talent trends in asean “ready to take off”• for the right career move 15% • ‘tiptoers’...

TRANSCRIPT

TALENT TRENDS IN ASEAN“READY TO TAKE OFF”29th of April 2014

Godelieve KroonenbergASEAN Business Leader – Talent Information SolutionsSingapore

MERCER

Today we are looking forward to discussing with you…..

• Operating in ASEAN– Opportunities & Challenges– Business Outlook– HR Facts and Figures– Compensation and Benefits Trends

• Country Highlights– Indonesia– Malaysia– Myanmar– Philippines– Singapore– Thailand– Vietnam

• Q&A

1May 5, 2014

MERCER

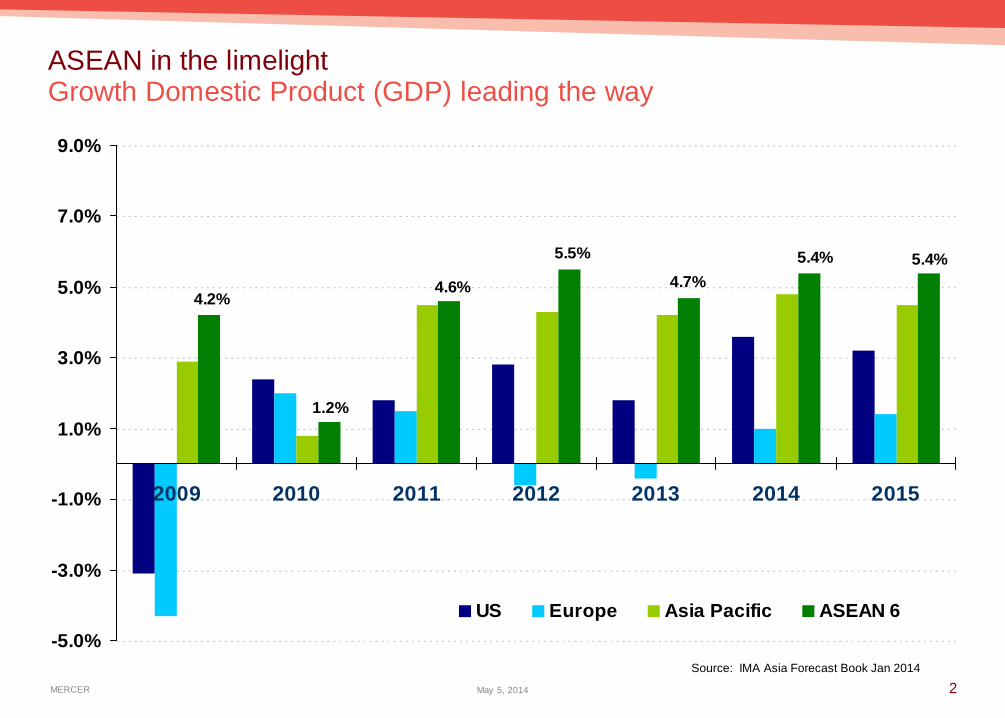

4.7%5.4%5.4%5.5%

4.6%

1.2%

4.2%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

2009 2010 2011 2012 2013 2014 2015

US Europe Asia Pacific ASEAN 6

ASEAN in the limelightGrowth Domestic Product (GDP) leading the way

Source: IMA Asia Forecast Book Jan 2014

2May 5, 2014

MERCER

ASEAN has a bright future

3May 5, 2014

Young, urbanized and growing population with great naturalresources and political stability are key attractions for ASEAN

MERCER

Country growth rates differ significantly

• Indonesia rises from28% of ASEAN 6 to39% by 2012 (and2020).

• Vietnam rises from5% in 2000 to 7% in2012 and 10% by2020.

• Thailand is No.2 butdrops from 21% in2000 to 16% in 2012and 17% in 2020.

