tax effects of coronavirus (covid-19) and cares act · tax effects of coronavirus (covid-19) and...

TRANSCRIPT

Tax Effects of Coronavirus (Covid-19)and CARES Act

Congress and IRS Open the Floodgates

Bradley Burnett, J.D., LL.M. (Taxation)

BradleyBurnettTaxSeminars.com

Disclaimer

• This presentation and accompanying course materials are designed to provide accurate and authoritative information as to the subject matter covered

• Neither the sponsor(s), distributor, publisher author, nor presenter, by and through this presentation, is rendering legal, accounting or other professional service

• This presentation and accompanying course materials does not create an attorney-client or accountant-client relationship

• If legal advice or other expert advice is required, the services of a competent professional person should be sought

2© 2020 Bradley Burnett Tax Seminars, Ltd.03/30/20

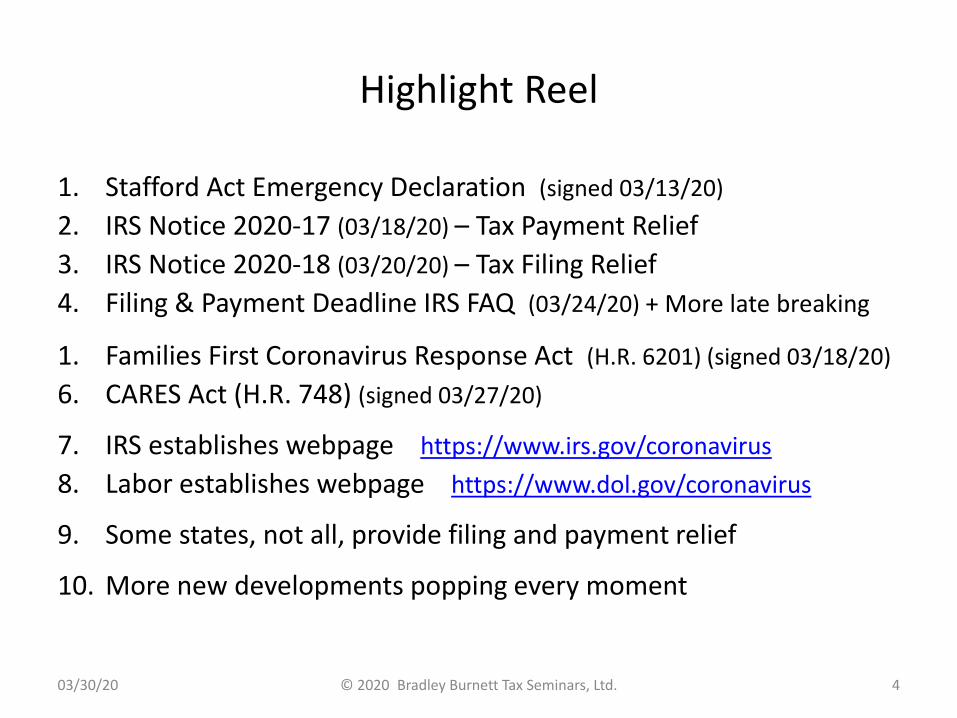

Highlight Reel

© 2020 Bradley Burnett Tax Seminars, Ltd. 303/30/20

Highlight Reel

1. Stafford Act Emergency Declaration (signed 03/13/20)

2. IRS Notice 2020-17 (03/18/20) – Tax Payment Relief

3. IRS Notice 2020-18 (03/20/20) – Tax Filing Relief

4. Filing & Payment Deadline IRS FAQ (03/24/20) + More late breaking

1. Families First Coronavirus Response Act (H.R. 6201) (signed 03/18/20)

6. CARES Act (H.R. 748) (signed 03/27/20)

7. IRS establishes webpage https://www.irs.gov/coronavirus

8. Labor establishes webpage https://www.dol.gov/coronavirus

9. Some states, not all, provide filing and payment relief

10. More new developments popping every moment

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 4

Covid-19Shakes Things Up

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 5

Coronavirus and Social Media

• Puyllup, Washington Police Department Facebook message:

“Due to local cases of ♯COVID-19, PPD is asking all criminal activities and nefarious behavior to cease

We appreciate your anticipated cooperation in halting crime & thank all criminals in advance

We will certainly let you know when you can resume your normal criminal behavior

Until then … ♯washyourhands & #behaveyourself “

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 6

Stafford Act

• Stafford Act Emergency Declaration (signed 03/13/20)

1. President Trump declares National Emergency, invoking Stafford Act

2. Stafford Act, if federal disaster declared, permits IRS to postpone certain tax compliance deadlines (IRC §7508A(a))

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 7

Breaking News

• April 15 filing deadline has been postponed to July 15

1. “No extensions (generally) need be filed on April 15

2. If more time needed, file extension on July 15” (per IRS)

- Source: Treasury Secretary Steven Mnuchin tweet (03/20/20)

followed by Notice 2020-18 (03/20/20) and IR-2020-58 (03/21/20)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 8

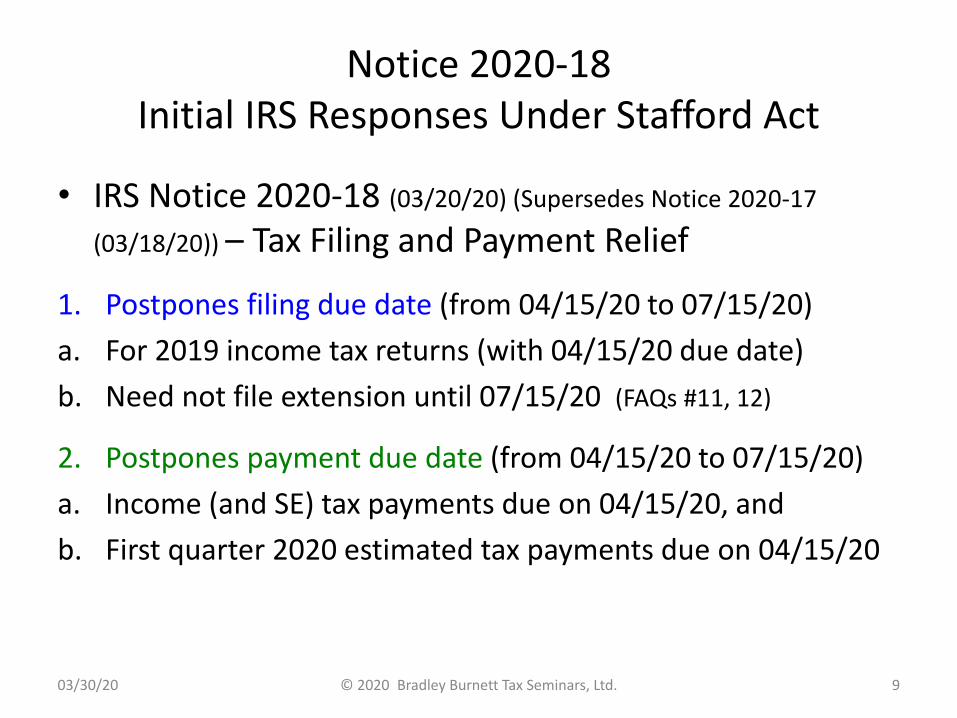

Notice 2020-18Initial IRS Responses Under Stafford Act

• IRS Notice 2020-18 (03/20/20) (Supersedes Notice 2020-17

(03/18/20)) – Tax Filing and Payment Relief

1. Postpones filing due date (from 04/15/20 to 07/15/20)

a. For 2019 income tax returns (with 04/15/20 due date)

b. Need not file extension until 07/15/20 (FAQs #11, 12)

2. Postpones payment due date (from 04/15/20 to 07/15/20)

a. Income (and SE) tax payments due on 04/15/20, and

b. First quarter 2020 estimated tax payments due on 04/15/20

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 9

To Defer Until 07/15/20You Need Not Be Sick (FAQ #2)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 10

Polling Question 1

• If you think Coronavirus hasn’t changed life much in the U.S. today, just wait for tomorrow

A. True. Tomorrow you’ll be more stir crazy than today.

B. False. Baseball season will begin tomorrow.

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 11

Notice 2020-18Filing Deadlines Extended (or Not)

Type Filing Deadline Extended Through 07/15/20

Filing DeadlineNot Extended

Overall Any return originally due on 04/15/20

Any return not originally due on 04/15/20

Individual Form 1040 (calendar yr end) Form 1040 (non-calendar yr end)

Fiduciary Form 1041 (calendar yr end) Form 1041 (non-calendar yr end)

C Corp Form 1120 (calendar yr end) Form 1120 (non-calendar yr end)

Exempt Org

Form 990 (or 990-T) (if 04/15/20 original due date)

Form 990 (or 990-T) (if non-04/15/20 original due date)

Partnership Form 1065 (only 01/31 yr end) Form 1065 (non-01/31 yr end)

S Corp Form 1120S (only 01/31 yr end) Form 1120S (non-01/31 yr end)

Gift &GSTT

Form 709 -

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 12

Source: FAQs #1, 3 Source for 709: Notice 2020-20 (03/27/20)

Notice 2020-18What If Extended Due Date Is 04/15/20?

• Special rule for fiscal year end (FYE) tax returns

- If federal income tax return for fiscal year ending during 2019 is due on 04/15/20, whether that is original due date or due date on extension, due date postponed to 07/15/20 (IRS FAQ #4)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 13

Notice 2020-18Filing Deadlines NOT Extended

Type Filing Deadline Extended Through 07/15/20

Filing DeadlineNot Extended (FAQ #5)

Overall Any return originally due on 04/15/20

Any return not originally due on 04/15/20

Employment Tax No (FAQ #6) Forms 941, 940

Excise Tax No (FAQ #5) Various

Info Returns No (FAQ #10) Forms W-2, 1099, etc.

Estate and Estate GSTT Returns

No (FAQ #7) Forms 706, 706-GS, etc.

