tactical allocation to gold - lbma allocation to gold lbma conference, hong kong prepared by:...

TRANSCRIPT

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

1 Session 2 - Morris

For Professional Clients only)

Tactical allocation to gold LBMA conference, Hong Kong

Date: November 2012 Prepared by: Charlie Morris

22

99

7-A

MG

52

99

2d

High quality assets have performed well

Asset quality has been the single greatest factor that

can explain asset price changes since 2000

Equities Consumer brands, low volatility equities

Bonds “Good” government bonds

FX Swiss Franc, Yen, Singapore Dollar

Commodities Gold

Property Prime real estate

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

2 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Measuring asset quality in equities

Equities with low volatility have been rewarded

since 2000

Balance sheet strength, stable cash flows, sustainability of profits, robust

franchises have been highly sought after

These fundamental factors have been reflected in price volatility

We can conclude that high quality equities have low volatility

This is not only true for the stock market, but for all asset classes

22

99

7-A

MG

52

99

2d

Quality in equities

S&P low volatility equities versus high beta equities

1990 to 2000

0

200

400

600

800

1000

1,200

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Low Volatility TR High Beta TR S&P 500 TR

1990 to 2000

Source HSBC, Bloomberg. Date range from 31 December 1999 to 30 November 1990.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

3 Session 2 - Morris

22

99

7-A

MG

52

99

2d

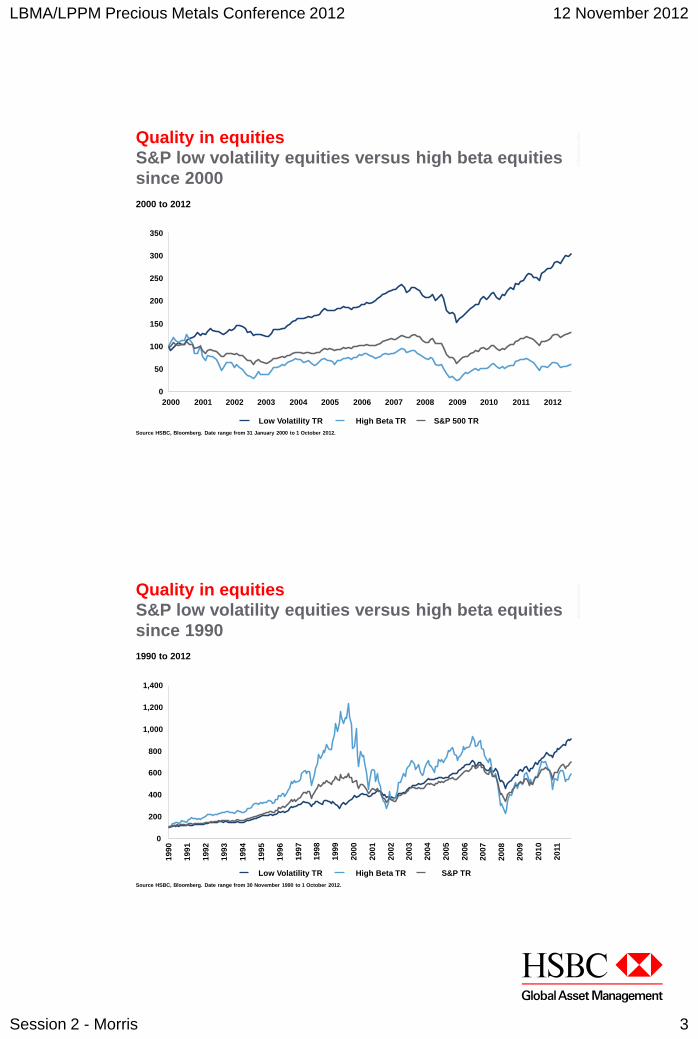

Quality in equities

S&P low volatility equities versus high beta equities

since 2000

2000 to 2012 2000 to 2012

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Low Volatility TR High Beta TR S&P 500 TR

Source HSBC, Bloomberg. Date range from 31 January 2000 to 1 October 2012.

