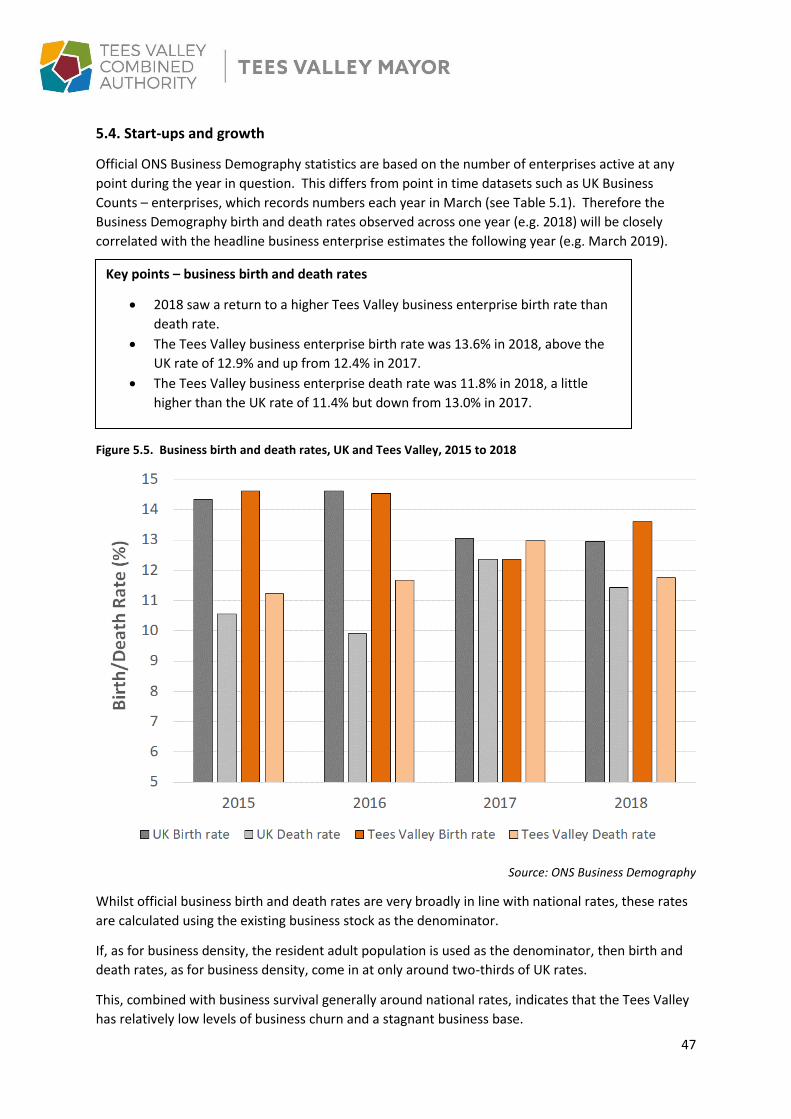

tees valley economic assessment 2019

TRANSCRIPT

1

2

CONTENTS

Section 1: Introduction 3

Section 2: Executive Summary 4

Section 3: Area Profile 10

Section 4: Economic Growth and Productivity 24

Section 5: Business Growth 41

Section 6: Research & Development, Innovation and Energy 52

Section 7: Education, Employment and Skills 61

Section 8: Transport & Digital Infrastructure 103

Section 9: Place and Culture 114

Section 10: Performance Gaps and Baselines 135

Bibliography 139

3

Section 1: Introduction

The Tees Valley Economic Assessment is the core statistical document related to economic development in Tees Valley. It is based upon data and analysis for key areas that contribute towards growth in our economy including: o Economy and Productivity (economic conditions, innovation activity, the business base and

key sectors);

o Skills and Labour Market (attainment, employment and future demand); and

o Growth Enablers (connectivity, education, place and culture).

The Economic Assessment is updated annually. It reflects the priorities in the Tees Valley Strategic Economic Plan and the draft Local Industrial Strategy for Tees Valley (agreed by Cabinet in July 2019). The Economic Assessment provides an evidence base that underpins the Tees Valley Investment Plan, supporting the development of business cases, as well as helping to inform local authority assessments, Local Plans and other policy and strategy documents. In 2020, it is also intended that updated analysis will underpin the joint agreement with Government of a Local Industrial Strategy for Tees Valley. Data is presented for Tees Valley wherever possible and where appropriate includes analysis at Local Authority level. When available, performance is benchmarked against the North of England and nationally.

4

Section 2: Executive Summary

2.1 . Economic Overview

Headline metrics for Tees Valley:

• Total population in 2018 = 674,300

• Working age (16-64) population in 2018 = 414,400

• Economically active population aged 16-64 in 12 months to June 2019 = 302,900

• Economically inactive population aged 16-64 in 12 months to June 2019 = 106,700

• Employment (employed residents aged 16-64) in 12 months to June 2019 = 281,100

• Jobs (people employed within Tees Valley) in 12 months to June 2019 = 283,300

• Number of businesses in 2019 = 17,765. 87.8% of Tees Valley firms are micro-businesses

(under 10 employees) and 0.5% of firms are large companies (250+ employees)

• Economic output / Gross Domestic Product (GDP) in 2018 = £16.2bn

• Productivity in 2018 = £31.8 per hour

• In 2018, 125,700 or 30.6% of residents aged 16-64 were qualified to NVQ Level 4 (degree

level) or above

Tees Valley covers over 300 square miles. It is located on the North East coast, and comprises the

five Local Authority areas of Darlington, Hartlepool, Middlesbrough, Redcar & Cleveland and

Stockton-on-Tees. It is highly urbanised, with 98% of the population living in built-up areas of which

90% can be classed as ‘urban’.

The Tees Valley economy has well established strengths in Chemical & Process, Energy and

Advanced Manufacturing. There are also emerging strengths in Digital, Business & Professional

Services and the Logistics sector, which are playing an increasing role in the region’s economy.

These priority sectors are supported by several key assets in the region, including:

• Cost effective sites and premises, with significant opportunities for development at the

4,500 acre South Tees Development site, and further potential at the region’s seven

Enterprise Zones.

• Teesside University – an internationally recognised university in terms of working with

business. The University was the winner of the Improving the Business Environment

category in the 2018 Enterprising Britain Awards.

• National centres of excellence including the Centre for Process Innovation (CPI) and National

Horizons Centre (specialising in training for UK bioscience), the Materials Processing Institute

(MPI) and TWI.

• A major East Coast rail hub at Darlington providing fast north-south connections across the

country.

• An International Airport and The Port of Tees and Hartlepool - the largest port in England in

terms of outwards traffic tonnage, providing a critical gateway to world markets for the Tees

Valley industrial platform.

The Tees Valley labour market and wider economy suffered a difficult 2016 following the closure of

the SSI steelworks in 2015, resulting in around 4,000 job losses at SSI and across associated suppliers

and contractors. Whilst the local economy stabilised in 2017, 2018 was another difficult year with

Brexit uncertainty impacting negatively on business investment. Tees Valley Gross Domestic Product

(GDP) was 3.5% lower in 2018 than it was in 2015. The area’s relative economic performance

5

remains well below national levels and rates and the region experiences some persistent economic

challenges.

Key economic messages for the Tees Valley include:

• Labour demand issues, including the relative lack of Tees Valley jobs. Additionally, Tees

Valley has consistently recorded some of the highest economic inactivity and unemployment

rates in the country. However, economic output per job is close to national averages and

above the North of England average, demonstrating that there are well paid and productive

jobs in the region with the opportunity for further growth.

• Tees Valley has significant sectoral strength and relatively high employment in higher

productivity sectors such as Chemical & Process, Clean Energy, Low Carbon & Hydrogen and

Advanced Manufacturing. Construction sub-sectors including civil engineering and

specialised construction are also well represented.

• The area has a relatively aged population profile and, as with many other areas, an ageing

population. There has been slow population growth over recent years, below national

increases, along with significant out migration of working age people. Future projections

suggest that labour supply constraints will increase, which could result in the potential for

there to be a lack of local workers in the future. However, there remains significant scope

for mitigating the majority of this potential constraint by addressing the area’s particularly

high rates of economic inactivity and unemployment.

• A key constraint on the Tees Valley economy is the relatively small size of its private sector,

reflected by its low business density at less than two-thirds the size of the UK average. If the

Tees Valley public sector broadly mirrors national public sector trends the Tees Valley

private sector growth must significantly out-perform UK private sector growth just to keep

up with aggregate UK GDP or GVA growth rates. However, with local private sector business

growth metrics typically running at or a little below national rates, the Tees Valley economy

was 3.5% smaller in 2018 than in 2015.

• The Tees Valley is home to the single biggest development opportunity in the UK in the form

of the South Tees Development Corporation. This significant opportunity means that Tees

Valley’s private sector business and economic growth potential is amongst the greatest in

the country.

6

2.2 . Key metrics

The following bullet points highlight some of the key metrics underpinning the above key messages.

Chart 10.1 in Section 10 shows how a number of these metrics translate in terms of gap to reach

national performance rates.

• Economic output across Tees Valley, measured in terms of Gross Domestic Product or GDP, stood at £16.2bn in 2018. Tees Valley GDP per capita was £24,085 or 75.3% of the UK rate. However, the Tees Valley’s high levels of economic inactivity provide significant scope for increasing GDP per capita greatly. Any paid work undertaken by those residents previously economically inactive will increase GDP per capita.

• Productivity – GVA per hour worked – was £31.8 in 2018, third highest of all North of England LEPs and at 90.9% of the UK rate, far closer to the national average than the GVA per capita measure (71.5% of UK rate). The GVA per hour worked indicator is the best measure of an economy’s underlying productivity and removes employment rate, economic inactivity, demographic, and commuting considerations that are present within GVA per capita. This again highlights that whilst Tees Valley has relatively low numbers of jobs, the jobs it does have are amongst the most productive anywhere in the North of England.

