technical strategies - the technical analyst · technical strategies quarter in brief: core asset...

TRANSCRIPT

TECHNICAL STRATEGIES QUARTER IN BRIEF: CORE ASSET ALLOCATION REVIEW Q3 // 2014

EOGHAN LEAHY, CMT, MSTA

MAURIZIO PIETRINI, MSTA

GUIDO RIOLO, MSTA

OLIVER WOOLF, CAIA, CMT, MSTA

PAUL CIANA, CMT

GREG BENDER, CMT

<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<<

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

2

Bloomberg BRIEF: Technical

Strategies Quarter in Brief

Contributors

Eoghan Leahy, CMT, MSTA

Ph: +44-20-7392-0599

Maurizio Pietrini, MSTA

Ph: +44-20-7073-3666

Guido Riolo, MSTA

Ph: +44-20-7330-7211

Oliver Woolf, CAIA, MSTA

Ph: +44-20-7073-3148

Paul Ciana, CMT

Ph: +1-212-617-8229

Greg Bender, CMT

Ph: +1-646-324-3169

“Implied volatility across markets registers multi-year lows

hitting levels not seen since before the Global Financial Crisis.”

CONTENTS

1. ABSTRACT AND CONTENTS Eoghan Leahy, Oliver Woolf, Gudio Riolo

2. GLOBAL MARKET OVERVIEW Eoghan Leahy, Oliver Woolf, Gudio Riolo, Greg

Bender, Maurizio Pietrini

3. GLOBAL EQUITY MARKETS

Eoghan Leahy, Oliver Woolf, Paul Ciana

4. RATES AND FX

Oliver Woolf

1. COMMODITIES

Oliver Woolf

6. BRIEF MARKET SPOTLIGHT

Guido Riolo

7. BLOOMBERG SENTIMENT SURVEY

Guido Riolo, Jennifer Warren

8. STRATEGIES IN BRIEF

Oliver Woolf, Maurizio Pietrini

9. EXPERT BRIEFING

Lex Van Dam

10. APPENDIX AND DISCLAIMER

ABSTRACT The high correlation and extreme low volatility across asset classes continues as the implied volatility

across markets registers multi-year lows hitting levels not seen since before the Global Financial

Crisis. US and European CDS continue to fall with the spread between the two now virtually zero.

Meanwhile rate increases have been sharper in Europe over the quarter. Sterling remains strong

versus the US Dollar while the Euro has pulled back significantly from its 52 week highs.

Equity markets continue to push higher although the Euro Stoxx is starting to show short term signs of

weakness. There seems to be a shift in the emerging market space with BRICs starting to look

relatively more attractive as investors rotate out of peripheral European indices which have been

strong for several quarters. Russia and India have performed very well over the last quarter.

Meanwhile Dubai and Saudi Arabia look to be recovering from a sharp yet healthy correction.

The commodity space is interesting with several markets such as copper, gold and silver testing long

term resistance levels. There appears to be a rotation out of agricultural commodities such as wheat,

corn and cotton into industrial metals like nickel, copper and silver which have been significant

relative underperformers.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW EQUITIES 3

1. Blue/red signals from Volstall indicator 2. Painted bars from triple moving average crossover 3. Lower panel is Fisher Transform with Squeeze

Chart 2

Chart 3 Chart 4

S&P continues to drive higher however the recent Volstall signal and Fisher

Transform divergence suggest waning momentum in the near term. The uptrend continues, TEMA is still bullish however there is a Volstall

exhaustion signal. Fisher still bullish.

TEMA remains bullish as the Euro Stoxx continues to drive higher.

Fisher starting to mean revert suggesting weakening momentum. Daily Euro Stoxx 600 looking negative. TEMA has turned bearish

following a recent Volstall signal. Potential rising wedge pattern.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW FIXED INCOME 4

1. Blue/red signals from Volstall indicator 2. Painted bars from triple moving average crossover 3. Lower panel is Fisher Transform with Squeeze

Chart 1 Chart 2

Chart 3 Chart 4

Downtrend channel has been broken by strong recent move higher that

saw a very extreme Fisher reading of 7.5. However Fisher mean

reversal highlights loss of momentum.

Daily TEMA negative also as the US 10 year continues to trade between

122 and 127. Volstall marking reversals nicely. US 10 Year continues to trade in a tight consolidation range. TEMA

remains negative and uptrend support has been broken.

More bullish outlook in Europe as weekly trend is up as confirmed by

TEMA. However Fisher mean reversion suggests waning upside

momentum.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW FX 5

1. Blue/red signals from Volstall indicator 2. Painted bars from triple moving average crossover 3. Lower panel is Fisher Transform with Squeeze

Euro failed dramatically at the key psychological 1.40 level. TEMA is

now negative following a Squeeze signal. Break of uptrend support

would likely result in a sharp move lower.

GBP continues to surge higher. TEMA remains positive and Fisher

continues to stay at elevated levels. No signs of weakness yet on

weekly indicators.

Daily chart of GBP is showing some early exhaustion signals, there is a

Volstall exhaustion signal but given the strong weekly signals this is less

significant. TEMA remains bullish and uptrend is intact.

