tax system and procedure in usa, uk, india by simon (bubt)

TRANSCRIPT

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 1/165

1

Tax system and procedures are different in different countries, Here, the tax system and

procedure in USA, UK, India are described :

Tax system & procedure in the United States of America (USA)

Taxation in the United States is a complex system which may involve payment to many different levelsof government and many methods of taxation. United States taxation includes local government, possiblyincluding one or more of municipal, township, district and county governments. It also includes regionalentities such as school and utility, and transit districts as well as including state and federal government.

History

The federal, state, and local tax systems in the United States have been marked by significantchanges over the years in response to changing circumstances and changes in the role of government. The types of taxes collected, their relative proportions, and the magnitudes of the

revenues collected are all far different than they were 50 or 100 years ago. Some of thesechanges are traceable to specific historical events, such as a war or the passage of the 16thAmendment to the Constitution that granted the Congress the power to levy a tax on personalincome. Other changes were more gradual, responding to changes in society, in our economy,and in the roles and responsibilities that government has taken unto itself.

Colonial Times

For most of our nation's history, individual taxpayers rarely had any significant contact withFederal tax authorities as most of the Federal government's tax revenues were derived fromexcise taxes, tariffs, and customs duties. Before the Revolutionary War, the colonial government

had only a limited need for revenue, while each of the colonies had greater responsibilities andthus greater revenue needs, which they met with different types of taxes. For example, thesouthern colonies primarily taxed imports and exports, the middle colonies at times imposed aproperty tax and a "head" or poll tax levied on each adult male, and the New England coloniesraised revenue primarily through general real estate taxes, excises taxes, and taxes based onoccupation.

England's need for revenues to pay for its wars against France led it to impose a series of taxeson the American colonies. In 1765, the English Parliament passed the Stamp Act, which was thefirst tax imposed directly on the American colonies, and then Parliament imposed a tax on tea.Even though colonists were forced to pay these taxes, they lacked representation in the English

Parliament. This led to the rallying cry of the American Revolution that "taxation withoutrepresentation is tyranny" and established a persistent wariness regarding taxation as part of theAmerican culture.

The Post Revolutionary Era

The Articles of Confederation, adopted in 1781, reflected the American fear of a strong centralgovernment and so retained much of the political power in the States. The national government

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 2/165

2

had few responsibilities and no nationwide tax system, relying on donations from the States forits revenue. Under the Articles, each State was a sovereign entity and could levy tax as it pleased.

When the Constitution was adopted in 1789, the Founding Fathers recognized that nogovernment could function if it relied entirely on other governments for its resources, thus the

Federal Government was granted the authority to raise taxes. The Constitution endowed theCongress with the power to "…lay and collect taxes, duties, imposts, and excises, pay the Debtsand provide for the common Defense and general Welfare of the United States." Ever on guardagainst the power of the central government to eclipse that of the states, the collection of thetaxes was left as the responsibility of the State governments.

To pay the debts of the Revolutionary War, Congress levied excise taxes on distilled spirits,tobacco and snuff, refined sugar, carriages, property sold at auctions, and various legaldocuments. Even in the early days of the Republic, however, social purposes influenced whatwas taxed. For example, Pennsylvania imposed an excise tax on liquor sales partly "to restrainpersons in low circumstances from an immoderate use thereof." Additional support for such a

targeted tax came from property owners, who hoped thereby to keep their property tax rates low,providing an early example of the political tensions often underlying tax policy decisions.

Though social policies sometimes governed the course of tax policy even in the early days of theRepublic, the nature of these policies did not extend either to the collection of taxes so as toequalize incomes and wealth, or for the purpose of redistributing income or wealth. As ThomasJefferson once wrote regarding the "general Welfare" clause:

To take from one, because it is thought his own industry and that of his father has acquired toomuch, in order to spare to others who (or whose fathers) have not exercised equal industry andskill, is to violate arbitrarily the first principle of association, "to guarantee to everyone a free

exercise of his industry and the fruits acquired by it."

With the establishment of the new nation, the citizens of the various colonies now had properdemocratic representation, yet many Americans still opposed and resisted taxes they deemedunfair or improper. In 1794, a group of farmers in southwestern Pennsylvania physically opposedthe tax on whiskey, forcing President Washington to send Federal troops to suppress theWhiskey Rebellion, establishing the important precedent that the Federal government wasdetermined to enforce its revenue laws. The Whiskey Rebellion also confirmed, however, thatthe resistance to unfair or high taxes that led to the Declaration of Independence did notevaporate with the forming of a new, representative government.

During the confrontation with France in the late 1790's, the Federal Government imposed thefirst direct taxes on the owners of houses, land, slaves, and estates. These taxes are called directtaxes because they are a recurring tax paid directly by the taxpayer to the government based onthe value of the item that is the basis for the tax. The issue of direct taxes as opposed to indirecttaxes played a crucial role in the evolution of Federal tax policy in the following years. WhenThomas Jefferson was elected President in 1802, direct taxes were abolished and for the next 10years there were no internal revenue taxes other than excises.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 3/165

3

To raise money for the War of 1812, Congress imposed additional excise taxes, raised certaincustoms duties, and raised money by issuing Treasury notes. In 1817 Congress repealed thesetaxes, and for the next 44 years the Federal Government collected no internal revenue. Instead,the Government received most of its revenue from high customs duties and through the sale of public land.

The Civil War

When the Civil War erupted, the Congress passed the Revenue Act of 1861, which restoredearlier excises taxes and imposed a tax on personal incomes. The income tax was levied at 3percent on all incomes higher than $800 a year. This tax on personal income was a new directionfor a Federal tax system based mainly on excise taxes and customs duties. Certain inadequaciesof the income tax were quickly acknowledged by Congress and thus none was collected until thefollowing year.

By the spring of 1862 it was clear the war would not end quickly and with the Union's debt

growing at the rate of $2 million daily it was equally clear the Federal government would needadditional revenues. On July 1, 1862 the Congress passed new excise taxes on such items asplaying cards, gunpowder, feathers, telegrams, iron, leather, pianos, yachts, billiard tables, drugs,patent medicines, and whiskey. Many legal documents were also taxed and license fees werecollected for almost all professions and trades.

The 1862 law also made important reforms to the Federal income tax that presaged importantfeatures of the current tax. For example, a two-tiered rate structure was enacted, with taxableincomes up to $10,000 taxed at a 3 percent rate and higher incomes taxed at 5 percent. Astandard deduction of $600 was enacted and a variety of deductions were permitted for suchthings as rental housing, repairs, losses, and other taxes paid. In addition, to assure timely

collection, taxes were "withheld at the source" by employers.

The need for Federal revenue declined sharply after the war and most taxes were repealed. By1868, the main source of Government revenue derived from liquor and tobacco taxes. Theincome tax was abolished in 1872. From 1868 to 1913, almost 90 percent of all revenue wascollected from the remaining excises.

The 16th Amendment

Under the Constitution, Congress could impose direct taxes only if they were levied inproportion to each State's population. Thus, when a flat rate Federal income tax was enacted in1894, it was quickly challenged and in 1895 the U.S. Supreme Court ruled it unconstitutionalbecause it was a direct tax not apportioned according to the population of each state.

Lacking the revenue from an income tax and with all other forms of internal taxes facing stiff resistance, from 1896 until 1910 the Federal government relied heavily on high tariffs for itsrevenues. The War Revenue Act of 1899 sought to raise funds for the Spanish-American Warthrough the sale of bonds, taxes on recreational facilities used by workers, and doubled taxes on

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 4/165

4

beer and tobacco. A tax was even imposed on chewing gum. The Act expired in 1902, so thatFederal receipts fell from 1.7 percent of Gross Domestic Product to 1.3 percent.

While the War Revenue Act returned to traditional revenue sources following the SupremeCourt's 1895 ruling on the income tax, debate on alternative revenue sources remained lively.

The nation was becoming increasingly aware that high tariffs and excise taxes were not soundeconomic policy and often fell disproportionately on the less affluent. Proposals to reinstate theincome tax were introduced by Congressmen from agricultural areas whose constituents feared aFederal tax on property, especially on land, as a replacement for the excises.

Eventually, the income tax debate pitted southern and western Members of Congressrepresenting more agricultural and rural areas against the industrial northeast. The debateresulted in an agreement calling for a tax, called an excise tax, to be imposed on businessincome, and a Constitutional amendment to allow the Federal government to impose tax onindividuals' lawful incomes without regard to the population of each State.

By 1913, 36 States had ratified the 16th Amendment to the Constitution. In October, Congresspassed a new income tax law with rates beginning at 1 percent and rising to 7 percent fortaxpayers with income in excess of $500,000. Less than 1 percent of the population paid incometax at the time. Form 1040 was introduced as the standard tax reporting form and, thoughchanged in many ways over the years, remains in use today.