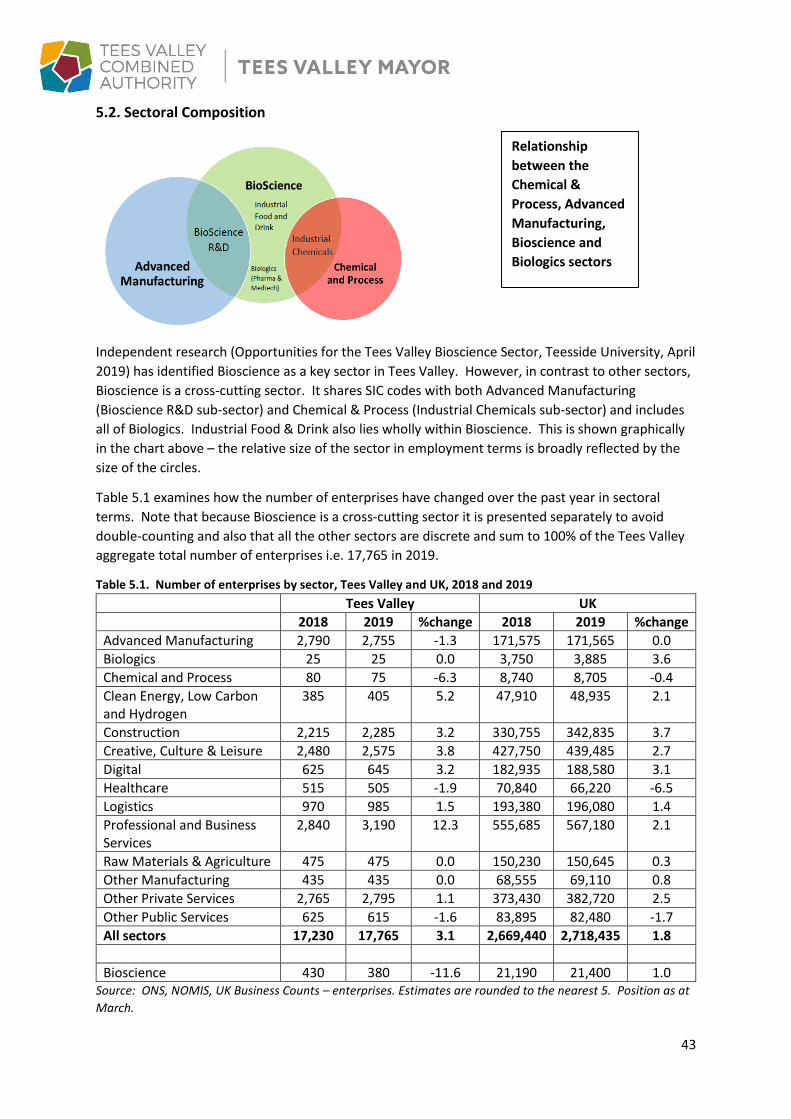

• Enterprise – the number of business enterprises located in Tees Valley – stood at 17,765 in 2019. This total represents 64.8% of the UK rate for enterprises per resident adults aged 16+. The number of business enterprises increased by 1,265 between 2015 and 2019. However, this rate of growth was a little slower than for the UK resulting in Tees Valley business density falling from 65.5% of the national rate in 2015. Business density remains a key challenge for Tees Valley going forwards. However, with historical sectoral strength in those sectors where fewer but larger firms tended to predominate e.g. traditional heavy industry, the ongoing diversification of the economy can only help to close the present enterprise gap.

• Throughout the past three years, the Tees Valley employment rate has been broadly matching its pre-recession highs observed during the mid-2000s. However, with 281,100 Tees Valley residents aged 16 to 64 in employment in the year to June 2019, the Tees Valley employment rate of 68.6% remains significantly below the UK rate of 75.5%. This difference in employment rates translates to an employment gap of 27,900.

• Local demand for highly skilled workers remains robust and there is currently high job demand for teachers, carers, nurses, engineers, IT professionals, and teaching/nursery assistants. In 2019, there were close on 2,500 job vacancies in each of the broad professional occupation groups of Teaching & Education Professionals; Science, Research, Engineering & Technology Professionals and Health Professionals. Similarly, Caring Personal Service occupations recorded around 2,500 vacancies across Tees Valley.

• The skills levels of residents can present a challenge in meeting labour demands, Tees Valley residents are less well qualified than many other parts of the country. In terms of Degree/Level 4+ qualifications in 2018, the area needs an additional 34,800 residents qualified to that level to match the UK rate.

• Tees Valley primary schools perform above the national average with high quality schools and above average key stage 2 results. However, the quality and performance of Tees Valley secondary schools is below national average. Tees Valley has good quality Post 16 skills provision with all Further Education colleges now rated as either ‘Good’ or ‘Outstanding’ by Ofsted.

7

• Commercialisation, in terms of the proportion of firms introducing either a new or

significantly improved product or service between 2014 and 2016, stood at 21% in Tees

Valley compared to the Local Enterprise Partnerships’ (LEP) average of 25%. However,

amongst those Tees Valley firms that do innovate, higher than average proportions of sales

were derived from innovative products or services (42% of Tees Valley firms v 37% LEP

average) – an indicator of short-term success of firms’ innovation. This implies that

interventions to encourage Tees Valley firms to innovate are likely to generate greater

returns than in some other parts of the country.

• Tees Valley remains a strong exporting region. However, recent sharp growth in imports (up

15.8% on 2017) means that it no longer runs a trade in goods surplus i.e. imports into Tees

Valley are now greater than exports out. In 2018, Tees Valley goods exports totalled

£3,278m with imports at £3,423m, a deficit of £145m. No English region now runs a trade in

goods surplus (Scotland and N. Ireland still do) but the North East remains the region with

the lowest deficit (£830m in 2018). However, reflecting the Tees Valley’s increasing reliance

on imports, the North East region recorded the largest percentage increase in imports of any

region/country of the UK (NE 6.2% up, UK 2.9% up).

• Tees Valley runs a trade in goods surplus with the EU but a deficit with the rest of the world.

In 2018, export trade with EU countries was £1,863m (up 4.8% on 2017) whilst that with

non-EU countries totalled £1,415m (up 2.2%). EU goods imports were £1,675m (up 9.6% on

2017) and those from non-EU countries totalled £1,748m (up 22.4%). The UK has trade

agreements (until the end of 2020) with many of these non-EU countries through its

membership of the EU. The recent strong growth in exports to these non-EU countries

highlights the opportunity for further export growth provided the present country by

country agreements can be replicated or improved upon with UK bilateral deals by the end

of 2020.

• Congestion is less of a problem in Tees Valley than in many other areas. Tees Valley average

‘A’ road speeds (30.0 mph) are significantly quicker than other metropolitan areas in the

North of England e.g. Manchester at 18.3 mph and are also well above the national average

(24.9 mph).

• The relatively low cost of living in the Tees Valley helps boost the quality of life. With

average wage rates (Tees Valley £25,300 p.a., England £30,400 p.a.) far closer to the national

average than house prices (TV £155,700, England £304,000), Tees Valley has some of the

most affordable homes in the country (TV ratio of house price to salary 6.2, England 10.0).

Average housing rental costs also account for a significantly smaller share of wages than

nationally e.g. % of take home pay on two bedroom home in TV 30%, England 47%.

• Tees Valley has a relatively high proportion of localities within the most deprived 10%

nationally, as ranked by the 2019 Index of Multiple Deprivation, ranking as the second most

deprived LEP in England (out of 38 LEP areas). Whilst this ranking is unchanged since 2015,

there has been a slight increase in relative deprivation across Tees Valley over this time.

• Digital connectivity in Tees Valley is well above the national average, especially for Ultrafast

broadband with an average availability of 90% of all residential and business premises

covered compared to 59% nationally.