Source: IMA Asia October 2013

ASEAN due forrealignment by 2020

4May 5, 2014

MERCER

HK

JP

KR

SG

TH

TW

0% 20% 40% 60% 80% 100%

Less Optimistic

Moderately reduce from 2013 level (5 – 15% reduction)Be similar to 2013 level (+/- 5% change)Moderately increase from 2013 level (5 – 15% increase)Significantly increase from 2013 level (> 15% increase)

0% 20% 40% 60% 80% 100%

ID

IN

MY

PH

VN

More Optimistic

Moderately reduce from 2013 level (5 – 15% reduction)Be similar to 2013 level (+/- 5% change)

Moderately increase from 2013 level (5 – 15% increase)Significantly increase from 2013 level (> 15% increase)

Revenue growth expectations for 2014

More companies expect the growth to come from ASEAN countries5May 5, 2014

ASEAN Countries

Source: Mercer Surveys & Analysis

MERCER

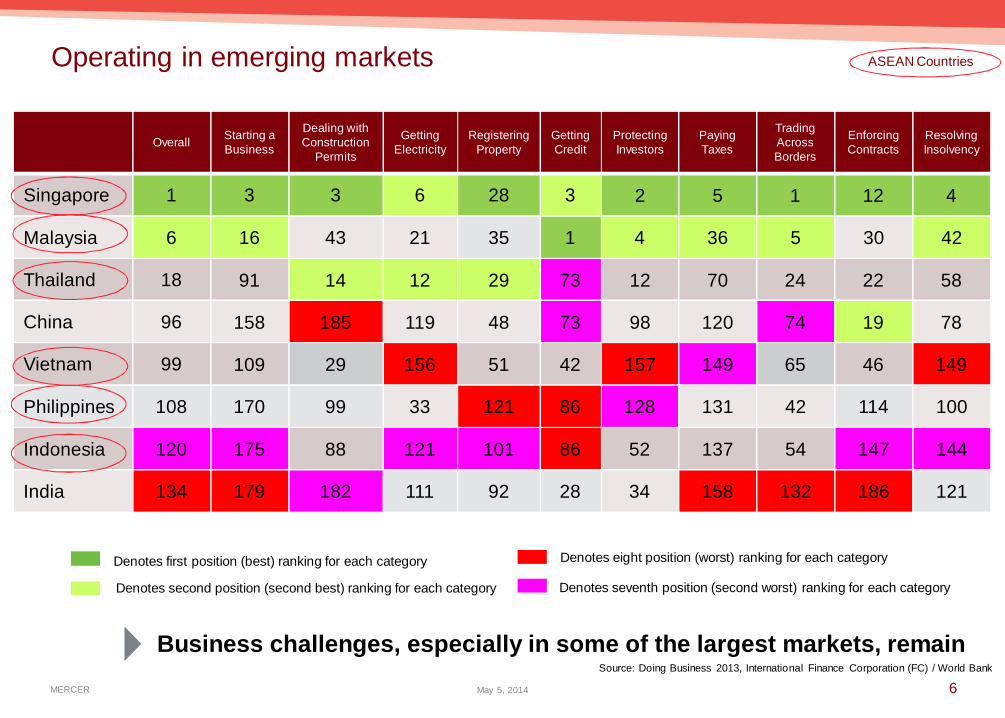

Operating in emerging markets

Denotes first position (best) ranking for each category

Denotes second position (second best) ranking for each category

Denotes eight position (worst) ranking for each category

Denotes seventh position (second worst) ranking for each category

Overall Starting aBusiness

Dealing withConstruction

Permits

GettingElectricity

RegisteringProperty

GettingCredit

ProtectingInvestors

PayingTaxes

TradingAcrossBorders

EnforcingContracts

ResolvingInsolvency

Singapore 1 3 3 6 28 3 2 5 1 12 4

Malaysia 6 16 43 21 35 1 4 36 5 30 42

Thailand 18 91 14 12 29 73 12 70 24 22 58

China 96 158 185 119 48 73 98 120 74 19 78

Vietnam 99 109 29 156 51 42 157 149 65 46 149

Philippines 108 170 99 33 121 86 128 131 42 114 100

Indonesia 120 175 88 121 101 86 52 137 54 147 144

India 134 179 182 111 92 28 34 158 132 186 121

Source: Doing Business 2013, International Finance Corporation (FC) / World Bank

Business challenges, especially in some of the largest markets, remain6May 5, 2014