22

99

7-A

MG

52

99

2d

Quality in equities

S&P low volatility equities versus high beta equities

since 1990

1990 to 2012 1990 to 2012

0

200

400

600

800

1,000

1,200

1,400

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Low Volatility TR High Beta TR S&P TR

Source HSBC, Bloomberg. Date range from 30 November 1990 to 1 October 2012.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

4 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Quality in commodities

The least volatile commodities have delivered the highest returns

A plentiful “above ground” supply broadly correlates with volatility

Supply days is a best estimate as these figures are impossible to

determine with accuracy

Commodity Volatility Supply days

Gold 16% 14,381

Silver 29% 5,755

Copper 27% 231

Wheat 31% 82

Soybeans 31% 57

Corn 29% 47

Oil 33% 46

Natural gas 56% 42

22

99

7-A

MG

52

99

2d

Technical analysis of the gold market

Technical analysis is a trading discipline

– Trend following works best on less volatile securities

– Reversion to the mean works best on more volatile securities

Gold has low volatility follow the trend

– Lower volatility allows the trading strategy to slow down

– Less speed lowers the turnover which cuts trading costs

Technical strategy for gold

– Confirm the bull market

– Determine your “core position” size

– Implement a tactical overlay to increase that position size periodically

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

5 Session 2 - Morris

22

99

7-A

MG

52

99

2d

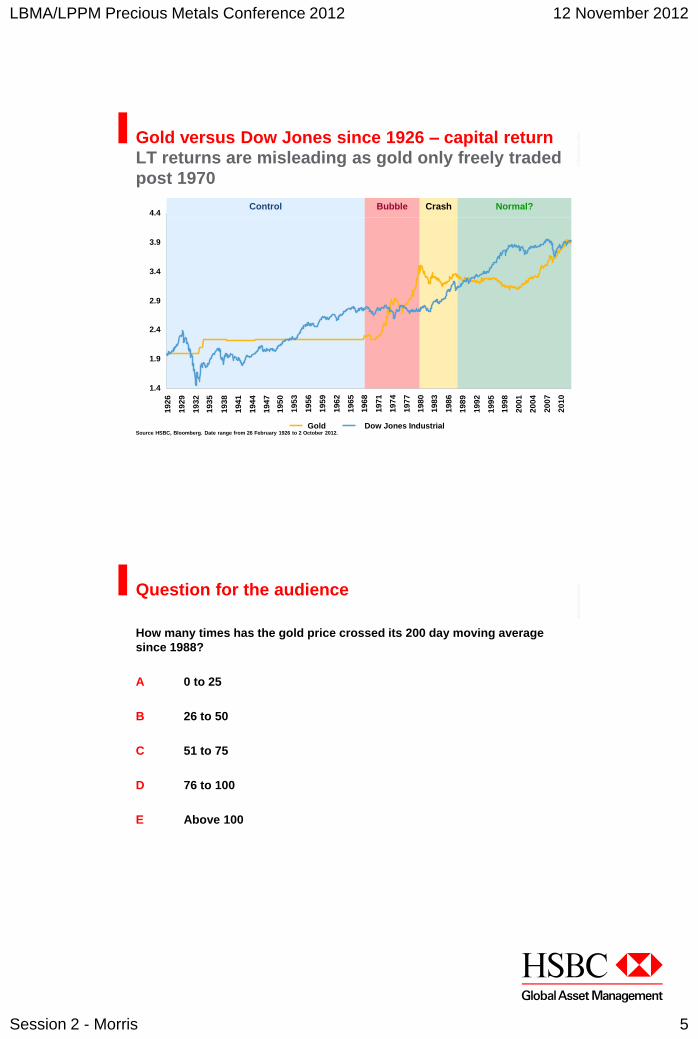

Gold versus Dow Jones since 1926 – capital return

LT returns are misleading as gold only freely traded

post 1970

Normal? Crash Bubble Control

1.4

1.9

2.4

2.9

3.4

3.9

4.4

19

26

19

29

19

32

19

35

19

38

19

41

19

44

19

47

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

Gold Dow Jones Industrial Source HSBC, Bloomberg. Date range from 26 February 1926 to 2 October 2012.

22

99

7-A

MG

52

99

2d

Question for the audience

How many times has the gold price crossed its 200 day moving average

since 1988?

