tamil nadu generation and distribution corporation...

TRANSCRIPT

TAMIL NADU GENERATION AND DISTRIBUTION CORPORATION LTD(ACCOUNTS BRANCH)

(Taxation Division)

FromM.Manoharan, M.Com., ACMA,Director (Finance)144, Anna SalaiChennai - 600 002

ToAll Chief EngineersAll Superintending EngineersAll Financial ControllersAll DDO's Head Quarters

Lr.No.CFC/GL/FC/ACCTS/DFC/AO/Tax/F.GST -11/D.No.103/2017 dt.S.S.2017.Sir,

Sub: GST - Implemented from 1st July 2017 - Reverse ChargeMechanism (RCM) - Additional instructions issued for adherencereg.

Ref: Lr.No.CFC/GL/FC/ACC/DFC/AO/Tax/F.GST-7/D.NO.65/2017dt.07 .07 .2017

******1. Preamble:

Under the erstwhile indirect tax regime, the Central Excise, or Service Tax(Central levy) or as the case may be VAT (State levy) were being generallyimposed on persons who are manufacturer-suppliers, service providers ordealers. There would be requirement of registration and payment of duties/taxesby such persons, which is generally understood as FORWARD CHARGE. Thetax so imposed would be borne by the buyers/end-customers of such supply ofgoods / services. Under Forward Charge, TANGEDCO was duly registered forproviding certain services like imparting training, testing, etc. which are likely tocontinue even under GST. Some additional areas of activities for TANGEDCOwillbe required to pay GST under FORWARD CHARGE are being closely identified(in addition to disposal of fly ash, renting, survey, certain support services fortransmission, distribution of electricity, etc.), and examined for GST liability.

As exception to the above generic principles, there were instances wherethe Government of India / State Government, in select cases, made the recipientof the goods / services as persons liable to pay the indirect tax themselves,either partially or fully, through specific provisions, including Notifications /orders. Such changes in the indirect tax provisions amounted to shifting theresponsibility of paying tax and complying with the provisions to the recipient,partially or fully, is generally called payment of tax under REVERSE CHARGEMechanism.

1

II. Reverse Charge under Service Tax regime:

Under the service tax regime, upto 30.06.2017, TANGEDCO had paid theapplicable service tax under Reverse charge mechanism (including the partialreverse charge) for vehicle charges, manpower charges and advocate fees etc.in terms of the erstwhile Notification No. 30/2012 ST. The applicability ofservice tax under RCMmay be considered after taking into account circular videLr.No.CFC/GL/FC/ACCTS/DFC/AO/Tax/F.GST_8/D.NO. 79/2017 dt. 24.7.2017.

III. Reverse charge under GST:

person to Registered Person: (to TANGEDCO) from unre istered

• An unregistered Person is someone who is not required to be registeredwith GST (i.e. annual turnover not exceeding Rs.20 lakhs).

• Provisions of Reverse Charge under Section 9(4) are applicable only forsupplies within the same state.

• The provisions of Reverse Charge under this Section are not applicable toInter-state supplies as inter-state supplies cannot be made byunregistered persons. Therefore, there cannot be any interstatetransactions of supply of goods / services from unregistered personsfrom other states, as it is not permissible under GST.

• If TANGEDCO opts to purchase goods or services from non-registeredpersons / entities within Tamil Nadu, TANGEDCO is liable to pay GSTunder reverse charge mechanism and observe all the proceduralrequirements associated with it.

• Under GST provlslons, certain specific exemptions such as thresholdexemption of Rs.5000/- per day for aggregate value of supplies of goodsor services or both, have been provided. Since, under GST regime,TANGEDCO has to ideally have only single GST registration forTAMIL NADU, the above exemption may not validly accrue toTANGEDCO.

• In this case of RCM, the TANGEDCOcircles shall raise an Invoice on selfi.e. TANGEDCOcircle for all purchases from unregistered dealers and suchInvoices shall be issued on a monthly consolidated basis (a format of theinvoice under Reverse charge mechanism is enclosed).