ASEAN Countries

MERCER

And so do Talent challengesRequiring a different approach

7May 5, 2014

Resulting in

• Competition for talent• High employeeexpectations

• Gap in leadershipskills

• Managers get “drivinglicense” too soon

• Unstructuredcompensation

• Immature benefitslandscape

Opportunity – Growth Expectations

1

Challenge - Talent not there to deliver

2

MERCER

0.00%2.00%4.00%6.00%8.00%

10.00%12.00%14.00%16.00%18.00%

HK ID IN JP KR MY PH SG TH TW VN

12.50%

9.80%

13.50%

5.90%7.50%

14.90%

9.90%11.90%

17.20%

11.10% 11.80%

Average voluntary attrition percentage

Average voluntary percentage

HK ID IN JP KR MY PH SG TH TW VN

Chemical(7.5%)

Automobile &Component (4.3%)

Machinery &Elec.Equip(7.8%)

Machinery & Elec.Equip(3.6%)

Automobile(3.2%)

Energy(8.2%)

Energy(3.6%)

Chemicals (8.0%)

Automobile&Component(9.5%)

Transportation &Logistics(6.4%)

Metals &Mining(5.3%)

Machinery& Elec.Equip(9.9%)

Energy(6.1%)

Energy(9.0%)

HighTech(5.0%)

Chemicals(5.3%)

Chemicals(11.9%)

High Tech(7.5%)

Consumer Goods(11.4%)

Chemicals(11.7%)

Chemicals(7.3%)

RealEstate(7.0%)

Industries doing better than country average

Relatively high turnover rates across ASEANImpact on the cost of doing business

8May 5, 2014

Source: Mercer Surveys & Analysis

MERCER 905 May 2014

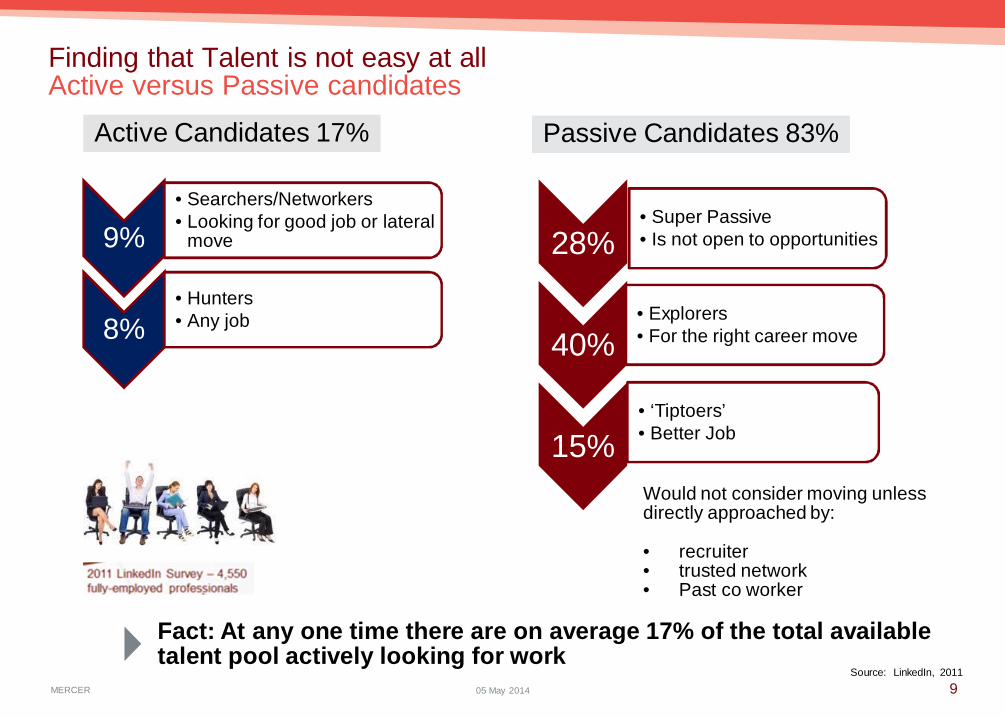

17%Inbound

9%• Searchers/Networkers• Looking for good job or lateral

move

8%• Hunters• Any job

28%• Super Passive• Is not open to opportunities

40%• Explorers• For the right career move

15%• ‘Tiptoers’• Better Job

Would not consider moving unlessdirectly approached by:

• recruiter• trusted network• Past co worker

Active Candidates 17% Passive Candidates 83%

Finding that Talent is not easy at allActive versus Passive candidates

Fact: At any one time there are on average 17% of the total availabletalent pool actively looking for work

Source: LinkedIn, 2011

MERCER

What do Job Seekers seek?

