telecom italia · telecom italia morgan stanley 11th annual technology media & telecoms...

TRANSCRIPT

Telecom Italia

Morgan Stanley 11th Annual Technology Media & Telecoms Conference

Barcelona, November 17, 2011

TELECOM ITALIA GROUP

MARCO PATUANO – Chief Operating Officer

1 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

Safe Harbour

These presentations contain statements that constitute forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995. These statements appear in a number of places in this

presentation and include statements regarding the intent, belief or current expectations of the customer base,

estimates regarding future growth in the different business lines and the global business, market share, financial

results and other aspects of the activities and situation relating to the Company and the Group.

Such forward looking statements are not guarantees of future performance and involve risks and uncertainties, and

actual results may differ materially from those projected or implied in the forward looking statements as a result of

various factors.

Forward-looking information is based on certain key assumptions which we believe to be reasonable as of the date

hereof, but forward looking information by its nature involves risks and uncertainties, which are outside our control,

and could significantly affect expected results.

Analysts are cautioned not to place undue reliance on those forward looking statements, which speak only as of the

date of this presentation. Telecom Italia S.p.A. undertakes no obligation to release publicly the results of any

revisions to these forward looking statements which may be made to reflect events and circumstances after the

date of this presentation, including, without limitation, changes in Telecom Italia S.p.A. business or acquisition

strategy or planned capital expenditures or to reflect the occurrence of unanticipated events. Analysts and investors

are encouraged to consult the Company's Annual Report on Form 20-F as well as periodic filings made on Form 6-K,

which are on file with the United States Securities and Exchange Commission.

2 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

Agenda

► TI Group 3Q11 Progress Report

► Focus on Domestic Mobile Market

► Focus on Domestic Fixed Market

► Conclusions

3 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

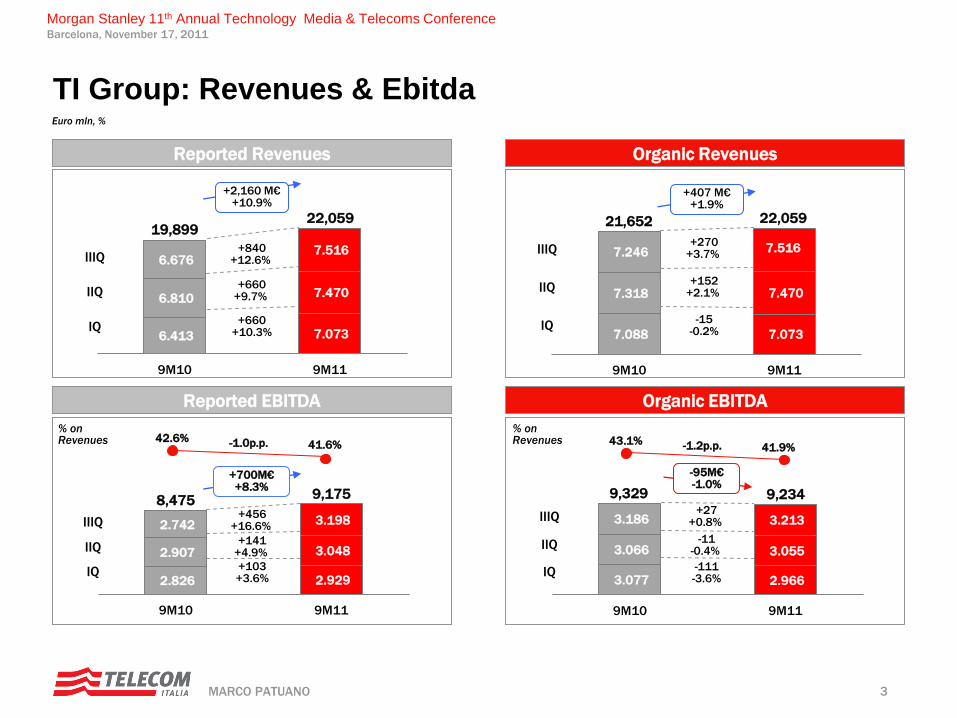

7.088 7.073

7.318 7.470

7.246 7.516

9M10 9M11

Euro mln, %

Reported EBITDA

Reported Revenues Organic Revenues

Organic EBITDA

42.6% 41.6%

+2,160 M€ +10.9%

% on Revenues

% on Revenues -1.0p.p.

+660 +9.7%

+660 +10.3%

19,899 22,059

IIQ

IQ

TI Group: Revenues & Ebitda

IIIQ +840

+12.6%

+407 M€ +1.9%

+152 +2.1%

-15 -0.2%

21,652 22,059

IIQ

IQ

IIIQ +270

+3.7%

IIQ

IQ

IIIQ

8,475 9,175

+141 +4.9%

+103 +3.6%

+456 +16.6%

43.1% 41.9% -1.2p.p.

9,329 9,234

-95M€ -1.0%

-11 -0.4%

-111 -3.6%

+27 +0.8%

IIQ

IQ

IIIQ

6.413 7.073

6.810 7.470

6.676 7.516

9M10 9M11

+700M€ +8.3%

3.077 2.966

3.066 3.055

3.186 3.213

9M10 9M11

2.826 2.929

2.907 3.048

2.742 3.198

9M10 9M11

4 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

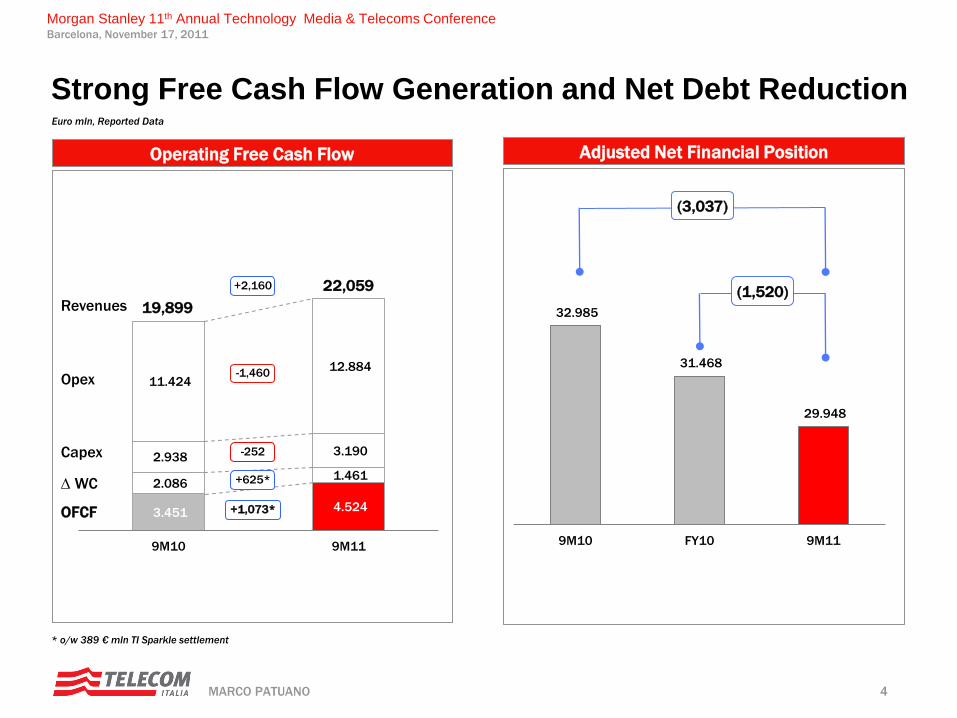

3.451 4.524

2.086 1.461

2.938 3.190

11.424

12.884

9M10 9M11

Euro mln, Reported Data

Operating Free Cash Flow

Revenues

Opex

Capex

D WC

OFCF

19,899

22,059 +2,160

-252

+625*

+1,073*

-1,460

* o/w 389 € mln TI Sparkle settlement

Strong Free Cash Flow Generation and Net Debt Reduction

32.985

31.468

29.948

9M10 FY10 9M11

Adjusted Net Financial Position

(3,037)

(1,520)

5 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

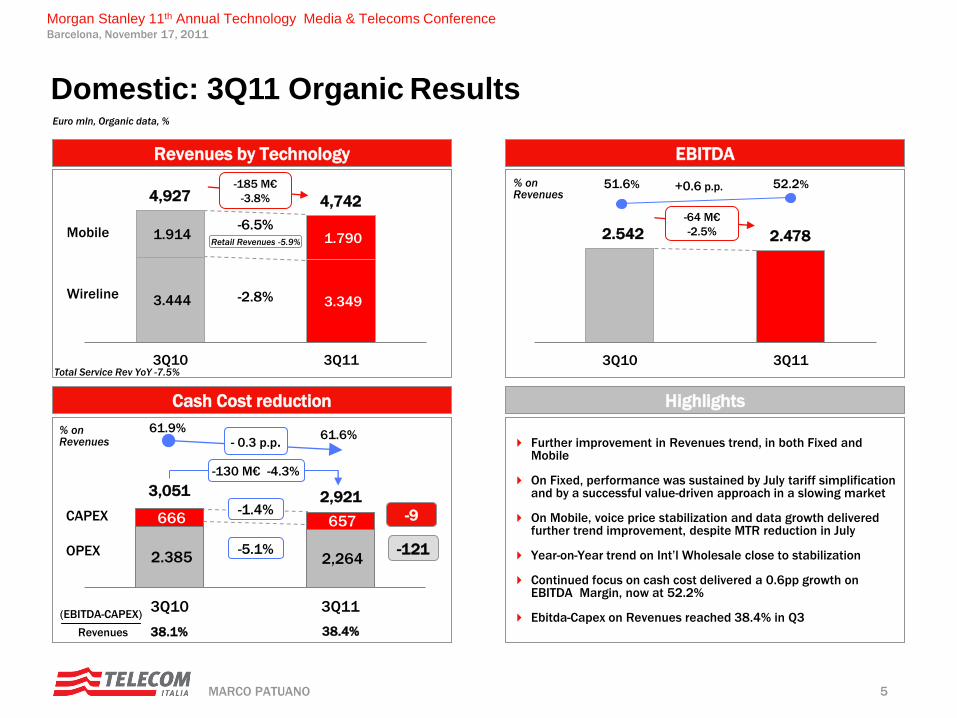

3.444 3.349

1.914 1.790

3Q10 3Q11

2.542 2.478

3Q10 3Q11

Domestic: 3Q11 Organic Results Euro mln, Organic data, %

Further improvement in Revenues trend, in both Fixed and Mobile

On Fixed, performance was sustained by July tariff simplification and by a successful value-driven approach in a slowing market

On Mobile, voice price stabilization and data growth delivered further trend improvement, despite MTR reduction in July

Year-on-Year trend on Int’l Wholesale close to stabilization

Continued focus on cash cost delivered a 0.6pp growth on EBITDA Margin, now at 52.2%

Ebitda-Capex on Revenues reached 38.4% in Q3

% on Revenues

-185 M€

-3.8%

-2.8% Wireline

4,927 4,742 -64 M€

-2.5%

51.6% 52.2% +0.6 p.p.