Chart 1 Chart 2

Chart 3 Chart 4

Weekly Squeeze signal fired short as Euro has reversed lower. TEMA

has now turned negative and the uptrend support is currently being

tested.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW COMMODITIES 6

1. Blue/red signals from Volstall indicator 2. Painted bars from triple moving average crossover 3. Lower panel is Fisher Transform with Squeeze

TEMA remains bullish despite recent pullback. Should uptrend

support hold then retest of 2013 highs looks likely. Support around

psychologically significant $100 level will be key.

Having found support at the key 300 level, Copper is now driving

higher to test its long term downtrend. TEMA is positive and Fisher is

increasing in support of the move.

Chart 1 Chart 2

Chart 3 Chart 4

Daily chart of Crude is more bearish. TEMA is negative following Volstall

signal at recent high. Fisher now negative. Confluence of uptrend and

horizontal support around $100 mark likely to provide some support.

Daily TEMA is also bullish and extreme Fisher reading supports

strength of the recent move but is starting to mean revert. Volstall

signal right at downtrend suggests resistance may hold. Key level.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW PRECIOUS METALS 7

1. Blue/red signals from Volstall indicator 2. Painted bars from triple moving average crossover 3. Lower panel is Fisher Transform with Squeeze

Multiple Volstall signals at horizontal support marked the lows. Strong

move higher has broken downtrend but like Gold we have a negative

Volstall signals and potential flag. Perhaps a pause before a surge higher.

Chart 1 Chart 2

Chart 3 Chart 4

Gold starting to look more positive. TEMA has turned bullish, Fisher

has turned positive and the price is once again trading above the

prior downtrend resistance which now looks to be offering support.

Recent blue Volstall signal may mark the right shoulder of an inverse head

and shoulders pattern. However upside momentum has stalled as signalled

by red Volstall indicator. Potential near term bullish flag continuation pattern.

Silver finally looks to be mirroring the strength of Gold which is

bullish for both markets. TEMA is now positive and long term

downtrend is broken.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW VOLATILITY 8

4. Volatility bands

Chart 1 Chart 2

Chart 3 Chart 4

The S&P 500 gained nearly 4% in Q2 and the VIX fell to its lowest

levels since 2007. The 12 level was considered the floor for volatility –

the new floor may be closer to 10.

Implied volatility of Treasury options continued to trend lower in Q2. The

spikes in early April and June were quickly retraced by lower lows. The

MOVE finished Q2 by tagging the -3SD Bollinger Band – the lowest reading

since May 2013.

Currency volatility was under its 60 day moving average every day of

Q2. An all-time low was reached on June 19th.

The implied volatility of the United States Oil Fund ETF made another all-

time low in early June but quickly rebounded to tag the +1SD Bollinger

Band. Bandwidth (distance between bands) has reverted to more normal

levels as some volatility has returned to volatility.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW VOLATILITY 9

4. Volatility bands

Comments…

Conclusions

Chart 1

Chart 3

Gold volatility continued to trend lower in Q2, tagging the -3SD band

multiple times. Like crude oil, bandwidth is slowly starting to widen.

Below is a normalized chart of the past quarter of the relative

implied volatility of all five asset classed covered in this

section.

The theme for Q2 has been quiet markets with low volatility

and low volumes. After a brief correction in April, the S&P 500

has established a strong bullish trend. The widely followed

VIX, which has a strong negative correlation to equity prices,

has drifted lower.

Treasuries and currency markets have been largely range

bound and in tight ranges following benchmark U.S. interest

rates.

Commodities have slowly started to diverge and show some

volatility relative to equities. But historically volatility is still low

on an absolute basis.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW ASSET CLASS TRENDS 10

Virtually every market across the asset classes covered in the Quarterly has been up over the past two quarters. The two

exceptions are copper which is reversing up and the euro which is reversing down. The risk on phase continues and the

extreme levels of correlation between markets remains. Bonds continue to advance despite the strong gains seen in equity

markets. These intermarket relationships are slightly unexpected and unlikely to last forever.

5. World Trends Graph

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

OVERVIEW ASSET CLASS TRENDS 11

The weekly Relative Rotation Graph (RRG <GO>) highlights some interesting divergent relationships between securities within the

same asset classes. The Euro has been very weak and is now in the lagging quadrant, however Sterling remains strong and is still

leading. Both the US 10 year and the Bund are leading with equities which is interesting. There is also a recent divergence in relative

price and momentum between the S&P and the Euro stoxx which may be driven by the weaker Euro. Meanwhile we have Oil

consolidating within the leading zone while copper is improving, Finally, both Gold and Silver are improving together however for the

first time in months Silver has been improving relative to Gold which may be bullish for both precious metals.

