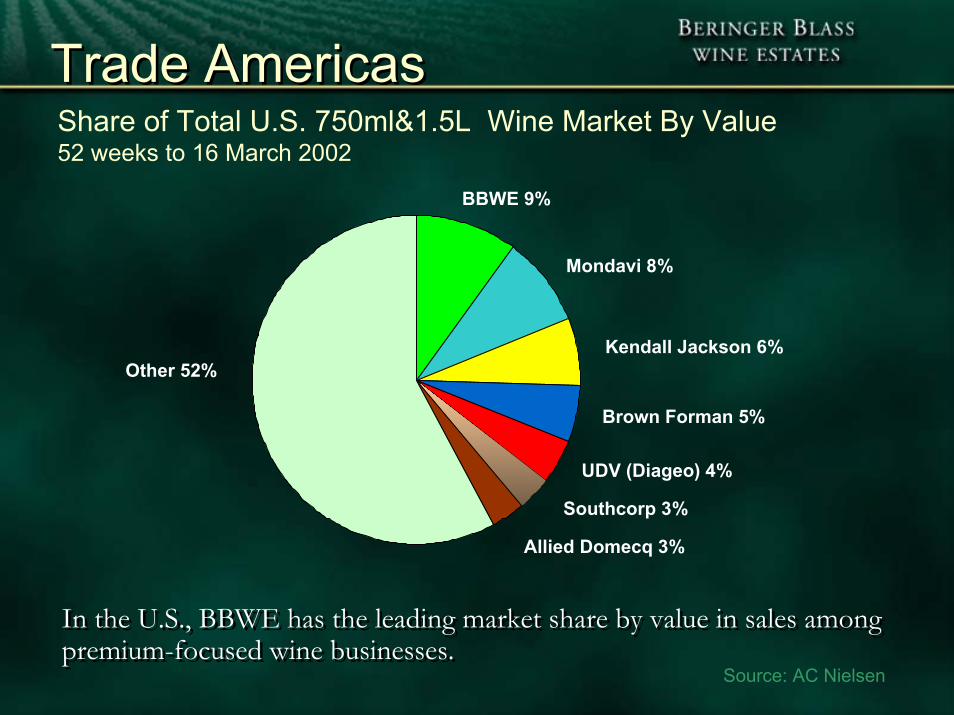

Trade AmericasTrade AmericasShare of Total U.S. 750ml&1.5L Wine Market By Value52 weeks to 16 March 2002

BBWE 9%

Brown Forman 5%

Other 52%

Mondavi 8%

Kendall Jackson 6%

UDV (Diageo) 4%

Allied Domecq 3%

Southcorp 3%

In the U.S., BBWE has the leading market share by value in sales among premium-focused wine businesses.In the U.S., BBWE has the leading market share by value in sales among premium-focused wine businesses.

Source: AC Nielsen

Trade AmericasTrade AmericasU.S. Value Growth BBWE Brands vs Total Food & Drug52 Weeks ending March 16, 2002

U.S. Domestic Brands*

Australian Brands*

U.S. Domestic Brands*

Australian Brands*

BBWEMkt Share#

BBWEMkt Share#

BBWEGrowthBBWEGrowth

CategoryGrowth

CategoryGrowth

+18%

+28%

+18%

+28%+7%

+21%

+7%

+21%

10.6%

9.4%

10.6%

9.4%

*All 750ml + 1.5 litre varietal wines# By value

Source:AC Nielsen

BBWE is substantially outgrowing the market in both the U.S.-produced and Australian brand segments.BBWE is substantially outgrowing the market in both the U.S.-produced and Australian brand segments.

Trade Asia PacificTrade Asia Pacific

By Volume

Southcorp 27%

BRL Hardy 11%

BBWE 10%

Orlando 12%

Other 40%

Share of Australian Bottled Wine Market in Scan Data 12 weeks to Feb 02

By Value

Southcorp 25%

BRL Hardy 10%

BBWE 12%

Orlando 11%

Other 42%

In Australia, BBWE has #2 market share in bottled wine by value, due to its concentration in the high-value, high-growth >$10 price segments.In Australia, BBWE has #2 market share in bottled wine by value, due to its concentration in the high-value, high-growth >$10 price segments.

Source: AC Nielsen

Trade Asia PacificTrade Asia PacificAustralian Volume Growth BBWE Brands vs Total ScanData52 Weeks ending February, 2002

All Bottled WineAll Bottled Wine

BBWEGrowth#BBWE

Growth#CategoryGrowth#CategoryGrowth#

+19%+19%+2%+2%

# By volume

BBWE brand sales volumes are substantially outgrowing the bottled wine market in Australia.BBWE brand sales volumes are substantially outgrowing the bottled wine market in Australia.

Source:AC Nielsen

Trade EuropeTrade EuropeBBWE’s Premium Market Share by Value in U.K. Vs USA & Aust.

9%

4%

12%

0%

2%

4%

6%

8%

10%

12%

14%

US Australia UK

BBWE’s under-representation in the U.K. provides a key growth opportunity.BBWE’s under-representation in the U.K. provides a key growth opportunity.

Source: AC Nielsen, Company Estimates

Wine ClubsWine Clubs

• Global Structure.• Key initiatives:

- Maintain moderate growth in Australia.

- Transfer business models to UK/Europe.

- Grow U.S. business.

• Global Structure.• Key initiatives:

- Maintain moderate growth in Australia.

- Transfer business models to UK/Europe.

- Grow U.S. business.

Wine ServicesWine Services• Global Structure.• Key initiatives:

- Solid organic growth for global business

- Enhancement of “one-stop shop” concept in Australia and Europe with assessment for other markets

- Scope to vertically integrate into dry goods manufacture.

- Maintain returns in high teens.

• Global Structure.• Key initiatives:

- Solid organic growth for global business

- Enhancement of “one-stop shop” concept in Australia and Europe with assessment for other markets

- Scope to vertically integrate into dry goods manufacture.

- Maintain returns in high teens.

AgendaAgenda

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

Financial ObjectivesFinancial Objectives

• Growth• Growth

• Profitability

• Returns• Returns

• Cash Flow

• Profitability

• Cash Flow

AgendaAgenda

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

• Foster’s Strategy

• BBWE Strategy

• Overview of Channels

• Financial Performance Objectives

• Summary

SummarySummary

• Build global brands/drive organic growth

• Build strong geographic trade organizations

• Continue to build on 3 channel strategy

• Bolt-on acquisitions in key markets

A Global Leader in Premium WineA Global Leader in Premium Wine