-6.5% Mobile

2.385 2,264

666 657

3Q10 3Q11

-9

-121

61.9% 61.6%

- 0.3 p.p.

CAPEX

-5.1% OPEX

-1.4%

-130 M€ -4.3%

3,051 2,921

% on Revenues

(EBITDA-CAPEX)

Revenues 38.1% 38.4%

Retail Revenues -5.9%

Total Service Rev YoY -7.5%

Cash Cost reduction

Revenues by Technology EBITDA

Highlights

6 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

Agenda

► TI Group 3Q11 Progress Report

► Focus on Domestic Mobile Market

► Focus on Domestic Market Fixed

► Conclusions

7 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

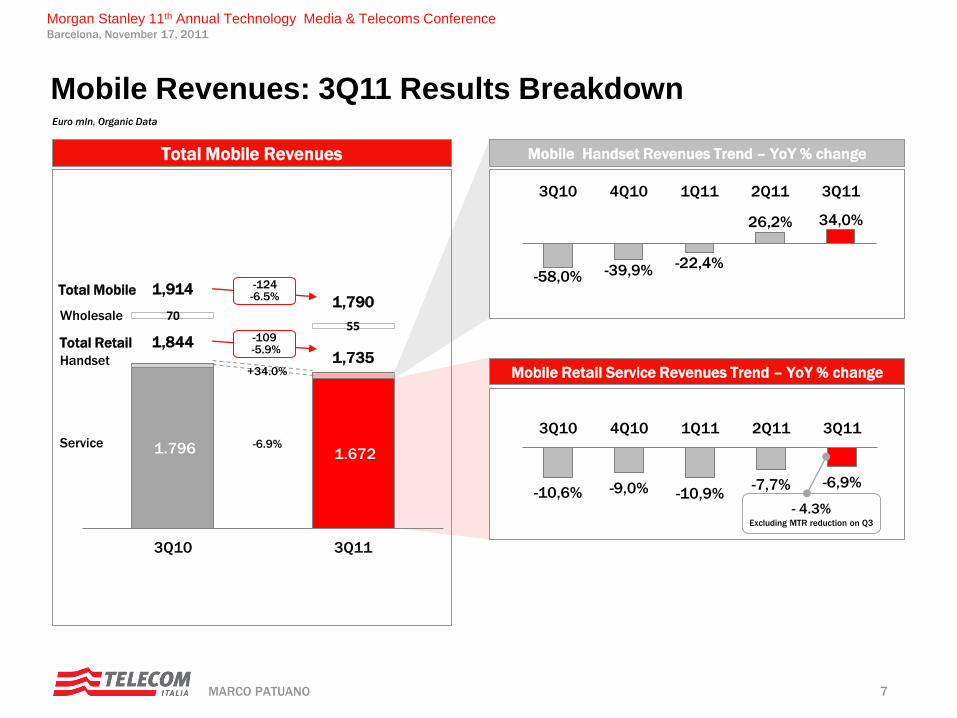

-10,6% -9,0% -10,9% -7,7% -6,9%

3Q10 4Q10 1Q11 2Q11 3Q11

1.796 1.672

70 55

3Q10 3Q11

+34.0%

Euro mln, Organic Data

Mobile Revenues: 3Q11 Results Breakdown

-58,0% -39,9% -22,4%

26,2% 34,0%

3Q10 4Q10 1Q11 2Q11 3Q11

- 4.3% Excluding MTR reduction on Q3

Total Mobile Revenues Mobile Handset Revenues Trend – YoY % change

Mobile Retail Service Revenues Trend – YoY % change

-124 -6.5%

1,914 Total Mobile 1,790

Total Retail 1,735

1,844

Wholesale

-109 -5.9%

Service -6.9%

Handset

8 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

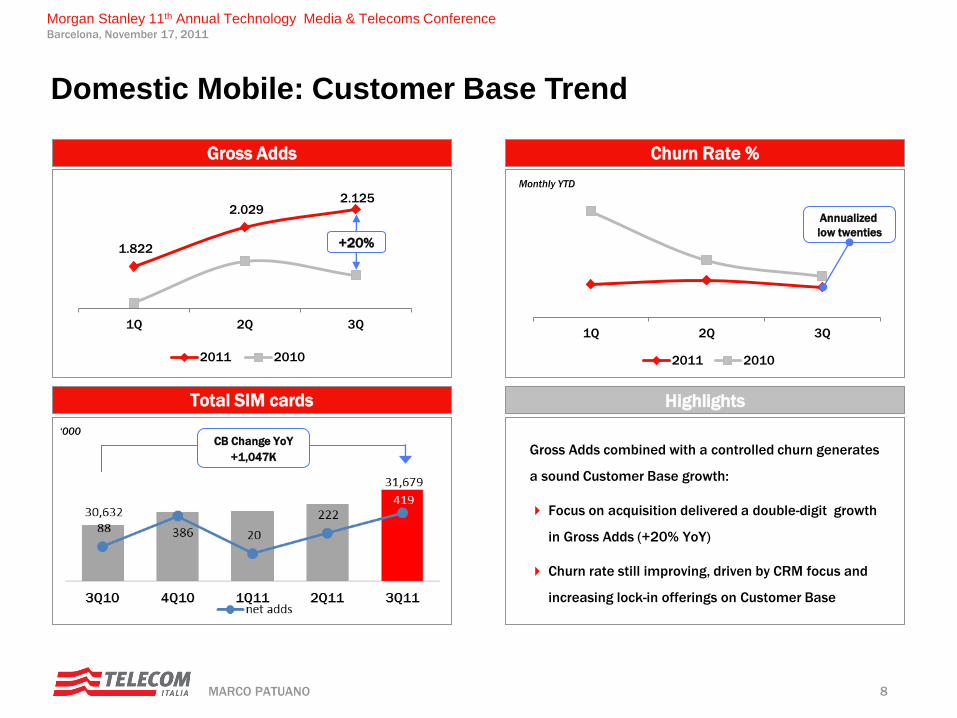

‘000

Gross Adds combined with a controlled churn generates

a sound Customer Base growth:

Focus on acquisition delivered a double-digit growth

in Gross Adds (+20% YoY)

Churn rate still improving, driven by CRM focus and

increasing lock-in offerings on Customer Base

Monthly YTD

1Q 2Q 3Q

2011 2010

1.822

2.029 2.125

1Q 2Q 3Q

2011 2010

+20%

Annualized

low twenties

Total SIM cards

Gross Adds Churn Rate %

Highlights

CB Change YoY

+1,047K

Domestic Mobile: Customer Base Trend

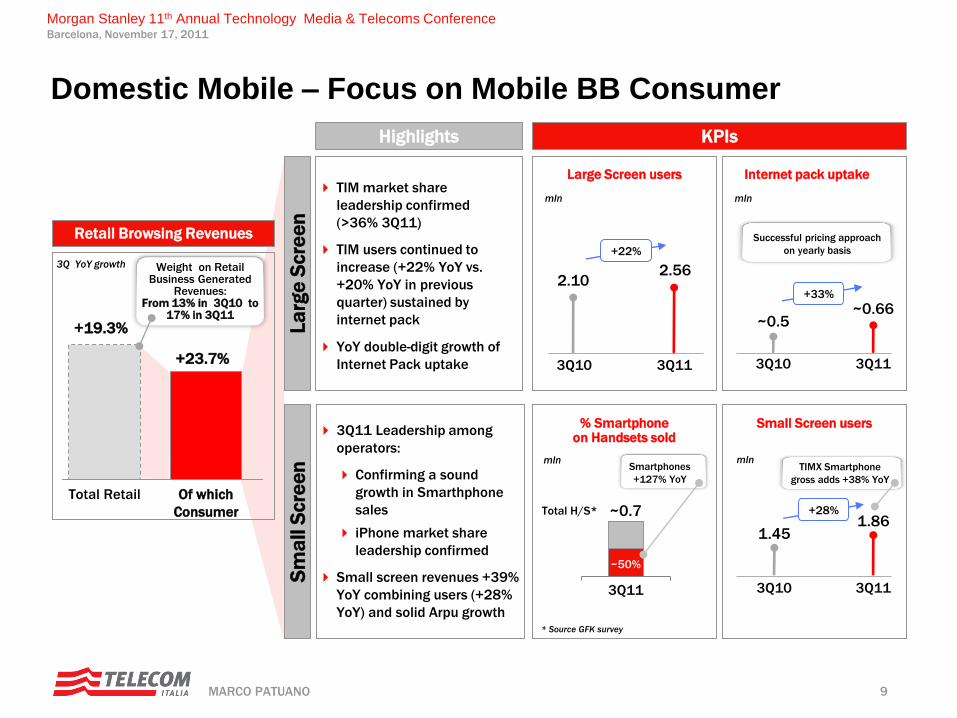

9 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

3Q11 Leadership among

operators:

Confirming a sound

growth in Smarthphone

sales

iPhone market share

leadership confirmed

Small screen revenues +39%

YoY combining users (+28%

YoY) and solid Arpu growth

TIM market share

leadership confirmed

(>36% 3Q11)

TIM users continued to

increase (+22% YoY vs.