6. Relative Rotation GraphsTM

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

GLOBAL EQUITY MARKETS 12

6. Relative Rotation GraphsTM

There have been some interesting rotations taking place over the last quarter in the emerging market space. Dubai has seen a

sharp sell offs which can be expected following the huge move it has enjoyed following the classification upgrade from frontier

status. European peripheral markets have been relatively weak with Portugal, Ireland, Greece in the lagging quadrant with Spain

and Italy weakening too. The BRICs are showing some relative strength with Russia in particular looking interesting as the

INDEXCF is poised to move into the outperform quadrant having been a strong relative laggard just a few weeks ago.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

GLOBAL EQUITY MARKETS 13

7. Scatter plot chart

The Scatter chart shows 3 month price performance (X axis) versus 1 year price performance (Y axis). The market colours show

the level of volatility as depicted by the Bollinger %B which refers to the distance between the upper and lower Bollinger bands;

wider bands give higher values and suggest more volatile markets. Finally the marker size represents 60 day volatility. Last quarter

we highlighted the performance persistence amongst the indices as they were displaying a positive regression between the

quarterly and annual performance. This relationship has broken down this quarter as we have seen the fortunes of several markets

reverse. The two strongest performers the MERVAL (extreme currency devaluation) and the DFMGI have also been the most

volatile. The DFMGI has pulled back over the last quarter but has still been an incredible performer over 12 months and is

showing sings of recovery (see the market breadth section). The recent underperformance of the European peripherals is clear.

While, the Russian INDEXCF and Indian SENSEX have performed well over the quarter.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

GLOBAL EQUITY MARKETS BREADTH 14

8. Market breadth indicators

Above is a Scatter Plot Chart (GS <GO>) of global equity markets with several Bloomberg market breadth fields applied. We

compare the 3 month price performance (Y axis) to the percentage of shares above 50 day moving averages (X axis), the market

colour denotes the percentage of stocks in each index with RSI above 70 while the marker size shows a relative value of the

percentage of securities that have given MACD buy signals over the past 10 days. The stand out performers have been Russia and

India, both had the biggest price gains over the quarter and highest percent of members above the 50 day moving average. The

majority or indices have shown moderate gains without extreme readings on RSI breadth or percent above 50 day MAs. The

peripheral European stocks have been weak and are clustering around the lower left corner of the scatter chart. Both the Dubai and

Saudi indices have sold off sharply but are showing signs of recovery as they are registering the largest percentage of MACD buy

signals in the last 10 days, which can be visualised by the larger size of their markers.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

15

8. Market breadth indicators

Analysing Russia and Dubai in more detail highlights how the market breadth tools can be used to spot turning points. The Russian

Micex formed an inverse head and shoulder pattern that was met with an extreme low reading on the percent of stocks above 50 day

SMA and then a huge spike on the percentage of MACD buy signals. The index is not testing resistance with an extreme reading on

the percent above the 50 day SMA and potentially some bearish divergence on the percent of members overbought on RSI. There is

a similar setup in the Dubai DFMGI as the percent of MACD buy signals is above 80 while the percentage of stocks above the 50 day

SMA is sub 10 which is an extreme low reading. This may signal a significant low has been established.

GLOBAL EQUITY MARKETS BREADTH

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

16

8. Market breadth indicators

GLOBAL EQUITY MARKETS BREADTH

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

RATES & FX 17

The top right chart demonstrates that interest rate increases have been sharper in the Eurozone over the last quarter, with the

shorter end of the US curve seeing marginal decreases. However, the anticipated rise in rates over the coming year from the

implied curves (US bottom left, EU bottom right) is less aggressive than 1 quarter ago when the 1 year forward implied rates

for the 10 year tenor were around 3.25 and 2.25 for the US and EU respectively (now c. 3.07 and 1.70).

9. Implied forward curves 10. Historical curves

The benchmark US (black) and European (orange) CDS

indices continue to fall and the spread between the two

(lower panel) is now virtually zero.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

RATES & FX 18

The Market Picture diagram above highlights levels that have been particularly actively traded for DXY Index over the past 6

months. Here each letter represents a day of the month starting with A for 1st (as opposed to its customary use where each

letter represents an intraday interval, usually 30 minutes). The histogram on the left is an overlay of all 6 months in the chart.

Last quarter (looking 6 months back) the overlay identified 80.6 as the most traded level and subsequently this became

resistance in both April and May. Although this level broke on the upside in the first days of June in then failed at its monthly

price projection, marked by the dashed black line (high + |mid-point - POC| * 2), and retreated to the middle of May’s value area

(70% of activity denoted by the horizontal blue lines). The range bound nature of the DXY over recent times is reflected by the

normal distribution of the overlay on the left, the apex of which, marked by the horizontal red line, is circa 80.2. This is the level

at which the DXY seems to have found acceptance currently.

11. Market Picture

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

FX & RATES 19

In line with recent GBP performance the CFTC net large speculator

position is the most positive it has been since 2007 (bottom panel)

and the 25D Risk Reversal has risen accordingly. In contrast the

net speculator position for EUR (top panel) is the most negative it

has been for over a year. However, the falling EUR is contradicted

by its 25D Risk Reversal which has been rising of late.

The analyst consensus for the end of Q3 is over 2 big figures lower

than the forward for EUR (top) and over 1.5 lower for GBP (bottom ).

Both implied probability bell curves are fairly normally distributed. In

the case of the EUR the curve is slightly translated to the right which

would could have mildly positive connotations

12. Sentiment and positioning 13. Implied probability forecast

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

RATES & FX 20

2. SEK is the only currency to have a positive implied – realized

spread (3m) despite being the only one to have seen an increase in

realized volatility in over the last quarter (albeit marginal).