Split-Interest Trust Info Return

No (FAQ #5) Form 5227

‘Ee Benefit Plans No (FAQ #5) Form 5500 series

Refund claim for 2016 Income Tax

No (FAQ #22) 1040X, Amended 1041, 1120X

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 14

Transfer Tax ReturnsEstate Not Extended, Gift Extended

1. Estate and estate related GSTT tax returns NOT automatically extended until 07/15/20

- Must timely file Form 4768 to extend estate tax return Form 706, 706-A, 706-NA or 706-QDT

2. Gift and related GSTT tax returns NOT automatically extended until 07/15/20 (Notice 2020-20 (03/27/20))

a. Gift tax Form 709 & related payment extended to 07/15/20

b. File Form 8892 by 07/15/20 to extend Form 709 to 10/15/20

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 15

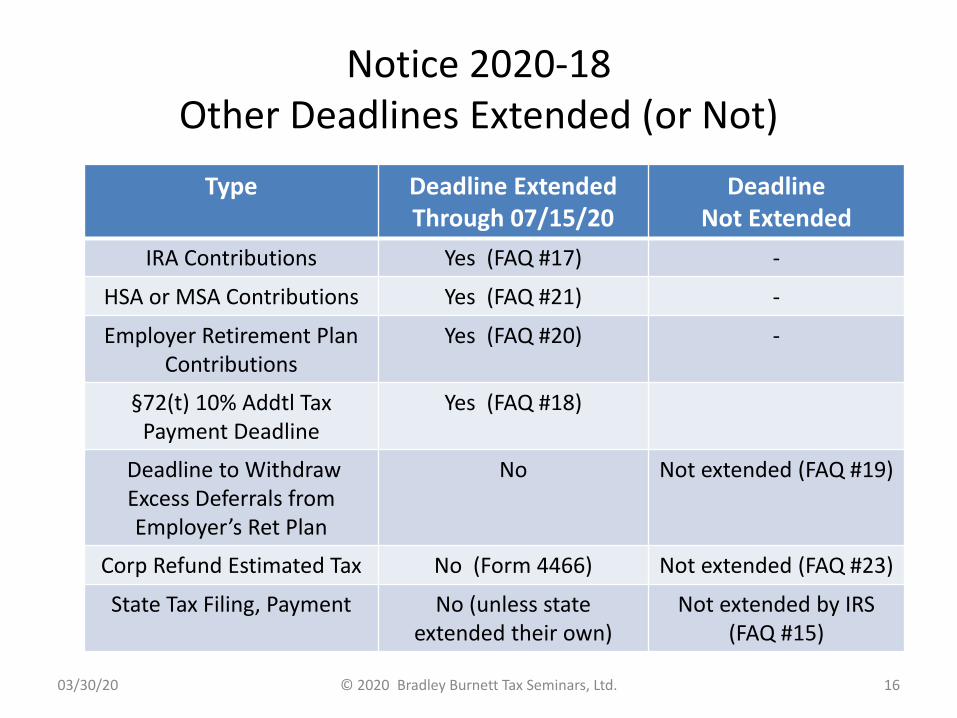

Notice 2020-18Other Deadlines Extended (or Not)

Type Deadline Extended Through 07/15/20

DeadlineNot Extended

IRA Contributions Yes (FAQ #17) -

HSA or MSA Contributions Yes (FAQ #21) -

Employer Retirement Plan Contributions

Yes (FAQ #20) -

§72(t) 10% Addtl Tax Payment Deadline

Yes (FAQ #18)

Deadline to Withdraw Excess Deferrals from Employer’s Ret Plan

No Not extended (FAQ #19)

Corp Refund Estimated Tax No (Form 4466) Not extended (FAQ #23)

State Tax Filing, Payment No (unless state extended their own)

Not extended by IRS(FAQ #15)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 16

I’m Free!!

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 17

Should We Put OffGathering Income Tax Info?

• “We don’t want to wait for extensions to process your tax info

- “Waiting just makes it harder to request info and as more and as more people take COVID leave it will only get harder and harder to get hold of people and request info

- “When employees return to work everyone will be behind

- “The government may even make my own employees unavailable so please take time to send us information while it is more readily available” David Frizzell, CPA

“A duty dodged is like a debt unpaid; it is only deferred, and we must come back and settle the account at last.” Joseph Fort Newton (1876-1950)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 18

Polling Question 2

• Since 2019 Forms 1040 need not be filed until July 15, it is best to mindlessly not extend until July 15

A. True – Throw caution to the wind

B. Not true – Absolutes are not always best

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 19

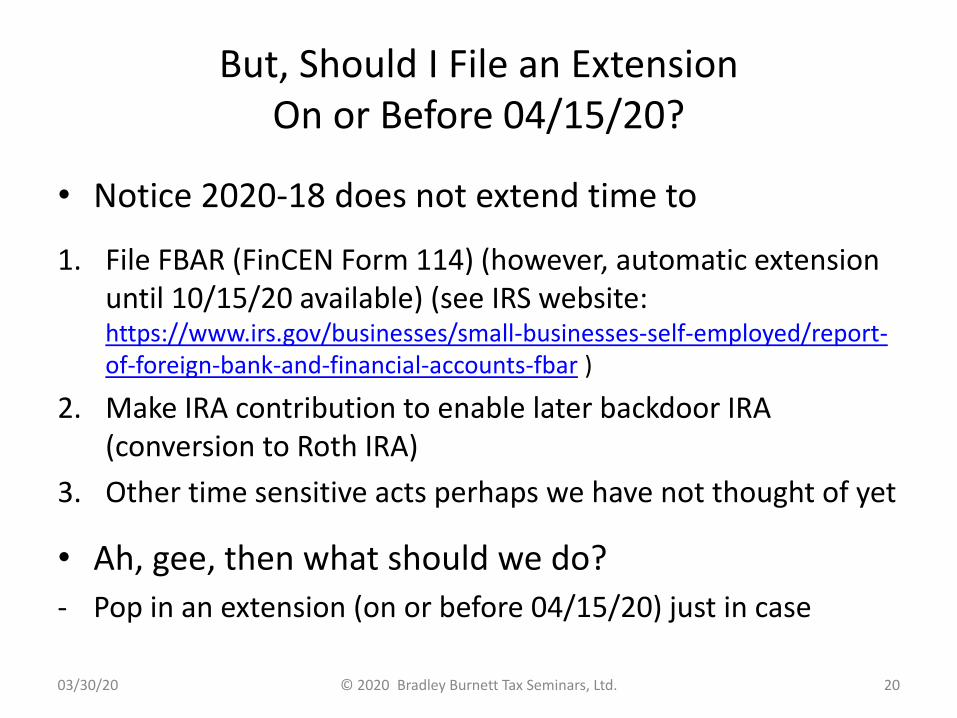

But, Should I File an ExtensionOn or Before 04/15/20?

• Notice 2020-18 does not extend time to

1. File FBAR (FinCEN Form 114) (however, automatic extension until 10/15/20 available) (see IRS website: https://www.irs.gov/businesses/small-businesses-self-employed/report-of-foreign-bank-and-financial-accounts-fbar )

2. Make IRA contribution to enable later backdoor IRA (conversion to Roth IRA)

3. Other time sensitive acts perhaps we have not thought of yet

• Ah, gee, then what should we do?

- Pop in an extension (on or before 04/15/20) just in case

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 20

State TaxFiling Deadlines

• State Closings, Filing Delays and Extensions re: Coronavirus

1. Forbes online article (03/12/20) (continuously updated)

https://www.forbes.com/sites/kellyphillipserb/2020/03/12/heres-what-we-know-about-extensions-other-tax-relief-due-to-coronavirus-concerns/#42a4fb1d3412

2. AICPA State Tax Filing Guidance Coronavirus (03/26/20 7am ET)

https://www.aicpa.org/content/dam/aicpa/advocacy/tax/downloadabledocuments/coronavirus-state-filing-relief.pdf?mod=article_inline (67 pages)

3. Check your state’s website for the latest

https://www.taxadmin.org/state-tax-agencies

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 21

State TaxFiling Deadlines*

Extensions Thru 07/15/20

Extensions ThruOther Dates

No Income Tax Extension Relief

Various Other Extensions

AL, AZ, AR, CA, CO, CT, DC, DE,

GA, IL, IN, KS, KY, LA, ME, MD, MA, MI, MN, MO, MT, NE, NM, NY, NC, ND, OH, OK, OR,PA, SC, TN, UT,

WV, WI

IA 07/31, ID06/15, OR 04/30,

MS 05/15, VA 06/01, WA 06/15,

PR 06/15

AK, FL, HI, ME, NV, NH, NJ, RI, SD,

TX, VT, WY

IL Estates (30 days), IA (07/31), LA Excise (05/20), MI Sales, Use &

W/H (04/20), NM W/H (07/25), SC Various (06/01),

WA Various

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 22

* Current through 03/30/20 7:00 am. Check your state’s website for the latest.** Not official

When to File Early

1. Q: Which clients are served best by filing early?

A: Clients expecting a refund

2. Distinction: File early vs. pay early

a. Any qualifying taxpayer can file early, yet still pay later (IRS

FAQ #13)

b. If filed early and scheduled payment for 04/15/20, payment must be cancelled and rescheduled for 07/15/20 (IRS FAQ #14)

c. If seeking fastest “recovery check*” (CARES Act) (later slide), file 2019 early to get into queue (*based on 2019 return income)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 23

Tax Payment Due Dates

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 24

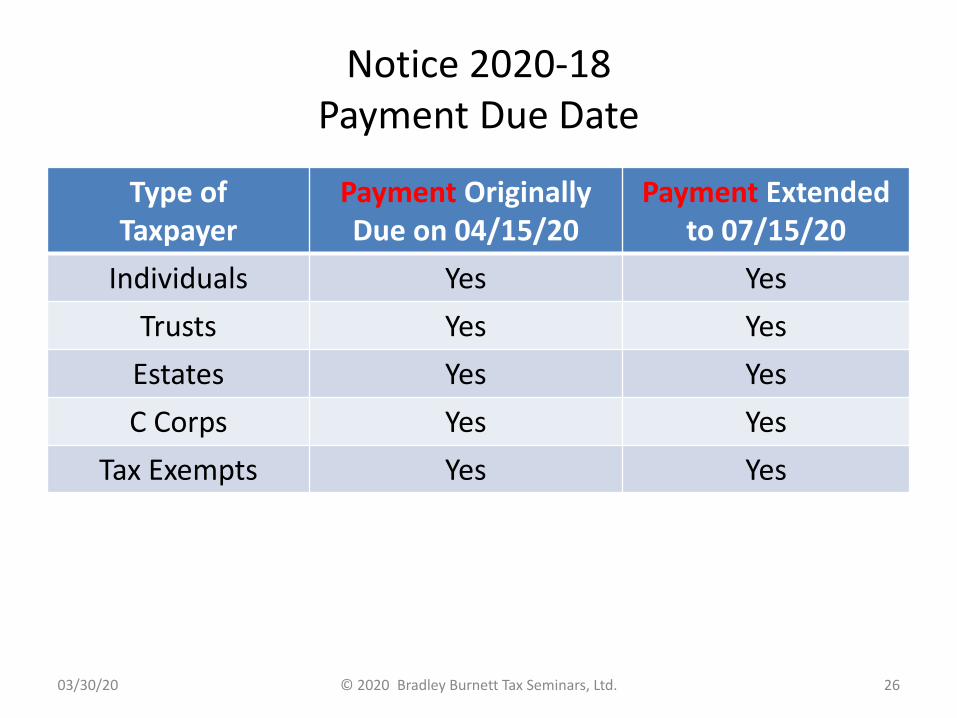

Notice 2020-18Payments Due

• Notice 2020-18 (§III) – Any person w/ a federal income tax payment due on 04/15/20 is affected by COVID-19