+20% YoY in previous

quarter) sustained by

internet pack

YoY double-digit growth of

Internet Pack uptake 3Q10

+22%

3Q11

2.10 2.56

Large Screen users

mln

3Q10 3Q11

~0.5 ~0.66

Successful pricing approach

on yearly basis

Internet pack uptake

mln

% Smartphone on Handsets sold

mln

~50%

~0.7 Total H/S*

Smartphones

+127% YoY

3Q11

+33%

Small Screen users

mln

3Q10 3Q11

1.45 1.86

TIMX Smartphone

gross adds +38% YoY

+28%

* Source GFK survey

+19.3%

+23.7%

Total Retail Of which

Consumer

KPIs Highlights

Retail Browsing Revenues

3Q YoY growth Weight on Retail Business Generated

Revenues: From 13% in 3Q10 to

17% in 3Q11

Sm

all S

cre

en

L

arg

e S

cre

en

Domestic Mobile – Focus on Mobile BB Consumer

10 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

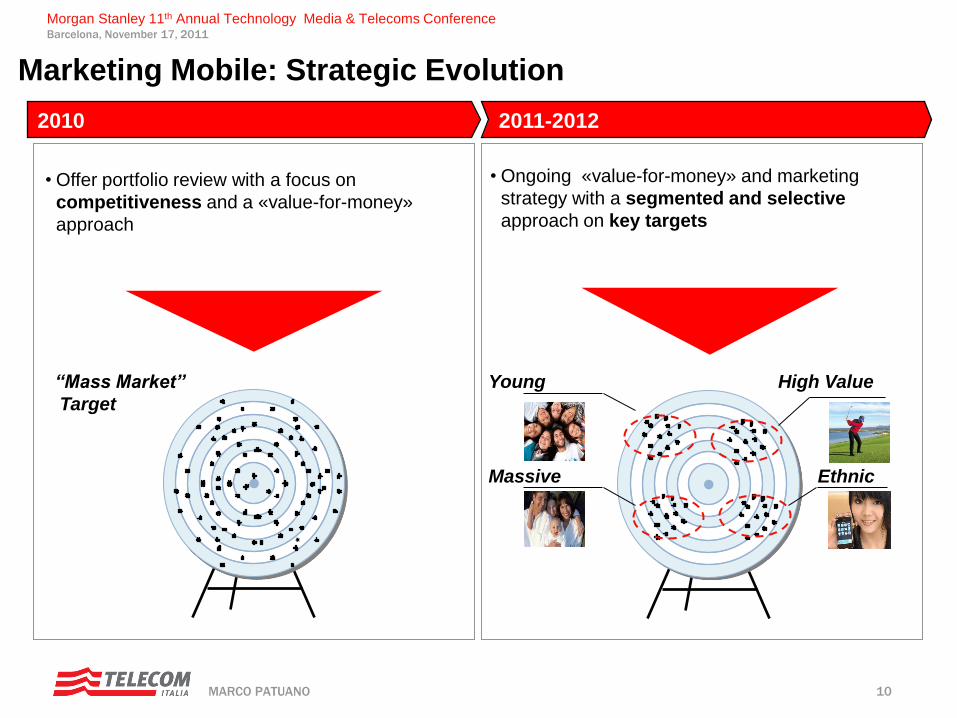

Marketing Mobile: Strategic Evolution

2010 2011-2012

• Offer portfolio review with a focus on

competitiveness and a «value-for-money»

approach

• Ongoing «value-for-money» and marketing

strategy with a segmented and selective

approach on key targets

“Mass Market”

Target

Young High Value

Ethnic Massive

11 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

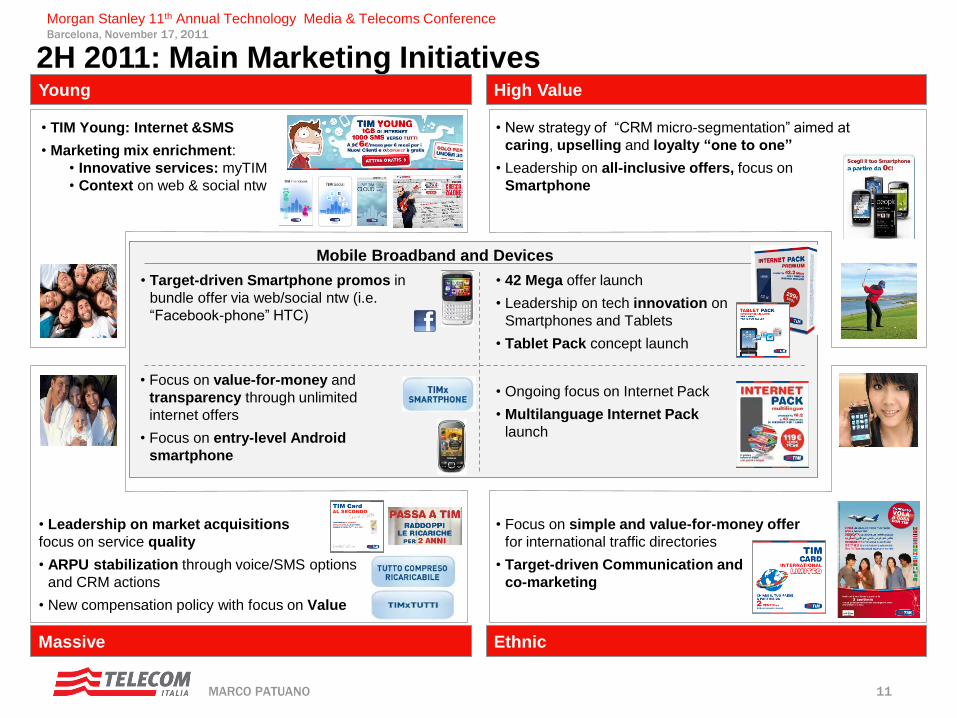

2H 2011: Main Marketing Initiatives Young High Value

Massive Ethnic

• TIM Young: Internet &SMS

• Marketing mix enrichment:

• Innovative services: myTIM

• Context on web & social ntw

• New strategy of “CRM micro-segmentation” aimed at

caring, upselling and loyalty “one to one”

• Leadership on all-inclusive offers, focus on

Smartphone

• Leadership on market acquisitions

focus on service quality

• ARPU stabilization through voice/SMS options

and CRM actions

• New compensation policy with focus on Value

• Focus on simple and value-for-money offer

for international traffic directories

• Target-driven Communication and

co-marketing

• Target-driven Smartphone promos in

bundle offer via web/social ntw (i.e.

“Facebook-phone” HTC)

• Focus on value-for-money and

transparency through unlimited

internet offers

• Focus on entry-level Android

smartphone

• 42 Mega offer launch

• Leadership on tech innovation on

Smartphones and Tablets

• Tablet Pack concept launch

• Ongoing focus on Internet Pack

• Multilanguage Internet Pack

launch

Mobile Broadband and Devices

12 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

Agenda

► TI Group 3Q11 Progress Report

► Focus on Domestic Mobile Market

► Focus on Domestic Fixed Market

► Conclusions

13 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

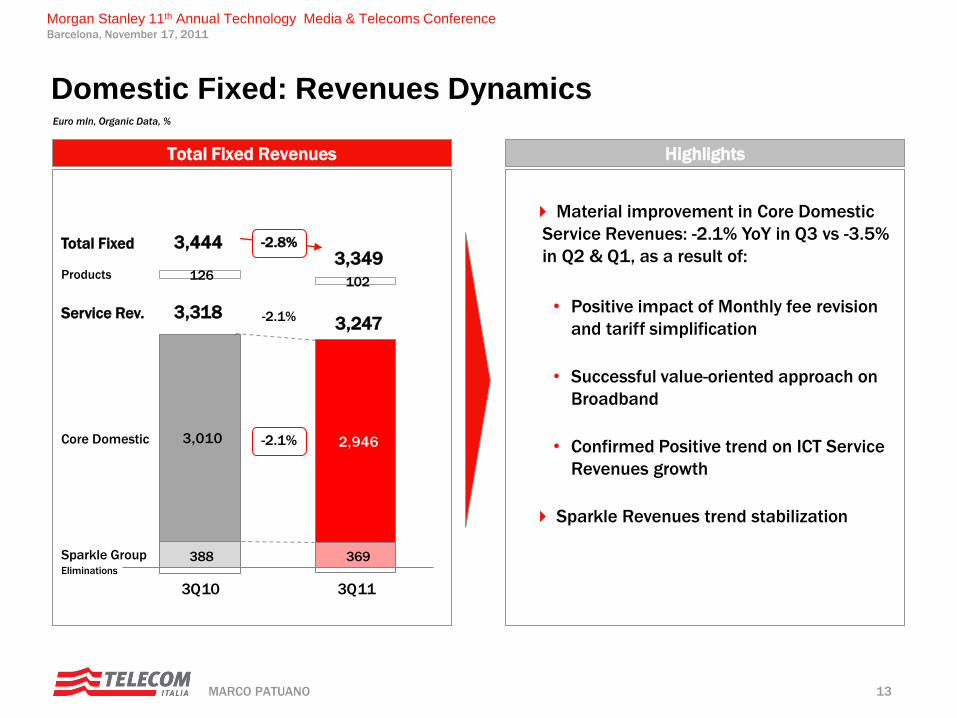

388

3,010 2,946

126 102

3Q10 3Q11

369

Euro mln, Organic Data, %

Domestic Fixed: Revenues Dynamics

Core Domestic

Products

Sparkle Group

Service Rev.

