tactics to win in the state and local cloud market

TRANSCRIPT

Tactics to Win in the State & Local Cloud Market

pr

written by:

Tactics to Winin the State & Local

Cloud Market

Paul IrbyMarket Analyst

State Local

www.onvia.com

2© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

This white paper examines trends and tactics to win in the state and local government cloud marketplace and provides additional contracting insights regarding working with these agencies. Cloud is an exciting and timely topic in public sector IT, and many of Onvia’s technology clients are directly involved. Onvia’s data shows that in the first three quarters of 2013 there was an increase of more than 35% in the number of cloud projects that were advertised for bid or described in an RFP, making this segment one of the fastest growing within the universe of state and local IT procurement.

Because of our comprehensive industry-leading database of SLED (state/local/education) technology project awards and bids/RFPs, Onvia is in a unique position to bring understanding and perspective around the dynamics and challenges that cloud represents. To accomplish this, our market analysis team integrated data from Onvia’s database of over 83,000 state and local government purchasing departments and approximately 200,000 awards, RFPs and bids for technology projects in the 2011-2013 time frame, with articles and reports from leading industry sources on state and local cloud computing trends.

SECTION 1: WHAT ARE THE INDUSTRY TRENDS FOR CLOUD?

With the recent impact of the federal government’s sequestration of 2013 and a weak forecast of only two percent growth in annual federal IT spending1, state and local IT budgets appear to offer the most potential for growth. General support for this can be found in recent confidence surveys of city and county finance officers, which indicate local agencies have benefited from the national economic recovery. For example, the National League of Cities recently surveyed 350 finance officers and found 72% of their local governments were in better financial shape in 2013 than 20122. Similarly, counties have recently been reporting higher property taxes and a leveling off of foreclosures3. Of course, “better” is relative; state and local government buyers may have become “less challenged” with budgets but they’re still accountable for meeting increasing demands while holding down costs.

Cloud represents a substantial opportunity for experienced IT

vendors in the state and local market.

1 The most recent 2014-19 federal IT forecast from the TechAmerica Foundation is for only 2.3% average annual growth for the next 5 years. Reported in “Fed IT Spending To Rise After 3-Year Decline,” Wyatt Kash, InformationWeek, October 17, 20132 “The post-recession shuffle,” Stephanie Johnston and Victoria Sicaras, Public Works, January 20143 National Association of Counties survey, reported in Ibid.

3© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

In these fiscally challenging times, government is under pressure to embrace practices that will make it more efficient and responsive long-term, while de-emphasizing those practices that will not. Technology solutions that promise significant long-term improvement and cost-cutting should fare better provided they can maintain security, preserve the ability to control and manage systems and data, and stay clear of regulatory hurdles. Cloud projects should perform particularly well because cloud technology routinely delivers value and added efficiency. This first section will cover several notable cloud project trends and aspects of contracting within states and municipalities.

Cloud: Broad impact within the state and local IT market

State and local agencies face a number of demands for expanded IT services but budgets are often not sufficient for traditional legacy solutions. This is where the efficiencies of cloud can help, as the short-term investments enable long-term software and hardware savings and service improvement4. Crystal Cooper, Vice President of Public Sector Solutions at Unisys said, “Despite continued concerns about cloud security, [state & local government] agencies are recognizing that the cloud can help them reduce costs, adopt mobile devices into their organizations, and modernize old legacy software applications.”5

Cloud’s impact can be seen in many places:

• Onvia’s own database of RFPs and bids from state and local governments confirmed that over the past year cloud projects have been growing at a much faster rate (i.e. 37% vs. 4%) than other types of IT services.6

• An IT industry report from Business Monitor International7 noted, “Cloud computing has emerged as one of the key growth areas of the worldwide software market.” Within the United States, “Federal and local governments are among verticals where strong interest in cloud services is being expressed.” The report added, “An increasing number of government organizations at the federal and state level are rolling out or, at least, studying cloud strategies.”

• Finally, a recent August 2013 survey by Unisys of 109 decision-makers at state and local agencies8 found that 32% already had implemented cloud and one in eight were planning to do so. That result suggests nearly one-half of the state and local government purchasing departments are already sold on the concept.

4 “Cloud gaining traction as state and local cost-cutter,” Rutrell Yasin, GCN, October 16, 20135 Ibid.6 Onvia internal database of government bids and RFPs. State and local government records were selected for analysis. Period of comparison was Q1- Q3 2012 vs. Q1-Q3 2013, broken out by cloud vs. all other IT project types7 United States Information Technology Report Q4 2012, Business Monitor International, pg. 25,26,398 Survey report titled, “Cloud Adoption and Procurement Practices,” prepared by Center for Digital Government (sponsored by Unisys), August 2013

4© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Vast opportunities, but slower adoption curve for cities and towns

While the general trend in cloud adoption in state and local government is one of growth, with reduced barriers and increased chances of contracts being offered, cities continue to lag somewhat behind and require a tailored approach.