Illustration 1:

• A unregistered consultant firm M/s. XYZ, in TN may have providedservices to TANGEDCO, for a consultancy fees of Rs. 1,00,000/- andraised a bill dated July, 2017 (from 01.07.2017 to 31.07.2017). Being,unregistered, XYZ would not have obviously mentioned the GSTregistration number, GST Rate, GST amount, etc in the claim bill.TANGEDCO being recipient of service from XYZ, would be liable to payapplicable CGST and SGST, under reverse charge mechanism For theabove bill and remit it to the Govt. by 20th August, 2017.

2

• So, TANGEDCO will not only pay Rs. 1,00,000 to XYZ, but will have topay GST of Rs.18,OOO/- (Rs. 9,000 of CGST and Rs.9000 of SGST) tothe Government.

Illustration 2:

TANGEDCO purchases stationery of Rs. 5,500 from unregistered PersonTANGEDCO is required to pay GST on Rs. 5,500 under Reverse ChargeMechanism directly to Govt through GST portal.

Transactions that may attract GSTunder ReM:

All the circles have to closely monitor the payments such as Imprest,Temporary advance, Chit agreements, K2 agreements, Lumpsum contracts,Local POs, CE POs, Turnkey contracts, etc, in order to assess the GST liability bylooking after the following:

i) Whether supplier is unregistered person?ii) Whether expenses are not exempted from GST ?iii) Whether supplier is not registered under composition scheme of

GST?

Following are illustrative expenses/payments which can attract GST under RCMi.e.TANGEDCO shall pay applicable GST directly to Govt, in addition to incurringof expenses:

• Rent• Printing and stationery• Repairs and Maintenance• Office Maintenance• Vehicle hire charges• Computer maintenance• Advertisement• Snacks, food for meeting / training

All the day to day purchases of goods or services (except exempt goods orservice) from unregistered person will require payment under RCM.

Exceptions

For these items, RCM will not apply for the simple reason that GST is notapplicable on these:

• Salary and wages (payments under employer employee relations)• Electricity (out of ambit of GST)• Interest payments• Car fuel (Diesel/petrol) (out of ambit of GST)