-2.8% Total Fixed 3,444 3,349

3,318 3,247

-2.1%

Eliminations

-2.1%

Material improvement in Core Domestic

Service Revenues: -2.1% YoY in Q3 vs -3.5%

in Q2 & Q1, as a result of:

• Positive impact of Monthly fee revision

and tariff simplification

• Successful value-oriented approach on

Broadband

• Confirmed Positive trend on ICT Service

Revenues growth

Sparkle Revenues trend stabilization

Total Fixed Revenues Highlights

14 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

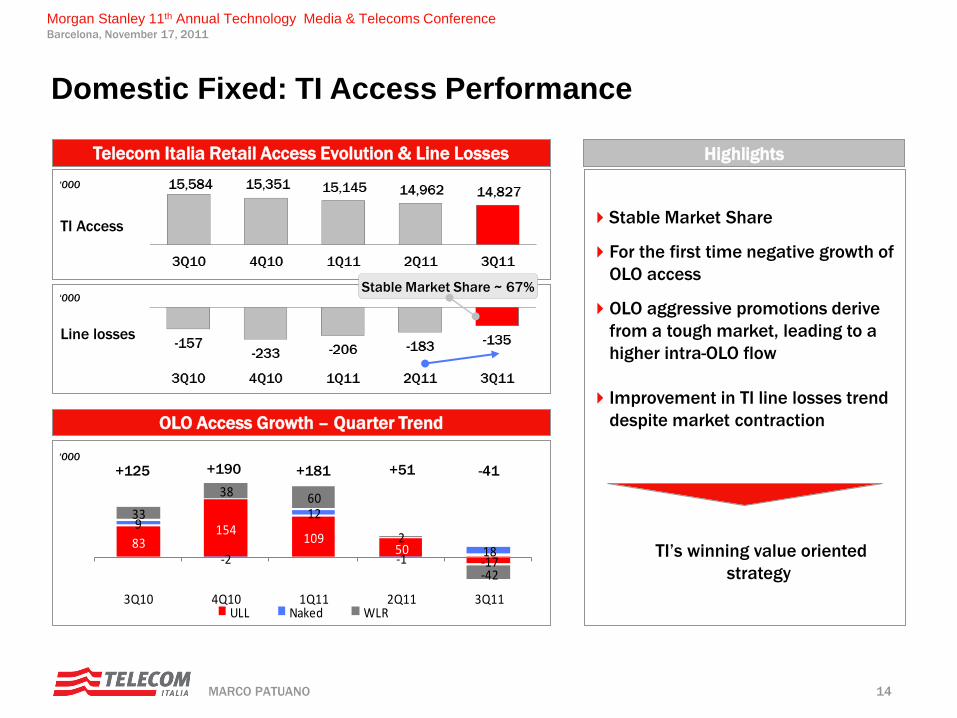

TI Access

Line losses

Stable Market Share

For the first time negative growth of

OLO access

OLO aggressive promotions derive

from a tough market, leading to a

higher intra-OLO flow

Improvement in TI line losses trend

despite market contraction

‘000

‘000

‘000

Stable Market Share ~ 67%

83154

10950

-17

9

-2

12

-118

33

38 60

2

-42

3Q10 4Q10 1Q11 2Q11 3Q11ULL Naked WLR

-41 +51 +181 +190 +125

Domestic Fixed: TI Access Performance

OLO Access Growth – Quarter Trend

Telecom Italia Retail Access Evolution & Line Losses Highlights

TI’s winning value oriented

strategy

15 MARCO PATUANO

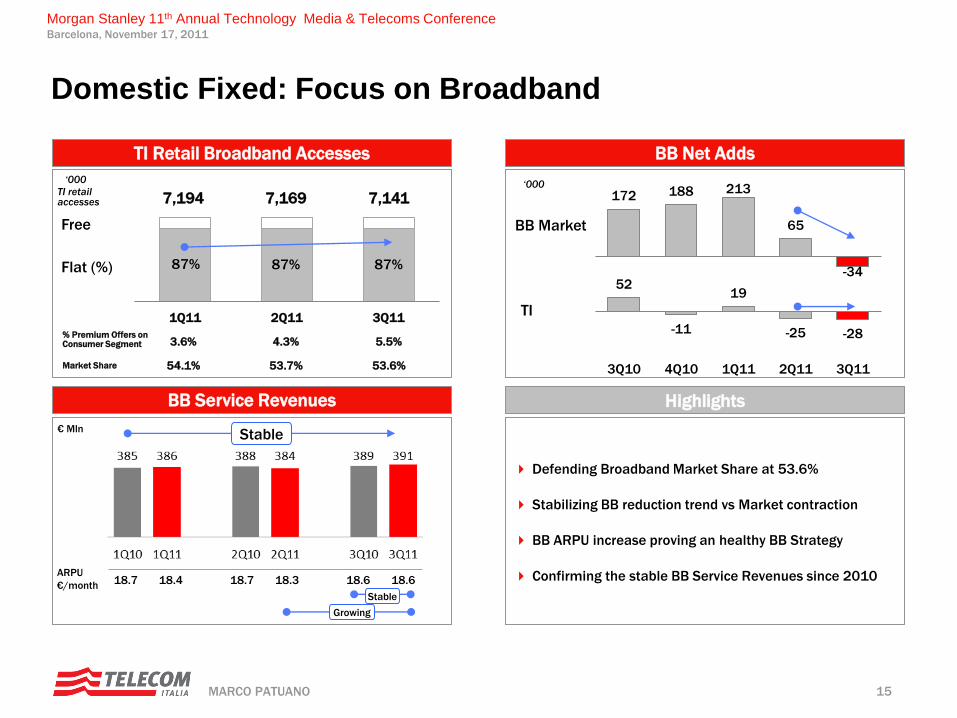

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

172 188 213

65

-34 52

-11

19

-25 -28

3Q10 4Q10 1Q11 2Q11 3Q11

‘000

Free

TI retail accesses

Defending Broadband Market Share at 53.6%

Stabilizing BB reduction trend vs Market contraction

BB ARPU increase proving an healthy BB Strategy

Confirming the stable BB Service Revenues since 2010

BB Market

TI

Flat (%)

€ Mln

‘000

% Premium Offers on Consumer Segment

Market Share

1Q11 2Q11 3Q11

87%

7,194

3.6%

54.1%

87%

7,169

4.3%

53.7%

87%

7,141

5.5%

53.6%

Stable

18.7 18.4 18.7 18.3 18.6 18.6 ARPU

€/month Stable

Growing

BB Service Revenues

TI Retail Broadband Accesses BB Net Adds

Highlights

Domestic Fixed: Focus on Broadband

16 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

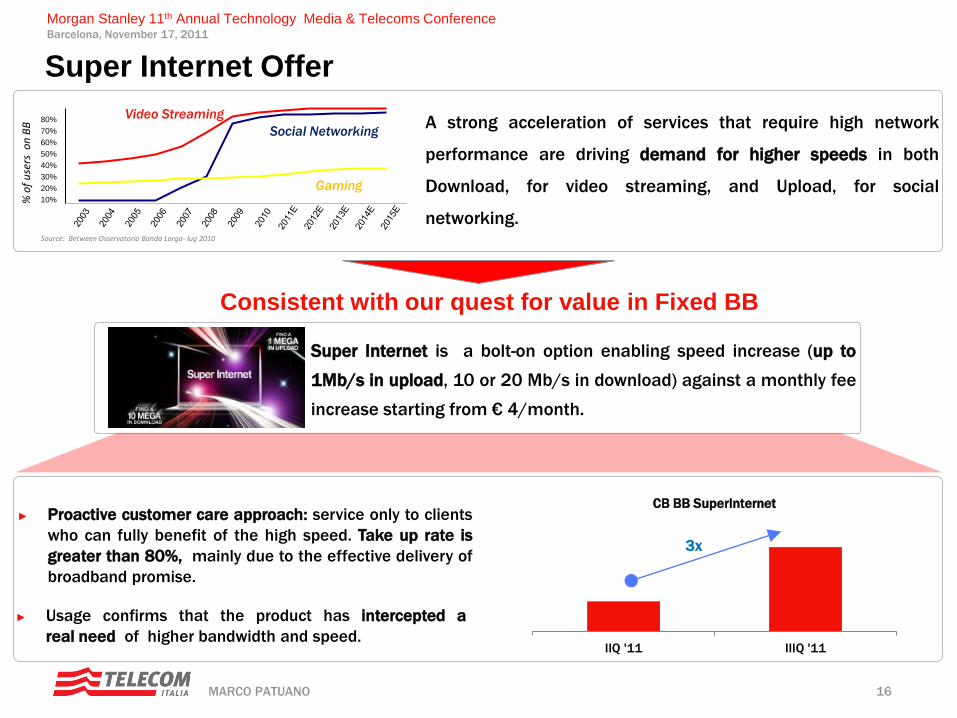

Super Internet Offer

Source: Between Osservatorio Banda Larga- lug 2010

% o

f u

sers

on

BB

10%

20%

30%

40%

50%

60%

80%

70% Social Networking

Video Streaming

Gaming

A strong acceleration of services that require high network

performance are driving demand for higher speeds in both

Download, for video streaming, and Upload, for social

networking.

► Proactive customer care approach: service only to clients

who can fully benefit of the high speed. Take up rate is

greater than 80%, mainly due to the effective delivery of

broadband promise.