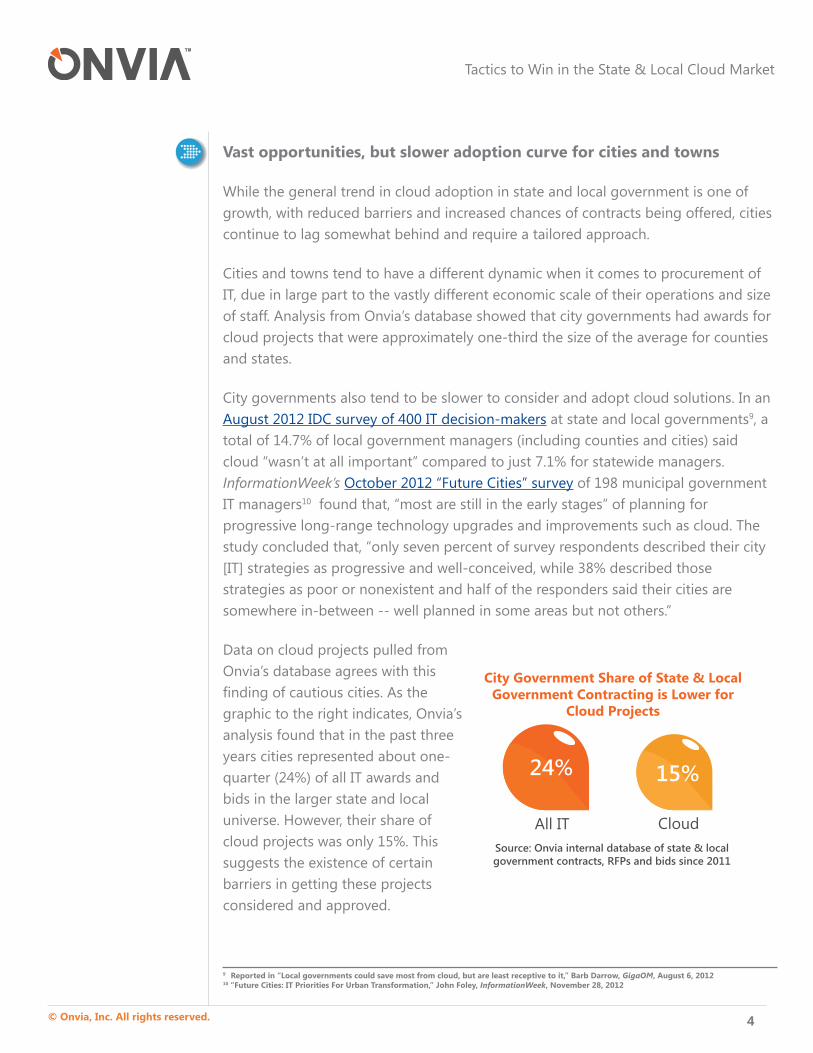

Cities and towns tend to have a different dynamic when it comes to procurement of IT, due in large part to the vastly different economic scale of their operations and size of staff. Analysis from Onvia’s database showed that city governments had awards for cloud projects that were approximately one-third the size of the average for counties and states.

City governments also tend to be slower to consider and adopt cloud solutions. In an August 2012 IDC survey of 400 IT decision-makers at state and local governments9, a total of 14.7% of local government managers (including counties and cities) said cloud “wasn’t at all important” compared to just 7.1% for statewide managers. InformationWeek’s October 2012 “Future Cities” survey of 198 municipal government IT managers10 found that, “most are still in the early stages” of planning for progressive long-range technology upgrades and improvements such as cloud. The study concluded that, “only seven percent of survey respondents described their city [IT] strategies as progressive and well-conceived, while 38% described those strategies as poor or nonexistent and half of the responders said their cities are somewhere in-between -- well planned in some areas but not others.”

Data on cloud projects pulled from Onvia’s database agrees with this finding of cautious cities. As the graphic to the right indicates, Onvia’s analysis found that in the past three years cities represented about one-quarter (24%) of all IT awards and bids in the larger state and local universe. However, their share of cloud projects was only 15%. This suggests the existence of certain barriers in getting these projects considered and approved.

9 Reported in “Local governments could save most from cloud, but are least receptive to it,” Barb Darrow, GigaOM, August 6, 201210 “Future Cities: IT Priorities For Urban Transformation,” John Foley, InformationWeek, November 28, 2012

City Government Share of State & LocalGovernment Contracting is Lower for

Cloud Projects

24% 15%

All IT CloudSource: Onvia internal database of state & localgovernment contracts, RFPs and bids since 2011

5© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

While slower adoption can be a frustration for vendors in the short term, it presents a great opportunity for companies that start building government relationships early to be well-positioned when an agency becomes ready to buy.

Because of much smaller staff sizes, the lack of capacity for IT planning at the local level could account for some of the difference. In a CloudTimes article11 it was noted that “it’s mostly just lack of understanding that prevents local governments from seeing the cloud’s potential, as local IT people are usually so busy just keeping things on their end running in tip top shape that they fail to do broad strategic planning.” A related issue was how to maintain direct control over operations, including continuity of reporting and access to data. This was a theme in the GigaOM article. One city IT official interviewed explained that local IT managers “need to have confidence that they can get the same results and have the same management capabilities in the cloud that they have now on premise.”