1. Payment due date extended (from 04/15/20) to 07/15/20

- If tax already paid, no effect

2. Waiver (until 07/15/20) of statutory additions for

a. Interest

b. Penalties

c. Additions to tax

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 25

Notice 2020-18Payment Due Date

Type of Taxpayer

Payment Originally Due on 04/15/20

Payment Extended to 07/15/20

Individuals Yes Yes

Trusts Yes Yes

Estates Yes Yes

C Corps Yes Yes

Tax Exempts Yes Yes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 26

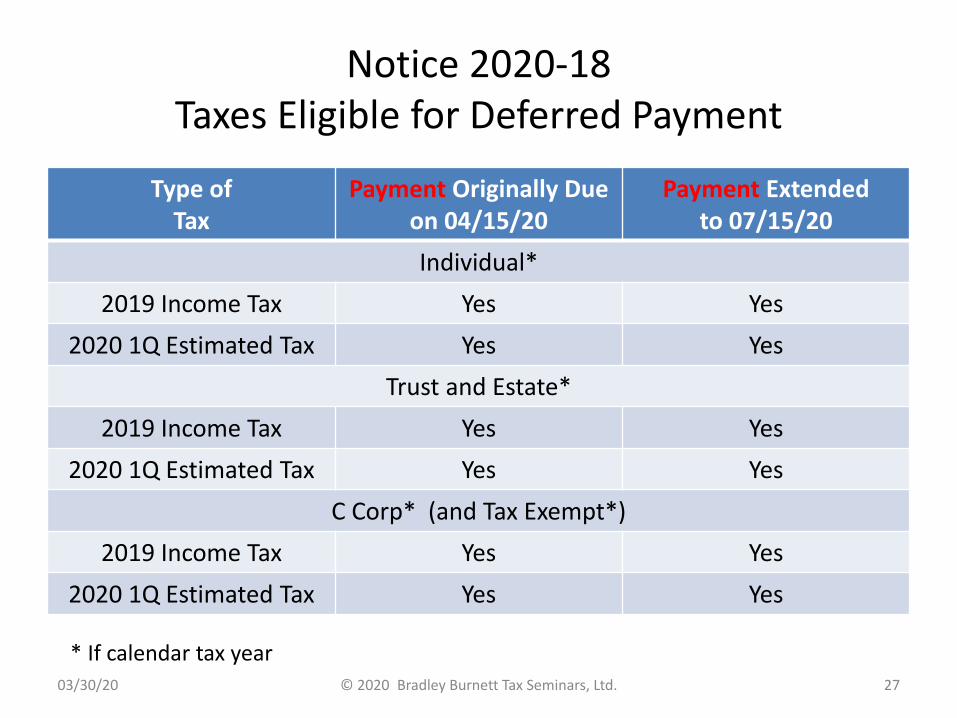

Notice 2020-18Taxes Eligible for Deferred Payment

Type of Tax

Payment Originally Due on 04/15/20

Payment Extended to 07/15/20

Individual*

2019 Income Tax Yes Yes

2020 1Q Estimated Tax Yes Yes

Trust and Estate*

2019 Income Tax Yes Yes

2020 1Q Estimated Tax Yes Yes

C Corp* (and Tax Exempt*)

2019 Income Tax Yes Yes

2020 1Q Estimated Tax Yes Yes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 27

* If calendar tax year

Avoiding Underpayment of Estimated Tax Penalty for 2020

Amount Due 1 Q 2 Q 3 Q 4 Q Total

General Rule

25% of total

25% of total

25% of total

25% of total

100% of last year’s tax*

Annualized May be < 25%

May be < 25%

May be< 25%

May NOT be < total

100% of last year’s tax*

Notice 2020-17

Not re-quired until 07/15/20

Req’d by 06/15/20 (FAQ #16)

Required by

09/15/20

Required by

01/15/21

100% of last year’s tax*

* 90% of current year tax (if less than 100% of last year’s tax)

* 110% of last year’s tax (if last year’s AGI > $150,000)

No penalty if underpayment < $1,000

No penalty if casualty, disaster or other unusual circumstance and penalty against equity and good conscience

Penalty = IRS §6621 underpayment rate x each installment for period of shortfall

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 28

Notice 2020-18Taxes Eligible (and Not)

• Individual taxes eligible for deferred payment

1. Income tax

2. Self employment (SE) Tax

• Individual taxes perhaps not? eligible for deferred payment

1. Household employment taxes (Schedule H)

2. Excise taxes (e.g., Form 5329 re: IRA mishaps)

3. AMT

4. Repayment of advance premium tax credit

- “No extension is provided in this notice for the payment or deposit of any other type of federal tax … .” (Notice 2020-17, § III)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 29

Notices 2020-17 and 2020-18Amount Eligible for Deferred Payment

Type of Tax

Amount Originally Due on 04/15/20

Payment Extended to 07/15/20

Individual*

2019 Income Tax $1M Entire amount Yes

2020 1Q Estimated Tax $1M Entire amount Yes

Trust and Estate*

2019 Income Tax $1M Entire amount Yes

2020 1Q Estimated Tax $1M Entire amount Yes

C Corp* (and Tax Exempt*)

2019 Income Tax $10M Entire amount Yes

2020 1Q Estimated Tax $10M Entire amount Yes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 30

* If calendar tax year

Shelter or NotIf Outside of 2020-18 Relief?

• Are there other ways to avoid penalty and interest if (within time period 04/15/20 – 07/15/20) you’re not within Notice 2020-18 relief?

1. Yes for penalties – Reasonable cause* abatement

- See IRM Penalty Handbook https://www.irs.gov/irm/part20/irm_20-001-001r

2. No for interest – Unless delay IRS’s fault (it won’t be)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 31

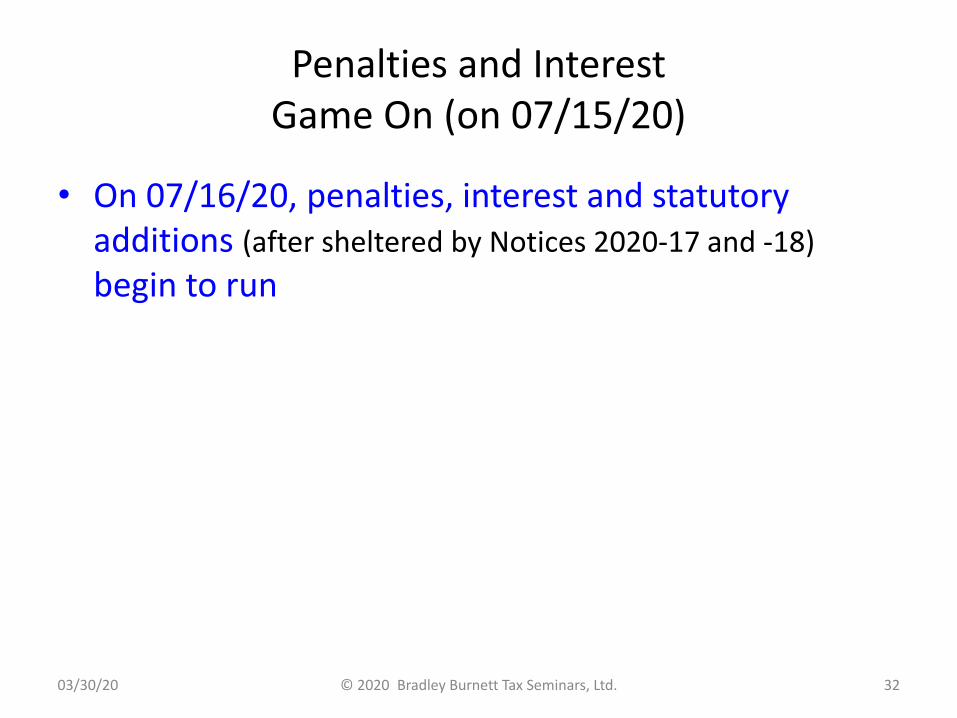

Penalties and InterestGame On (on 07/15/20)

• On 07/16/20, penalties, interest and statutory additions (after sheltered by Notices 2020-17 and -18)

begin to run

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 32

Does IRS Filing and Payment Relief Apply toPersons Outside of U.S.?

1. Any person w/ fed income tax payment or tax return due 04/15/20 is affected by COVID-19 emergency for purposes of Notice 2020-18 (§III) relief (Affected Taxpayer) (FAQ #1)

a. “Person” includes individual, trust, estate, partnership, association, company or Corp per §7701(a)(1)

b. For Affected Taxpayer, due date for filing fed income tax returns and making fed income tax payments due April 04/15/20 is automatically postponed to 07/15/20

2. Form 1040 Instructions (01/08/20): These tps may file later:

a. Serving in, or in support of, U.S. armed forces in combat zone or contingency operation may file later

b. U.S. citizen or resident alien (or military duty) outside U.S. & Puerto Rico

c. Not clear as to how Notice 2020-18 affects these

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 33

These Little Guys Spread FastAnd So Do Government Covid-19 Tax Giveaways

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 34

IRS Operationsin Face of Coronavirus

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 35

IRS Operations in Face of Coronavirus

Service Before Coronavirus During Coronavirus

Taxpayer Assistance Centers

Open Closed

Face-to-face service Open Closed

Process tax returns Yes Yes

Issue refunds Yes Yes

Average refund time 21 days (per IRS.gov) 21 days (per IRS.gov)

Fastest refund _ For fastest refund, file electronically and select direct deposit method

Special coronavirus info page

No Yes https://www.irs.gov/coron

avirus

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 36

IRS Operationsin Face of Coronavirus

Service Before Coronavirus During Coronavirus

Practitioner Priority Service Phone Lines (Effective 03/27/20)

Practitioner Hotline Open Closed (Indefinitely)

E-Services Help Desk Open Closed (Indefinitely)

Filing Info Return Electronically Line

Open Closed (Indefinitely)

ACA Info Return Line Open Closed (Indefinitely)

Other Services (Effective 03/27/20)

Income Express Verification Service (IVES) – New Requests

Open Closed (Indefinitely)

Transcript Delivery System Open Open

EITC Verification Reviews Operational No denials thru 07/15/20

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 37

IRS Operations in Face of CoronavirusCollections, Exams and Appeals

Service Before Coronavirus During Coronavirus

New Field, Office & Correspondence

Exams

Operational In-person meetings re: IRS exams suspended. IRS will continue

exams remotely. Tps encouraged to respond to info requests if able

In-Person Meetings Operational Suspended

Unique Situations Operational If tp desires to pursue in-person exam meeting(s), IRS may agree if

in best interest of both

General requests for info

Operational IRS encourages tps to respond to IRS correspondence requesting

additional info if possible

Non-Filers Enforcement Enforcement

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 38

IRS Operations in Face of CoronavirusInstallment Agreements

Service Before Coronavirus During Coronavirus

Installment Agreements

Existing Installment Agreements

Usual practices Payments due 04/01/20 thru 07/15/20 suspended

New Installment Agreements

Open Application availableGo for it

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 39

IRS Operations in Face of CoronavirusOffers in Compromise

Service Before Coronavirus During Coronavirus

Offers in Compromise

Pending OICs Usual practices Tps have ‘til 07/15/20 to supply requested additional info