Consistent with our quest for value in Fixed BB

► Super Internet is a bolt-on option enabling speed increase (up to

1Mb/s in upload, 10 or 20 Mb/s in download) against a monthly fee

increase starting from € 4/month.

► Usage confirms that the product has intercepted a

real need of higher bandwidth and speed. IIQ '11 IIIQ '11

CB BB SuperInternet

3x

17 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

Agenda

► TI Group 3Q11 Progress Report

► Focus on Domestic Mobile Market

► Focus on Domestic Fixed Market

► Conclusions

18 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

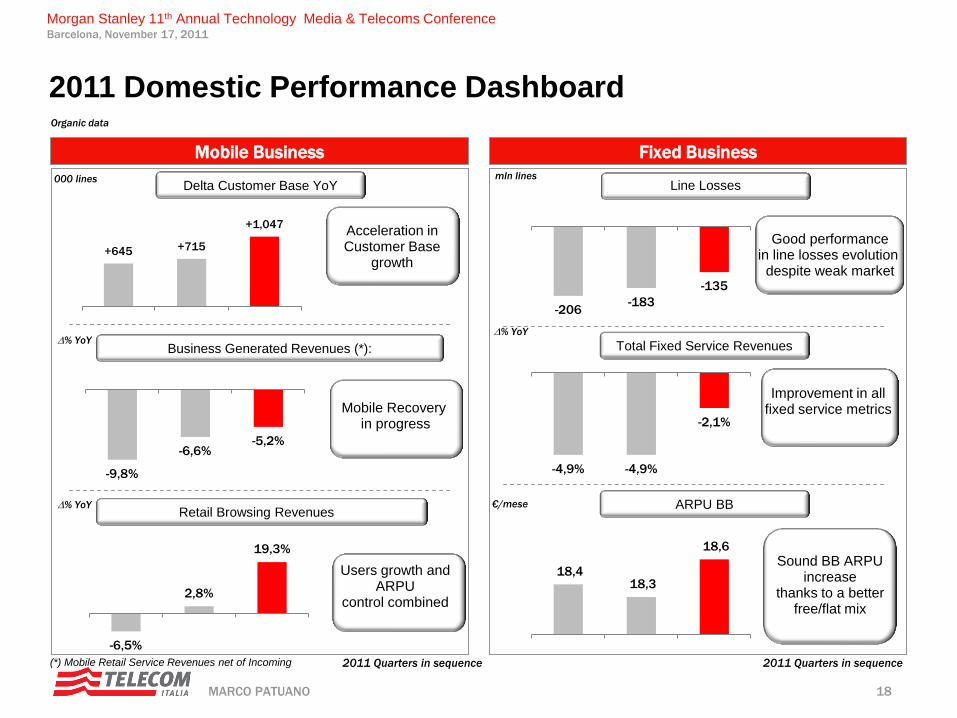

2011 Domestic Performance Dashboard Organic data

Mobile Business Fixed Business

Business Generated Revenues (*):

Delta Customer Base YoY

Retail Browsing Revenues

Total Fixed Service Revenues

Line Losses

Mobile Recovery in progress

Acceleration in Customer Base

growth

Users growth and ARPU

control combined

D% YoY

D% YoY

D% YoY

mln lines

ARPU BB

Sound BB ARPU increase

thanks to a better free/flat mix

2011 Quarters in sequence 2011 Quarters in sequence

Good performance in line losses evolution

despite weak market

Improvement in all fixed service metrics

-206 -183

-135

-4,9% -4,9%

-2,1%

18,4 18,3

18,6

+645 +715

+1,047

000 lines

(*) Mobile Retail Service Revenues net of Incoming

€/mese

-9,8%

-6,6% -5,2%

-6,5%

2,8%

19,3%

19 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

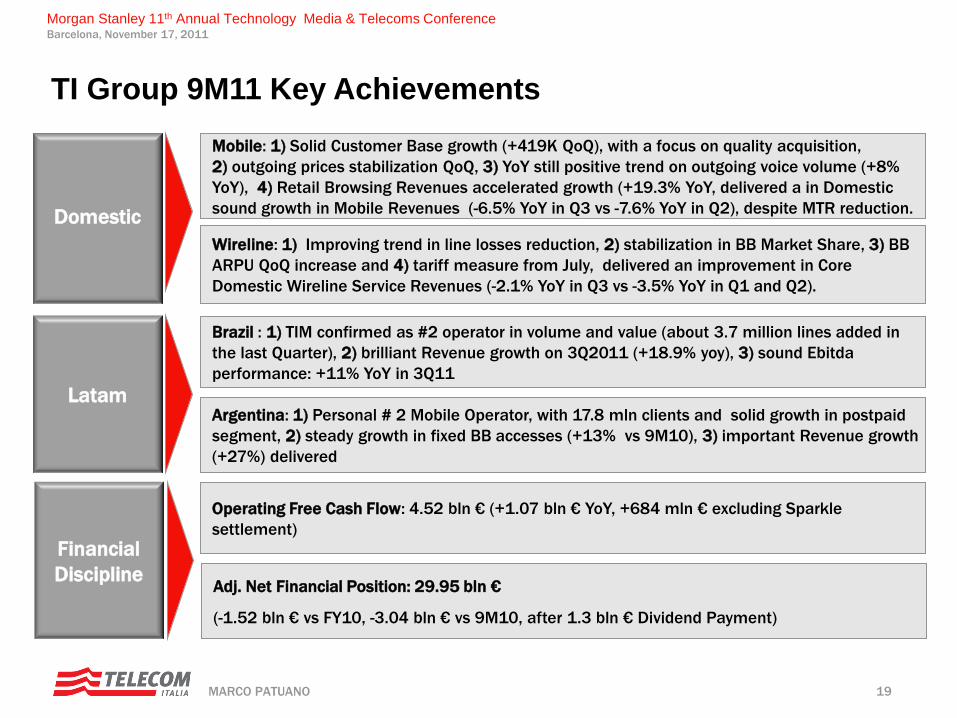

TI Group 9M11 Key Achievements

Financial

Discipline

Operating Free Cash Flow: 4.52 bln € (+1.07 bln € YoY, +684 mln € excluding Sparkle

settlement)

Adj. Net Financial Position: 29.95 bln €

(-1.52 bln € vs FY10, -3.04 bln € vs 9M10, after 1.3 bln € Dividend Payment)

Latam

Brazil : 1) TIM confirmed as #2 operator in volume and value (about 3.7 million lines added in

the last Quarter), 2) brilliant Revenue growth on 3Q2011 (+18.9% yoy), 3) sound Ebitda

performance: +11% YoY in 3Q11

Argentina: 1) Personal # 2 Mobile Operator, with 17.8 mln clients and solid growth in postpaid

segment, 2) steady growth in fixed BB accesses (+13% vs 9M10), 3) important Revenue growth

(+27%) delivered

Domestic

Mobile: 1) Solid Customer Base growth (+419K QoQ), with a focus on quality acquisition,

2) outgoing prices stabilization QoQ, 3) YoY still positive trend on outgoing voice volume (+8%

YoY), 4) Retail Browsing Revenues accelerated growth (+19.3% YoY, delivered a in Domestic

sound growth in Mobile Revenues (-6.5% YoY in Q3 vs -7.6% YoY in Q2), despite MTR reduction.

Wireline: 1) Improving trend in line losses reduction, 2) stabilization in BB Market Share, 3) BB

ARPU QoQ increase and 4) tariff measure from July, delivered an improvement in Core

Domestic Wireline Service Revenues (-2.1% YoY in Q3 vs -3.5% YoY in Q1 and Q2).

20 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

Back-up

21 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

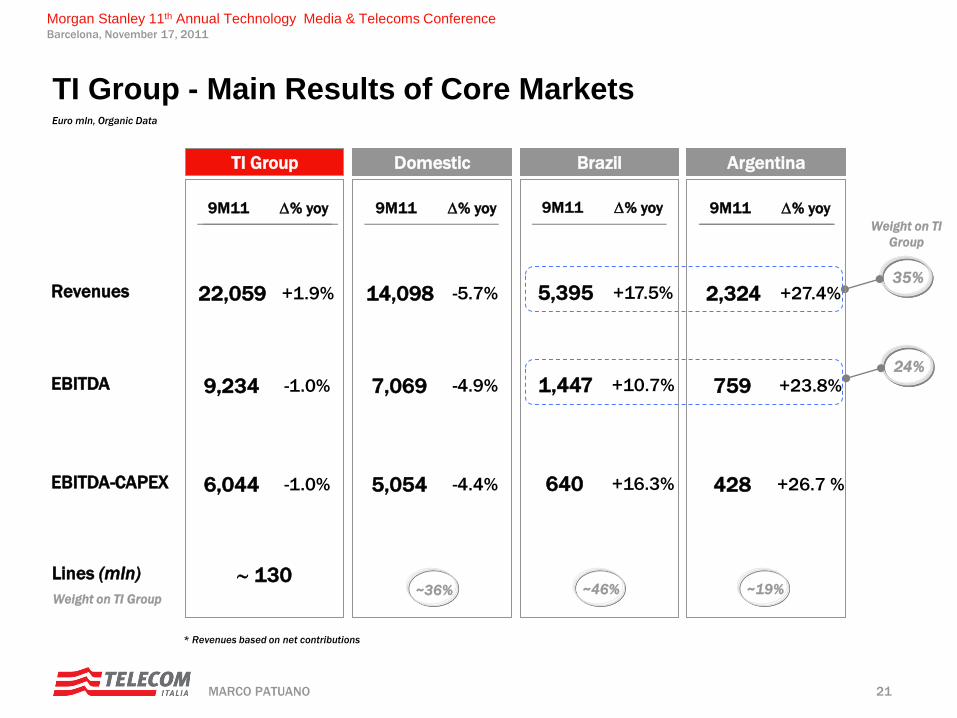

Revenues

EBITDA

EBITDA-CAPEX

* Revenues based on net contributions

35%

TI Group - Main Results of Core Markets Euro mln, Organic Data

Lines (mln)