8

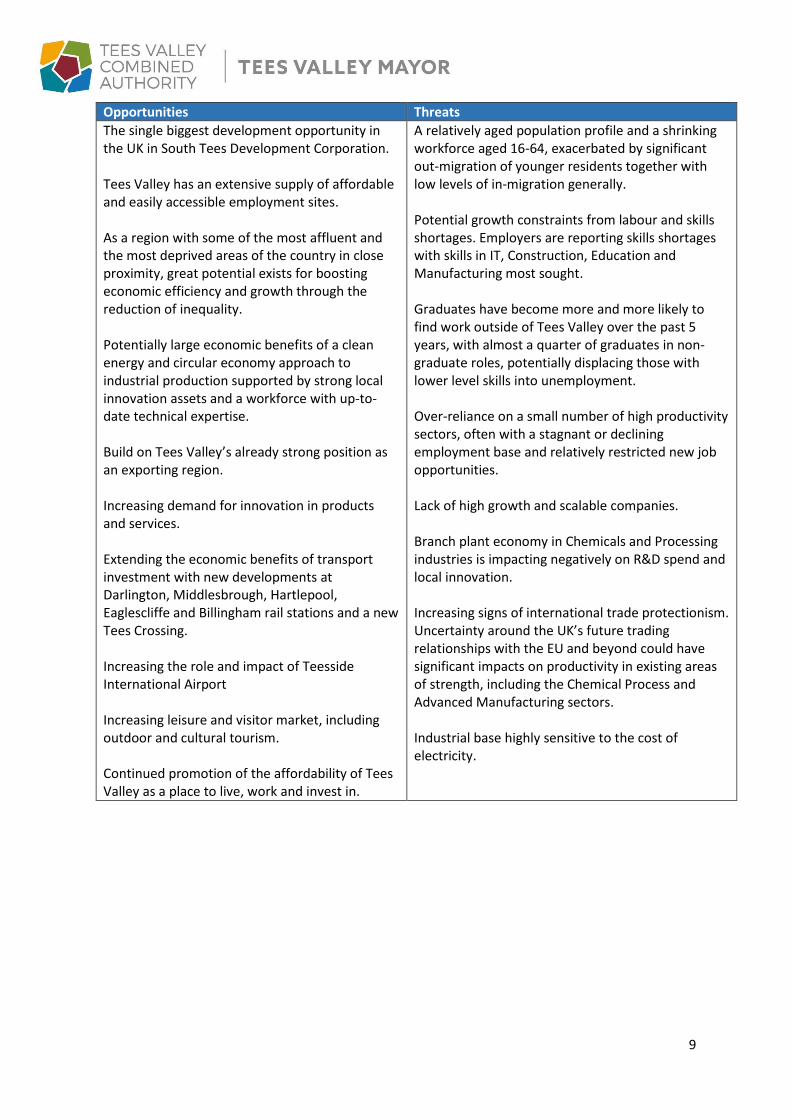

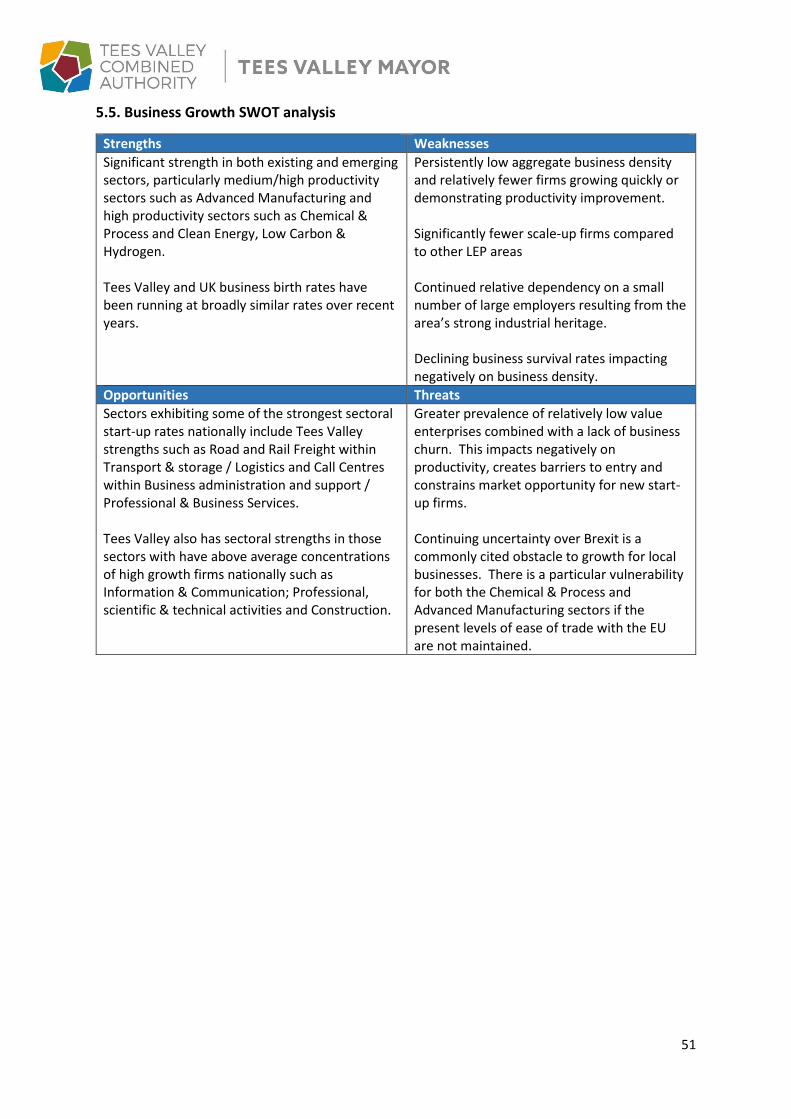

2.3. Tees Valley SWOT assessment

Strengths Weaknesses

Underlying aggregate productivity one of the highest of the northern LEPs and well represented in relatively high productivity sectors such as Energy & Circular Economy, Chemical & Process and Advanced Manufacturing. Strong recent GVA trend growth in sectors such Civil Engineering, Food Manufacturing and Wholesale. Tees Valley is a strong exporting region and is supported by England’s largest port in terms of outwards traffic tonnage with strong links to northern Europe and considerable potential for expansion around the world. Above average Tees Valley performance across primary school level and above average participation in Higher Education. Higher percentage of 16-34 year old residents starting an apprenticeship than nationally and apprenticeship achievement rates are consistently higher than the national average. Staff costs and other business overheads such as office rental costs are amongst the most price competitive in the country. Major East Coast rail hub at Darlington providing fast north-south connections across Great Britain. Relatively low levels of traffic congestion. Attractive and affordable towns, countryside and coast. Low cost of living generally.

A stagnant economy with an increasing output gap. Some of the country’s highest economic inactivity rates – closely correlated with relatively low levels of health and well-being – and stubbornly high unemployment rates when compared to other areas. Youth unemployment is an issue with a higher than average number of young people unemployed and claiming benefits and a high number NEET (Not in Education, Employment or Training). Lowest business density rates in England and low levels of innovation activity / spend among businesses. Lack of business churn with enterprise start-up rates constrained by lack of demand. Lack of jobs and the second lowest jobs density of all combined authority areas in England. The quality and performance of Secondary schools is below average. School performance at a local level varies between Local Authorities with pockets of under-achievement in both primary and secondary. The number of residents with higher level skills is below average and Tees Valley has a higher than average number of residents with no qualifications. Economic growth constrained by recent employment growth being skewed towards low pay, low skill occupations. Negative external perceptions of Teesside and lack of awareness re Tees Valley. Variable housing stock and relatively low house prices.

9

Opportunities Threats

The single biggest development opportunity in the UK in South Tees Development Corporation. Tees Valley has an extensive supply of affordable and easily accessible employment sites. As a region with some of the most affluent and the most deprived areas of the country in close proximity, great potential exists for boosting economic efficiency and growth through the reduction of inequality. Potentially large economic benefits of a clean energy and circular economy approach to industrial production supported by strong local innovation assets and a workforce with up-to-date technical expertise. Build on Tees Valley’s already strong position as an exporting region. Increasing demand for innovation in products and services. Extending the economic benefits of transport investment with new developments at Darlington, Middlesbrough, Hartlepool, Eaglescliffe and Billingham rail stations and a new Tees Crossing. Increasing the role and impact of Teesside International Airport Increasing leisure and visitor market, including outdoor and cultural tourism. Continued promotion of the affordability of Tees Valley as a place to live, work and invest in.

A relatively aged population profile and a shrinking workforce aged 16-64, exacerbated by significant out-migration of younger residents together with low levels of in-migration generally. Potential growth constraints from labour and skills shortages. Employers are reporting skills shortages with skills in IT, Construction, Education and Manufacturing most sought. Graduates have become more and more likely to find work outside of Tees Valley over the past 5 years, with almost a quarter of graduates in non-graduate roles, potentially displacing those with lower level skills into unemployment. Over-reliance on a small number of high productivity sectors, often with a stagnant or declining employment base and relatively restricted new job opportunities. Lack of high growth and scalable companies. Branch plant economy in Chemicals and Processing industries is impacting negatively on R&D spend and local innovation. Increasing signs of international trade protectionism. Uncertainty around the UK’s future trading relationships with the EU and beyond could have significant impacts on productivity in existing areas of strength, including the Chemical Process and Advanced Manufacturing sectors. Industrial base highly sensitive to the cost of electricity.

10

Section 3: Area Profile

The Tees Valley connects five local authority areas, with the river Tees running through all, and

forms a functioning economic geography. It has a con-terminus, fully integrated Combined

Authority and Local Enterprise Partnership in the area, responsible for overseeing economic growth.

The unique assets and strengths across the five Tees Valley local authorities combine to create the

opportunity to build a diverse and inclusive economy for Tees Valley residents and businesses, with

specialisms in Chemical & Process, Advanced Manufacturing, Clean Energy, Low Carbon and

Hydrogen. The Tees Valley also includes the South Tees Development Corporation, which is the

single biggest development opportunity in the UK right now. It is the first Mayoral Development

Corporation outside of Greater London and the 4,500-acre site is six times bigger than the City of

London.

Key messages

• Tees Valley is a predominantly urban area, covering five distinct town centres. The

unique natural assets and sectoral strengths across the five Tees Valley local authorities

combine to create the opportunity to build a diverse and inclusive economy for Tees

Valley residents and businesses.

• In addition to ranking as one of the most deprived parts of the country, Tees Valley has a

highly-polarised distribution of deprivation. It ranks as the second most deprived LEP

area in England with all five Tees Valley districts ranking in the most deprived 15% of

local authorities nationally.

• Tees Valley is most deprived in the Health domain, with Employment deprivation second

and Income deprivation a close third. However, Tees Valley shows relatively low levels

of deprivation in both Barriers to Housing & Services and Living Environment domains.

• Tees Valley has a wide range of extensive development sites, opportunities and financial

incentives including the Mayoral South Tees Development Corporation and Special

Economic Area, together with seven Enterprise Zones offering Business Rate Relief and

Enhanced Capital allowances.

• The Tees Valley total resident population stood at 674,300 in 2018 – the smallest

Combined Authority in terms of total population numbers. However, in terms of the

wider economic catchment area population, around three million people live within an

hour’s drive of Tees Valley – on a par with the core population of other urban areas in

the North of England such as Greater Manchester and Leeds City Regions.

• The Tees Valley can be defined as a functional economic area with close to 9 in 10 local

jobs filled by Tees Valley residents and similarly close to 9 in 10 local residents employed

within Tees Valley i.e. relatively small and balanced levels of in and out-commuting.

• The population of Tees Valley has grown in recent years, albeit this has been at a slower

rate of growth than levels seen nationally. The majority of the increase in our population

size can be attributed to an ageing population.

11

The following section provides a geographical overview of the Tees Valley, taking into consideration,

the emerging demographic profile of the region, the urban/rural split in terms of population and the

location of key industrial sites and Enterprise Zones offering Business Rate Relief and Enhanced

Capital allowances. Relative deprivation rates at the community level are also examined.

A focus on geography is particularly important in the Tees Valley Strategic Economic Plan, which calls

for capital investment to be focused in urban settlements and enterprise zones. It is also important

to plan local programmes and make the case to attract national resources on the basis of need,

which can maximise economic impact and increase social inclusion. By understanding our

geography, we can develop initiatives and plan for developments that play to our region’s strengths,

including our natural assets, and address areas of challenge.

3.1. Geography Covering over 300 square miles and located on the North East coast, Tees Valley comprises five local

authority areas including: Darlington, Hartlepool, Middlesbrough, Redcar & Cleveland and Stockton-

on-Tees.

The Tees Valley area represents 1.2% of the population of England and 0.6% of the English land

mass; it is highly urbanised, with 90% of the population in urban areas. Around one third of the total

population is concentrated in the five main town centres with the remaining population located in

the suburbs, in smaller settlements, or rural areas.

• Compared to national averages, Tees Valley has a relatively aged population profile.

There is a smaller than average labour force with relatively more residents aged 65+ and

relatively fewer aged 16 to 64 compared to the UK. Projections indicate that this trend is

set to continue, with population growth driven mainly by those over retirement age in

the next two decades. However, decreasing numbers of 16 to 64 residents will be

potentially offset to a degree by ongoing increases in the State Retirement Age.

• There is a risk that these demographic trends lead to skills shortages as highly skilled

staff leave the workforce.

• The region has relatively poor levels of health impacting negatively on the pool of

available labour supply.

• Tees Valley international net in-migration rose sharply (up 86%) in 2018, however both in

and out international migration rates continue to be half that observed nationally.

• Migration flows are relatively low in Tees Valley compared to many other parts of the

country. Whilst this does result in a more stable population, it does exacerbate the Tees

Valley’s relatively aged population profile as migrants tend on average to be younger

people.

12

Figure 3.1. Tees Valley area

As a major settlement with a growing service industry, Stockton-on-Tees is the largest of the Local

Authority areas in employment and population terms. The borough’s economy is diverse, with

sectoral strengths in Chemical & Process, Advanced Manufacturing, Clean Energy Low Carbon &

Hydrogen and Construction. Key companies include Fujifilm Diosynth Biotechnologies and Johnson

Matthey, heavy industries include the expansion of the SUEZ UK energy from waste site, and a

growing digital sector includes fast growing Visualsoft. A range of office and industrial business

accommodation is available, such as Wynyard Business Park, Teesside Industrial Estate and Belasis

Business Park, together with the industrial areas of North Tees and Seal Sands, plus incubation

facilities. Numbers of overseas students in the area continue to grow with Durham University’s

International Study Centre. A large percentage of the population of Stockton-on-Tees is located in

the Stockton built up town area, with the remainder of the population spread between a number of

local areas such as Billingham, Thornaby, Ingleby Barwick, Norton and Fairfield.

