tax return basics swasfaa conference november 8 – 10, 2006

TRANSCRIPT

Tax Return Basics

SWASFAA Conference

November 8 – 10, 2006

What must FAAs know about Federal tax returns????

Federal Student Aid Handbook states “Financial Aid Administrators must have a fundamental understanding of relevant tax issues that can considerably affect the need analysis. (06-07 page AVG-101)

Required Verification Items from Tax Return

• Adjusted Gross Income

• U.S. Income Taxes paid

• Certain Untaxed Income and Benefits

FAAs should have a basic understanding of:

• Filing Requirements

• Filing Status• Personal Exemptions

• Implied Assets

FAAs are required to know…

• whether individual was required to file a federal tax return

• what the correct filing status should be

• that an individual cannot be claimed as an exemption by more than one person

Conflicting Information

• There are zero assets on the FAFSA yet there is business and/or investment income on the Tax Return

• Discrepant tax data such as incorrect filing status, incorrect number of personal exemptions, or failure to file when required are all considered conflicting information

• FAAs MUST resolve conflicting information before disbursing FSA funds

Conflicting Information (cont.)• “..a school must have an adequate internal

system to identify conflicting information – regardless of the source and regardless of whether the student is selected for verification..”

• “If you discover discrepancies after disbursing FSA funds, you must still reconcile the conflicting information and take appropriate actions under the specific program requirements.”

06-07 AVG-101

Who is required to file a tax return?

• To determine if a taxpayer is required to file a federal return, you need to know:– Marital status– Age– Gross Income

Who is required to file a tax return?

• Generally a federal tax return IS required when gross income equals or exceeds the taxpayer’s standard deduction plus personal exemptions.– Exception: Self employment net earnings > $400– Exception: Church employee income > $108.28, if church is

exempt from employer social security and Medicare taxes– Exception: Married filing separate taxpayer, if gross income

exceeds personal exemption ($3,200 in 2005)– Exception: Taxpayer received “advance” earned income credit

(EIC) payments from employer (box 9 on W-2) – Exception: Taxpayer received tip income that was not reported

to their employer

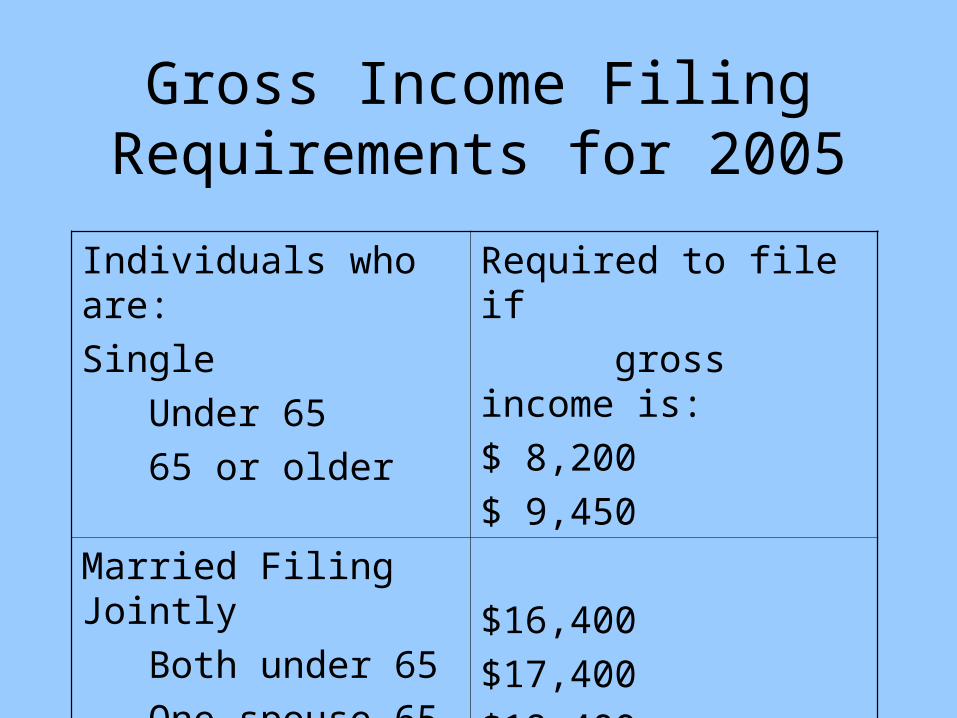

Gross Income Filing Requirements for 2005

Individuals who are:

Single

Under 65

65 or older

Required to file if

gross income is:

$ 8,200

$ 9,450

Married Filing Jointly

Both under 65

One spouse 65 +

Both 65 or older

$16,400

$17,400

$18,400

Gross Income Filing Requirements for 2005 (cont)

Married Filing Separately (any age) $ 3,200

Head of Household

Under 65

65 or older

$10,500

$11,750

Qualifying Widow(er)

With Dependent Child

Under 65

65 or older

$13,200

$14,200

Filing Requirements for Dependents*

• If parents (or someone else) can claim taxpayer as a dependent*, then taxpayer has different filing requirements (Generally cannot be considered a dependent* on someone else’s tax return if income is > $3,200 unless < 19 or full-time student < 24.)