Weight on TI Group

TI Group

9M11

22,059

9,234

6,044

D % yoy

+1.9%

-1.0%

-1.0%

130

9M11

5,395

1,447

640

D % yoy

+17.5%

+10.7%

+16.3%

Brazil

~46%

9M11

2,324

759

428

D % yoy

+27.4%

+23.8%

+26.7 %

Argentina

~19%

9M11

14,098

7,069

5,054

D % yoy

-5.7%

-4.9%

-4.4%

Domestic

~36%

Weight on TI

Group

24%

22 MARCO PATUANO

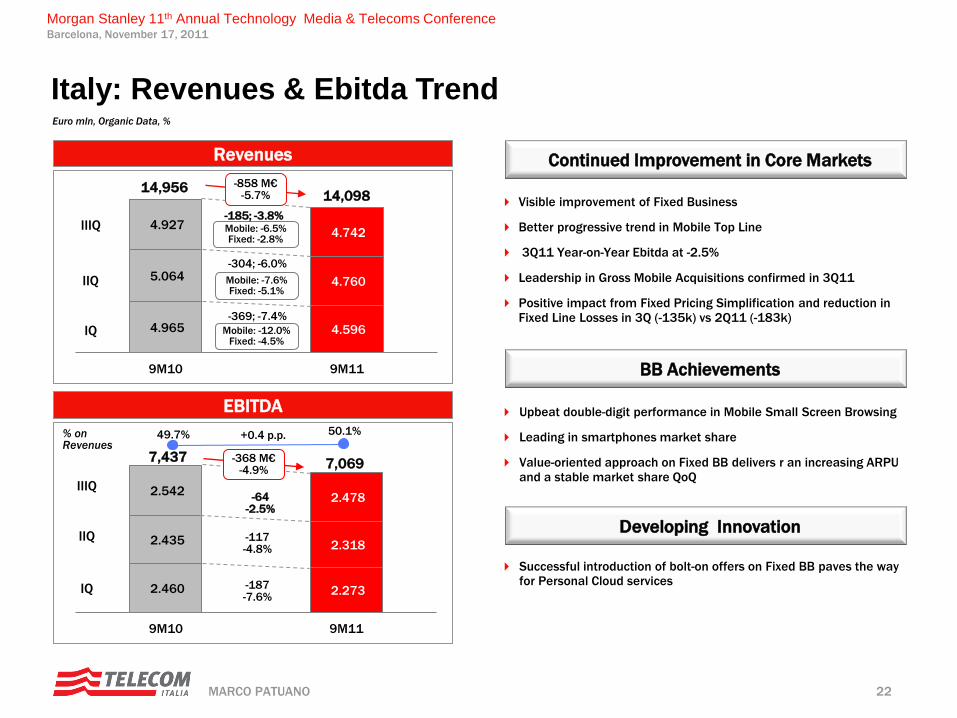

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

4.965 4.596

5.064 4.760

4.927 4.742

9M10 9M11

Mobile: -6.5% Fixed: -2.8%

-185; -3.8%

2.460 2.273

2.435 2.318

2.542 2.478

9M10 9M11

-64 -2.5%

7,437

Euro mln, Organic Data, %

-368 M€ -4.9%

-369; -7.4%

-304; -6.0%

49.7% 50.1% +0.4 p.p.

7,069

Upbeat double-digit performance in Mobile Small Screen Browsing

Leading in smartphones market share

Value-oriented approach on Fixed BB delivers r an increasing ARPU and a stable market share QoQ

Visible improvement of Fixed Business

Better progressive trend in Mobile Top Line

3Q11 Year-on-Year Ebitda at -2.5%

Leadership in Gross Mobile Acquisitions confirmed in 3Q11

Positive impact from Fixed Pricing Simplification and reduction in Fixed Line Losses in 3Q (-135k) vs 2Q11 (-183k)

-117 -4.8%

-187 -7.6%

Mobile: -7.6% Fixed: -5.1%

Mobile: -12.0% Fixed: -4.5%

Revenues

EBITDA

Developing Innovation

BB Achievements

Continued Improvement in Core Markets

Successful introduction of bolt-on offers on Fixed BB paves the way for Personal Cloud services

Italy: Revenues & Ebitda Trend

% on Revenues

IIQ

IQ

IIIQ

-858 M€ -5.7%

14,956 14,098

IIQ

IQ

IIIQ

23 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

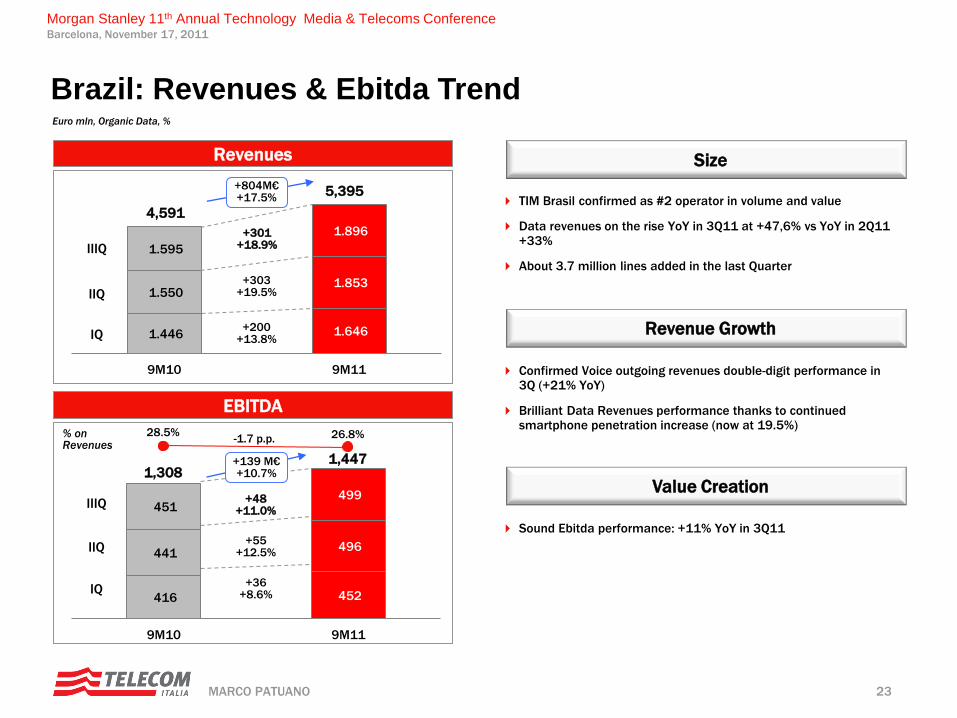

416 452

441 496

451 499

9M10 9M11

1.446 1.646

1.550 1.853

1.595

1.896

9M10 9M11

+301 +18.9%

Euro mln, Organic Data, %

Revenues

EBITDA

Brazil: Revenues & Ebitda Trend

+804M€ +17.5%

+303 +19.5%

+200 +13.8%

4,591

5,395

IIQ

IQ

IIIQ

+55 +12.5%

+36 +8.6%

1,308 1,447

-1.7 p.p. 26.8%

+48 +11.0%

+139 M€ +10.7%

28.5%

IIQ

IQ

IIIQ

% on Revenues

Value Creation

Revenue Growth

Size

TIM Brasil confirmed as #2 operator in volume and value

Data revenues on the rise YoY in 3Q11 at +47,6% vs YoY in 2Q11 +33%

About 3.7 million lines added in the last Quarter

Sound Ebitda performance: +11% YoY in 3Q11

Confirmed Voice outgoing revenues double-digit performance in 3Q (+21% YoY)

Brilliant Data Revenues performance thanks to continued smartphone penetration increase (now at 19.5%)

24 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

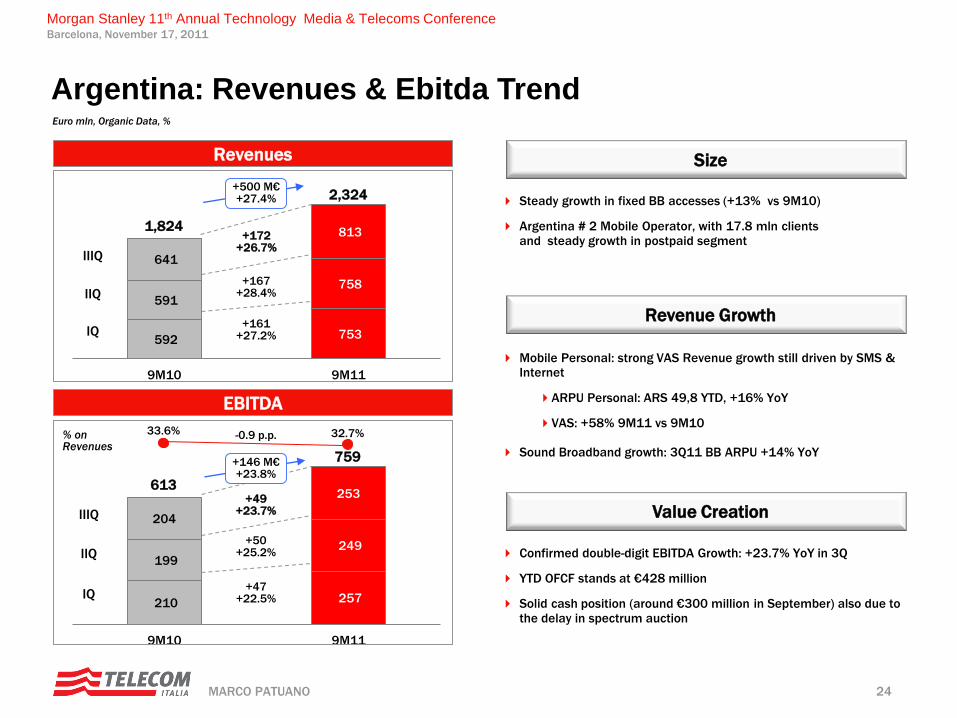

210 257

199

249

204

253

9M10 9M11

+49 +23.7%

592 753

591

758

641

813

9M10 9M11

+172 +26.7%

Euro mln, Organic Data, %

Revenues

EBITDA

Argentina: Revenues & Ebitda Trend

% on Revenues

Value Creation

Revenue Growth

Size

Mobile Personal: strong VAS Revenue growth still driven by SMS & Internet

ARPU Personal: ARS 49,8 YTD, +16% YoY

VAS: +58% 9M11 vs 9M10

Sound Broadband growth: 3Q11 BB ARPU +14% YoY

Confirmed double-digit EBITDA Growth: +23.7% YoY in 3Q

YTD OFCF stands at €428 million

Solid cash position (around €300 million in September) also due to the delay in spectrum auction