Security presented another well-known obstacle that was cited in cloud articles and surveys, regardless of the level of government. The Unisys survey of state and local government IT staff showed that “ensuring data security” was by far the top decision factor for cloud adoption, as mentioned by 81% of state and local decision-makers surveyed.

Shawn McCarthy, research director with IDC Government Insights, generally agreed with the assessment of slower cloud adoption for cities based on their 2012 IDC survey12 of government IT staff. He indicated there is a “need for outreach” within city government. One approach, which McCarthy recommended and was mentioned in the GigaOM article, was to have regional deployments, such as having groups of cities band together to spearhead common initiatives with a shared services model that can reduce per city costs. A regional approach could also provide stronger coordination and vision for an effective marketing and awareness campaign.

Whether they embrace cloud alone or in partnership with other nearby cities, the IT vendor community has a consulting role to play in educating IT decision-makers so they understand the important choices they face.

11 “IDC: Local Governments Need to Catch up on Cloud Computing,” Xath Cruz, CloudTimes, August 22, 2012 12 Quoted in “Many gov IT managers unsure about cloud strategy, study finds,” Rutrell Yasin, GCN, Aug 06, 2012

6© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Statewide cloud initiatives bypass local uncertainty and drive investment for a larger area

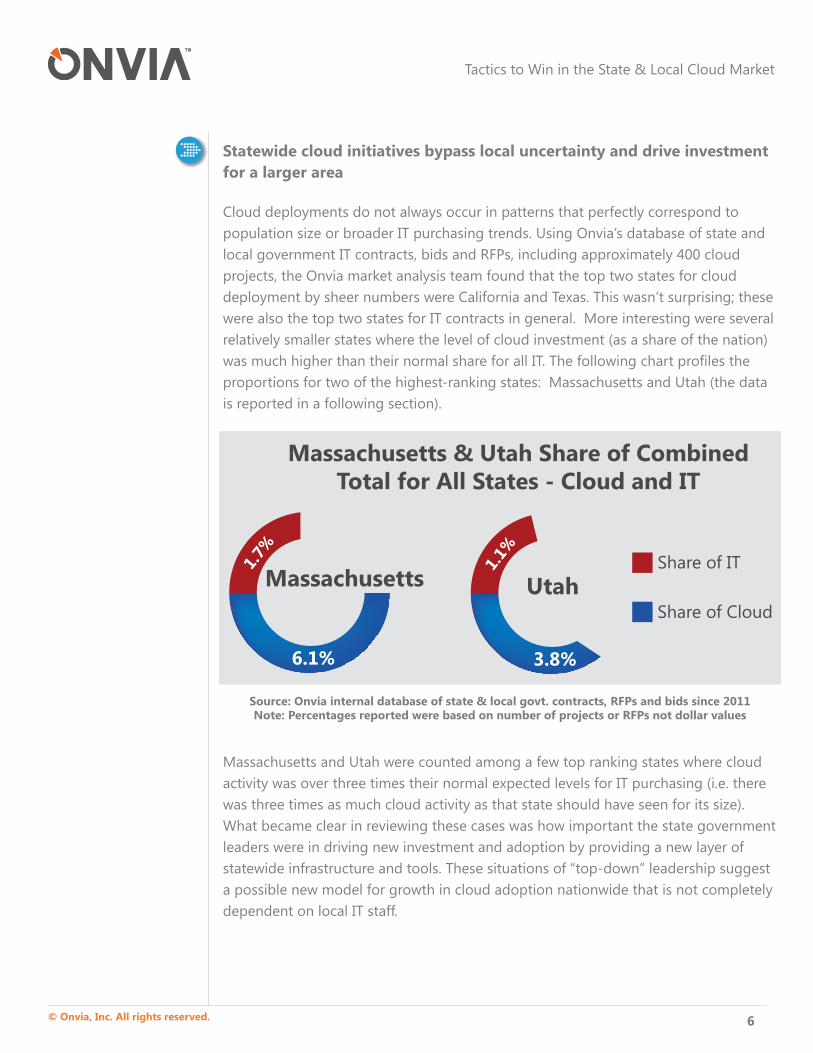

Cloud deployments do not always occur in patterns that perfectly correspond to population size or broader IT purchasing trends. Using Onvia’s database of state and local government IT contracts, bids and RFPs, including approximately 400 cloud projects, the Onvia market analysis team found that the top two states for cloud deployment by sheer numbers were California and Texas. This wasn’t surprising; these were also the top two states for IT contracts in general. More interesting were several relatively smaller states where the level of cloud investment (as a share of the nation) was much higher than their normal share for all IT. The following chart profiles the proportions for two of the highest-ranking states: Massachusetts and Utah (the data is reported in a following section).

Massachusetts and Utah were counted among a few top ranking states where cloud activity was over three times their normal expected levels for IT purchasing (i.e. there was three times as much cloud activity as that state should have seen for its size). What became clear in reviewing these cases was how important the state government leaders were in driving new investment and adoption by providing a new layer of statewide infrastructure and tools. These situations of “top-down” leadership suggest a possible new model for growth in cloud adoption nationwide that is not completely dependent on local IT staff.