3

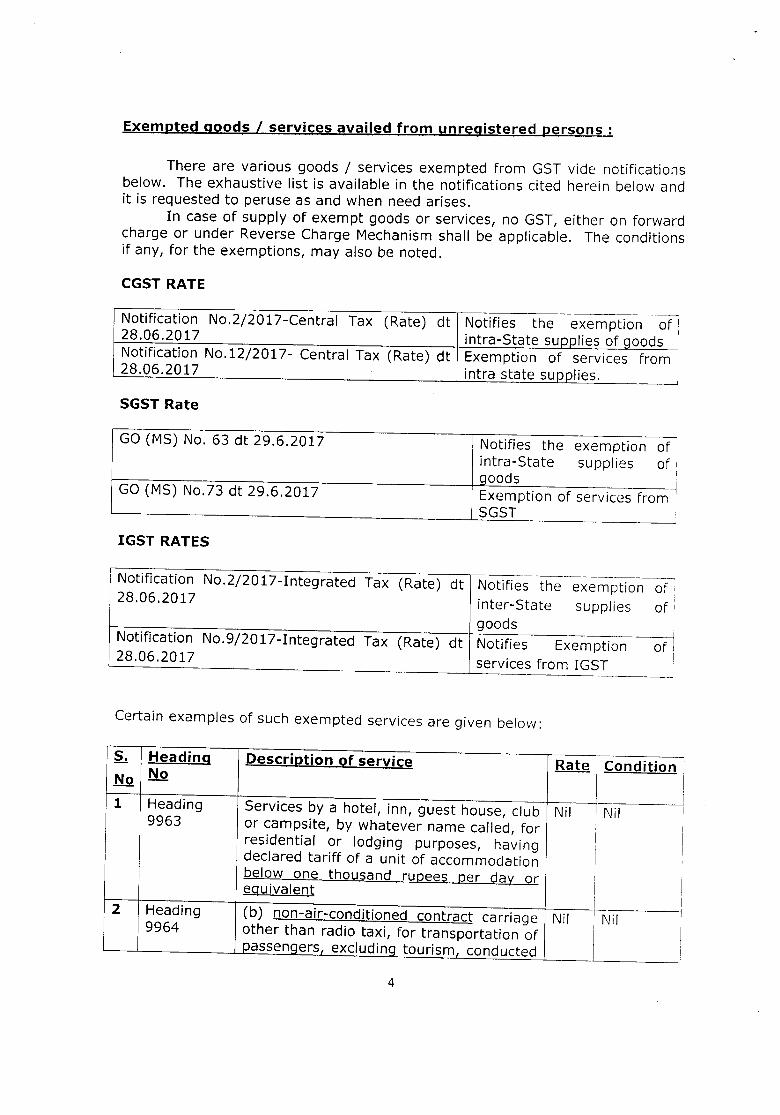

Exempted goods I services availed from unregistered persons:

There are various goods / services exempted from GST vide notificationsbelow. The exhaustive list is available in the notifications cited herein below andit is requested to peruse as and when need arises.

In case of supply of exempt goods or services, no GST, either on forwardcharge or under Reverse Charge Mechanism shall be applicable. The conditionsif any, for the exemptions, may also be noted.

CGSTRATE

Notification No.2/2017-Central Tax (Rate) dt28.06.2017

Notifies the exemption of:intra-State supplies of _goods !

Notification No.12/2017- Central Tax (Rate) dt28.06.2017

Exemption of services from I

intra state sU__Q_plies.

SGSTRate

GO (MS) No. 63 dt 29.6.2017 Notifies the exemption of I

intra-State supplies of IIgoods J

Exemption of services from i

SGSTGO (MS) No.73 dt 29.6.2017

IGST RATES

Notification No.2/2017-Integrated Tax (Rate) dt Notifies the exemption of;28.06.2017 inter-State supplies of I

Igoods~~~~~~~~~~--~~~~~~~~~--------------iNotification No.9/2017-Integrated Tax (Rate) dt Notifies Exemption of i

28.06.2017 services from IGST

Certain examples of such exempted services are given below:

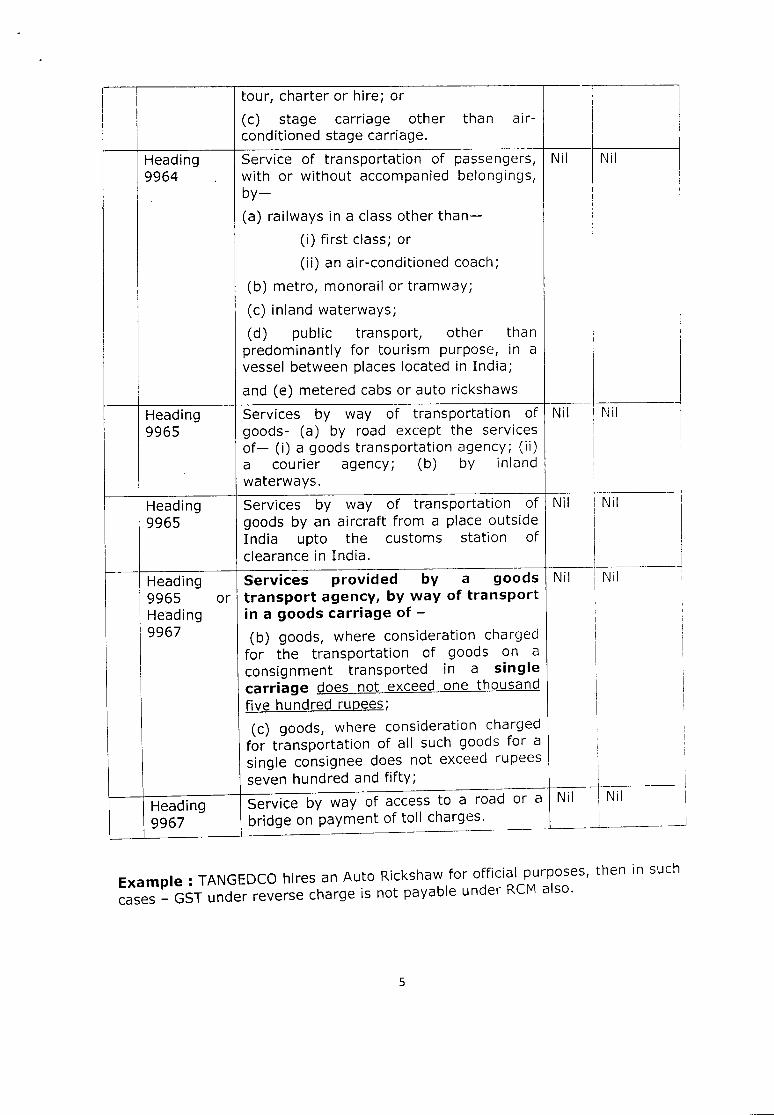

S. Heading Description of service Rate I condition!No No

1 Heading Services by a hotel, inn, guest house, club Nil I Nil ii9963 or campsite, by whatever name called, for I iresidential or lodging purposes, having I I

I I

declared tariff of a unit of accommodationbelow one thousand ruzees Rer da~ or I Ieguivalent

i III2 Heading (b) non-air-conditioned contract carriage Nil I Nil I9964 other than radio taxi, for transportation of

I,Ipassel'l9.ers__Lexcluding tourism conducted I

4

Service of transportation of passengers, Nil I Nil Iwith or without accompanied belongings, I I

by- I

(a) railways in a class other than- I

(i) first class; or II

(ii) an air-conditioned coach;(b) metro, monorail or tramway; I

(c) inland waterways; I II I(d) public transport, other than I ipredominantly for tourism purpose, in a· I

~ __~ __~ -+~v_e_ss_e~l_b_e_t~w_e_e_n__p_la_c_e_s_l_o_ca_t_e_d_'_ln_I_n_d_i_a_;__~ JI __I and (e) metered cabs or auto rickshaws

Heading Services by way of transportation of Nil I Nil9965 goods- (a) by road except the services I

of- (i) a goods transportation agency; (ii) IIa courier agency; (b) by inland I

waterways. I

tour, charter or hire; or -;(c) stage carriage other than air- Iconditioned stage carriage. i

lI

Heading9964

Nil

Services provided by a goods Nilor transport agency, by way of transport

in a goods carriage of -(b) goods, where consideration chargedfor the transportation of goods on aconsignment transported in a singlecarriage does not exceed one thousandfive hundred rupees;(c) goods, where consideration chargedfor transportation of all such goods for asingle consignee does not exceed rupees j~seven hundred and fifty;

~--I-H--e-a-d-in-g----+-s-e-rv-i-c-e---:-b-y-w--a-y-o-f=--a-c-ce-s-s~to--a--r-o-a-;d--o-r-:a-r-~N;-:-;i1--- Nil ~I

9967 bridge on payment of toll charges. _____J

Heading9965

Heading9965Heading9967

Services by way of transportation of Nilgoods by an aircraft from a place outsideIndia upto the customs station ofclearance in India.

Nil

Example: TANGEDCOhires an Auto Rickshaw for official purposes, then in suchcases - GST under reverse charge is not payable under ReM also.

5

B) Notified categories of supplies under reverse charge:In addition to payment of GST under RCM for purchase of goods/services

from unregistered person, GST is also payable under RCM basis for certainnotified services/goods. The Goods/ Services on which GST shall be leviedunder Reverse Charge are available in www.cbec.gov.in/htdocs-cbec/gst/centraltax-rate-notfns-2017. The SGST notification is available inhttps:/lctd.tn.gov.in/home under GST corner. The exhaustive list is available inthe said notifications and it is requested to go through the below notificationswhich are available in the internet.

IGST RATES

Notification NoA/2017-Integrated28.06.2017Notification No.10/2017-Integrated Tax (Rate) dt28.06.2017

Tax (Rate) dt Notifies Reverse charge on "certain goods JNotifies reverse charge on :

Jservices.