One of the problems with the new income tax law was how to define "lawful" income. Congressaddressed this problem by amending the law in 1916 by deleting the word "lawful" from thedefinition of income. As a result, all income became subject to tax, even if it was earned byillegal means. Several years later, the Supreme Court declared the Fifth Amendment could not beused by bootleggers and others who earned income through illegal activities to avoid paying

taxes. Consequently, many who broke various laws associated with illegal activities and wereable to escape justice for these crimes were incarcerated on tax evasion charges.

Prior to the enactment of the income tax, most citizens were able to pursue their privateeconomic affairs without the direct knowledge of the government. Individuals earned theirwages, businesses earned their profits, and wealth was accumulated and dispensed with little orno interaction with government entities. The income tax fundamentally changed this relationship,giving the government the right and the need to know about all manner of an individual orbusiness' economic life. Congress recognized the inherent invasiveness of the income tax into thetaxpayer's personal affairs and so in 1916 it provided citizens with some degree of protection byrequiring that information from tax returns be kept confidential.

World War I and the 1920's

The entry of the United States into World War I greatly increased the need for revenue andCongress responded by passing the 1916 Revenue Act. The 1916 Act raised the lowest tax ratefrom 1 percent to 2 percent and raised the top rate to 15 percent on taxpayers with incomes inexcess of $1.5 million. The 1916 Act also imposed taxes on estates and excess business profits.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 5/165

5

Driven by the war and largely funded by the new income tax, by 1917 the Federal budget wasalmost equal to the total budget for all the years between 1791 and 1916. Needing still more taxrevenue, the War Revenue Act of 1917 lowered exemptions and greatly increased tax rates. In1916, a taxpayer needed $1.5 million in taxable income to face a 15 percent rate. By 1917 ataxpayer with only $40,000 faced a 16 percent rate and the individual with $1.5 million faced a

tax rate of 67 percent.

Another revenue act was passed in 1918, which hiked tax rates once again, this time raising thebottom rate to 6 percent and the top rate to 77 percent. These changes increased revenue from$761 million in 1916 to $3.6 billion in 1918, which represented about 25 percent of GrossDomestic Product (GDP). Even in 1918, however, only 5 percent of the population paid incometaxes and yet the income tax funded one-third of the cost of the war.

The economy boomed during the 1920s and increasing revenues from the income tax followed.This allowed Congress to cut taxes five times, ultimately returning the bottom tax rate to 1percent and the top rate down to 25 percent and reducing the Federal tax burden as a share of

GDP to 13 percent. As tax rates and tax collections declined, the economy was strengthenedfurther.

In October of 1929 the stock market crash marked the beginning of the Great Depression. As theeconomy shrank, government receipts also fell. In 1932, the Federal government collected only$1.9 billion, compared to $6.6 billion in 1920. In the face of rising budget deficits which reached$2.7 billion in 1931, Congress followed the prevailing economic wisdom at the time and passedthe Tax Act of 1932 which dramatically increased tax rates once again. This was followed byanother tax increase in 1936 that further improved the government's finances while furtherweakening the economy. By 1936 the lowest tax rate had reached 4 percent and the top rate wasup to 79 percent. In 1939, Congress systematically codified the tax laws so that all subsequent

tax legislation until 1954 amended this basic code. The combination of a shrunken economy andthe repeated tax increases raised the Federal government's tax burden to 6.8 percent of GDP by1940.

World War II

Even before the United States entered the Second World War, increasing defense spending andthe need for monies to support the opponents of Axis aggression led to the passage in 1940 of two tax laws that increased individual and corporate taxes, which were followed by another taxhike in 1941. By the end of the war the nature of the income tax had been fundamentally altered.Reductions in exemption levels meant that taxpayers with taxable incomes of only $500 faced abottom tax rate of 23 percent, while taxpayers with incomes over $1 million faced a top rate of 94 percent. These tax changes increased federal receipts from $8.7 billion in 1941 to $45.2billion in 1945. Even with an economy stimulated by war-time production, federal taxes as ashare of GDP grew from 7.6 percent in 1941 to 20.4 percent in 1945. Beyond the rates andrevenues, however, another aspect about the income tax that changed was the increase in thenumber of income taxpayers from 4 million in 1939 to 43 million in 1945.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 6/165

6

Another important feature of the income tax that changed was the return to income taxwithholding as had been done during the Civil War. This greatly eased the collection of the taxfor both the taxpayer and the Bureau of Internal Revenue. However, it also greatly reduced thetaxpayer's awareness of the amount of tax being collected, i.e. it reduced the transparency of thetax, which made it easier to raise taxes in the future.

Developments after World War II

Tax cuts following the war reduced the Federal tax burden as a share of GDP from its wartimehigh of 20.9 percent in 1944 to 14.4 percent in 1950. However, the Korean War created a needfor additional revenues which, combined with the extension of Social Security coverage to self-employed persons, meant that by 1952 the tax burden had returned to 19.0 percent of GDP.

In 1953 the Bureau of Internal Revenue was renamed the Internal Revenue Service (IRS),following a reorganization of its function. The new name was chosen to stress the service aspectof its work. By 1959, the IRS had become the world's largest accounting, collection, and forms-

processing organization. Computers were introduced to automate and streamline its work and toimprove service to taxpayers. In 1961, Congress passed a law requiring individual taxpayers touse their Social Security number as a means of tax form identification. By 1967, all business andpersonal tax returns were handled by computer systems, and by the late 1960s, the IRS haddeveloped a computerized method for selecting tax returns to be examined. This made theselection of returns for audit fairer to the taxpayer and allowed the IRS to focus its auditresources on those returns most likely to require an audit.

Throughout the 1950s tax policy was increasingly seen as a tool for raising revenue and forchanging the incentives in the economy, but also as a tool for stabilizing macroeconomicactivity. The economy remained subject to frequent boom and bust cycles and many

policymakers readily accepted the new economic policy of raising or lowering taxes andspending to adjust aggregate demand and thereby smooth the business cycle. Even so, however,the maximum tax rate in 1954 remained at 87 percent of taxable income. While the income taxunderwent some manner of revision or amendment almost every year since the majorreorganization of 1954, certain years marked especially significant changes. For example, theTax Reform Act of 1969 reduced income tax rates for individuals and private foundations.

Beginning in the late 1960s and continuing through the 1970s the United States experiencedpersistent and rising inflation rates, ultimately reaching 13.3 percent in 1979. Inflation has adeleterious effect on many aspects of an economy, but it also can play havoc with an income taxsystem unless appropriate precautions are taken. Specifically, unless the tax system's parameters,i.e. its brackets and its fixed exemptions, deductions, and credits, are indexed for inflation, arising price level will steadily shift taxpayers into ever higher tax brackets by reducing the valueof those exemptions and deductions.

During this time, the income tax was not indexed for inflation and so, driven by a rising inflation,and despite repeated legislated tax cuts, the tax burden rose from 19.4 percent of GDP to 20.8percent of GDP. Combined with high marginal tax rates, rising inflation, and a heavy regulatory

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 7/165

7

burden, this high tax burden caused the economy to under-perform badly, all of which laid thegroundwork for the Reagan tax cut, also known as the Economic Recovery Tax Act of 1981.

The Evolution of Social Security and Medicare

The Social Security system remained essentially unchanged from its enactment until 1956.However, beginning in 1956 Social Security began an almost steady evolution as more and morebenefits were added, beginning with the addition of Disability Insurance benefits. In 1958,benefits were extended to dependents of disabled workers. In 1967, disability benefits wereextended to widows and widowers. The 1972 amendments provided for automatic cost-of-livingbenefits.

In 1965, Congress enacted the Medicare program, providing for the medical needs of personsaged 65 or older, regardless of income. The 1965 Social Security Amendments also created theMedicaid programs, which provides medical assistance for persons with low incomes andresources.

Of course, the expansions of Social Security and the creation of Medicare and Medicaid requiredadditional tax revenues, and thus the basic payroll tax was repeatedly increased over the years.Between 1949 and 1962 the payroll tax rate climbed steadily from its initial rate of 2 percent to 6percent. The expansions in 1965 led to further rate increases, with the combined payroll tax rateclimbing to 12.3 percent in 1980. Thus, in 31 years the maximum Social Security tax burden rosefrom a mere $60 in 1949 to $3,175 in 1980.

Despite the increased payroll tax burden, the benefit expansions Congress enacted in previousyears led the Social Security program to an acute funding crises in the early 1980s. Eventually,Congress legislated some minor programmatic changes in Social Security benefits, along with an

increase in the payroll tax rate to 15.3 percent by 1990. Between 1980 and 1990, the maximumSocial Security payroll tax burden more than doubled to $7,849.