14. World Currency Ranker 15. Correlation Matrix

1. Despite having the worst spot returns amongst the G10 group over

the last 3 months SEK and NOK are forecast to be the major

outperformers for the remainder of the year.

3. Of the countries that have USD denominated CDSs, AUD and

NZD, which have also had positive spot returns, have seen the

greatest drop in CDS levels. Only CHF has experienced a CDS rise.

4. Correlations vs. USD

Strongest positive – EUR & DKK

Strongest negative – N/A

Weakest – AUD & CHF

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

21

The Relative Rotation Graph (RRG<GO>) depicts a significant change in the fortune of different commodity groups over the

last quarter (source is the new BCOM Index, formally the DJ-UBS Index). Whereas in April the agricultural commodities looked

as though they were beginning to outperform they have since seen a significant downturn in relative fortunes, wheat, corn and

cotton being amongst the laggards. On the other hand, the industrial metals, which were the major underperformers previously,

are increasingly exhibiting strength. Despite a drop in momentum, nickel is the leading performer, whilst copper, silver,

aluminium and zinc are all showing signs of improvement.

NG1 Nat Gas

BO1 Soybean Oil

LC1 Live Cattle

CO1 Brent Crude

HO1 Heating Oil

C 1 Corn

S 1 Soybean Oil

LH1 Lean Hogs

LMNIDS03 Nickel

XB1 Gasoline

SM1 Soybean Meal

GC1 Gold

SI1 Silver

KW1 Winter Wheat

HG1 Copper

LMAHDS03 Aluminium

CL1 WTI Crude

W 1 Wheat

CT1 Cotton

SB1 Sugar

LMZSDS03 Zinc

KC1 Coffee

6. Relative Rotation GraphsTM 16. BCOM Index

COMMODITIES BCOM INDEX

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

COMMODITIES BCOM INDEX 22

The scatter plot from GS<GO> shows the 3 month percent change on the X axis versus the 60 day rate of change of aggregate

open interest on the Y axis for the constituents of Bloomberg’s new BCOM Index (formerly DJ-UBS). Last month the huge open

interest hike anticipated the outbreak of a large upward move for nickel. This time round it is heating oil, followed by gasoline and

gold which have the larges rates of change in open interest. The colour scheme and sphere size represent the Bollinger %B

(position within the bands) and 60 day realized volatility respectively. In this light zinc is moving particularly strongly whilst nickel

and coffee (large blue sphere) - both of which were shown to have lost some momentum in the Relative Rotation Graph – are the

most volatile.

NG1 Nat Gas

BO1 Soybean Oil

LC1 Live Cattle

CO1 Brent Crude

HO1 Heating Oil

C 1 Corn

S 1 Soybean Oil

LH1 Lean Hogs

LMNIDS03 Nickel

XB1 Gasoline

SM1 Soybean Meal

GC1 Gold

SI1 Silver

KW1 Winter Wheat

HG1 Copper

LMAHDS03 Aluminium

CL1 WTI Crude

W 1 Wheat

CT1 Cotton

SB1 Sugar

LMZSDS03 Zinc

KC1 Coffee

6. Relative Rotation GraphsTM 16. BCOM Index

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

23

In the first week of July the VIX has reached a low of 10.28,

a level not seen since February 2007. While most people

would agree that this level of volatility is unusual and

unsustainable, timing the upward reversal could be a tricky

affair without the appropriate tools.

One toolkit often associated with market timing are the

DeMark Studies, developed by Tom DeMark over a career

that spans over 40 decades. Of the many indicators

available we will focus on TD Sequential and TD Combo.

The purpose is not to teach calculation or interpretation, for

which we would suggest contacting DeMARK Analytics via

the Bloomberg function DEMA<GO>.

BRIEF MARKET SPOTLIGHT

The studies comprise two phases: the first one,

identical on both, is called TD Setup, it is numbered in

green and it is momentum based; the second phase,

TD Countdown, is the more directional phase and it is

normally in red and magenta respectively. However,

for the purpose of this publication Combo countdown

will be in blue instead. A setup 9 tends to indicate an

increased chance of a correction, a countdown 13

indicates the current trend is vulnerable.

The daily chart of the VIX (above) shows a sequential

13 formed back in December and a combo 13 in May,

with the recent lows showing a disqualified breakout to

the downside, one that is more likely to fail than

succeed. The weekly chart (left) shows a sequential

13 from April 2013 and a setup 9 from last May.

Overall the signals on the VIX suggest a potential

base is forming.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

24 If instead of using the VIX Index which does not actually

trade, we will now concentrate on the traded future on

the VIX. The future contract used is the continuation UX1

Index. As this is a traded instrument it should better

capture and reflect the psychology of market

participants. Generating clearer trading signals.

On the daily chart (top right) a quick visual examination

seems to confirm this assumption. The reversal last

summer was heralded by a combo 13,confirmed a

couple of months later by setup 9. The subsequent rally

came to an abrupt end on a sell setup 9. The next 3

turning points, in November, February and April were

also identified.