CGSTRATE

Notification NoA/2017-Central Tax (Rate) dt Reverse charge on certain i28.06.2017 goods ___iNotification No.13/2017- Central Tax (Rate) dt Reverse charge on services28.06.2017

SGSTRate,---------------------------------------~----------------~-~GO (MS) No.65 dt 29.6.2017 Reverse charge on certain i!

qoods'-G=O---'('-'-M__:_:S=--;)~N_.:::_0_:_c.7_4-=--=d_::_t-=2:_.::9_:_.6:::._.:._::2:...:::0~1:...:.-7----------------~--:-:R~e:_.=._v.:::_e~rs~e~c~h-.:.:a~r~services;

Example:1. Services provided or agreed to be provided by a goods transport agency

(GTA) in respect of transportation of goods by road2. Services provided by an individual advocate including a Senior Advocate

by wa.y of Representational Services before any Court, Tribunal orAuthority by way of Legal Services, to a Business Entity

3. Services provided or agreed to be provided by Government or localauthority excluding-(1) renting of immovable property, and(2) services specified below

(ii)

Services by the ~ep~rtment of Posts by way of speed post, expressparcel post, life Insurance, and agency services provided to aperson other than Government·,

Services in :elation to an aircraft or a vessel, inside or outsidethe precincts of a port or an airport.

Transport of goods or passengers

(i)

(iii)

4. Services of a director to a company.

6

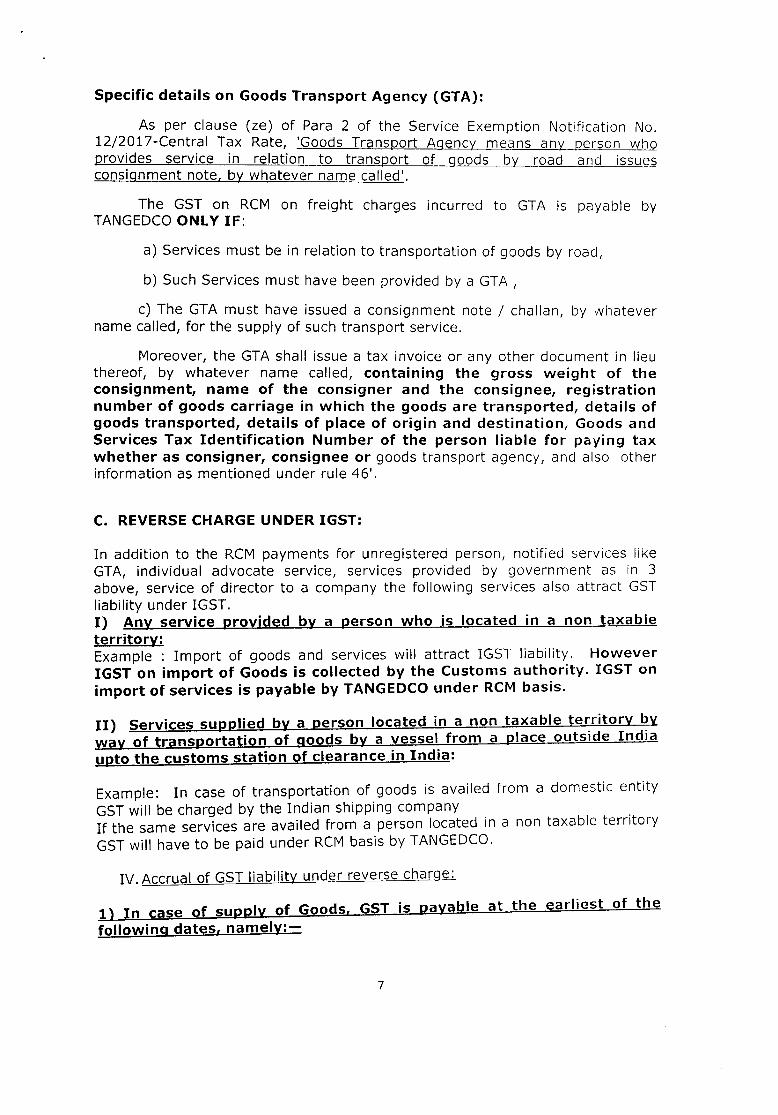

Specific details on Goods Transport Agency (GTA):

As per clause (ze) of Para 2 of the Service Exemption Notification No.l2/20l7-Central Tax Rate, 'Goods Transport Agency means a__ny_personwhoprovides service in relation to transport of goods by road and issuesconsignment note, by whatever name called'.

The GST on RCM on freight charges incurred to GTA is payable byTANGEDCOONLY IF:

a) Services must be in relation to transportation of goods by road,

b) Such Services must have been provided by a GTA ,

c) The GTA must have issued a consignment note / challan, by whatevername called, for the supply of such transport service.