1.7%

6.1%

Massachusetts 1.1%

3.8%

UtahShare of Cloud

Share of IT

Massachusetts & Utah Share of CombinedTotal for All States - Cloud and IT

Source: Onvia internal database of state & local govt. contracts, RFPs and bids since 2011Note: Percentages reported were based on number of projects or RFPs not dollar values

7© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Massachusetts’ strong ranking can be tied to a set of related statewide technology initiatives. Over the past few years the state has been building an innovative project called Massachusetts “Open Cloud” or “MOC”, associated with the Boston University

Cloud Computing Initiative. The official website explains that it “will be a public cloud based on a new model that allows many companies and institutions to participate in its implementation and operation.” The goal is to provide infrastructure as a service by offering virtual machines as well as applications and Big Data platforms and services. The state also has a “Big Data Initiative” that fits in nicely with the mission of the MOC. According to the website, “A central focus of the MOC will be its use for solving problems that require analysis of massive data sets such as those targeted by the Commonwealth’s Big Data Initiative, taking advantage not only of services offered by the MOC but the ability to efficiently exchange large volumes of data between MOC users.” As a public cloud, technology will not be controlled by a single entity but the MOC will “operate as a marketplace in which hardware capacity, software and services can be flexibly supplied, purchased, and resold by many participants.” Based on statistics from Onvia’s database, around 60% of cloud projects or bids over the last three years in Massachusetts came from the state’s Information Technology division, with most of these implementations related to setting up this new statewide cloud infrastructure.

Utah’s stellar ranking since 2011 can be traced to a massive statewide public sector cloud initiative that kicked off in 2009. Unlike Massachusetts’s version, this cloud type is hybrid (mostly private) and is aimed at serving other local government offices rather than targeting private sector cooperation. Starting in August 2009, Utah’s CIO announced the state’s intention to offer a private cloud to deliver “hosted email and web applications” to the local government agencies. By 2010, a project briefing indicated that “by December 2009, 510 servers had been moved to the virtualized infrastructure. By May [2010], 1686 physical servers

had been provisioned virtually in the new environment.” Two large data centers were established to support the private cloud infrastructure.

The goal is to provide infrastructure as a service by offering virtual machines as well

as applications and Big Data platforms and services.

011010101000101011110101001001011100110110

1

0

1

1

00

00

1

8© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Additionally, “Utah’s cloud initiative supports access to a growing number of self-provisioned public cloud services. Many of these are identified in Utah’s Internet-Based Collaboration Tools standard … Prior to its approval, many agencies were reluctant to use public cloud applications.” The initiative supports use of state-provided software applications, and gives access to platforms and virtual servers. William Eggers, Director of Public Sector Research at Deloitte13 noted that, “The state of Utah is looking to save $4 million a year in hosting services by consolidating data centers, virtualizing servers and moving to a private cloud platform. It is expected that Utah’s hybrid private cloud will eventually deliver hosted e-mail and Web applications to cities and counties throughout the state.” In recent years, the vast majority of Utah’s cloud projects in Onvia’s project database have come from the state government’s Department of Administrative Services, which is leading the way in setting up this comprehensive statewide system including public cloud hosting services and software as a service solutions.

SECTION 2: WHO’S WINNING?

Not only is cloud activity important and growing, it is currently open to vendors of all

sizes and configurations in the state and local market.

The Wild West of cloud contracting: Vendor size is not a barrier to entry

In the unrestricted environment of cloud contracting at the state and local level, vendor size seems to have little impact on being selected. While large vendors do tend to target the larger contracts, some of the smallest suppliers in terms of total revenue end up with some of the largest cloud awards.

In reviewing the list of recent cloud project awards, Onvia decided to focus on the top 50 vendors based solely on the average size of their awards. Separately, total company revenues were estimated for the vendors using available business lists such as Dun & Bradstreet. When the vendors were sorted by the size of their organization the results tell a story of the “open” dynamics of this market.

13 “Cloud Computing in Government Explodes,” William Eggers, Director of Public Sector Research at Deloitte, Governing -The States and Localities, January 31, 2011

9© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Most of these vendors offered SaaS solutions which agencies can easily implement without having to make extensive changes to IT infrastructure. In some cases, such as a migration of email to the cloud in a large agency, even a SaaS implementation can be expensive (with several running over $1 million in value). Term contracts where the award or contract value were not specified or award notices where an agency did not choose to disclose the value of the award were excluded from our analysis to allow for statistical analysis of average award values. This group of 50 had a total of 59 awards averaging $488,000 (including cloud awards in our database since 2011).

Onvia’s market analysis team found only four vendors out of the 50 that had at least $1 billion in annual revenue and they only represented a slim minority (10%) of the award counts. This allowed the smaller, more locally accessible consultants, VARs or systems integrators the opportunity to meet the demands of clients who were presumably looking for hands-on assistance with responsive account service. Looking at the annual revenues of the vendors below $1 billion, the average company had revenues of $64 million. Awards generally involved budgets of anywhere from $15,000 to $5 million with an overall average of $417,000 ($488,000 including the $1B+ segment). While their revenues were much smaller than the industry giants, these

small to mid-sized vendors in Onvia’s database were generally large enough to operate in multiple states and serve a range of government types from municipal to state agencies and educational clients.