1005 May 2014

Source: LinkedIn Talent Trends 2014

MERCER 1105 May 2014

Compensation & Benefits trends in Asia

A Balancing Act

Wild East ofRewards

Evolution ofMobility

1

2

3

• Opportunities• Growth• Young

population• First rule is……

there are norules!

• Sustainability of pay multiples from grads to executives• Delinking salary increments from inflation• Over focus on base salary?• STI, LTI and Benefits as branding differentiators

• Short term assignments as development opportunities• Rise of “returnees”• Hardship? What hardship?• Rise of “Local Plus”

• Challenges• “War for Talent”• Legislative changes• Foreign labor restrictions• “Employee friendly”

markets• Governance

Source: Mercer Surveys & Analysis

MERCER

4.4 10.4 10.2 1.9 5.0 5.3 6.6 4.3 5.7 3.6 10.0

4.7

9.710.7

2.1

5.05.6

6.7

4.3

5.8

3.7

10.2

4.8

10.210.7

2.1

5.15.7

6.6

4.4

5.8

3.8

11

0

2

4

6

8

10

12

HK ID IN JP KR MY PH SG TH TW VN

Salary increase

2014 (Actual) 2014(Budgeted) 2015 ( Forecast)

Planned salary increases remain highAverage salary increase across countries

HK ID IN JP KR MY PH SG TH TW VN

Machinery &Elec. Equip(5.5%)

Machinery &Elec. Equip(13.4%)

Pharma(12.7%)

High Tech(2.7%)

Transportation &Logistics(5.8%)

Energy(7.3%)

Energy(7.4%)

Pharma(4.8%)

Chemicals(6.2%)

Machinery& Elec.Equip(5.3%)

Pharma(12.3%)

ConsumerGoods(5.3%)

Automobile &Compnt.(11.4%)

High Tech(10.7%)

Consumer(2.4%)

Energy(5.5%)

Pharma(6.7%)

Chemical(7.3%)

Real Estate(4.6%)

Automobile &Compnt.(6.1%)

High Tech(4.2%)

High Tech(11.6%)

Industries planning to pay higher than ‘overall’ projected 2015 Salary

1205 May 2014Source: Mercer Surveys & Analysis

MERCER

And so do variable bonusesWith a highly “fixed” nature

14.9 15.8 11.9 14.4 12.9 18.5 14.0 17.5 14.4

13.7 15.5

14.8

17.5

12.1

19.5

14.9

18.5

13.1

17.416.4

14.3 15.4

15.7

18.5

12.7

18.1

14.8

18.9

11.6

17.015.7

14.1 15.1

0.0

5.0

10.0

15.0

20.0

25.0

HK ID IN JP KR MY PH SG TH TW VN

Variable Bonus as a % of annual salary

2014 (Actual) 2014(Budgeted) 2015 ( Forecast)