Moreover, the GTA shall issue a tax invoice or any other document in lieuthereof, by whatever name called, containing the gross weight of theconsignment, name of the consigner and the consignee, registrationnumber of goods carriage in which the goods are transported, details ofgoods transported, details of place of origin and destination, Goods andServices Tax Identification Number of the person liable for paying taxwhether as consigner, consignee or goods transport agency, and also otherinformation as mentioned under rule 46'.

C. REVERSECHARGEUNDERIGST:

In addition to the RCM payments for unregistered person, notified services likeGTA, individual advocate service, services provided by government as in 3above, service of director to a company the following services also attract GSTliability under IGST.I) Any service provided by a person who is located in a non taxableterritory:Example : Import of goods and services will attract IGST liability. HoweverIGST on import of Goods is collected by the Customs authority. IGST onimport of services is payable by TANGEDCOunder RCMbasis.

II) Services supplied by a person located in a non taxable te~ritory ~Yway of transportation of goods by a vessel from a place outsIde IndIaupto the customs station of clearance in India:

Example: In case of transportation of goods is availed from a domestic entityGSTwill be charged by the Indian shipping company .If the same services are availed from a person located in a non taxable territoryGSTwill have to be paid under RCMbasis by TANGEDCO.

IV. Accrual of GST liability under reverse charge:

1) In case of supply of Goods, GST is payable at the earliest of thefollowing dates, namely:-

7

(a) the date of the receipt of goods; or

(b) the date on which payment to Suppliers is made;or

(c) the date immediately following thirty days from the date of issue of invoice

Provided that where it is not possible to determine the time of supply underclause (a) or clause (b) or clause (c), the time of supply shall be the date ofentry in the books of account of TANGEDCO.

VARIOUS SCENARIOS

of Time of ExplanationI

Date of Date of Date I

Receipt of invoice payment supply (GSTGoods under RCM

liabilityaccrues)

29.07.2017 5.08.2017 10.11.2017 29.07.2017 The Date of Receipt ofgoods is earlier is earlier. Ifrom the date of payment!, II or within 30 days from ithe date of invoice. I

15.08.2017 25.08.2017 30.07.2017 30.07.2017 The date of payment is Iearlier than the date of Ireceipt of goods and 30 I

I ?ay~ from the date of the iI inVOice. _ i

20.08.2017 05.07.2017 15.08.2017 4.8.2017 30 days from the date of ithe invoice is earlier than I

I

the date of payment and iI the date of receipt of Igoods. J

2) In case of supply of Services, GST is payable at the earliest of thefollowing dates, namely:-

(a) the date of payment or(b) the date immediately following sixty days from the date of issue of invoice orany other document, by whatever name called, in lieu thereof by the supplier:

Provided that where it is not possible to determine the time of supply underclause (a) or clause (b), the time of supply shall be the date of entry in thebooks of account of TANGEDCO

Example 1:Date of payment 15th July 2018Date of invoice 1st July 2018Date of entry in books of receiver 18th July 2018

8

Time of supply of service 15th July 2018If for so~e reason time of supply could not be determined supply under (1) or(2) then It would be 18th July 2018 i.e., date of entry in books.

V.· GST Compensation Cess:

GST Compensation Cess will also be applicable under reverse charge. Asof now, on Coal, there is GST compensation cess of Rs.400 per MT. Since coalprocurement are being made from only from registered persons, the GSTCompensation Cess under RCM does not arise, at present.

VI. GST PAYMENTSTO BE MADE AT NOTIFIED RATES:

Kindly note that the GST is to be paid (whether under Reverse ChargeMechanism or under forward charge mechanism) at the rates specifically notifiedfor goods and services by the Government and by citing the specific HSN code(for goods) or the SAC (for service) and for this website information underwww.cbec.gov.inorhttps:llctd.tn.gov.in may be referred to.