Middlesbrough continues to diversify its economy with a stronghold in engineering companies

across the borough, the recently developed TeesAMP site provides world-class research and

commercial premises, including a home to TWI, an internationally renowned research institute. The

digital cluster centred in the Boho area is becoming nationally recognised and has a unique

opportunity to play a critical role in the productivity growth of the Tees Valley’s industrial base in its

adoption of Industry 4.0 (industrial digitalisation). Middlehaven continues to develop as a mixed use

regeneration site with leisure (home to Middlesbrough FC and the site for a new snow centre),

offices including Boho 5, innovative residential developments and education facilities. Home to

Teesside University, the development of modern student facilities and proposals for a student village

integrates the role of the university within the town. The town is also home to Tees Valley’s largest

employer South Tees NHS Trust, with almost 9,000 employees. The introduction of direct rail

services to London and improvements at the station and the surrounding area will form the stimulus

for independent businesses in the Historic Quarter linking the centre to the Boho area. A significant

13

amount of the population of Middlesbrough is located in Middlesbrough’s built up area with the

remainder of the population spread between a number of local areas such as Acklam, Linthorpe,

Coulby Newham, Grove Hill & Beechwood and Marton.

Darlington is a gateway to Tees Valley, with direct connections to the A1(M) and the East Coast

mainline as well as Teesside International Airport. Sectoral strengths are Advanced Manufacturing,

Digital, Logistics and Healthcare and the town is home to some major engineering and specialist

services companies (Cleveland Bridge, Magnet, Cummins and Wood) including subsea and seabed

companies (Deep Ocean and Modus). At Central Park, the home to CPI’s National Biologics

Manufacturing Centre and Teesside University’s National Horizons Centre, the town is the ideal

location for the development of the biologics market. With its proximity to the A1(M) the borough is

a growing location for logistics distribution centres – Amazon has recently announced plans to open

a new fulfilment centre and is starting to recruit for more than 1,000 new permanent jobs – with the

opportunity for further developments at key sites. It has arich heritage including the first railway

from Darlington to Stockton (with a bicentenary in 2025). A large percentage of the population of

Darlington is located in the Darlington built up area, with the remainder of the population spread

between a number of towns and villages. Outside of the town centre the largest population shares

are in Middleton St. George, Hurworth, Faverdale, Heighington and Harrowgate Village.

Redcar and Cleveland, which contains the coastal town of Redcar and is historically associated with

the steel and chemicals industry has the third largest population. It has a broad range of sectoral

strengths including Raw Materials and Agriculture, Chemical & Process, Clean Energy Low Carbon &

Hydrogen, Advanced Manufacturing, Logistics and Creative, Culture & Leisure. Redcar & Cleveland is

home to the UK’s largest integrated industrial complex with Wilton International one of the UK’s

most important locations for process manufacturing including global companies, Sabic, Sembcorp

Utilities, Ensus, Lotte Chemical, Huntsman and Falck. The South Tees Development Corporation is

one of the biggest industrial and coastal development sites (4,500 acres) in Britain and it presents a

unique opportunity to develop the Tees Valley’s strength in clean growth. With the combination of

assets including large scale sites, deep access port facilities, global companies and innovation

organisations including the Materials Processing Institute and the Centre for Process Innovation, the

area can become the clean growth centre of the UK. The borough is still home to a significant steel

industry and mining and processing of minerals is growing with Boulby mine, one of the deepest in

Europe, and the new £2.3bn polyhalite mine under construction in North Yorkshire with processing

to take place at Wilton. A large amount of the population of Redcar and Cleveland is located in the

Redcar area with the remainder of the population spread between a number of local towns and

villages such as Guisborough, Eston, Marske, Skelton, Grangetown, Ormesby, Saltburn and Brotton.

Hartlepool is the smallest Local Authority in both population and employment terms. It is home to

Hartlepool Port, has strong historic links to the maritime industry and sectoral strengths in Clean

Energy Low Carbon & Hydrogen, Chemical & Process, Advanced Manufacturing, Healthcare and

Education. The town is home to the Northern School of Art, the leading provider of specialist

creative art and design in the north, counting Sir Ridley Scott among its former pupils. It is central to

the opportunity to create the biggest film studios outside London on the former council depot site,

which will put Hartlepool at the centre of film making in the north. The town offers excellent

opportunities for port-related industries with more than 300 acres at the Port of Hartlepool owned

and operated by PD Ports, with deep water access, warehousing and open storage. Engineering

companies employ around 1,700 people with Liberty Steel and Able, with Seaton Port one of the

largest dry dock facilities in the world and a recycling facility of international significance (currently

dismantling the Shell Brent Delta platform). The chemicals industry is still also important to the town

14

and clean energy production at EDF’s Nuclear Power Plant generates 60GW (2% of GB’s peak

electricity demand). A smaller percent of the population of Hartlepool is located in and around the

town centre area, with the population mainly spread between a number of local areas such as

Throston, West View, Seaton Carew, Middle Warren and Clavering.

Figure 3.2 compares the urban/rural composition of the Tees Valley area:

Figure 3.2. Rural/Urban split of Tees Valley area

3.2. Local level deprivation

The Ministry of Housing, Communities and Local Government (MHCLG) published the latest Index of

Multiple Deprivation (IMD 2019) in September 2019. This comprises deprivation scores and national

ranks for all Lower Super Output Areas (LSOAs) in England, plus Local Enterprise Partnership (LEP)

and local authority (LA) results. A wide variety of indicators are combined to form seven domains –

Income, Employment, Education, Health, Crime, Barriers to Housing & Services and Living

Environment. The Income domain includes two sub-domains namely IDACI (Income Deprivation

Affecting Children Index) and IDAOPI (Income Deprivation Affecting Older People Index). The seven

domains are then combined into overall deprivation scores (the IMD) for every LSOA in England.

IMD is a nationally recognised measure of deprivation in small areas across England and is used

widely to target programmes that tackle inequality and deprivation. The IMD also provides a useful

means to guide the allocation of resources, with the potential to be used to inform allocation of

funding going forward, for example, UK Shared Prosperity Fund (UKSPF). Tees Valley’s relative levels

of deprivation can therefore be used in messaging to shape government policy and resource

allocation that reflects levels of need and vulnerabilities to economic shocks.

© Crown Copyright and database rights 2014 Ordnance Survey Licence No. 100022861 | Source: ONS, DEFRA, DCLG

15

Key messages for Tees Valley

• IMD 2019 shows a slight increase in relative deprivation across Tees Valley compared with 2015, with little change to the overall pattern of highly-polarised deprivation in the area

• Tees Valley has a relatively high proportion of LSOAs within the most deprived 10% nationally, ranking as the second most deprived LEP in England (out of 38 LEP areas). This ranking is unchanged since 2015

• 121 or 29% of Tees Valley’s 417 LSOAs are in the 10% most deprived nationally, almost three times the national rate

• Tees Valley is most deprived in the Health domain, with Employment deprivation second and Income deprivation a close third

• More positively, Tees Valley shows relatively low levels of deprivation in both Barriers to Housing & Services and Living Environment domains

• At the local authority level and out of 317 districts nationally, Middlesbrough has the highest proportion of LSOAs within the national most deprived 10% with Hartlepool 10th, Redcar & Cleveland 29th, Stockton-on-Tees 39th and Darlington 47th

• All five local authority areas now rank amongst the 15% most deprived local authorities in England.

The figure below depicts the distribution of deprivation levels across Tees Valley. It shows how the

most deprived neighbourhoods are generally concentrated within the urban areas of Tees Valley.

Figure 3.3. Indices of Multiple Deprivation, Tees Valley LSOAs, 2019

Source: MHCLG. English Indices of Deprivation 2019

16

Ranking by domain - key points

• Tees Valley ranks as the least deprived LEP area on the Living Environment domain. This

domain covers two sub-domains; the indoors sub-domain measuring the quality of housing

and the outdoors sub-domain measuring air quality and road traffic accidents. Tees Valley

also ranks as relatively less deprived on the Barriers to Housing and Services domain as

discussed in Section 9.1.

• Tees Valley ranks as the most deprived LEP area in regards to the Income deprivation

affecting children index (IDACI) sub-domain. All five Tees Valley local authority areas record

higher levels of relative deprivation on the IDACI sub-domain as compared to the IDAOPI –

the Income deprivation affecting older people index. With Tees Valley also ranking as the

fourth most deprived LEP on the IDAOPI sub-domain, this suggests that child poverty is

relatively more of an issue than pensioner poverty in the Tees Valley.

• Reflecting Tees Valley’s overall IMD of second most deprived LEP area, the area also ranks

second most deprived on many domains including the overall Income domain, the

Employment domain, the Education domain and the Health domain. Tees Valley ranks as

the third most deprived LEP in terms of the Crime domain.

The table below summarises the IMD domain ranks by local authority.

Table 3.1. Rank of proportion of LSOAs in most deprived 10% nationally

Rank out of 317 LA areas Rank out of 38 LEP areas

Darlington Hartlepool Middlesbro’ R&C Stockton Tees Valley

Income 41 7 1 24 33 2

- IDACI 30 3 1 13 37 1

- IDAOPI 79 15 11 52 55 4

Employment 52 5 2 12 39 2

Education 42 38 3 46 61 2

Health 35 16 4 18 28 2

Crime 20 14 3 58 84 3

Barriers 199 250 250 250 219 35

Living Env. 251 251 251 235 251 38

IMD 47 10 1 29 39 2

Source: IMD 2019

3.3. Enterprise Zones There are a wide range of cost-effective sites and premises across Tees Valley, with seven Enterprise

Zones offering Business Rate Relief and Enhanced Capital allowances. The list of enterprise zones

includes:

Business Rate Relief Enterprise Sites:

• Northshore, Stockton-on-Tees;

• Central Park, Darlington; and

• Middlesbrough Historic Quarter.

The Business Rate Relief sites offer a discount of up to £55,000 each year for five years, totalling

£275,000. The sites benefit from excellent transport links, simplified planning and broadband

connections:

17

Enhanced Capital Allowance (ECA) Sites:

• South Bank Wharf, Redcar & Cleveland;

• New Energy & Technology Park; Stockton-on-Tees;

• Wilton International, Redcar & Cleveland; and

• Hartlepool Port Estates

The ECA benefits are on the larger industrial sites to help incentivise investment from companies in

the renewable energy, chemicals and advanced manufacturing and engineering sectors. Companies

locating on these sites can apply to receive first-year capital allowance at 100% on qualifying plant

and machinery, to a maximum of £100m to offset against corporation tax when the investment is

made before March 2020. Tees Valley is one of only a small number of areas across the country that

can offer large-scale occupiers enhanced capital allowances on their plant and machinery.

3.4. South Tees Development Corporation/Special Economic Area

The South Tees Development Corporation is the single biggest development opportunity in the UK

right now. It is the first Mayoral Development Corporation outside of Greater London and the 4,500-

acre site is six times bigger than the City of London.

The vision will see the area transformed into a hotbed of new industry and enterprise, focused on

clean energy, the circular economy, industrial symbiosis and advanced manufacturing, that will

create 20,000 new jobs and add an additional £1bn per annum into the Tees Valley economy.