A 0 to 25

B 26 to 50

C 51 to 75

D 76 to 100

E Above 100

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

6 Session 2 - Morris

22

99

7-A

MG

52

99

2d

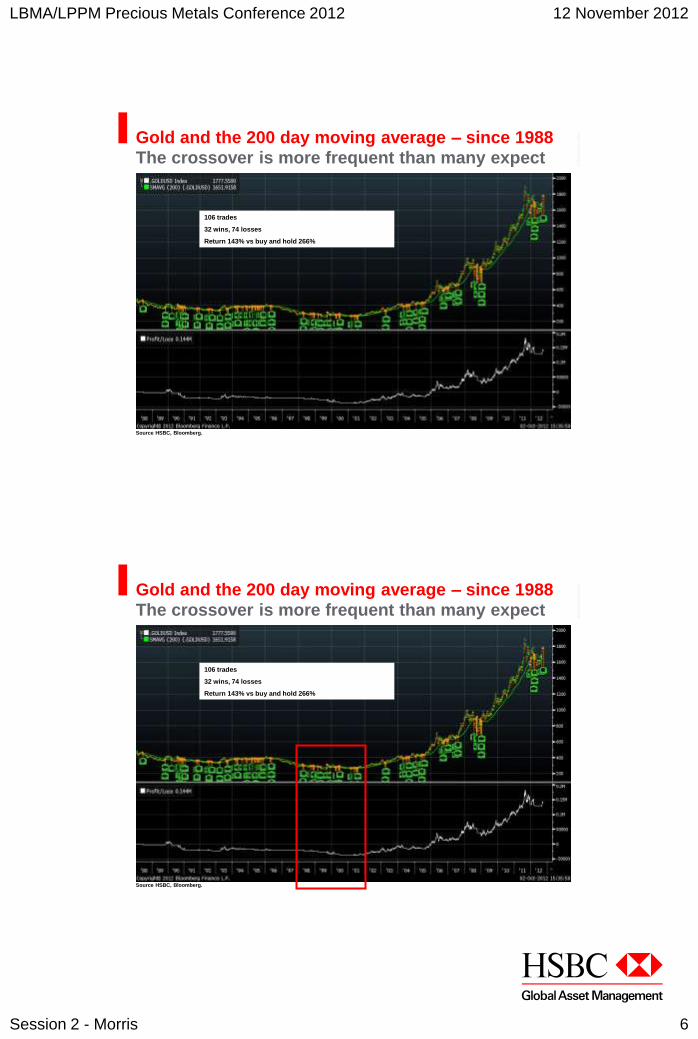

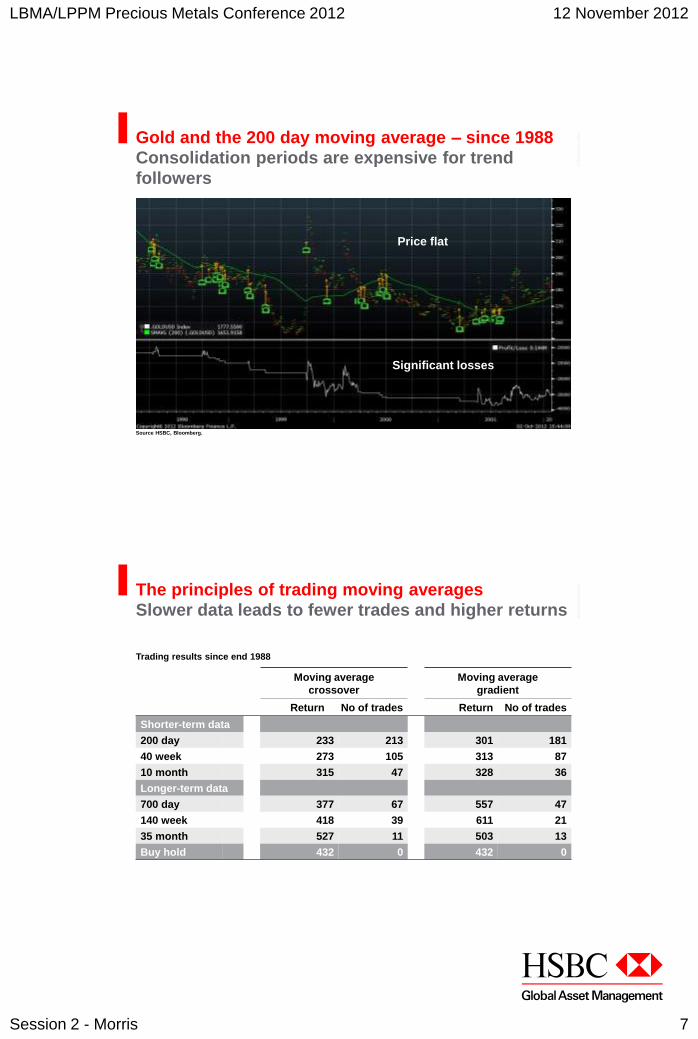

Gold and the 200 day moving average – since 1988

The crossover is more frequent than many expect

106 trades

32 wins, 74 losses

Return 143% vs buy and hold 266%

Source HSBC, Bloomberg.