• For dependents* the marital status, the age, and gross income determine if a return is required

Note: *IRS dependent is NOT the same as a Financial Aid dependent student

Filing Requirements for Dependents* (cont)

Single Dependents* (Under 65 & Not Blind) Must File a Return in 2005 if:

– Unearned income was more than $800– Earned income was more than $5,000– Gross income was more than the larger of:

• $800 or• Earned income (up to $4,750) + $250

Note: *IRS dependent is NOT the same as a Financial Aid dependent student

Filing Requirements for Dependents* (cont.)

Married Dependents* (Under 65 & Not Blind) Must File a Return in 2005 if:– Unearned income was more than $800– Earned income was more than $5,000– Gross income was at least $5 and spouse files a

separate return with itemized deductions– Gross income was more than the larger of:

• $800 or• Earned income (up to $4,750) + $250

Note: *IRS dependent is NOT the same as a Financial Aid dependent student

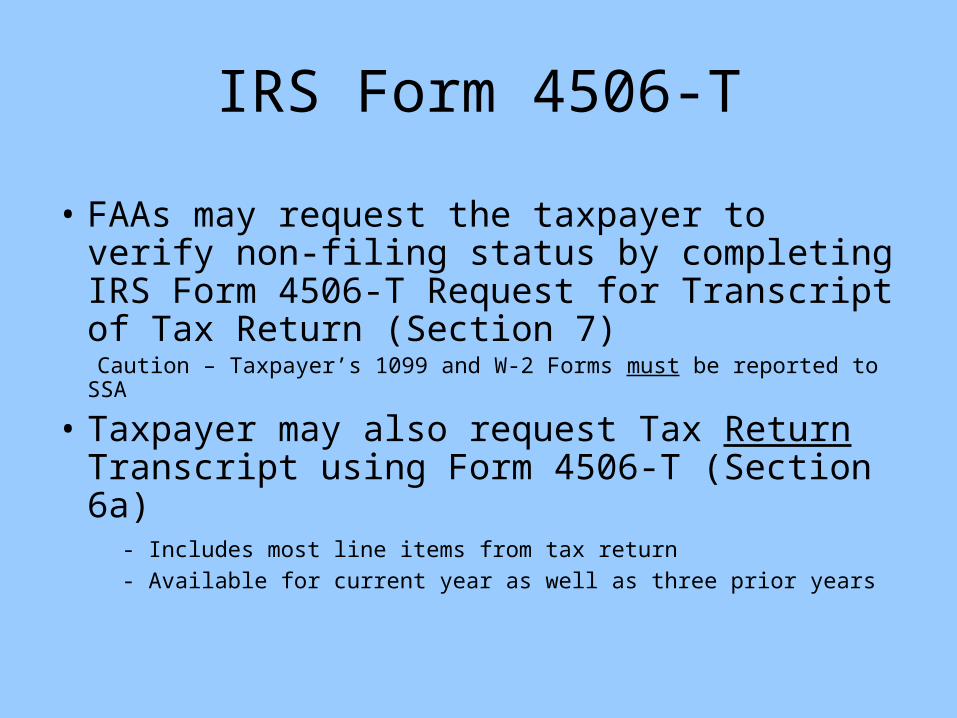

IRS Form 4506-T

• FAAs may request the taxpayer to verify non-filing status by completing IRS Form 4506-T Request for Transcript of Tax Return (Section 7)

Caution – Taxpayer’s 1099 and W-2 Forms must be reported to SSA

• Taxpayer may also request Tax Return Transcript using Form 4506-T (Section 6a)

- Includes most line items from tax return

- Available for current year as well as three prior years

Federal Tax Filing Status

• Single

• Married filing jointly

• Married filing separately

• Head of household

• Qualifying widow(er)

Federal Tax Filing Status (cont.)• Single

- Taxpayers who are legally separated or have final divorce decree

as of December 31 would file as Single (or Head of Household, if eligible)

• Married (as of December 31 of tax year) - Married taxpayers living together at the end of the year may file either:

- Married filing jointly, or - Married filing separately

- Same sex unions are not considered “married” on the FAFSA (Reference GEN 05-16)

- If Spouse dies during the year, taxpayer still considered married for the entire year for tax purposes.