Steady growth in fixed BB accesses (+13% vs 9M10)

Argentina # 2 Mobile Operator, with 17.8 mln clients and steady growth in postpaid segment

+500 M€ +27.4%

+146 M€ +23.8%

+50 +25.2%

+47 +22.5%

613

759

33.6% -0.9 p.p. 32.7%

+167 +28.4%

+161 +27.2%

1,824

2,324

IIQ

IQ

IIIQ

IIQ

IQ

IIIQ

25 MARCO PATUANO

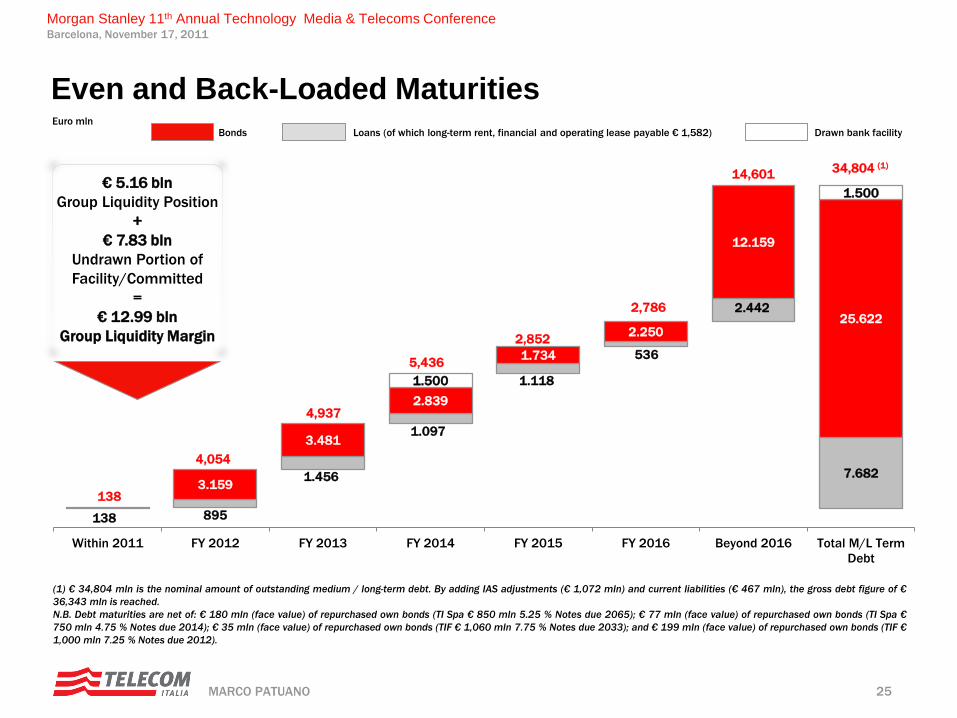

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

138 895

1.456

1.097

1.118

536

2.442

7.682 3.159

3.481

2.839

1.734

2.250

12.159

25.622

1.500

1.500

Within 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 Beyond 2016 Total M/L Term

Debt

4,054

4,937

5,436

2,852

2,786

14,601 34,804 (1)

Bonds Loans (of which long-term rent, financial and operating lease payable € 1,582) Drawn bank facility

Even and Back-Loaded Maturities Euro mln

€ 5.16 bln

Group Liquidity Position

+

€ 7.83 bln

Undrawn Portion of

Facility/Committed

=

€ 12.99 bln

Group Liquidity Margin

138

(1) € 34,804 mln is the nominal amount of outstanding medium / long-term debt. By adding IAS adjustments (€ 1,072 mln) and current liabilities (€ 467 mln), the gross debt figure of €

36,343 mln is reached.

N.B. Debt maturities are net of: € 180 mln (face value) of repurchased own bonds (TI Spa € 850 mln 5.25 % Notes due 2065); € 77 mln (face value) of repurchased own bonds (TI Spa €

750 mln 4.75 % Notes due 2014); € 35 mln (face value) of repurchased own bonds (TIF € 1,060 mln 7.75 % Notes due 2033); and € 199 mln (face value) of repurchased own bonds (TIF €

1,000 mln 7.25 % Notes due 2012).

26 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

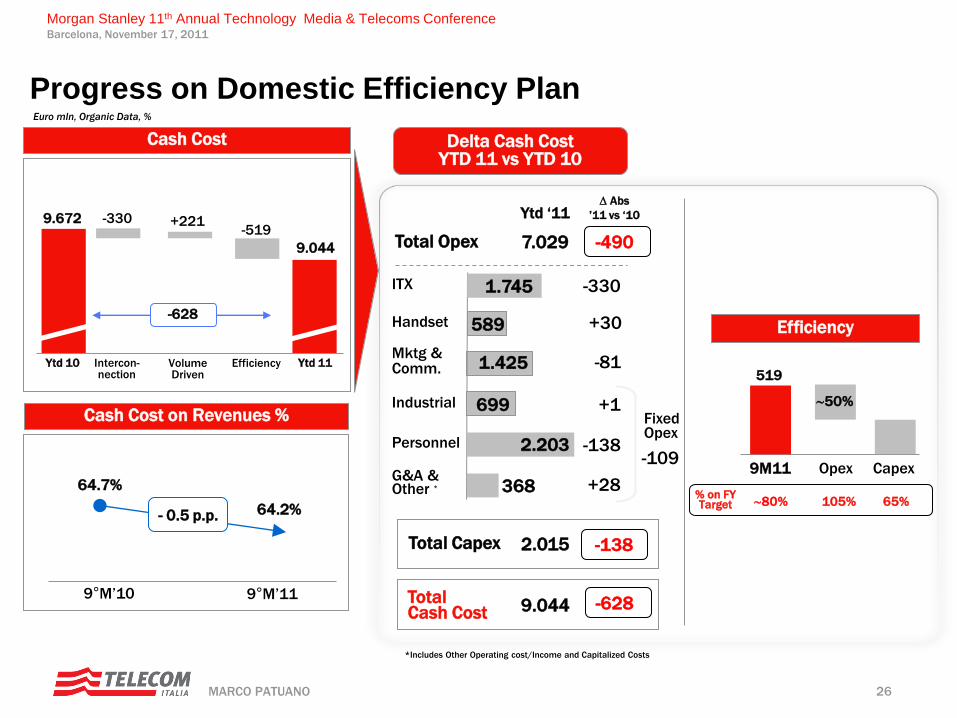

Progress on Domestic Efficiency Plan Euro mln, Organic Data, %

D Abs

’11 vs ‘10 Ytd ‘11

-330

2.015 Total Capex

1.425

699

-81

2.203

+1

-138

+28

7.029 Total Opex -490

1.745

Delta Cash Cost YTD 11 vs YTD 10

Industrial

Personnel

Mktg & Comm.

ITX

G&A & Other * 368

Cash Cost

Efficiency Volume Driven

-330 9.672

-628

-519

Intercon- nection

Ytd 10 Ytd 11

9.044

+221

Cash Cost on Revenues %

9°M’10 9°M’11 9.044

64.7%

64.2% - 0.5 p.p.