1305 May 2014

Source: Mercer Surveys & Analysis

MERCER

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

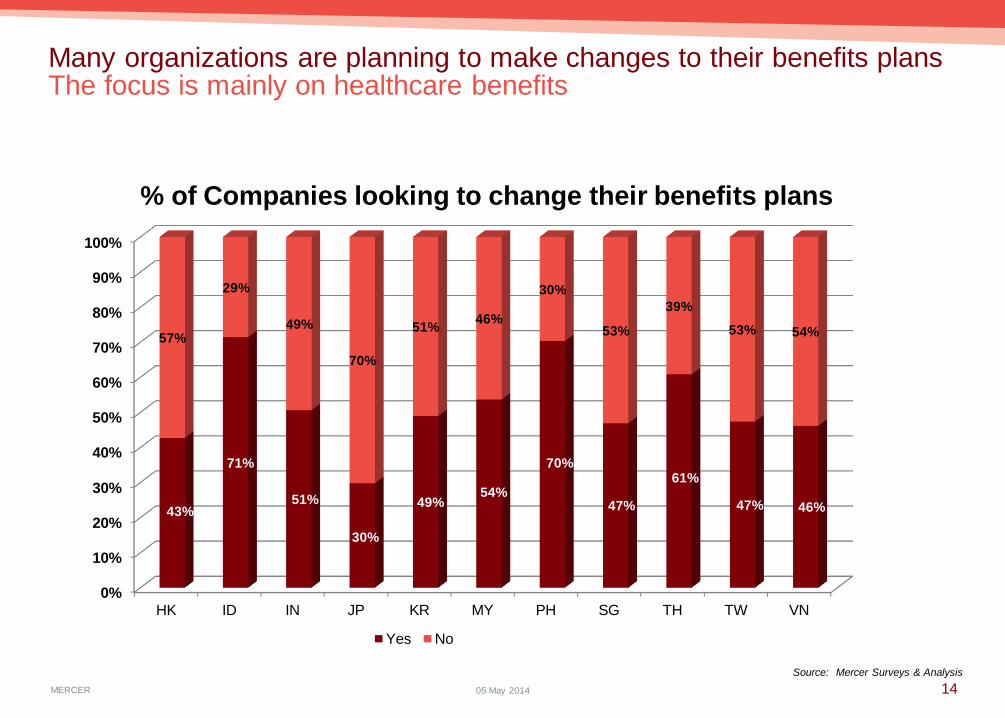

HK ID IN JP KR MY PH SG TH TW VN

43%

71%

51%

30%

49%54%

70%

47%

61%

47% 46%

57%

29%

49%

70%

51% 46%

30%

53%

39%

53% 54%

Yes No

Many organizations are planning to make changes to their benefits plansThe focus is mainly on healthcare benefits

1405 May 2014

Source: Mercer Surveys & Analysis

% of Companies looking to change their benefits plans

MERCER

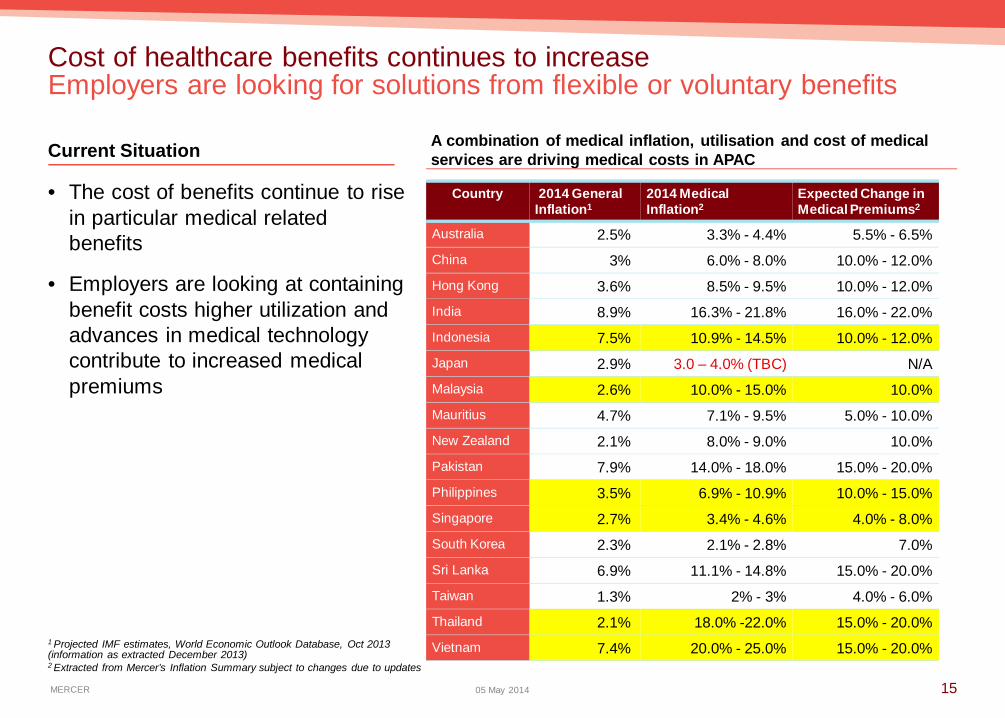

Cost of healthcare benefits continues to increaseEmployers are looking for solutions from flexible or voluntary benefits