Federal Tax Filing Status (cont.)• Married (cont.)

- Common Law Marriages are recognized in 16 states including Oklahoma and Texas. Generally to be considered “common law married” heterosexual couples must:

- cohabitate for a “significant (undefined) period of time”,- hold themselves out as married (refer to each other as

“my husband” or my wife” and/or file a joint tax return), AND

- intend to be married.

• Head of household- Taxpayer is unmarried or “considered unmarried” on the last day of

the year- Taxpayer paid more than half the cost of keeping up a home for

the year- Taxpayer had “qualifying child and/or relative” live in their home for

more than half the year (exceptions would include children away at school or parent(s) who met the support test.)

Federal Tax Filing Status (cont.)

• Head of Household (cont.)- A married taxpayer may file as Head of Household if they are

considered “unmarried” for tax purposes and meet other HOH eligibility requirements. Refer to IRS Pub.17

• Qualifying Widow(er) w/ Dependent Child- Taxpayer may be eligible to file as Qualifying widow(er) for two

years following spouse’s death if - eligible to file joint return when spouse was living

- taxpayer has child, step-child, foster child or adopted child for

whom they can claim an exemption- taxpayer paid more than half the cost of keeping up a home

that is the main home for the child for the entire year.

Married but Considered Unmarried for Tax Purposes

A married Taxpayer is considered “unmarried” for tax purposes on the last day of the tax year IF they meet ALL five (5) of the following tests:– Taxpayer files a separate return– Taxpayer paid more than half the cost of keeping up their home

for the tax year– Taxpayer’s spouse did NOT live in their home during the last 6

months of the tax year. Their spouse is considered to live in their home even if he/she is temporarily absent due to special circumstances.

– Taxpayer’s home was the main home for their child for more than half the year or the main home of a foster child for the entire year

– Taxpayer must be able to claim an exemption for the child (unless non-custodial parent is allowed to claim exemption using IRS Form 8332-”Release of Claim to Exemption for Child of Divorced or Separated Parents”)

“A legally married couple that is living together on December 31 can NEVER use head of household as a filing status. If they use head of household as their filing status, you have conflicting information”

NASFAA Student Aid Transcript “Discovering Tax Discrepancies” by James Briggs, 2005

Personal Exemption

• Only one personal exemption is allowed per person

- Schools must resolve situations where the student claimed his/herself as a personal exemption AND the parent claims the student as well. Either the parent or student must file an amended return.

Revenue Producing Assets

• Rental Properties, Oil/Gas Royalties, Partnerships, S-Corps – Schedule E

• Self Employment Income – Schedule C or Schedule C-EZ

• Stocks and Bonds – Dividend Income – 1040 Line 9a

• Capital Gains/Losses - Schedule D• Depreciation - Schedule 4562• Mutual Funds, Savings Accounts, Trusts

Assets• Property owned by the family with an

exchange value

• Required to report on the FAFSA- Cash, Savings, & Checking Accounts

- Investments

- Businesses (except Small Business Assets <100 employees GEN 06-05)

- Investment Farms

• Value as of the day the FAFSA was signed- Net Worth Reported (FMV minus debt owed)