22

99

7-A

MG

52

99

2d

Gold and the 200 day moving average – since 1988

The crossover is more frequent than many expect

106 trades

32 wins, 74 losses

Return 143% vs buy and hold 266%

Source HSBC, Bloomberg.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

7 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Gold and the 200 day moving average – since 1988

Consolidation periods are expensive for trend

followers

Price flat

Significant losses

Source HSBC, Bloomberg.

22

99

7-A

MG

52

99

2d

Moving average

crossover

Moving average

gradient

Return No of trades Return No of trades

Shorter-term data

200 day 233 213 301 181

40 week 273 105 313 87

10 month 315 47 328 36

Longer-term data

700 day 377 67 557 47

140 week 418 39 611 21

35 month 527 11 503 13

Buy hold 432 0 432 0

The principles of trading moving averages

Slower data leads to fewer trades and higher returns

Trading results since end 1988

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

8 Session 2 - Morris

22

99

7-A

MG

52

99

2d

The tactical and strategic approach

Position size reflects conviction

Large position

No position For illustrative pursposes only.

22

99

7-A

MG

52

99

2d

Gold bear market

No position

The tactical and strategic approach

Position size reflects conviction

Large position

No position For illustrative pursposes only.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

9 Session 2 - Morris

22

99

7-A

MG

52

99

2d

The tactical and strategic approach

Position size reflects conviction

Large position

Gold bull market No position

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

For illustrative pursposes only. Amounts shown are approxiamte indications.

22

99

7-A

MG

52

99

2d

The tactical and strategic approach

Position size reflects conviction

Large position

Gold bull market

AND market is timely

No position

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

For illustrative pursposes only. Amounts shown are approxiamte indications.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

10 Session 2 - Morris

22

99

7-A

MG

52

99

2d

The tactical and strategic approach

Position size reflects conviction

Large position

Gold bull market

AND market is timely

AND conditions are optimal

No position

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

For illustrative pursposes only. Amounts shown are approxiamte indications.

22

99

7-A

MG

52

99

2d

LESS when too good to be true

The tactical and strategic approach

Position size reflects conviction

Large position

Gold bull market

AND market is timely

AND conditions are optimal

No position

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

For illustrative pursposes only. Amounts shown are approxiamte indications.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

11 Session 2 - Morris

Core gold models

to identify a bull market in gold

22

99

7-A

MG

52

99

2d

Real interest rates

US real rates since 1982

Gold has performed best when real rates are <2%

US Real Rates

(6)

(4)

(2)

0

2

4

6

8

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Loose money - bullish

Tight money - bearish Return 347% versus buy and hold 239%

13 occurrences since 1988

The zone is 1.7% to 2%

Source HSBC, Bloomberg. Date range from 31 October 1982 to 2 October 2012.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

12 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Gold and the long-term trend

Gold in a global currency basket with a 35-month

exponential MA since 1985

Use the gradient and not the crossover

Return 342% vs buy and hold 252%

5 gradient changes since 1988

10 Moving average crosses

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Gold without dollars Three Year Trend Source HSBC, Bloomberg. Date range from 28 February 1985 to 2 October 2012.

22

99

7-A

MG

52

99

2d

Gold versus the S&P 500

Gold S&P ratio with a 35-month exponential MA

since 1988 – Use the gradient and not the crossover

Return 342% vs buy and hold 252%

18 gradient changes since 1970

3 gradient changes since 1988

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

.GOLDSPX Index - Last Price EMAVG (35) Source HSBC, Bloomberg. Date range from 31 October 1967 to 2 October 2012.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

13 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Core model summary

Real interest rates are low – bullish since 2009

The gold trend is strong in a global currency basket – bullish since 2001

Gold is beating equities – bullish since 2002

Gold is in a bull market

22

99

7-A

MG

52

99

2d

Core model summary

Real interest rates are low – bullish since 2009

The gold trend is strong in a global currency basket – bullish since 2001

Gold is beating equities – bullish since 2002

Gold is in a bull market

Therefore the tactical models can now be implemented

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

14 Session 2 - Morris

Tactical models to increase the position size

22

99

7-A

MG

52

99

2d

Gold volatility

Gold in global money 1988 to 2000

Non trending market = model useless

Source HSBC, Bloomberg.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

15 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Gold volatility

Gold in global money 2000 to 2012

Trending market = model effective

High volatility, mean revert

Low volatility, trend follow

Source HSBC, Bloomberg.