The Tax Reform Act of 1986

Following the enactment of the 1981, 1982, and 1984 tax changes there was a growing sense thatthe income tax was in need of a more fundamental overhaul. The economic boom following the1982 recession convinced many political leaders of both parties that lower marginal tax rateswere essential to a strong economy, while the constant changing of the law instilled in policymakers an appreciation for the complexity of the tax system. Further, the debates during thisperiod led to a general understanding of the distortions imposed on the economy, and the lost jobs and wages, arising from the many peculiarities in the definition of the tax base. A new andbroadly held philosophy of tax policy developed that the income tax would be greatly improvedby repealing these various special provisions and lowering tax rates further. Thus, in his 1984State of the Union speech President Reagan called for a sweeping reform of the income tax so itwould have a broader base and lower rates and would be fairer, simpler, and more consistentwith economic efficiency.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 8/165

8

The culmination of this effort was the Tax Reform Act of 1986, which brought the top statutorytax rate down from 50 percent to 28 percent while the corporate tax rate was reduced from 50percent to 35 percent. The number of tax brackets was reduced and the personal exemption andstandard deduction amounts were increased and indexed for inflation, thereby relieving millionsof taxpayers of any Federal income tax burden. However, the Act also created new personal and

corporate Alternative Minimum Taxes, which proved to be overly complicated, unnecessary, andeconomically harmful.

The 1986 Tax Reform Act was roughly revenue neutral, that is, it was not intended to raise orlower taxes, but it shifted some of the tax burden from individuals to businesses. Much of theincrease in the tax on business was the result of an increase in the tax on business capitalformation. It achieved some simplifications for individuals through the elimination of suchthings as income averaging, the deduction for consumer interest, and the deduction for state andlocal sales taxes. But in many respects the Act greatly added to the complexity of businesstaxation, especially in the area of international taxation. Some of the over-reaching provisions of the Act also led to a downturn in the real estate markets which played a significant role in the

subsequent collapse of the Savings and Loan industry.

Seen in a broader picture, the 1986 tax act represented the penultimate installment of anextraordinary process of tax rate reductions. Over the 22 year period from 1964 to 1986 the topindividual tax rate was reduced from 91 to 28 percent. However, because upper-incometaxpayers increasingly chose to receive their income in taxable form, and because of thebroadening of the tax base, the progressivity of the tax system actually rose during this period.

The 1986 tax act also represented a temporary reversal in the evolution of the tax system.Though called an income tax, the Federal tax system had for many years actually been a hybridincome and consumption tax, with the balance shifting toward or away from a consumption tax

with many of the major tax acts. The 1986 tax act shifted the balance once again toward theincome tax. Of greatest importance in this regard was the return to references to economicdepreciation in the formulation of the capital cost recovery system and the significant newrestrictions on the use of Individual Retirement Accounts.

Between 1986 and 1990 the Federal tax burden rose as a share of GDP from 17.5 to 18 percent.Despite this increase in the overall tax burden, persistent budget deficits due to even higherlevels of government spending created near constant pressure to increase taxes. Thus, in 1990 theCongress enacted a significant tax increase featuring an increase in the top tax rate to 31 percent.Shortly after his election, President Clinton insisted on and the Congress enacted a second majortax increase in 1993 in which the top tax rate was raised to 36 percent and a 10 percent surchargewas added, leaving the effective top tax rate at 39.6 percent. Clearly, the trend toward lowermarginal tax rates had been reversed, but, as it turns out, only temporarily.

The Taxpayer Relief Act of 1997 made additional changes to the tax code providing a modest taxcut. The centerpiece of the 1997 Act was a significant new tax benefit to certain families withchildren through the Per Child Tax credit. The truly significant feature of this tax relief, however,was that the credit was refundable for many lower-income families. That is, in many cases thefamily paid a "negative" income tax, or received a credit in excess of their pre-credit tax liability.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 9/165

9

Though the tax system had provided for individual tax credits before, such as the Earned IncomeTax credit, the Per Child Tax credit began a new trend in federal tax policy. Previously tax relief was generally given in the form of lower tax rates or increased deductions or exemptions. The1997 Act really launched the modern proliferation of individual tax credits and especiallyrefundable credits that are in essence spending programs operating through the tax system.

The years immediately following the 1993 tax increase also saw another trend continue, whichwas to once again shift the balance of the hybrid income tax-consumption tax toward theconsumption tax. The movement in this case was entirely on the individual side in the form of aproliferation of tax vehicles to promote purpose-specific saving. For example, Medical SavingsAccounts were enacted to facilitate saving for medical expenses. An Education IRA and theSection 529 Qualified Tuition Program was enacted to help taxpayers pay for future educationexpenses. In addition, a new form of saving vehicle was enacted, called the Roth IRA, whichdiffered from other retirement savings vehicles like the traditional IRA and employer-based401(k) plans in that contributions were made in after-tax dollars and distributions were tax free.

Despite the higher tax rates, other economic fundamentals such as low inflation and low interestrates, an improved international picture with the collapse of the Soviet Union, and the advent of aqualitatively and quantitatively new information technology led to a strong economicperformance throughout the 1990s. This, in turn, led to an extraordinary increase in the aggregatetax burden, with Federal taxes as a share of GDP reaching a postwar high of 20.8 percent in2000.

The Bush Tax Cut

By 2001, the total tax take had produced a projected unified budget surplus of $281 billion, witha cumulative 10 year projected surplus of $5.6 trillion. Much of this surplus reflected a rising tax

burden as a share of GDP due to the interaction of rising real incomes and a progressive tax ratestructure. Consequently, under President George W. Bush's leadership the Congress halted theprojected future increases in the tax burden by passing the Economic Growth and Tax Relief andReconciliation Act of 2001. The centerpiece of the 2001 tax cut was to regain some of theground lost in the 1990s in terms of lower marginal tax rates. Though the rate reductions are tobe phased in over many years, ultimately the top tax rate will fall from 39.6 percent to 33percent.

The 2001 tax cut represented a resumption of a number of other trends in tax policy. Forexample, it expanded the Per Child Tax credit from $500 to $1000 per child. It also increased theDependent Child Tax credit. The 2001 tax cut also continued the move toward a consumption taxby expanding a variety of savings incentives. Another feature of the 2001 tax cut that isparticularly noteworthy is that it put the estate, gift, and generation-skipping taxes on course foreventual repeal, which is also another step toward a consumption tax. One novel feature of the2001 tax cut compared to most large tax bills is that it was almost devoid of business taxprovisions.

The 2001 tax cut will provide additional strength to the economy in the coming years as moreand more of its provisions are phased in, and indeed one argument for its enactment had always

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 10/165

10

been as a form of insurance against an economic downturn. However, unbeknownst to the BushAdministration and the Congress, the economy was already in a downturn as the Act was beingdebated. Thankfully, the downturn was brief and shallow, but it is already clear that the tax cutsthat were enacted and went into effect in 2001 played a significant role in supporting theeconomy, shortening the duration of the downturn, and preparing the economy for a robust

recovery.

One lesson from the economic slowdown was the danger of ever taking a strong economy forgranted. The strong growth of the 1990s led to talk of a "new" economy that many assumed wasvirtually recession proof. The popularity of this assumption was easy to understand when oneconsiders that there had only been one very mild recession in the previous 18 years.

Taking this lesson to heart, and despite the increasing benefits of the 2001 tax cut and the earlysigns of a recovery, President Bush called for and the Congress eventually enacted an economicstimulus bill. The bill included an extension of unemployment benefits to assist those workersand families under financial stress due to the downturn. The bill also included a provision to

providing a temporary but significant acceleration of depreciation allowances for businessinvestment, thereby assuring that the recovery and expansion will be strong and balanced.Interestingly, the depreciation provision also means that the Federal tax on business has resumedits evolution toward a consumption tax, once again paralleling the trend in individual taxation.

Federal tax code

The Federal tax law is administered primarily by the Internal Revenue Service, a bureau of theTreasury. The U.S. tax code is known as the Internal Revenue Code of 1986 (title 26 of theUnited States Code). The Code's complexity generally arises from two factors: the use of the taxcode for purposes other than raising revenue, and the feedback process of amending the code.

While the main intent of the law is to provide revenue for the federal government, the tax code isfrequently used for public policy reasons i.e., to achieve social, economic, and political goals.For example, to encourage home ownership, the tax law provides a deduction for mortgageinterest expense on debt secured by primary residences. In addition, the law does not allow adeduction for renters for rent paid to offset the advantage of non-recognition of exclusion of imputed owner occupied rent. An income tax system that favors neither renting nor owninghomes would not allow the mortgage interest deduction and would tax the imputed rent forowners who live in their own homes.