More advanced DeMark users will also appreciate the

finer points, such as the touching of the Risk line one

year ago and again at the turn of the year. Also, the

rejection of the TDST level last October before breaking

the level in February as well as the pull back on the

previous support TDST, which had turned into a

resistance, this June.

If we look at the current developments on the daily chart

(bottom right) , the sequential completed a 13 on the 9th

of June; whereas combo, in blue, completed its 13 on the

19th of June. Suggesting a potential exhaustion of

downside momentum provided the TDST risk levels

hold.

The risk level for the first signal, at 12.70, has been

challenged many times since it’s completion, but the

breakout was never qualified and therefore never

suggested an increased chance of continuation on the

down side. The risk line for combo came at 12.10 and

has not been tested at the time of going to press.

BRIEF MARKET SPOTLIGHT

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

25 BRIEF MARKET SPOTLIGHT By using the futures contract instead of the VIX, we also get interesting readings on the weekly and monthly timeframes. The weekly

chart (below left) shows a combo 9-13-9 formation, which often signals exhaustion after an extended move suggesting a larger counter

trend move may be at hand. There is also a second 13 at the beginning of June 2014 which confirms the potential reversal scenario.

There is also a sequential 13 from the end of March whose Risk line has been touched last week by the setup 9 bar.

The monthly chart (bottom right) also shows a sequential 13 two months ago in May 2014, however combo currently on 11 might

require another two months to complete the count. These signals suggest a reversal could take place imminently but may need a few

more months before the combo signal will confirm the 13 on the sequential.

Having analysed both the VIX and the VIX future (UX1) using the DeMark indicators across several timeframes it looks like a base is

being formed,. The daily charts are potentially displaying all the hallmarks of an imminent change of trend. However, we should not

underestimate the lack of completion on the monthly combo which may take two or more months to complete the 13 count, suggesting

a potential lower low may be seen before a reversal higher.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

26

On December 17th, 2013, Bloomberg hosted the first Annual Technical Analysis Summit, in the London headquarters. During the

course of the event we disseminated a questionnaire on views of the financial world for the quarter to come. As we go forward, we

would like to ask you again about your views. Results will be available on the Bloomberg Quarterly Brief, which can be downloaded

for free under the function BRIEF<GO>. If you are interested in taking part, please contact a member of the team listed on the front

cover of this publication.

The questionnaire was broken down by assets and regions, with 6 of each. In detail we asked: Risk (on or off), and then up or

down for the S&P500, oil, gold, dollar index and 10 year rates, without specifying the currency, leaving people to decide what was

the most important rate in their mind. We then asked which regions were going to be most appealing in the next quarter: US,

Europe, Japan, BRICs, Emerging markets and Frontier markets.

In total we got 96 answers, from a universe

selected without any statistical filter.

The first picture is a breakdown of the view of the

markets. The highest conviction was on bullish

oil, with around 65%, up from 45%. During the

same time, Nymex oil was largely unchanged,

but with a 10% swing low to high. Risk-on and

Gold up were both selected by 56-57% of

respondents, 3 points up and 3 points down

respectively from the previous quarter. The price

of gold dropped almost 2% since the previous

survey, with a 10% swing, high to low.

The percentage of bulls on dollar and rates, both

around 55%, came down from 73% and 65%

respectively. The dollar barely changed, whereas

US 10yr rates dropped 1.8% or 6bp. S&P views

remain very balanced, with the narrow bullish

lead seen 3 months ago switching now to the

bearish side, with downward pressure now

expected by 52% vs 48% 3 months ago. Of the

assets under observation, the S&P500 was the

one with the best performance since the last

survey, with a +6.91% at time of going to press.

BLOOMBERG QUARTER IN BRIEF (QIB) SENTIMENT SURVEY

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

27

The main story in the geographic

breakdown was that Europe recovered

second place behind the US. Europe

rose from 25% 3 months ago to 36.7%,

just 1 point behind the US. Emerging

markets stayed stable within the views

of our respondents, going from 26% to

27.5%.

Japan’s chances of outperformance

also improved markedly, almost

doubling from 10% to a shade less

than 20%.

BRIC countries prove difficult to

predict, going back to around 6% of

preferences, where it was in January,

before popping up to around 12% last

quarter.

Obviously the sum is not meant to be

100, as multiple selections were

allowed

Among dollar bulls, once more Japan showed an improved appeal, the only country to increase the preferences among

respondents who saw the dollar index up. Japan went from 9% to 19% by stealing 5 points from the US, 1 point from Europe, 4

points from BRICs. Emerging Markets and Frontier Markets were unchanged at 22% and 3% respectively.