IRS won’t close any OIC prior to 07/15/20 w/o tp’s consent

OIC Payments Usual practices Payments on accepted OICs suspended until 07/15/20

Effect of Delinquent Income Tax Return

Usual practices IRS won’t default OIC for late 2018 return ‘til > 07/15/20

New OIC Applications

Usual practices Application available

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 40

IRS Operations in Face of CoronavirusCollections, Exams and Appeals

Service Before Coronavirus During Coronavirus

Non-Filers Enforcement Enforcement

AutomatedLiens and Levies

Operational Suspended thru 07/15/20

Field Collection Liens and Levies

Operational Suspended thru 07/15/20, except for high income tps &

others where warranted

Statute of Limitations (S/Ls)

Operational IRS will continue to take steps to protect S/Ls, but if S/L blowing in 2020, IRS unlikely to pursue

until at least 07/15/20

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 41

IRS Operations in Face of CoronavirusIDRs (Info Document Requests)

Service Before Coronavirus During Coronavirus

LB&I Issuance of IDRs Operating Operating

LB&I Receipt of IDRs Operating Operating

LB&I IDR Enforcement Procedures

Operating (Actively Enforced)

Temporarily suspended for tps unable, due to Covid-19,

to timely respond to IDR

Exception: In IRS manager’s discretion, IDR enforcement will continue when interests of tax administration warrant

(e.g., short statutes, listed transactions and fraud)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 42

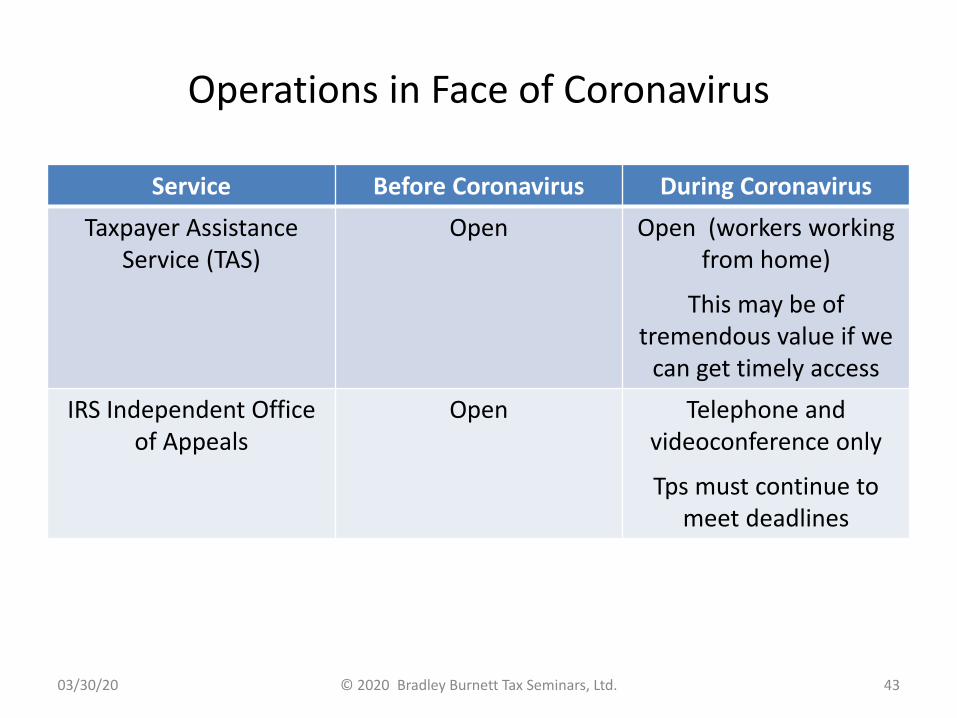

Operations in Face of Coronavirus

Service Before Coronavirus During Coronavirus

Taxpayer Assistance Service (TAS)

Open Open (workers working from home)

This may be of tremendous value if we

can get timely access

IRS Independent Office of Appeals

Open Telephone and videoconference only

Tps must continue to meet deadlines

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 43

Coronavirus and Health Savings Accounts

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 44

IRS Cuts Break to HDHPs and HSAsfor Covid-19 Related Testing

• High-deductible health plans (HDHPs) can pay for COVID-19 related testing and treatment without jeopardizing their status, regardless of whether plan’s deductible met (IR 2020-54,

Notice 2020-15 (03/11/20))

1. Individuals covered by such a plan will not fail to be eligible individuals under §223(c)(1)

2. Thus, may contribute to HSA

3. Does not otherwise modify previous guidance re: requirements to be an HDHP

- Vaccinations continue to be preventive care under §223(c)(2)(C)

for HDHP purposes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 45

CARES Act Cuts Break to HDHPs and HSAs for Telemedicine Without Cost Sharing

• CARES Act removes block from increased use of telemedicine to encourage participants to self isolate

1. Non-HSA plans may waive co-pays, coinsurance and deductibles w/o endangering their status

2. Prior to CARES, HSAs could not so waive ‘til deductible met

3. CARES Act creates safe harbor for telemedicine services provided in absence of a deductible

a. Opens up deductible-free telemed services whether re: Covid-19 or not

b. Change applies to plan years beginning on or < 12/31/21

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 46

CARES Act Cuts Broad Tax Breakfor Over the Counter Meds

• CARES Act renders over the counter meds tax deductible, regardless of prescription

1. Prior law: ACA limited deduction for over the counter meds to those prescribed by doctor

2. CARES Act: Over the counter meds (and menstrual care products) reimburseable tax-free by HSAs, HRAs and FSAs

a. Retroactive to 01/01/20

b. Plan docs may need to be amended

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 47

Coronavirus and Affordable Care Act

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 48

Coronavirus ACA / Health Insurance Issues

• Under ACA affordability rules, large employers* face penalties if insurance not affordable to employees

1. One affordability safe harbor based on expected W-2 wages

2. If wages drop for unpaid leave, insurance could become unaffordable

• Large employer status may also be affected

1. 50 employee threshold for large employer* status

2. With many ‘ees terminated or placed on leave, employer may lose large employer status in 2021

- Would reduce ACA coverage and reporting requirements

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 49

Coronavirus ACA / Health Insurance Issues

1. ACA requires large employers must continue to offer coverage during “stability periods”

a. Employees (meeting 30 hrs/week threshold) deemed eligible for health insurance during “measurement period” must remain eligible during entire subsequent stability period

b. Holds true even if hours reduced, including for Covid-19

2. Small employers (< 50 full-time ‘ees) need not maintain coverage under ACA

- But watch out for policy, employment agreement or other

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 50

Coronavirus ACA / Health Insurance Issues

3. How best to collect premiums, if any, during business closure?a. Payroll deductions from paid employeesb. If unpaid leave, 3 options- ‘Ee prepays - ‘Ees pay as you go - Float it for ‘ee, collect later

4. COBRAa. If coverage continues, no COBRA issuesb. Loss of coverage, provide COBRA noticec. If COBRA no applies, watch out for state mini-COBRA laws

5. HIPPA – Beware privacy obligations – Arguably, however, can tell other ‘ees if an ‘ee has Covid-19

Excellent article: https://www.mondaq.com/unitedstates/Employment-and-HR/906674/Employee-Benefits-In-The-Time-Of-COVID-19

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 51

CoronavirusRetirement Plans

1. 401(k) plan deferrals

a. If ‘ee paid during business closure, ‘er should timely w/hold deferrals and timely submit

b. If ‘ee not paid during closure, 401(k) contributions and deferrals cease as there is no underlying comp under plan

2. Entirely discretionary contributions may be suspended

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 52

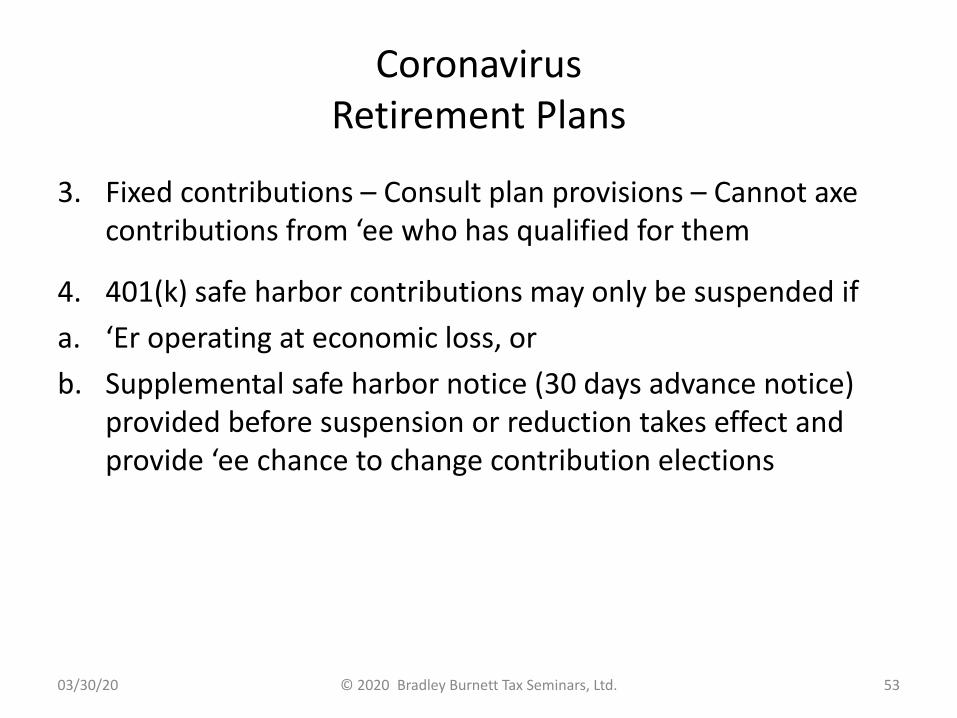

CoronavirusRetirement Plans

3. Fixed contributions – Consult plan provisions – Cannot axe contributions from ‘ee who has qualified for them

4. 401(k) safe harbor contributions may only be suspended if

a. ‘Er operating at economic loss, or

b. Supplemental safe harbor notice (30 days advance notice) provided before suspension or reduction takes effect and provide ‘ee chance to change contribution elections

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 53

Coronavirus.govGuidelines for America

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 54

Employees Who Work From HomeTax Considerations

• Issues: Company and worker in different locations

1. General rule: Apply payroll tax in location employee works

a. Do inventory – Where have workers scattered to?

- Example: Company in Philadelphia, PA. Worker in NJ or DE.

- Example: Company in NY. Worker in London, England.

b. Will states, localities relax rules? None yet

c. Payroll tax exposure could jump up and bite you

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 55

Employees Who Work From HomeTax Considerations

• Issues: Company and worker in different locations

2. Does employee working in another state expose worker to income tax filing requirement / liability in that state?

- Same question if ‘ee working outside U.S.

3. Does employee working in another state expose company to that state’s income tax?

- Same question if ‘ee working outside U.S.