Many of the largest cloud awards went to the smaller or mid-size vendors that would not be considered among the most established of IT competitors. One-half (50%) of the vendors in this top 50 vendor group had annual revenues below $10 million. The vendor with the highest average cloud award of nearly $5 million had estimated company revenues of just over $20 million, which is far smaller than many of its peers in this space. A single award of $5 million for this firm would represent approximately one-quarter of their total annual sales, or presumably a much larger share of their total government sales or total cloud sales. The fact that their agency buyers were comfortable enough with this scenario provides further anecdotal evidence of a cloud market that remains fairly open to all sizes of vendors – even when the award seems somewhat large from a risk management perspective (in comparison to the vendor’s size and workload capacity).

Many of the largest cloud awards went to the smaller or mid-size vendors that would not be considered among the

most established of IT competitors.

10© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

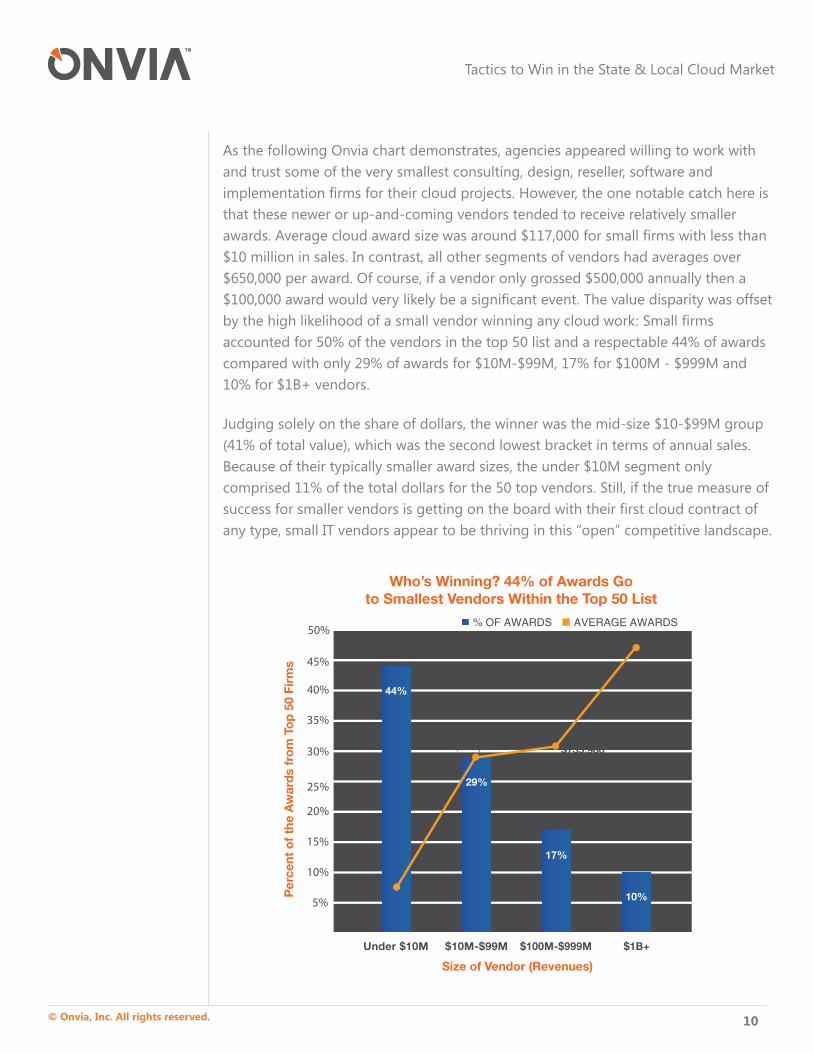

As the following Onvia chart demonstrates, agencies appeared willing to work with and trust some of the very smallest consulting, design, reseller, software and implementation firms for their cloud projects. However, the one notable catch here is that these newer or up-and-coming vendors tended to receive relatively smaller awards. Average cloud award size was around $117,000 for small firms with less than $10 million in sales. In contrast, all other segments of vendors had averages over $650,000 per award. Of course, if a vendor only grossed $500,000 annually then a $100,000 award would very likely be a significant event. The value disparity was offset by the high likelihood of a small vendor winning any cloud work: Small firms accounted for 50% of the vendors in the top 50 list and a respectable 44% of awards compared with only 29% of awards for $10M-$99M, 17% for $100M - $999M and 10% for $1B+ vendors.

Judging solely on the share of dollars, the winner was the mid-size $10-$99M group (41% of total value), which was the second lowest bracket in terms of annual sales. Because of their typically smaller award sizes, the under $10M segment only comprised 11% of the total dollars for the 50 top vendors. Still, if the true measure of success for smaller vendors is getting on the board with their first cloud contract of any type, small IT vendors appear to be thriving in this “open” competitive landscape.