• The cost of benefits continue to risein particular medical relatedbenefits

• Employers are looking at containingbenefit costs higher utilization andadvances in medical technologycontribute to increased medicalpremiums

Country 2014 GeneralInflation1

2014 MedicalInflation2

Expected Change inMedical Premiums2

Australia 2.5% 3.3% - 4.4% 5.5% - 6.5%China 3% 6.0% - 8.0% 10.0% - 12.0%Hong Kong 3.6% 8.5% - 9.5% 10.0% - 12.0%India 8.9% 16.3% - 21.8% 16.0% - 22.0%Indonesia 7.5% 10.9% - 14.5% 10.0% - 12.0%Japan 2.9% 3.0 – 4.0% (TBC) N/AMalaysia 2.6% 10.0% - 15.0% 10.0%Mauritius 4.7% 7.1% - 9.5% 5.0% - 10.0%New Zealand 2.1% 8.0% - 9.0% 10.0%Pakistan 7.9% 14.0% - 18.0% 15.0% - 20.0%Philippines 3.5% 6.9% - 10.9% 10.0% - 15.0%Singapore 2.7% 3.4% - 4.6% 4.0% - 8.0%South Korea 2.3% 2.1% - 2.8% 7.0%Sri Lanka 6.9% 11.1% - 14.8% 15.0% - 20.0%Taiwan 1.3% 2% - 3% 4.0% - 6.0%Thailand 2.1% 18.0% -22.0% 15.0% - 20.0%Vietnam 7.4% 20.0% - 25.0% 15.0% - 20.0%

Current Situation A combination of medical inflation, utilisation and cost of medicalservices are driving medical costs in APAC

1 Projected IMF estimates, World Economic Outlook Database, Oct 2013(information as extracted December 2013)2 Extracted from Mercer’s Inflation Summary subject to changes due to updates

1505 May 2014

MERCER 1605 May 2014

ben·e·fit (b n’ -f t)

n.

1. Something that promotes or enhanceswell-being; an advantage

Shifting perspective on benefitsLooking at low cost options

• Present day definition of benefits policies goes beyond the traditionalbenefits provided such as health, retirement, insurance etc

More focus on how benefits are offered: cost effective and efficient!

Communication!

• Employees take on a broader perspective of what defines benefitse.g.– Flexible working arrangements– Recreational items and work environment