4. Does employee working in another state (country) expose company to registration / legal liability in that location?

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 56

Employees Who Work From HomeTax Considerations

• Issues: Company and worker in different locations

5. Reimbursing worker for out-of-pocket costs at home office

a. Cash pmts w/o an accounting will be payroll taxable income

b. Tax-free if accounted for and reimbursed under properly structured and operated accountable plan

c. Office supplies can be bought and shipped to ‘ee by company

6. Home office expenses (e.g., depreciation)

a. Not deductible if unreimbursed

b. For reimbursements (for most, this dog won’t hunt – Likely fail exclusive use test and other requirements)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 57

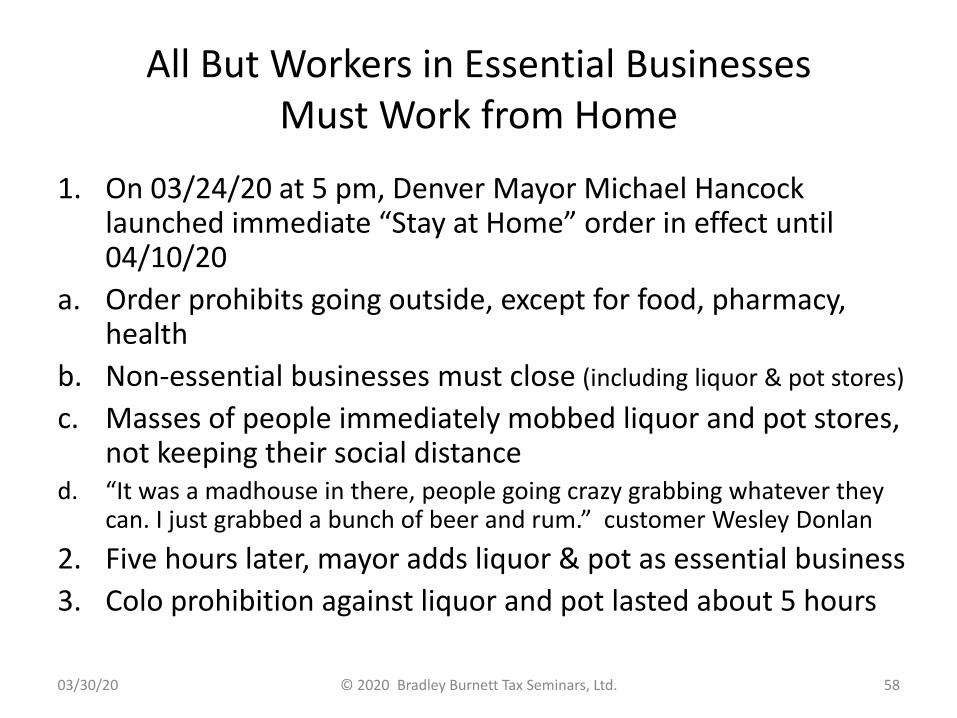

All But Workers in Essential BusinessesMust Work from Home

1. On 03/24/20 at 5 pm, Denver Mayor Michael Hancock launched immediate “Stay at Home” order in effect until 04/10/20

a. Order prohibits going outside, except for food, pharmacy, health

b. Non-essential businesses must close (including liquor & pot stores)

c. Masses of people immediately mobbed liquor and pot stores, not keeping their social distance

d. “It was a madhouse in there, people going crazy grabbing whatever they can. I just grabbed a bunch of beer and rum.” customer Wesley Donlan

2. Five hours later, mayor adds liquor & pot as essential business

3. Colo prohibition against liquor and pot lasted about 5 hours

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 58

Let’s Wash Our Hands

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 59

Families First Response ActH.R. 6201

1. H.R. 6201 Legislative historya. Signed into law by President on 03/18/20

b. Contains

1) Emergency Paid Sick Leave Act

2) Emergency Family and Medical Leave Expansion Act

3) Tax Credits for Paid Sick and Paid Family and Medical Leave ($105 billion)

2. Applies to: a) government agencies and private employers w/ < 500 employees; and b) self-employed individuals

2. Duration

a. Effective beginning on 04/01/20 (Notice 2020-21 (03/27/20))

b. Ending on 12/31/20

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 60

Families First Response Act1st Round of Guidance

• IR-2020-57 (03/20/20) – Treasury, IRS and Labor outline plan to implement mandated Coronavirus paid leave for workers and related tax credits

1. Highlights mandate for employers to make sick and family leave payments

2. Projects scope and mechanics of payroll tax credit

3. Prophesizes timing of implementation

- Employer may get 30 day non-enforcement period for reasonable and good faith compliance efforts

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 61

Families First Response ActH.R. 6201 (Signed 03/18/20)

Sick Pay Family & Medical Leave

Applies To Government or Businesses w/ < 500

Employees

Government or Businesses w/ < 500 Employees

PossibleExemption

- Business < 50 ’ees if 1. school closing or child care unavailable, and 2. jeopardize viability of business as going concern

Required Pay sick pay for 2 weeks Pay family and medical leave for 12 weeks* *(1st 2 weeks (10 days) may be unpaid) (after 10 days, must pay for 10 weeks)

Full Time ‘Ee 80 hours (10 days) Employee must be on payroll for at least 30 days

Part Time ‘Ee

Typical # of hours worked in 2 week period

-

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 62

Families First Response ActH.R. 6201 (Signed 03/18/20)

Sick Pay Family & Medical Leave

EligibleEmployee

Ee’ unable to work (or telework) due to:1. Federal, state or local quarantine or

isolation order2. Self quarantining under advice of

healthcare provider due to Covid-19 concerns

3. Obtaining diagnosis due to Covid-19 symptoms

4. Assisting a family member quarantined under order or advice of healthcare provider

5. Caring for child if school closed or child care provider closed or unavailable due to Covid-19

6. Addtl categories added by HHS

Ee’ unable to work (or telework) due to:1. Caring for child if school

closed 2. Caring for child if child care

provider closed or unavailable due to Covid-19

Employees who have not been employed 30 days are excluded

Healthcare providers and emergency responders may be excluded

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 63

Families First Response Act (FFRA)H.R. 6201 (Signed 03/18/20)

Sick Pay Family & Medical Leave

Amount Full compensation up to $511/day ($5,110/’ee cap)

2/3 of compensation up to $200/day ($10,000/’ee cap)

Amount If to care for family member w/ coronavirus or child after school

or day care closing, then $200/day* ($2,000/’ee cap)

-

Relation to Existing

Programs

FFRA sick leave is in addition to sick leave already offered by

employer (whether required by law or not)

-

Credit 100% of mandatedsick pay (see above)

+ Employer’s health insurance plan expenses (per ‘ee)

100% of mandated family and medical leave pay (see above)+ Employer’s health insurance

plan expenses (per ‘ee)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 64

Families First Response ActH.R. 6201 (Signed 03/18/20)

Sick Pay Family & Medical Leave

Mechanics of Credit

Offsets against FIT,employee FICA and HI* and

employer FICA and HI

Offsets against FIT,employee FICA and HI* and

employer FICA and HI

Credit Refundable

Any credit > employment tax due is refundable

Any credit > employment tax due is refundable

How Refunded Treasury will pay cash within 2 weeks (IR 2020-57)

Treasury will pay cash within 2 weeks (IR 2020-57)

Income Tax Effect

Credit does not reduce income tax deduction for payroll tax, but must be included in income

Credit does not reduce incometax deduction for payroll tax, but

must be included in income

Effect on §45S Credit

Reduces wages for §45S credit for paid family and medical leave

Reduces wages for §45S credit for paid family and medical leave

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 65

* Statute does not allow immediate access to trust fund taxes, but IR 2020-57 does

Polling Question 3

• Families First Coronavirus Response Act credits are refundable (beyond an employer’s actual payroll tax liability) within certain limits

A. Yes, you can take that to the bank

B. No, you’ll have to go hire more people to get the benefit

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 66

Sick Pay for Quarantine

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 67

Paid Sick LeaveIf Employee’s Health on Ropes

1. If employee unable to work because ‘ee:

a. Isolated or quarantined due to Covid-19; or

b. Experiencing symptoms and seeking medical diagnosis,

then

c. ‘Ee entitled to regular pay, subject to $511/day, $5,110 aggregate limit

Example: Mona Lisa’s usual pay is $600/day. She’s being quarantined for Covid-19. She’s entitled to 10 days of sick pay at $511/day ($5,110 max).

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 68

School’s Out for Summer

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 69

Paid Sick LeaveIf Caring for Another

2. If employee unable to work (including unable to telework) because ‘ee is caring for individual:

a. Who is quarantined, or

b. At home due to school or daycare closures,

then

c. ‘Ee entitled to 2/3 of regular pay, subject to $200/day ($2,000 aggregate cap)

Example: The lovely child’s school has been cancelled for the year. Parent’s pay is usually $270/day ($67,500/yr). $270 x 2/3 = $180/day sick pay for 10 days = $1,800. This is below the $2,000 aggregate cap.

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 70

Family and Medical Leave

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 71

Family and Medical LeaveExample: Day Care Dries Up

1. FMLA expanded to give employees (on payroll for at least 30 days) the right to take up to 12 weeks of leave to care for:

a. Child of ‘ee under age 18

b. If school or daycare not operational by reason of Covid-19

2. First 10 days may be unpaid

3. After 10 days, ‘er must pay ‘ee at no less than 2/3 of usual pay, subject to max of $200/day, $10,000 aggregate

Example: Parent in photo has a whole pile of kids normally in day care. Day care center shuts down over Covid-19. Parent bails out at work to take care of kid. Parent’s usual pay is $450/day. 2/3 x $450 = $300. Family leave pay = $200/day x 10 weeks. $10,000 aggregate.

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 72

Tax Credits for BOTH Paid Sick and Paid Family (and Med) Leave

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 73

Tax Credits for BOTH Paid Sick and Paid Family (and Med) Leave

1. When do sick and family leave payments (and, thus, tax credit) begin?

a. As early as 04/02/20

b. 30 day non-enforcement period for good faith compliance

2. THEREFORE,

a. 1Q 2020 Form 941 appears unaffected by payroll tax credit

b. 2Q 2020 and 2 later quarters (3Q and 4Q 2020) it’s game on

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 74

Tax Credits for Paid Sick andPaid Family and Medical Leave

Example: Employer ABC Co. pays $5,000 in sick leave and and is otherwise required to deposit $8,000 in payroll taxes

1. ‘Er could use up to $5,000 of the $8,000 of taxes it was going to deposit to make qualified leave payments

2. ‘Er only required to deposit remaining $3,000 on its next regular deposit date

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 75

Tax Credits for Paid Sick andPaid Family and Medical Leave

Example: Employer DEF Co. paid $10,000 in sick leave and was required to deposit $8,000 in taxes

1. ’Er may use entire $8,000 of taxes to make qualified leave payments, and

2. May file a request for an accelerated credit for the remaining $2,000

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 76

Self Employed Income Tax Credit

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 77

Self Employed SE (Income) Tax Credit

• Sick leave and family leave credit for self employed

1. Credit against Form 1040 SE tax

- Will reduce estimated tax payments

2. Eligibility similar to that of employees

3. Credit for 100% of daily SE income for self care ($511/day cap)

4. 66.7% if caring for family member or child w/ school or day care closed ($200/day cap)

5. 10 day limit for sick leave, 50 day limit for family leave

6. Based on period beginning 04/01/20 and ending 12/31/20

7. Treasury must provide guidance as to documentation self-employed must submit to claim credit

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 78

Families First Response ActLabor Law Stuff

1. Employers required to post appropriate notices

2. Severe penalties for interfering w/ an employee’s rights

3. Affected businesses should begin immediately to implement newly required sick pay and family leave policies

4. More to follow – Keep an eye on https://www.dol.gov/coronavirus

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 79

What If One Is Merely Suspected of Having Coronavirus?