Because the government uses the tax code as an instrument of social policy, the code as a whole

appears to some critics to lack a coherent organizing principle. The purported lack of a coherentorganizing principle arguably has become magnified over time, due to the interplay betweensuccessive legislative amendments and regulatory changes to the law and the private sectorresponses to those amendments and changes. For instance, suppose that Congress enacts a taxcredit to encourage a particular type of activity. In response, a group of taxpayers who are not theintended beneficiaries of the credit re-order their affairs, or the superficial aspects of their affairs,to qualify for the credit. Congress responds by amending the code to add restrictions and targetthe credit more effectively. Certain taxpayers manage to use this change to claim additional

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 11/165

11

benefits, so Congress acts again, and so on. The result is a feedback loop of enactment andresponse, which, over an extended period of time, produces significant complexity.

Tax distribution

As of 2007, there are about 138 million taxpayers in the United States. The Treasury Departmentin 2006 reported, based on Internal Revenue Service (IRS) data, the share of federal incometaxes paid by taxpayers of various income levels. The data shows the progressive tax structure of the U.S. federal income tax system on individuals that reduces the tax incidence of people withsmaller incomes, as they shift the incidence disproportionately to those with higher incomes - thetop 0.1% of taxpayers by income pay 17.4% of federal income taxes (earning 9.1% of theincome), the top 1% with gross income of $328,049 or more pay 36.9% (earning 19%), the top5% with gross income of $137,056 or more pay 57.1% (earning 33.4%), and the bottom 50%with gross income of $30,122 or less pay 3.3% (earning 13.4%). If the federal taxation rate iscompared with the wealth distribution rate, the net wealth (not only income but also includingreal estate, cars, house, stocks, etc) distribution of the United States does almost coincide with

the share of income tax - the top 1% pay 36.9% of federal tax (wealth 32.7%), the top 5% pay57.1% (wealth 57.2%), top 10% pay 68% (wealth 69.8%), and the bottom 50% pay 3.3% (wealth2.8%).

Other taxes in the United States with a less progressive structure or a regressive structure, andlegal tax avoidance loopholes change the overall tax burden distribution. For example, thepayroll tax system (FICA), a 12.4% Social Security tax on wages up to $106,800 (for 2009) anda 2.9% Medicare tax (a 15.3% total tax that is often split between employee and employer) iscalled a regressive tax on income with no standard deduction or personal exemptions but ineffect is forced savings which return to the payer in the form of retirement benefits and healthcare. The Center on Budget and Policy Priorities states that three-fourths of U.S. taxpayers pay

more in payroll taxes than they do in income taxes.

The National Bureau of Economic Research has concluded that the combined federal, state, andlocal government average marginal tax rate for most workers to be about 40% of income.

United States Department of Justice Tax Division

The United States Department of Justice Tax Division is responsible for the prosecution of both civiland criminal cases arising under the Internal Revenue Code and other tax laws of the United States. TheDivision began operation in 1934, under United States Attorney General Homer Stille Cummings, who

charged it with primary responsibility for supervising all federal litigation involving internal revenue(following an executive order from President Franklin Delano Roosevelt).

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 12/165

12

Responsibilities

The Tax Division works closely with public schools and corporations of the state and theCriminal Investigation Division and other units of the Internal Revenue Service to develop andcoordinate federal tax policy. Among the Division's duties are:

Participating in the President's Corporate Fraud Task Force Working with the Securities and Exchange Commission to promote corporate

integrity Pursuing criminal tax investigations and prosecutions of corporate executives Handling criminal investigations and prosecutions of terrorist financing cases Fighting abusive and fraudulent tax promotions Seeking civil injunctions against promoters of abusive tax schemes Handling criminal prosecutions of major tax fraud promoters Working with the Federal Trade Commission to combat internet fraud schemes Using both civil and criminal tools to put tax fraud promoters out of business

Enforcing IRS summonses for records of corporate tax shelters Attacking the use of foreign bank accounts to evade taxes Enforcing IRS summonses for records of offshore credit card transactions Initiating criminal investigations of suspects in offshore tax evasion cases Combating schemes that cheat the IRS through abuse of the bankruptcy system Enhancing policy coordination between the Tax Division and the IRS.

Leadership

The current head of the Tax Division is Acting Assistant Attorney General John A. DiCicco,who is also the Deputy Assistant Attorney General for the Civil Matters Branch of the Tax

Division.

Organization

The head of the Tax Division is an Assistant Attorney General, who is appointed by thePresident of the United States. The Assistant Attorney General is assisted by four DeputyAssistant Attorneys General, who are each career attorneys, who each oversee a different branchof the Tax Division's sections.

Assistant Attorney General for Tax Division

Deputy Assistant Attorney General for Policy and Planning

Office of Legislation, Policy and Management Office of Training and Career Development Office of Management and Administration

Deputy Assistant Attorney General for Criminal Matters

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 13/165

13

Northern Criminal Enforcement Section Southern Criminal Enforcement Section Western Criminal Enforcement Section Criminal Appeals and Tax Enforcement Policy Section

Deputy Assistant Attorney General for Review and appellate

Civil Appellate Section Office of Review

Deputy Assistant Attorney General for Civil Matters

Central Civil Trail Section Eastern Civil Trail Section Northern Civil Trail Section Southern Civil Trail Section Southwestern Civil Trail Section Western Civil Trail Section Court of Federal Claims Section

List of taxes

Taxes and fees imposed by federal, state or local laws.

Alternative minimum tax (AMT). U.S. capital gains tax. Corporate income tax. U.S. estate tax.

U.s. excise tax. U.S. federal income tax. Federal unemployment tax. FICA tax (including social security tax& related programs). Gasoline tax. Generation skipping tax. Gift tax. IRS penalties. Local income tax. Luxury taxes. Property tax. Real estate tax. Recreational vehicle tax. Rental car tax. Resort tax. Road usage taxes. School tax. State income tax. State unemployment tax.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 14/165

14

Tariffs. Telephone federal excise tax. Vehicle sales tax. Workers compensation tax.

Alternative Minimum Tax

Alternative Minimum Tax (AMT) is part of the Federal income tax system of the UnitedStates. There is an AMT for those who owe personal income tax, and another for corporationsowing corporate income tax. Only the AMT for those owing personal income tax is describedhere.

The AMT operates as a parallel tax system to the regular tax system with its own definition of taxable income, exemptions, and tax rates. It was originally called the "millionaire's tax", in thatit targeted only the wealthiest households. The income triggers were not indexed for inflation soas incomes rose the AMT touched more of the middle class. Without periodic Congressional

action to temporarily raise the income limits that trigger the AMT, almost a quarter of the UnitedStates' 90 million taxpayers could be required to pay the tax.

In practice, taxpayers must compute tax owed under the "regular" and AMT systems and areliable for whichever is higher. The AMT system has in general a broader definition of taxableincome, a larger exemption, and lower tax rates than the regular system. For taxpayers subject tothe AMT, it means that a portion of their itemized deductions are effectively eliminated, andthereby increases the tax they owe the federal government vs. the regular tax system.

History and current controversies of AMT

The AMT was introduced by the Tax Reform Act of 1969 and became operative in 1970. It wasintended to target 155 high-income households that had been eligible for so many tax benefitsthat they owed little or no income tax under the tax code of the time. However, the AMT hasevolved significantly in many ways since then, with substantial changes in 1978, 1982, 1986,1990, and 1993, among others. According to the Congressional Joint Committee on Taxation, theAMT provisions enacted in the Tax Equity and Fiscal Responsibility Act of 1982 are thefoundation for the present individual alternative minimum tax: these provisions included thedisallowal of state and local taxes, the deduction for personal exemptions, the standarddeduction, and the deduction for interest on home equity loans.

A further shift, involving many definitional changes and extensive reorganization, occurred withthe Tax Reform Act of 1986.

However both participation and revenues from the AMT temporarily plummeted after the 1986changes. Further significant changes occurred as a result of the Omnibus Budget ReconciliationActs of 1990 and 1993, which raised the AMT rate to 24%, and to 26%/28% respectively, fromthe prior level of 21%. Now many taxpayers who do not have high incomes or participate in anyspecial tax shelter activities have to pay AMT.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 15/165

15

The AMT is imposed under 26 U.S.C. § 55 and disallows many deductions and exemptionsallowable in computing "regular" tax liability. (Regular tax liability is defined in 26U.S.C. § 55(c)(1), with reference to 26 U.S.C. § 26(b), and does not include AMT and variousother categories of taxes imposed under Chapter 1 of Subtitle A of the Internal Revenue Code.)The AMT currently sets a minimum tax rate of either 26% or 28% (depending on the amount of

the taxpayer's "alternative minimum taxable income," as adjusted) on amounts above a largeexemption so that taxpayers cannot use certain types of deductions to lower their tax below acertain minimum. Affected taxpayers are those who have what are known as "tax preferenceitems". These include state and local income, sales and property taxes, accelerated depreciation, a portion of otherwise deductible medical expenses, miscellaneous itemized deductions, thebargain element in exercised incentive stock options, percentage depletion, certain tax-exemptincome, certain credits, personal exemptions and the standard deduction. In addition, due to adifferent system of exemption phase outs, items such as long-term capital gains may result inAMT.