The Development Corporation area is prime development land on the banks of the River Tees and benefits from the presence of strategically important businesses, facilities and operations that enhance the attractiveness of the site, including Teesport, Redcar Bulk Terminal, Northumbrian Water, British Steel and BOC. The South Tees Development Corporation owns more than half of all the developable land within its boundary following a deal with Tata Europe UK to acquire 1,420 acres in early 2019. It continues to engage with other landowners and interested parties and is expecting to have concluded all land deals by mid-2020. It offers access to the River Tees as well as one of the deepest water ports on the east coast of England, making it ideal for companies looking to export to global markets. The area has excellent transport connections, with rail-connected port-side facilities and access to the wider strategic road network and the rest of the UK. It is less than 30 minutes away from Teesside International Airport. The South Tees Development Corporation has significant Government support and in the 2018 Autumn Budget it was granted Special Economic Area status, the only site in the UK to have such status. So far Government has backed the Development Corporation with more than £208m to prepare the land for new investment.

18

Key Findings:

• There has been an upward

trend since the turn of the

millennium of the population

size of Tees Valley.

• This population growth of

2.8% has still lagged below

that in the North of England

(7.4%) and England as a

whole (17%).

Figure 3.4. South Tees Development Corporation area

3.5. Demography

The mid-2018 population of Tees Valley is estimated to be 674,300, with a total of three million

people living within an hour’s drive of the area. Figure 3.5 illustrates the overall population change

in Tees Valley over the last 27 years.

Figure 3.5. Total resident population in Tees Valley, 1991-2018

Source: ONS Population Estimates

Whilst the population of Tees Valley is predominantly White British (93%), Tees Valley is home to a

small Black and Minority Ethnic (BME) community with Middlesbrough having an ethnic make-up

that more closely reflects the national picture (86% of Middlesbrough’s population is White British

compared with 80% of England’s).

Health levels have improved across Tees Valley, however they remain lower than in the country as a

whole with 7% of the working age population claiming to be long term sick compared 4.6%

nationally.

19

Key Findings:

• 19.5% are aged between 0-15

years old (131,400 people),

compared to 19.2% nationally.

• 61.5% are aged between 16-64

years old (414,440 people),

compared to 62.6% nationally).

• 19% are aged over 65 (128,420

people), compared to 18.2%

nationally.

Figure 3.6. Age split of current population

Source: ONS Mid-2018 Population Projections

Table 3.2 compares the demographic profile of Tees Valley to England as a whole:

Table 3.2. Demographic profile, Tees Valley and England

Description Tees Valley England

Population (2018) 674,300 55,977,200

Population projection (2028) 679,700 59,043,500

Population projection (2038) 680,600 61,326,400

Geographical coverage (hectares) 79,400 13,027,800

Population density 8.5 4.3

Birth rate 1.11% 1.12%

Death rate 1.07% 0.90%

Life expectancy (2016-18) 79.3 years 81.4 years

Healthy life expectancy (2016-18) 59.5 years 63.6 years

International in-migration rate 0.50% 1.00%

International out-migration rate 0.10% 0.60%

Internal in-migration rate 3.90% n/a

Internal out-migration rate 4.00% n/a

Median age 40 38.9

Population growth rate 0.3% 0.6%

Sources/notes: ONS mid-2018 population estimates, ONS 2016-based population projections, Census 2011. Tees Valley life

and healthy life expectancy are simple averages of district estimates, ONS. Rates are a percentage of population in mid-

2018.

20

Key Findings:

• International net immigration

was higher in all five local

authorities in Tees Valley, with

Middlesbrough seeing the

largest rise of 510 when

compared with 2017.

• This drop in 2017 and rise in

2018 mirrors trends seen

across the wider North East

and UK.

3.6. Migration

Following the vote to leave the EU in 2016 and reflecting national trends, there was a sharp drop in

international net migration in Tees Valley in 2017. However recent figures show that in the year to

Mid-2018 international net migration in Tees Valley increased by 86.4%, up by 1,250 on the year

from 1,450 in 2017 to 2,700 in the year to mid-2018.

Figure 3.7. International Net Migration trends by Local Authority

Source: ONS

Migration flows are relatively low in Tees Valley compared to many other parts of the country.

Whilst this does result in a more stable population, it does exacerbate the Tees Valley’s relatively

aged population profile as migrants tend on average to be younger people. Compared to England as

a whole, Tees Valley international in and out migration rates were less than half that observed

nationally. Rates were highest in Central London, the university cities of Oxford and Cambridge and

large cities across the country.

Figure’s 3.8 and 3.9 illustrate the international inflow and outflow rates for the Tees Valley

compared with the wider North East and England.

Figure 3.8. International Inflow

Figure 3.9. International Outflow

Source: ONS

21

Key Findings:

• The Tees Valley population is

projected to increase by 0.8%

over the next 10 years (to

around 679,900 by 2029),

however this is a small increase

compared to a 5.2% increase

nationally and a 2.8% increase

across the North of England.

• Over the next 20 years (2039)

the population is expected to

increase by 0.9% compared to a

9.2% rise nationally and a 4.6%

rise across the North of England.

3.7. Population Trends and Projections

The population projections shown in this section are taken from the ONS 2016 based subnational

population projections. ONS recognise that these projections are not forecasts and take no account

of local policy or development aims that have not yet had an impact on observed trends.

The Tees Valley population is projected to continue its long-term growth seen since the start of the

millennium of approximately 1,000 per year until 2020, growth is then projected to slow both locally

and nationally reaching around 680,700 by 2039.

Figure 3.10. Projected total resident population in Tees Valley, 2019-2039

Source: ONS Population Projections

Although there is projected growth in the following 20 years, growth is not expected in all age

groups. Figure 3.11 shows the age make-up of the Tees Valley population in 2018 and then

projected make-up in 2028 and 2038:

Figure 3.11. Demographic Projections

2018 Estimates 2028 Projection 2038 Projection

Source: ONS Population Projections

22

Currently (ONS mid 2018) 0-15 year olds make up 19% of the population. We are moving towards

the projected peak of this age group in 2021, with an extra 700 children projected, adding pressure

to our schools over the next few years, before then falling steadily each year until 2039.

The working age population (16-64s) is predicted to be almost 28,400 lower in 20 years’ time, from

61% of the total population in 2018 to 57% in 2038.

There will be an increase in the proportion of over 65s with the percentage of population over the

retirement age expected to grow from 19% in 2018 to over a quarter of the population in 2038, this

coupled with the fall in working age population will bring skills shortages when experienced and

highly skilled staff leave the workforce. There will also be implications on health services as

pressures increase.

Figure 3.12 illustrates the change in detailed age group from 2001 until 2037.

Figure 3.12. Population estimates and projections by age group

Source: ONS Population Projections

23

3.8. Area Profile SWOT analysis

Strengths Weaknesses

There are a wide range of cost-effective sites and premises across Tees Valley, with seven Enterprise Zones providing a range of financial incentives to companies choosing to locate in the region, as well as simplified planning and super-fast broadband. Tees Valley demonstrates low levels of deprivation in relation to Living Environment and Barriers to Housing and Services.

Health levels in Tees Valley remain lower than in the country as a whole. The number of people with a long term illness is above national average, affecting the working age population. In addition to high levels of Health deprivation, Tees Valley ranks highly deprived on Employment, Income and Crime domains.

Opportunities Threats

Tees Valley contains the South Tees Development Corporation (STDC) – the first Mayoral Development Corporation outside of London, and often cited as the single biggest development opportunity in the UK at the current time. STDC was set up to promote economic growth and commercial development by converting assets in the South Tees area into opportunities for business investment and economic growth. A new Special Economic Area (SEA) will soon be established in Tees Valley across the STDC site with the power to retain business rates to reinvest in developing more of the site, reducing the ask of local taxpayers. Tees Valley’s sector strengths and natural assets, present opportunities for the region to become a global leader in clean energy, low carbon and hydrogen. The cost and quality of living in Tees Valley create an opportunity to attract and retain skilled workers, with the area having relatively low levels of deprivation in both Barriers to Housing & Services and Living Environment domains.

The population growth in Tees Valley is now projected to slow, with the growth rate much lower than national; however these ONS projections do not take into account local policy or development aims that have not yet had an impact on observed trends. The Tees Valley has a rapidly ageing population and declining working age population / labour force. There is a risk of skill shortages when experienced and highly skilled staff leave the workforce with an added implication on health services. The number of 0-15 year old Tees Valley residents is expected to peak in 2021, with extra pressures expected on primary and secondary school places in the short term before numbers are projected to drop steadily. Following the vote to leave the EU in 2016 and reflecting national trends, there was a sharp drop in international net migration into Tees Valley in 2017. Although this has seen a rise in 2018 there is a risk that EU negotiations in 2020 will affect international net migration in the coming years, and therefore access to skilled workers.

24

Section 4: Economic Growth and Productivity

The following section provides a summary of the Tees Valley economy in terms of Gross Domestic

Product (GDP), Gross Value Added (GVA), productivity and trade. Sectoral breakdowns are identified

where feasible and comparisons made against national and local indicators where appropriate. This

section seeks to determine the degree of the Tees Valley productivity gap and identify its constituent

parts.

Economic growth is an important indicator of wealth creation and economic performance. A key

target in the Tees Valley Strategic Economic Plan is to raise productivity. In addition, productivity is

the primary focus of the locally agreed draft Tees Valley Local Industrial Strategy.

Key messages

• Whilst Tees Valley economic output contributed £16.2bn to the UK economy in 2018, the

region has a significant productivity challenge, particularly in relation to GDP and GVA

per head of population. At £24,085 per annum, Tees Valley GDP per capita was some

75.3% of the UK rate in 2018, representing a Tees Valley GDP gap of £5.3bn. This gap has

doubled in current price terms since 2010. GVA per capita in Tees Valley was £20,370 in

2018 at 71.5% of the UK’s £28,489.

• However, despite the relatively poor performance of Tees Valley based on GDP and GVA

per capita, the region fares much better on GVA per hour worked and GVA per job. Tees

Valley GVA per hour worked was 90.9% of the UK rate in 2018 whilst GVA per job was

88.8% - both rates being broadly around English LEP medians and above North of

England LEP averages.

• The Tees Valley economy recorded a real terms decline in GDP of £329m in 2018 – a

2.1% decrease on 2017. This makes Tees Valley the worst performing LEP area in terms

of growth by some margin – the next worst performing LEP saw GDP fall by 0.9%. UK

GDP growth averaged 1.4% in 2018.

• In real terms the Tees Valley economy (GDP) is marginally smaller now (2018) than it was

in 2011. 2016 and 2018 in particular were difficult years, with Tees Valley real GDP

decreasing by 3.5% between 2015 and 2018. Only two of the past seven years have seen

any economic growth. However, these two years (2014 and 2015) saw robust growth

with local real GDP up by 4.0% between 2013 and 2015.