VII. CLAIMING, RECORDING and ADMISSION OF BILLS:

As per the existing procedures in vogue, every bill/claim must besupported with documents, certificate for claim, admissibility, approval, powersdelegated, register entry, etc from the field engineers / officers, so as to admitthe claims in APS section. These process would also be applied on GST regimealso. However, the bills covered under RCM shall have to be taken careseparately, as it involves additional GST commitment to be incurred, to bereported in GST returns, subject to GST Audit, etc.

a) In case of GST liability on the bills / claims from registeredsuppliers of goods / services, the actual GST liability would havebeen included in the invoice itself, in which case, the claimingauthority, admitting authority, paying authority, etc will verify thegenuineness of appropriate GST liability.

b) In case of Bills / claims from Unregistered persons, the GSTliability would not be in their invoices. But the applicable GSTliability arises under ReM basis have to be additionally incurred foreach and every such bills from unregistered persons by TANGEDC~.

c) The claiming authority shall record the applicable GST alo~gwlthHSN / SACcode and GST rates in their claim, certificate, re.9Isters,M.Book, etc. Besides indicating amount claimed as per. bll~s, theadditional GST liability under RCM basis shall also be indicated,separately.

9

d) In case of imprest and temporary advance also, there may be manyprocurement from unregistered persons, for which GST applicablerates also vary. While recording the bills, proper entry of GSTliability, rates, HSN/SAC code shall be made in PCB as well asvouchers certified. In the abstract of expenses, exclusive abstract

. of additional GST under RCM with respect to each account codeshall also be furnished, at time of closing the imprest andtemporary advance.

e) In APS section, all the claims covered under RCM has to betabulated in a format communicated, so as to quantify the GSTliability under RCM. While admitting and making pass order forpayment in APS section the GST under RCM as claimed additionallyfrom field officers, the applicability of HSN / SAC code, GST rates,GST amount, etc are to be entered in a separate register as per theformat.

f) At the end of every month, such register for GST under RCM maybe totalled and appropriate GST invoice under ReM shall becreated for the entire value of goods / services and admitted forremittance to govt.

g) In addition to GST under RCM, there will be GST recovery fromconsumers / contractors for supply of flyash, scraps, or fees for anyservices of TANGEDCO through our tax invoices, which have tobe remitted to Govt, in the next month.

h) The mode of payment of GST liability (both GST recovery and GSTunder RCM) whether through cash / bank/ central payment/ etc arenot yet fi nalised as of now.

VIII. PAYMENTOF GST :

TANGEDCO is required to have a single GST registration for its taxableactivities, within TAMIL NADU. We are in the process of implementing a Softwareprogramme that will .not only integrate all the circles, but also help in Mining ofData from all the Circles for due consolidation, compilation, payment of GST(both under forward charge and reverse charge) and filing of the GSTReturns at the Headquarters, within the due date.

IX. Monthly Abstract:

. In APS section, all the bills/claims such as imprest, Temporary advancechit / K2 / lumpsum contract, other claims, etc are to be tabulated at the end ofebverymOt~th, so as to assess the GST liability under RCM to be payable on orefore 20 of next month.

10

In view of the same we will shortly intimate the procedure for payment ofGST under RCM and for other taxable supplies like the GST collected from sale ofscrap, fly ash, training fees, etc. All the circles are instructed not to pay theGST under ReM and GST collected on sale and other taxable su lies tillfurther orders issued from Head quarters.

Copy to the Executive Assistant to CMD(TANGEDCO.CY-~'1 tJ&b"Copy to the Executive Assistant to the Director General of Police'.Copy to the Secretary/BOSB/TANGEDCO, Chennai.Copy to All the Directors of TANGEDCOand TANTRANSCOCopy to the Chief Financial Controller/General, Revenue & Regulatory Cell.Copy to the Chief Financial Controller/TANTRANSCO.Copy to the Chief Internal Audit Officer/BOAB.Copy to the Chief Engineer/IT with a request to post in the intranet mail.Copy to the Resident Audit Officer,III Floor NPKRRMaaligai, Chennai.Copy to the Asst.Accounts Officer/Establishment, Accounts Branch.Copy to the Chief Public Relations Officer, TANGEDCO,Chennai.Copy to all Deputy Financial Controllers in Accounts Branch/HQ.Copy to the Stores Controller, TANGEDCO,Chennai.Copy to the Assistant Personnel Officer/Tamil Development (2 copies) - forpublication in TANGEDCOBulletin.

11