MERCER 1705 May 2014

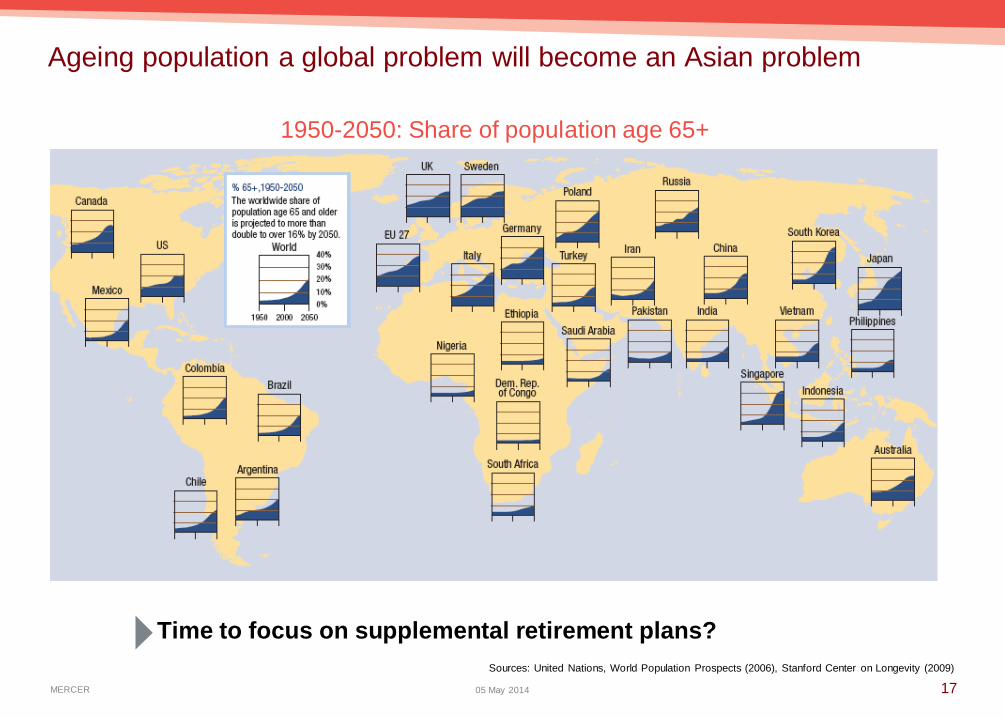

Sources: United Nations, World Population Prospects (2006), Stanford Center on Longevity (2009)

Ageing population a global problem will become an Asian problem

Time to focus on supplemental retirement plans?

1950-2050: Share of population age 65+

COUNTRY UPDATESTAKING A CLOSER LOOK

MERCER 1905 May 2014

• Economy is still doing well with 2014 forecasted GDP at 6% (slightlyhigher than 2013) and Inflation rate at 6.5% (lower than 2013).

• Around 70% companies are recruiting, adding headcount particularly inEngineering and Sales & marketing.

• In order to attract talent, 68% of companies are offering sign upbonuses especially to Managers with 48% bond for the employee in a 1year contract. However, less than 30% of companies have retentionprogram and its mostly monetary. Companies need to think of ways tonot only attract but also to retain.

Economy andworkforce trend

IndonesiaAdapting to Changes

• Health expenditure CAGR among fastest in Asia, though per capita spendlags. Medical costs growing rapidly, with 2013 medical inflation projectedat 12-13% double than total country inflation.

• Indonesia is 1 of 3 countries in Asia where average employer benefitexpenditure exceeds 25% of payroll.

• New National social security (BPJS) will be applied in Jan 1st 2015 whereit will be mandatory to for companies . This will add additional cost tocompany H&B budget.

• From Mercer pulse survey among 155 companies :• 79% companies have not prepared cost/benefit analysis in

preparation for BPJS and more than half have not decided onBPJS execution, 20% will run both BPJS and Private insurance and16% will supplement BPJS with private insurance.

• With regards to BPJS companies should focus on communications,health plan coverage options, and impact to overall H&B budget.

Trends & Newregulation on

Employee HealthBenefit

Source: Mercer Surveys & Analysis

MERCER

Malaysia OutlookLooking up

20

16.1% 16.7%

8.2%

0.0%

5.0%

10.0%

15.0%

20.0%

2011 2012 2013 first-half

Turnover Rate

Source: 2013 TRS All Industries Survey / IMA Asia – Asia Pacific Executive Brief Apri l2014

Implementation of Goods and Services Tax (“GST”)effective 1 April 2015 with a standard rate of 6%.

Corporate Tax rate is proposed to reduce from 25% to24%.

To ensure employees achieve work life balance, it isproposed that expenses incurred in the training ofemployees, supervisors and managers as well asconsultancy fees to design appropriate Flexible WorkArrangements (“FWAs”) will be given further taxdeductions.

4.8%

3.5%

3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2011 2012 2013 2014

GDP Inflation Unemployment

0.0%1.0%2.0%3.0%4.0%5.0%6.0%

2012 2013 2014

5.4% 5.5% 5.5%

4.2%5.0% 5.0%

2.0% 2.0% 2.0%

Salary Increase PromotionMarket Adjustment

Salary Increase, Promotion and MarketAdjustment

05 May 2014

MERCER

MyanmarOn a growth spurt

21

Myanmar to allow foreignbanks to operate this year

33 Foreign Bank Rep Offices11 Private Banks

4 State-owned Banks9 Semi-state owned Banks

Bridges

Increasing consumption patternValue-adding labour force

Precious resourcesHigh capital inflow

International Oil & Gasspotlight

30 offshore blocks

Influx of Hospitality playersBoutique | International Brands

Barriers

Labour productivity issuesGeopolitical

Interpretation of the lawRising expectations

Source: Mercer Surveys & Analysis

05 May 2014

MERCER

PhilippinesTight labor market benefits key talent

• Despite a devastating typhoon and little infrastructure work, the economy grewto 7.2% in 2013.