• During the 2008/09 recession Tees Valley GDP fell less sharply than the UK, with other

parts of the country that had relatively larger private sectors perhaps quicker to cut

employment during the downturn. However, this in turn meant that the Tees Valley was

slower to recover post-recession. Because of the Tees Valley’s relatively small private

sector, it retains a dependency on the public sector with Public Administration,

Education and Health all accounting for a larger share of the economy than is the case

nationally.

• Tees Valley has relatively high employment concentrations in some higher than average

productivity sectors and sub-sectors, particularly within the Chemicals/Process,

Advanced Manufacturing, Construction and Clean Energy, Low Carbon & Hydrogen

sectors.

25

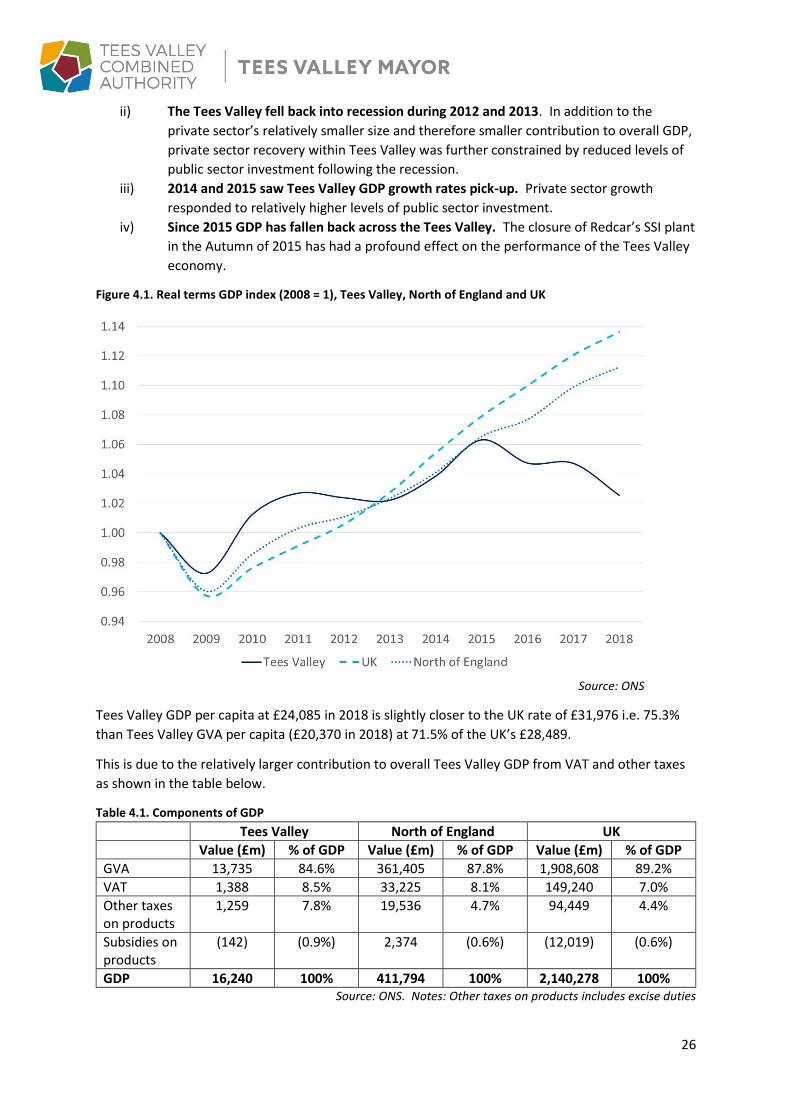

4.1. Total GDP and GVA

Office for National Statistics annual GDP and GVA statistics (GDP essentially comprises GVA plus

taxes e.g. VAT or Excise duties, less any subsidies) are now published for local level geographies.

However, GDP is only available at the aggregate level and so GVA is still used to provide the sectoral

breakdown. Whilst current prices are used for point in time headlines e.g. 2018 estimates, change

over time is measured in ‘real’ terms i.e. allowances made for inflation. These real term estimates

are thus consistent with other economic measures such as the quarterly headline estimates of UK

GDP.

Aggregate economic output (as measured by GDP) from Tees Valley amounted to £16.2bn in 2018, a

2.1% real terms decrease on 2017. This compares to real terms increases of 1.4% nationally and

1.2% in the North of England as a whole. Tees Valley GDP now accounts for 3.9% of the North of

England’s GDP, 0.88% of England’s and 0.76% of the UK’s.

However, Tees Valley GDP per capita was just 75.3% of the UK rate in 2018, down significantly from

80.8% of the UK rate observed as recently as 2015.

This means that the Tees Valley now has a GDP or output gap of £5.3bn – the additional level of

economic output required in Tees Valley to match the UK GDP per capita rate. This gap is now more

than twice what is was (in nominal terms) immediately following the 2008/09 recession in 2010.

As an approximate measure of productivity, GDP per capita is dividing a workplace-based numerator

(GDP) by a residence-based denominator (residential population). This means that this measure

does not account for people commuting into and out of a region and significant commuting flows

can lead to highly distorted results. Also, by including all the residential population (including

children, pensioners and others not economically active) and not just those who are in employment,

the denominator includes residents who are not directly contributing to GDP i.e. those residents not

in employment.

Tees Valley GDP performance against the UK and the North of England over the past decade is

shown below. Four broad economic phases are identified:

i) The 2008/09 recession impacted relatively less negatively on the economy in Tees

Valley than in the North of England and the UK as a whole. As the private sector is

more immediately responsive to economic change and with the private sector

comprising larger proportions of the economy in both the North of England and the UK

than Tees Valley, the region was firstly relatively protected during the recession but

secondly was less able to recover in the years following the 2008/09 recession.

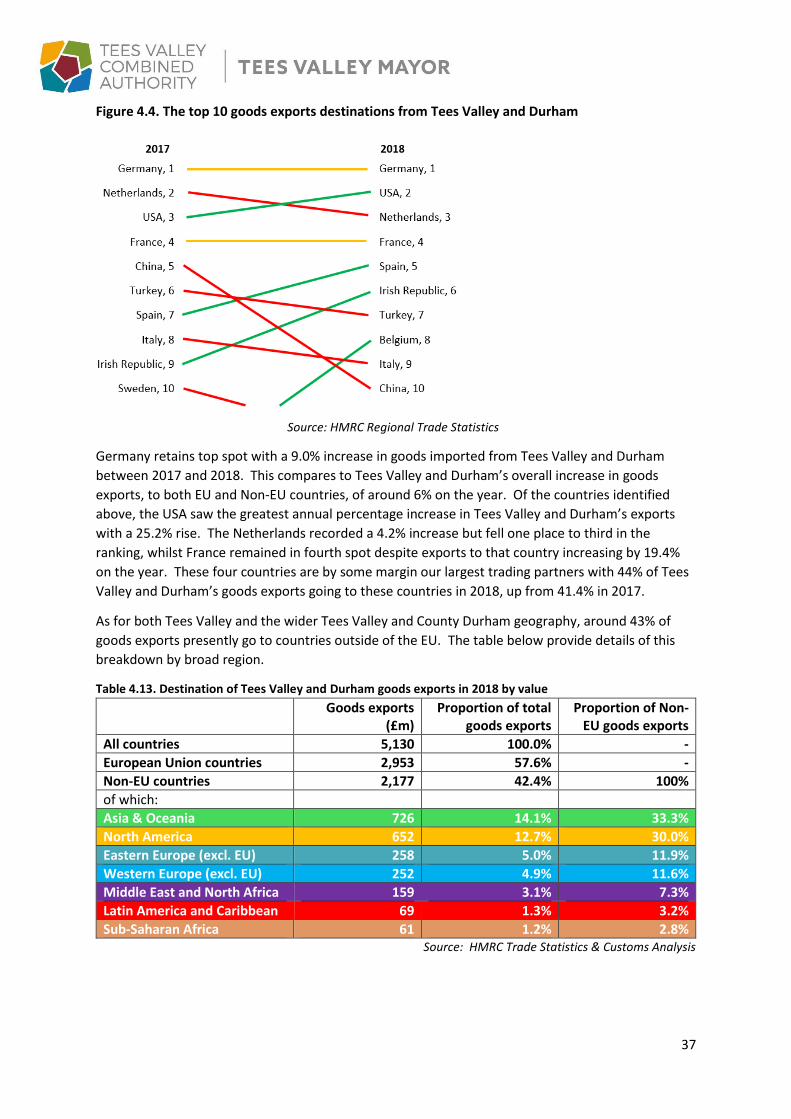

• Tees Valley is a strong exporting region and exported close on £3.3bn of goods during

2018, equivalent to around 20% of Tees Valley GDP. This proportion is well above the UK

rate of 16% and the North of England average of 14%.

• Reflecting the area’s strength in Chemicals, 37% of goods exported in Tees Valley &

Durham are from this sector, compared to 16% nationally.

• Tees Valley service exports totalled £1.3bn in 2017. £412m or 31% of the total were

manufacturing sector services – over 5 times the national concentration for this sector.

26

ii) The Tees Valley fell back into recession during 2012 and 2013. In addition to the

private sector’s relatively smaller size and therefore smaller contribution to overall GDP,

private sector recovery within Tees Valley was further constrained by reduced levels of

public sector investment following the recession.

iii) 2014 and 2015 saw Tees Valley GDP growth rates pick-up. Private sector growth

responded to relatively higher levels of public sector investment.

iv) Since 2015 GDP has fallen back across the Tees Valley. The closure of Redcar’s SSI plant

in the Autumn of 2015 has had a profound effect on the performance of the Tees Valley

economy.

Figure 4.1. Real terms GDP index (2008 = 1), Tees Valley, North of England and UK

Source: ONS

Tees Valley GDP per capita at £24,085 in 2018 is slightly closer to the UK rate of £31,976 i.e. 75.3%

than Tees Valley GVA per capita (£20,370 in 2018) at 71.5% of the UK’s £28,489.

This is due to the relatively larger contribution to overall Tees Valley GDP from VAT and other taxes

as shown in the table below.