*Includes Other Operating cost/Income and Capitalized Costs

-628 Total Cash Cost

589 +30 Handset Efficiency

Fixed Opex

-109 9M11

519

Opex

50%

Capex

% on FY Target 80% 105% 65%

-138

27 MARCO PATUANO

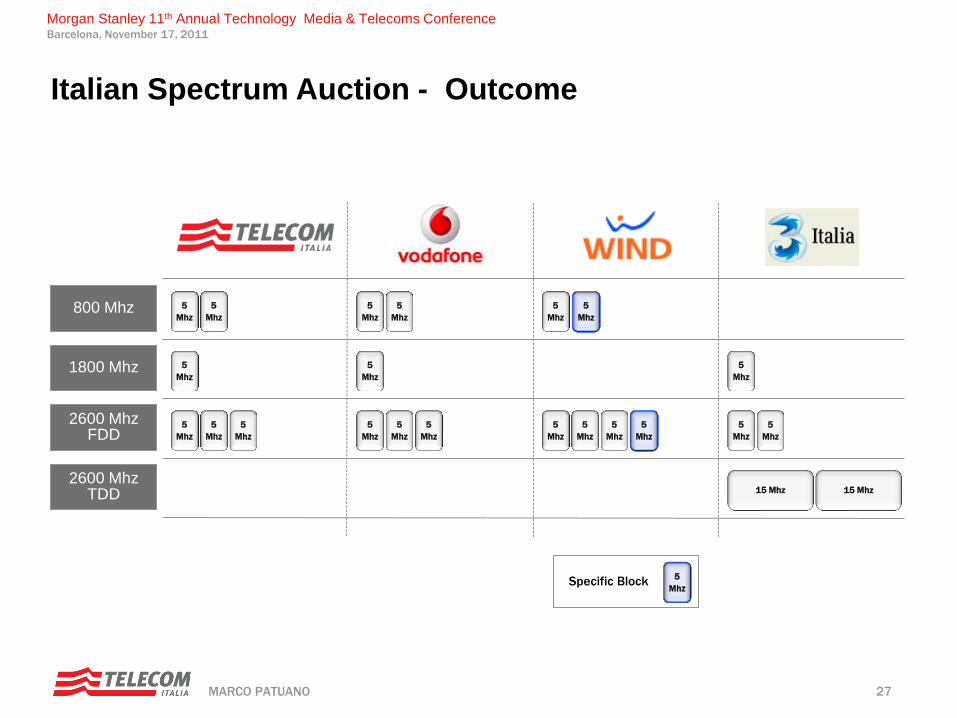

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

5

Mhz

Italian Spectrum Auction - Outcome

800 Mhz 5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

1800 Mhz 5

Mhz

5

Mhz

5

Mhz

2600 Mhz FDD

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

5

Mhz

2600 Mhz TDD 15 Mhz 15 Mhz

Specific Block 5

Mhz

28 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

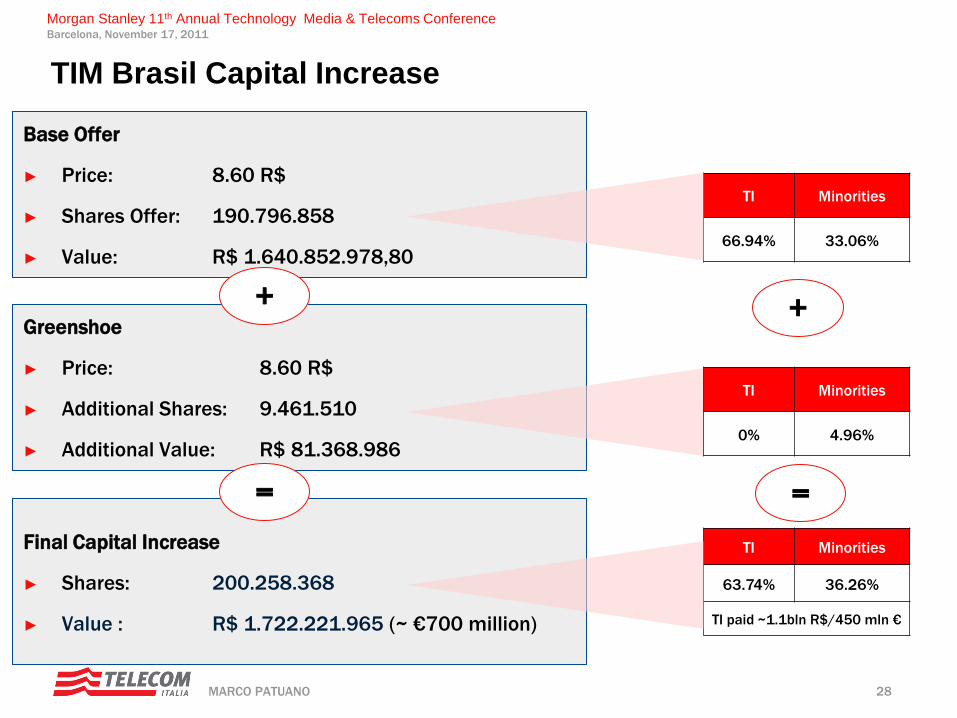

TIM Brasil Capital Increase

Base Offer

► Price: 8.60 R$

► Shares Offer: 190.796.858

► Value: R$ 1.640.852.978,80

Greenshoe

► Price: 8.60 R$

► Additional Shares: 9.461.510

► Additional Value: R$ 81.368.986

Final Capital Increase

► Shares: 200.258.368

► Value : R$ 1.722.221.965 (~ €700 million)

+

=

TI Minorities

66.94% 33.06%

+

=

TI Minorities

63.74% 36.26%

TI paid ~1.1bln R$/450 mln €

TI Minorities

0% 4.96%

29 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

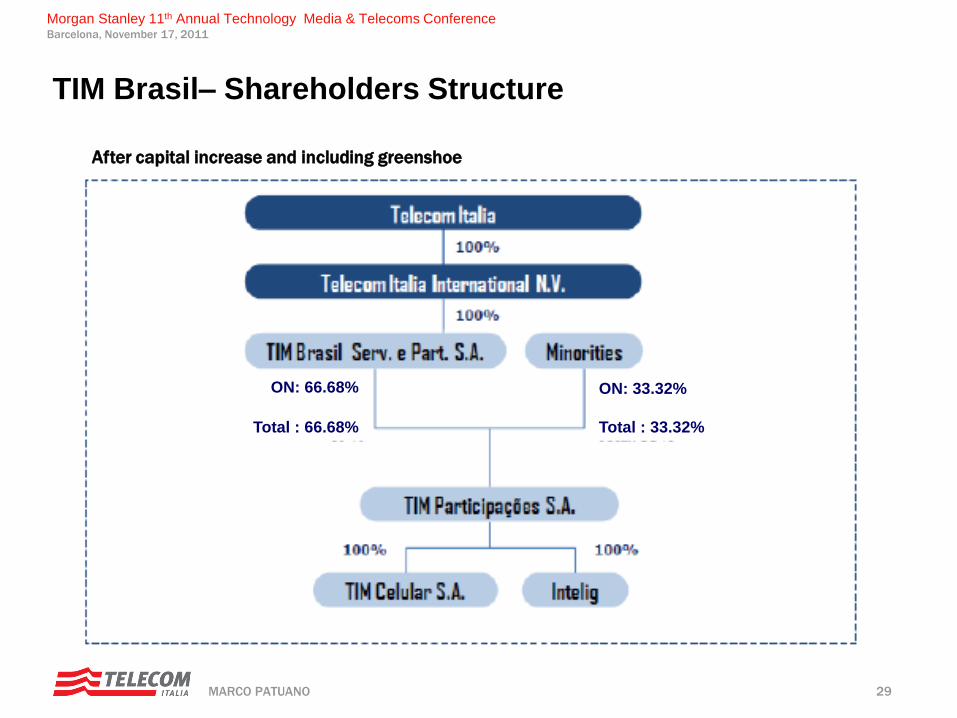

TIM Brasil– Shareholders Structure

After capital increase and including greenshoe

ON: 66.68%

Total : 66.68%

ON: 33.32%

Total : 33.32%

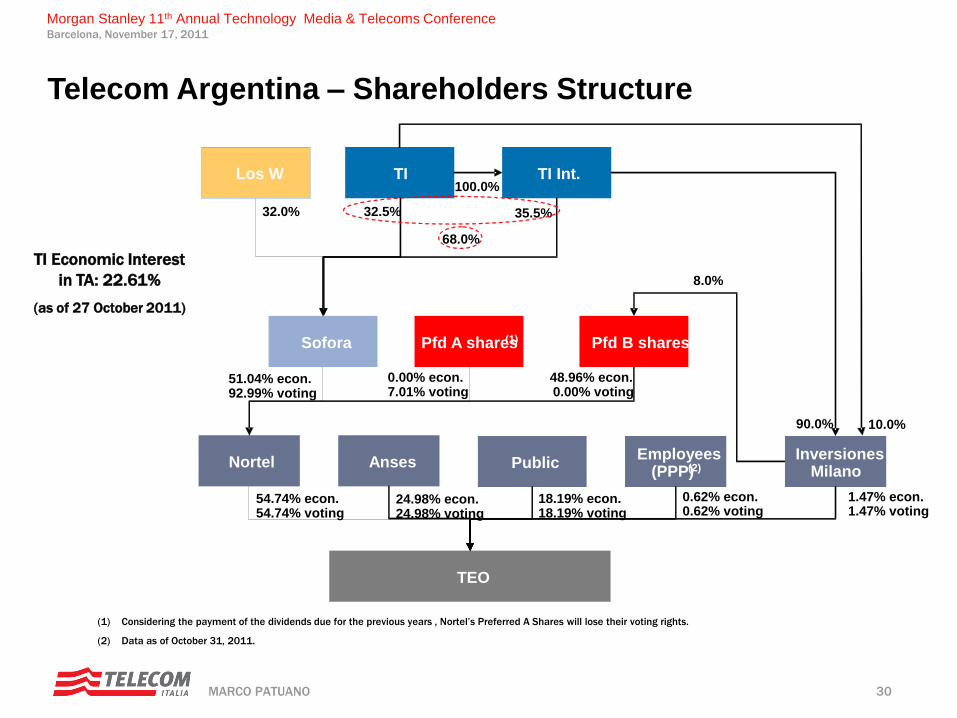

30 MARCO PATUANO

Morgan Stanley 11th Annual Technology Media & Telecoms Conference Barcelona, November 17, 2011

(1) Considering the payment of the dividends due for the previous years , Nortel’s Preferred A Shares will lose their voting rights.

(2) Data as of October 31, 2011.

54.74% econ. 54.74% voting

Los W

Nortel

Sofora

TI

Pfd A shares (1) Pfd B shares

Public

32.0% 32.5%

51.04% econ. 92.99% voting

0.00% econ. 7.01% voting

48.96% econ. 0.00% voting

TEO

Employees (PPP) (2)

18.19% econ. 18.19% voting

0.62% econ. 0.62% voting

8.0%

TI Int. 100.0%

35.5%

68.0%

Anses

24.98% econ. 24.98% voting

Inversiones Milano

1.47% econ. 1.47% voting

90.0% 10.0%

TI Economic Interest

in TA: 22.61%

(as of 27 October 2011)

Telecom Argentina – Shareholders Structure