Who’s Winning? 44% of Awards Goto Smallest Vendors Within the Top 50 List

Per

cent

of

the

Aw

ard

s fr

om

To

p 5

0 Fi

rms

$1,113,563

Size of Vendor (Revenues)

Under $10M $10M-$99M $100M-$999M $1B+

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%AVERAGE AWARDS% OF AWARDS

44%

$735,980

29%

17%

10%

$687,926

$116,702

11© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Focus and core competency in only one area? Not a barrier

The state and local agency cloud market is served directly by a wide range of vendor types. One would be hard pressed to find any dominant category in a list of successful prime contractors for these agencies. These vendors include industry giants like Microsoft, specialized software developers, full-service VARs and SaaS hosting companies, IaaS infrastructure hosting providers offering virtual servers, operating systems, configurations and storage in a shared environment and finally, consultants and systems integrators that determine approaches, design custom plans and provide implementation. It is largely an open market, where IT vendors of all sizes and many configurations can potentially compete and win. Giant software or hardware companies can compete directly in one case and serve as silent supplier in another case. Specialized software vendors who compete directly can bring in other players if needed. VARs can tap their software partner’s engineers to show up and assist in a project for value-add. Consultants can propose an integrator, VAR or hosting company to set up and deploy new hosted software or infrastructure that follows their recommendation.

State and local agencies are also known to occasionally manage multiple cloud contracts at once to cover several major components, drawing from the core competency of each vendor. Because of the additional contracting hassles managing multiple primes, this is typically done at the county or statewide level for larger scale implementations. For example, when the Oregon Department of Human Services needed both infrastructure as a service and a SaaS application, they selected a local IaaS solution provider and a specialized software maker for the SaaS subscription-based hosted application. In another example, the Orange County Transportation Authority hired a systems integrator vendor to migrate their email to the cloud and hired a VAR to install VMware cloud networking software.

The different phases of larger cloud projects typically draw from diverse skill sets (i.e. management consulting, design, implementation and migration of data, on-going hosting, follow-up support, etc.) Few firms can offer all of these in-house simultaneously and do them well, which means the ability to leverage their network of trusted suppliers/partners through certifications and alliances is critical.

12© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Awards at every level: Government size is not a barrier

IT budgets tend to increase along with the size and scale of the government agency being served. Onvia found this to be true among cloud projects in our data, with cities running well below the overall average for project budgets within state and local government. One might expect that the smaller award average ($117K) of the sub-$10 million dollar vendors could be explained by a list of cloud projects containing mainly city government work.

However, rather than loading up on only city government projects, Onvia’s analysis showed that the smallest vendors generally had a diverse set of awards including counties, state agencies and the educational sector. Their lower overall average can be attributed to smaller scale or more limited cloud projects at all levels of agencies rather than simply being due to only working with their local cities. A standard SaaS implementation of Salesforce used by a team within the larger agency, for example, would presumably be easier and cheaper than enterprise-wide migrations of email, productivity software, platform-level or infrastructure-level systems.

The states and counties tended to have much larger budgets for cloud projects. Those averages included some lower value work that the biggest vendors tended to avoid. While larger contracts of $500,000 or more were common among statewide agencies, there were also $50,000 to $200,000 smaller opportunities.

Onvia’s analysis also found that the occasional large city cloud projects were worth just as much as those of a typical state agency because of the size of the city and scale of IT work required. One example client within the top 50 group was the City of Atlanta, which awarded a $1 million dollar contract for a package of cloud services supporting its 311 Call Center project.

Onvia market analysis concludes that smaller vendors should pay attention to award size, but they should not be constrained in bidding on projects simply because of the level of government.

Large City Cloud Projects

13© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Lack of state & local government experience? Not a barrier

Due to the newness of cloud in the state and local space, this isn’t a market where buyers have the luxury of selecting vendors with dozens of directly relevant project examples. Among successful bidders who won at least one cloud contract over the past several years and are in the top 50 vendor list, the average number of cloud projects was only 1.2 per firm, with the majority having only one award. Since one project does not normally prove proficiency or demonstrate full expertise, Onvia suggests that this competitive situation forced vendors to emphasize either their non-cloud IT experience in their submittals, or cloud work done in the private sector, with federal agencies, or with below threshold smaller contracts in state and local government.

SECTION 3: TACTICS TO WIN

Be a solutions expert and bring a full package of tools and service

The appearance of broad capability and good service helps in this market. A few very large and successful vendors like Microsoft and IBM have won cloud contracts due in part to having the “big” IT industry credibility and authoritative consulting capability with their in-house consulting/design/integration departments. However, the success of the smaller players suggests that buyers are finding compelling value in the small to midsize vendor business model, which represents nearly 80% of the dollars in our top 50 vendor data. These smaller firms offered broad capabilities, secure partnerships with major players and other necessary providers and good customer service. Those that happen to be located within the same state may also benefit from the common contracting bias toward local providers (driven by a desire to benefit the local economy).

As a newer trend, cloud is not ‘business as usual’ for this market. State and local agency IT chiefs are looking for trustworthy vendors to provide

expert guidance, and to win their trust you need to be willing to engage in a relationship.

Ronit Cohn, Sales Manager/IT Consultant, Onvia

14© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

While some might assume that a business like cloud services could thrive keeping human-to-human contact at a minimum to support lower fees for a mostly self-service IT client base, industry observers have mentioned the continued importance of customer service as a key ingredient to winning business at the enterprise level. A recent InfoWorld blog14 cautioned that as the public cloud providers “push into larger enterprises, they will have no choice but to provide a richer customer service experience. Large enterprise IT demands that level of service, and public clouds won’t be able to penetrate the large enterprise market without it.” Back in 2009, a CNET contributor15 argued that “Service is the name of the game in cloud computing. It is at the heart of why end users can worry less knowing that their providers are doing most of the worrying for them. Treating customers right is a differentiator.”