In recent years, the AMT has been under increased attention. Because the AMT is not indexed toinflation and because of recent tax cuts, an increasing number of middle-income taxpayers have

been finding themselves subject to this tax. The lack of indexing produces bracket creep. Therecent tax cuts in the regular tax have the effect of causing many taxpayers to pay some AMT,reducing or eliminating the benefit from the reduction in regular rates. (In all such cases,however, the overall tax payable will not increase. In 2006, the IRS's National TaxpayerAdvocate's report highlighted the AMT as the single most serious problem with the tax code.The Advocate noted that the AMT punishes taxpayers for having children or living in a high-taxstate and that the complexity of the AMT leads to most taxpayers who owe AMT not realizing ituntil preparing their returns or being notified by the IRS.

A brief issued by the Congressional Budget Office (CBO) (No. 4, April 15, 2004), concludes:

"Over the coming decade, a growing number of taxpayers will become liable for theAMT. In 2010, if nothing is changed, one in five taxpayers will have AMT liability andnearly every married taxpayer with income between $100,000 and $500,000 will owe thealternative tax. Rather than affecting only high-income taxpayers who would otherwisepay no tax, the AMT has extended its reach to many upper-middle-income households.As an increasing number of taxpayers incur the AMT, pressures to reduce or eliminatethe tax are likely to grow."

However, CBO's rules state that it must use current law in its analysis, and at the time the abovetext was written, the AMT threshold was set to expire in 2006 and be reset to far lower values.

For years, Congress has passed one-year patches aimed at minimizing the impact of the tax. Forthe 2007 tax year, a patch was passed on 12/20/2007, but only after the IRS had already designedits forms for 2007. The IRS had to reprogram its forms to accommodate the law change.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 16/165

16

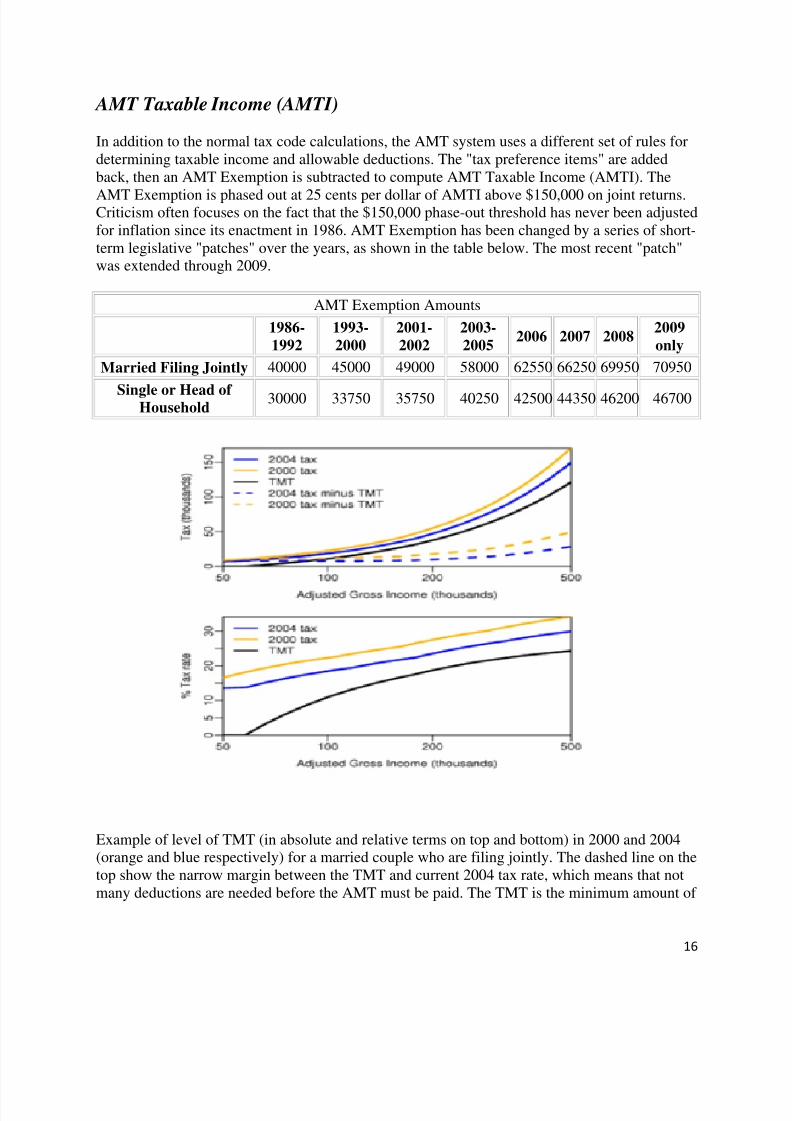

AMT Taxable Income (AMTI)

In addition to the normal tax code calculations, the AMT system uses a different set of rules fordetermining taxable income and allowable deductions. The "tax preference items" are addedback, then an AMT Exemption is subtracted to compute AMT Taxable Income (AMTI). The

AMT Exemption is phased out at 25 cents per dollar of AMTI above $150,000 on joint returns.Criticism often focuses on the fact that the $150,000 phase-out threshold has never been adjustedfor inflation since its enactment in 1986. AMT Exemption has been changed by a series of short-term legislative "patches" over the years, as shown in the table below. The most recent "patch"was extended through 2009.

AMT Exemption Amounts

1986-1992

1993-2000

2001-2002

2003-2005

2006 2007 20082009only

Married Filing Jointly 40000 45000 49000 58000 62550 66250 69950 70950

Single or Head of Household

30000 33750 35750 40250 42500 44350 46200 46700

Example of level of TMT (in absolute and relative terms on top and bottom) in 2000 and 2004(orange and blue respectively) for a married couple who are filing jointly. The dashed line on thetop show the narrow margin between the TMT and current 2004 tax rate, which means that notmany deductions are needed before the AMT must be paid. The TMT is the minimum amount of

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 17/165

17

tax a person will end up paying, if it is less than the usual tax, there is no AMT. If it is more thanthe usual tax, the AMT makes up the difference.

Tentative Minimum Tax (TMT)

Applying a 26/28% rate schedule to the AMTI gives the "Tentative Minimum Tax" (TMT).TMT is 26% of AMTI up to $175,000, plus 28% of the rest of the AMTI, if any. The TMT iscompared to the income-tax amount calculated for the taxpayer. If the regular income-taxamount is greater than the TMT, no special action is required. If the TMT is greater than the taxcalculated using the regular rules, the difference between the TMT and the regular tax is added tothe regular tax amount, so the taxpayer pays the full amount of the TMT. In effect, the taxliability (before application of credits) is the greater of the regular income tax amount and theTMT.

AMT Exemption Phase-out and Effective Marginal Rates

For 2007, the AMT Exemption is not fully phased out until AMTI surpasses $415,000 for jointreturns. Like any deduction that phases out with income, the AMT Exception increases theeffective marginal tax rate within the phase out range. Within the $150,000 to $415,000 range,the TMT rates of 26% and 28% are effectively multiplied by 1.25, becoming 32.5% and 35%(See note below). The TMT rate for capital gains becomes 21.5% to 22% rather than 15%,because each dollar of capital gain causes 25 cents more of ordinary income to be taxed at 26%or 28%. These are the true marginal federal tax rates for most taxpayers owing AMT. Thesemarginal rates for TMT exceed regular tax rates at the lower end of this income range. ThereforeAMT liability (the excess of TMT over regular tax) typically increases as income increasesabove $150,000. Non-deductibility of state income tax under the TMT exacerbates this problem.Advice to accelerate income when you will be liable for AMT is therefore exactly backwards for

most taxpayers.

AMT Credit

A portion of the tax that is considered AMT may be available in later years as a "Minimum TaxCredit", reducing the tax due in later years, but usually not below the taxpayer's TMT level inthose later years. A full description of the AMT Credit is The Fairmark web site has a guide toAMT Credit.

Transfer taxes

The transfer tax generates roughly 1.5% ($30 billion) of the federal government's annual revenue($2 trillion). It consists of the gift tax, the estate tax and the generation-skipping transfer tax("GSTT"). Opponents of the transfer tax label these taxes "death taxes". The term "death tax"was popularized by Frank Luntz, a Republican political consultant, but its use goes back to atleast the 19th century.

The gift tax is a tax levied on wealth transfers during the transferor's life while the estate tax islevied on transfers made after the transferor's death. The GSTT is a tax in addition to the gift and

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 18/165

18

estate tax and is levied (in rough terms) on transfers made during life or after death to individualsremoved by more than one generation from the transferor, for example, from a grandmother to agrandson. Usually transfer tax liabilities are paid by the transferor or the transferor's estate. Payment of transfer taxes by the transferor when the liability is due from the recipient is also ataxable gift.