Among rates bulls again the big story was the recovery in expectations for Europe and Japan, at the expense of the US (down

from 38% to 27%) and BRICs, down to just 1%. Emerging markets remained substantially unchanged, moving from 25% to 24%,

but crucially moved to 3rd place, behind the US and Europe

See charts overleaf

BLOOMBERG QUARTER IN BRIEF (QIB) SENTIMENT SURVEY

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

28

Dollar Up Rates Up

Risk On Risk Off

The next level of analysis was done by qualifying the regional choice based on the views on risk and, displayed on below. Among

risk-on respondents, 35% saw Europe as their main performance area. An interesting, if counterintuitive, detail that transpired is that

there are more Risk-off respondents expecting Emerging Markets to do well (23%, 2nd position) than there are Risk-on with the same

view (19%). Risk off-Japan bulls increased from 7% last quarter to an impressive 19%, pushing Europe in 4th place with 17%

BLOOMBERG QUARTER IN BRIEF (QIB) SENTIMENT SURVEY

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

STRATEGY IN BRIEF 29

True Strength Index (Double Momentum)

The True Strength Index (TSI) was created by William Blau and introduced in Stocks and Commodities magazine. It is an

oscillator calculated as the ratio of a double smoothed 1 day net change divided by a double smoothed 1 day absolute

change. An exponential average is then applied to the ratio in a similar fashion to the MACD indicator.

The formula which can be replicated via .Lite in

STDY<GO> is:

Double Smoothed PC

PC = C - C>>1;

FS = EMAvg(PC, 23);

SS = EMAvg(FS, 13);

Double Smoothed Absolute PC

absPC = Abs(PC);

aFS = EMAvg(absPC, 25);

aSS = EMAvg(aFS, 13);

TSI

TSI = 100 * (SS / SSa);

Signal

Signal = EMAvg(TSI, signal);

As seen in the chart below, the double exponential

smoothing technique of the TSI (middle panel) results in

a very similar output to the MACD (lower panel).

However, a key benefit of the TSI is that it is scaled,

thus making it easier to identify extreme (perhaps

overbought / oversold) levels, and also to draw

comparisons across different securities.

17. Strategy creation and backtesting

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

STRATEGY IN BRIEF 30

The TSI Double Momentum strategy is as follows: as a trend filter, only longs can be taken when TSI is greater than 0 and

only shorts when TSI is less than 0. The entry and exit points are then generated by the crossovers between the TSI and its

Signal line. As it is a medium to long term trend following strategy a weekly periodicity is employed.

The chart of the S&P 500, below, is colour coded to depict where the trades would occur – the blue bars represent the long

trades and the red the short.

Although this strategy could be easily replicated with the MACD, the benefits of the TSI are obvious from an observational

perspective. For example, the TSI resistance at the overbought level twice marked exhaustion in 2012, whilst the

subsequent support at the same level in 2013 and 2014 highlighted trend strength.

17. Strategy creation and backtesting

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

STRATEGY IN BRIEF 31

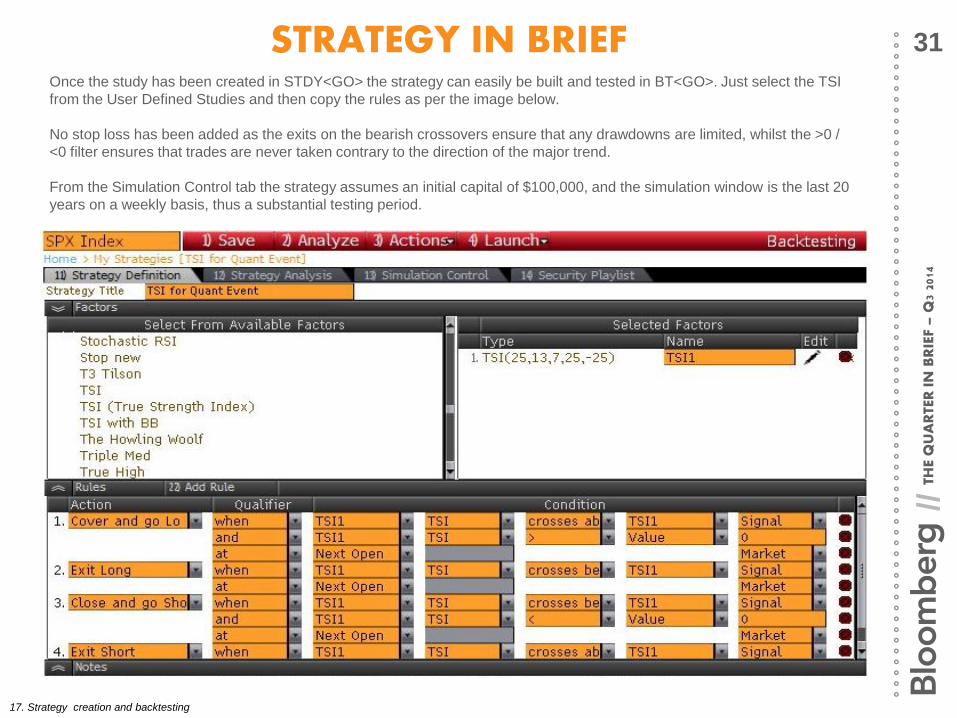

Once the study has been created in STDY<GO> the strategy can easily be built and tested in BT<GO>. Just select the TSI

from the User Defined Studies and then copy the rules as per the image below.

No stop loss has been added as the exits on the bearish crossovers ensure that any drawdowns are limited, whilst the >0 /

<0 filter ensures that trades are never taken contrary to the direction of the major trend.

From the Simulation Control tab the strategy assumes an initial capital of $100,000, and the simulation window is the last 20

years on a weekly basis, thus a substantial testing period.