When a vendor is not a giant software or hardware company with a household name, they will often emphasize their certifications, affiliations or alliances. This reinforces their “well-connected in the industry” status and (through their partnerships) their ability to take on a larger scope than their own limited staff might suggest. Since many IT managers in local government will not plan to buy direct from a Microsoft or Google they will take the smaller competitors seriously and search for evidence they can be trusted with a complex and often multi-faceted IT project.

In a recent 2013 report issued by the IBM Center for the Business of Government16, the authors acknowledge that “It is not uncommon for a cloud provider to outsource certain aspects of their business.” In addition to holding the prime fully responsible for all aspects of the contract regardless of subcontracted work, the authors in their guidelines called for more visibility into the subcontracting component to make sure agencies were aware of which parts were being delegated and the name of the subcontractor(s).

The trend of placing a spotlight on the partners and subcontractors underscores the importance of having the right partnerships in the industry ahead of time. If a public agency needs to approve each one, it means the partners of a prime contractor will have to stand up to scrutiny to be easily and quickly approved, which may not bode well for the most inexperienced players in the industry.

14 “Cloud computing’s Achilles’ heel: Poor customer service,” David Linthicum, InfoWorld blog, January 8, 201315 “Customer service and cloud computing,” James Urquhart, CNET blog, April 22, 200916 “Cloudy with a Chance of Success: Contracting for the Cloud in Government,” Shannon Howle Tufts and Meredith Leigh Weiss, IBM Center for the Business of Government, 2013

15© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Be patient and knowledgeable to cultivate city contracts

City government IT leaders struggle to keep up with the demands of managing day-to-day operations. As a result, they often require education and help to frame and scope these issues and make progress unlocking the potential of cloud computing. The situation calls for building partnering relationships with local IT agency contacts, which could involve free advice or explanations and the main steps in the adoption process to shorten the learning curve and demonstrate value and interest. Onvia believes that one way to build trust and credibility is to offer occasional updates to local agency contacts where a vendor shares timely and interesting news about cloud implementations at the statewide (or even federal) level (i.e. “Did you know about…?”) along with their expertise. Local agencies are typically interested in trends at the higher levels of government and these busy IT chiefs do not always have the time to stay current on cloud computing news.

To assist in the person-to-person marketing approach, Onvia offers a valuable service to clients called Spending Forecast Center, which tracks published capital improvement plans and agency budgets and provides a forward-looking trend line of expected spending up to ten plus years into the future. Clients can select the city government agencies within their territory and see which ones already discuss or plan on funding cloud projects in the near future. The vendor can watch out for “trigger events” such as an upcoming purchase of new servers or larger system upgrades, where questions can be posed about how cloud solutions might be integrated in a way that could save costs and improve service levels.

The key is advance knowledge and patience. Depending on the IT sub-vertical, Onvia recommends getting in six months to a year before the RFP is written or the bid is released. For the best outcome, stakeholders and decision-makers need time to consider the advice and recommendations of a qualified vendor, and the vendor needs time to build a cooperative relationship of trust. That vendor will then be in a more advantageous position when it comes to actually competing for the contract.

It’s mostly just lack of understanding that prevents local governments from seeing the

cloud’s potential, as local IT people are usually so busy just keeping things on their end running

in tip top shape that they fail to do broad strategic planning.

Xath Cruz, CloudTimes, August 22, 2012

16© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Target state agencies that are further along in cloud adoption for faster results

State government departments and agencies continue to be a strong market for cloud solutions due to their greater scale, available IT budgets, opportunities for making a significant impact among diverse constituencies and generally larger and more sophisticated IT staff.

The challenge for regional and nationally deployed cloud vendors is how to target them to best allocate limited marketing budgets and sales resources. Selecting states simply based on the volume of IT spending may infer that there are opportunities in cloud, but if those opportunities come with a higher degree of competition attached, then the effort required to win might not be worth it. Conversely, finding relatively smaller states that are also known for being more open to cloud might lead a vendor to execute more productive bidding and secure more profitable business opportunities.

In order to help vendors better evaluate how receptive or hostile to cloud computing a given state’s government agencies were, Onvia created a geographic tool that can normalize data from states (from the very smallest to the very largest) for ease of ranking. For the purposes of this paper, an index was calculated using data on the number of awards, RFPs and bids within state and local government, sorted by each state. The values refer to how frequent cloud projects happen within a given state as a share of the nation compared to what is “normal” for that state in IT buying. For example, if a state’s normal share of the nation in IT was 5% but it was 10% for cloud, the cloud sub-set would be said to over-index by a factor of two (a share that is twice as high as one would expect).

The challenge for regional and nationally deployed cloud vendors is how to target [states] to best allocate

limited marketing budgets.

17© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

The top five states in terms of rate of contracting and purchasing for cloud relative to IT in general were Vermont, Massachusetts, Utah, Oregon and Arkansas. None of these can be considered “large” in size based on population. Each state over-indexed their expected share by around three times when cloud contracting at all levels was compared. Because of this evidence of having more “early adopters” in taking on cloud, these five states presumably contain more interested and less skeptical decision-makers in general. The top 10 list are in the “2011-2013 State & Local Cloud Buying Index” table to provide additional visibility into the above-average states.

Onvia’s market analysis team decided to include local agencies in the “state and local” index calculation to provide a broader metric that would pick up on conversations and influencing taking place across the agency levels. This allowed Onvia’s team to assess the overall environment for promoting cloud further within each state. For example, if a major city like Chicago adopted cloud in a significant way, the IT heads in the Illinois state government would most likely hear about it and be positively influenced, and it could then lead to the entire state growing more cloud-receptive. Likewise, local governments can also be influenced by the leadership of state agencies.

ToP FIVe STaTeSRATE OF CONTRACTING AND PURCHASING FOR CLOUD

18© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

These ten states as a group represented 10% of the IT contracting nationally for state and local government but a full 26% of cloud contract activity, with an overall index of 2.64 (264% or 2.6 times the normal expected level).

In states that have a higher cloud purchasing index, vendors will be less likely to have to start at the ground level in educating and raising awareness around cloud computing and its benefits.

Similar to the city government recommendations above, Onvia suggests engaging in partnership-building conversations with state IT leaders around the kinds of cloud projects that have already been published, awarded or advertised (either in that office or in another area of state government) and learn how the vendor might fit into the kinds of statewide projects that are possible in the future.

*Method: Index scores were calculated by dividing a state’s share of cloud awards, bids and RFPs with its corresponding share for all IT buying; index values greater than 1.00 indicate a market where cloud projects tend to be purchased at a higher rate than normal given that state’s typical IT purchasing patterns

*Note1: Uses recent timeframe of 2011 to Q3 ’13, with local, state, and educational agencies included; sample sizes for cloud projects in the smallest states were very limited so states with only two cloud projects were excluded from Top 10 status because a difference of only one could have significantly lowered the index making the state no longer eligible; in the case of Vermont there were four projects or around 1% of the national total for this period; the data set included approximately 200,000 IT projects nationally for these months and around 400 cloud projects

*Note2: The decision of which states to enter and focus on is a critical one for IT vendors. The data shared here is not intended to replace standard considerations such as proximity to a vendor’s office, but should be seen as supplemental. onvia’s goal is to offer a different and useful perspective based on patterns or concentrations of cloud activity

States where agenciesare located

“Normal”IT Share of Nation

Cloud Shareof Nation

CloudBuyingIndex

Vermont

Massachusetts

Utah

Oregon

Arkansas

Hawaii

Nebraska

Wisconsin

New Mexico

Indiana

Total - Top 10

0.3 %

1.7%

1.1%

1.3%

0.7%

0.9%

0.9%

1.3%

0.8%

0.7%

9.7%

1.0%

6.1%

3.8%

3.8%

1.8%

2.5%

2.0%

2.3%

1.3%

1.0%

25.7%

3.89

3.49

3.44

3.01

2.69

2.68

2.25

1.76

1.52

1.49

2.64

2011-2013 State & Local Cloud Buying IndexBased on procurement activity of cloud projects

compared to all IT projects within each state

19© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

CONCLUSION

Cloud represents a substantial opportunity for experienced IT vendors in the state and local market who are ready to compete directly for these projects. Industry trends and Onvia’s purchasing data both point to continued growth in cloud contracts.

Not only is cloud activity important and growing, it is currently open to vendors of all sizes and configurations in the state and local market. The successful vendors who recently won contracts do include a few giant competitors, such as Microsoft and IBM, but 77% of the values of these awards went to the small to midsize players.

To win, vendors need to understand and satisfy client needs and be ready to deliver a range of IT products and services through industry partnerships as needed. Government buyers are looking for capable, service-minded, consulting-oriented vendors who can patiently work with agency staff and stakeholders for what are often more complicated engagements than with other types of IT work.

With more than 83,000 state and local purchasing departments for a vendor to choose from, Onvia believes a key tactic for marketing success is to use smart targeting to narrow down the list of agencies and offices. Onvia strongly recommends gaining prior knowledge about recent and upcoming trends in spending, and then developing positive relationships with decision-makers well in advance of when they may be willing to release an RFP or bid.

Vendors do not have to be large to be selected but they need to be trusted; relationship building with the right contacts can make all the difference.

The information contained in this Onvia publication has been obtained from publicly available federal, state and local and government data sources. Onvia disclaims all warranties as to the accuracy, completeness or adequacy of such information. The views and opinions expressed in this publication are those of Onvia’s research organization and are subject to change.

20© Onvia, Inc. All rights reserved.

Tactics to Win in the State & Local Cloud Market

Onvia specializes in providing business intelligence solutions to vendors to grow their government business, helping them get ahead of the bid and RFP process. Active vendors in the government market that need timely, comprehensive and unique insights in their industry vertical, key buyers and competitive landscape should visit http://www.onvia.com/ and request a demo to speak with a Business Development Manager. Onvia helps clients strategically grow their government business with solutions for project intelligence, agency intelligence and vendor intelligence in the public sector.