As of December 2002, tax rates for gift and estate taxes begin at 18% and rise to 50% for giftsover $12,000 or taxable estates over $2.5 million under the Unified Transfer Tax Rate Schedule.The GSTT is a flat 50%. Each individual is granted a Unified Credit (currently $345,800) theeffect of which exempts estates under $1 million. Each individual is also granted an annualexclusion amount the effect of which exempts total gifts to any one individual during the year upto the annual exclusion amount (As of 2009, $13,000 per person per year). If the transferor doesnot elect to pay the gift tax on the value of gifts totaling more than the annual exclusion amount,the individual is deemed to have used a portion of his Unified Credit. An exemption (currently$1.1 million) for transfers subject to the GSTT is also granted to each individual during hislifetime. The Unlimited Marital Deduction allows (non-foreign) spouses to transfer any amount

of wealth with no transfer tax consequences.

Social Security tax

The next largest tax is Social Security tax formally known as the Federal Insurance andContributions Act (FICA). This contribution or tax is 6.2% of an employees' income paid by theemployer, and 6.2% paid by the employee (12.4% total). Self-employed workers must pay bothhalves of the Social Security tax because they are their own employers. This tax is paid only onearned income and, as noted above, only up to a threshold income for calendar year 2009 of $106,800 called the "Social Security Wage Base" (SSWB), for an maximum individualcontribution of $6,621.60 ($13,243.20 combined). The SSWB increases every year according to

the national index average of wages which also indexes the bend points in the Primary InsuranceAmount (PIA) computations. Unearned income like interest from bonds, money market and bank accounts, dividends from REITs and common stocks, rents, and royalties are not subject to theSocial Security tax. Wages are defined in the United States Code 42 USC Section 409. Thus, bysimple arithmetic, higher earners pay a lower average tax rate than those with earned income atthe upper end, making this an extremely regressive tax. Thus, earners above the SSWB pay amuch lower combined marginal federal tax rate, when including Social Security and Medicaretaxes, than those at the SSWB.

City and county tax

Cities and counties in the individual states may levy additional taxes, for instance to improveparks or schools, or pay for police, fire departments, local roads, and other services. As in thecase of the IRS, they generally require a tax payment account number. Other local governmentalagencies may also have the power to tax, notably independent school districts.

Local government usually collect property taxes but may also collect sales taxes and incometaxes. Some cities collect income tax on not only residents but non-residents employed in thecity. This tax can even be incurred when a non-resident works temporarily in the city. For

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 19/165

19

example, in 1992 the city of Philadelphia began enforcing the collection of city wage taxes onvisiting baseball players who played games in Philadelphia. At least some counties levy anOccupational Privilege Tax (OPT), usually for a small amount, in some cases less than $100/yr.

Corporate income tax

In the United States, the federal corporate income rate for the year 2006 varies between 15 and39% depending on taxable income. But since 1999, when Treasury announced the "check thebox" system many corporations can elect to be treated as a pass-through entity, thereby skippingthe entity level 35% tax and having all income pass through to the shareholders. This is the taxtreatment that the much discussed "S" corporations receive; but now many more types of state-law corporations may avoid double taxation by "checking the box". Dividends are also subject toa lower rate of income tax in the United States.

Capital gains tax

In the United States, individuals and corporations pay income tax on the net total of all theircapital gains just as they do on other sorts of income. Capital gains are generally taxed at apreferential rate in comparison to ordinary income. This is intended to provide incentives forinvestors to make capital investments and to fund entrepreneurial activity. The amount aninvestor is taxed depends on both his or her tax bracket, and the amount of time the investmentwas held before being sold. Short-term capital gains are taxed at the investor's ordinary incometax rate, and are defined as investments held for a year or less before being sold. Long-term

capital gains, which apply to assets held for more than one year, are taxed at a lower rate thanshort-term gains. In 2003, this rate was reduced to 15%, and to 5% for individuals in the lowesttwo income tax brackets. These reduced tax rates were passed with a sunset provision and areeffective through 2010; if they are not extended before that time, they will expire and revert tothe rates in effect before 2003, which were generally 20%.

The reduced 15% tax rate on qualified dividends and long term capital gains, previouslyscheduled to expire in 2008, was extended through 2010 as a result of the Tax Reconciliation Actsigned into law by President George W. Bush on May 17, 2006. As a result:

In 2008, 2009, and 2010, the tax rate on qualified dividends and long term capital gains is

0% for those in the 10% and 15% income tax brackets. After 2010, dividends will be taxed at the taxpayer's ordinary income tax rate, regardless

of his or her tax bracket. After 2010, the long-term capital gains tax rate will be 20% (10% for taxpayers in the

15% tax bracket). After 2010, the qualified five-year 18% capital gains rate (8% for taxpayers in the 15%

tax bracket) will be reinstated.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 20/165

20

Capital Gains Taxation in the United States from 2003 forward

2003 - 2010 2011 -

2003 - 2007 2008 - 2010 2011 -

OrdinaryIncomeTax Rate

Short-

termCapitalGains

Tax Rate

Long-term

CapitalGains

Tax Rate

Short-

termCapitalGains

Tax Rate

Long-term

CapitalGains

Tax Rate

OrdinaryIncomeTax Rate

Short-

termCapitalGains

Tax Rate

Long-term

CapitalGains

Tax Rate

10% 10% 5% 10% 0%15% 15% 10%

15% 15% 5% 15% 0%

25% 25% 15% 25% 15% 28% 28% 20%

28% 28% 15% 28% 15% 31% 31% 20%

33% 33% 15% 33% 15% 36% 36% 20%

35% 35% 15% 35% 15% 39.6% 39.6% 20%

When the taxable gain or loss resulting from the sale of an asset is calculated, its cost basis isused rather than its actual purchase price. The cost basis is an adjustment of the purchase pricethat takes into account factors such as fees paid (brokerage fees, certain legal fees, sales fees),taxes paid (including sales tax, excise taxes, real estate taxes, etc.), and depreciation.

The United States is unlike other countries in that its citizens are subject to U.S. tax regardless of where in the world they reside. U.S. citizens therefore find it difficult to take advantage of personal tax havens. Although there are some offshore bank accounts that advertise as taxhavens, U.S. law requires reporting of income from those accounts and failure to do soconstitutes tax evasion.

History of capital gains tax in the U.S.

From 1913 to 1921, capital gains were taxed at ordinary rates, initially up to a maximum rate of 7 percent. In 1921 the Revenue Act of 1921 was introduced, allowing a tax rate of 12.5 percentgain for assets held at least two years. From 1934 to 1941, taxpayers could exclude percentagesof gains that varied with the holding period: 20, 40, 60, and 70 percent of gains were excluded onassets held 1, 2, 5, and 10 years, respectively. Beginning in 1942, taxpayers could exclude 50percent of capital gains on assets held at least six months or elect a 25 percent alternative tax rateif their ordinary tax rate exceeded 50 percent. Capital gains tax rates were significantly increasedin the 1969 and 1976 Tax Reform Acts. In 1978, Congress reduced capital gains tax rates byeliminating the minimum tax on excluded gains and increasing the exclusion to 60 percent,thereby reducing the maximum rate to 28 percent. The 1981 tax rate reductions further reducedcapital gains rates to a maximum of 20 percent.

The Tax Reform Act of 1986 repealed the exclusion of long-term gains, raising the maximumrate to 28 percent (33 percent for taxpayers subject to phase-outs). When the top ordinary taxrates were increased by the 1990 and 1993 budget acts, an alternative tax rate of 28 percent was

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 21/165

21

provided. Effective tax rates exceeded 28 percent for many high-income taxpayers, however,because of interactions with other tax provisions. The new lower rates for 18-month and five-year assets were adopted in 1997 with the Taxpayer Relief Act of 1997. In 2001, PresidentGeorge W. Bush signed the Economic Growth and Tax Relief Reconciliation Act of 2001, intolaw as part of a $1.35 trillion tax cut program.