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 80

Polling Question 4

• Is a person eligible for coronavirus related sick leave if someone on the elevator hears them sneeze?

A. No, the eligibility criteria are more strict than that

B. Yes, sneezing on the elevator is smoking gun evidence

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 81

What If Business Closed or Workers Laid Off?

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 82

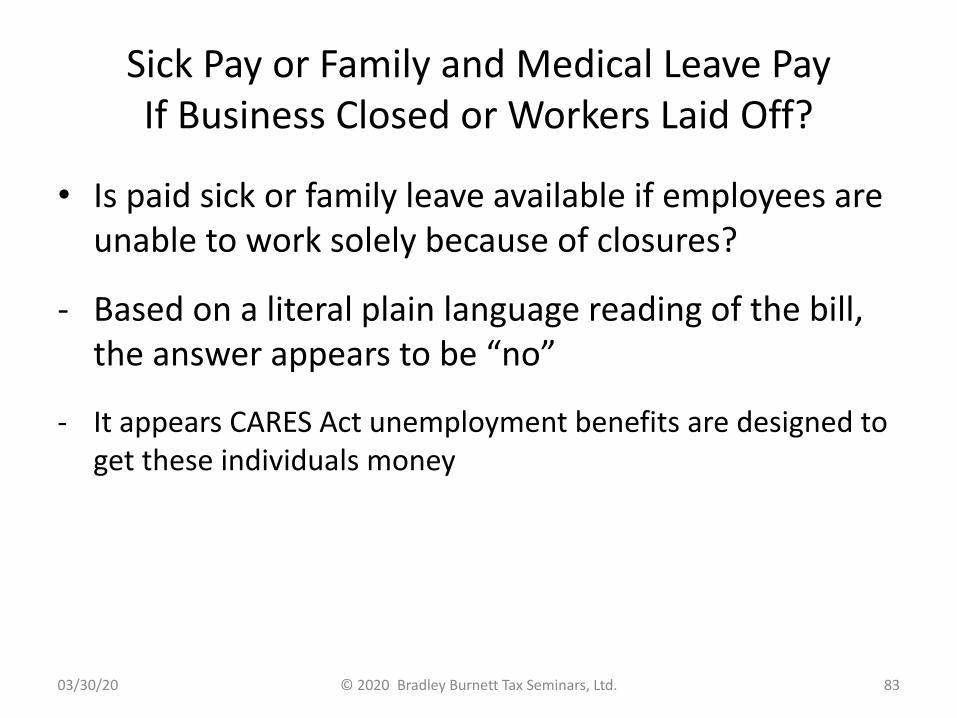

Sick Pay or Family and Medical Leave PayIf Business Closed or Workers Laid Off?

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 83

• Is paid sick or family leave available if employees are unable to work solely because of closures?

- Based on a literal plain language reading of the bill, the answer appears to be “no”

- It appears CARES Act unemployment benefits are designed to get these individuals money

Coronavirus Tax (and Labor) LawA Supersized Combo Meal

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 84

CARES Act

1. Coronavirus Aid, Relief & Economic Security Act (H.R. 748)

(Signed 03/27/20)

2. Repeal TCJA NOL changes – 80% rule and “no carryback” rule

- Carryback of 2018, 2019 and 2020 NOLs back 5 years

3. §163(j) – Increase business interest expense deduction limit from 30% to 50% (for 2019 & 2020) & use 2019 income

4. Relax §461(l) excess business loss rule

5. Make QIP (qual. improvement prop) §168(k) bonus eligible

6. Payroll Protection Program loan forgiveness

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 85

Coronavirus Aid, Relief & Economic Security Act CARES Act (H.R. 748)

7. Penalty free access to virus related financial hardships

8. Expanded deduction for charitable contributions

9. Other TCJA technical corrections

10. Direct cash (recovery rebate) payments to lower income individuals

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 86

How Do These Laws Help UsHave Money to Buy Food?

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 87

Rebate Checksfor Individuals

MFJ Non-MFJ Head of Household

Amount $2,400 $1,200 $1,200

Plus per child $500 $500 $500

Phaseout Rate 5% 5% 5%

Phaseout Range $75,000 –99,000

$150,000 –198,000

$112,500 –146,500

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 88

(CARES Act §2201)

Rebate Checksfor Individuals

Topic Detail

Credit Based On AGI from 2019 1040 if already filed -or-2018 return if 2019 1040 not filed -or-

2019 Form SSA-1099 if not filed 2018 or 2019 1040

If Entitled To, But Did Not Receive

Refundable credit against 2020 income taxMight happen if no 2019 income, but 2020 income

If Not Entitled To, But Did Receive

Taxpayer responsible to pay it backNo current mechanism for payback

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 89

Rebate Checksfor Individuals

Topic Detail

Best Way To Get Money Fast

Supply IRS with direct deposit info on 2019 1040If no direct deposit, IRS will mail check to address on

most recently filed tax return

Eligibility Cannot be nonresident alien or estate or trust

Dependent of Another

Not entitled to rebate check

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 90

Rebate Checksfor Individuals

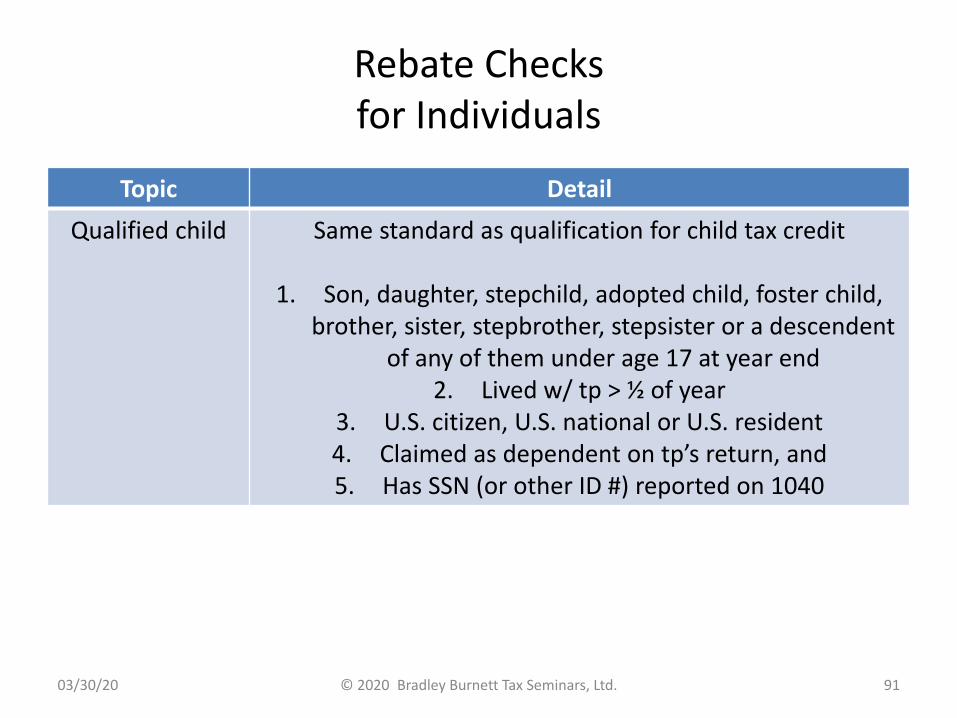

Topic Detail

Qualified child Same standard as qualification for child tax credit

1. Son, daughter, stepchild, adopted child, foster child, brother, sister, stepbrother, stepsister or a descendent

of any of them under age 17 at year end2. Lived w/ tp > ½ of year

3. U.S. citizen, U.S. national or U.S. resident4. Claimed as dependent on tp’s return, and5. Has SSN (or other ID #) reported on 1040

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 91

Charitable ContributionsAbove-the-Line

• Above-the-line deduction for non-itemizers for up to $300 cash charitable contribution to public charities (excluding private foundations, supporting organizations or donor advised funds (DAFs)) in 2020 (CARES Act §2202)

- Charitable contributions from prior years not eligible

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 92

Polling Question 5

For 2020, an above-the-line deduction is allowed for cash charitable contributions whether a taxpayer itemizes or not

A. True – This is going to be great

B. False – That’s an overblown fish story

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 93

Charitable ContributionsModification of Limitations

• Temporary suspension of limit on deductions for cash contributions (CARES Act §2205)

1. Individuals – For cash charitable contribution to public charities (excluding private foundations, supporting organizations or donor advised funds (DAFs)) in 2020, individuals may deduct:

a. 100% of AGI remaining after factoring in all other current year charitable contributions subject to AGI limitations

b. Any excess cash contributions not deducted in 2020 carried forward subject to 60% limit for succeeding 5 years

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 94

Charitable ContributionsModification of Limitations

• Temporary suspension of limit on deductions for cash contributions (CARES Act §2205)

2. C Corps – May deduct cash charitable contributions up to 25% of taxable income (up from 10%) in 2020 to public charities (other than supporting organizations and donor advised funds)

3. Food Inventory – Enhanced deduction for contributions of food for C Corps for 25% (up from 15%)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 95

Losses

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 96

Non-C Corp Excess Business LossesNew §461(l)

• For tax years beginning after 12/31/17 and before 01/01/26,

excess business losses of a taxpayer (other than a corporation) not allowed for the tax year

1. Excess business loss (EBL) = Excess of aggregate deductions attributable to trades or businesses, over sum of aggregate gross business income or gain, plus a threshold amount

2. Threshold amount $250,000* non-MFJ, $500,000* MFJ

3. Disallowed amount = Excess business loss (EBL)

4. EBL becomes NOL carryover under §172

* $255,000 (2019), $510,000 (2019), $259,000 (2020), $518,000 (2020)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 97

Excess Business LossesDeferral of Effective Date

• CARES postpones effective date of §461(l) excess business loss (EBL) limitation from years beginning after 12/31/17 to years beginning after 12/31/20 (CARES Act §2304)

1. If 2018 or 2019 return filed reporting EBL, amended return (possibly generating a refund) available

2. Technical correction: In EBL computation, wages not business income

3. Technical correction: In EBL computation, capital gains only included to extent of lesser of net cap gain attributable to trade or business or capital gain net income

4. On Form 1065 Schedule K-1 Box 20 Code AH and Form 1120S Sched. K-1 Box 17 Code AC, all reporting §461(l) info, disclosures not needed for 2018, 2019 and 2020