17. Strategy creation and backtesting

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

STRATEGY IN BRIEF 32

The results below demonstrate that the strategy produces steady gains over time.

Although out of 39 trades over the 20 years there are marginally more losing than winning trades, the average winner is just

over twice the average user and, most importantly, the strategy substantially limits the drawdowns. The greatest loss over

the period is reduced to 26.41% in contrast to drops of over over 50% in the S&P over the same interval.

17. Strategy creation and backtesting

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

STRATEGY IN BRIEF 33

However the real benefit of the strategy becomes apparent when it is diversified over a basket of indices.

The chart below is the cumulative profit with an initial $100,000 investment in all the 18 major global equity benchmarks from

the front page of WEI<GO>.

What is extremely impressive is not only the consistency of the gains but also the smoothness of the equity curve.

17. Strategy creation and backtesting

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

EXPERT BRIEFING 34 Lex Van Dam is a Dutch hedge fund

manager based in London. In his 20+

career he has worked at Goldman

Sachs, GLG and is currently at

Hampstead Capital.

In 2009 he featured in the BBC2

programme "Million Dollar Traders"

where eight ordinary people were given

the training and capital to trade the

stock market. In November 2010 Lex has

launched the "Lex Van Dam Trading

Academy“ - www.lexvandam.com

How would you describe who you are

and what you do?

I have been trading and investing for a

living since 1992, and currently I am a

partner in a hedge fund, which also has an

excellent long only strategy. Aside from

that, I also run an online trading academy,

teaching other people how to trade and

invest in stocks and currencies.

What attracted you to the financial

markets?

I love the financial markets because they

are continuously moving so it is always

intellectually stimulating to be involved with

them, and because you are only ever as

good as your last trade, you need to keep

reinventing yourself and develop new skills.

Please describe your approach to

understanding the markets, do you use

technical analysis, fundamental analysis

or both, please explain why?

As a common thread in my trading and

investing I use a process called 5-Step-

Trading® which makes sure I don’t listen to

rumours or copy other traders, but instead I

focus on coming up with my own original

ideas, which helps me avoid consensus

positions. Also, the fact that I understand

the stocks I invest in helps me decide when

a stock moves against me whether I should

cut or hold on, as I am much better able to

judge news flow. That would be much

harder if the original investment idea wasn’t

mine. 5-Step-Trading® uses both

fundamental as well as technical analysis,

so I use both.

What technical analysis techniques, if

any, do you favour?

When investing, it is super-important to be

able to interpret charts and patterns. They

tell you the story of a stock and point out

historical demand and supply patterns,

which is a pretty important driver when you

are trying to get a feel of what might

happen to a stock in the future. They help

me optimise my trade entry timing, and help

me set profit targets and stop losses. When

it comes to specific technical analysis I also

try to understand what drives other purely

technical traders, so when I look at, for

example, Japanese stocks or the Yen, I

would look at Ichimoku clouds, while for

Dutch stocks I would be more interested at

looking at Windmill patterns, which are

based on rotating matrixes. But the bottom

line remains that you first need to make a

judgement if a stock is ranging or trending.

Do you use automated systems or rely

on judgment?

We have a very strong process for stock

selection. It is our own proprietary tool

which ranks stocks based on their exposure

to a large range of fundamental drivers and

valuation metrics, and ends up giving us a

‘buy’ list of those stocks with attractive

fundamentals that are relatively cheap. Our

goal is to have a portfolio of stocks that we

are happy to hold even when the market

turns down. We are definitely not

momentum players. Basically we use

automation to screen for attractive names

but at the end of the day the decisions will

be made by human beings and not

computers.

What timeframes do you favour,

historical, intraday or a combination of

both?

It really depends on the timeframe of my

opinion: for trading, less than two weeks;

for investing, at least 3 to 6 months.

Do you use a trading system? If you do

what are the key statistics to consider

when evaluating one?

Yes, we do have a trading system in place

that is based on our proprietary tool, where

we look for buy entry points for the stocks

we like fundamentally, and for sell signals

for the stocks we don’t like. These triggers

can be trend reversals, but we also have

signals that look at a resumption of the

main trend when a stock has retraced. The

statistics we use to evaluate the

performance of our systems are mainly the

equity curve and the maximum drawdown.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

EXPERT BRIEFING 35

What is the least important aspect to

consider when building trading

systems?

Not sure what the least important aspect

is, but the most important aspect to

consider is the execution impact. As soon

as you start trading in any size high

frequency traders will front run you. The

first thing I always ask other portfolio

managers who suffer performance issues

is how they execute their trades and on

what venue. Often they have no idea and

that is exactly where the performance

issues arise as slippage can be huge. It

might not that much per individual trade,

but this can add up to a lot more than

people realise.

Do you employ portfolio management

and/or pyramiding techniques?

Of course. We aim to have a portfolio of

uncorrelated bets so that when one idea

goes against us we have plenty of other

that can make us some money. We do

scenario analysis and a key parameter is

of course the VAR of our portfolio. I don’t

normally average down, I want an idea to

work before adding to a position.

How important are drawdowns and

money management in your opinion?