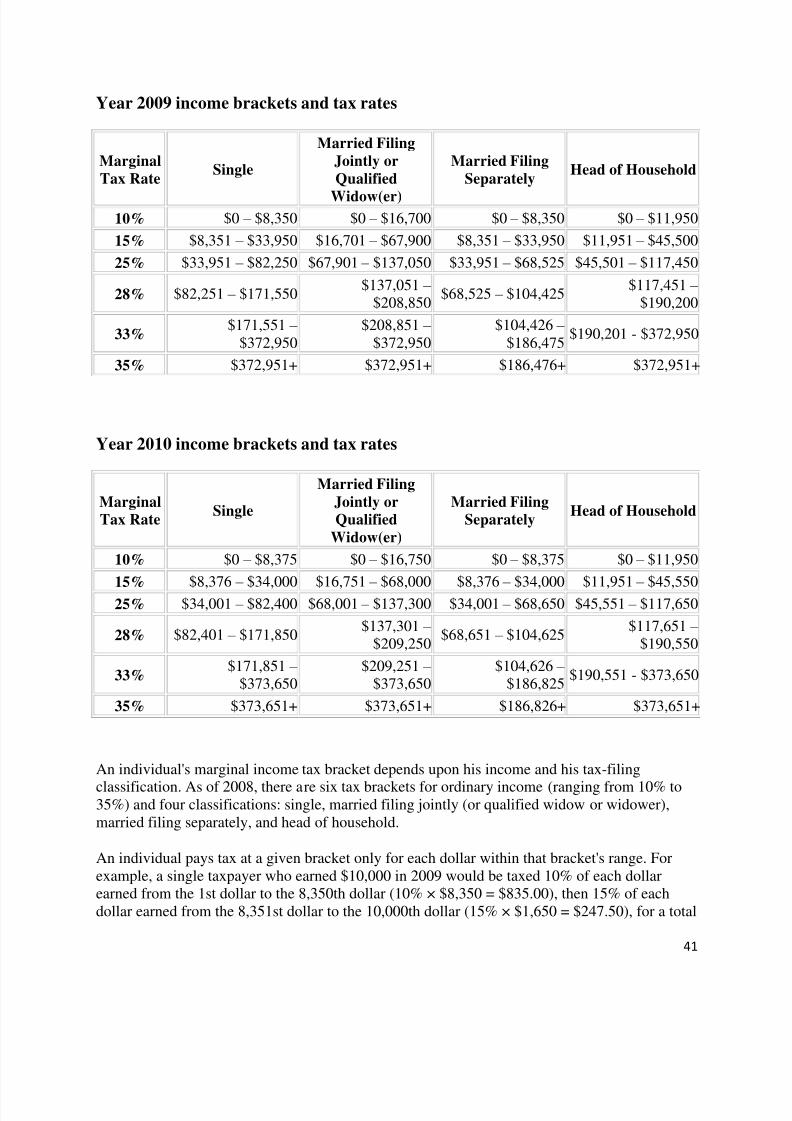

Tax rates for 2009

*Note: the dollar amount refers to taxable income, not adjusted gross income (AGI).

MarginalOrdinaryIncome

TaxRate[3]

Single

Married FilingJointly orQualified

Widow(er)

Married FilingSeparately

Head of Household

10% $0 – $8,350 $0 – $16,700 $0 – $8,350 $0 – $11,950

15% $8,351 – $33,950 $16,701 – $67,900 $8,351 – $33,950 $11,951 – $45,500

25% $33,951 – $82,250 $67,901 – $137,050 $33,951 – $68,525 $45,501 – $117,450

28% $82,251 – $171,550$137,051 –

$208,850$68,525 – $104,425

$117,451 – $190,200

33%$171,551 –

$372,950$208,851 –

$372,950$104,426 –

$186,475$190,201 - $372,950

35% $372,951+ $372,951+ $186,476+ $372,951+

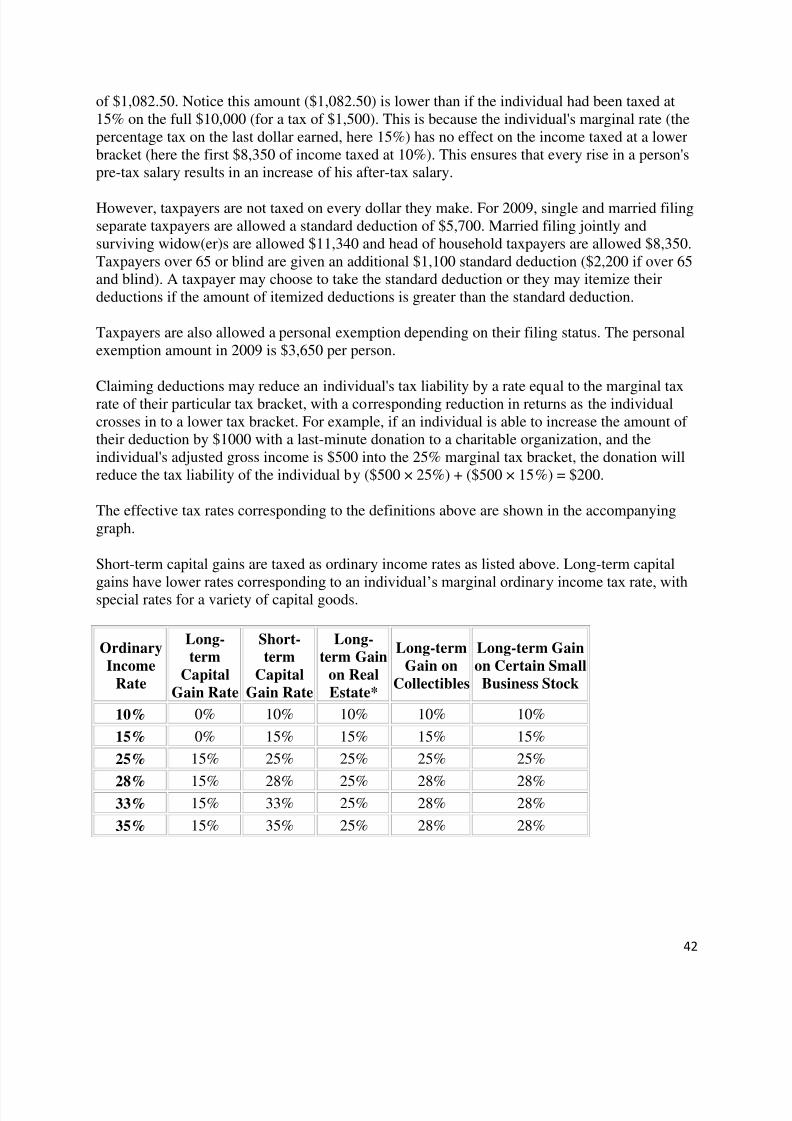

Short-term capital gains are taxed as ordinary income rates as listed above. Long-term capital

gains have lower rates corresponding to an individual‘s marginal ordinary income tax rate, withspecial rates for a variety of capital goods.

OrdinaryIncome

Rate

Long-term

CapitalGain Rate

Short-term

CapitalGain Rate

Long-term Gain

on RealEstate*

Long-termGain on

Collectibles

Long-term Gainon Certain SmallBusiness Stock

10% 0% 10% 10% 10% 10%

15% 0% 15% 15% 15% 15%

25% 15% 25% 25% 25% 25%

28% 15% 28% 25% 28% 28%

33% 15% 33% 25% 28% 28%

35% 15% 35% 25% 28% 28%

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 22/165

22

Corporate tax

Corporate tax or company tax refers to a tax imposed on entities that are taxed at the entity

level in a particular jurisdiction. Such taxes may include income or other taxes. The tax systemsof most countries impose an income tax at the entity level on certain type(s) of entities (companyor corporation). Many systems additionally tax owners or members of those entities on dividendsor other distributions by the entity to the members. The tax generally is imposed on net taxableincome. Net taxable income for corporate tax is generally financial statement income withmodifications, and may be defined in great detail within the system. The rate of tax varies by jurisdiction. The tax may have an alternative base, such as assets, payroll, or income computed inan alternative manner.

Most income tax systems provide that certain types of corporate events are not taxabletransactions. These generally include events related to formation or reorganization of the

corporation. In addition, most systems provide specific rules for taxation of the entity and/or itsmembers upon winding up or dissolution of the entity.

In systems where financing costs are allowed as reductions of the tax base (tax deductions), rulesmay apply that differentiate between classes of member-provided financing. In such systems,items characterized as interest may be deductible, subject to interest limitations, while itemscharacterized as dividends are not. Some systems limit deductions based on simple formulas,such as a debt-to-equity ratio, while other systems have more complex rules.

Some systems provide a mechanism whereby groups of related corporations may obtain benefitfrom losses, credits, or other items of all members within the group. Mechanisms include

combined or consolidated returns as well as group relief (direct benefit from items of anothermember).

Most systems also tax company shareholders on distribution of earnings as dividends. A fewsystems provide for partial integration of entity and member taxation. This is often accomplishedby "imputation systems" or franking credits. In the past, mechanisms have existed for advancepayment of member tax by corporations, with such payment offsetting entity level tax.

Many systems (particularly sub-country level systems) impose a tax on particular corporateattributes. Such non-income taxes may be based on capital stock issued or authorized (either bynumber of shares or value), total equity, net capital, or other measures unique to corporations.