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 98

TCJANet Operating Losses

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 99

TCJA NOL Tweaks

• Net Operating Loss (NOL) % of Application1. Prior law – NOLs generated before 2018 continue to offset 100%

of taxable income (TI) 2. TCJA – NOLs generated in years beginning after 2017 may only

offset 80% of TI of year NOL carried to

• Carrybacks and carryforwards1. Prior law – NOLs carry back 2 years, forward 20- However, §172(b)(1) allowed for different loss carryback periods for

casualty, theft, farmers

2. TCJA – For NOLs generated in years beginning > 2017a. No more NOL carrybacks (except 2 years for farmers*)b. NOLs indefinitely carry forward

© 2020 Bradley Burnett Tax Seminars, Ltd. 10003/30/20

CARES Act (CARES Act §2303)

NOL Tweaks and More Tweaks

1. Repeals 80% limit for years beginning before 01/01/20

a. Helps C Corps that generated NOLs in 2018 or 2019 or will generate NOL in 2020

b. May help or hurt non-C Corp depending on rate brackets

2. For NOLs arising in years > 12/31/17 and < 01/01/21, NOLs allowed as carrybacks to each of 5 years prior

a. Helps C Corps that generated NOLs in 2018 or 2019 (or 2020) get refunds at up to 35% rate if amended returns filed

b. May help or hurt non-C Corp depending on rate brackets

c. May waive NOL carryback (for 1 yr after 03/27/20)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 101

TCJA - §163(j) Business Interest Expense Limit

© 2020 Bradley Burnett Tax Seminars, Ltd. 10203/30/20

TCJA §163(j) (New Regime)

• §163(j)(1) – For years beginning > 12/31/17, deduction for business interest expense (BIE) cannot exceed sum of:

1. “Business interest income” (BII);

2. 30% of “adjusted taxable income” (ATI*); and

3. Floor financing interest expense (vehicle dealers) (§163(j)(9))

• However, exempt small business or excepted business not subject to limit

* ATI cannot be < zero

© 2020 Bradley Burnett Tax Seminars, Ltd. 10303/30/20

CARES ActTweaks to §163(j)

1. For years beginning in 2019 and 2020, CARES increased 30% of ATI limit to 50% (CARES §2306)

- Can elect out of 50% rule

2. Special rule for partnerships – 50% of 2019 excess business interest expense allocated by partnership to partner deductible by partner in 2020 not subject to §163(j) limit

- Partnerships and partners can elect for this rule not to apply

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 104

§168(k)Qualified Improvement Property (QIP)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 105

§168(k)Qualified Improvement Property (QIP)

• Qualified improvement property = Improvements to interior of commercial building placed in service after building placed in service

a. Not residential

b. Not exterior

c. Not expansion

d. Not structural

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 106

Qualified Improvement Property (QIP)Timeline

Qualified Improvement Property (QIP)

2015 2016-2017 2018 and Later

39 Year Property N/A Yes Yes

Bonus Eligible N/A Yes No (BotchedAttempt)

Elect Out if Don’t Want

N/A Yes N/A

15 Year Property N/A No No (BotchedAttempt)

§179 Eligible N/A No Yes

Elect In if Want N/A No Yes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 107

Qualified Improvement Property (QIP)Timeline (CARES §2307)

Qualified Improvement Property (QIP)

2015 2016-2017 2018 and Later

39 Year Property N/A Yes Yes

Bonus Eligible N/A Yes No (BotchedAttempt) Yes

Elect Out if Don’t Want

N/A Yes N/A Yes

15 Year Property N/A No No (BotchedAttempt) Yes

§179 Eligible N/A No Yes

Elect In if Want N/A No Yes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 108

QIP15 Year Bonus Eligible Retroactive to 2018

1. CARES renders QIP 15 year property (20 year ADS) retroactive to property placed in service > 12/31/17 (CARES

§2307)

2. Amended returns apparently available 2018 and later (?)

3. Accounting method changes also available (guidance soon)

4. Partnerships under new Centralized Partnership Audit (CPAR) regime file AAR with adjustments taken into account in 2020

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 109

Delay in Deposit of Employment Taxes

• Delay in Deposit of Employment Taxes (Act §2302)

1. May delay deposit of employer share of FICA

2. Taxes eligible for deferral = Taxes incurred from 03/27/20 through 12/31/20

3. Half required to be deposited by end of 2021

- Other half required to be deposited by end of 2022

4. Individual may delay deposit of one half of SE tax

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 110

Polling Question 6

It is a terrifically great idea to wait to pay your payroll taxes (even if you can) under the CARES Act and invest the money into something like the stock market

A. No, not even in your wildest dreams

B. Go for it, no guts, no glory

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 111

Penalty Free Access to Retirement Funds

• Penalty Free Access to Retirement Funds (Act §2202(a))

1. CARES Act permits individuals affected by coronavirus to take year 2020 distributions from tax favored employer sponsored retirement funds and IRAs of up to $100,000

a. No 10% §72(t) additional tax

b. Income spread over 3 years at recipient’s election

2. Individual may repay over 3 year period

- Any amount repaid treated as rollover

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 112

Increased Limits on LoansFrom Retirement Plans

• Increased Limits on Loans From Retirement Plans for Individual Affected by Coronavirus (Act §2202(b))

1. Increases loan dollar limit to $100,000

2. Loan may be up to 100% of participant’s vested accrued benefit

3. Repayment terms relaxed

a. New loans issued for 6 years (up from 5)

b. Existing loans may be suspended for 1 year, extended for 1 year and reamortized

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 113

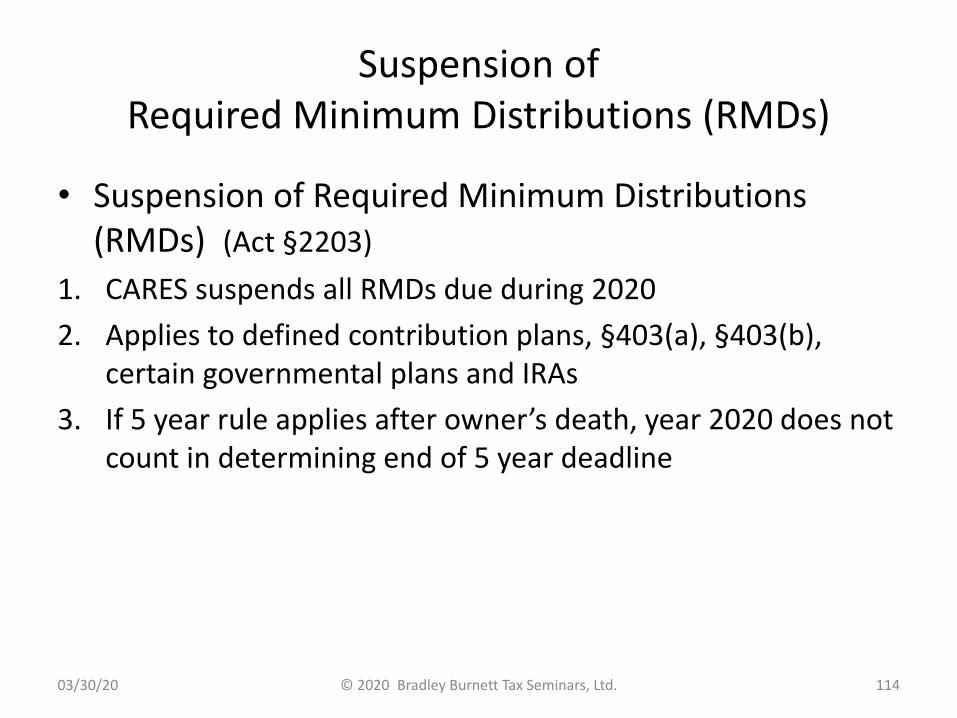

Suspension of Required Minimum Distributions (RMDs)

• Suspension of Required Minimum Distributions (RMDs) (Act §2203)

1. CARES suspends all RMDs due during 2020

2. Applies to defined contribution plans, §403(a), §403(b), certain governmental plans and IRAs

3. If 5 year rule applies after owner’s death, year 2020 does not count in determining end of 5 year deadline

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 114

Employee Retention Credit

1. Employee retention credit for employers subject to closure due to coronavirus who continue to pay employees wages during closure (Act §2301)

2. Credit = 50% of wages to each ‘ee ($10,000/’ee cap)

3. Credit offsets against ‘er share of FICA, excess refunded

4. To be eligible, must carry on business in 2020, and either:

a. Ordered by a government to shut down or reduce operations due to Covid-19; or

b. Suffered significant decline in business during a calendar quarter in 2020

5. Businesses and tax exempts qualify, but not government

6. Not available if SBA loan forgiveness (see later slides)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 115

Loans

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 116

Payroll Protection Program

• Loan program to any business, non-profit, veterans org or tribal business with 500 or < employees (Act §§1102 and 1106)

1. Designed to keep workforce together

2. Covered period 02/15/20 – 06/30/20

3. Self employed qualify

4. Restaurants w/ not > 500 ‘ees/location qualify

5. May be forgiven if used to pay payroll

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 117

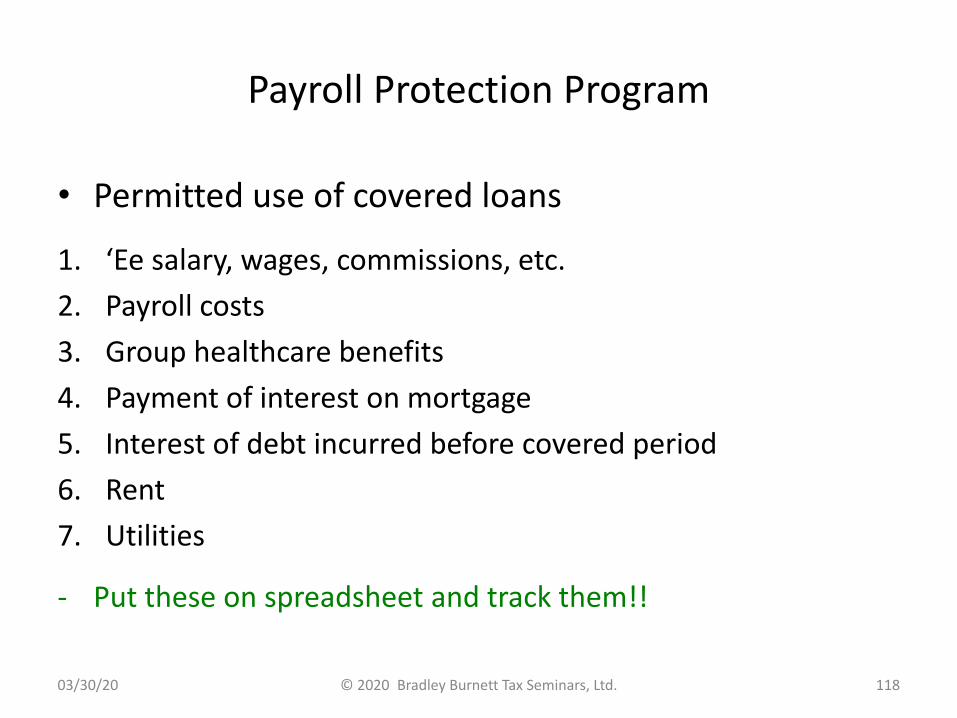

Payroll Protection Program

• Permitted use of covered loans

1. ‘Ee salary, wages, commissions, etc.