22

99

7-A

MG

52

99

2d

The gold silver ratio

Since 1988

Useful to identify relative value between gold and silver but even better

measure of macro economic risk

When silver is leading leads, gold is more likely to rise

Avoid data mining this series

Silver cheap relative to gold

Silver expensive relative to gold

Average pre 2001 = 72

Average post 2001 = 60

30

40

50

60

70

80

90

100

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Source HSBC, Bloomberg. Date range from 21 October 1988 to 3 October 2012.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

16 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Sentiment

Studying the crowd, not the price

There are numerous was of approaching this inexact science

CFTC data is useful as is the Hulbert Sentiment Index

However the web hits is the most timely and is also the broadest measure

Source www.alexa.com

22

99

7-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

For illustrative pursposes only. Amounts shown are approxiamte indications.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

17 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

Real rates are low, the non-dollar price trend is rising

and gold is beating equities

22

99

7-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

Real rates are low, the non-dollar price trend is rising

and gold is beating equities

Volatility is low OR Silver is cheap

OR sentiment is weak

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

18 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

Real rates are low, the non-dollar price trend is rising

and gold is beating equities

Volatility is low OR Silver is cheap

OR sentiment is weak

Volatility is low AND Silver is cheap

AND sentiment is weak

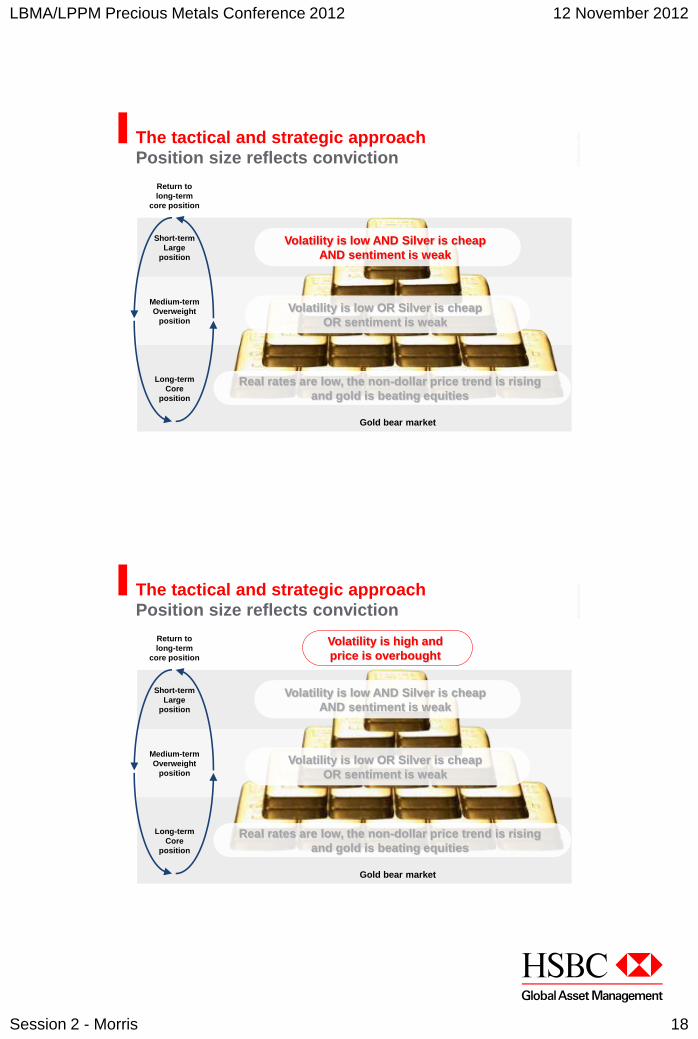

22

99

7-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

Real rates are low, the non-dollar price trend is rising

and gold is beating equities

Volatility is low OR Silver is cheap

OR sentiment is weak

Volatility is low AND Silver is cheap

AND sentiment is weak

Volatility is high and

price is overbought

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

19 Session 2 - Morris

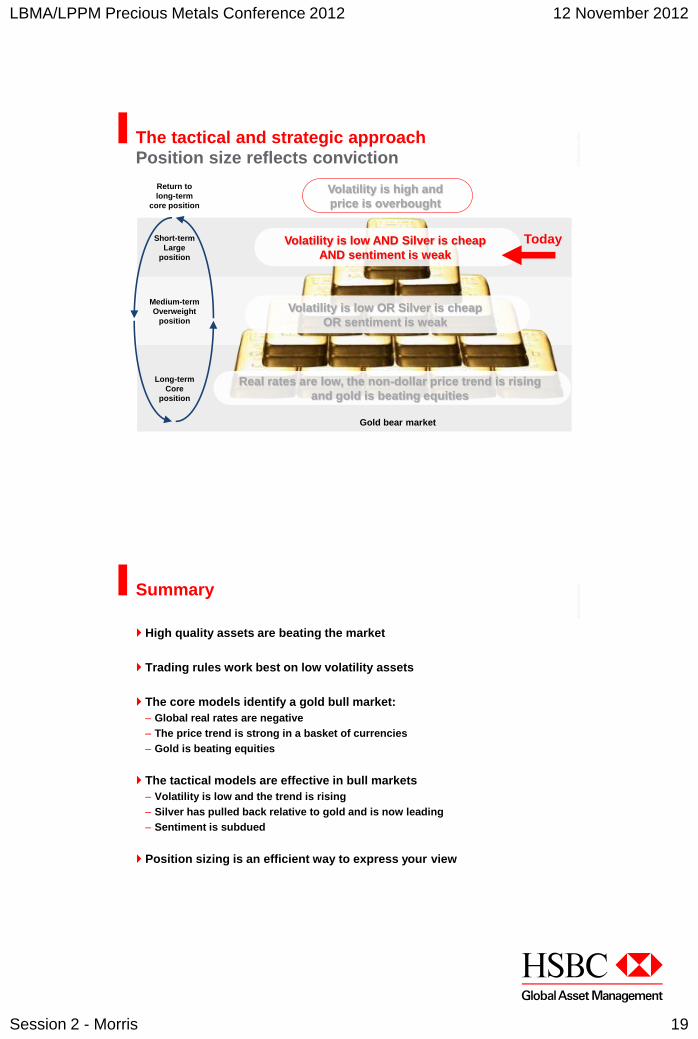

22

99

7-A

MG

52

99

2d

Long-term

Core

position

Short-term

Large

position

Medium-term

Overweight

position

Return to

long-term

core position

Gold bear market

The tactical and strategic approach

Position size reflects conviction