Corporations, like other entities, may be subject to withholding tax obligations upon makingcertain varieties of payments to others. These obligations are generally not the tax of thecorporation, but the system may impose penalties on the corporation or its officers or employeesfor failing to withhold and pay over such taxes

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 23/165

23

Taxation of corporations

Corporations may be taxed on their incomes, property, or existence by various jurisdictions.Many jurisdictions impose a tax based on the existence or equity structure of the corporation. Forexample, Maryland imposes a tax on corporations organized in that state based on the number of

shares of capital stock issued and outstanding. Many jurisdictions instead impose a tax based onstated or computed capital, often including retained profits.

Most jurisdictions tax corporations on their income. Generally, this tax is imposed at a specificrate or range of rates on taxable income as defined within the system. Some systems have aseparate body of law or separate provisions relating to corporate taxation. In such cases, the lawmay apply only to entities and not to individuals operating a trade. Such laws may differentiatebetween broad types of income earned by corporations and tax such types of income differently.Generally, however, most such systems tax all income of a corporation in the same manner.

Some systems (e.g., Canada and the United States) tax corporations under the same framework

of tax law as individuals. In such systems, there are normally taxation differences related todifferences between the inherent natures of corporations and individuals or unincorporatedentities. For example, individuals are not formed, amalgamated, or acquired, and corporations donot generally incur medical expenses except by way of compensating individuals.

Many systems allow tax credits for specific items. Such direct reductions of tax are commonlyallowed for foreign taxes on the same income and for withholding tax. Often these credits are thesame as those available to individuals or for members of flow through entities such aspartnerships.

Most systems tax both domestic and foreign corporations. Often, domestic corporations are taxed

on worldwide income while foreign corporations are taxed only on income from sources withinthe jurisdiction. Many jurisdictions imposing an income tax impose such tax income from apermanent establishment within the jurisdiction.

Corporations are also subject to property tax, payroll tax, withholding tax, excise tax, customsduties, value added tax, and other common taxes, generally in the same manner as othertaxpayers. These, however, are rarely referred to as ―corporate tax.‖

Corporate tax rates

Corporate tax rates generally are the same for differing types of income. However, many systems

have graduated tax rate systems under which corporations with lower levels of income pay alower rate of tax. Some systems impose tax at different rates for different types of corporations.Tax rates vary by jurisdiction. In addition, some countries have sub-country level jurisdictionsthat also impose corporate income tax. Some jurisdictions also impose tax at a different rate onan alternative tax base (see below). Note that some entities may be eligible for tax exemption onpart or all of their income in some jurisdictions

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 24/165

24

United States: Federal 15% to 35%. States: 0% to 10%, deductible in computing Federal taxableincome. Some cities: up to 9%, deductible in computing Federal taxable income. The FederalAlternative Minimum Tax of 20% is imposed on regular taxable income with adjustments.

Tax returns

Most systems require that corporations file an annual income tax return. Some systems (such asthe Canadian and United States systems) require that taxpayers self assess tax on the tax return.Other systems provide that the government must make an assessment for tax to be due. Somesystems require certification of tax returns in some manner by accountants licensed to practice inthe jurisdiction, often the company's auditors.

Tax returns can be fairly simple or quite complex. The systems requiring simple returns oftenbase taxable income on financial statement profits with few adjustments, and may require thataudited financial statements be attached to the return. Returns for such systems generally requirethat the relevant financial statements be attached to a simple adjustment schedule. By contrast,

United States corporate tax returns require both computation of taxable income from componentsthereof and reconciliation of taxable income to financial statement income.

Many systems require forms or schedules supporting particular items on the main form. Some of these schedules may be incorporated into the main form. For example, the Canadian corporatereturn, Form T-2, an 8 page form, incorporates some detail schedules but has nearly 50additional schedules that may be required.

Some systems have different returns for different types of corporations or corporations engagedin specialized businesses. The United States has 13 variations on the basic Form 1120 for Scorporations, insurance companies, Domestic international sales corporations, foreign

corporations, and other entities. The structure of the forms and imbedded schedules vary by typeof form.

Preparation of non-simple corporate tax returns can be time consuming. For example, the U.S.Internal Revenue Service states in the instructions for Form 1120 that the average time needed tocomplete form is over 56 hours, not including record keeping time and required attachments.

Tax return due dates vary by jurisdiction, fiscal or tax year, and type of entity. In self assessmentsystems, payment of taxes is generally due no later than the normal due date, though advance taxpayments may be required. Canadian corporations must pay estimated taxes monthly. In eachcase, final payment is due with the corporation tax return.

Luxury tax

A luxury tax is a tax on luxury goods -- products not considered essential. A luxury tax may bemodeled after a sales tax or VAT, charged as a percentage on all items of particular classes,except that it mainly affects the wealthy because the wealthy are the most likely to buy luxuriessuch as expensive cars, jewelry, etc. It may also be applied only to purchases over a certainamount, for instance, some U.S. states charge luxury tax on real estate transactions over a limit.

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 25/165

25

A luxury good may be a Veblen good, which is a type of good for which demand increases asprice increases. Therefore the effect of a luxury tax may be to increase demand for certain luxurygoods. In general, however, since a luxury good has a high income elasticity of demand bydefinition, both the income effect and substitution effect will decrease demand sharply as the taxrises.

History

In the United States, many states used to collect state sales tax through the use of "luxury taxtokens" instead of calculating a percentage to be paid in cash like the modern-day practice.Tokens could be purchased from the state and then used at checkout instead of rendering thesales tax in cash. Presumably, the purpose of the practice was to remove the incentive for storesand businesses to avoid reporting income. Some tokens were copper or base metal while somewere even plastic.

Impact

When a luxury tax is imposed, typically there is little to no outcry from the majority of thepopulation as most people are not in a position to pay the tax. Over time, what is viewed as"luxury" might change, resulting in more and more people being affected by the tax. Despite theanimosity that ensues, the government may view the income from the luxury tax as essential andwill not restrict or rescind it. So it may happen over time that goods considered "ordinary" mightalso incur luxury tax. An example of this can be seen with various commodities in the country of Norway, where at the beginning of last century, cars and chocolate were viewed as luxury goods.Thus, additional taxes were levied upon these goods. Today few Norwegians consider cars orchocolate a luxury, but the luxury taxes on these goods remain. In Ireland, many personalhygiene products are within the luxury tax bracket.

In addition, this can lead to decreased exchange of luxury goods due to the higher price, resultingin luxury good manufacturers and employees bearing the brunt of the tax and the governmentfacing substantially lower tax revenue. This effect, including the economic damage that it entails,led to the repeal of the luxury tax in the United States.

Medicare tax

The Medicare tax funds the Medicare program, a health insurance program for the elderly anddisabled. 1.45% of the employee's income is paid by the employer as Medicare tax, and 1.45% ispaid by the employee. Unlike Social Security, there is no cap on the Medicare tax.

For Self-Employed people, Medicare taxes are fixed at 2.9% on all earnings (can be offset byincome tax provisions.)

As in FICA, unearned income is not subject to the Medicare contribution.

Together, Social Security and Medicare taxes compose the payroll tax. These taxes are based onincome, but unlike the Federal income tax, they are set aside for their specific purposes. That is,

8/4/2019 tax system and procedure in USA, UK, India by Simon (BUBT)

http://slidepdf.com/reader/full/tax-system-and-procedure-in-usa-uk-india-by-simon-bubt 26/165

26

there is a statutory requirement that expenditures on these programs Medicare and SocialSecurity come out of current taxes or accumulated trust funds, so if they go broke, the SocialSecurity Administration and Medicare would be without the authority to pay benefits. UnlikeCongress, they cannot borrow on the federal government's creditworthiness to fund operationsfrom the credit markets.

Estate tax

The estate tax in the United States is a tax imposed on the transfer of the "taxable estate" of adeceased person, whether such property is transferred via a will, according to the state laws of intestacy or otherwise made as an incident of the death of the owner, such as a transfer of property from an intestate estate or trust, or the payment of certain life insurance benefits orfinancial account sums to beneficiaries. The estate tax is one part of the Unified Gift and Estate

Tax system in the United States. The other part of the system, the gift tax, imposes a tax ontransfers of property during a person's life; the gift tax prevents avoidance of the estate taxshould a person want to give away his/her estate.

In addition to the federal government, many states also impose an estate tax, with the stateversion called either an estate tax or an inheritance tax. Since the 1990s, opponents of the taxhave used the pejorative term "death tax." The equivalent tax in the United Kingdom has alwaysbeen referred to as "death duties."

If an asset is left to a spouse or a charitable organization, the tax usually does not apply.

Federal estate tax

The Federal estate tax is imposed "on the transfer of the taxable estate of every decedent who is

a citizen or resident of the United States." The starting point in the calculation is the "grossestate." Certain deductions (subtractions) from the "gross estate" amount are allowed in arrivingat a smaller amount called the "taxable estate."

The "gross estate"