- Partial Ownership of an Asset

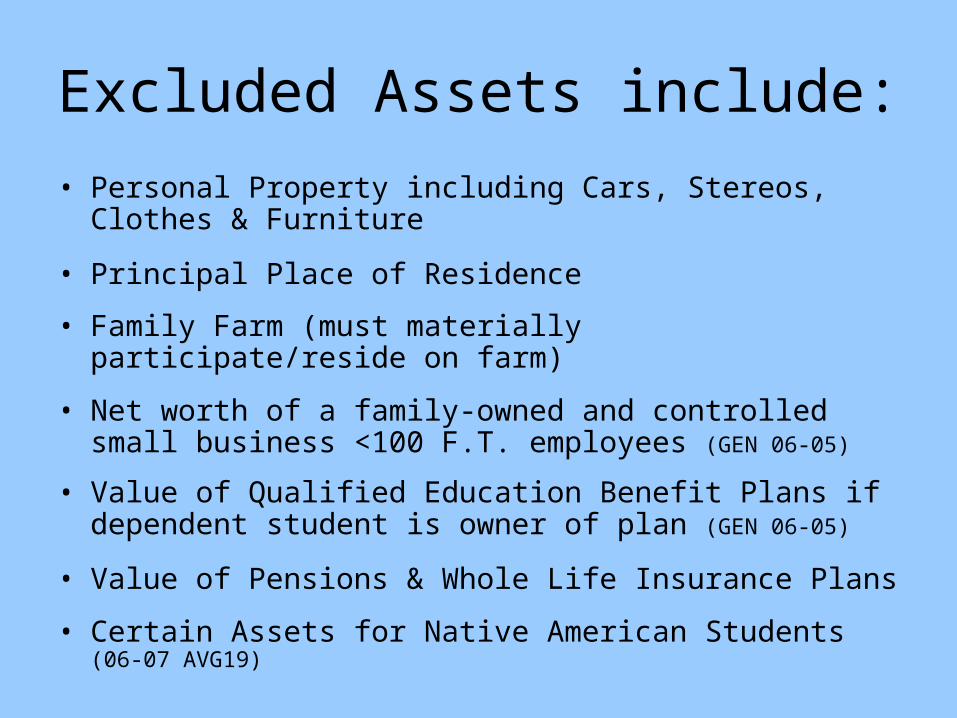

Excluded Assets include:

• Personal Property including Cars, Stereos, Clothes & Furniture

• Principal Place of Residence

• Family Farm (must materially participate/reside on farm)

• Net worth of a family-owned and controlled small business <100 F.T. employees (GEN 06-05)

• Value of Qualified Education Benefit Plans if dependent student is owner of plan (GEN 06-05)

• Value of Pensions & Whole Life Insurance Plans

• Certain Assets for Native American Students (06-07 AVG19)

Resolution of Conflicting Tax Information

“If an institution has reason to believe that any information on an application used to calculate an EFC is inaccurate, it shall require the applicant to verify the information that it has reason to believe is inaccurate.” 34 CFR 668.54(a)(3)

Resolution of Conflicting Tax Information

• Possible resolutions include:– Amended tax returns– Change of facts/Written explanation– Statement from IRS/tax preparer

• Resolution must be documented in the student’s file

Acceptable Tax Returns

• A copy of the original signed return (1040, 1040A, or 1040EZ (photocopy, fax, or digital image)

• A copy of the original unsigned return with the signature of the filer (at least one of the filers if a joint return)

• A tax form that has been completed to duplicate the filed return with at least one filer’s signature

Acceptable Tax Returns (Cont.)

• Electronic Return if it contains all the information normally provided on the IRS tax return with the filer’s signature (IRS Form 8453 is not acceptable)

• A copy of an IRS form with tax return information that the IRS mailed directly to your school (otherwise must be signed by one of the filers)

• TeleFile discontinued in 2005

Tax Preparer Signatures

• In lieu of the signature of the tax filer, the school may accept a return on which the tax preparer has stamped, typed, signed, or printed his/her name AND his/her SSN, EIN (Employer Identification Number) or PTIN (Preparer Tax Identification Number)

• “Tax Preparer’s Name” refers to an individual person’s name, not the name of a company or organization. For example, “H&R Block” would not be acceptable as a tax preparer’s name.

1040 Required?

• To determine if the student qualifies for the simplified need formula or auto zero EFC you must determine if the tax filer was REQUIRED to file a 1040 instead of a 1040A or 1040EZ

(See IRS Publication 17 “Which Form Should I Use?” pages 6 - 8)

• The maximum income to file a 1040A and 1040EZ have increased; the AGI limit for the simplified needs analysis has not changed

• If a 1040 was filed solely to claim an education tax credit the applicant may still eligible for the simplified formula or auto zero EFC

Simplified Needs Test

• To be eligible:– AGI less than $50,000; and– Student/Spouse (Independent) or Parent (Dependent)

were not required to file or were eligible to file 1040A or 1040EZ, or

– Student/Spouse (Independent) or Parent/Student (Dependent) received means-tested benefits in previous 12 month period (DCL GEN 06-05)

• Asset information NOT considered in the EFC calculation• States & Schools may require asset information for their

own aid programs

Automatic Zero EFC

• Parent/s (Dependent) or Student/Spouse (Independent) had adjusted gross income of $20,000 or less; and

Either• Parent/s (Dependent) or Student/Spouse

(Independent) were not required to file or were eligible to file 1040A or 1040EZ, or

• Parent/Student (Dependent) or Student/Spouse (Independent) received means-tested benefits in the previous 12-month period (GEN 06-05)

Resources

• 2006-2007 Federal Student Aid Handbook http://ifap.ed.gov

• IRS Publication 17 - Federal Income Tax for Individuals www.irs.gov or (800) 829-3676

• IRS Form 4506-T

• Student Aid Transcript, The Tax Detective Discovering Tax Discrepancies

Questions???

Deborah McIntyre

Tulsa Community College

Email: [email protected]

Telephone: (918) 595-7284