Real rates are low, the non-dollar price trend is rising

and gold is beating equities

Volatility is low OR Silver is cheap

OR sentiment is weak

Volatility is low AND Silver is cheap

AND sentiment is weak

Volatility is high and

price is overbought

Today

22

99

7-A

MG

52

99

2d

Summary

High quality assets are beating the market

Trading rules work best on low volatility assets

The core models identify a gold bull market:

– Global real rates are negative

– The price trend is strong in a basket of currencies

– Gold is beating equities

The tactical models are effective in bull markets

– Volatility is low and the trend is rising

– Silver has pulled back relative to gold and is now leading

– Sentiment is subdued

Position sizing is an efficient way to express your view

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

20 Session 2 - Morris

22

99

7-A

MG

52

99

2d

Disclaimer

This document is issued in the UK by HSBC Global Asset Management, a trading name of HSBC Private Bank (UK) Limited and

HSBC Global Asset Management (UK) Limited. Both are authorised and regulated by the Financial Services Authority and

registered in England at 8 Canada Square, E14 5HQ.

The contents of this document are confidential and may not be reproduced or further distributed to any person or entity,

whether in whole or in part, for any purpose. This document is not intended for distribution to or use by any person or entity in

any jurisdiction or country where such distribution or use would be contrary to law or regulation.

HSBC Global Asset Management has based this document on information obtained from sources it believes to be reliable but

which it has not independently verified. HSBC Global Asset Management and HSBC Group accept no responsibility as to its

accuracy or completeness.

This document is intended for discussion only and shall not be capable of creating any contractual or other legal obligations

on the part of HSBC Global Asset Management or any other HSBC Group company. Care has been taken to ensure the

accuracy of this presentation but HSBC Global Asset Management accepts no responsibility for any errors or omissions

contained therein.

Any forecast, projection or target where provided is indicative only and is not guaranteed in any way. HSBC Global Asset

Management accepts no liability for any failure to meet such forecast, projection or target.

© Copyright. HSBC Global Asset Management 2012. All Rights Reserved. 22997 GD/1012 FP12 - XXXX