Table 4.1. Components of GDP

Tees Valley North of England UK

Value (£m) % of GDP Value (£m) % of GDP Value (£m) % of GDP

GVA 13,735 84.6% 361,405 87.8% 1,908,608 89.2%

VAT 1,388 8.5% 33,225 8.1% 149,240 7.0%

Other taxes on products

1,259 7.8% 19,536 4.7% 94,449 4.4%

Subsidies on products

(142) (0.9%) 2,374 (0.6%) (12,019) (0.6%)

GDP 16,240 100% 411,794 100% 2,140,278 100% Source: ONS. Notes: Other taxes on products includes excise duties

27

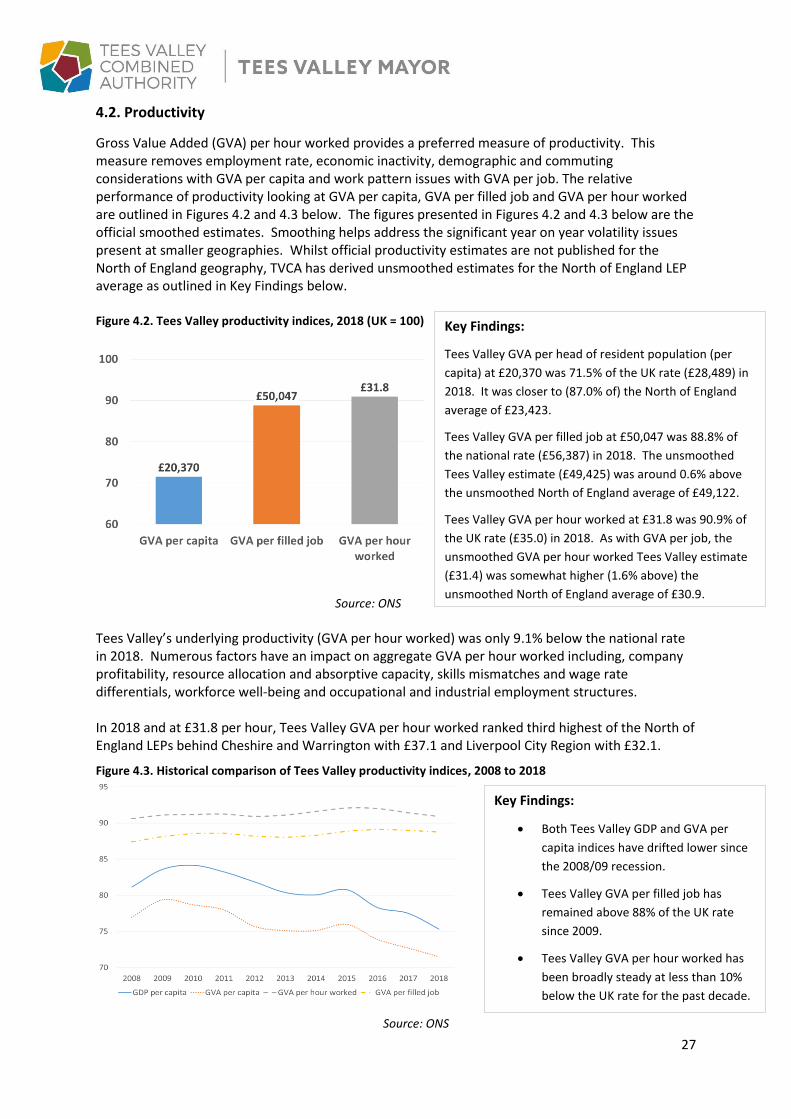

4.2. Productivity

Gross Value Added (GVA) per hour worked provides a preferred measure of productivity. This measure removes employment rate, economic inactivity, demographic and commuting considerations with GVA per capita and work pattern issues with GVA per job. The relative performance of productivity looking at GVA per capita, GVA per filled job and GVA per hour worked are outlined in Figures 4.2 and 4.3 below. The figures presented in Figures 4.2 and 4.3 below are the official smoothed estimates. Smoothing helps address the significant year on year volatility issues present at smaller geographies. Whilst official productivity estimates are not published for the North of England geography, TVCA has derived unsmoothed estimates for the North of England LEP average as outlined in Key Findings below.

Figure 4.2. Tees Valley productivity indices, 2018 (UK = 100)

Source: ONS

Tees Valley’s underlying productivity (GVA per hour worked) was only 9.1% below the national rate in 2018. Numerous factors have an impact on aggregate GVA per hour worked including, company profitability, resource allocation and absorptive capacity, skills mismatches and wage rate differentials, workforce well-being and occupational and industrial employment structures. In 2018 and at £31.8 per hour, Tees Valley GVA per hour worked ranked third highest of the North of England LEPs behind Cheshire and Warrington with £37.1 and Liverpool City Region with £32.1.

Figure 4.3. Historical comparison of Tees Valley productivity indices, 2008 to 2018

Source: ONS

Key Findings:

Tees Valley GVA per head of resident population (per

capita) at £20,370 was 71.5% of the UK rate (£28,489) in

2018. It was closer to (87.0% of) the North of England

average of £23,423.

Tees Valley GVA per filled job at £50,047 was 88.8% of

the national rate (£56,387) in 2018. The unsmoothed

Tees Valley estimate (£49,425) was around 0.6% above

the unsmoothed North of England average of £49,122.

Tees Valley GVA per hour worked at £31.8 was 90.9% of

the UK rate (£35.0) in 2018. As with GVA per job, the

unsmoothed GVA per hour worked Tees Valley estimate

(£31.4) was somewhat higher (1.6% above) the

unsmoothed North of England average of £30.9.

Key Findings:

• Both Tees Valley GDP and GVA per

capita indices have drifted lower since

the 2008/09 recession.

• Tees Valley GVA per filled job has

remained above 88% of the UK rate

since 2009.

• Tees Valley GVA per hour worked has

been broadly steady at less than 10%

below the UK rate for the past decade.

28

4.3. Sectoral GVA

This section examines the most recent five year Tees Valley GVA trends across 17 broadly defined

ONS sectors.

Table 4.1 breaks these 17 sectors down by sub-sector for 2018 and provides an indication as to that

sector’s relative share of total Tees Valley GVA as compared to that sector’s share nationally.

Sectors accounting for the same share of total GVA as nationally are said to have a location quotient

(LQ) of 1. Those with a higher share have a higher LQ and those with a lower share a lower LQ.

Overall Tees Valley GVA makes up 0.7% of UK GVA but in those sectors with an LQ of over one this

proportion is higher. The Tees Valley sub-sector that contributes the highest proportion of UK GVA

is the one with the highest LQ i.e. Social work activities with 1.3% of the UK GVA total for that sub-

sector.

Key points – change since 2013

• Tees Valley GVA was 2% higher in real terms in 2018 than it was in 2013. UK GVA was up by

10% over this time.

• Human health and social work activities is now the largest sector in Tees Valley with GVA of

more than £1.7bn in 2018 – up by 14% in five years. The sector also has the highest LQ of

any sector across Tees Valley and has replaced Manufacturing as the largest sector. Tees

Valley Manufacturing GVA has been revised down to £1.5bn (2018), 12% smaller in real

terms than in 2013.

• Within the Manufacturing sector, Wood, Petroleum, Chemicals & Minerals was down by 26%

since 2013 with Metals, Electrical products & Machinery down by 12%. Whilst these two

sectors remain relatively strong in Tees Valley (LQs>1), these strengths are significantly less

than previously. However, Food, Beverages, Textiles & Clothing was up by 36%.

• Driven by strong growth in Civil Engineering (up 52%) and Construction of Buildings (up

38%), the Construction sector was 7% larger in 2018 than in 2013. However, Specialised

Construction was down by 17%.

• Motor and Wholesale trades were up by over 40% since 2013 but Retail was down by 8%.

• Both Arts, entertainment & recreation and Transportation & storage were down by one-fifth

whilst Architectural and engineering services was down by one-quarter.

• Other sectors seeing increases in GVA between 2013 and 2018 included Accommodation

and food services (up 5%), Finance & insurance (up 35%), Professional, scientific & technical

(up 8%), Administrative & support services (up 11%), Public administration & defence (up

7%) and Other services (up 35%).

• Other sectors seeing decreases in GVA between 2013 and 2018 included Education (down

11%), Agriculture, mining, electricity, gas, water and waste (down 11%) and Information &

communication (down 2%). Real estate activities GVA was unchanged.

29

Sub-sectoral GVA

Table 4.2 below examines the 17 broad sectors in the above graphs by sub-sector and compares the

relative GVA contributions of those sub-sectors to national rates.

Table 4.2. GVA and GVA location quotient (LQ), 2018

GVA (£m) LQ (UK=1)

Agriculture, mining, electricity, gas, water and waste 617 1.03

Manufacturing - Manufacture of food, beverages, textiles and clothing - Manufacture of wood, petroleum, chemicals and minerals - Manufacture of metals, electrical products and machinery - Other manufacturing, repair and installation

1,569 216 521 711 120

1.15 0.86 1.33 1.17 1.07

Construction - Construction of buildings - Civil engineering - Specialised construction activities

891 191 252 448

1.07 0.73 1.56 1.09

Wholesale and retail trade; repair of motor vehicles - Motor trades - Wholesale trade - Retail trade

1,492 333 383 777

1.02 1.34 0.78 1.08

Transportation and storage - Land, water and air transport - Warehousing, transport support, postal and courier activities

540 309 231

0.95 1.05 0.85

Accommodation and food service activities 296 0.77

Information and communication 816 0.85

Financial and insurance activities 689 0.71

Real estate activities - Real estate activities, excluding imputed rental - Owner-occupiers' imputed rental

1,653 506

1,147

0.91 0.91 0.91

Professional, scientific and technical activities - Legal and accounting activities - Head offices and management consultancy - Architectural and engineering activities - Other professional, scientific and technical activities

787 213

87 197 290

0.73 0.60 0.47 1.03 0.85

Administrative and support service activities - Rental and leasing activities - Employment activities; tourism and security services - Services to buildings and landscape activities - Office administration and business support activities

530 132 215

46 138

0.72 0.84 0.67 0.55 0.80

Public administration and defence 878 1.32

Education 849 1.08

Human health and social work activities - Human health and residential care activities - Social work activities

1,734 1,384

351

1.66 1.62 1.84

Arts, entertainment and recreation 171 0.77

Other service activities - Membership organisations; repair of household goods - Other personal service activities

192 32

161

0.87 0.43 1.09

Activities of households 31 0.76

All sectors 13,735 1.00

Source: ONS

30

4.4 Sectoral productivity

The majority of Tees Valley’s key sectors have relatively high levels of productivity, with only

Healthcare and Creative, Culture & Leisure displaying relatively low productivity rates. Even then,

certain sub-sectors within Creative, Culture & Leisure have above average rates.

In total, a majority of key sectors record either or both of above average productivity rates and

above average employment concentrations. These sectors are Clean Energy, Low Carbon and

Hydrogen, Chemical and Process, Bioscience, Advanced Manufacturing, Construction and Logistics.

Only the Creative, Culture & Leisure sector displays both relatively low productivity and relatively

low employment concentration. However, this sector, alongside the Healthcare and Professional &

Business Services sectors is highly job rich, with these three sectors accounting for around one-third

of total employment in Tees Valley.

Finally, the Tees Valley Digital sector, whilst highly productive, is still relatively small compared to

many other parts of the country. However, the sector is growing rapidly and projections indicate

that this sector will play an important role in generating many jobs in the future. In addition, the

cross-cutting nature of the sector will support the development of other sectors, including with the

increasing trend towards manufacturing and industrial digitisation.