Money management is key if you want to

build a business and survive in this

industry. It is about building up a track

record with low drawdowns and executing

what you set out to do, i.e. you need to

avoid style drift. Know your market, know

your investor.

What is your opinion/approach to

optimization?

I am an econometrician, so I do

understand mathematical equations, but it

is very easy to think that you are

optimising your process while in fact all

you have done is take on more risk, which

one day will end up really hurting you.

Understand your edge and your risk, and

then find the most efficient liquid way to

implement it.

What advice would you give to those

who are new to the financial markets

and want to become the next Tom Pelc?

Educate yourself as much as possible

about the markets, and realise that

winning traders don’t try to copy others,

but in fact have a great understanding of

themselves. Trading is a mental game,

which takes place between the ears.

Can we have the name of someone who

has impressed you during your career?

Fischer Black, the Nobel laureate. He told

me that he had run the performance

numbers on a very famous risk arbitrage

desk at a large investment bank, and

found that a passive risk arbitrage strategy

would have outperformed them. It taught

me that asset allocation is the ultimate

driver of returns and that there is a lot of

smoke and mirrors in this field.

Is there anything you would do

differently, if you were given a chance?

In this life nothing, but if possible in my

next life I would like to come back as a

bull. There must be something amazing

about being able to always be optimistic

about the future, despite the facts on the

ground.

Is the future all into algo trading and

automated systems or does human

intuition still have a role?

It depends on the regulator and the

exchanges and the end clients. There are

still too many fish in the pond serving as

food for the sharks. If it was automated

systems trading just against other

automated systems then it would end very

soon. But as long as many institutions

don’t understand that they de facto are the

raison d’etre for the automated systems,

and the exchanges profit from this, then

they will continue to exist.

THE

QU

AR

TER

IN

BR

IEF –

Q3

2014

//

APPENDIX 36

1. The red and blue signals in the Overview section are an indicator called Volstall. It is our own indicator created in STDY<GO>. It uses the rate of change of

the moving standard deviation of price to identify possible reversal points through decreasing momentum. A guide to STDY<GO> as well as a forum can be

found within red toolbar in the function.

2. In the Overview section the bars are painted according to a triple exponential moving average crossover with averages of 4, 9 and 18. The blue and red

Volstall signals and painted bars are created in the strategy events. From a chart click on the events flag ,+Add Event, Browse then select option17)

Strategies & Studies.

3. The indicator below the charts in the Overview section is the Fisher Transform with Squeeze (Indicator outlined by John F. Carter) . The indicator uses a

Gaussian probability density function (Gaussian PDF) as opposed to a more traditional bell-shaped probability density function to calculate the position of

the price compared to its range (see TECH<GO>). Squeeze signals are shown as red bars and occur when the Bollinger bandwidth is less than the Keltner

band with signalling low directional volatility.

4. On the volatility charts we have used Bollinger bands with a 60 period moving average with upside deviations of 1, 2, and 3. On the downside we have used

1,1.5 and 2 standard deviations from the average, to reflect the inherent skew in volatility indices.

5. World Trend Graph can be found at WT<GO>

6. Relative Rotation GraphsTM can be found at RRG<GO>. Relative Rotation GraphsTM of Relative Rotation Graphs Limited. See

www.RelativeRotationGraph.com . Please see DOCS 2063266<GO> for more information.

7. The scatter plot chart can be found at GS<GO> and allows for the visualisation of 4 unique sets of data.

8. More information on Bloomberg’s Market Breadth indicators across 54 different markets can be found at DOCS 2068663<GO>

9. Implied forward curves can be charted in FWCM<GO>

10. Historical curves can be charted in GC<GO>

11. Market Picture can be found at MKTP<GO>. For more information on mechanics of Market Picture hit the HELP key from within the function.

12. Sentiment and positioning data can be located at IPSP<GO>

13. Implied probability FX forecasts are derived from FX options and can be found at FXFM<GO>

14. The World Currency Ranker can be found at WCRS<GO>

15. Correlation matrices can be created at CORR<GO>

16. The Commodities in this section are taken from the Bloomberg’s new BCOM Index, part of the Bloomberg Commodity Index Family, formerly known as the

DJ-UBS. With reference to the selection of the both the selection of the constituents and the calculation methodology, the design of the index embodies four

key principles: economic significance, diversification, continuity and liquidity. More information can be found at BCOM<GO>.

17. Use BT<GO> for the creation, backtesting and optimisation of strategies. It will integrate your own custom studies built in STDY<GO> and can also

generate alerts. A guide to BT<GO> as well as a forum can be found within red toolbar in the function.

OTHER RESOURCES

• CHART<GO> is the homepage for Bloomberg charts and technical analysis with links to a variety of functions and resources including documents on

Bloomberg’s own proprietary studies.

• ‘Getting Started With Bloomberg Charts’ at DOCS 2069346<GO> for an introduction to what is possible.

• ‘A Guide to Bloomberg Charts’ at DOCS 2065187<GO> for a more thorough walkthrough how to use our charting and technical analysis functionality.

DISCLAIMER - Read the full Bloomberg Tradebook disclaimer here: http://goo.gl/UewDb