• The industry and service sector together with strong public and governmentspending will remain as the main driver of growth.• Industrial production, automotive and BPO are expected to sustain economic

growth

Philippineeconomy stillon track

• The inadequacy of employment opportunities in the country is causing the out-migration of professionals and skilled workers and is discouraging their return.

• Increasing compensation and benefits costs -• Increase contribution in Social Security and salary brackets in Health

Insurance• Companies spend 30% of total payroll on benefits

Labour IssuesandChallenges

• Salary is expected to increase at 7% this year, driven by marketcompetitiveness.

• Sales and Finance remain to be the hot jobs across industries• Insured (HMO) type of benefit is the most prevalent. MNCs are shifting to

Defined Contribution type of retirement.• Companies responded to typhoon/disaster by providing financial assistance,

emergency loans and leave advances to employees.

Compensationand BenefitsTrends

22Source: Mercer Surveys & Analysis

05 May 2014

MERCER

RedundancyMinistry of Manpower (MOM): Redundancyremains low in 2013, while it is expected to slightlyincrease in 2014 due to economic restructuring.Top reasons for redundancy: restructuring ofbusiness processes, high costs andreorganization of businesses.

Labor ProductivitySingapore's labor productivity sees zero growth in2013 – still an improvement compared to the -2%in 2012.Construction sector had the poorest performancefor six consecutive quarters.

Tight Labor MarketTight labor market continues to push up number ofjob vacanciesServices and construction sectors generates thebulk of job openings due to unattractive pay andphysically demanding tasks.

Key trends across major industriesMerger and AcquisitionInternal restructuringShortage of right talent pool

SingaporeShift in labour focus

2305 May 2014

MERCER

ThailandWorkforce issues

• Compensation observations– From 10 years tracking, it proves that compensation management is different in

each industry.– Those long established in Thailand e.g. Chemical companies’ base pay is well

ahead of other industries. While Pharmaceutical companies drive pay at TotalCash component.

• Pay positioning shifting to a higher percentile for the last 2 years– The shift of Pay positioning from Median to 75th percentile is found in some

industries e.g. Automotive, Banking, and FMCG.– This is a reflection from the market growth and the attraction policy.

• Skilled workforce in demand– Another significant movement is on the Hiring intention from growing industries

e.g. Electronics appliances, Retails, Automotive and Hire purchase.– Good workforce planning and recruiting will become a long winning game for

Talent strategy (build vs buy).

2405 May 2014

Source: Mercer Surveys & Analysis

MERCER 2505 May 2014

FORECAST for 2014 business is slightly better than 2013. Based on the pulse surveyconducted in March 2014, 75% of the survey participants are optimistic and report betterforecast for business performance in 2014, especially in Pharmaceutical, Insurance andConsumer Goods industries

1

MINIMUM WAGES: from 1 Jan 2014, the minimum wages for all types of enterprises willincrease between 14,3% and 16,7% compared to the current wages.

2

SOCIAL CONTRIBUTION: from 1 Jan 2014, the contribution rate of social insurance willincrease with 1% for both employee and employer.

3

TRADE UNIONS: agencies, organizations and enterprises will have to contribute to TradeUnion funds (2% of the salary fund for Social Insurance contributions for employees) -regardless of whether these agencies, organizations and enterprises have a Trade Union ornot Organizations/enterprises must pay into Trade Union funds once per month at the sametime as they make payment for social insurance contribution for employees

4

PRIVATE PENSION INSURANCE: is newly introduced in Vietnam from mid 2013. Thereare tax deductions although these remain relatively low at the moment.

5

VietnamLabor cost increase

Source: Mercer Surveys & Analysis

MERCER

Building a sustainable competitive advantageCompanies in emerging markets should start now…

Total RewardsTalent Mobility

Health andWellness

StrategicWorkforcePlanning

TalentDevelopment

2605 May 2014

MERCER

QUESTIONS?For more information please contact your Mercer representative or:Godelieve Kroonenberg at [email protected]

MERCER

Mercer (Singapore) Pte Ltd (1978 02499E)