The ten key sectors can be categorised as follows:

Sub-sectoral productivity

The following analysis examines the ten sectors outlined above in more detail. The main sub-

sectors, ranked in terms of employment contribution, are identified for each sector. Note that in

terms of all sector average productivity, this is estimated at £52,000 for the UK in 2018. Also note

that Tees Valley total employment accounts for 1.0% of England’s total employment, so any Tees

Valley sub-sector that accounts for more than 1.0% of England’s employment is relatively strong in

terms of employment concentration (shaded green in the tables).

31

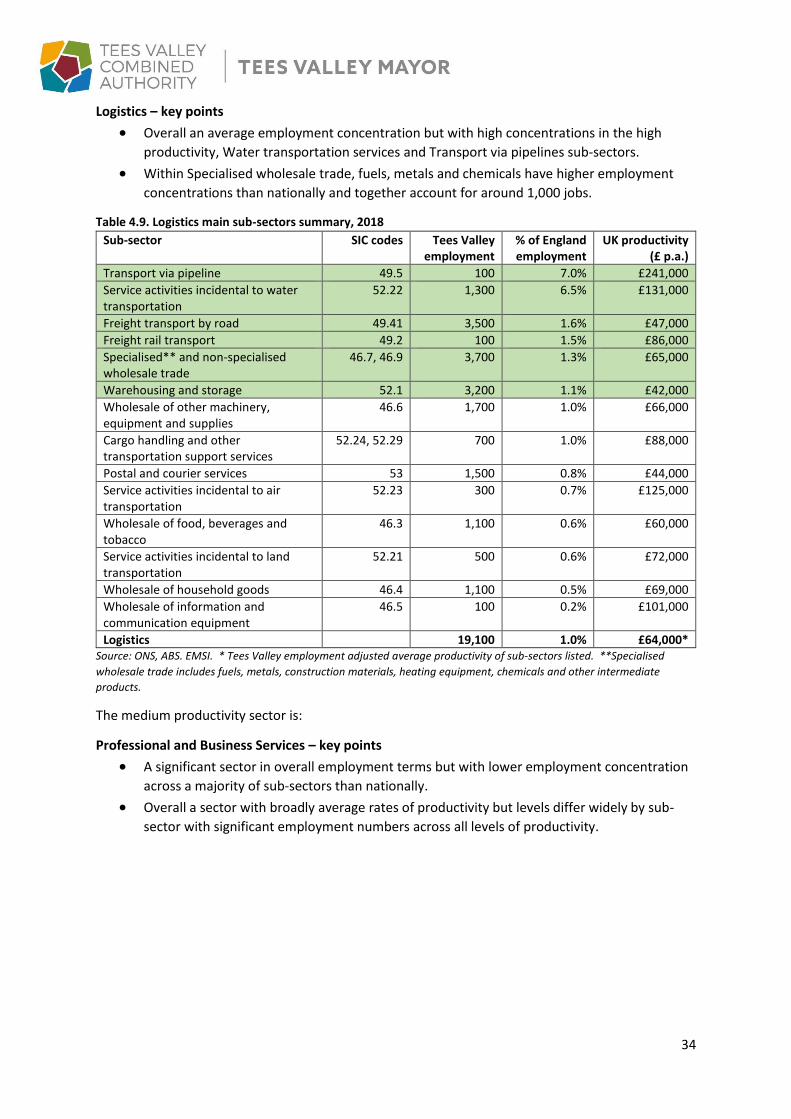

The three high productivity sectors are:

Clean Energy, Low Carbon & Hydrogen – key points

• High employment concentration across the majority of key sub-sectors, particularly with

regards to Remediation activities, Extraction of crude petroleum and Materials recovery.

• All sub-sectors display relatively high levels of productivity.

Table 4.3. Clean Energy, Low Carbon & Hydrogen main sub-sectors summary, 2018

Sub-sector SIC codes Tees Valley employment

% of England employment

UK productivity (£ p.a.)

Remediation activities 39 1,300 12.7% £93,000

Extraction of crude petroleum 6.1 200 7.8% £1.2m

Materials recovery 38.3 800 4.7% £95,000

Repair of fabricated metal products, machinery and equipment

33.1 2,100 2.5% £76,000

Electric power generation, transmission and distribution

35.1 1,100 1.4% £185,000

Renting and leasing of construction, civil engineering and other machinery

77.32, 77.39

700 1.2% £105,000

Water and sewerage 36, 37 500 1.0% £191,000

Waste collection, treatment & disposal 38.1, 38.2 800 0.8% £60,000

Clean Energy, Low Carbon & Hydrogen 8,100 1.5% £136,000* Source: ONS, Annual Business Survey (ABS). EMSI. Note: *Tees Valley employment adjusted average productivity of sub-

sectors listed.

Chemicals and Process – key points

• High employment concentration across all key sub-sectors.

• Chemicals manufacture is a high productivity sector and employs a large number of workers.

• Plastics is a medium productivity sector and a significant employer.

Table 4.4. Chemicals and Process main sub-sectors summary, 2018

Sub-sector SIC codes

Tees Valley employment

% of England employment

UK productivity (£ p.a.)

Manufacture of refined petroleum products 19.2 500 6.9% £186,000

Manufacture of chemicals and chemical products

20 3,300 3.8% £94,000

Manufacture of plastic products 22.2 1,500 1.1% £51,000

Chemicals and Process 5,400 2.2% £91,000*

Associated sub-sector: Mining of chemical and fertiliser minerals**

8.91 600 94.8% £73,000

Source: ONS, ABS. EMSI. Note: *Tees Valley employment adjusted average productivity of sub-sectors listed. **Technically

not defined as part of the Chemicals & Process sector, ‘Mining of chemical and fertiliser minerals’ is included here as a

significant associated sub-sectoral strength in employment terms. Productivity for this sub-sector is proxied as the broader

‘Mining and quarrying n.e.c.’ sub-sector (2017 estimate).

Digital – key points

• All sub-sectors display high rates of productivity.

• High employment concentration in high value Telecommunications sub-sector.

• Relatively lower levels of employment in other Digital sub-sectors.

32

Table 4.5. Digital main sub-sectors summary, 2018

Sub-sector SIC codes Tees Valley employment

% of England employment

UK productivity (£ p.a.)

Telecommunications** 61 2,500 1.3% £148,000

Computer consultancy activities 62.02 2,600 0.6% £90,000

Computer and peripherals repair 95.11 100 0.5% £79,000

Other IT and computer services 62.09 500 0.4% £101,000

Computer programming activities 62.01 600 0.3% £95,000

Data processing, web portals & related 63.1 100 0.2% £131,000

Digital sector 6,500 0.6% £114,000* Source: ONS, ABS. EMSI. Note: * Tees Valley employment adjusted average productivity of sub-sectors listed. ** Local

Contact/Call Centres – technically part of Professional & Business Services (PBS) – are often officially recorded under the

parent company’s Telecommunications SIC code. This tendency acts to over-report local level Digital sector employment

and under-report local level PBS employment.

The four medium/high productivity sectors are:

Bioscience – key points

• Reflecting SIC code issues, high productivity sectors such as Pharmaceuticals are not

effectively identified within Tees Valley.

• Significant representation of high productivity Chemical and Process sub-sectors support the

overall medium/high productivity rate for the sector.

Table 4.6. Bioscience main sub-sectors summary, 2018

Sub-sector SIC codes Tees Valley employment

% of England employment

UK productivity (£ p.a.)

Manufacture of industrial gases, organic chemicals, nitrogen compounds and primary plastics

20.11, 20.14, 20.15, 20.16

2,100

10.1% £118,000 a

Manufacture of other food products n.e.c.

10.89 800 2.7% £64,000

Research and experimental development on natural science and engineering

72.1 2,800 2.5% £30,000 b

Technical testing and analysis 71.2 700 1.4% £62,000

Manufacture of bread, fresh pastries and cakes

10.71 600 0.9% £31,000

Manufacture of beer 11.05 100 0.9% £84,000

Manufacture of plastic packaging 22.22 100 0.6% £52,000

Manufacture of pharmaceutical preparations

21.2 100 0.3% £224,000

Manufacture of soaps and detergents 20.4 100 0.2% £66,000

Bioscience 7,500 1.7% £66,000* Source: ONS, ABS. EMSI Note: * Tees Valley employment adjusted average productivity of sub-sectors listed. a Productivity

does not includes the unavailable SIC 20.11 Manufacture of industrial gases. b Productivity only available for broader SIC 72

Scientific R&D sub-sector.

Advanced Manufacturing – key points

• High employment concentration across the majority of sub-sectors.

• Most sub-sectors record Medium/High productivity rates.

33

Table 4.7. Advanced Manufacturing main sub-sectors summary, 2018

Sub-sector SIC codes

Tees Valley employment

% of England employment

UK productivity (£ p.a.)

Manufacture of iron, steel and piping 24.1, 24.2

1,100 5.7% £42,000 a

Manufacture of engines and turbines 28.11 800 4.8% £52,000

Research and experimental development on natural science and engineering

72.1 2,800 2.5% £30,000 b

Manufacture of electric motors, cables and electronics

27.11, 27.32

400 2.2% £74,000 c

Manufacture of specialist machinery 28.9 600 1.9% £76,000

Engineering consultancy services 71.12 4,700 1.6% £73,000

Manufacture of motor vehicle parts 29.32 800 1.6% £59,000

Machining, metals treatment, metal structures, wire products and tools manufacture

25 4,100 1.5% £52,000

Technical testing and analysis 71.2 700 1.4% £62,000

Manufacture of instruments and appliances for measuring and testing

26.51 400 0.9% £81,000

Other professional, scientific and technical activities n.e.c.

74.9 800 0.8% £57,000

Manufacture of aircraft, spacecraft and related machinery

30.3 500 0.7% £42,000

Advanced Manufacturing 17,800 1.5% £56,000* Source: ONS, ABS. EMSI. * Tees Valley employment adjusted average productivity of sub-sectors listed. a Productivity only

available for SIC 24.1 Manufacture of basic iron and steel. b Productivity only available for broader SIC 72 Scientific R&D

sub-sector. c Productivity only available for SIC 27.11 Manufacture of electric motors.

Construction – key points

• Overall a broadly average employment concentration than nationally but with a high

concentration in the Demolition and site preparation sub-sector and a relatively low

concentration in the construction installation and completion of buildings sub-sectors.

• Construction is a medium/high productivity sector with the majority of its sub-sectors within

or close to this productivity range. However, with self-employment rates in the sector

approaching 50%, there may be some under-reporting of total employment and therefore

over-stating of productivity level.

Table 4.8. Construction main sub-sectors summary, 2018

Sub-sector SIC codes

Tees Valley employment

% of England employment

UK productivity (£ p.a.)

Demolition and site preparation 43.1 500 2.8% £69,000

Construction of roads and motorways 42.11 700 1.5% £63,000

Construction of other civil engineering projects

42.9 1,600 1.4% £68,000

Construction of buildings 41 4,600 1.2% £96,000

Roofing, scaffolding and other specialised construction activities

43.9 1,600 1.2% £61,000