2. Payroll costs

3. Group healthcare benefits

4. Payment of interest on mortgage

5. Interest of debt incurred before covered period

6. Rent

7. Utilities

- Put these on spreadsheet and track them!!

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 118

Payroll Protection Program

• Payroll costs include

1. Salary, wages, commissions, etc.

2. Paid leave

3. Tips

4. Healthcare payments

5. Retirement benefit payments

6. Some independent contract labor

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 119

Payroll Protection Program

• Payroll costs do not include

1. Comp of individual employee in excess of $100,000 annual salary (prorated for covered period)

2. Qualified sick leave or family leave pay for which credit allowed under Families First Coronavirus Response Act

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 120

Payroll Protection Program

• Loan cap = Lesser of

1. $10M, or

2. Computed factor x 2.5

Computed factor = Average monthly payroll + mortgage payments + rent payments + payments on debt incurred within 1 year period before date on which loan made

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 121

Payroll Protection ProgramLoan Particulars

1. Loans nonrecourse – Except if proceeds used for unauthorized purpose*

2. No personal guarantee or collateral required

3. No requirement that loan not available elsewhere

4. MAKE SURE APPLICATION OF LOAN PROCEEDS ARE A VERY CLEAR MATCH TO PERMITTED USE

5. Good faith certification required

* Operating loss funded by loan may not be deductible right away – Since nonrecourse, §465 at-risk, §752 basis or S Corp basis rules may not allow basis allocation or current writeoff

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 122

Payroll Protection ProgramGood Faith Certification Required

• Good Faith Certification Required

1. “Funds will be used to retain workers, finance payroll expenses, make mortgage, rent and utility payments”

2. Current uncertainty makes loan necessary to support ongoing operations

3. For how long? Is 6 months cash flow enough? Longer?

4. Exact language of certification needed to be crafted

5. AICPA working on guidance

6. CPA need not certify good faith

7. Take this extremely seriously – We don’t want perjury

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 123

Payroll Protection ProgramGeneral Terms

1. Interest rate – During covered period, covered loan interest rate not to exceed 4%

2. Payment deferment – 6 to 12 month deferment includes principal, interest and fees

3. Origination fees – Lender reimbursed by SBA

4. Forgiveness of portion of loan available

5. Remaining balance after forgiveness guaranteed by SBA

- Max maturity 10 years from date loan forgiveness applied for

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 124

Payroll Protection ProgramLoan Forgiveness

• Principal (not interest) forgiven in amount equal to following costs incurred during covered period (02/15-

06/30/20):

1. Wages, etc.

2. Payroll costs

3. Mortgage interest

4. Rent

5. Utilities

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 125

Payroll Protection ProgramLoan Forgiveness

• Loan forgiveness amount reduced if salaries and wages are reduced

1. Forgiveness reduced by amount of reduction of salaries and wages of any employee in excess of 25% during covered period, compared to most recent full quarter

2. Excludes employees with annualized pay > $100,000

3. Exemption from loan forgiveness reduction for employees rehired w/in 30 days of 03/27/20

- Can rehire workers fast to get back into good graces of payroll protection program

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 126

Payroll Protection ProgramLoan Forgiveness Taxability

• Loan Forgiveness Taxability (Act §1106)

1. Any amount forgiven does not have to be paid back

2. Any amount forgiven is excluded from gross income

3. However, related payroll expense is deductible

- This is incredible!!

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 127

Polling Question 7

Payroll protection program loans may be forgiven income tax-free if conditions are met

A. Yes, and glory hallelujah

B. No, don’t even think about it

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 128

Mutually Exclusive Pick Only One

• Only one available

1. Loan Forgiveness

2. Employee Retention Credit

3. Delay and Deposit of Employment Taxes

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 129

Cyber Security Grim Reaper

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 130

2020 IRS Form W-12 PTIN ApplicationQuestion 12 Data Security Responsibilities

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 131

This question asks if PTIN applicant is aware of legal obligation to have a data security plan and to provide data and system security protections for all taxpayer Information. “Check the box to confirm you are aware.”

IRS Pub 4557 spells out data security system requirements

Cyber SecurityIRS Pub 4557

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 132

Cyber SecurityIRS Pub 4557

• Tax preparers must comply w/ FTC safeguards rule

1. Gramm-Leach-Bliley Act (GLBA) requires “financial institutions” to ensure security and confidentiality of collected consumer information

2. “Financial institutions” include professional tax preparers

3. Under GLBA, Federal Trade Commission (FTC) issued Safeguards Rule requiring companies to develop a written information security plan

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 133

Cyber SecurityFTC Safeguards Rule

1. Designate one or more employees to coordinate info security program

2. Identify and assess risks to customer info in each relevant area of company’s operation, and evaluate effectiveness of current safeguards for controlling these risks

3. Design and implement a safeguards program, and regularly monitor and test it

4. Select service providers that maintain appropriate safeguards, make sure your contract requires them to maintain safeguards and oversee their handling of customer info, and

5. Evaluate and adjust program in light of relevant circumstances, including changes in firm’s business or operations, or results of security testing and monitoring

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 134

Cyber SecuritySafeguards Rule Checklist

• Safeguards rule requires companies to assess and address risks to customer info in all areas, including three particularly important areas

1. Employee Management and Training

2. Information Systems

3. Detecting and Managing System Failures

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 135

Cyber SecuritySafeguards Rule Checklist

1. Employee Management and Training

a. Check references or do background checks before hiring employees who’ll h/ access to customer info

b. Employee must sign agreement to follow company’s confidentiality and security customer info standards

c. Limit access to customer info to employees w/ business reason to see it

d. Control access to sensitive info by requiring employees to use “strong” passwords that must be changed regularly

- IRS recommends 8 character passwords

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 136

Cyber SecuritySafeguards Rule Checklist

1. Employee Management and Training

d. Control access to sensitive info by requiring employees to use “strong” passwords that must be changed regularly

- IRS recommends 8 character passwords

e. Password-activated screen savers to lock employee computers after period of inactivity

f. Develop policies for appropriate use and protection of laptops, PDAs, cell phones or other mobile devices

1) Store these devices in a secure place when not in use

2) Customer info in encrypted files will be better protected in case of theft of device

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 137

Polling Question 8

IRS has looks in an unfriendly manner upon an employee accessing a tax preparation firm’s database with an unsecured remote device

A. True – IRS admires such risk exposure

B. False – Such a transgression may be sanctionable

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 138

Cyber SecuritySafeguards Rule Checklist

1. Employee Management and Training

g. Develop policies for employees who telecommute

- Consider whether or how employees should be allowed to keep or access customer data at home

h. Require employees who use personal computers to store or access customer data to use protections against viruses, spyware and other unauthorized intrusions

i. Impose disciplinary measures for security policy violations

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 139

Cyber SecuritySafeguards Rule Checklist

1. Employee Management and Training

j. Prevent terminated employees from accessing customer info by immediately deactivating their passwords and user names and taking other appropriate measures

g. If collect information online directly from customers, make secure transmission automatic

h. Caution customers against transmitting sensitive data, like account numbers, via email or in response to an unsolicited email or pop-up message

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 140

Cyber SecuritySafeguards Rule Checklist

2. Detecting and managing systems failures

a. Use appropriate oversight or audit procedures to detect the improper disclosure or theft of customer information

b. Use up-to-date intrusion detection system to alert of attacks

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 141

Data Security Plan

• Accounting Today online offers a free “Sample Security Policy for CPA Firms”

http://pages.marketing.accountingtoday.com/act_affinipay_44721_wp_lp.html?source=site

- Not as comprehensive as I prefer for my own purposes, but arguably a decent start

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 142

This Is No Time for Us to Panic

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 143

Tax Planning Amidst TurmoilLiquidity Strategies

1. Wait to pay tax until 07/15/20 – Time value of money

2. Refinance debt at currently low interest rates

3. Payroll Protection Program and other loans (CARES Act)

4. Defer payment of payroll taxes (CARES Act)

5. Carryback 2018 and 2019 NOLs for refunds

- All the way back to 2013 possible

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 144

Let’s Beef Up on Tax Planning

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 145

Tax Planning Amidst TurmoilGiving Strategies

1. Help others make it through

a. $15,000 annual exemption donor/donee ($30,000 gift split)

b. Basic exclusion amounts $11,580,000 per donor

c. Avoids family selling for liquidity while values are low

2. Stock values low – Great time for gifting - Client may not want to hear about it

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 146

Tax Planning Amidst TurmoilGiving Strategies

3. Donate to community relief

a. Above-the-line deduction up to $300

b. Individuals 100% deductible for gifts to public charity

c. C Corps 25% deductible (for 2020, up from 10%)

d. Food inventory 25% deductible (for 2020, up from 15%)

- Do so quickly if restaurant closed / food perishable

e. Be smart about charitable orgs

1) Check credentials of charitable org

- Charity Navigator publishes info about charities, has page “Coronavirus Hot Topic” listing orgs responding to Covid-19

2) Confirm IRS qualified status online at “IRS Tax Exempt Org Search”

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 147

Tax Planning Amidst TurmoilGiving Strategies

4. Refinance family loans at screaming low interest rates

a. Lowers debt service payments for borrower

b. Reduces income and wealth of patriarch

c. April 2020 applicable federal rates (AFRs)

1) Short term (3 years or <) 0.91%

2) Mid term (> 3 up to 9 years) 0.99%

3) Long term (> 9 years) 1.44%

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 148

Tax Planning Amidst TurmoilGiving Strategies

5. Utilize GRATs and CLTs to make additional tax free gifts

a. Grantor Retained Annuity Trusts (GRATs) and Charitable Lead Trusts (CLTs) allow appreciated assets to pass tax free

b. Low interest rates and depressed prices strongly favor

c. GRAT – Transfer assets to trust, receive annuity payments over trust term (often 2 years), remainder to beneficiaries without resulting taxable gift

d. CLT operate in similar way, but make annuity payments to charity, not donor

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 149

Tax Planning Amidst TurmoilIncome Tax Strategies

1. Loss harvest (side step wash sale rules)

1. Refinance debt at currently low interest rates

a. Structure for interest deductibility

1) Interest tracing rules

2) §163(j) Business interest expense deductibility

b. Structure for loss deductibility (basis, at-risk, excess bus. loss)

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 150

Tax Planning Amidst TurmoilIncome Tax Strategies

3. Convert traditional IRA to Roth IRA

- Income based on IRA’s value at time of conversion

4. Play high bracket low bracket game

a. Accelerate income into low tax bracket year

b. Defer deductions away from low bracket year

5. Keep eye on opportunities created by CARES Act

a. Tax credits galore

b. Optimal management of losses

c. Elections abound

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 151

That’s All Folks

03/30/20 © 2020 Bradley Burnett Tax Seminars, Ltd. 152